IQF Fruits And Vegetables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

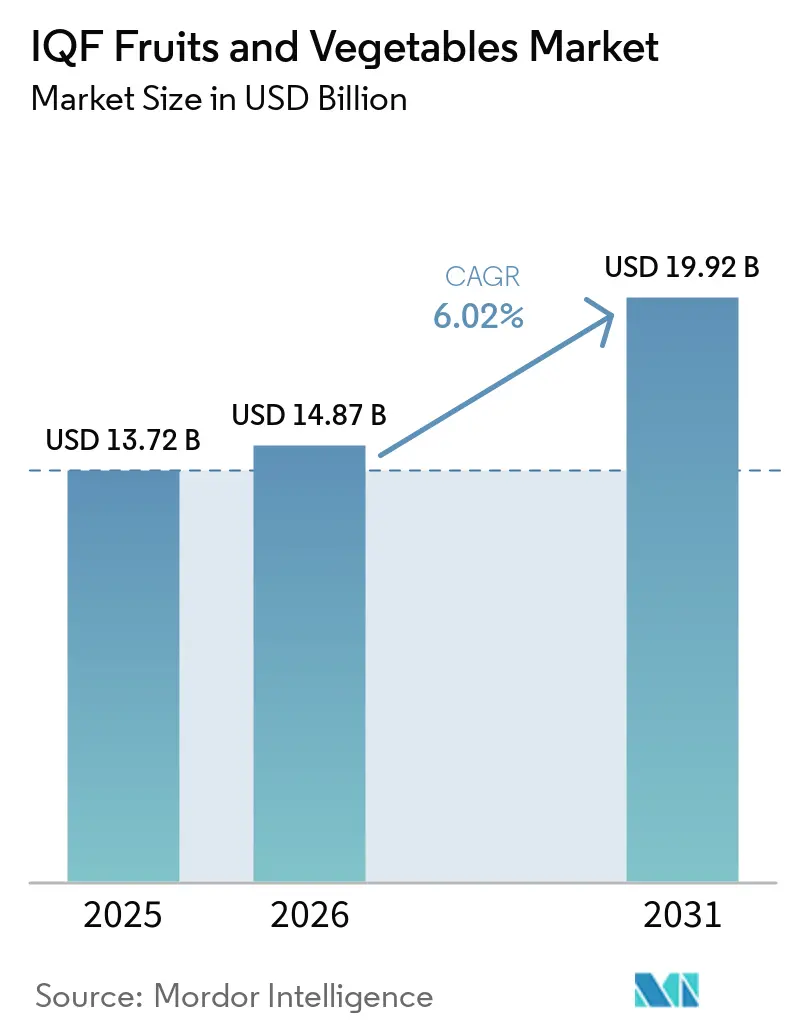

| Market Size (2026) | USD 14.87 Billion |

| Market Size (2031) | USD 19.92 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IQF Fruits And Vegetables Market Analysis by Mordor Intelligence

The IQF fruits and vegetables market size is expected to increase from USD 13.72 billion in 2025 to USD 14.87 billion in 2026 and reach USD 19.92 billion by 2031, growing at a CAGR of 6.02% over 2026-2031. Robust cold-chain upgrades, menu innovation among quick-service restaurants, and accelerating organic certification underpin this steady expansion across North America, Europe, and Asia-Pacific. Retailers are widening freezer aisles to meet demand for convenient, nutrient-retaining produce, while processors invest in energy-efficient tunnels and low-GWP refrigerants to hedge against rising power prices and regulatory penalties. Vertical integration, automation, and genetic advances in berry cultivation are widening the gap between well-capitalized incumbents and smaller operators. Governments in China, India, and Chile are underwriting blast freezers and reefer fleets, helping local processors secure export contracts with North American and European buyers.

Key Report Takeaways

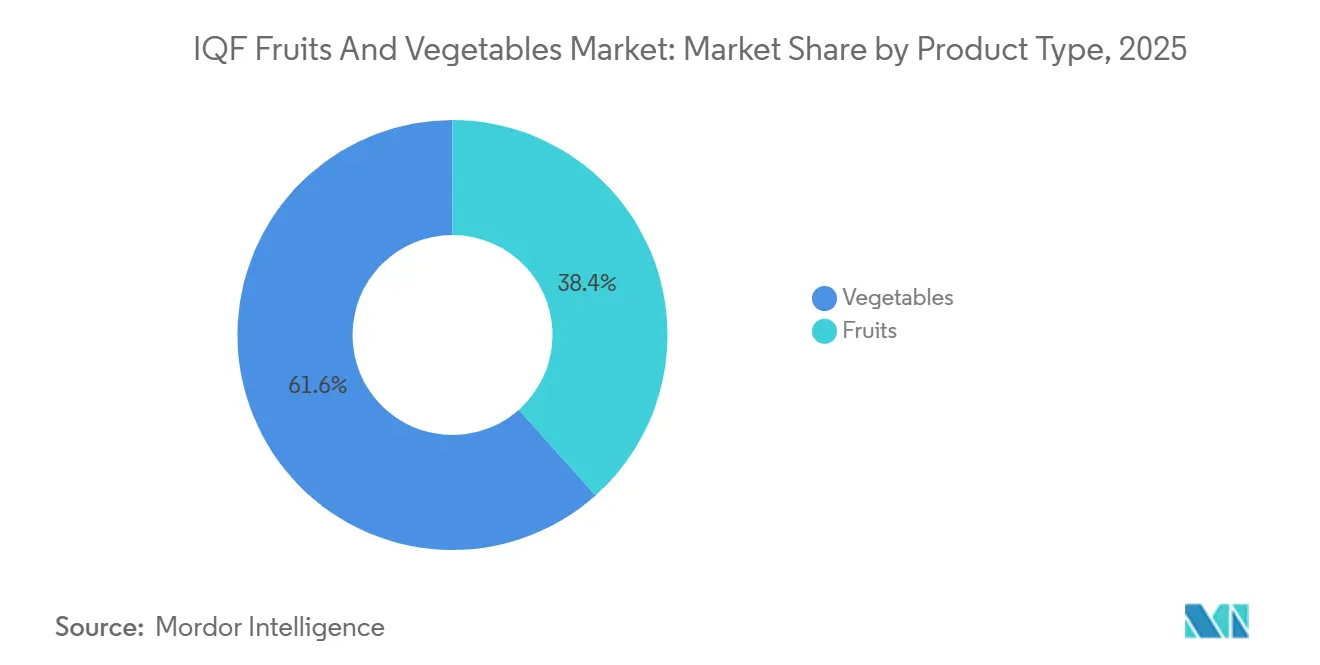

- By product type, Vegetables led with 61.59% of the IQF fruits and vegetables market share in 2025, whereas fruits are projected to grow at a 7.08% CAGR through 2031.

- By category, Conventional processing held 78.69% of 2025 revenue, while organic lines are forecasted to expand at 7.67% annually between 2026 and 2031.

- By form, Cuts, slices, and dices commanded 67.81% of 2025 sales, whereas whole formats are expected to advance at a 7.29% CAGR through 2031.

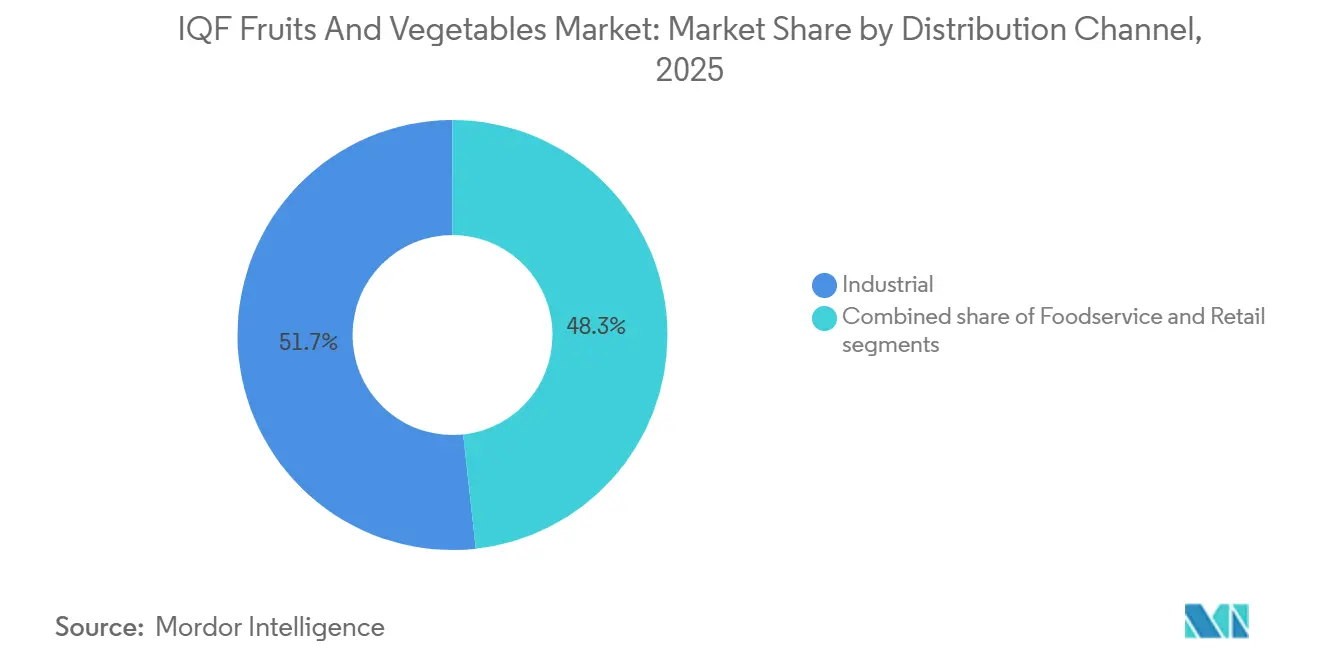

- By end use, Industrial applications accounted for 51.72% of the 2025 volume, while food-service channels are anticipated to grow fastest at 7.81% through 2031.

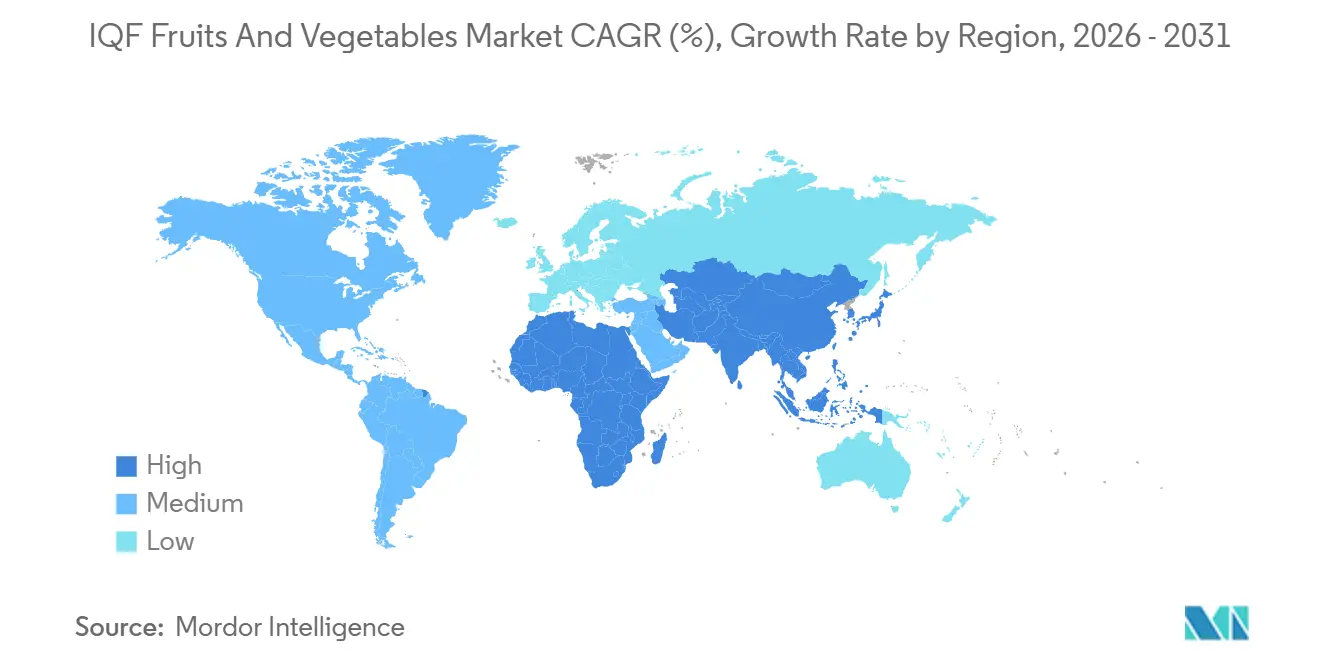

- By geography, North America contributed 35.40% of global revenue in 2025, yet Asia-Pacific is predicted to register the highest 7.92% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IQF Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient, nutrient-retaining frozen produce | +1.2% | Global, with the strongest uptake in North America and Western Europe | Medium term (2-4 years) |

| Expansion of the food-service and QSR sector | +1.0% | Global, led by North America, Asia-Pacific (India, China, Southeast Asia) | Short term (≤ 2 years) |

| Advancements in IQF processing and cold-chain infrastructure | +0.9% | Asia-Pacific (China, India, Philippines), South America (Chile, Peru) | Long term (≥ 4 years) |

| Growth of retail private-label frozen produce lines | +0.7% | North America, Europe (the United Kingdom, France, Germany) | Medium term (2-4 years) |

| Surge in smoothie/functional-beverage makers sourcing IQF berries | +0.6% | North America, Europe, and emerging in Asia-Pacific | Short term (≤ 2 years) |

| Carbon-footprint labelling driving processors toward IQF to cut waste | +0.5% | Europe (Austria, Italy, the United Kingdom), North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient Nutrient-Retaining Frozen Produce

