Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 14.51 Billion |

| Market Size (2031) | USD 18.48 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canned Fruits Market Analysis by Mordor Intelligence

The canned fruits market size was valued at USD 13.82 billion in 2025, reached USD 14.51 billion in 2026, and is projected to grow to USD 18.48 billion by 2031, registering a compound annual growth rate (CAGR) of 4.95% during 2026–2031. This growth is primarily driven by increasing demand for convenient, shelf-stable, and ready-to-eat fruit options that cater to fast-paced urban lifestyles and rising health consciousness. Canned fruits offer year-round availability, extended shelf life, and minimal preparation, providing a practical alternative to fresh produce for consumers seeking to incorporate fruits into their daily diets. Additionally, the growing focus on fruit-based nutrition, plant-forward eating habits, and balanced diets enhances the relevance of canned fruits across various age groups.

Key Report Takeaways

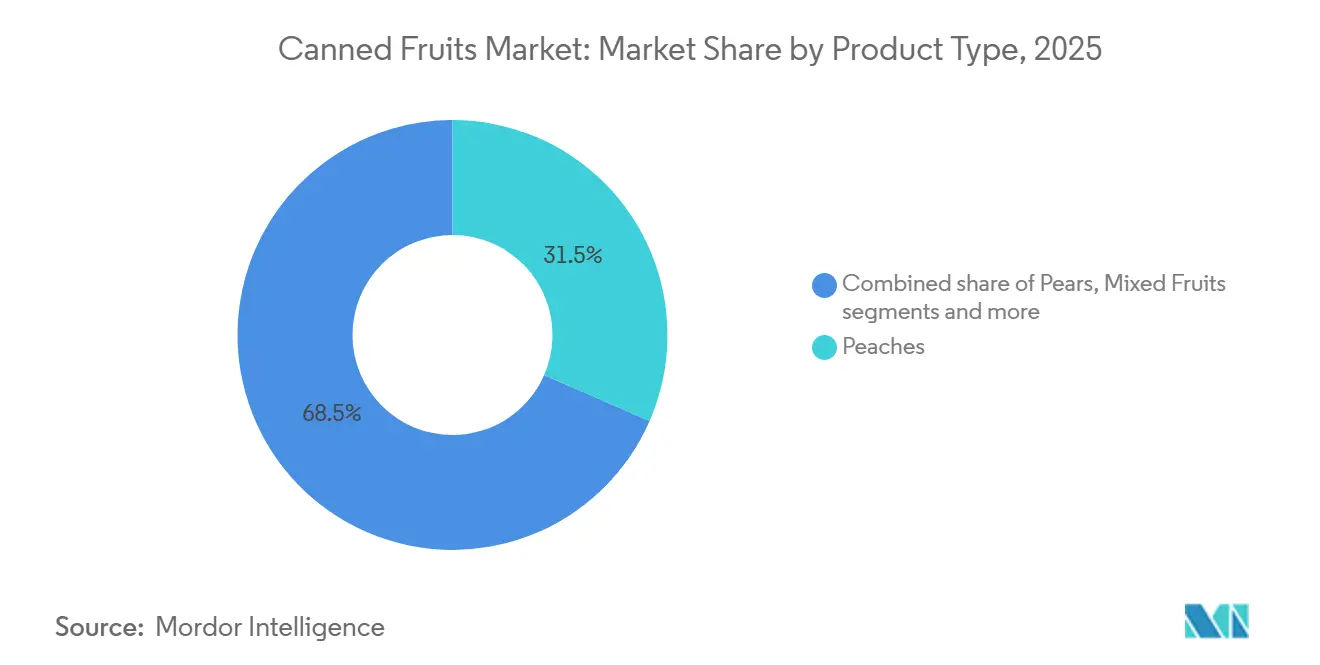

- By product type, peaches led with 31.54% of 2025 revenue, whereas mandarin oranges are projected to expand at a 6.21% CAGR to 2031, the fastest across all fruit categories.

- By form, whole fruits commanded 46.65% of 2025 sales, while cut-fruit formats are forecast to grow at a 5.49% CAGR through 2031 on the back of food-service demand for portion-controlled inputs.

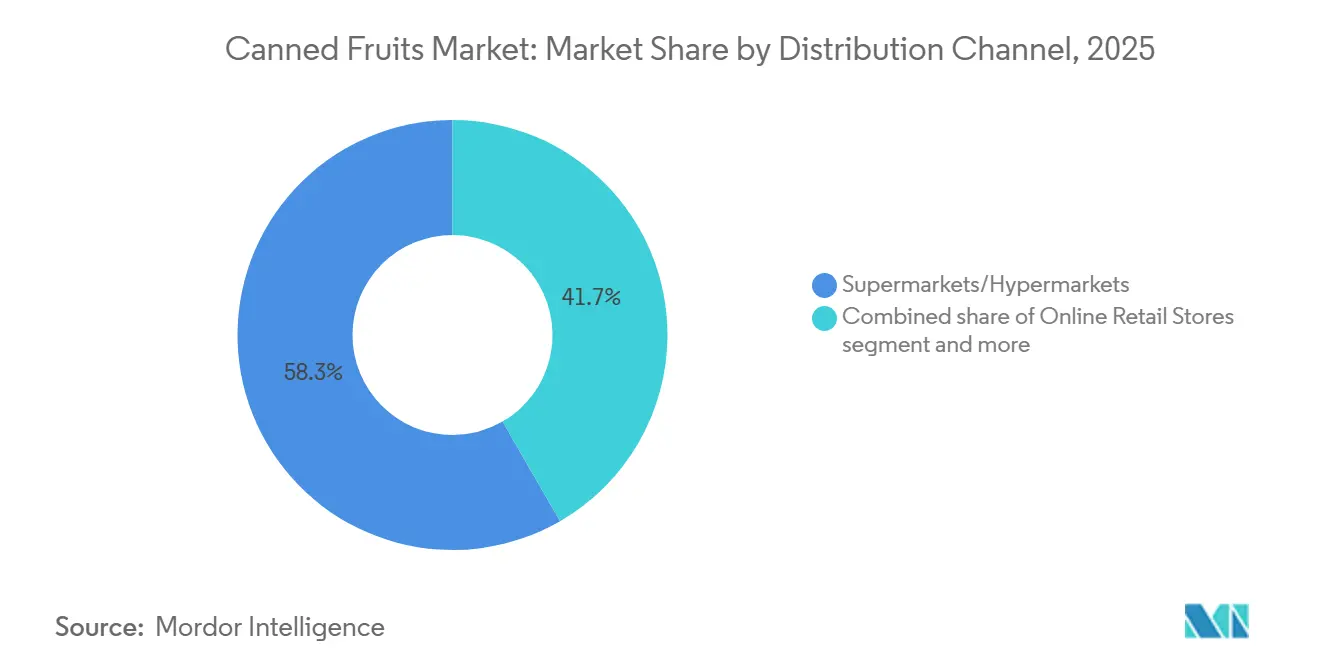

- By distribution channel, supermarkets and hypermarkets captured 58.34% of 2025 sales, yet online retail is set to rise at a 6.67% CAGR as pantry-loading and subscription models take hold.

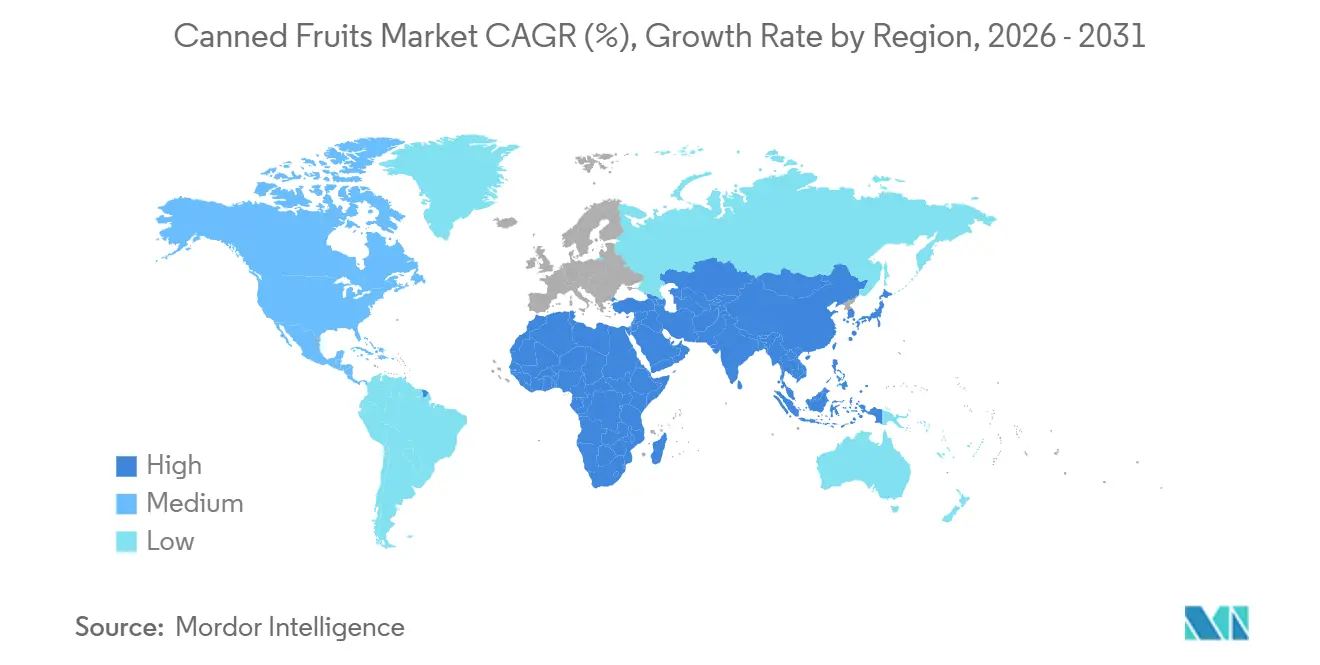

- By geography, North America accounted for 32.43% of 2025 demand, but the Middle East and Africa region is expected to post the fastest growth at a 5.56% CAGR through 2031, fueled by retail modernization initiatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Canned Fruits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising focus on fruit-based diets for nutrition drives consumption | +0.8% | Global, with pronounced uptake in North America and Europe | Medium term (2-4 years) |

| Busy urban lifestyles boost the need for ready-to-eat fruit | +1.2% | Asia-Pacific urban centers, North America metro areas | Short term (≤ 2 years) |

| Growing preference for organic and preservative-free options | +0.9% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Growing fitness culture among younger demographics | +0.7% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Sustainability and waste-reduction positioning | +0.6% | Europe, North America, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Increasing adoption in breakfast formats | +0.5% | North America, Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising focus on fruit-based diets for nutrition drives consumption

The increasing global focus on fruit-based diets as part of balanced and preventive nutrition is driving the growth of the canned fruits market. Rising awareness of the health benefits of fruits, including their natural fiber, antioxidants, vitamins, and hydration properties, has encouraged consumers to incorporate fruits more regularly into their daily diets. As dietary guidelines and wellness trends advocate for higher fruit consumption to support digestive health, immunity, and overall well-being, canned fruits offer a convenient, year-round alternative to fresh produce. Their extended shelf life, ready-to-eat format, and availability in juice or no-added-sugar options make them a practical choice for consumers aiming to meet recommended fruit intake levels. Additionally, the growing popularity of plant-forward diets and clean-label preferences continues to drive demand for shelf-stable fruit products.

Busy urban lifestyles boost the need for ready-to-eat fruit

Rapid urbanization and increasingly busy lifestyles are driving the demand for convenient, ready-to-eat fruit options. As working professionals, dual-income households, and students face tighter schedules, the need for time-saving food solutions has grown. Canned fruits address this demand by eliminating the need for washing, peeling, and cutting, while also reducing spoilage concerns. They offer the convenience of immediate consumption without compromising nutritional value. This trend is particularly prominent in highly urbanized regions. For example, the United Nations Economic and Social Commission for Asia and the Pacific reports that the Asia-Pacific region is home to over 2.2 billion urban residents, making it the most populous urban area globally. Furthermore, the region's urban population is projected to grow by 50% by 2050 [1]Source: United Nations Economic and Social Commission for Asia and the Pacific, "Urban-transformation-asia-and-pacific-growth-resilience", unescap.org. This rapid urbanization is influencing food consumption patterns, increasing the preference for shelf-stable, easy-to-store, and ready-to-eat products.

Growing preference for organic and preservative-free options

The growing consumer preference for organic and preservative-free food products is driving significant market growth. Increased awareness of clean-label ingredients, chemical-free farming practices, and minimally processed food options has led consumers to opt for organic canned fruit products that align with health-conscious and environmentally sustainable lifestyles. In response, manufacturers are broadening their certified organic product portfolios, removing artificial preservatives, and prioritizing transparent sourcing practices. This trend is particularly evident in developed markets. According to the Organic Trade Association, organic food sales in the United States reached USD 71.6 billion in 2024, demonstrating continued consumer commitment to organic products [2]Source: Organic Trade Association, "Growth of U.S. Organic Marketplace Accelerated in 2024", ota.com. As the demand for natural and traceable food products grows, organic and preservative-free canned fruit offerings are expected to gain more shelf space and premium positioning, contributing to the overall growth of the market value.

Growing fitness culture among younger demographics

The growing fitness culture among younger demographics is driving demand as health-conscious consumers emphasize balanced nutrition and natural energy sources. Millennials and Gen Z are increasingly adopting active lifestyles, including gym memberships, home workouts, and sports participation, which has heightened interest in nutrient-rich, plant-based food options. Fruits are widely valued for their natural sugars that provide quick energy, dietary fiber that aids digestion, and essential vitamins that support recovery and overall wellness. Canned fruits, especially those without added sugar, offer a convenient and shelf-stable option suitable for pre-workout snacks, post-workout smoothies, yogurt bowls, and calorie-controlled meal plans. Furthermore, portion-controlled packaging supports fitness goals such as calorie monitoring and macronutrient tracking. As younger consumers continue to combine nutrition awareness with active lifestyles, the fitness culture is anticipated to drive consistent growth in the canned fruits market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar and syrup-related health concerns | -0.9% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) |

| Growing preference for minimally processed foods | -0.7% | North America, Europe, Australia | Medium term (2-4 years) |

| Competition from frozen and aseptic fruit formats | -0.6% | North America, Europe, with spillover to Asia-Pacific urban centers | Medium term (2-4 years) |

| Logistics weight and space inefficiency | -0.4% | Global, particularly affecting e-commerce and last-mile delivery operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High sugar and syrup-related health concerns

Health concerns related to high sugar intake are a significant restraint on the global canned fruits market, particularly for products packed in heavy or light syrup. Many traditional canned fruit products include added sugars to enhance flavor and preservation, which conflicts with the growing consumer preference for low-sugar and clean-label foods. Rising awareness of obesity, diabetes, and metabolic health risks has led consumers to be more cautious about products high in free sugars. For example, the World Health Organization recommends limiting free sugar consumption to less than 10% of total daily energy intake, supporting global public health efforts to reduce sugar consumption. Consequently, consumers are increasingly opting for fruit packed in natural juice, no-added-sugar formulations, or fresh alternatives. This focus on sugar content pressures manufacturers to reformulate products and may limit the growth potential of traditional syrup-based canned fruits, thereby restraining overall market growth.

Growing preference for minimally processed foods

The growing consumer preference for minimally processed and fresh-like food options poses a significant challenge for the canned fruits market. Contemporary dietary trends prioritize natural texture, nutrient retention, and limited thermal processing, leading to a perception that canned fruits are more processed compared to fresh or frozen alternatives. Increased awareness of ingredient transparency, processing techniques, and clean-label claims has further amplified skepticism toward heat-treated and shelf-stable products. As plant-based and whole-food dietary patterns continue to gain popularity, consumers increasingly favor products that undergo minimal processing. This perception issue may reduce the appeal of canned fruits, particularly among younger and health-conscious consumers who associate minimal processing with greater nutritional value and authenticity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mandarin Oranges Outpace Traditional Leaders

Peaches, accounting for 31.54% of the Global Canned Fruits Market revenue in 2025, play a significant role in driving market growth due to their strong cross-channel demand, versatile applications, and broad consumer acceptance across age groups. Canned peaches provide an optimal balance of sweetness, texture retention after thermal processing, and visual appeal, making them one of the most commercially viable fruits for canning compared to softer or highly seasonal alternatives. Additionally, peaches align well with product innovation trends such as no-added-sugar formulations, juice-packed variants, diced and sliced convenience formats, and portion-controlled cups. These innovations enable manufacturers to cater to health-conscious consumers without compromising on taste. The fruit’s compatibility with premium positioning, including organic offerings and clean-label packaging, further supports value growth within this segment.

Mandarin oranges, projected to grow at a CAGR of 6.21% through 2031, are emerging as one of the fastest-growing segments within the Global Canned Fruits Market, contributing significantly to incremental revenue growth and category diversification. Their naturally sweet flavor, bright color, seedless convenience, and easy-to-separate segments make them highly appealing across children, family, and institutional consumption segments. Mandarin oranges maintain strong structural integrity and visual appeal after canning, making them ideal for applications such as fruit salads, dessert cups, yogurt toppings, bakery products, and ready-to-eat snack packs. Additionally, mandarins are widely cultivated and well-suited for large-scale processing, supporting export-oriented production hubs and private-label expansion.

By Form: Cut Fruits Dominate Ready-to-Eat Convenience

Whole fruits are expected to account for 46.65% of the Global Canned Fruits Market revenue in 2025, maintaining a dominant position due to their strong association with quality, naturalness, and premium appeal. Consumers often perceive whole canned fruits as minimally processed, offering better texture retention than sliced or diced alternatives, thereby enhancing purchase confidence. These products are commonly available in juice or light-syrup variants, aligning with the growing demand for cleaner labels and reduced-sugar options. Furthermore, their ability to endure thermal processing without significant shape degradation improves shelf presentation and perceived value, supporting premium and mid-tier pricing strategies. The combination of these factors positions whole fruits as a cornerstone of the canned fruits market, appealing to health-conscious consumers and premium product seekers alike.

Cut fruits are projected to grow at a CAGR of 5.49% through 2031, emerging as a key growth driver in the Global Canned Fruits Market. This growth is primarily attributed to their convenience, portion control, and versatility in various applications. Pre-sliced, diced, chunked, or segmented formats eliminate preparation time, making them highly appealing to busy households, quick-service restaurants, bakeries, and institutional kitchens. Their ready-to-use nature meets the increasing demand for breakfast bowls, desserts, smoothies, fruit salads, and dairy inclusions, where uniform size and consistent texture are essential for presentation and operational efficiency. The adaptability of cut fruits to diverse culinary uses and their alignment with modern consumer lifestyles further solidify their role as a significant contributor to market expansion.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets, projected to account for 58.34% of canned fruits market sales in 2025, serve as a key driver of growth for the category. These large-format retail outlets offer a wide product assortment, strong private-label presence, and attract high consumer footfall. Their extensive shelf space allows brands to showcase various fruit types, packing mediums, pack sizes, and price tiers in one location, enhancing cross-category visibility and encouraging impulse purchases. Structured merchandising, promotional campaigns, and bundle offers significantly boost volume sales, particularly during festive seasons and periods of heightened demand. Additionally, supermarkets and hypermarkets support premiumization by featuring dedicated sections for organic, clean-label, and no-added-sugar products, enabling manufacturers to introduce value-added variants with improved shelf positioning.

Online retail channels, expected to grow at a CAGR of 6.67% through 2031, are emerging as one of the fastest-growing distribution platforms in the canned fruits market. This growth is driven by increasing adoption of digital grocery shopping and evolving consumer purchasing behaviors. The ability to compare nutritional labels, sugar content, brand positioning, and pricing in real time enhances transparency and supports informed decision-making, particularly among health-conscious consumers. Subscription models and bulk purchasing options further promote repeat purchases of pantry staples like canned fruits. Additionally, promotional discounts, personalized recommendations, and bundled offers contribute to larger basket sizes and increased cross-category sales.

Geography Analysis

North America accounted for 32.43% of the canned fruits market revenue in 2025, supported by the United States' highly developed and mature retail infrastructure, strong private-label penetration, and established household consumption patterns. The region benefits from robust domestic fruit production and processing capabilities, particularly in peaches and pears. For instance, according to the United States Department of Agriculture, total peach production in the United States reached 709,200 tons in 2024, representing a 20% increase compared to the previous year, ensuring stable raw material availability for canning operations [3]Source: United States Department of Agriculture (USDA), "Production volume of peach in the United States", usda.gov. The presence of advanced food processing technologies, strong distribution networks, and high consumer familiarity with shelf-stable fruit products further anchors the region’s dominance.

The Middle East and Africa are forecast to grow at a CAGR of 5.56% through 2031, driven by expanding urban retail infrastructure, rising adoption of packaged and shelf-stable food products, and increasing product availability through import channels. Growing awareness of food safety, longer shelf life, and year-round fruit access is gradually enhancing market penetration across metropolitan areas in this region. Europe represents another major regional contributor, supported by established fruit-processing traditions and structured retail networks across Germany, the United Kingdom, Italy, France, and Spain. The region’s demand is reinforced by a strong preference for clean-label, organic, and reduced-sugar canned fruit variants, alongside steady consumption in household and retail channels.

Asia-Pacific is projected to record steady growth, supported by rising urbanization, modernization of grocery retail, and evolving dietary patterns. Key markets such as China, India, Japan, and Australia are driving demand due to increasing consumption of bakery products, dairy desserts, and ready-to-eat meal components that incorporate canned fruits. Improvements in domestic fruit processing capacity, combined with strong export potential from regional production hubs, are expected to further accelerate growth. As modern retail penetration expands and consumers seek convenient, long-lasting fruit options, Asia-Pacific remains a significant contributor to incremental global revenue growth in the canned fruits market.

Competitive Landscape

The canned fruits market demonstrates moderate concentration, characterized by competition among multinational corporations and strong regional processors across various price tiers and product formats. Prominent players such as Dole plc, The Kraft Heinz Company, Del Monte Foods, Inc., Rhodes Food Group, and Seneca Foods Corporation maintain significant global and regional presence. This is achieved through vertically integrated sourcing, large-scale processing capabilities, and diversified distribution networks. These companies capitalize on brand recognition, established retailer relationships, and private-label collaborations to sustain their market position. Competitive strategies primarily focus on portfolio diversification, sugar-reduction reformulations, organic product offerings, and expansion into emerging markets to meet growing demand.

White-space opportunities are increasingly influencing strategic decisions within the market. Emerging segments such as protein-enriched fruit blends, fortified variants, and functional products are creating new value-added opportunities beyond traditional syrup-packed formats. Additionally, single-serve pouches and portion-controlled packaging designed for on-the-go consumption offer significant growth potential, particularly among younger and urban consumers seeking convenience. Premiumization efforts, including clean-label claims, exotic fruit combinations, and sustainable sourcing certifications, enable brands to differentiate themselves in a category often viewed as commoditized. These innovation-driven strategies are expected to heighten competition while broadening the market's appeal.

Technology adoption is advancing rapidly across processing and packaging operations, enhancing efficiency and sustainability. Investments in retort-pouch lines and advanced thermal processing technologies are gaining momentum, as these formats reduce packaging weight, improve logistics efficiency, and minimize material usage compared to traditional metal cans. Automation in grading, cutting, and quality inspection processes is further optimizing yields and ensuring consistency. Additionally, advancements in BPA-free linings and recyclable packaging materials are addressing regulatory requirements and consumer safety concerns, reinforcing the industry's commitment to sustainability and innovation.

Canned Fruits Industry Leaders

-

Dole PLC

-

The Kraft Heinz Company

-

Del Monte Foods Inc.

-

Rhodes Food Group

-

Seneca Foods Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Del Monte introduced a unique range of fresh fruit products. The 15-ounce cans are available in three flavors: Brown Sugar Sliced Peaches, Salted Caramel Sliced Pears, and Cinnamon Sliced Pears. This new line features an "extra light" syrup, making the products suitable for seasonal baking or fruit salads.

- August 2025: Countree Food introduced the Fruit Ball Series, a new range of canned whole fruit spheres made entirely from real fruit and prepared in a spoon-ready size. The collection includes Yellow Peach Ball, Cantaloupe Ball, and Vanilla Pear Ball.

- January 2024: Dole Food Company introduced a new shipping service to enhance transportation options for mangoes, pineapples, and other tropical fresh fruits imported from Central America to the United States.

Global Canned Fruits Market Report Scope

Canned fruits are products prepared from fresh, frozen fruits following the thermal process, or processed by another physical method. Depending on the product type, the products go through various operations such as washing, peeling, coring, stemming, grading, cutting, etc. The canned fruits market is segmented into product type, form, distribution channels, and geography. By product type, the market is segmented into peaches, pineapple, mandarin oranges, pears, and other fruit types. Based on the form, the market is classified into whole fruits and cut fruits. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. The market has also been studied by geography under North America, Europe, Asia Pacific, South America, and the Middle East and Africa regions. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Peaches |

| Pineapple |

| Mandarin Oranges |

| Mixed Fruits |

| Pears |

| Other Fruit Types |

By Form

| Whole Fruits |

| Cut Fruits |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Peaches | |

| Pineapple | ||

| Mandarin Oranges | ||

| Mixed Fruits | ||

| Pears | ||

| Other Fruit Types | ||

| By Form | Whole Fruits | |

| Cut Fruits | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global canned fruits market in 2026?

The canned fruits market size is valued at USD 14.51 billion in 2026 and is projected to reach USD 18.48 billion by 2031 at a 4.95% CAGR.

Which product type is growing the fastest?

Mandarin oranges are forecast to rise at a 6.21% CAGR through 2031, outpacing all other fruit segments.

Why are online channels critical for future growth?

E-commerce orders deliver repeat-purchase rates 30% higher than fresh produce and are set to expand at a 6.67% CAGR, making digital shelves pivotal for canned fruits penetration.

How will the EU BPA ban affect suppliers?

Manufacturers must adopt plant-based or oleoresin linings by January 2028, lifting costs 8-12% but unlocking premium shelf placement and export eligibility.

Page last updated on: