Machine Glazed Paper Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

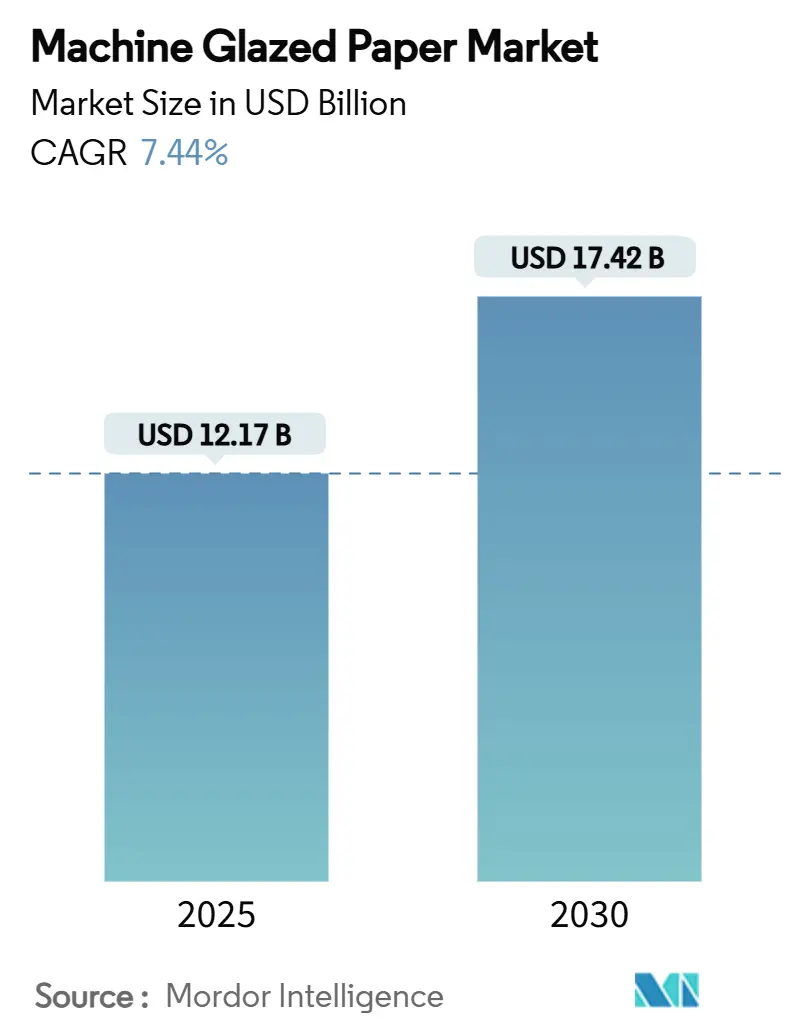

| Market Size (2025) | USD 12.17 Billion |

| Market Size (2030) | USD 17.42 Billion |

| Growth Rate (2025 - 2030) | 7.44% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Machine Glazed Paper Market Analysis by Mordor Intelligence

The machine glazed paper market size stands at USD 12.17 billion in 2025 and is forecast to reach USD 17.42 billion by 2030, expanding at a 7.44% CAGR. Heightened sustainability regulations, brand-owner commitments to recyclability, and the accelerating pivot away from PFAS in food contact materials collectively underpin demand. E-commerce growth multiplies shipments that need strong yet lightweight mailers, while Asia-Pacific’s installed capacity keeps production costs competitive. Investments in premium bleached grades address the healthcare sector’s sterility requirements, and capacity optimizations help large producers counter pulp-price volatility. Trade policies, however, inject cost uncertainty that smaller converters must manage through long-term supply contracts.

Key Report Takeaways

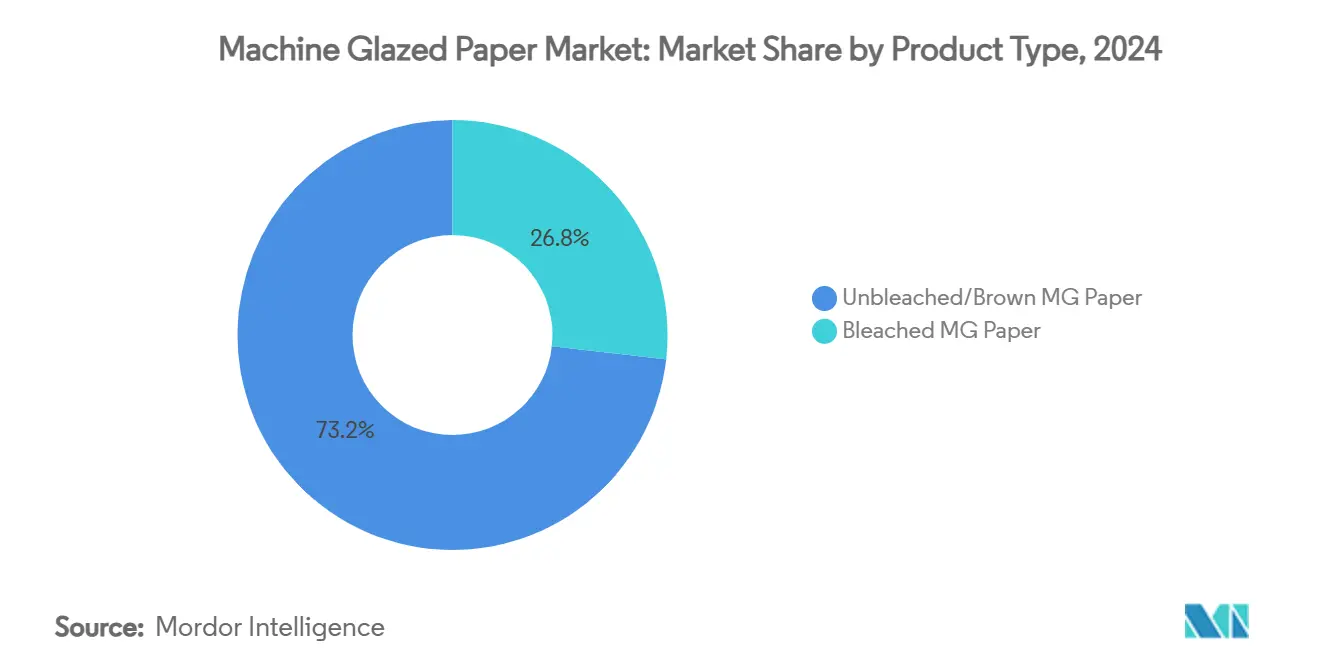

- By product type, the machine-glazed paper market size for the bleached MG paper segment is projected to grow at an 8.86% CAGR between 2025-2030.

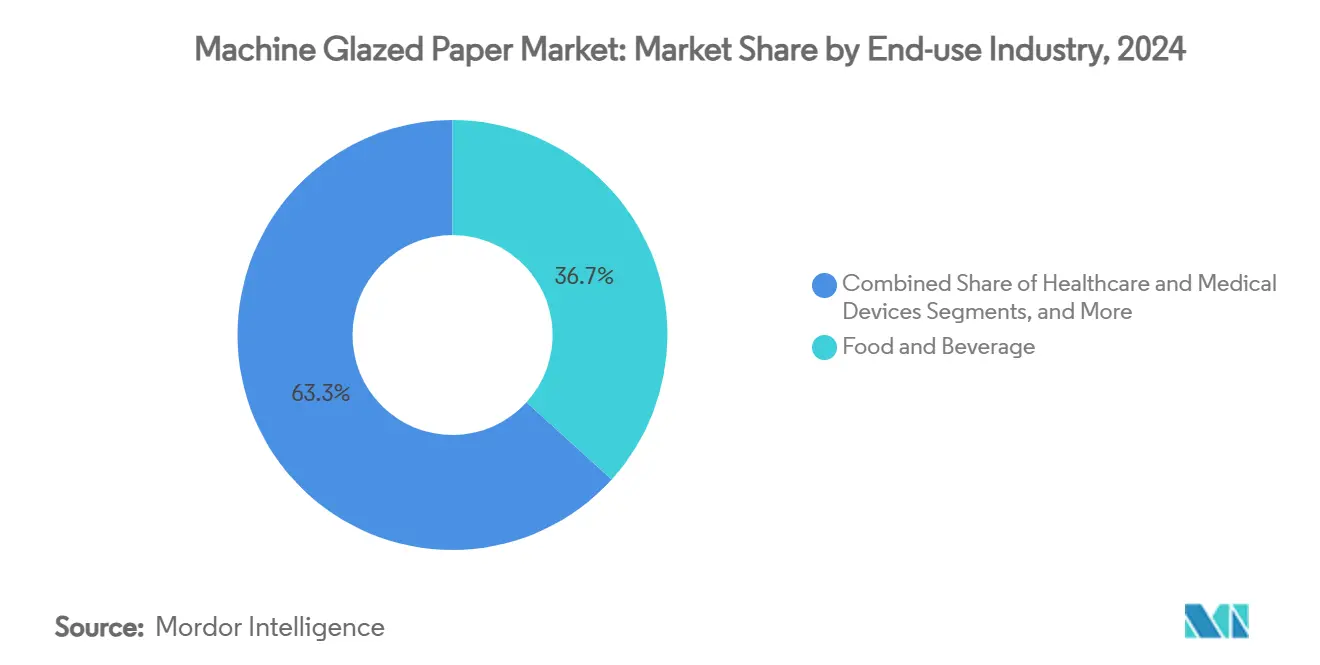

- By end-use industry, the food and beverage industry captured a 36.72% of the machine-glazed paper market share in 2024.

- By application, the machine-glazed paper market size for the pouches and sachets segment is projected to grow at an 8.91% CAGR between 2025-2030.

- By geography, Asia-Pacific captured a 33.15% of the machine-glazed paper market share in 2024.

Global Machine Glazed Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability regulations favour paper over plastics | +1.2% | Global, with EU and North America leading | Medium term (2-4 years) |

| E-commerce surge boosting flexible paper packaging demand | +1.8% | Global, concentrated in APAC and North America | Short term (≤ 2 years) |

| Food-service bans on PFAS and plastics | +0.9% | North America and EU primarily | Short term (≤ 2 years) |

| Growth in medical device sterilizable wraps | +0.7% | Global, with developed markets leading | Long term (≥ 4 years) |

| Installed MG capacity shifts to Asia creating cost advantage | +1.1% | APAC core, spill-over to global markets | Medium term (2-4 years) |

| Brand-owner shift to glossy fibre-based mailers | +0.5% | North America and EU primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustainability Regulations Favour Paper Over Plastics

Global regulators intensify efforts to phase out single-use plastics, positioning the machine glazed paper market as a primary beneficiary. The European Union’s Packaging and Packaging Waste Regulation mandates economic recyclability by 2030 and restricts PFAS in food contact packaging, prompting brand owners to switch to fibre-based solutions.[1]European Commission, “New EU Regulation Promotes the Procurement of Sustainable Packaging,” europa.eu Parallel initiatives in North America elevate recycled-content targets and impose landfill fees on difficult-to-process polymers, further widening the cost differential. Public-sector procurement rules that prioritize renewable materials institutionalize demand for recyclable wraps and mailers. Harmonized labelling improves consumer recognition of paper’s end-of-life advantages, translating policy into purchasing behaviour. Producers that certify materials under relevant eco-labels gain preferential access to procurement frameworks, reinforcing first-mover advantages within the machine glazed paper market.

E-commerce Surge Boosting Flexible Paper Packaging Demand

Online retail maintains double-digit growth, reshaping logistics networks and elevating packaging performance requirements. Asia-Pacific, home to the world’s largest e-commerce user base, now channels a rising share of parcels through fulfilment centres that demand space-efficient fibre mailers. Machine-glazed papers combine tensile strength with printability, enabling brands to ship, market, and display sustainability credentials in one substrate. Cross-border orders expose packages to multiple handling points, making burst strength a critical differentiator over uncoated kraft. Direct-to-consumer subscription models amplify demand for pouch and sachet formats that deliver portion control and vivid graphics. As returns handling gains strategic focus, lightly coated MG mailers that withstand reverse logistics cycles retain product resale value, positioning the machine glazed paper market for sustained volume gains.

Food-Service Bans on PFAS and Plastics

The United States Food and Drug Administration completed the phase-out of PFAS-containing grease-proofing agents in June 2025, opening a considerable substitution window for MG wraps that can accommodate hot, oily foods. Several U.S. states add further restrictions that bar expanded polystyrene clamshells, putting quick-service chains under immediate compliance deadlines. Similar PFAS bans in Denmark and the Netherlands reinforce European momentum. MG substrates engineered with aqueous dispersion coatings deliver the required oil and moisture barrier while retaining recyclability, a benefit plastic-lined papers lack. National restaurant franchises use the shift to highlight corporate ESG goals, pulling demand through global supply chains. Incremental cost premiums are offset by avoiding potential litigation linked to PFAS exposure, solidifying long-term adoption within the machine glazed paper industry.

Growth in Medical Device Sterilizable Wraps

ISO 11607-1:2019 codifies strict performance criteria for terminally sterilized medical device packaging, raising the entry bar for materials that maintain sterility until point of use. Bleached machine-glazed grades exhibit pore size uniformity and resistance to high-temperature steam autoclaves, satisfying institutional buyers. Ageing Western populations and expanded surgical volumes in emerging markets increase consumption of single-use sterile barrier systems. Hospitals pressured to reduce plastic waste profile MG wraps as the sustainable complement to reusable instrument trays. Device manufacturers seek global standardization of packaging SKUs, favoring multi-regional MG suppliers that guarantee consistent quality. The premium pricing achievable in this niche offsets higher pulp input costs, supporting revenue diversification across the machine glazed paper market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile pulp prices squeeze MG producer margins | -1.4% | Global, with fiber-dependent regions most affected | Short term (≤ 2 years) |

| Competition from MF kraft and glassine release papers | -0.8% | Global, concentrated in industrial applications | Medium term (2-4 years) |

| Energy-intensive Yankee cylinder drying caps ESG scores | -0.6% | Global, with stricter regulations in developed markets | Long term (≥ 4 years) |

| Trade barriers on unbleached kraft imports | -0.7% | North America and EU primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp Prices Squeeze MG Producer Margins

Wood-pulp costs remain the largest single variable in MG production and have fluctuated sharply, with the U.S. Producer Price Index rising to 219.835 in May 2024 before easing only marginally. Producers pass through surcharges but often with a multi-quarter lag, compressing EBITDA in the interim. Integrated mills hold a partial hedge, yet still confront higher harvesting and transportation expenses as fossil-fuel prices stay elevated. Smaller converters without long-term fibre contracts face the steepest risk, prompting consolidation or exit. Country-specific incentives such as the USDA’s Wood Innovation Grants promise future feedstock diversification, but near-term relief appears limited. Consequently, pulp volatility weighs on investment appetite, tempering upside in the machine glazed paper market.

Competition from MF Kraft and Glassine Release Papers

Certain industrial segments can substitute machine-finished kraft or glassine for core MG applications, especially when gloss and printability take a back seat to basic wrap functions. Glassine’s natural grease resistance suits bakery liners, while MF kraft presents a lower-price option for manual bagging lines. Recycling infrastructure also favours uncoated liners in some jurisdictions, diverting orders from coated MG formats. Technological improvements narrow the tensile-strength gap, weakening MG’s historical performance moat. Brand-owner trials with hybrid structures indicate willingness to experiment when cost-savings exceed marketing benefits. Although MG retains leadership in aesthetic-driven niches, the machine glazed paper industry must continue value-engineering to defend share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bleached Grades Close the Gap

Unbleached substrates retained 73.21% of 2024 volume, reflecting their cost effectiveness and alignment with rustic branding in organic foods. The segment’s dominance anchors base-load demand in the machine glazed paper market. Scarcity of bleaching chemicals in some emerging regions further entrenches natural brown grades for industrial sacks. That said, bleached MG is forecast at an 8.86% CAGR, reflecting health-care sterility norms and premium confectionery wrappers that prioritize pristine aesthetics. Bleached formats command higher unit margins, helping producers counter pulp inflation. Investments in elemental-chlorine-free processes and optical brighteners extend shelf appeal without compromising recyclability.

Bleached advances also benefit from ISO-driven medical device protocols demanding low bioburden surfaces. Suppliers certify bacterial filtration levels, allowing hospitals to streamline validation steps. Consumer awareness campaigns equating whiteness with cleanliness boost take-up in ready-to-eat meal pouches. Graphic designers capitalize on the substrate’s high opacity for photorealistic imagery, a challenge on darker kraft. Manufacturers balance the added energy load of bleaching against brand-owner willingness to absorb small cost premiums. These dynamics underpin the sustained expansion of bleached grades within the machine glazed paper industry.

By End-Use Industry: Healthcare Ascends

Food and beverages accounted for 36.72% revenue in 2024, underpinned by quick-service chains switching from plastic to MG wraps post-PFAS bans. Embossable textures give artisanal bakeries tactile differentiation and moisture control. Yet the healthcare vertical is accelerating at an 8.74% CAGR to 2030, propelled by ageing populations and surgical volume growth that elevate demand for sterile barrier systems. Medical-device OEMs specify MG for autoclave-compatibility and fibre-tear performance during aseptic opening, ensuring sterility maintenance. Contract sterilizers also favour MG due to its predictable moisture vapour transmission, reducing cycle adjustments.

Cosmetics and personal care add incremental growth as indie brands adopt fibre tubs and sachets to reinforce natural positioning. Building-materials suppliers utilize MG laminates as protective flooring during renovation, valuing abrasion resistance. Across each niche, regulatory endorsements amplify confidence in paper-based solutions. Consequently, diversified downstream usage stabilizes revenue volatility across the machine glazed paper market.

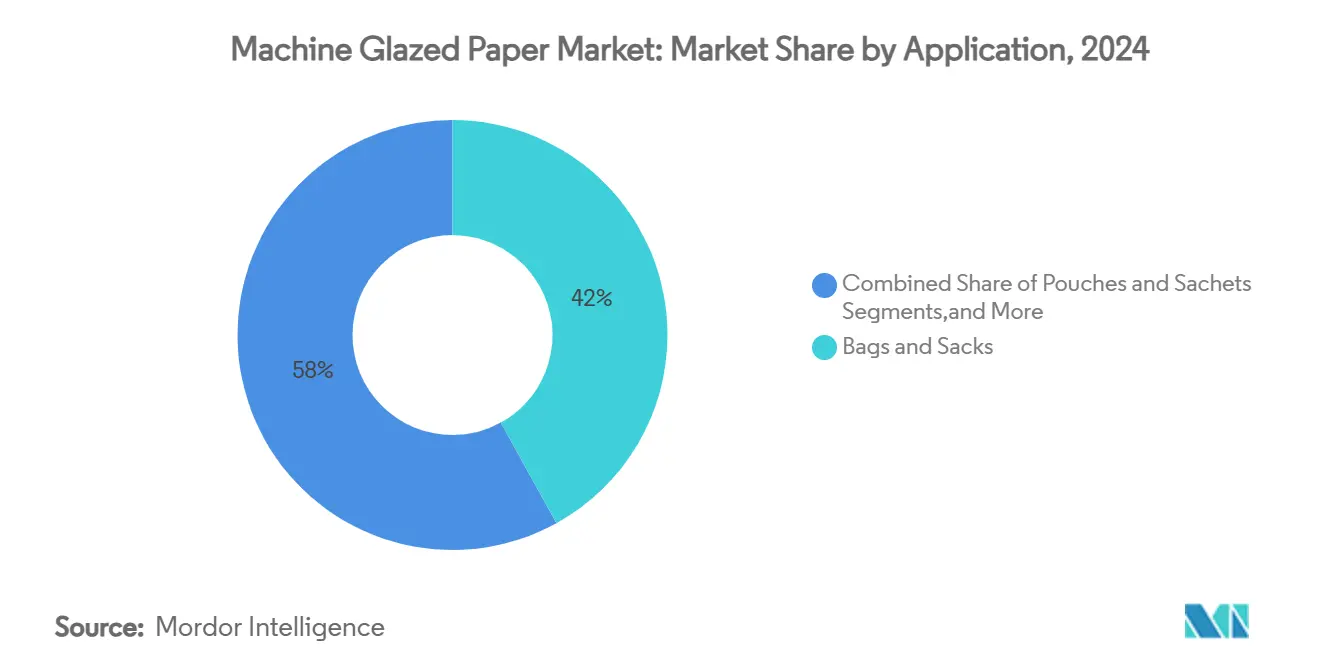

By Application: Flexible Formats Outpace Legacy Bags

Bags and sacks still delivered 41.97% of 2024 turnover, supported by entrenched grocery and industrial distribution channels. Cost-per-unit advantages and existing filling lines keep converters loyal to the format. However, pouches and sachets record the fastest expansion at an 8.91% CAGR, mirroring single-serve trends in nutraceuticals and instant beverages. Lightweight formats reduce freight expenditure for cross-border e-commerce shipments prevalent in Asia-Pacific. MG papers laminated with thin bio-resins provide moisture oxygen barriers necessary for powdered foods.

Release liners face recycling headwinds due to silicone contamination, tempering volume prospects despite growth in pressure-sensitive labels. Wraps and laminates enjoy niche demand for protective layers around engineered wood panels and metal coils. Collectively, diversification across applications enhances revenue resilience and broadens the total addressable opportunity for the machine glazed paper market.

Geography Analysis

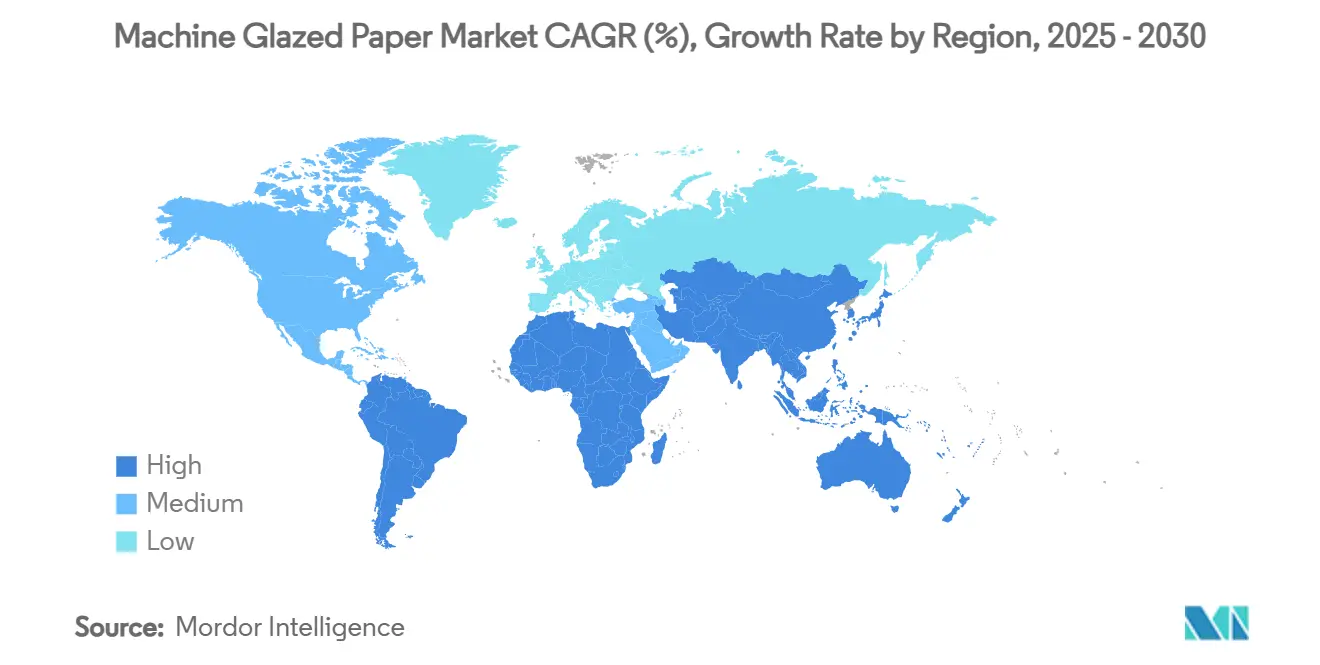

Asia-Pacific led the machine-glazed paper market with a 33.15% share in 2024, leveraging expansive mill networks and supportive fiscal policy. China’s 280.21 million t pulp-and-paper output underscores industrial heft, while subsidies for 5.8 million ha of pulpwood plantations bolster long-term fibre security.[2]Barr C. and Cossalter C., “China’s Development of a Plantation-Based Wood Pulp Industry,” ingentaconnect.com Rapid e-commerce uptake fuels conversion demand, especially for glossy mailers that enable brands to cross national borders cost-effectively. Japan and South Korea emphasize premium white grades for cosmetics and medical devices, enhancing value density per tonne.

The Middle East and Africa posts the fastest 9.08% CAGR through 2030, buoyed by consumer-goods expansions in Saudi Arabia, the UAE, and Nigeria. Economic diversification agendas include packaging clusters that import MG reels for local conversion, creating a pull market for global suppliers. Infrastructure spend raises cement bag demand, a niche that unbleached MG fills efficiently.

North America remains stable, but tariff regimes on Chinese imports skew sourcing toward domestic mills despite higher unit costs. PFAS bans drive substitution toward MG in foodservice, yet pulp price swings challenge margin management. Europe’s PPWR accelerates recyclable packaging uptake; however, energy levies and emission caps pressure operating costs. South America offers fibre-rich locations but contends with rail and port bottlenecks that elongate export lead times. Collectively, these regional dynamics shape strategic capital allocation across the machine glazed paper industry.

Competitive Landscape

Market concentration is moderate, with vertically integrated groups leveraging scale to weather pulp volatility. Stora Enso lifted Q1 2025 sales 9% to EUR 2,362 million (USD 2,556 million) by pivoting toward renewable packaging boards. Mondi’s EUR 1.2 billion (USD 1.29 billion) capital programme targets corrugated and flexible upgrades meant to lock in energy efficiency gains.[3]Mondi Group, “Half-Year Results Announcement 2024,” mondigroup.com Smurfit Westrock’s decision to close 500,000 t of United States capacity while adding converting sites exemplifies the shift from commodity paper toward higher-margin downstream formats.

Sustainability remains the competitive fulcrum. WestRock reports 96% of its packaging is recyclable, compostable, or reusable, supporting large CPG targets for fibre content. Investments in biomass boilers and heat-recovery hoods signal the next efficiency frontier as energy-intensive MG lines pursue carbon-reduction roadmaps. Technological differentiation emerges via barrier-coating chemistries that swap fluorocarbons for bio-based polymers without sacrificing oil resistance.

Mid-tier players pursue geographic specialization, focusing on MEA demand spikes or Latin American fibre abundance to carve defensible niches. Private-equity interest increases as packaging valuations stay resilient, though execution risk tied to pulp volatility tempers deal multiples. Start-ups with enzyme-assisted refining technologies promise lower-energy MG production, challenging incumbents if scalability hurdles fall. Overall, disciplined capital deployment centred on sustainable competitive advantages underpins value retention in the machine glazed paper market.

Machine Glazed Paper Industry Leaders

Stora Enso Oyj

Georgia-Pacific LLC

Oji Holdings Corporation

Mondi PLC

Smurfit Westrock PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smurfit Westrock reported first-quarter 2025 net sales of USD 7,656 million with adjusted EBITDA of USD 1,252 million, while announcing closure of over 500,000 t of paper capacity in North America and construction of new converting plants to enhance efficiency.

- April 2025: The White House issued an executive order implementing a reciprocal tariff policy with an additional 10% duty on imports, significantly impacting paper product costs and reshaping supply-chain strategies.

- February 2025: The European Union’s Packaging and Packaging Waste Regulation came into force, mandating economic recyclability by 2030 and restricting PFAS in food contact packaging.

- February 2025: Stora Enso posted a 9% year-on-year increase in Q1 2025 sales to EUR 2,362 million (USD 2,556 million) with adjusted EBIT of EUR 175 million (USD 189 million), reflecting continued performance improvements.

Global Machine Glazed Paper Market Report Scope

| Bleached MG Paper |

| Unbleached/Brown MG Paper |

| Food and Beverage |

| Healthcare and Medical Devices |

| Personal Care and Cosmetics |

| Building and Construction |

| Industrial and Others |

| Bags and Sacks |

| Wraps and Laminates |

| Pouches and Sachets |

| Release Liners and Labels |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Bleached MG Paper | ||

| Unbleached/Brown MG Paper | |||

| By End-use Industry | Food and Beverage | ||

| Healthcare and Medical Devices | |||

| Personal Care and Cosmetics | |||

| Building and Construction | |||

| Industrial and Others | |||

| By Application | Bags and Sacks | ||

| Wraps and Laminates | |||

| Pouches and Sachets | |||

| Release Liners and Labels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current machine glazed paper market size?

The machine glazed paper market size is USD 12.17 billion in 2025 and is projected to hit USD 17.42 billion by 2030.

Which region leads the machine glazed paper market?

Asia-Pacific holds the largest share at 33.15% owing to extensive manufacturing capacity and supportive fiscal policies.

Which application segment is growing fastest?

Pouches and sachets achieve the highest 8.91% CAGR through 2030 as e-commerce and single-serve product formats gain traction.

How do PFAS bans influence demand?

PFAS bans in food contact materials redirect orders toward MG wraps that deliver grease resistance without fluorochemicals, boosting North American and EU volumes.

Why are bleached grades gaining momentum?

Bleached machine-glazed papers grow at 8.86% CAGR because healthcare and premium food brands require high cleanliness perception and sterilization compatibility.

Page last updated on: