Ice-Cream Paperboard Cups Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

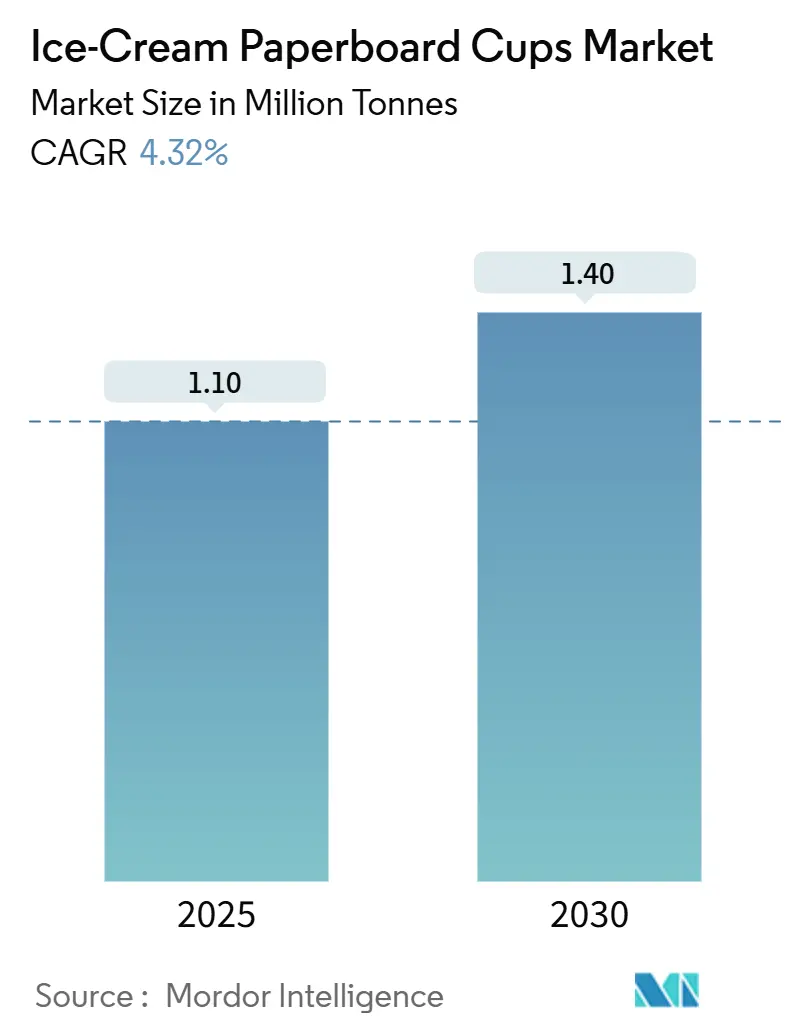

| Market Volume (2025) | 1.10 Million tonnes |

| Market Volume (2030) | 1.40 Million tonnes |

| Growth Rate (2025 - 2030) | 4.32% CAGR |

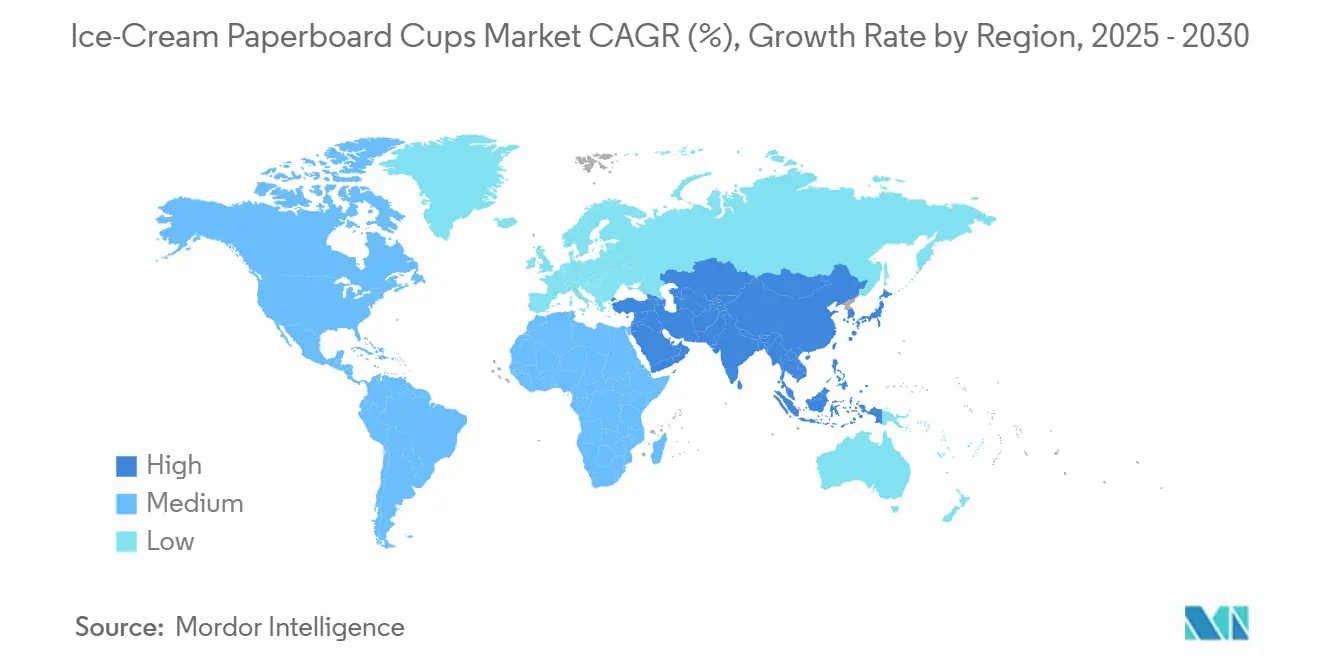

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ice-Cream Paperboard Cups Market Analysis by Mordor Intelligence

The Ice-Cream Paperboard Cups Market size is estimated at 1.10 Million tonnes in 2025, and is expected to reach 1.40 Million tonnes by 2030, at a CAGR of 4.32% during the forecast period (2025-2030).

Heightened regulatory scrutiny of single-use plastics, swift progress in PFAS-free barrier technologies, and a steady shift in consumer sentiment toward low-impact packaging together underpin a clear, medium-term growth runway. Manufacturers possessing aqueous dispersion coating lines enjoy a first-mover cost edge because recent FDA and EU rulings have tightened compliance timelines. Mid-range cup capacities gain further traction as premium take-home formats proliferate, while virgin fiber continues to dominate input selection owing to its freezer performance and printability. Regionally, Asia-Pacific sets the growth pace on the back of quick-service restaurant expansion and rising disposable incomes, whereas North America and Europe provide regulatory-driven stability that rewards technology-led incumbents. Strategic investments in vertical integration, recycled-content blending, and short-run digital printing are therefore becoming critical to margin resilience against raw-material volatility.

Key Report Takeaways

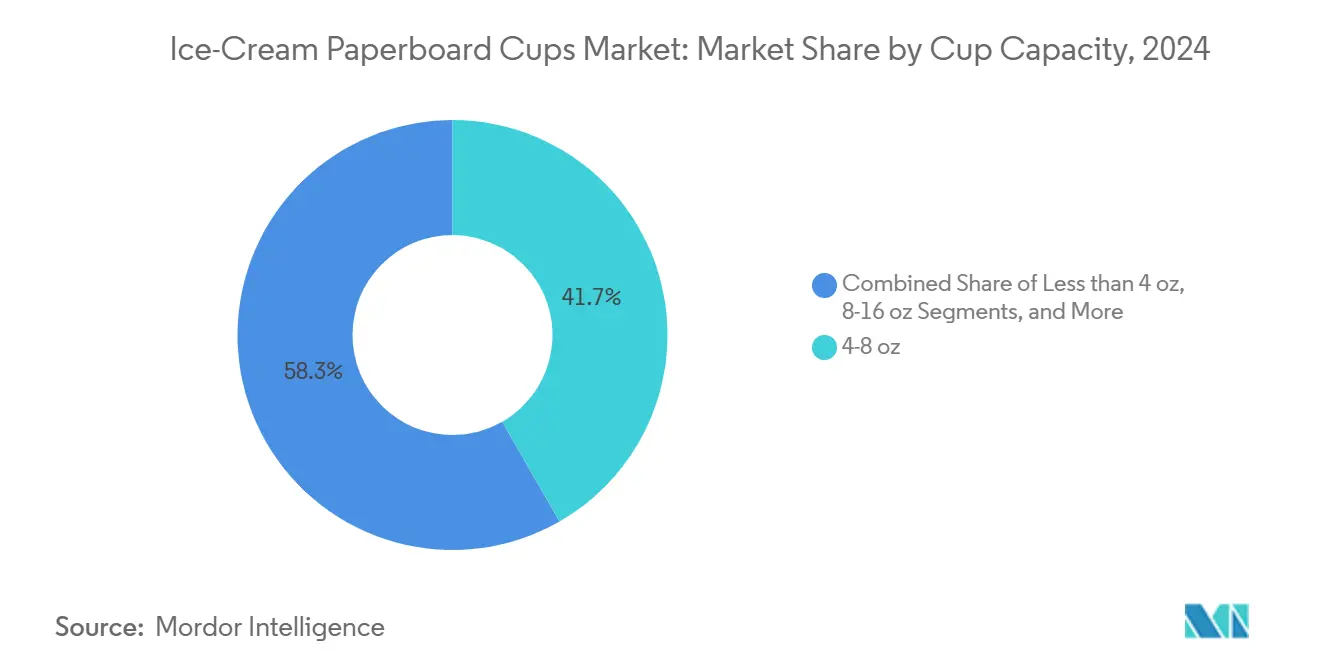

- By cup capacity, the 4-8 oz capacity segment captured 41.71% of the ice-cream paperboard cups market share in 2024.

- By coating type, the polyethylene segment accounted for 67.41% of the ice-cream paperboard cups market size in 2024.

- By end-user, the ice-cream paperboard cups market size for the retail take-home cups is projected to grow at a 4.81% CAGR between 2025-2030.

- By material, the virgin fiber secured 74.67% of the ice-cream paperboard cups market size in 2024.

- By geography, the ice-cream paperboard cups market size for Asia-Pacific is projected to expand at a 6.47% CAGR between 2025-2030.

Global Ice-Cream Paperboard Cups Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability regulations shifting demand from plastic to fiber cups | +1.2% | EU, North America, gradually global | Medium term (2-4 years) |

| Growth in take-home pint and multi-serve ice-cream consumption | +0.8% | North America, Europe, spreading to APAC | Long term (≥ 4 years) |

| QSR dessert menu expansion in emerging economies | +1.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Digital short-run printing enabling artisanal gelato brands | +0.3% | North America & EU premium segments | Short term (≤ 2 years) |

| Commercialization of PFAS-free water-based barrier technologies | +0.7% | Global | Medium term (2-4 years) |

| Government PFAS bans accelerating coating conversions | +0.9% | North America & EU, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustainability Regulations Shifting Demand from Plastic to Fiber Cups

A tightening policy backdrop is decisively altering material choices for frozen-dessert packaging. The EU Single-Use Plastics Directive outlawed expanded polystyrene containers and placed paperboard cups with plastic linings under extended producer responsibility, forcing converters to accelerate PFAS-free innovation[1]European Parliament and Council, “Directive (EU) 2019/904 of 5 June 2019 on the reduction of the impact of certain plastic products on the environment,” europa.eu. In North America, the FDA’s March 2025 revocation of 35 PFAS food-contact approvals triggers mandatory coating changeovers by mid-2025[2]U.S. Food and Drug Administration, “FDA determines authorization for 35 food contact notifications related to PFAS are no longer effective,” fda.gov. Canada’s single-use plastics ban, coupled with the United Kingdom’s nationwide restrictions, further narrows the window for non-compliant substrates. Manufacturers equipped with aqueous dispersion assets can therefore secure multi-year supply contracts, as brand owners realign portfolios toward certified recyclable formats. Short-run digital print capability strengthens this advantage by allowing quick artwork changes without interrupting coating workflows, ensuring speed-to-market for seasonal SKUs.

Growth in Take-Home Pint and Multi-Serve Ice-Cream Consumption

Premiumisation is reshaping retail freezer aisles. U.S. ice-cream makers produced 1.3 billion gallons in 2023, and low-fat plus non-fat variants crossed the 35% threshold for the first time[3]USDA Economic Research Service, “Low-fat and nonfat ice cream production is heating up the market,” ers.usda.gov. The shift toward better-for-you options often entails higher-value recipes that merit rigid, moisture-resistant cups sized at 8-16 oz—the fastest-growing capacity bracket at a 5.57% CAGR. Consumers buying fewer occasions yet trading up to indulgent flavours regard durable paperboard as proof of freshness, especially for products that travel between click-and-collect depots and home freezers. Retailers, meanwhile, demand shelf-ready graphics plus tamper-evident sealing, reinforcing the attractiveness of virgin-fiber board with advanced aqueous barriers.

QSR Dessert Menu Expansion in Emerging Economies

Fast-food operators across Asia and the Middle East are adding soft-serve and sundae lines to drive ticket sizes. Franchise formats require uniform packaging specifications that perform under hot-to-cold service cycles and intense delivery-app handling. Portion-controlled 4-8 oz cups suit these menus and simplify inventory across multi-country networks. Suppliers that can certify compliance with China’s updated GB 4806.1 food-contact rules and similar regional standards are positioned to capture rapid outlet growth. In parallel, a young urban demographic with rising disposable income is normalising on-the-go ice-cream consumption, sustaining high reorder volumes for fibre cups.

Digital Short-Run Printing Enabling Artisanal Gelato Brands

Micro-batch gelaterias and direct-to-consumer pint services lean on low-minimum-order digital presses that imprint vibrant graphics on pre-coated board. Variable data capability supports personalised campaigns and geography-specific labelling without surplus inventory, reducing waste while lifting perceived exclusivity. As a result, niche players can command premium shelf pricing despite lower run lengths, expanding the addressable base for mid-range board converters.

Commercialisation of PFAS-Free Water-Based Barrier Technologies

Academic breakthroughs in lignin-particle dispersions, beeswax-in-water systems, and water-dispersible silicone have yielded Cobb60 performance below 3 g/m², rivaling polyethylene while retaining pulping recyclability. Early adopters are recording yield gains in repulping trials above 90%, helping mills hit fibre-recovery targets without expensive de-inking. As detection limits for fluorinated compounds fall and brand-owner pledges tighten, these chemistries are drawing accelerated capital budgets for curtain and blade coaters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile virgin paperboard and pulp prices | -0.9% | Global, pronounced in North America | Short term (≤ 2 years) |

| Persistent price gap versus PET and PP cups | -0.6% | Worldwide, acute in price-sensitive tiers | Long term (≥ 4 years) |

| Limited freezer-grade ink sets for aqueous-barrier substrates | -0.3% | Global premium segments | Medium term (2-4 years) |

| High capex for dispersion-coating retrofits | -0.5% | North America & Europe manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin Paperboard and Pulp Prices

Cost swings in wood fibre erode converter margins and complicate fixed-price customer contracts. Quarterly earnings from vertically integrated producers reveal that average sale prices climbed in 2024, yet shipped tonnes slipped owing to cautious replenishment cycles. Mills reliant on external pulp are more exposed to spot market gyrations, especially when energy costs spike. In response, larger groups deploy multi-mill sourcing pools, energy self-generation, and hedging instruments, mitigating EBITDA compression. Smaller regional cup converters that lack fibre integration must either absorb volatility or pass surcharges downstream, risking share loss to scaled rivals.

Persistent Price Gap Versus PET and PP Cups

Despite regulatory headwinds for plastics, polypropylene and PET remain cheaper on a per-unit basis for many catering-grade formats. Fibre solutions entail higher board grammage, two-stage forming and barrier application, adding labour and asset intensity. Advanced dispersion equipment and in-line dryers amplify capital requirements compared with single-shot injection moulds. While corporate buyers increasingly value recyclability, some high-volume QSR chains in emerging markets still default to plastic when local levies are absent. Closing the cost delta will depend on scale economies, rising landfill tariffs and broader consumer willingness to pay for low-carbon packaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cup Capacity: Mid-Range Volumes Anchor Category Growth

The ice-cream paperboard cups market size for 4-8 oz products reached 460,000 tonnes in 2024, equating to 41.71% of global shipments. These formats accommodate standard single-serve sundaes and soft-serve portions, allowing QSRs to run uniform scooping protocols that curb wastage. Their dominance also stems from tight alignment with automated filling equipment, easing throughput at co-manufacturers. Smaller-than-4-oz samplers retain niche relevance in events and kids’ menus, yet growth is modest because operators favour upselling to mid-range SKUs. Looking ahead, the 8-16 oz bracket is forecast to log a 5.57% CAGR to 2030, the fastest within the hierarchy. This acceleration rests on expanding premium pint sales that demand rigid, condensation-resistant board with high-definition branding. Retail chains increasingly allocate dedicated freezer facings to craft flavours, and e-grocery fulfilment heightens the need for sturdy lids and tamper evidence. At the bulk end, containers above 16 oz appeal to institutional buyers but carry logistics inefficiencies for direct-to-consumer parcels, restraining share growth.

By Coating Type: Incumbent PE Feels the Sustainable Squeeze

Polyethylene accounted for 67.41% of the ice-cream paperboard cups market share in 2024 because it delivers proven moisture barriers at a low incremental cost. Converters also value its wide process tolerance, which simplifies forming and sealing. Nevertheless, legislative deadlines on fluorochemicals have catalysed rapid scaling of water-based dispersions. This alternative is registering a 6.02% CAGR and should erode PE share as line speeds rise and unit costs normalize. Pilot studies show that modern dispersion chemistries achieve repulping yields above 90%, triggering inclusion in curbside recycling streams in several EU states. PLA coatings occupy specialty compostable niches where industrial waste channels are established, though current chill-crack sensitivity curbs broader use. Looking forward, multi-layer polymer-free barrier structures derived from lignin or cellulose promise full fibre recovery without dedicated cup-stock recycling paths, positioning early adopters for compliance with the EU 2030 recyclability mandate.

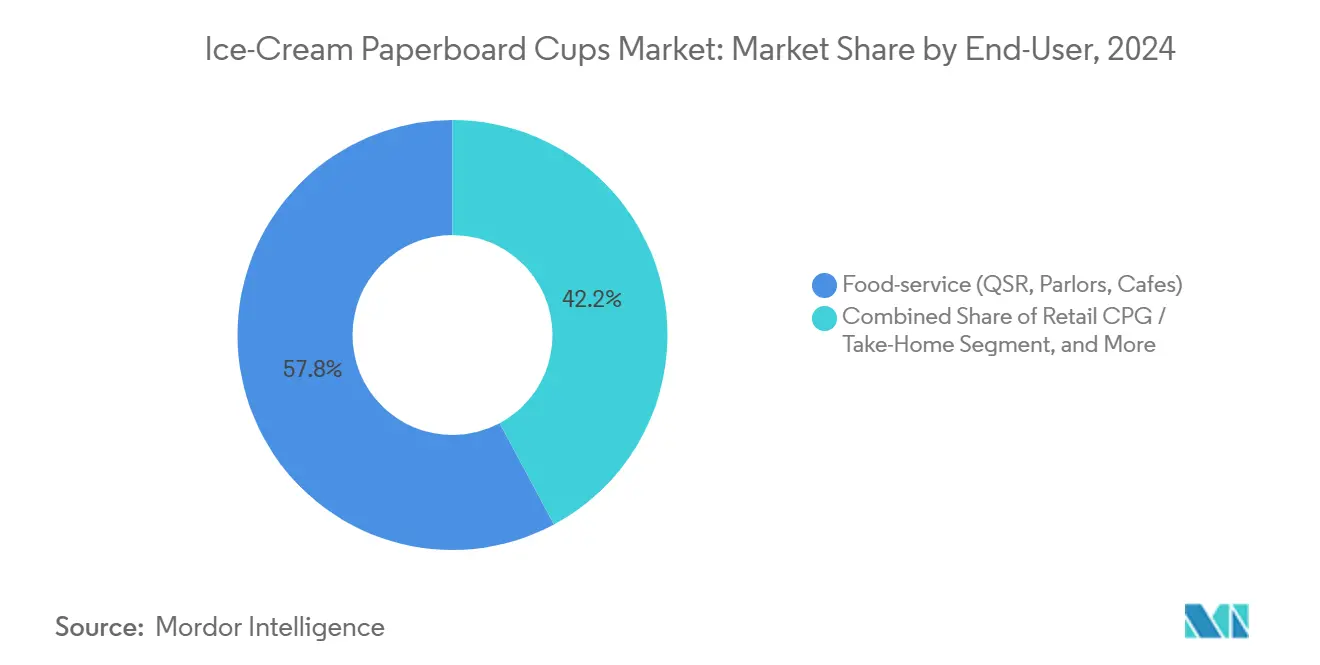

By End-User: Foodservice Dominance Meets Retail Momentum

Foodservice outlets consumed 57.82% of all cup tonnage in 2024, reflecting entrenched QSR dessert menus and convenience-store soft-serve counters. Chain operators value the stackability and controlled portioning that fibre cups offer under rapid-service conditions. Catering functions within airlines and cinemas further expand repeat purchase cycles. Retail take-home channels, however, present the most dynamic incremental volume: a 4.81% CAGR underpinned by home-delivery platforms and growth in better-for-you pint formats. Private-label grocers are refining multi-serve SKUs with laminated spoons under lids, a design only feasible with board rigidity. Institutional buyers, including schools and healthcare facilities, opt for larger tubs to economize scoop labour, though budget constraints modulate uptake. In the same vein, direct-to-consumer gelato startups rely heavily on online gifting, driving small-batch digital print runs that showcase artisanal branding and justify premium price tags.

By Material: Virgin Fiber Holds Dual Leadership

Virgin fibre delivers benchmark stiffness and surface smoothness essential for freezer applications, securing 74.67% volume share in 2024 and the highest projected CAGR at 5.93%. Certifications from sustainable forestry schemes bolster brand narratives, while consistent fibre length reduces crack risk under −20 °C cycles. Momentum toward recycled content is nevertheless building as municipal curbside systems mature. Hybrid boards blending 30-50% post-consumer fibre are entering pilot scale, but technical limitations around odour neutrality and strength currently confine them to limited-life promotions. Mills operating integrated de-inking and bleaching lines possess a margin cushion that helps neutralise virgin-pulp price shocks. Over the forecast period, policy instruments such as differentiated producer-responsibility fees could accelerate the shift toward higher-recycled ratios, yet virgin-grade substrates are expected to dominate premium SKUs that place a premium on optics and machine-side forming efficiency.

Geography Analysis

Asia-Pacific’s ascendance in the ice-cream paperboard cups market is anchored in favourable demographics and a franchise-driven QSR roll-out that demands uniform, freezer-safe fibre packs. The sub-region comprising China, India and Southeast Asia surpassed 550,000 tonnes in 2024 and is forecast to post a 6.47% CAGR, more than 200 basis points above the global average. Multinational converters are therefore localising barrier-coat assets to bypass import tariffs and shorten lead times. Domestic cup makers, meanwhile, secure pulp imports from fast-growing plantation corridors, partially offsetting currency risk.

North America and Europe collectively supply technology templates that underpin global compliance. Brand owners lean heavily on dispersion-coating know-how originating in these mature markets to fulfil upcoming recyclability benchmarks. Here, the ice-cream paperboard cups market size is stable in volume yet tilts toward higher-margin pint and novelty shapes. Premium-label producers favour virgin SBS grades with foil lids, a combination that broadcasts quality on crowded freezer shelves.

Emerging regions, Latin America, the Middle East and Africa are yet to exceed 15% combined share but hold latent demand via rising middle-class segments and warmer climates that support year-round consumption. Packaging players entering these geographies must navigate inconsistent chill-chain infrastructures and disparate recycling guidelines. Low-capital flexo print lines paired with modular forming equipment offer a flexible market-entry path, paving the way for stepwise upgrades once volume thresholds justify dispersion coaters.

Competitive Landscape

The ice-cream paperboard cups market exhibits moderate fragmentation, with roughly the top five converters accounting for an estimated 50–55% of global shipments. Graphic Packaging, Huhtamaki and Pactiv Evergreen anchor the tier-one cohort by virtue of integrated mills, global form-fill competence and multi-substrate portfolios. Graphic Packaging booked USD 8.807 billion in 2024 net sales, reflecting its ability to cross-sell board and converting capacity to both foodservice and retail brands[4]Graphic Packaging Holding Company, “2024 Form 10-K,” investors.graphicpkg.com. Huhtamaki continues to raise dispersion-coating utilisation across European plants while pledging full PFAS phase-out ahead of regulatory deadlines. Pactiv Evergreen has tied executive incentives to achieving 100% sales from recyclable, renewable or recycled materials by 2030, reinforcing its sustainability leadership.

Second-tier competitors often specialise in regional QSR contracts or niche artisan pints. They differentiate through short-run digital printing and quick artwork changeovers. Strategic deals include mill divestitures that swap lower-margin board mills for higher-return converted-product plants, as witnessed when Graphic Packaging exited its Augusta mill to focus on foodservice assets. Private-equity interest is rising in speciality coaters capable of supplying barrier stock to third-party cup formers, signalling consolidation potential.

Innovation races now centre on fluorine-free chemistries and robotics. Early adopters of curtain-coated dispersion lines achieve faster ramp-ups and reduced energy footprints versus classic extruders. Robotics within forming halls cut labour cost and ensure hygiene compliance, a competitive edge in post-pandemic manufacturing audits. Taken together, these moves point toward gradual concentration as capital budgets and compliance costs climb.

Ice-Cream Paperboard Cups Industry Leaders

Huhtamäki Oyj

Dart Container Corporation

Stanpac Inc.

Pactiv Evergreen Inc.

Genpak LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Avient reported 5% organic revenue growth in Q2 2024, citing demand for sustainable colorants used in paperboard lids.

- January 2025: FDA revoked 35 PFAS food-contact authorizations, setting a June 30, 2025, compliance deadline.

- January 2025: EU Regulation 2025/40 entered force, mandating recyclability for all packaging by 2030 with stepped recycled-content quotas.

- May 2024: Graphic Packaging divested its Augusta paperboard facility to sharpen focus on higher-margin foodservice lines.

Global Ice-Cream Paperboard Cups Market Report Scope

| Less than 4 oz |

| 4-8 oz |

| 8-16 oz |

| More than 16 oz |

| Polyethylene (PE) |

| Polylactic Acid (PLA) |

| Aqueous Dispersion |

| Bio-based Polymer-free |

| Food-service (QSR, Parlors, Cafes) |

| Retail CPG / Take-Home |

| Institutional and Catering |

| Virgin Fiber Paperboard |

| Recycled Fiber Paperboard |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Cup Capacity | Less than 4 oz | ||

| 4-8 oz | |||

| 8-16 oz | |||

| More than 16 oz | |||

| By Coating Type | Polyethylene (PE) | ||

| Polylactic Acid (PLA) | |||

| Aqueous Dispersion | |||

| Bio-based Polymer-free | |||

| By End-User | Food-service (QSR, Parlors, Cafes) | ||

| Retail CPG / Take-Home | |||

| Institutional and Catering | |||

| By Material | Virgin Fiber Paperboard | ||

| Recycled Fiber Paperboard | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the ice-cream paperboard cups market in 2025?

The ice-cream paperboard cups market size reached 1.1 million tonnes in 2025 and is projected to climb to 1.4 million tonnes by 2030.

Which cup capacity sells the most?

4-8 oz cups lead global demand, accounting for 41.71% of 2024 shipments.

What drives Asia-Pacific dominance?

Rapid QSR outlet growth, urbanisation and rising disposable incomes lift ice-cream servings, helping Asia-Pacific secure 42.06% share in 2024.

Why are PFAS-free coatings important now?

The FDA and EU have revoked or restricted PFAS food-contact uses, pushing converters toward aqueous dispersion or other fluorine-free barriers ahead of mid-decade deadlines.

Is polyethylene coating being phased out?

PE still holds 67.41% share but faces gradual displacement by water-based dispersions growing at 6.02% CAGR.

Page last updated on: