Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 104.13 Billion |

| Market Size (2031) | USD 127.18 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

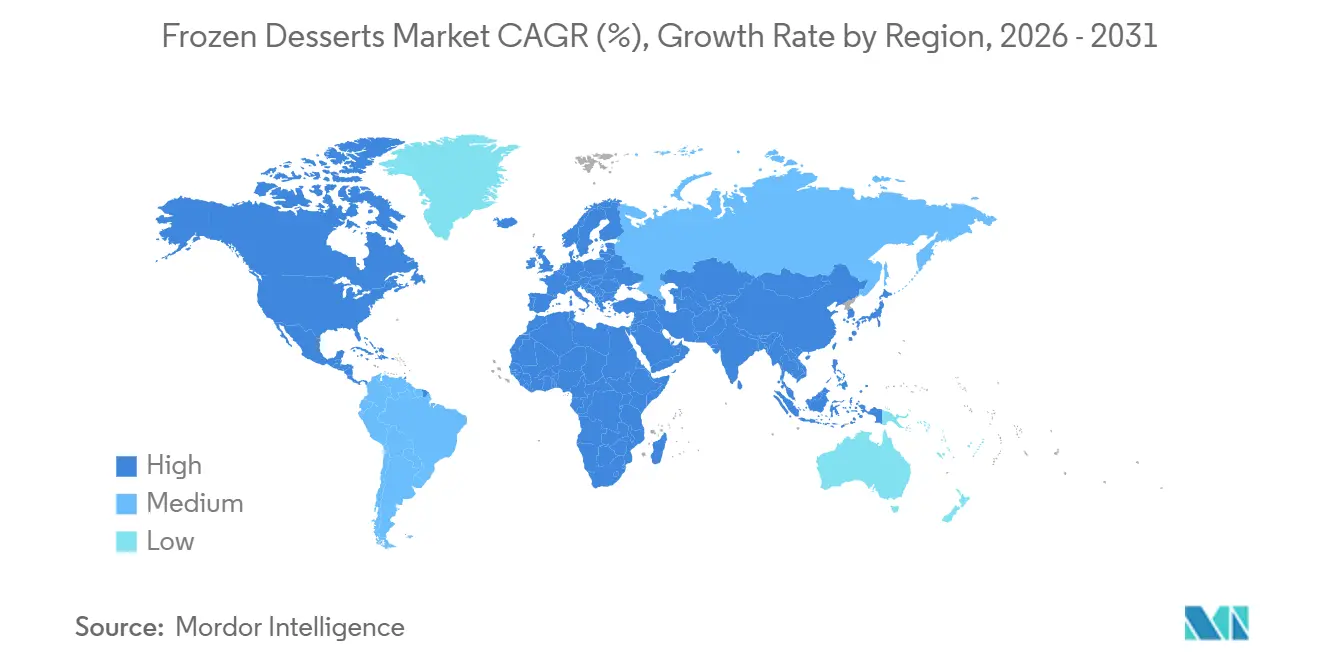

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

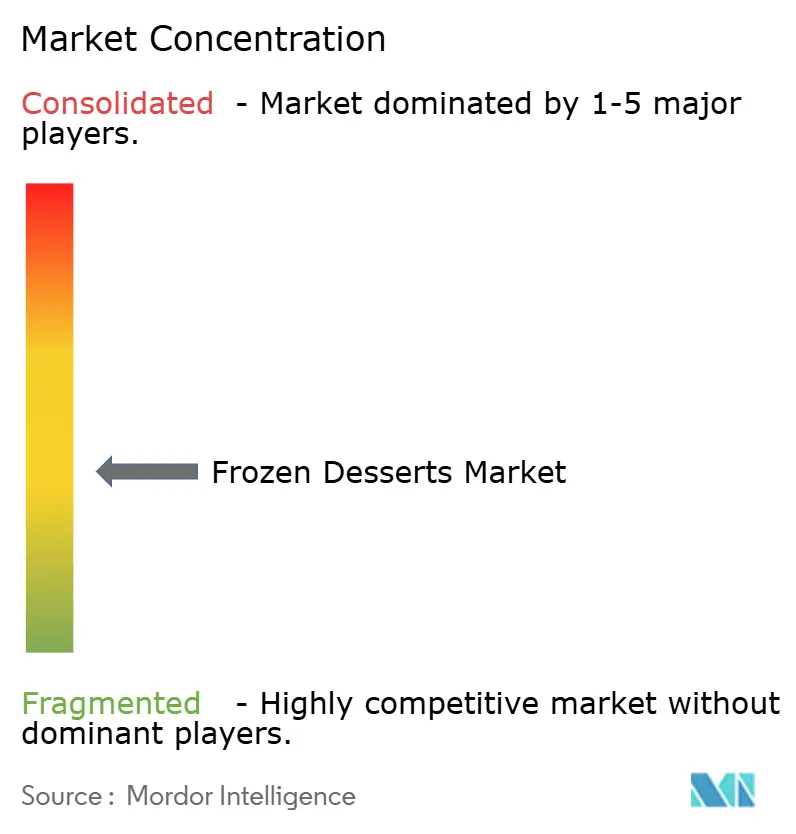

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Frozen Desserts Market Analysis by Mordor Intelligence

The Frozen desserts market size was valued at USD 100.03 billion in 2025 and is estimated to grow from USD 104.13 billion in 2026 to reach USD 127.18 billion by 2031, at a CAGR of 4.08% during the forecast period. This growth trajectory reflects the industry's resilience in the face of evolving consumer preferences and supply chain complexities. The market demonstrates remarkable adaptability as manufacturers pivot toward health-conscious formulations while maintaining indulgent appeal, creating a dual-track strategy that captures both wellness-focused and traditional consumer segments. Consumers are driving the frozen dessert market by seeking healthier options, including low-sugar, high-protein, and often non-dairy or plant-based treats. Simultaneously, they are drawn to innovative, premium flavors and textures that enhance their experience. Convenience plays a crucial role, as ready-to-eat and single-serve options, along with expanded availability in supermarkets, e-commerce platforms, and specialty stores, make these products more accessible. Furthermore, sustainability and ethical trends, such as eco-friendly packaging, clean labels, and a shift toward plant-based products, significantly influence product development and consumer preferences.

Key Report Takeaways

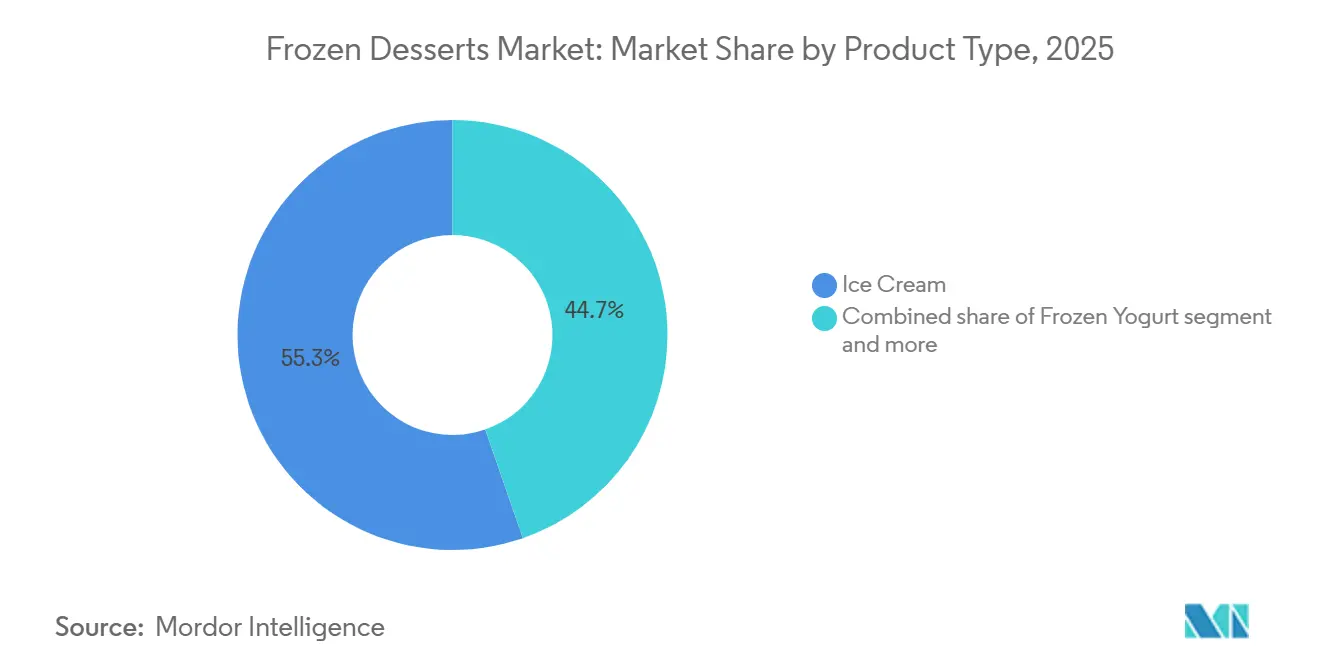

- By product type, ice cream led with 55.31% revenue share in 2025, while frozen yogurt is projected to record the highest CAGR at 5.11% through 2031.

- By category, conventional offerings held 80.18% of the frozen desserts market share in 2025; organic variants are forecast to expand at a 5.56% CAGR to 2031.

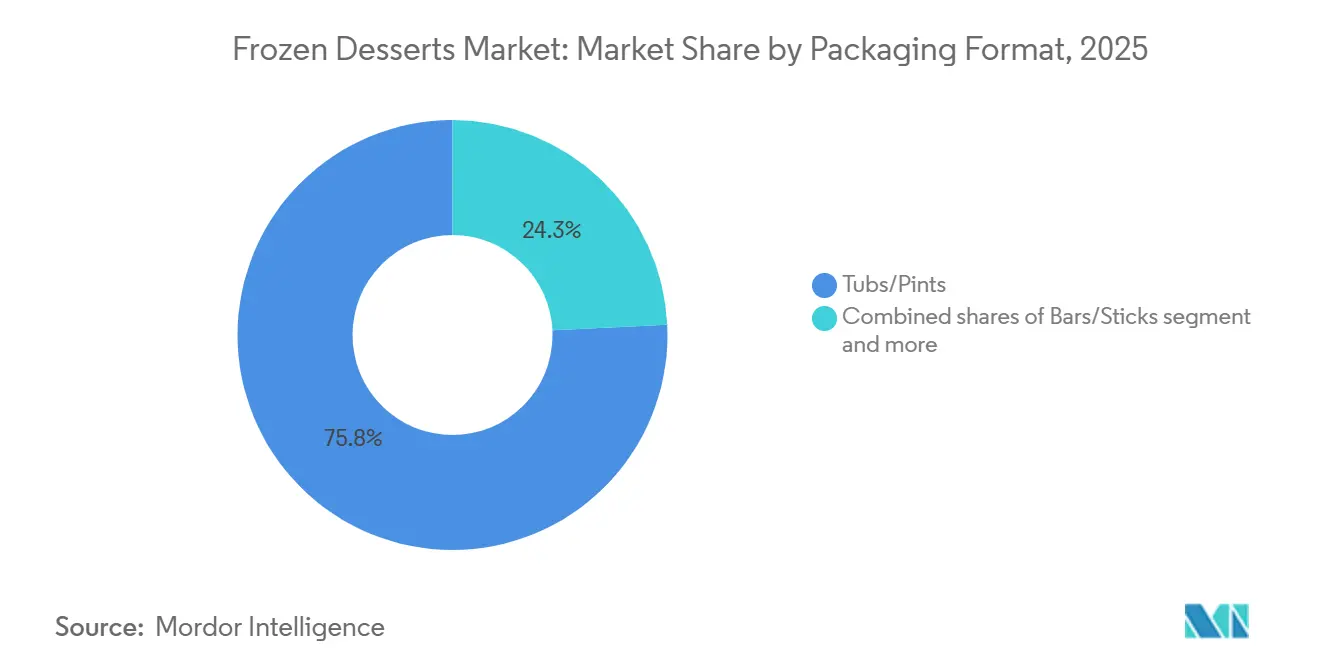

- By packaging format, tubs and pints accounted for 75.75% of the frozen desserts market size in 2025, whereas bars and sticks are advancing at a 4.89% CAGR through 2031.

- By distribution channel, retail controlled 83.18% sales in 2025, while foodservice/HoReCa is set to grow fastest at 5.01% CAGR over 2026-2031.

- Asia-Pacific secured 41.19% of the market share in 2025; the Middle East and Africa represent the quickest-growing region at 5.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Frozen Desserts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuous innovation in unique flavor varieties | +0.6% | Global, with premium positioning in North America and Europe | Medium term (2-4 years) |

| Rising demand for health-conscious and low-sugar dessert options | +0.9% | Global, led by North America and Europe, accelerating in Asia-Pacific urban centers | Long term (≥4 years) |

| Growth of premium and artisanal frozen desserts | +0.7% | North America and Europe core, spillover to Asia-Pacific affluent segments | Medium term (2-4 years) |

| Seasonal campaigns and promotional activities boosting sales | +0.4% | Global, peak impact in temperate regions during summer months | Short term (≤2 years) |

| Rising demand for plant-based and non-dairy frozen desserts | +1.0% | North America and Europe lead, Asia-Pacific following with lactose-intolerance prevalence | Long term (≥4 years) |

| Increasing adoption of sustainable and clean-label product formulations | +0.5% | Europe regulatory-driven, North America consumer-driven, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Continuous innovation in unique flavor varieties

Flavor innovation drives market differentiation as manufacturers leverages global culinary trends to capture adventurous consumer palates. Unilever showcases this approach with product launches like Talenti's bakery-inspired gelato layers and Good Humor's sustainably-farmed lime offerings. U.S. consumers increasingly prefer exotic fruit flavors such as mango, guava, and dragon fruit, while younger generations boost demand for global street food-inspired varieties. Collaborative product development, such as Baskin-Robbins' partnership with Trolli for sour-flavored ice cream, enhances cross-category appeal and extends seasonal relevance beyond traditional summer peaks. Social media-driven trends in flavor discovery and cultural fusion accelerate this innovation cycle. Manufacturers create consumer urgency and test market acceptance for permanent line extensions by focusing on limited-time offerings and co-branded flavors.

Rising demand for health-conscious and low-sugar dessert options

Consumers increasingly prioritize wellness, driving product development to offer indulgence without compromise. Frozen yogurt grows faster than traditional ice cream, while the organic segment shifts toward premiumization with a focus on cleaner ingredients and functional benefits. Perfect Day integrates its precision fermentation technology into Breyers' lactose-free chocolate ice cream, demonstrating how biotechnology addresses dietary restrictions while preserving dairy-like sensory qualities. Academic research on vegan ice cream formulations, using fermented hazelnut cake, reveals the potential of upcycled ingredients to enhance protein digestibility and antioxidant activity after digestion. Conagra targets the growing segment of GLP-1 medication users by developing high-protein, low-calorie frozen desserts with "On Track" labels to support weight management. This health-focused innovation not only enables premium pricing but also expands the market reach beyond traditional demographics.

Growth of premium and artisanal frozen desserts

The growth of premium and artisanal frozen desserts is emerging as a significant driver in the frozen desserts market. Consumers are increasingly seeking high-quality, indulgent products that offer unique flavors, natural ingredients, and a gourmet experience. This trend is fueled by rising disposable incomes, urbanization, and exposure to global dessert trends through social media and food tourism. Premium offerings, such as small-batch ice creams, gelatos, and innovative plant-based desserts, are gaining popularity among health-conscious and experience-driven consumers. Artisanal products also capitalize on clean-label formulations and locally sourced ingredients, appealing to sustainability-conscious buyers. As a result, manufacturers are investing in product innovation, sophisticated packaging, and targeted marketing campaigns to capture this growing segment. This shift toward premiumization not only enhances brand value but also supports higher profit margins, encouraging further expansion and competition in the frozen desserts market.

Increasing adoption of sustainable and clean-label product formulations

The increasing adoption of sustainable and clean-label product formulations is a key driver of growth in the frozen desserts market. Consumers are becoming more conscious of the ingredients in their desserts, preferring products with natural, minimally processed components and transparent labeling. According to research by the CBI Ministry of Foreign Affairs, clean-label products are projected to constitute over 70% of portfolios in 2025 and 2026, up from 52% in 2021, highlighting the rapid shift toward transparency and health-conscious choices[1]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities," cbi.eu. This trend is complemented by growing demand for environmentally sustainable practices, including responsibly sourced ingredients and eco-friendly packaging. Manufacturers are responding by reformulating recipes, reducing artificial additives, and introducing plant-based and organic variants to meet consumer expectations. The focus on clean-label and sustainable products not only strengthens brand trust but also enables companies to differentiate themselves in a competitive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to sugar content and artificial additives | -0.7% | Global, most acute in North America and Europe with stringent labeling | Long term (≥4 years) |

| High dependence on cold-chain logistics and temperature-controlled distribution | -0.9% | Emerging markets in Middle East, Africa, and South America; infrastructure gaps in rural Asia-Pacific | Medium term (2-4 years) |

| Shift in consumer preference toward fresh and alternative desserts | -0.4% | North America and Europe, urban centers with artisanal bakery proliferation | Short term (≤2 years) |

| Volatility in raw material prices including dairy and sugar | -0.8% | Global, with acute margin pressure in cost-sensitive Asia-Pacific and South America markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Health concerns related to sugar content and artificial additives

Health concerns related to sugar content and artificial additives are a significant restraint in the frozen desserts market. Increasing consumer health consciousness is creating formulation challenges, as manufacturers strive to balance taste and indulgence with nutritional expectations. Regulatory pressures are intensifying, with the U.S. Food and Drug Administration (FDA) proposing the revocation of 23 food standards of identity, which could impact the flexibility of frozen dessert formulations while ensuring consumer safety[2]Source: U.S Food & Drug Administration, "Proposal to Revoke 23 Standards of Identity for Foods; Preliminary Regulatory Impact Analysis", fda.gov. Additionally, the rising prevalence of diet-related diseases underscores the need for healthier products; according to the International Diabetes Federation (IDF), approximately 589 million adults (aged 20–79 years) were living with diabetes in 2024, and this number is projected to rise to 853 million by 2050[3]Source: International Diabetes Federation, "Diabetes around the world in 2024”, idf.org. These factors are driving manufacturers to explore sugar-reduced, natural, and functional ingredient-based alternatives, but reformulation without compromising taste remains a challenge.

High dependence on cold-chain logistics and temperature-controlled distribution

Cold-chain infrastructure limitations hinder market expansion, especially in emerging economies where the Asia-Pacific's growth potential encounters distribution challenges. Regulations from the USDA and FDA mandate continuous temperature monitoring at or below 0°F (-18°C), with documented compliance, adding operational complexity and cost pressures. Energy expenses for refrigerated transport and storage are substantial, and the push for sustainability complicates matters with demands for renewable energy adoption. While strong consumer demand exists, infrastructure gaps in developing markets restrict penetration. Conversely, established markets grapple with aging equipment and the need for efficiency upgrades. Reliance on specialized logistics providers introduces supply chain vulnerabilities, evident during peak seasons and extreme weather events. Although technology solutions like IoT monitoring and predictive maintenance present mitigation strategies, they necessitate significant capital investment and technical expertise, potentially sidelining smaller market players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ice Cream Dominance Faces Yogurt Challenge

In the frozen desserts market, ice cream dominates as the largest segment by product type, capturing a substantial 55.31% revenue share in 2025. This leadership stems from its widespread consumer appeal, driven by diverse flavors, textures, and formats that cater to both impulse purchases and family treats. Ice cream's entrenched position is bolstered by strong brand loyalty from global giants and extensive distribution networks in supermarkets, convenience stores, and foodservice outlets. Its versatility ranging from classic cones to premium artisanal varieties ensures consistent high-volume sales across demographics. Moreover, seasonal demand peaks during warmer months further solidify its market dominance, making it a staple in retail freezers worldwide.

Frozen yogurt stands out as the fastest-growing segment, projected to achieve the highest CAGR of 5.11% through 2031. This rapid expansion is fueled by rising health consciousness, positioning frozen yogurt as a lighter, probiotic-rich alternative to traditional ice cream for fitness enthusiasts and calorie-watchers. Innovations in low-sugar, plant-based, and dairy-free formulations are broadening its appeal, particularly among millennials and Gen Z consumers seeking indulgent yet guilt-free options. Self-serve frozen yogurt shops and ready-to-eat packaged formats are proliferating in urban areas, supported by e-commerce and quick-service channels. The segment's growth is further accelerated by flavor fusions like fruit-infused or functional varieties with added vitamins, tapping into wellness trends.

By Category: Organic Premiums Compress as Scale Arrives

Conventional offerings commanded the lion's share with an impressive 80.18% revenue share in 2025. This dominance is rooted in their affordability and mass-market appeal, making them the go-to choice for everyday consumers across households and foodservice settings. Widely available in supermarkets, convenience stores, and online platforms, conventional products benefit from established supply chains and economies of scale that keep prices competitive. Their broad flavor profiles and familiar formats such as standard ice creams, yogurts, and novelties resonate with price-sensitive families and impulse buyers alike. Major brands leverage heavy marketing and promotional tie-ins to maintain this stronghold, ensuring high shelf visibility and repeat purchases.

Organic variants in the frozen desserts market are poised for the fastest growth, forecasted to expand at a robust 5.56% CAGR through 2031. This surge reflects surging consumer demand for clean-label, pesticide-free, and sustainably sourced treats amid rising health and environmental awareness. Younger demographics, particularly millennials and Gen Z, drive adoption by prioritizing organic certifications that signal quality and ethical production. Innovations like dairy-free organic ice creams and yogurts with superfood add-ins are capturing premium shelf space in specialty and upscale retail channels. E-commerce platforms further amplify accessibility, enabling direct-to-consumer sales of these higher-margin products.

By Packaging Format: Bars and Sticks Capture On-the-Go Demand

Tubs and pints dominate with a commanding 75.75% share of the market size in 2025. This preeminence arises from their family-sized portions and value-for-money appeal, ideal for home consumption and sharing during gatherings. These formats excel in supermarkets and hypermarkets, where ample freezer space allows prominent displays that drive bulk purchases. Their versatility supports a wide array of flavors and premium upgrades, from indulgent classics to low-calorie options, catering to diverse household preferences. Strong supply chain efficiencies and longer shelf lives further bolster their position, minimizing waste and enabling widespread distribution. Ultimately, tubs and pints serve as the cornerstone of the market, leveraging volume sales to overshadow compact alternatives like bars and sticks.

Bars and sticks represent the fastest-growing packaging format in the frozen desserts market, advancing at a 4.89% CAGR through 2031. This growth is propelled by their portability and on-the-go convenience, perfectly suiting busy lifestyles and impulse buys at checkout counters. Rising demand for single-serve, mess-free indulgences appeals to children, teens, and active adults seeking quick treats without commitment. Innovations in fun shapes, novel flavors, and health-oriented variants like low-sugar or fruit-infused bars are capturing younger demographics and expanding market reach. Convenience stores and vending machines amplify their accessibility, fostering frequent, spontaneous purchases that boost overall category momentum.

By Distribution Channel: Foodservice Rebounds Post-Pandemic

Retail channels accounted for 83.18% of sales in 2025, establishing itself as the undisputed leader. This supremacy stems from its unparalleled reach through supermarkets, hypermarkets, convenience stores, and online platforms, where consumers make routine and impulse purchases. Retail's strength lies in its ability to offer extensive variety, from economy packs to premium novelties, all supported by eye-catching in-store displays and promotional endcaps. High-volume transactions during peak seasons, such as summer, further amplify its revenue generation, catering to families stocking freezers for everyday indulgences. Efficient cold-chain logistics ensure product freshness and availability across urban and suburban outlets, minimizing stockouts.

The foodservice and HoReCa segment is poised to exhibit the fastest growth in the frozen desserts market, with a projected 5.01% CAGR from 2026 to 2031. This expansion is driven by surging demand in restaurants, hotels, cafes, and catering events, where frozen desserts enhance dessert menus and elevate dining experiences. Premiumization trends favor artisanal ice creams, gelatos, and customized sundaes, appealing to diners seeking experiential treats post-meal. Urbanization and rising disposable incomes in emerging markets are boosting out-of-home consumption, particularly in quick-service and fine-dining establishments.

Geography Analysis

Asia-Pacific emerged as the largest regional market for frozen desserts in 2025, accounting for 41.19% of the total market value. The region’s dominance is primarily driven by large consumer bases in countries such as China, India, and Japan, coupled with rising urbanization and increasing disposable incomes. Growing adoption of western-style desserts, expansion of modern retail formats, and a strong presence of multinational brands have further strengthened market penetration. Additionally, a rising preference for premium and innovative frozen dessert options, including plant-based and functional variants, is supporting sustained growth in the region. The established cold-chain infrastructure in developed Asia-Pacific markets also facilitates wider distribution and availability, reinforcing the region’s leadership in the global frozen desserts market.

The Middle East and Africa represent the fastest-growing region, projected to expand at a CAGR of 5.33% between 2026 and 2031. This rapid growth is driven by increasing urbanization, rising disposable incomes, and greater exposure to global dessert trends through tourism and international food chains. Expanding modern retail networks, coupled with higher penetration of online grocery and delivery services, is further accelerating consumption. In addition, consumer demand for premium, artisanal, and indulgent frozen dessert products is steadily increasing, prompting both regional and global players to introduce localized flavors and formats.

Other regions, including Europe, South America, and North America, continue to play significant roles in the global frozen desserts market. Europe maintains a mature market with strong demand for premium, artisanal, and low-fat dessert options, particularly in countries like Germany, the UK, and France. North America exhibits steady growth, supported by innovation in flavors, convenience-focused formats, and plant-based alternatives, while the presence of established players like Unilever and Nestlé ensures a competitive landscape. South America, though smaller in market size, is witnessing gradual expansion driven by rising disposable incomes, urbanization, and increasing exposure to international dessert trends.

Competitive Landscape

The frozen desserts market exhibits moderate fragmentation, characterized by the presence of several multinational corporations alongside numerous regional and private-label manufacturers competing across product categories and price tiers. Leading companies such as Unilever, Nestlé, General Mills, and Froneri maintain strong global market positions through extensive distribution networks, strong brand portfolios, and continuous product innovation. However, regional brands and emerging artisanal producers continue to gain traction by focusing on premiumization, clean-label ingredients, and locally inspired flavors.

Competition in the market is largely driven by innovation, brand positioning, and expansion into new consumption occasions. Major players are actively introducing new formats, flavors, and health-oriented alternatives such as dairy-free, lactose-free, and high-protein frozen desserts to cater to changing dietary trends. Strategic collaborations, mergers, and acquisitions have also become common as companies aim to strengthen their geographic presence and optimize supply chains. At the same time, private-label brands are expanding rapidly, particularly in developed markets, leveraging competitive pricing and improving product quality to challenge established brands.

In addition, the competitive landscape is influenced by evolving retail dynamics and the growing role of e-commerce and direct-to-consumer channels. Companies are increasingly investing in digital marketing, cold-chain logistics, and omnichannel distribution strategies to enhance accessibility and consumer engagement. Sustainability initiatives, including environmentally friendly packaging and responsible sourcing of ingredients, have also emerged as key differentiators among market participants. While large multinational companies continue to dominate overall market share, the presence of niche and regional players ensures a diverse and competitive environment, contributing to the market’s moderately fragmented structure and ongoing innovation-driven growth.

Frozen Desserts Industry Leaders

-

General Mills Inc.

-

Meiji Holdings Co. Ltd

-

Nestlé S.A.

-

Unilever PLC

-

Fonterra Co-operative Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: GCMMF, operating as Amul and recognized as India's largest dairy cooperative, unveiled a bold initiative to channel INR 10,000 crore (approximately USD 1.2 billion) into food processing within the next two to three years. This substantial investment aims to establish 12 new manufacturing units, bolstering production capacities across dairy, ice cream, and various other food products. With this strategic expansion, Amul sets its sights on reaching a significant turnover target of INR 1 lakh crore (around USD 11 billion) in the coming years.

- June 2025: KLIMON, known for its entirely plant-based and dairy-free offerings, has expanded its retail footprint. The company announced that grocery chain Hy-Vee will feature a selection of its frozen desserts in 124 locations across the Midwest. Shoppers in states including Iowa, Missouri, Minnesota, Illinois, Nebraska, Kansas, and South Dakota can now pick up KLIMON pints. The lineup includes classics like Vanilla Boom and Chocolate Meltdown, alongside signature favorites such as Caramel Brûlée and Cherry Bomb, all enhanced with delightful mix-ins.

- April 2025: 16 Handles launched its Dubai Chocolate frozen yogurt flavor, riding the wave of a global dessert trend. This new offering melds a creamy pistachio base with crushed milk chocolate bits and a touch of cocoa, embodying the essence of this indulgent treat.

Global Frozen Desserts Market Report Scope

Frozen desserts are made by freezing liquids, semi-solids, and sometimes even solids. They may be based on flavored water, fruit purées, milk and cream, custard, and mousse. Most of these products are prepared from dairy products, such as milk and cream. The frozen desserts market is segmented by product type, category, packaging type, distribution channel, and geography. By product type, the market is segmented into frozen yogurt, ice cream, frozen cakes and pastries, and other types. By category, the market is segmented by conventional and organic. By packaging type, the market is segmented by tubs/pints, bars/sticks, cones/cups and others. By distribution channel, the market is segmented into foodservice/HoReCa and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market sizing has been done in value (USD) and volume (Tons).

By Product Type

| Ice Cream |

| Frozen Yogurt |

| Frozen Cakes and Pastries |

| Others |

By Category

| Conventional |

| Organic |

By Packaging Format

| Tubs/Pints |

| Bars/Sticks |

| Cones/Cups |

| Others |

By Distribution Channel

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Ice Cream | |

| Frozen Yogurt | ||

| Frozen Cakes and Pastries | ||

| Others | ||

| By Category | Conventional | |

| Organic | ||

| By Packaging Format | Tubs/Pints | |

| Bars/Sticks | ||

| Cones/Cups | ||

| Others | ||

| By Distribution Channel | Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the frozen desserts market in 2026?

It stands at USD 104.13 billion and is forecast to reach USD 127.18 billion by 2031.

How fast is the frozen desserts market expected to grow?

Between 2026 and 2031, the frozen desserts market is forecast to expand at a CAGR of 4.08%.

Which product type is growing quickest?

Frozen yogurt is projected to register the highest CAGR at 5.11% through 2031 due to probiotic positioning and lower sugar content.

Which region will see the fastest value expansion?

The Middle East and Africa are set to grow at a 5.33% CAGR through 2031 as cold-chain investment improves distribution reach.

What packaging formats are gaining popularity?

Single-serve bars and sticks are expected to grow at a 4.89% CAGR, reflecting on-the-go snacking trends and impulse purchases.

Page last updated on: