Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

The Mobile Data Protection Report is Segmented by Type (Software, and Services), Deployment (On-Premises, and Cloud), Enterprise (Large Enterprise, and Small and Medium Enterprise), End-User Industry (BFSI, Healthcare, Retail, Hospitality, and Transport), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

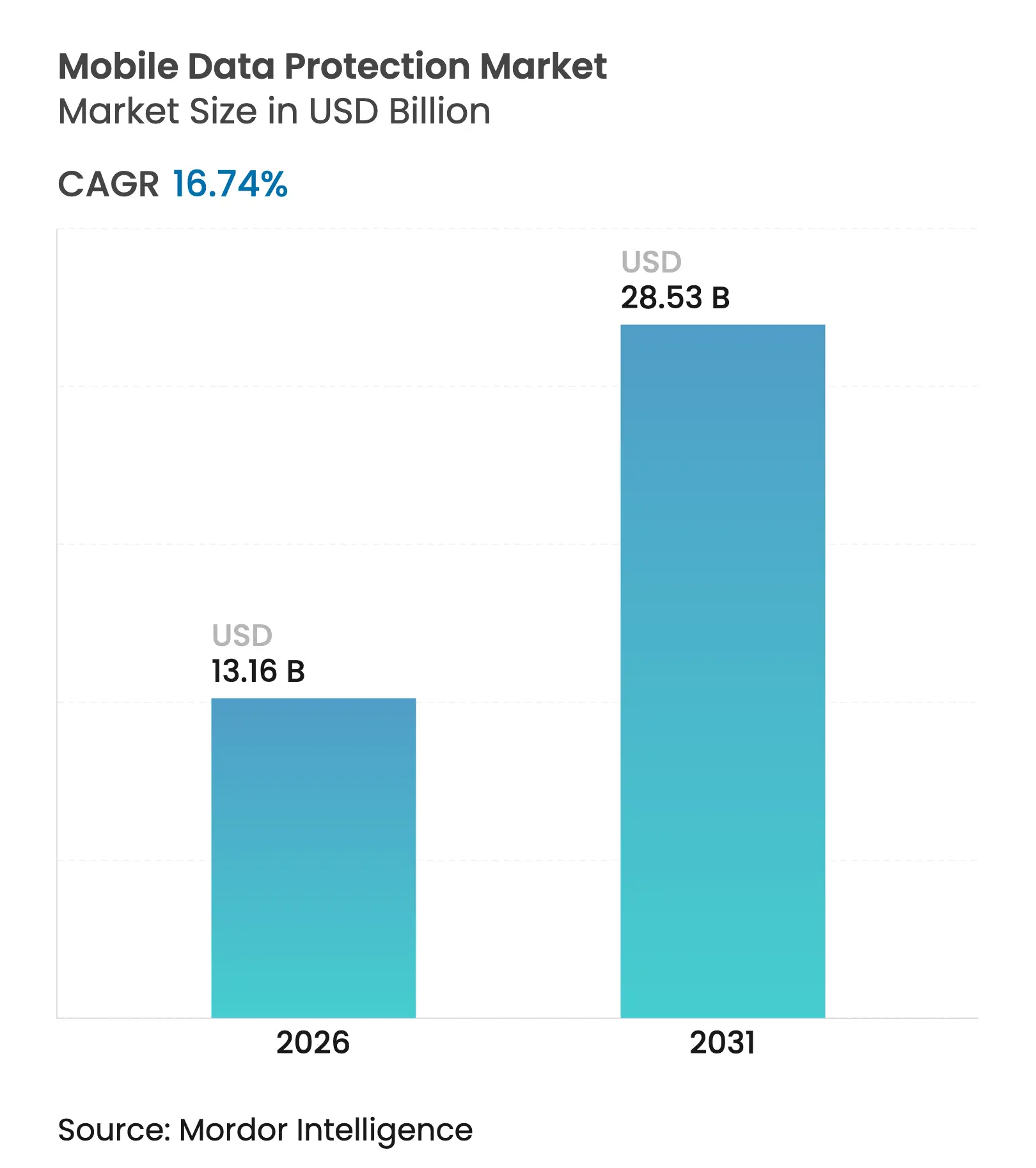

| Market Size (2026) | USD 13.16 Billion |

| Market Size (2031) | USD 28.53 Billion |

| Growth Rate (2026 - 2031) | 16.74 % CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

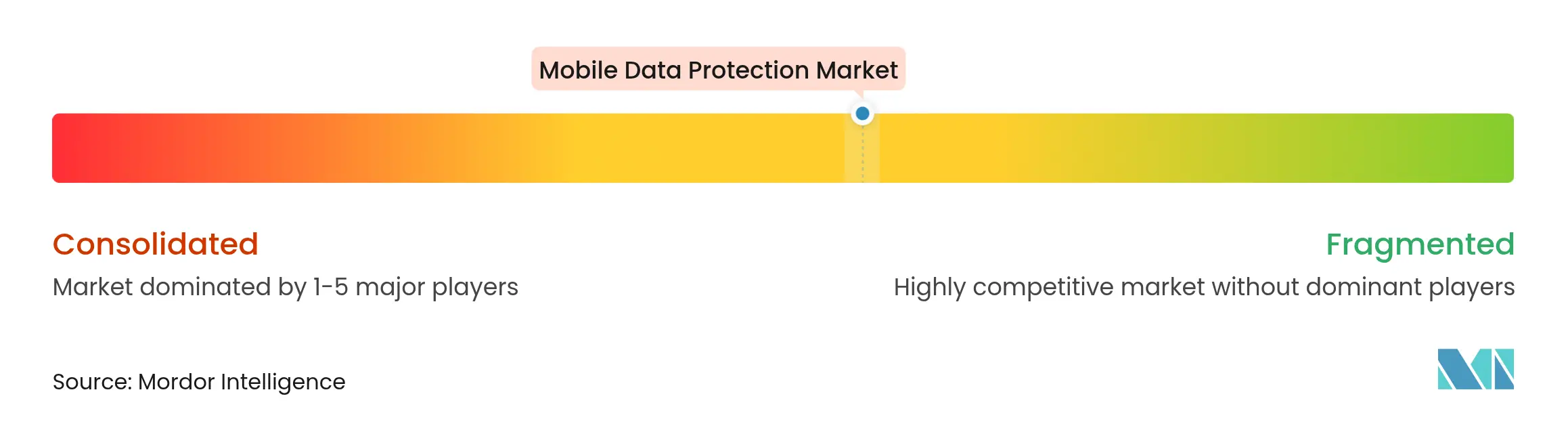

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The mobile data protection market size was valued at USD 11.27 billion in 2025 and estimated to grow from USD 13.16 billion in 2026 to reach USD 28.53 billion by 2031, at a CAGR of 16.74% during the forecast period (2026-2031). Rapid ransomware growth, new payment-security rules, and converging global privacy mandates are the strongest tailwinds. Software continues to dominate spending, but the relentless rise in outsourced threat-intelligence and incident-response work is shifting budget toward services. Cloud-based deployments are closing on-premises gaps as organizations favor software-as-a-service models that slash capital costs and shorten patch cycles, while unified endpoint management suites consolidate mobile threat defense, data-loss prevention, and zero-trust network access into a single console. Competitive intensity remains moderate, with the top five vendors holding a 38% slice of revenue and racing to integrate advanced analytics and compliance automation. Heightened workforce shortages and encryption overhead are the chief brakes on near-term velocity.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing adoption of mobile payment solutions Increasing adoption of mobile payment solutions | +2.8% | Asia-Pacific, North America, Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.8% | Geographic Relevance:Asia-Pacific, North America, Europe | Impact Timeline:Medium term (2-4 years) |

Growing bring-your-own-device adoption Growing bring-your-own-device adoption | +2.4% | North America, Europe | Short term (≤ 2 years) | |||

Escalating mobile ransomware and malware Escalating mobile ransomware and malware | +3.6% | Global | Short term (≤ 2 years) | |||

Heightened stringency of data-protection rules Heightened stringency of data-protection rules | +3.2% | Europe, North America, Asia-Pacific | Medium term (2-4 years) | |||

Demand for unified endpoint management suites Demand for unified endpoint management suites | +2.6% | North America, Europe, global enterprises | Medium term (2-4 years) | |||

Rising edge deployments in 5G environments Rising edge deployments in 5G environments | +2.1% | Asia-Pacific, Middle East, select U.S. metro areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Mobile Ransomware and Malware Incidents

The United States Cybersecurity and Infrastructure Security Agency logged a 15% year-over-year increase in ransomware events in 2024, totaling 5,289 reports, which moved mobile endpoints into the top tier of board-level risks.[1]nited States Cybersecurity and Infrastructure Security Agency, “Ransomware Statistics and Trends,” CISA, cisa.gov Kaspersky reported a 32% rise in mobile-banking malware, led by Anatsa and Godfather trojans that intercept one-time passwords and overlay legitimate app screens to steal credentials. Lookout counted over 4 million mobile phishing attempts, a 28% increase, driven by malicious progressive web apps masquerading as banking interfaces. The law-enforcement disruption of LockBit in February 2024 briefly eased pressure, yet successor groups quickly filled the gap, sustaining demand for real-time behavioral analytics and on-device machine-learning models. Procurement cycles are shortening as enterprises prioritize solutions that detect zero-day exploits without signature updates.

Heightened Stringency of Data Protection Regulations

The European Union’s Digital Operational Resilience Act requires financial institutions to implement incident-response and third-party risk controls by January 2025, mandating mobile-device encryption and remote-wipe capabilities for staff and contractors. California’s Delete Act gives residents a single-portal right to purge data from all registered brokers, amplifying the need for granular retention rules on mobile devices. India’s Digital Personal Data Protection Act, effective August 2024, imposes penalties up to INR 250 crore (USD 30 million) and requires explicit consent for cross-border transfers, accelerating the adoption of geo-fencing and residency controls. The Payment Card Industry Data Security Standard (PCI DSS) version 4.0, effective from March 2025, mandates multi-factor authentication for all remote access to card environments and quarterly penetration tests of mobile payment apps, thereby increasing demand for continuous validation platforms. Overlapping timelines compress decision windows and reward vendors with pre-built compliance templates.

Increasing Adoption of Mobile Payment Solutions

Visa recorded a 41% increase in enumeration attacks that target mobile wallets with low-value transactions, often preceding larger-scale fraud operations.[2]Visa Inc., “Payment Security Threat Landscape 2024,” visa.com Unified Payments Interface volumes in India surged 56% to 131 billion transactions during 2024, widening the attack surface for real-time payment interception. Mastercard processed 25 billion tokenized mobile payments, yet found that 18% of provisioning requests showed credential-stuffing patterns, spurring interest in device fingerprinting and behavioral biometrics. The European Central Bank’s digital-euro pilot embeds hardware-backed key storage, setting a benchmark that private issuers plan to match. Financial institutions are embedding mobile-threat-defense SDKs directly into apps to detect rooted devices, screen recording, and overlays, all without degrading the user experience.

Demand for Unified Endpoint Management Suites

Microsoft’s integration of Intune, Defender for Endpoint, and Purview Information Protection enables conditional-access rules that block unmanaged devices, cutting average breach containment from 287 days to 23 days in customer benchmarks. VMware added zero-trust network access to Workspace ONE, allowing enterprises to replace VPNs with identity-centric micro-segmentation. Organizations seek a single console to orchestrate policy, inventory, and threat intelligence across phones, tablets, and laptops, reducing administrative overhead and audit complexity. Platform consolidation pressures point solution vendors either to broaden capability through in-house R&D or pursue acquisition by larger suite providers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Functional interoperability issues Functional interoperability issues | -1.8% | Global | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:Global | Impact Timeline:Short term (≤ 2 years) |

High total cost of ownership of encryption High total cost of ownership of encryption | -2.2% | Global, especially cost-sensitive SMEs | Medium term (2-4 years) | |||

Limited qualified cyber-security talent Limited qualified cyber-security talent | -2.6% | North America, Europe, escalating worldwide | Long term (≥ 4 years) | |||

Low awareness in micro and small firms Low awareness in micro and small firms | -1.4% | Emerging Asia-Pacific, Middle East, Africa | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited Qualified Cyber-Security Talent Pool

The International Information System Security Certification Consortium estimates a global shortfall of 4.8 million professionals, with 68% of North American organizations reporting unfilled positions. The U.S. Bureau of Labor Statistics projects a 32% growth in security analyst roles from 2023 to 2033, far outstripping the demand for general labor. Salary premiums for mobile-security architects are straining mid-market budgets, and specialized skills in iOS and Android reverse engineering remain scarce, forcing many companies to turn to managed service providers that charge USD 15,000-40,000 per month for around-the-clock monitoring. Project timelines suffer as 42% of mobile-security rollouts experience overruns of 90 days or longer due to staffing shortages.

High Total Cost of Ownership for Full-Stack Encryption

A National Institute of Standards and Technology benchmark shows that AES-256 on mobile processors adds 12-47 milliseconds of latency per transaction, a drag on real-time payments and video apps.[3]National Institute of Standards and Technology, “Mobile Encryption Performance Benchmark 2024,” nist.gov Deploying hardware security modules, key-rotation systems, and escrow processes costs roughly USD 280,000 for a 5,000-device rollout. Future-proofing against upcoming quantum-safe algorithm mandates from the U.S. National Security Agency compounds the bill. The European Union Agency for Cybersecurity reports that 57% of firms under 500 employees view encryption expense as the main hurdle to adopting mobile defenses.

By Type: Services Gain as Threat Complexity Outpaces Internal Teams

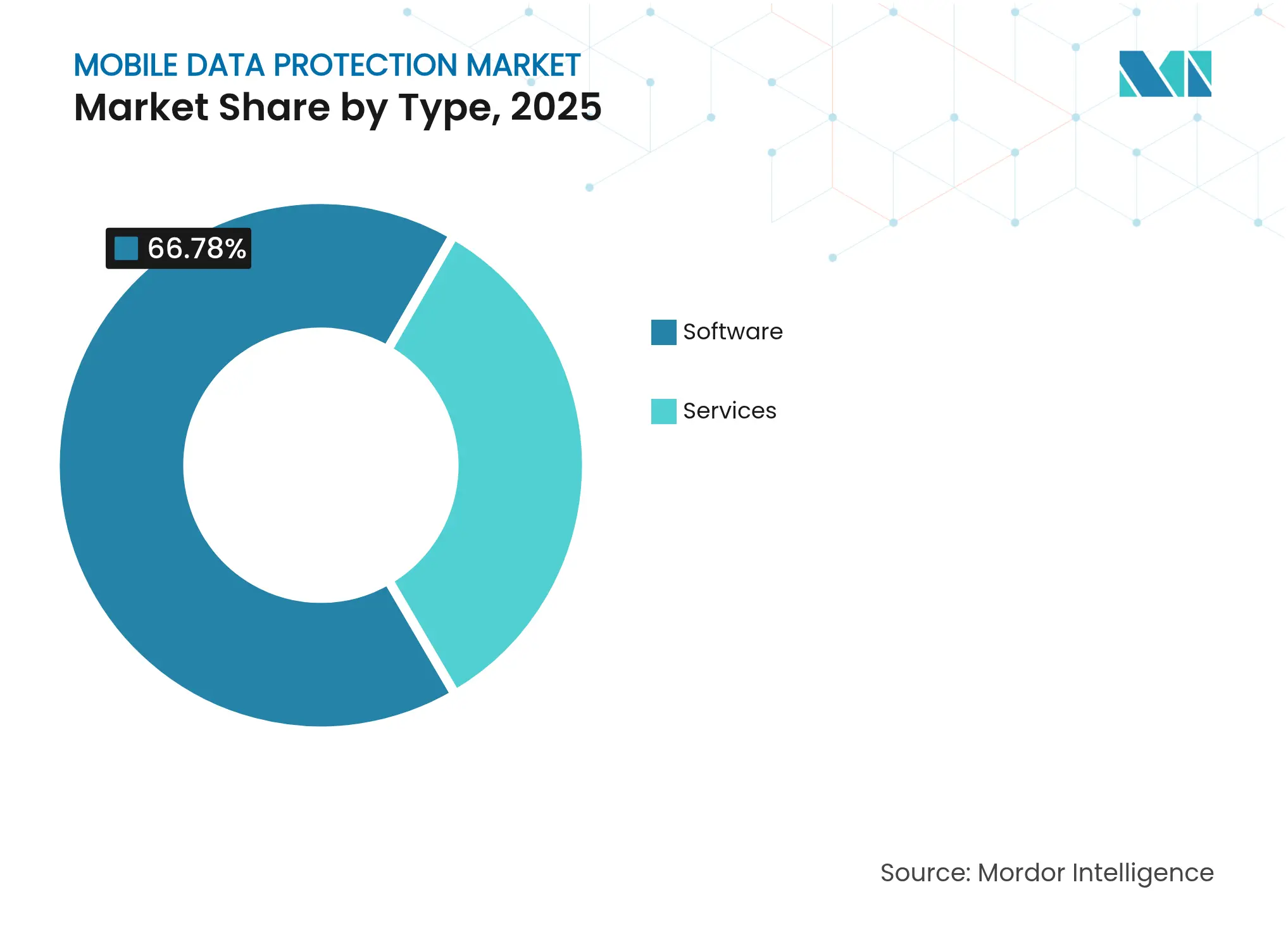

Services expand at an 18.12% CAGR through 2031, buoyed by incident-response outsourcing in the wake of breaches such as the Change Healthcare attack that exposed 100 million patient records and triggered a USD 22 million ransom. Software still owns 66.78% of 2025 revenue due to entrenched on-premises estates and air-gapped preferences in regulated sectors. The mobile data protection market size for services is projected to match software growth by the decade’s end as few enterprises can hire or retain forensic investigators and compliance specialists.

Integration work accelerates as clients collapse point tools into unified suites. Microsoft’s purchase of RiskIQ and its merger into Defender workflows shows the value of deep-linking threat intelligence to real-time response. Training and certification services grow alongside, with vendors obliging partners to complete extensive coursework before selling advanced offerings.

Note: Segment shares of all individual segments available upon report purchase

By Deployment: Cloud Architectures Accelerate Despite Sovereignty Concerns

Cloud installations are growing at a 18.66% annually as organizations favor subscription pricing and instant patching. The U.S. zero-trust maturity model identifies cloud-native policy engines as an advanced capability, encouraging regulated industries to adopt hosted control planes. Hybrid patterns bridge sovereignty gaps, keeping sensitive data on-premises while using public cloud for analytics.

On-premises retains 51.72% of 2025 spend and safeguards sectors bound by air-gap rules or local-hosting mandates, such as Saudi Arabia’s requirement that government data never leave national borders. Edge computing narrows the latency advantages once exclusive to on-premises environments; Verizon positions detection engines within 10 milliseconds of users across 47 U.S. metropolitan areas. The mobile data protection market share of cloud solutions is expected to continue climbing as latency and regulatory concerns recede.

By Enterprise Size: SMEs Accelerate Adoption Under Insurance Pressure

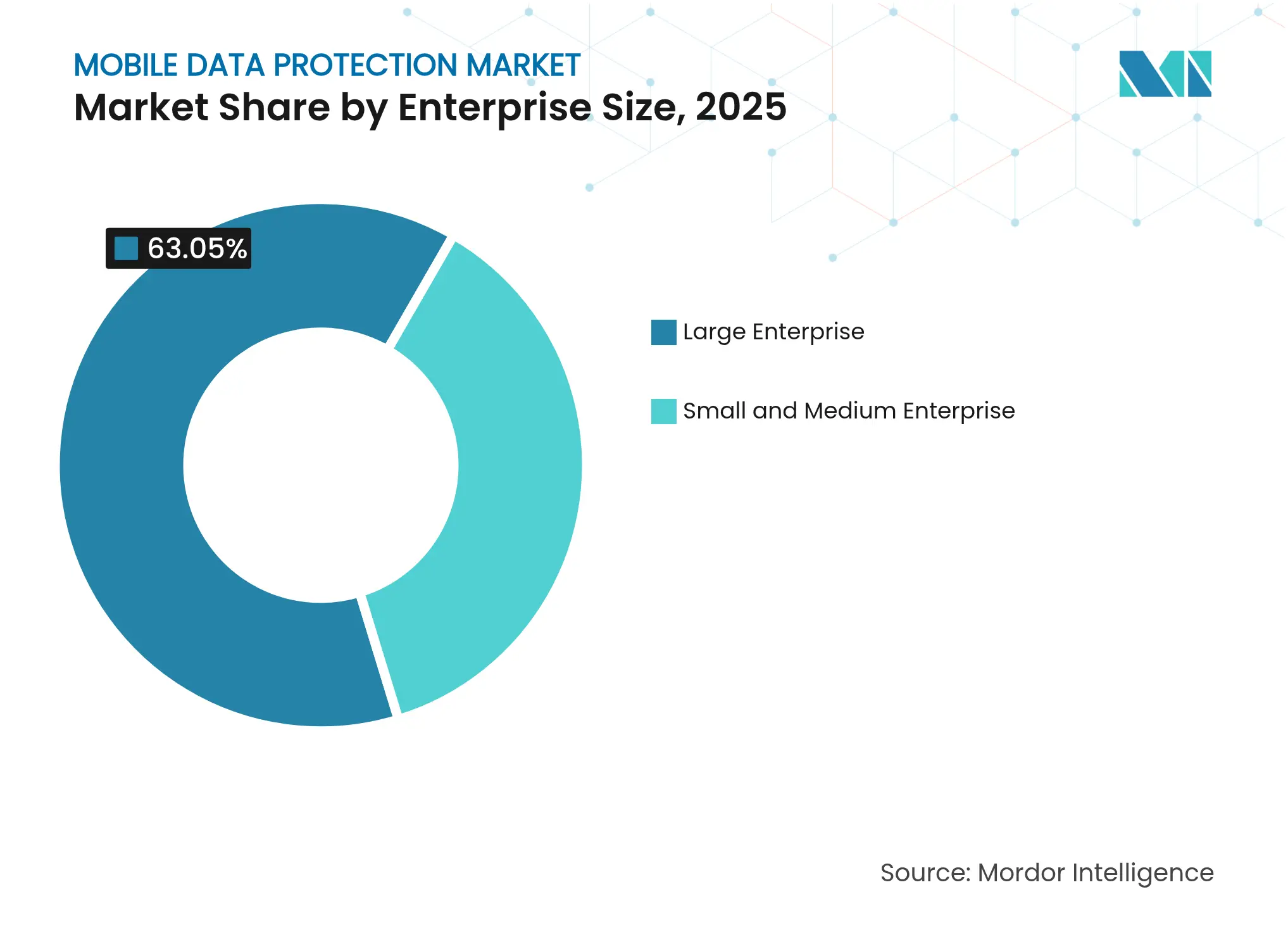

Small and medium enterprises expand at an 18.05% CAGR, propelled by underwriters that insist on endpoint detection and response before issuing cyber policies. Consumption-based pricing from vendors like Zscaler trims upfront costs and makes enterprise-grade defense affordable at USD 8-15 per user each month.

Large enterprises, which still control 63.05% of 2025 spend, extend mobile controls to contractors following supply-chain events such as the SolarWinds breach. The mobile data protection industry is gravitating toward license bundles in office productivity suites, helping corporate buyers rationalize tooling and accelerate rollouts.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: Healthcare Leads Growth Amid Breach Epidemic

Healthcare advances at a 18.71% CAGR as telehealth and electronic-record mobility collide with strict breach-notification penalties. The U.S. Office for Civil Rights reported 725 healthcare-sector incidents in 2024, with mobile-device theft and unauthorized access accounting for 28% of them. The February 2024 Change Healthcare event elevated board-room urgency for mobile threat defense.

Banking, financial services, and insurance preserve the largest slice at 34.21% thanks to PCI DSS and real-time payments. India now mandates mobile-app security tests for all banks by March 2025, sustaining demand for code analysis and runtime protection. Retail, hospitality, and transport trail but register rising device-management needs as mobile point-of-sale and connected-vehicle programs mature.

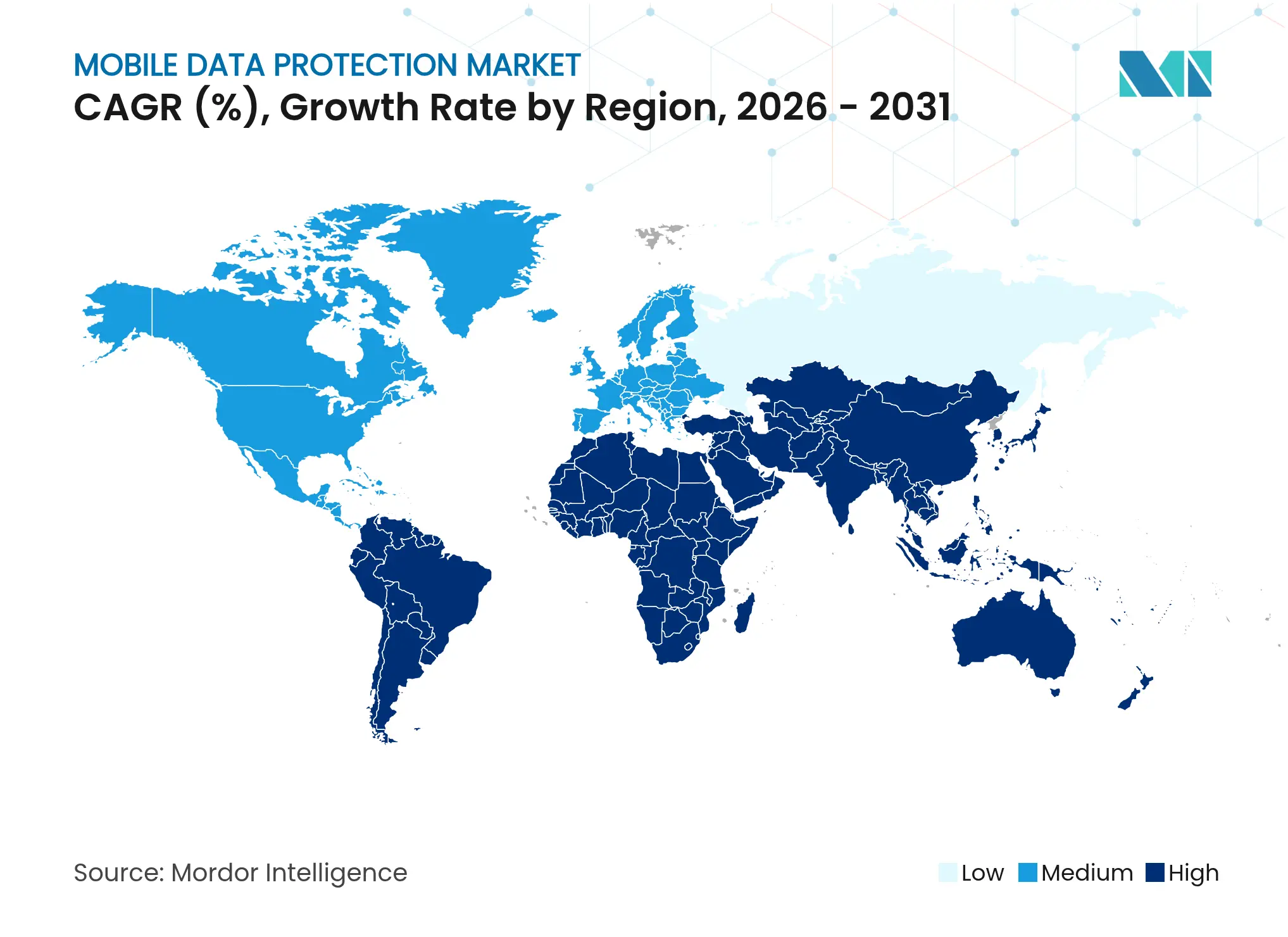

North America accounts for 41.05% of 2025 revenue. State privacy laws such as California’s Delete Act impose USD 180 per record breach costs, driving encryption and purge automation. The U.S. Secure-by-Design initiative encourages vendors to adopt default multi-factor authentication, while proposed Canadian amendments propose fines of up to CAD 25 million (USD 18.4 million) for delayed breach notices.

The Middle East is the fastest grower at 18.75%. Saudi Arabia orders all ministries to deploy mobile-device management for 1.2 million personnel by December 2025. The United Arab Emirates sets a June 2026 deadline for endpoint encryption across 47 free zones. Turkey now fines up to TRY 20 million (USD 650,000) for breaches involving stolen mobile devices, boosting demand for remote-wipe features.

Asia-Pacific gains momentum from mobile-first commerce and strict localization laws. India’s Digital Personal Data Protection Act punishes non-compliance with penalties reaching INR 250 crore (USD 30 million), compelling geo-fencing in apps. China levied CNY 1.2 billion (USD 165 million) in fines across 47 PIPL violations during 2024, several tied to poor mobile consent practices. Japan’s April 2024 reforms now require audits for apps processing sensitive data, while Australia logged 527 notifiable breaches and flagged mobile-device loss as 19% of them.

Europe remains shaped by GDPR plus the January 2025 Digital Operational Resilience Act cutoff. The European Data Protection Board ruled that pre-ticked boxes violate consent rules, forcing app developers to redesign permission flows. The United Kingdom National Cyber Security Centre recommends zero-trust and hardware-backed keys, setting procurement baselines for public agencies. South America’s spotlight is on Brazil, where LGPD enforcement fined companies BRL 45 million (USD 9 million) in 2024, some tied to weak mobile-endpoint controls.

Market Concentration

The mobile data protection market remains moderately fragmented. Top vendors hold a 38% combined slice and drive suite convergence to lock in customers and smooth compliance workflows. Microsoft bundles Intune and Defender with Microsoft 365 E5, leveraging its installed base of 345 million Office users to cross-sell security solutions. Cisco’s USD 28 billion Splunk buy marries network visibility to endpoint telemetry, promising correlated threat analytics across devices and cloud workloads.

Disruptors pursue consumption-based pricing that eliminates upfront spend, targeting the underserved SME cohort. Zscaler’s per-user model scales licenses with headcount shifts and now protects U.S. Department of Defense mobile endpoints under a USD 125 million deal. Specialist vendors exploit vertical depth. Imprivata offers single sign-on tightly woven into leading electronic health records, preserving HIPAA audit trails with minimal clinician friction. Patent filings underscore focus: Cisco lodged 14 applications on machine-learning anomaly detection and secure-enclave use, whereas Thales filed 11 covering quantum-resistant encryption.

White-space persists in micro-enterprises, where 73% of firms under 50 staff lack a formal mobile-security policy. Industrial control environments also emerge as a frontier as field-service tablets and wearables demand ruggedized threat defense.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE and GROWTH FORECASTS(VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The Mobile Data Protection Market study examines the increasing demand for securing sensitive data on mobile devices as organizations expand their digital and remote work environments. With rising cyber threats and regulatory requirements driving adoption, the study assesses key growth factors across software and service-based protection solutions and on-premises and cloud deployments.

The Mobile Data Protection Report is Segmented by Type (Software, Services), Deployment (On-Premises, Cloud), Enterprise (Large Enterprise, Small and Medium Enterprise), End-User Industry (BFSI, Healthcare, Retail, Hospitality, Transport), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.