Consumers now favor frozen formats that retain micronutrients while offering convenience, leading to a preference for IQF over slow-freeze or canned options. An Austrian life-cycle assessment found that frozen carrots produced 0.614 kg of CO₂-equivalent emissions per kilogram, factoring in consumer waste. In contrast, fresh carrots emitted between 0.186 and 0.200 kg. However, the frozen variant boasted better vitamin retention and avoided spoilage-related waste. In 2025, Nomad Foods analyzed the life cycles of 22 frozen products and found that most IQF vegetables and fruits have carbon footprints equal to or lower than their fresh counterparts, especially when considering retail waste and home refrigeration[1]Source: Nomad Foods, “Life Cycle Assessments of Frozen Produce,” nomadfoods.com. This data is influencing procurement strategies: retailers are broadening their frozen aisles to attract health-conscious consumers who once deemed frozen products as subpar. Simultaneously, foodservice operators are leveraging IQF to standardize portion sizes and cut down on preparation time. This trend is especially strong in North America and Western Europe, where dual-income families are on the lookout for meal solutions that prioritize nutrition, speed, and sustainability.

Expansion of Food-Service and QSR Sector

To address labor shortages and fluctuating prices of fresh produce, quick-service restaurants (QSRs) and institutional caterers are increasingly turning to Individually Quick Frozen (IQF) products. In Q3 2025, Smoothie King, known for its IQF fruit blends thawed in natural juice without added syrups, made significant strides by signing 32 new franchise commitments, marking its entry into Utah and Minnesota. The chain also introduced its high-protein "Power Eats" menu in 1,200 stores across the U.S. In December 2025, Cargill and McCain strengthened their partnership in India, moving McCain's portfolio entirely to RSPO Segregated palm oil. They are also co-developing soft oil blends for French fries, highlighting a trend of innovation in Asia's QSR frozen category. HyFun Foods, the sole Asian supplier endorsed by McDonald's, KFC, and Burger King, is set to double its French fry capacity in the next 9 months. With a goal of achieving a balanced revenue split between exports and domestic sales, HyFun has secured contracts for 300,000 tonnes of farmed potatoes in 2026, aiming to increase this to 600,000 tonnes within 2 years. These developments underscore the expanding QSR landscape in India, China, and Southeast Asia, driving a heightened demand for IQF vegetables and fruits. These products are essential for high-throughput kitchens, ensuring consistent flavor profiles across diverse regions.

Advancements in IQF Processing and Cold-Chain Infrastructure

In a bid to curb post-harvest losses and tap into export markets, governments across the Asia-Pacific and South America are backing the installation of blast freezers and bolstering refrigerated logistics. By 2025, India's Pradhan Mantri Kisan Sampada Yojana had successfully executed 300 out of the 404 projects it sanctioned. This initiative rolled out 1,924 pack houses and 6,485 reefer vans, and provided capital grants ranging from 35% to 50% for IQF blast-freezers, capping at INR 10 crore (around USD 1.2 million) per project. In 2025, China's cold-storage capacity saw a 5% uptick, reaching 277 million cubic meters. Concurrently, its fleet of refrigerated trucks expanded by 19%, totaling 587,900 units. These advancements empowered processors to tap into remote farming areas and cater to tier-2 cities[2]Source: Global Cold Chain Alliance, “Asia-Pacific Cold Storage Report 2026,” gcca.org. The Philippines, eyeing fruit and vegetable exporters, earmarked USD 53 million for the establishment of 100 cold-storage facilities. Chile's frozen-fruit industry underwent a transformation, embracing cutting-edge IQF lines, mechanical harvesting, and varietal renewal. This modernization propelled a 26% surge in 2024 exports, hitting 225,000 tonnes valued at USD 715 million. Notably, blueberries accounted for 46% of the shipments, while raspberries experienced a remarkable 70% uptick in early 2025. Thanks to these infrastructural strides, the time-to-freeze windows have shrunk, product quality has seen an uptick, and even smaller growers are now tapping into premium export markets that prioritize traceability and HACCP certification.

Surge in Smoothie and Functional-Beverage Makers Sourcing IQF Berries

Formulators of functional beverages and smoothie chains are securing multi-year contracts for IQF berries, ensuring access to antioxidant-rich ingredients at predictable prices. Organic IQF blackberries, which preserve up to 95% of their anthocyanins when rapidly frozen at -18°C, are being promoted to cafes and restaurants. These blackberries come with a slew of certifications: USDA Organic, EU Organic, HACCP, KOSHER, ISO 22000, and Halal. In December 2025, KD Healthy Foods targeted IQF blackberries for a diverse clientele, including manufacturers, bakeries, beverage producers, foodservice, retail, and private-label clients. They highlighted the advantage of free-flowing individual berries, allowing for precise portion control without the need to thaw entire packs. In 2024, Poland exported 103.9 million kg of frozen raspberries, fetching USD 206.4 million. Meanwhile, Chile moved 37.6 million kg, valued at USD 120.3 million. Unit prices varied between USD 3.00 to USD 8.09 per kg, influenced by origin and quality grade. This concentration of supply in Eastern Europe and South America results in counter-seasonal availability. Smoothie operators leverage this to ensure year-round menu consistency, while brands in the functional beverage sector utilize IQF berries to craft clean-label products, devoid of artificial colors and preservatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and energy costs of IQF lines | -0.8% | Global, acute in regions with high electricity prices (Europe, parts of Asia) | Medium term (2-4 years) |

| Consumer preference for fresh produce in key markets | -0.5% | North America, Western Europe, urban Asia | Long term (≥ 4 years) |

| Stricter pesticide-residue audits are causing shipment rejections | -0.6% | EU importers, North America (FDA enforcement), Asia-Pacific (Taiwan, Japan) | Short term (≤ 2 years) |

| Refrigerant phase-downs (HFC bans) are raising retrofit costs | -0.7% | Global, led by EU F-gas regulation and EPA AIM Act compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Energy Costs of IQF Lines

Processors grapple with the dual challenges of hefty upfront capital expenditures and persistent energy costs. This creates hurdles for mid-sized operators who find it tough to secure low-cost financing. Installations of Individual Quick Freezing (IQF) systems vary widely: from compact units managing 500 to 1,000 kg per hour to expansive systems that handle over 5 tonnes. Energy benchmarks for freezing typically hover between 140 to 220 kWh per tonne, while top-tier setups boast efficiencies of 80 to 130 kWh per tonne. In a notable case, an Egyptian IQF vegetable plant, after investing USD 1.1 million in efficiency upgrades, reaped annual energy savings of 1.4 GWh, translating to a payback period of just 5.2 years [Egypt IQF case study]. Adding to the complexity, electricity price fluctuations in Europe and select Asian regions pose challenges. For instance, processors in Germany and Italy find energy costs consuming 15% to 20% of their total operating expenses. In contrast, North American counterparts, benefiting from lower natural gas and hydroelectric tariffs, see these costs at a more manageable 8% to 12%. This disparity in energy expenses is driving industry consolidation. Major players like Greenyard and Conagra are capitalizing on their scale, securing advantageous utility contracts, and pouring investments into on-site renewable energy generation. Meanwhile, smaller processors face an uphill battle, striving to remain competitive on pricing without compromising on quality or regulatory compliance.

Refrigerant Phase-Downs (HFC Bans) Raising Retrofit Costs

Processors are being compelled by regulatory mandates to either retrofit or replace their freezing equipment, a move that can cost upwards of USD 1 million per facility. The EPA's AIM Act and the EU's F-gas Regulation 2024/573 enforce gradual reductions of HFCs, with deadlines set for January in 2025, 2026, 2027, and 2030, and impose penalties for non-compliance. New refrigerants like R-290 (propane), CO₂, and HFO blends necessitate the redesign of compressors, heat exchangers, and safety systems to address concerns of flammability and high operating pressures. EU processors grapple with added challenges due to the Kigali Amendment to the Montreal Protocol, which hastens phase-down schedules for developing economies, introducing uncertainty for exporters targeting European markets. Many smaller operators, lacking the technical know-how to assess retrofit options, face delays in compliance. This could lead to shipment rejections if their cold-chain partners refuse non-compliant loads. As a result of this regulatory shift, a performance gap is emerging: well-capitalized incumbents can absorb retrofit costs, while under-resourced newcomers risk losing market access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Berries Drive Fruit Segment Acceleration

From 2026 to 2031, fruits are set to grow at an annual rate of 7.08%, outpacing vegetables, which commanded 61.59% of the 2025 revenue. Berries, including strawberries, blueberries, raspberries, and blackberries, drive this growth, bolstered by the expansion of smoothie chains, the formulation of functional beverages, and a retail push for organic IQF packs. In 2024, Chile's frozen-fruit exports saw a 26% volume surge, reaching 225,000 tonnes. Blueberries made up 46% of these shipments, while raspberries experienced a notable 70% jump in early 2025, thanks to new plantings in the southern region and the adoption of mechanical harvesting. Tropical fruits like pineapple, mango, and papaya are gaining popularity in the Asia-Pacific and North American markets. Processors are crafting IQF dices for yogurt toppings and desserts, although these volumes still lag behind the berry categories. Meanwhile, other IQF fruits, such as stone fruits and citrus, find their niche in bakery and confectionery channels but contend with competition from canned and dried alternatives.

In 2025, vegetables held a 61.59% market share, led by root vegetables (like carrots and potatoes), legumes (such as peas and beans), and brassicas (including broccoli and cauliflower). Root vegetables, prized for their long shelf life, find versatile uses in soups, stews, and ready meals. Legumes, riding the wave of plant-based protein trends, position frozen peas and edamame as prime meat substitutes. Brassicas are seeing a resurgence, with QSR operators adding roasted Brussels sprouts and cauliflower rice to their health-focused menus. Other IQF vegetables, like peppers, onions, and leafy greens, cater to specialized needs, serving as pizza toppings and in stir-fry kits. Hortifrut's varietal-replacement initiative in Peru and China, which shuttered Mexican fields and incurred a USD 59.19 million loss in 2025, highlights a strategic shift. The focus is now on higher-yield, premium genetics that enhance post-harvest performance for both fresh and frozen markets.

By Category: Organic Certification Momentum Reshapes Supply Chains

From 2026 to 2031, organic IQF products are set to grow at an annual rate of 7.67%, outpacing the overall market by nearly a full percentage point. In 2025, conventional processing accounted for a dominant 78.69% share of the revenue. In March 2026, Sainsbury's unveiled a substantial GBP 5 billion investment, aiming to solidify long-term partnerships with 2,500 farms across Britain and Ireland. This includes 5-year contracts with 62 berry farms, ensuring price stability and promoting sustainability. Many of these contracts come with organic-transition assistance, helping farmers achieve USDA Organic, EU Organic, or similar certifications, which in turn, boosts their pricing potential. Retailers are capitalizing on consumers' readiness to pay a 20% to 30% premium for organic frozen products, especially in Western Europe and North America, where clean-label claims heavily influence buying choices.

While conventional IQF lines dominate the industrial and food-service sectors, driven primarily by cost considerations, the organic segment is witnessing a surge in interest. In Eastern Europe and South America, processors are capitalizing on lower labor and land costs, supplying conventional IQF vegetables to global QSR chains and private-label programs. Yet, with incentives like India's PMKSY subsidies covering 35% to 50% of blast-freezer costs for organic-certified facilities, smaller processors are increasingly eyeing organic certification as a unique selling proposition[3]Source: Ministry of Food Processing Industries (India), “PMKSY Progress Update 2025,” mofpi.gov.in. Compliance with standards like HACCP, ISO 22000, and region-specific organic benchmarks (USDA NOP, EU 2018/848) is becoming essential for export-focused processors, as buyers prioritize traceability and third-party audits to address food safety concerns.

By Form: Pre-Portioned Cuts Dominate Industrial Channels

In 2025, cuts, slices, and dices accounted for 67.81% of sales, reflecting industrial and food-service preferences for pre-portioned formats that reduce labor and waste. QSR operators specify dice sizes, 10 mm, 15 mm, or 20 mm cubes, for uniform cooking and visual consistency across locations. In February 2026, Greenyard partnered with Eureden, merging 4 Breton production sites to supply frozen gratins, ready meals, soups, and purées to 80 countries. Automated cutting and IQF tunnels ensure consistent portion sizes. Conagra’s USD 220 million Michigan expansion, featuring robotics and AI-driven process controls, aims to improve cutting precision and reduce rework for frozen-meal brands like Marie Callender's and Healthy Choice.

Whole IQF products are projected to grow at 7.29% annually from 2026 to 2031, driven by premium retail lines emphasizing visual appeal and nutrient retention. Whole berries, Brussels sprouts, and baby carrots command 15% to 25% price premiums over diced equivalents, as consumers perceive them as fresher and less processed. Organic IQF blackberries and raspberries with USDA Organic, KOSHER, and Halal certifications appeal to foodservice operators seeking clean-label ingredients that retain shape and color after baking or blending. E-commerce growth further boosts whole formats, as transparent packaging helps online shoppers assess quality, reducing returns and building loyalty. Form segmentation reflects end-use dynamics: industrial buyers prioritize cuts for cost efficiency, while retail and food-service channels pay premiums for whole IQF products to enhance menu differentiation.

By End Use: Food-Service Channels Outpace Industrial Growth

From 2026 to 2031, the food-service sector is set to experience the fastest growth rate among end-use segments, projected at an annual 7.81%. In contrast, industrial applications accounted for a significant 51.72% of the 2025 volume. To counteract labor shortages and the volatility of fresh-produce prices, QSR chains, institutional caterers, and full-service restaurants are increasingly standardizing their use of IQF ingredients. Demonstrating this trend, Smoothie King expanded in Q3 2025, committed to 32 new franchises, and rolled out the Power Eats menu across 1,200 US stores. These moves highlight how food-service operators leverage IQF fruit blends to ensure consistent flavor profiles and nutritional claims, all without the need for added syrups or preservatives. HyFun Foods, which boasts approvals from giants like McDonald's, KFC, and Burger King, is not only doubling its French-fries capacity but also aiming for an even split between export and domestic revenues. This strategy underscores the structural demand for IQF vegetables, driven by the expansion of Asian QSRs and their adherence to multinational quality standards.

Industrial end-users, including ready-meal manufacturers, bakeries, and ingredient suppliers, dominate the volume landscape, thanks to their long production runs and bulk purchasing power. These processors provide IQF vegetables and fruits to a range of operations, from frozen-pizza lines to soup manufacturers and bakeries, all of which prioritize consistent quality and year-round availability. Retail channels, spanning supermarkets, hypermarkets, convenience stores, and online platforms, are amplifying their frozen-aisle presence to attract health-conscious shoppers. Sainsbury's ambitious GBP 5 billion farm-investment initiative, featuring berry contracts, bolsters both its retail private-label offerings and food-service supplies. This move not only fosters vertical integration but also curtails procurement costs and enhances traceability. While online retail is carving out a niche as a burgeoning sub-channel, with e-commerce platforms promoting subscription models for organic IQF berry packs and meal kits pairing IQF vegetables with recipe cards, this segment still lags, representing under 10% of the total retail volume.

Geography Analysis

North America continues to dominate the global market with a substantial 35.40% share in 2025. The region's market leadership is built on a foundation of well-established market infrastructure, sophisticated cold chain logistics networks, and deep consumer understanding of frozen food products. North American consumers demonstrate high acceptance and trust in frozen food categories, supported by extensive retail distribution channels that ensure product availability across urban and suburban locations.

Asia-Pacific emerges as the fastest-growing region, advancing at an impressive 7.92% CAGR through 2031. This remarkable growth trajectory is fueled by accelerating urbanization patterns, particularly in major metropolitan areas, coupled with strategic investments in cold chain infrastructure development. The region's expanding middle class increasingly seeks convenient, high-quality food options, driving market expansion. China and India stand out as key growth markets, where improving distribution networks and evolving consumer preferences create substantial opportunities for market penetration.

Europe maintains its significant market position, controlling 47% of global frozen vegetable imports, valued at EUR 791 million in 2023. The region projects steady growth rates of 1-3% annually, supported by increasing consumer preference for convenience foods and growing adoption of plant-based diets. Germany, France, and the UK serve as primary market drivers, with Germany specifically excelling in preservation technology advancement and import volumes. The European market benefits from harmonized regulations and established quality standards, fostering international trade relationships and maintaining strong consumer confidence in frozen food products.

Competitive Landscape

The IQF fruits and vegetables market demonstrates fragmentation, creating a dynamic environment where both established companies and new entrants can secure market share through strategic positioning and technology adoption. Market participants implement a range of business strategies to maintain their competitive advantage, including vertical integration across the supply chain, production capacity expansion, sustainability-focused initiatives, and development of premium product lines. Conagra Brands illustrated this strategic approach through its significant capacity expansion program, which resulted in the introduction of over 50 new frozen products in 2025, while simultaneously addressing critical supply constraints that had led to inventory shortages and necessitated strict allocation measures.

The market's fragmented structure enables regional companies like Ardo to maintain strong competitive positions through focused sustainability programs and supply chain optimization efforts. Ardo's comprehensive MIMOSA+ program exemplifies this approach, targeting a substantial 40% reduction in carbon emissions by 2030 while fostering partnerships with 3,500 growers across multiple regions. Industry consolidation activities continue to reshape the competitive landscape, as demonstrated by SunOpta's strategic decision in 2023 to divest its commodity frozen fruit operations and redirect resources toward value-added product segments. This shift reflects a broader industry trend toward higher-margin opportunities, particularly in developing markets where expanding cold chain infrastructure creates increasing demand for advanced processing equipment and technical expertise.

Technological innovation continues to drive market evolution, with cryogenic freezing technology emerging as a significant advancement. Companies like Air Products are developing sophisticated freezing solutions that deliver superior quality preservation while reducing environmental impact compared to conventional mechanical freezing methods. The competitive environment is further defined by regulatory compliance requirements, particularly the FAO Codex standards for quick frozen vegetables. These standards serve a dual purpose, establishing entry barriers while creating quality benchmarks that facilitate international trade expansion and market growth.

IQF Fruits And Vegetables Industry Leaders

Ardo NV

Greenyard NV

Conagra Brands Inc.

Uren Food Group

Brecon Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Conagra Brands announced a USD 220 million investment to expand and modernize its Augusta, Michigan frozen-food manufacturing facility, creating approximately 400 jobs and substantially increasing production capacity for Marie Callender's and Healthy Choice frozen-meal brands through advanced automation, robotics, and AI-powered process control.

- March 2026: Sainsbury's strengthened backing for British and Irish farmers with a GBP 5 billion multi-year investment, expanding long-term agreements to more than 2,500 farms by 2027 and extending the model to 62 British berry farms through five new five-year contracts with Angus Soft Fruit, Chambers, Soft Fruits Direct, J.O. Sims, and Dyson Farming.

- February 2026: Greenyard acquired a majority stake in French agri-food cooperative Eureden's Gelagri Bretagne, combining frozen vegetable production and commercial activities across 4 Breton facilities employing approximately 900 workers to supply frozen vegetables, gratins, ready meals, soups, purées, and fruits to retail, food-service, and freezer-center customers in 80 countries including the EU, US, and Canada.

Global IQF Fruits And Vegetables Market Report Scope

IQF (Individually Quick Frozen) fruits and vegetables are produce items frozen individually at extremely low temperatures within hours of harvest. The global IQF fruits and vegetables market is segmented by product type, category, form, end use, distribution channel, and geography. By product type, the market is segmented into fruits and vegetables. The fruits segment is further sub-segmented into berries, tropical fruits, and other IQF fruits. Similarly, the vegetables segment is further sub-segmented into root vegetables, legumes, brassicas, and other IQF vegetables. By category, the market is segmented into conventional and organic. By form, the market is segmented into cut/slices/dices, and whole. By end use, the market is segmented into industrial, foodservice, and retail. The retail segment is further sub-segmented into supermarkets/hypermarkets, convenience stores, online retail, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Fruits | Berries |

| Tropical Fruits | |

| Other IQF Fruits | |

| Vegetables | Root Vegetables |

| Legumes | |

| Brassicas |

| Other IQF Vegetables |

| Conventional |

| Organic |

| Cut/Slices/Dices |

| Whole |

| Industrial | |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Other Distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Fruits | Berries |

| Tropical Fruits | ||

| Other IQF Fruits | ||

| Vegetables | Root Vegetables | |

| Legumes | ||

| Brassicas | ||

| Category | Other IQF Vegetables | |

| Conventional | ||

| Organic | ||

| Form | Cut/Slices/Dices | |

| Whole | ||

| End Use | Industrial | |

| Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the IQF fruits and vegetables market be by 2031?

The IQF fruits and vegetables market size is forecast to reach USD 19.92 billion by 2031, reflecting a 6.02% CAGR from 2026 to 2031.

Which segment grows fastest within IQF produce?

Fruits, led by berries, are projected to expand at a 7.08% CAGR through 2031 as smoothie and beverage demand accelerates.

Why are QSR chains adopting IQF ingredients?

Chains rely on IQF diced vegetables and berries to cut prep labor, stabilize input prices, and deliver uniform taste across outlets.

How do refrigerant regulations affect processors?

The EPA AIM Act and EU F-gas rules obligate a shift to low-GWP systems, adding up to USD 1 million in retrofit costs per facility but lowering long-term compliance risk.

Page last updated on: