Global G-Protein Coupled Receptors (GPCR) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.83 Billion |

| Market Size (2031) | USD 6.72 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

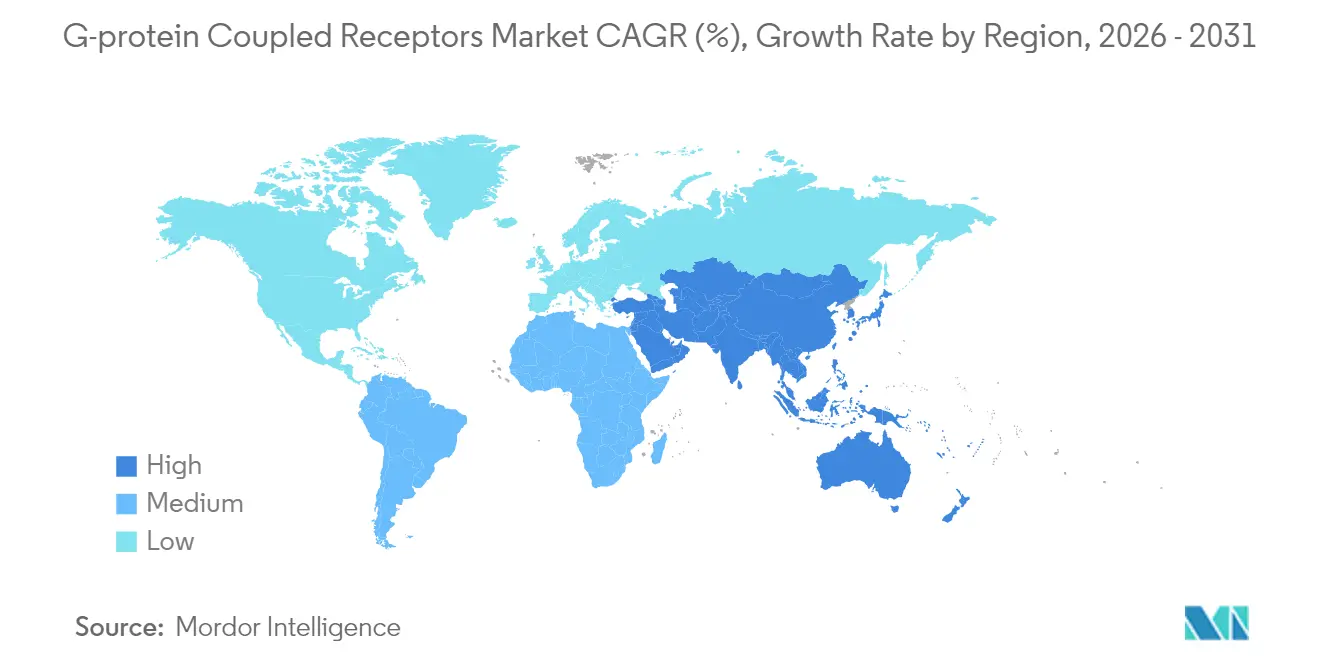

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

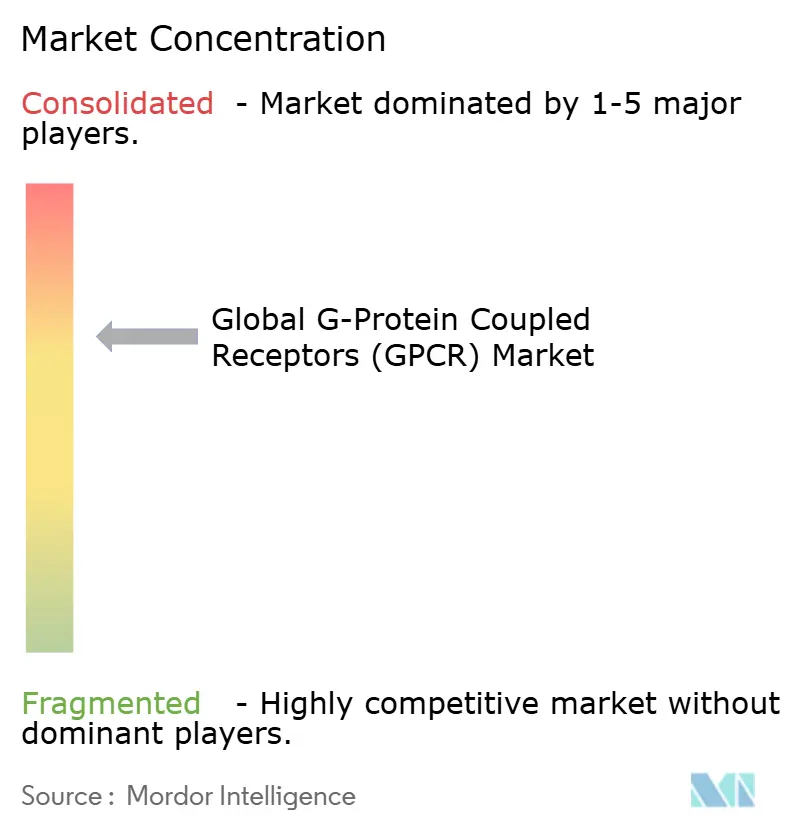

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global G-Protein Coupled Receptors (GPCR) Market Analysis by Mordor Intelligence

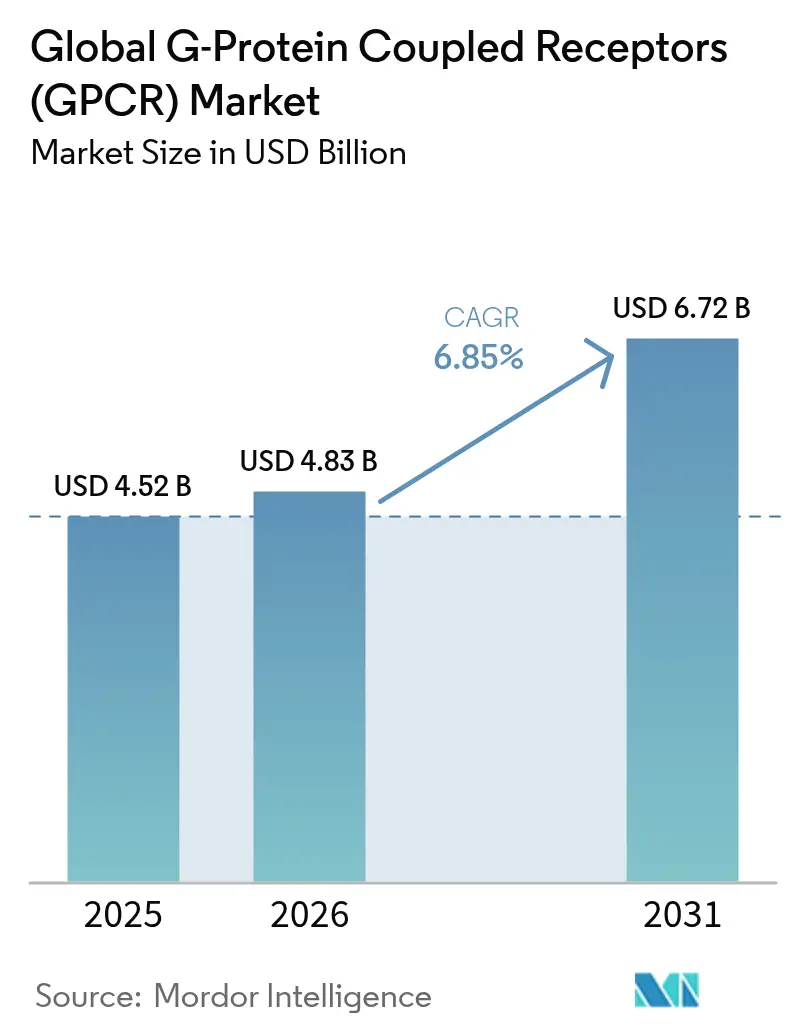

G-protein coupled receptors market size in 2026 is estimated at USD 4.83 billion, growing from 2025 value of USD 4.52 billion with 2031 projections showing USD 6.72 billion, growing at 6.85% CAGR over 2026-2031. Increasing adoption of structure-guided design based on AlphaFold2 models is broadening the addressable receptor universe, while oral small-molecule GLP-1 programs sustain venture funding momentum and catalyze new partnership structures. North American sponsors continue to dominate filings, yet Asia Pacific laboratories are scaling fastest as governments align review standards and subsidize translational infrastructure. Oncology keeps the largest therapeutic footprint, but cardiovascular projects post the sharpest acceleration on the back of allosteric discovery breakthroughs. Overall, the G-protein coupled receptors market is benefiting from modular platform innovation, moderated competitive intensity and a widening pool of first-in-class targets.

Key Report Takeaways

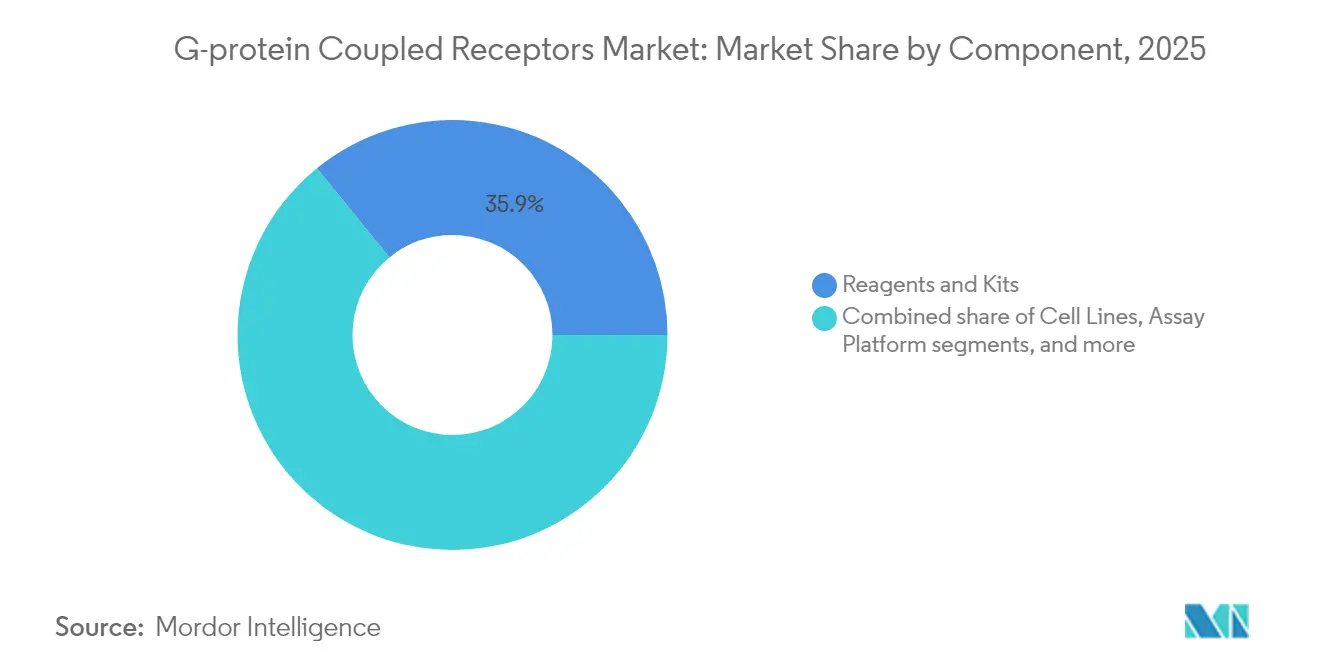

- By component, reagents and kits led with 35.86% of G-protein coupled receptors market share in 2025, while assay platforms are tracking an 8.58% CAGR to 2031.

- By assay type, calcium detection held 28.45% revenue in 2025 and cAMP assays are projected to advance at 8.85% CAGR through 2031.

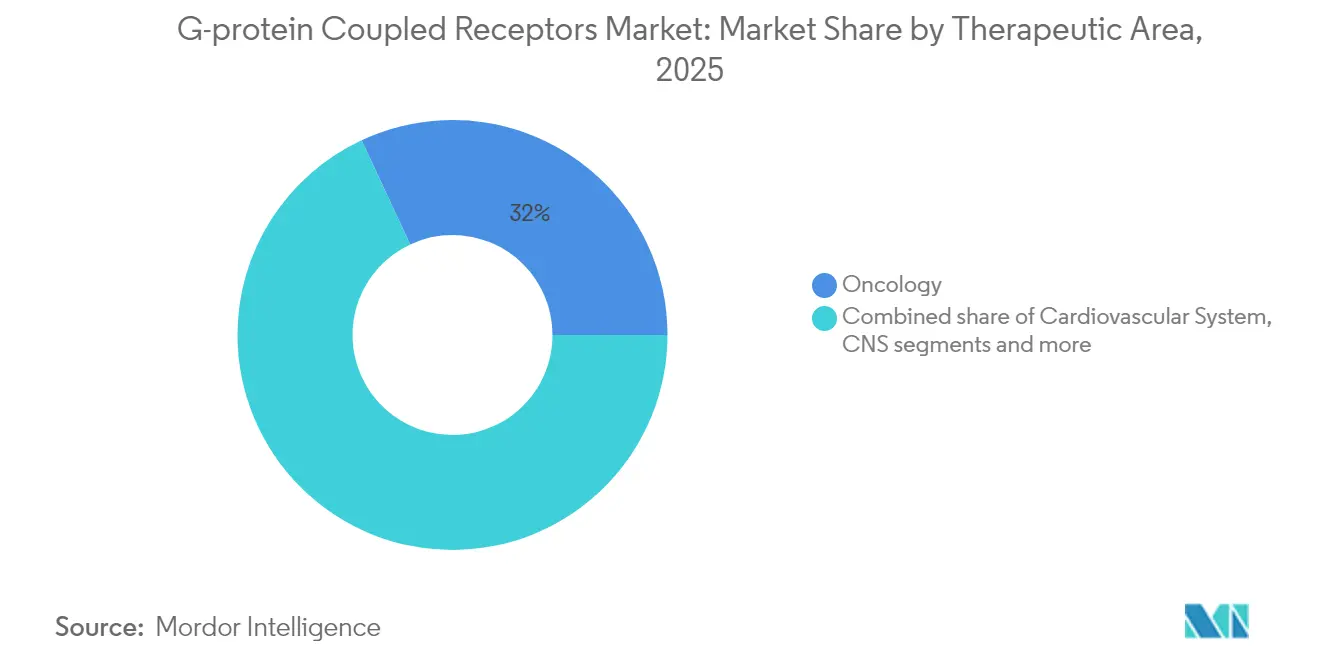

- By therapeutic area, oncology accounted for 31.95% of the G-protein coupled receptors market size in 2025; cardiovascular drugs are poised to rise at an 8.19% CAGR to 2031.

- By end-user, pharmaceutical and biotech companies captured 45.20% share in 2025; academic and research institutes record the quickest momentum at 8.53% CAGR.

- By geography, North America maintained 37.10% share during 2025, whereas Asia Pacific is expanding at an 8.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global G-Protein Coupled Receptors (GPCR) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of HTS platforms for GPCR assays | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing drug-discovery spend targeting GPCRs | +1.5% | Global, led by North America and Asia Pacific | Long term (≥ 4 years) |

| Rising burden of chronic & metabolic diseases | +1.2% | Global, with highest impact in developed markets | Long term (≥ 4 years) |

| Expansion of biologics & allosteric modulators | +1.0% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-enabled structure-guided GPCR modeling | +0.9% | Global, with early adoption in North America | Short term (≤ 2 years) |

| VC boom in oral small-molecule GLP-1 agonists | +0.8% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of HTS Platforms for GPCR Assays

High-throughput screening instruments are replacing manual radioligand methods as sponsors demand faster, label-free read-outs that eliminate isotope handling. Bioluminescence resonance energy transfer sensors further improve sensitivity by capturing conformational shifts in real time, and impedance-based microelectrode arrays provide a non-invasive proxy for electrophysiological responses with 0.85 correlation to patch-clamp data[1]Muhammad Fathul Ihsan, “Non-Invasive hERG Channel Screening Based on Electrical Impedance Tomography and Extracellular Voltage Activation (EIT–EVA),” Lab Chip, pubs.rsc.org. Vendor roadmaps integrate robotics for micro-volume dispensing and cloud analytics that rank ligand hits automatically. Together, these advances reinforce the G-protein coupled receptors market as a fertile ground for precision pharmacology projects.

Growing Drug-Discovery Spend Targeting GPCRs

G protein-coupled receptors (GPCRs) underpin 36% of approved medicines[2]David E. Gloriam, “GPCR Drug Discovery: New Agents, Targets and Indications,” Nature Reviews Drug Discovery, nature.com, yet three-quarters of receptor subtypes still lack marketed drugs, prompting sustained R&D allocations. Diabetes and obesity agents alone delivered nearly USD 30 billion in 2024 sales, validating the commercial upside and steering budgets toward oral small-molecule GLP-1, amylin and dual-agonist candidates. Structure Therapeutics illustrates the scale, carrying USD 883.5 million in cash earmarked for Phase 2b GLP-1 and GIPR programs. Licensing deals echo investor confidence, with Novo Nordisk’s collaboration with Septerna valued at up to USD 2.2 billion for oral obesity pills. Such capital flows underpin the near-term pipeline and solidify the G-protein coupled receptors market as a strategic priority for big pharma.

Rising Burden of Chronic & Metabolic Diseases

Global diabetes prevalence is projected to reach 12.2% by 2045, intensifying demand for GPCR-modulating therapies that regulate glucose and weight. Eli Lilly’s oral GLP-1 candidate orforglipron cut HbA1c by up to 1.6% and trimmed 16 lbs in Phase 3 trials[3]Eli Lilly and Company, “Lilly's Oral GLP-1, Orforglipron, Demonstrated Statistically Significant Efficacy Results and a Safety Profile Consistent With Injectable GLP-1 Medicines in Successful Phase 3 Trial,” Eli Lilly and Company, investor.lilly.com, matching injectables in efficacy and demonstrating patient-friendly dosing. Beyond metabolism, GPCR targets in hypertensive kidney damage and β-adrenergic cardiovascular signaling open new frontiers for chronic disease management. These epidemiological and clinical tailwinds sustain the double-digit expansion of late-stage pipelines inside the G-protein coupled receptors market.

Expansion of Biologics & Allosteric Modulators

Monoclonal antibodies, peptides and bitopic ligands are gaining traction because they bind distal receptor pockets, enhancing selectivity and lowering off-target toxicity. Nxera Pharma’s tie-up with Antiverse harnesses in-silico antibody design to unlock previously intractable GPCR epitopes. Meanwhile, structural biology has revealed that allosteric ligand AP8 activates FFAR1 via intracellular loop shifts rather than helical rearrangements, inspiring new chemistry campaigns. Oncology programs highlight the promise: GPRC5D-directed bispecific antibodies are moving through trials for multiple myeloma, underscoring biologics’ role in diversifying the G-protein coupled receptors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Purification & stability challenges of GPCRs | -1.2% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Signal-bias complexity hampers assay design | -0.8% | Global, affecting all research segments | Long term (≥ 4 years) |

| High cost of advanced assay platforms | -0.7% | Emerging markets and smaller research institutions | Short term (≤ 2 years) |

| IP clustering limits freedom-to-operate | -0.5% | North America & Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Purification & Stability Challenges of GPCRs

Membrane proteins lose native conformation once removed from lipid bilayers, complicating crystallography and biophysical assays. Detergent solubilization often strips stabilizing lipids, prompting adoption of styrene–maleic-acid copolymers that preserve native nanodiscs. Recent innovations attach Gα-mimetic peptides to chromatography resin[4]Anthony D. Shumate, “A Rapid, Tag-Free Way to Purify Functional GPCRs,” Journal of Biological Chemistry, jbc.org, enabling tag-free isolation of active receptors at preparative scale. Nevertheless, each GPCR subtype demands bespoke thermostabilization cycles, delaying platform standardization and tempering near-term efficiency gains in the G-protein coupled receptors market.

Signal-Bias Complexity Hampers Assay Design

GPCRs can preferentially trigger G-protein, β-arrestin or G-protein-independent pathways, and biased agonists may deliver divergent clinical outcomes. Capturing these nuances requires multiplexed sensors such as split-TEV barcoded reporters that track parallel cascades simultaneously. Even with live-cell biosensors, data harmonization across laboratories remains difficult, prolonging assay development cycles. Machine-learning classifiers trained on multi-omic read-outs are emerging, yet consensus benchmarks are scarce, constraining widespread deployment and moderating the growth trajectory of the G-protein coupled receptors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Drive Innovation Despite Reagent Dominance

Reagents and kits provided the backbone of GPCR discovery workflows and represented 35.86% of G-protein coupled receptors market share in 2025, reflecting universal demand for buffers, ligands and detection chemistries. Automated liquid handlers, photonic readers and impedance modules constitute the platform category, which is climbing at an 8.58% CAGR thanks to miniaturization and cloud-linked analytics. The convergence of AI algorithms with optical sensors now supports end-to-end hit triaging inside a single workstation, accelerating time-to-lead and widening access for mid-tier firms.

Service contracts are expanding as drug sponsors outsource high-content screens to CROs that maintain proprietary cell banks and assay libraries. Eurofins CEREP, for example, couples 20 years of receptor pharmacology know-how with high-density screening lines to shorten client program timelines. Hybrid offerings bundle reagents, plates and analytics licences under subscription models, allowing labs to align capital outlay with project milestones. Consequently, platforms and service ecosystems anchor the value shift within the G-protein coupled receptors market.

By Assay Type: cAMP Assays Lead Growth Through Enhanced Sensitivity

Intracellular calcium mobilization kits led revenues at 28.45% in 2025, mirroring their historic role in class-A receptor programs. Yet cAMP detection formats are projected to register a 8.85% CAGR, underpinned by NanoLuc binary technologies that quantify cyclic-AMP in live cells with sub-nanomolar sensitivity. Radioligand and GTPγS methods endure for orthogonal confirmation, although regulatory pressure on radioisotope waste curbs broader uptake.

β-arrestin biosensors continue to gain currency for pathways implicated in cardiometabolic safety profiling, and label-free impedance plates now record morphological changes without fluorescent tags. ThermoBRET protocols further streamline thermostability assessments by eliminating labelled ligands, trimming consumable costs during lead optimization. Collectively, these technologies extend the functional repertoire available to the G-protein coupled receptors market.

By Therapeutic Area: Cardiovascular Applications Accelerate Growth

Oncology retained the largest slice of the G-protein coupled receptors market size at 31.95% in 2025 as immune-targeted innovations such as GPRC5D bispecific antibodies advanced into pivotal trials. Cardiovascular projects, however, are slated for the quickest climb at an 8.19% CAGR, propelled by allosteric modulators that fine-tune β-adrenergic and angiotensin receptor responses while reducing tachyphylaxis risks.

Central nervous system research benefits from first-in-class GPR52 agonists aimed at schizophrenia’s negative and cognitive symptoms, reflecting a shift toward poly-symptomatic control. Metabolic disease programs retain commercial heft due to GLP-1 and amylin franchise expansions, while respiratory and renal indications explore orphan GPCRs as fresh intervention points. These developments diversify revenue anchors and amplify therapeutic optionality across the G-protein coupled receptors market.

By End-User: Academic Sector Drives Innovation Growth

Pharmaceutical and biotech firms occupied 45.20% of 2025 revenues, reflecting sustained pipeline ownership across discovery and pre-clinical phases. Yet academic and research institutes are projected to expand at an 8.53% CAGR as governments channel grants into deorphanization consortia that map ligand-receptor pairs. Public-private hubs equip universities with cryo-EM suites and long-read sequencing cores, enabling foundational discoveries that feed directly into out-licensing streams.

Contract research organizations have scaled specialist GPCR units, allowing sponsors to book turnkey panels covering 400+ receptors at fixed fees. Diagnostic laboratories, though nascent, are validating GPCR-derived biomarkers for disease monitoring and therapeutic response, an avenue expected to unlock ancillary revenues. Overall, multidisciplinary collaboration is deepening the innovation wellspring sustaining the G-protein coupled receptors market.

Geography Analysis

North America commanded 37.10% of 2025 sales as Boston, San Francisco and San Diego clusters combined venture capital, AI talent and FDA guidance that clarifies machine-learning evidence packages. Domestic incumbents release iterative instrumentation upgrades annually, enabling users to retrofit established laboratories without disruptive capital cycles. Long-standing NIH funding streams for structural biology further solidify the region’s dominance within the G-protein coupled receptors market.

Europe contributes a balanced mix of academic excellence and regulatory pragmatism. EMA endorsements of Winrevair for pulmonary arterial hypertension and Obgemsa for overactive bladder verified the approval pathway for novel GPCR therapies in 2024. Continental institutes such as the University of Basel are pushing envelope techniques like GPS-NMR to trace receptor motions at atomic resolution, insights that feed directly into ligand engineering cycles. Combined, these factors nurture a robust albeit steady growth profile across the European slice of the G-protein coupled receptors market.

Asia-Pacific, projected at an 8.69% CAGR through 2031, benefits from concerted governmental drives to bolster biotech self-reliance and harmonize approval timelines. Japan’s discovery of intracellular-side activators such as PCO371 exemplifies the region’s ingenuity, promising orally available agents with reduced systemic side-effects. China and South Korea are expanding manufacturing capacity for peptide therapeutics, while venture funds co-invest with multinationals to accelerate regional trial sites. Emerging economies in Latin America, the Middle East and Africa remain smaller but are ramping clinical infrastructure via technology-transfer agreements, positioning themselves as future contributors to the G-protein coupled receptors market.

Competitive Landscape

The G-protein coupled receptors market is moderately consolidated, with Thermo Fisher Scientific, Danaher (Molecular Devices) and Promega integrating reagents, detection modules and analytics into cohesive portfolios. Waters Corporation reports that 80% of 2025 novel-drug filings used its Empower software, illustrating how informatics integration cements switching costs. These incumbents supplement organic pipelines with bolt-on buys that add niche biosensor or microfluidic assets.

Specialist biotech entrants such as Structure Therapeutics wield focused GPCR platforms and substantial war-chests, pressuring traditional suppliers to accelerate innovation cycles. AI-native start-ups deploy proprietary ligand-prediction engines, carving out high-margin service layers that sit upstream of wet-lab assays. Patent clustering around algorithmic design continues apace, although USPTO guidelines mandating meaningful human input mitigate blanket claim risks. Consequently, collaboration models—exemplified by Novo Nordisk’s USD 2.2 billion alliance with Septerna—have emerged as favoured vehicles for de-risking early concepts while retaining commercial upside.

White-space opportunity persists in orphan receptor mapping, accounting for roughly 75% of unexploited GPCRs. Companies able to marry cryo-EM, deep learning and high-content pharmacology stand to capture outsized royalties as first-in-class therapeutics surface. In parallel, reagent vendors are experimenting with subscription pricing and cloud-hosted analytics to broaden access among mid-sized academic teams, further democratizing the G-protein coupled receptors market.

Global G-Protein Coupled Receptors (GPCR) Industry Leaders

Abcam plc.

Danaher Corporation

Promega Corporation

Revvity Inc

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Novo Nordisk partnered with Septerna in a transaction potentially worth USD 2.2 billion to develop oral GPCR-targeted obesity drugs.

- February 2025: Structure Therapeutics finished enrolling ACCESS trials for aleniglipron, backed by USD 883.5 million cash reserves.

- November 2024: Nxera Pharma and Antiverse initiated an antibody design alliance targeting difficult GPCR epitopes.

- June 2024: FDA authorized dual PPAR agonist Elafibranor (Iqirvo) for primary biliary cholangitis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the G-protein-coupled receptors (GPCR) market as the annual worldwide revenue generated from reagents, kits, cell lines, assay platforms, detection instruments, and contract research services that enable GPCR-based drug discovery and screening.

Scope Exclusion: Diagnostic test kits deployed in routine clinical laboratories are kept outside this estimate because they follow distinct procurement, pricing, and regulatory paths.

Segmentation Overview

- By Component

- Reagents & Kits

- Cell Lines

- Assay Platforms

- Detection Instruments

- Services

- By Assay Type

- Calcium Level Detection Assays

- Radioligand Binding & GTP?S Assays

- cAMP & cGMP Assays

- β-Arrestin Functional Assays

- Reporter Gene Assays

- Label-free Impedance Assays

- Other Assay Types

- By Therapeutic Area

- Cardiovascular System

- Central Nervous System

- Oncology

- Metabolic Disorders

- Respiratory Diseases

- Other Therapeutic Areas

- By End-User

- Pharmaceutical & Biotech Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Diagnostic Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts conducted interviews with in-house assay scientists at global pharma majors, procurement managers at contract research organizations, and academic core-facility heads across North America, Europe, and Asia-Pacific. Their insights validated reagent mark-ups, uptake of label-free impedance readers, and emerging demand for AI-guided structure screens, allowing us to fine-tune assumptions surfaced from desk work.

Desk Research

We began by mapping the universe of GPCR laboratory spending through publicly available sources such as the US NIH RePORTER grant database, Eurostat's R&D expenditure tables, World Bank health-innovation indicators, and import-export records from UN Comtrade for fluorescent dyes and microplates that dominate GPCR workflows. Company 10-Ks, investor decks, and trade-association fact sheets (e.g., AsiaBio, EFPIA) helped us assign baseline average selling prices and replacement cycles for reagents. Where revenue splits were not explicit, D&B Hoovers and Dow Jones Factiva subscription feeds provided directionally consistent ranges. The sources listed are illustrative; a broader set of open publications and paywalled feeds informed every datapoint.

Market-Sizing & Forecasting

We applied a top-down build, first estimating the global pool of active GPCR drug-discovery projects and then translating it into laboratory spending through penetration-rate and spend-per-project coefficients. Results were cross-checked with selective bottom-up roll-ups drawn from supplier disclosures and channel checks to reconcile any over- or under-shoot. Key drivers embedded in the model include R&D intensity per therapeutic area, high-throughput screening throughput upgrades, regional biotech funding rounds, reagent repurchase frequency, and average list prices of calcium-flux kits. A multivariate regression with lagged funding variables captures demand elasticity, while scenario analysis accounts for accelerated AI adoption or funding pullbacks.

Data Validation & Update Cycle

Outputs pass variance and anomaly screens, then a senior analyst review. We refresh the dataset each year and issue interim revisions when material events, such as a structural shortage of luminescence substrates, shift baseline assumptions.

Why Mordor's G-Protein Coupled Receptors Market Baseline Commands Reliability

Published estimates often differ; scope choices, currency timing, and refresh cadence explain most gaps. We anchor our baseline on current-year spending by every revenue-earning entity in the GPCR tool chain, whereas some publishers rely on pipeline counts or partially cover regions.

Key gap drivers include narrower product coverage that omits detection hardware, exclusion of fast-growing Asian start-ups, single ASP proxies instead of tiered pricing, and forecasts extrapolated from historic CAGR without segment checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.52 B (2025) | Mordor Intelligence | |

| USD 3.92 B (2024) | Global Consultancy A | Leaves out CRO screening services and uses 2023 currency averages |

| USD 4.00 B (2024) | Regional Consultancy B | Merges assay platforms with reagents, applies uniform ASP, omits early-stage Asia funding wave |

| USD 3.41 B (2025) | Trade Journal C | Focuses only on cell lines and kits, lacks instrument revenue and triangulation interviews |

In short, by aligning scope with real purchasing patterns, validating every ratio with practitioners, and refreshing models on an annual cadence, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can reliably trace and replicate.

Key Questions Answered in the Report

What key technology is reshaping early-stage GPCR drug discovery?

Structure-guided design powered by AlphaFold2 models is replacing radioligand screens by enabling rapid in-silico docking across hundreds of receptor templates.

Which product category is expanding fastest within GPCR research labs?

Automated assay platforms are outpacing traditional reagents because integrated optics and cloud analytics reduce hands-on time and boost hit validation speed.

Why are cardiovascular indications attracting new GPCR investment?

Discoveries in allosteric modulation of β-adrenergic and angiotensin pathways promise better safety profiles than earlier small-molecule antagonists.

How are academic institutions influencing the competitive landscape?

University-industry consortia are deorphanizing receptors through shared cryo-EM suites, creating licensing opportunities that challenge incumbent suppliers.

What intellectual-property trend could slow smaller GPCR start-ups?

Clustering of broad patents around AI-enabled screening workflows raises freedom-to-operate barriers for companies without deep legal resources.

Which assay innovation is gaining traction for label-free GPCR measurement?

Electrical impedance tomography coupled with extracellular voltage activation provides non-invasive readouts that correlate strongly with patch-clamp data.

Page last updated on: