Liquid Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

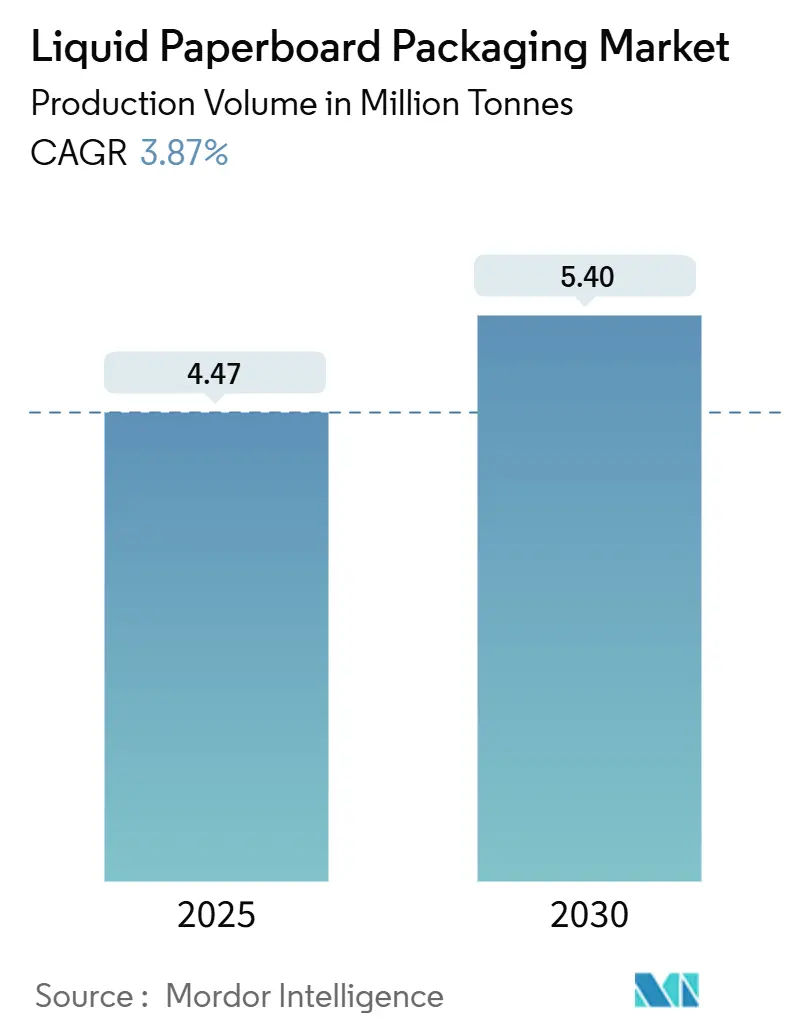

| Market Volume (2025) | 4.47 Million tonnes |

| Market Volume (2030) | 5.40 Million tonnes |

| Growth Rate (2025 - 2030) | 3.87% CAGR |

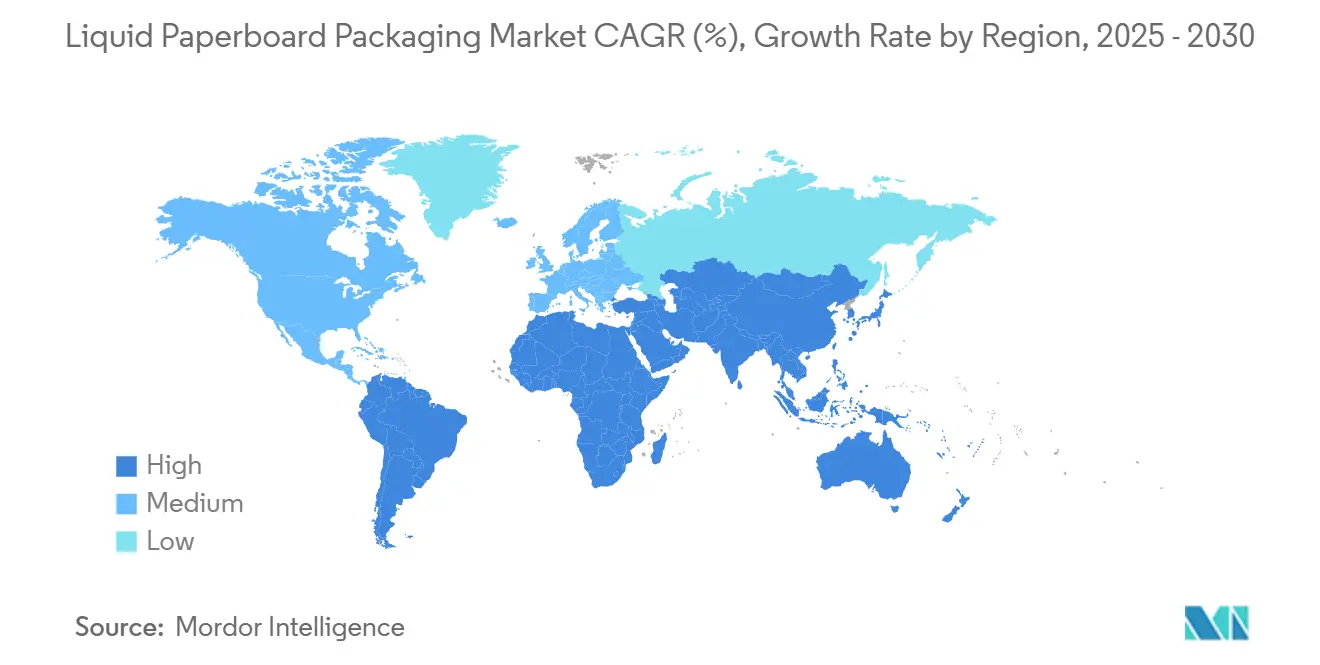

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Paperboard Packaging Market Analysis by Mordor Intelligence

The liquid paperboard packaging market size stood at 4.47 million tonnes in 2025 and is projected to reach 5.40 million tonnes by 2030, translating into a 3.87% CAGR over the forecast period. The trajectory reflects the steady substitution of rigid plastics with fiber-based formats, the growing influence of design-for-recycling rules, and heightened brand investments in carton barrier innovations that lift renewable content without compromising shelf life. Rising online grocery penetration, coupled with the push to decarbonize beverage logistics, is steering volume toward compact, cube-efficient carton formats that fit automated fulfillment systems. At the same time, school milk programs in emerging economies, breakthroughs in bio-based barriers in Europe, and large-scale upstream mill conversions signal that the liquid paperboard packaging market retains ample headroom for both volume-driven and value-driven gains. Competitive intensity remains elevated as three multinational converter groups secure filling-machine placements, creating sizable switching barriers for brand owners. However, mill forward integration and digital printing are opening new paths for differentiation. On balance, the liquid paperboard packaging market is shifting from compliance-led adoption toward performance-led innovation, positioning fiber cartons as a credible mainstream alternative to aluminum foil and multilayer plastic systems.

Key Report Takeaways

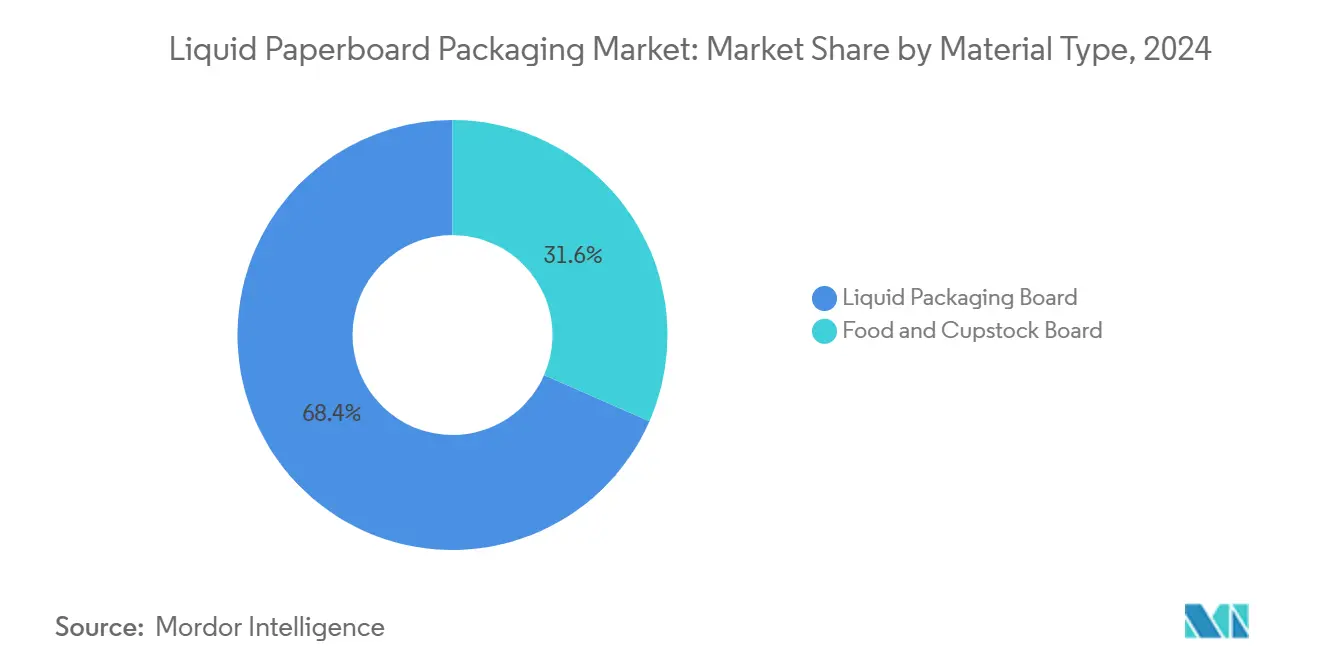

- By material type, liquid packaging board held 68.43% of 2024 volume and is expanding at a 4.64% CAGR through 2030.

- By carton type, gable-top formats led with 61.64% share in 2024, while shaped cartons are projected to grow at 5.35% annually to 2030.

- By shelf life, long shelf-life cartons captured 74.75% of 2024 shipments and are advancing at a 4.87% CAGR.

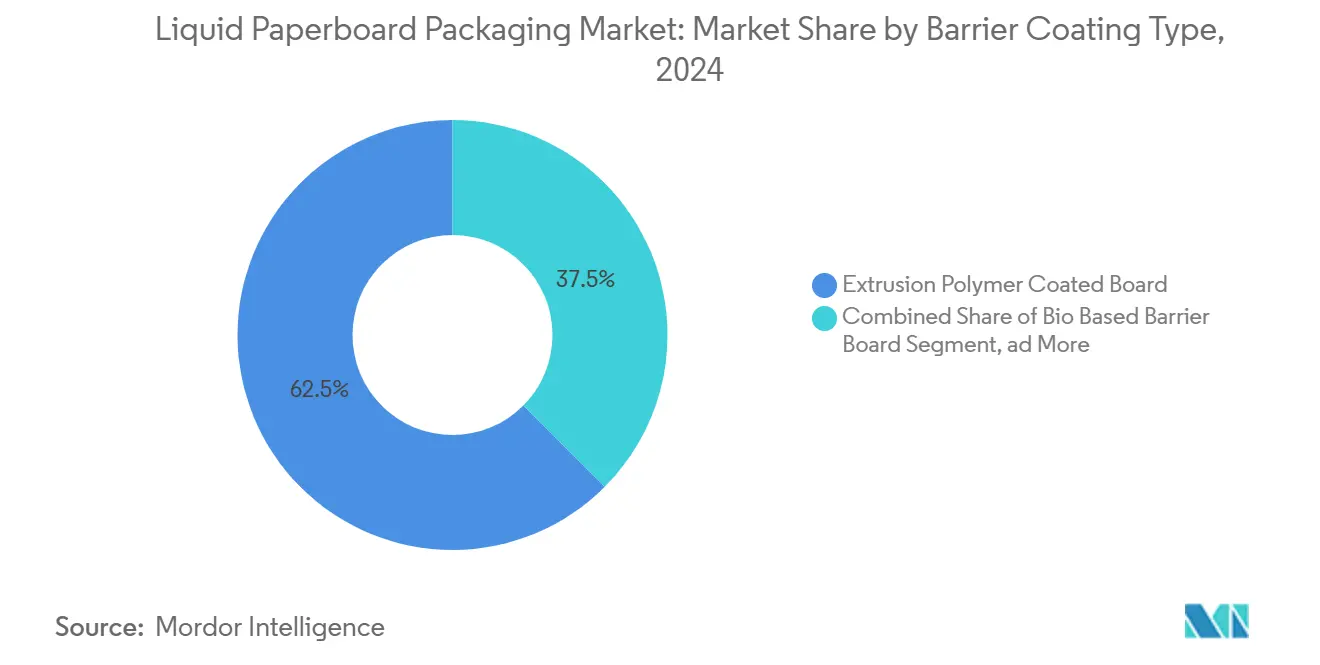

- By barrier coating, extrusion polymer-coated board represented 62.53% of 2024 demand, whereas bio-based barrier board is rising at 5.98% per year.

- By end-use application, beverages held 67.42% of 2024 consumption, but nutraceuticals are pacing the field with a 6.01% CAGR to 2030.

- By geography, Asia-Pacific commanded 40.32% of 2024 volume, while the Middle East and Africa region is set to climb at a 6.21% CAGR.

Global Liquid Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient and shelf-stable beverages | +1.2% | Global with focus on Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Accelerating push toward sustainable and recyclable packaging | +1.5% | Europe and North America lead, Asia-Pacific following | Long term (≥ 4 years) |

| Expansion of aseptic cartons in plant-based dairy alternatives | +0.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Government-funded school milk carton programs | +0.6% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Growth of online grocery boosting on-the-go cartons | +0.7% | Global with high uptake in North America, Europe, China | Short term (≤ 2 years) |

| Digital watermark adoption for closed-loop recycling | +0.4% | Europe and North America pilots, Asia-Pacific scale-up | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient and Shelf-Stable Beverages

Rapid urban expansion and time-pressed lifestyles are driving demand for ambient, ready-to-drink products that eliminate the need for refrigeration until opening. Functional beverages, valued at USD 766.69 billion in 2024, are projected to reach over USD 1 trillion by 2032, growing at a rate of nearly 6% annually. Aseptic cartons align with the trend because they achieve a six-to-twelve-month shelf life without the need for preservatives, thereby lowering cold-chain costs and expanding distribution outlets to convenience stores, gyms, and quick-commerce hubs. The Tetra Recart solution ships 20% more product per pallet than cans and trims freight emissions, illustrating the logistics edge that cartons bring. [1]Tetra Pak, “Paper-Based Barrier Technology,” TETRAPAK.COM Growing protein-shake penetration, USD 21.5 billion retail value in 2024 further aligns with cartons that tolerate high-solid formulations while reinforcing a premium, eco-messaged positioning.

Accelerating Push Toward Sustainable and Recyclable Packaging

Design-for-recycling rules are converging worldwide, pressing brand owners to phase out hard-to-separate multilayer laminates. The European Union now mandates that all beverage cartons placed on the market be fully recyclable by 2030 and achieve collection targets of over 70%. [2]European Parliament, “Packaging and Packaging Waste Regulation,” EUROPARL.EUROPA.EUCarton leaders are responding with fiber-rich structures that swap aluminum foil for paper-based oxygen barriers. Tetra Pak’s new barrier raises renewable content to 80% and cuts carbon emissions by one-third compared with legacy laminates. Converters are also adopting Forest Stewardship Council-certified pulp as a base expectation, with over 90% of global carton capacity now backed by traceable fiber.[3]Forest Stewardship Council, “FSC Certification Standards,” FSC.ORG Bio-derived dispersion coatings from Billerud, Stora Enso, and Sappi are helping cartons transition toward a mono-material status, enabling them to enter mainstream paper-recycling streams.

Expansion of Aseptic Cartons in Plant-Based Dairy Alternatives

Plant-based milk brands are transitioning from chilled PET to ambient cartons to expand their reach and reduce retail energy consumption. Elopak’s Pure-Pak adoption by Dutch cooperative Boermarke extends shelf life to nine months and raises renewable content to 75%. Australian player Milkadamia exported macadamia milk across Asia in Tetra Prisma Aseptic cartons that do not rely on continuous cold storage. Nut and grain beverages benefit most because ultra-high-temperature treatment neutralizes enzymes that cause off-flavors, while the carton's surface area provides a canvas for high-resolution graphics that underscore environmental claims. The shift is reinforcing volume growth in the liquid paperboard packaging market as dairy alternatives enter price parity with traditional milk.

Government-Funded School Milk Carton Programs

Public nutrition schemes continue to distribute billions of single-serve cartons to schoolchildren, underpinning baseline demand in emerging nations. Tetra Pak reported supplying 9.2 billion packages to 64 million children across 49 countries in 2024. Programs in the Philippines and Uganda, for example, provided 1.837 million and 50,000 beneficiaries respectively, highlighting the inclusive reach of aseptic cartons. Similar initiatives in India and Bangladesh link nutrition goals with dairy market stimulation, securing long-term volume commitments for local processors and converters. As health ministries integrate fortified milk into curricula, carton manufacturers gain predictable base-load volume, buffering against short-term retail swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competitive pressure from flexible pouches and PET bottles | -0.9% | Global, highest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Raw material price volatility for pulp and polymers | -0.7% | Global with focus on Europe and North America | Medium term (2-4 years) |

| Insufficient poly-aluminum recycling infrastructure | -0.4% | Asia-Pacific, Middle East and Africa, Latin America | Long term (≥ 4 years) |

| Regulatory shift away from aluminum-foil layers raising costs | -0.3% | Europe and North America, Asia-Pacific spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competitive Pressure from Flexible Pouches and PET Bottles

Flexible pouches and PET bottles account for roughly 40% of beverage-packaging volume and are expanding share through lower unit costs and established deposit-return networks. Pouches are growing at 5.8% annually, promoting spouted formats that resonate with parents of young children and rural consumers. PET enjoys collection rates of 80% or more in jurisdictions such as Germany, while carton recycling remains below 50% in many regions due to composite layers that hinder fiber recovery. Carton makers respond with aluminum-free barriers and bottle-shaped formats, but these carry cost premiums that still confine uptake to premium SKUs.

Raw Material Price Volatility for Pulp and Polymers

Northern bleached softwood kraft pulp swung from USD 1,400 per ton in early 2024 to USD 1,100 per ton by the third quarter, squeezing converters bound by fixed-price contracts. Polyethylene resin, which can account for up to one-quarter of the carton weight, is sensitive to oil and gas price fluctuations, adding further unpredictability. Although Stora Enso’s EUR 1 billion (USD 1.13 billion) Oulu line adds 750,000 tons of board capacity per year, the asset will not reach full run-rate before 2027, leaving a near-term supply gap that may push prices higher. Vertically integrated players with captive pulp enjoy a buffer, while smaller converters face working-capital stress during spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Liquid Packaging Board Captures Core Aseptic Volume

The liquid paperboard packaging market size for liquid packaging board stood at 3.02 million tons in 2024, equal to 68.43% of total volume, and this substrate is projected to expand at a 4.64% CAGR through 2030. Superior stiffness, low-taint bleaching, and dual polyethylene coatings enable ultra-high-temperature filling lines to deliver dairy, juice, and plant-based drinks with six-to-twelve-month shelf life. Stora Enso’s digitally optimized Oulu line illustrates the capital flow chasing this demand, integrating real-time fiber-orientation controls that lift yield per ton of pulp.

In parallel, food and cupstock board services fresh milk and ice-cream applications that rely on refrigeration, but its slower growth highlights the defensive nature of short-life formats in the liquid paperboard packaging market. Brand owners are experimenting with tactile varnishes and holographic foils to premiumize dairy desserts, yet these finishes cannot offset the structural pull toward ambient-stable cartons. The emergence of water-based dispersion coatings such as Billerud’s FibreForm signals the next wave, improving repulpability and opening the door for mono-material claims without sacrificing oxygen barrier performance.

By Carton Type: Shaped Cartons Accelerate Branding Differentiation

In 2024, gable-top cartons controlled 61.64% of the liquid paperboard packaging market share for carton formats, reflecting installed high-speed machines that can output 12,000 units per hour. Shaped cartons, however, are the fastest-growing style at 5.35% CAGR, underlining a shift toward attention-grabbing silhouettes that communicate premium cues on crowded shelves. The Pure-Pak Sense design introduces a contoured waist and easy-grip panel that elevates consumer ergonomics while lifting perceived value.

Brick cartons remain critical for aseptic milk and juice where pallet efficiency rules, yet regulatory pressure to remove foil layers is gradually narrowing their cost advantage. Tooling for shaped molds costs three to six times more than standard dies, but elasticity in plant-based beverage pricing supports the economics. Digital printing advances allow small-batch runs with near-offset quality, enabling regional brands to justify shaped-carton investment without risking obsolete inventory, bolstering segment momentum within the liquid paperboard packaging market.

By Shelf Life: Long-Life Formats Dominate Ambient Distribution

Long-shelf-life cartons represented 74.75% of shipments in 2024 and are projected to grow at a 4.87% CAGR to 2030, driven by the demand for ready-to-drink protein shakes and plant-based dairy alternatives that can be shipped globally without refrigeration. Aseptic machines sterilize both the product and the package, reducing logistics costs and carbon footprint in lanes that lack reliable cold chains. Short-life cartons retain relevance in European fresh-milk channels, but contraction of 1-2% a year suggests a gradual pivot to ambient in mature markets.

The liquid paperboard packaging market benefits from the wider retail footprint that long-life formats unlock, especially in e-commerce, where heat-mapped fulfillment centers prize packages that are tolerant of ambient temperature swings. Case studies, such as Milkadamia’s macadamia milk, which is shipped from Australia to Japan with nine-month stability, prove that long-life cartons unlock export revenue streams for mid-scale brands that could not otherwise manage dual inventory.

By Barrier Coating Type: Bio-Based Solutions Gain Traction

Extrusion polymer-coated board still accounts for 62.53% of the barrier-coating volume in the liquid paperboard packaging market, maintaining its lead due to its known runnability and reliable oxygen barrier properties. Nevertheless, bio-based barrier board is expanding at a rate of 5.98% annually as converters align with design-for-recycling mandates and brand promises regarding fossil-free content. Dispersion coatings reduce energy use by up to 40% compared to extrusion, while innovations such as Stora Enso’s CKB bio-polymer achieve oxygen transmission rates below 8 cc/m²/day, which is sufficient for six-month juice stability.

Dispersion solutions are achieving early wins in fresh-milk lines, where barrier demands are lower and recycling simplicity is paramount. Cost remains a hurdle, but European extended producer-responsibility fees that penalize non-recyclable structures are beginning to tip the total delivered cost in favor of bio-derived coatings, broadening addressability in the liquid paperboard packaging market.

By End-Use Application: Nutraceuticals Leap Ahead

Beverages accounted for 67.42% of end-use demand in 2024, but nutraceuticals represented the fastest-growing application, with a 6.01% CAGR, mirroring global trends in protein, collagen, and vitamin-fortified drinks. Cartons accommodate high-protein formulations that may denature in hot-fill PET, while also providing a renewable narrative that resonates with health-conscious consumers. Tetra Recart’s retortability and stackability demonstrate clear freight benefits, a 35% lower carbon footprint compared to stand-up pouches, and support cross-border shipments where shelf life must span multiple weeks.

Food staples such as soups and sauces also migrate into cartons to capitalize on warehouse-club and e-commerce channels that reward cube efficiency. Home-care liquids remain niche but are gathering interest as retailers pilot refill-and-return models, suggesting future optionality for the liquid paperboard packaging industry as it looks to diversify end-use risk.

Geography Analysis

The Asia-Pacific region maintained a 40.32% share of the 2024 volume in the liquid paperboard packaging market, underpinned by large school milk schemes in China, India, and Japan that collectively consume billions of single-serve cartons each year. Rising upper-middle-class consumption in Chinese tier-two cities, coupled with the adoption of dairy alternatives among lactose-intolerant adults, is driving structural growth. India’s PM POSHAN initiative supplied 100,000 children in Chandigarh alone with 130 milliliters of aseptic packs during 2024, exemplifying the role of public procurement in securing a base load for local converters.

Europe and North America remain innovation test beds even as volume growth slows to the low single digits. The European Union’s recyclability directive requires converters to accelerate the development of aluminum-free barriers and invest in digital watermark trials that promise high-precision sorting. In North America, the closure of a Canadian board mill in 2026 is expected to remove approximately 30% of domestic folding-carton capacity, likely increasing import reliance and amplifying price sensitivity for regional fillers. E-commerce grocery, forecast to hit 40% of chain retail by 2026, is reshaping carton dimensions toward slimmer footprints that optimize shipping cube.

The Middle East and Africa is the fastest-growing zone at 6.21% CAGR, powered by higher disposable income in Gulf states and government-backed nutrition drives in Kenya, Nigeria, and South Africa. Pilot recovery programs, such as Nestlé’s MILO CARETON in Thailand which collected 89 tons of cartons via watermark-enabled vending units provide blueprints for African cities seeking scalable recycling without heavy capital layouts. Latin America shows parallel momentum as public-sector milk contracts converge with private-label juice growth, rounding out the global expansion story for the liquid paperboard packaging market.

Competitive Landscape

The liquid paperboard packaging industry displays moderately fragmentation. Tetra Pak, SIG Combibloc, and Elopak dominate filling-machine installations, creating proprietary ecosystems that tie consumable sales to equipment leases. Switching a single aseptic line can cost upward of USD 5 million, reinforcing vendor lock-in and underpinning pricing power. Mill groups, such as Stora Enso, are moving downstream, as evidenced by the EUR 1 billion Oulu conversion, which integrates digital twin controls and pursues co-branded environmental narratives.

Consolidation among box plants is also reshaping buyer power. The July 2024 merger of Smurfit Kappa and WestRock formed a USD 31 billion revenue giant spanning 62 mills and more than 500 converting sites, unlocking USD 400 million in synergy potential and a global procurement scale previously unmatched in fiber packaging. Smaller converters are differentiating through shaped-carton capability, digital printing, and aluminum-free barriers, creating niches where agile capex and faster product-launch cycles counterbalance incumbent scale.

Technology disruptors advance closed-loop goals. Digital watermarks, orchestrated by the HolyGrail 2.0 project, prove nearly perfect identification of multilayer cartons on sortation belts, foreshadowing region-wide rollouts that could lift carton recycling rates above 70%. On a parallel track, lab studies show solvent-based fiber-polymer separation processes achieving full material recovery, which, if commercialized, would erode the principal recycling critique levied against composite cartons. Collectively, these innovations sustain competitive churn and reinforce the forward momentum of the liquid paperboard packaging market.

Liquid Paperboard Packaging Industry Leaders

Tetra Pak International S.A.

International Paper Company

Amcor plc

Smurfit WestRock

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Stora Enso began production at its EUR 1 billion (USD 1.13 billion) Oulu consumer-board line in Finland, adding 750,000 tons of annual liquid packaging board capacity, with full run-rate targeted for 2027.

- October 2024: Elopak rolled out Pure-Pak eSense, a gable-top carton featuring embedded NFC and QR codes for real-time consumer engagement.

- September 2024: Tetra Pak debuted Tetra Evero Aseptic, a shaped carton that removes aluminum foil and trims material use by 10% versus standard bricks.

- August 2024: Billerud secured EN 13432 certification for its FibreForm water-based barrier, enabling industrial compostability within 12 weeks.

Global Liquid Paperboard Packaging Market Report Scope

The Liquid Paperboard Packaging Market encompasses the production and utilization of paperboard materials specifically designed for liquid packaging applications. These materials are engineered to provide durability, barrier protection, and sustainability, catering to industries such as beverages, food, nutraceuticals, and personal care.

The Liquid Paperboard Packaging Market Report is Segmented by Material Type (Liquid Packaging Board, Food and Cupstock Board), Carton Type (Gable Top Cartons, Brick Cartons, Shaped Cartons), Shelf Life (Long Shelf Life Cartons, Short Shelf Life Cartons), Barrier Coating Type (Extrusion Polymer Coated Board, Dispersion Coated Board, Bio Based Barrier Board), End Use Application (Beverage, Food, Nutraceuticals, Homecare and Personal Care, Other End Use Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Million Tonnes).

| Liquid Packaging Board |

| Food and Cupstock Board |

| Gable Top Cartons |

| Brick Cartons |

| Shaped Cartons |

| Long Shelf Life Cartons |

| Short Shelf Life Cartons |

| Extrusion Polymer Coated Board |

| Dispersion Coated Board |

| Bio Based Barrier Board |

| Beverage |

| Food |

| Nutraceuticals |

| Homecare and Personal Care |

| Other End Use Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Liquid Packaging Board | ||

| Food and Cupstock Board | |||

| By Carton Type | Gable Top Cartons | ||

| Brick Cartons | |||

| Shaped Cartons | |||

| By Shelf Life | Long Shelf Life Cartons | ||

| Short Shelf Life Cartons | |||

| By Barrier Coating Type | Extrusion Polymer Coated Board | ||

| Dispersion Coated Board | |||

| Bio Based Barrier Board | |||

| By End Use Application | Beverage | ||

| Food | |||

| Nutraceuticals | |||

| Homecare and Personal Care | |||

| Other End Use Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected 2030 volume for liquid paperboard cartons?

The liquid paperboard packaging market is expected to reach 5.40 million tons by 2030, growing at a 3.87% CAGR from 2025.

Which carton type is growing fastest?

Shaped cartons are advancing at a 5.35% CAGR as brand owners seek differentiated silhouettes for premium beverages.

Why are bio-based barriers gaining traction in beverage cartons?

They eliminate aluminum foil and cut polyethylene use, enabling cartons to meet European recyclability mandates while reducing carbon footprints.

Which region leads carton demand today?

Asia-Pacific holds just over 40% of global volume, driven by large dairy consumption and school milk programs.

How do cartons compare to cans and glass in logistics efficiency?

Aseptic cartons such as Tetra Recart ship 20% more product per pallet than cans and 50% more than glass, reducing freight costs and emissions.

What drives nutraceutical adoption of cartons?

High-protein and fortified drinks favor cartons for ambient distribution, lower carbon profiles, and a premium, eco-centric brand image.

Page last updated on: