Printed Cartons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

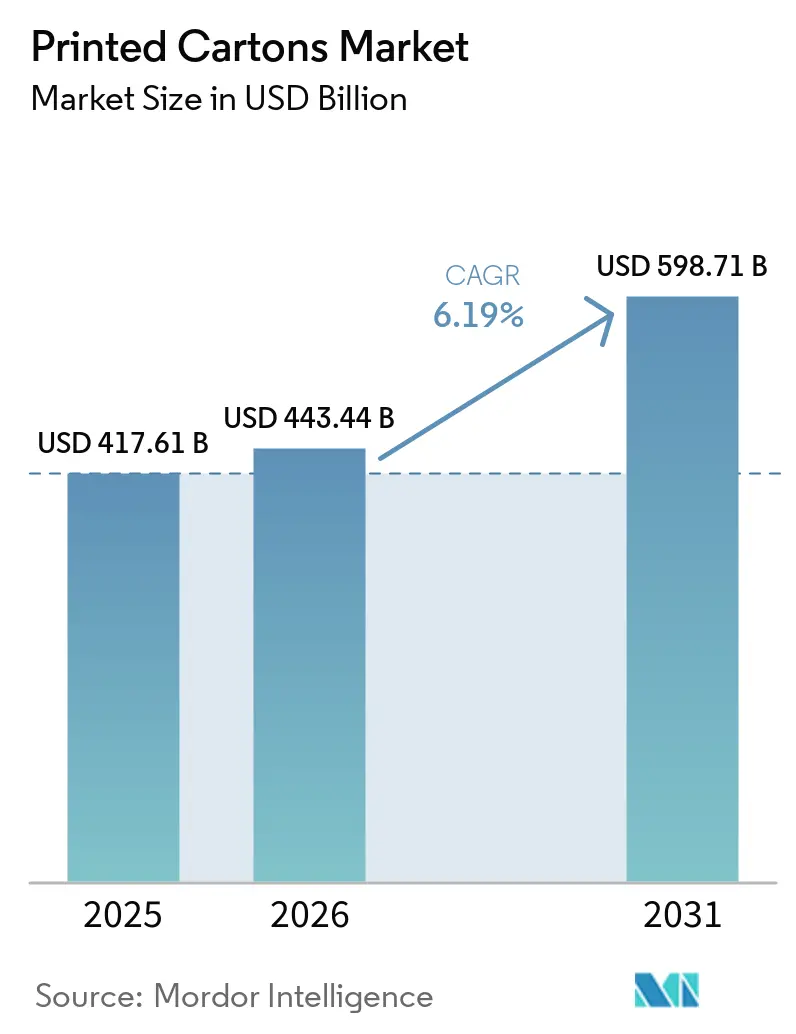

| Market Size (2026) | USD 443.44 Billion |

| Market Size (2031) | USD 598.71 Billion |

| Growth Rate (2026 - 2031) | 6.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Printed Cartons Market Analysis by Mordor Intelligence

The printed cartons market size was USD 417.61 billion in 2025 and is forecast to reach USD 598.71 billion by 2031 at a CAGR of 6.19% during 2026-2031. The printed cartons market is being shaped by a steady shift away from single-use plastic, the expansion of e-commerce fulfillment networks, stricter pharmaceutical traceability rules, and the faster adoption of digital printing equipment. These forces support each other because brands that move from plastic into fiber packaging often also want better print quality, stronger shelf presence, and formats that work across retail and online channels. The printed cartons market is also seeing procurement move toward higher-grade substrates and converting capabilities that can meet both branding and compliance needs. Competitive behavior reflects this change, with larger suppliers using scale, fiber integration, and technical specialization to defend margins while regional converters compete through faster delivery, niche certifications, and proximity to demand centers. The outlook remains constructive, although raw material volatility, energy costs, flexible packaging substitution, and changing EPR fee structures continue to shape pricing and investment decisions across the printed cartons market.

Key Report Takeaways

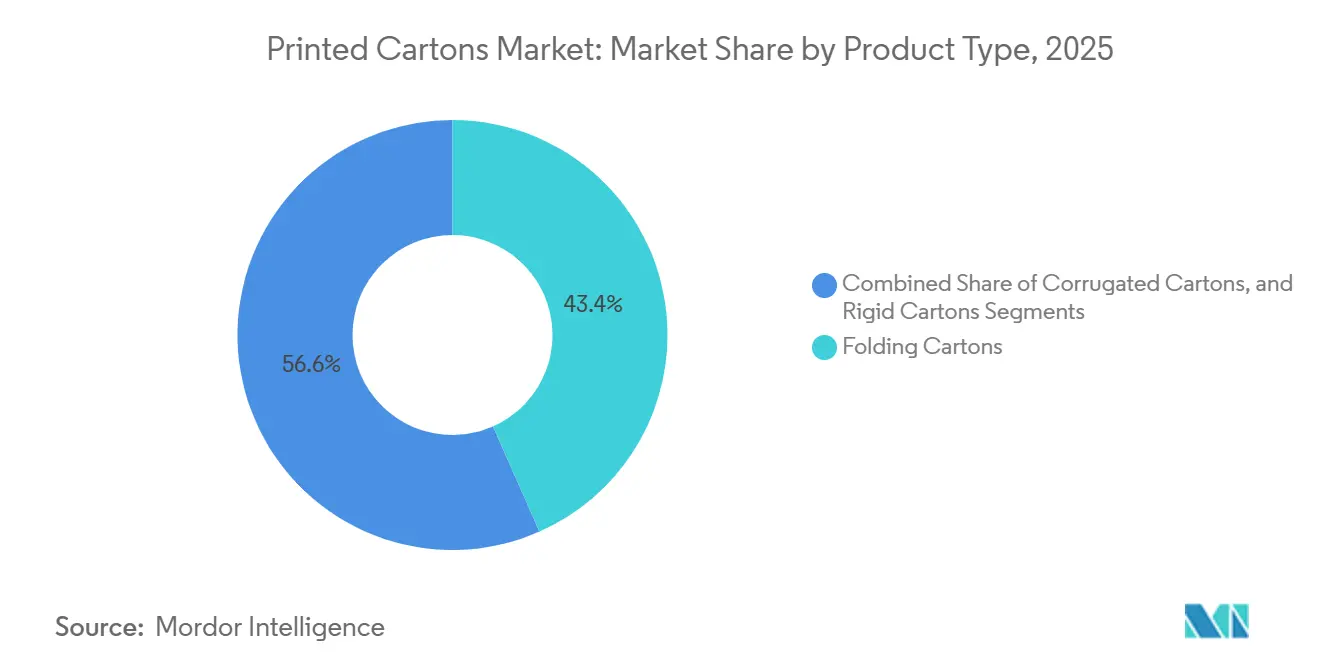

- By product type, folding cartons held 43.36% of the printed cartons market in 2025.

- By printing technology, the printed cartons market for digital printing is projected to grow at a 7.32% CAGR through 2031.

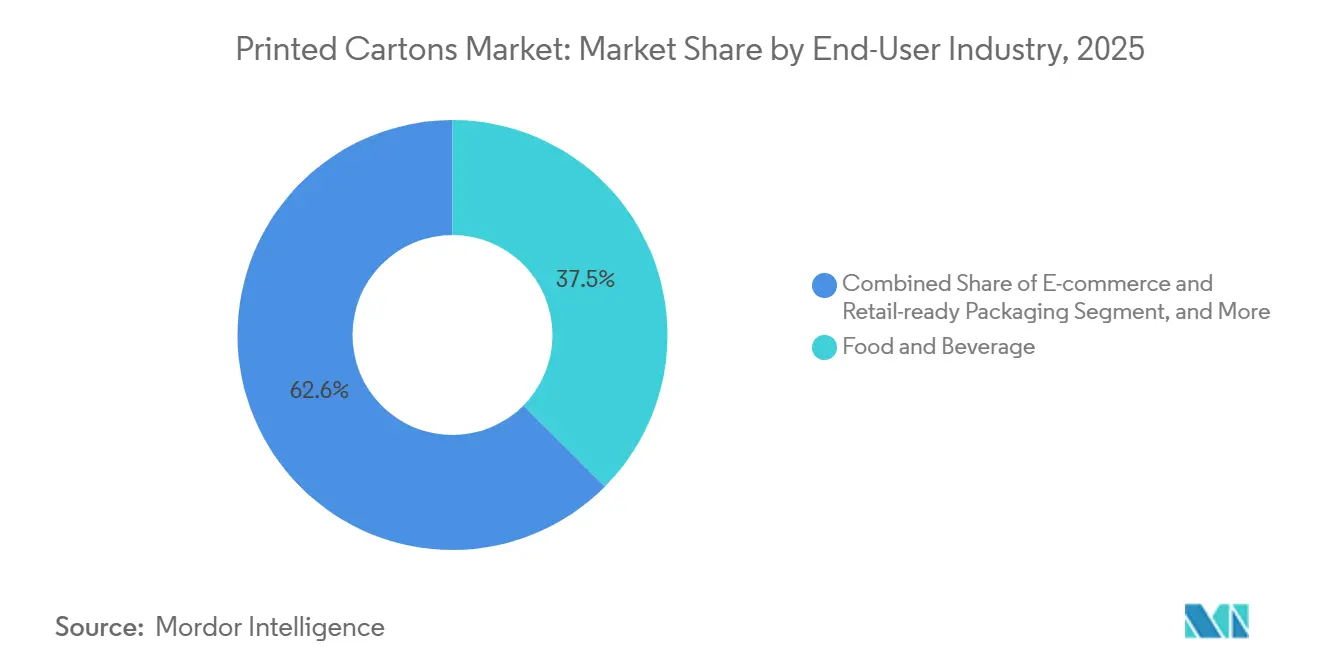

- By end-user industry, food and beverage captured 37.45% of the printed cartons market in 2025.

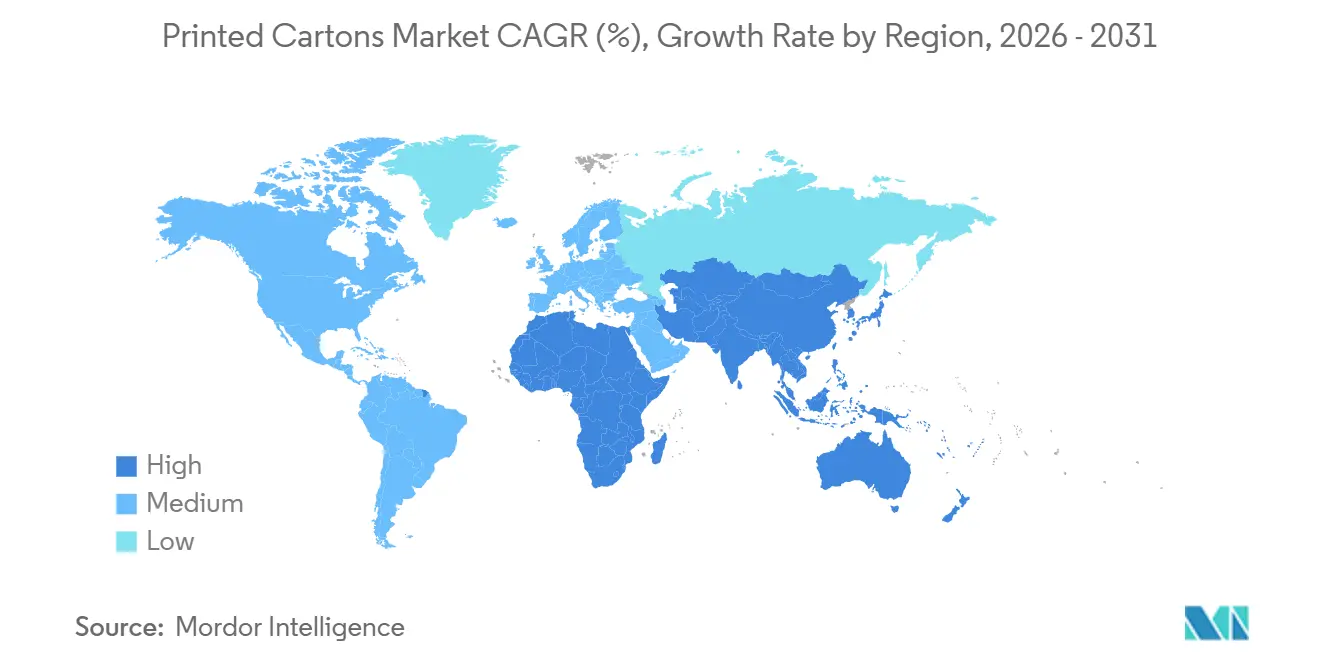

- By geography, the printed cartons market for Asia-Pacific is projected to grow at a 7.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Printed Cartons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from Plastic to Recyclable Fiber Packaging | +1.4% | Global | Medium term (2-4 years) |

| Pharmaceutical Serialization and Tamper-Evident Carton Requirements | +1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Premiumization and Shelf-Ready Branding Demand | +0.9% | Global, Strongest in Europe and Asia-Pacific | Short term (≤ 2 years) |

| E-commerce and Omnichannel Secondary Packaging Demand | +0.8% | Global, Strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| PFAS-Free Barrier Board Innovation Unlocking Food Applications | +0.7% | North America and Europe, Spill-Over to Asia-Pacific | Medium term (2-4 years) |

| SKU Proliferation Favoring Short-Run Digital Cartons | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift From Plastic to Recyclable Fiber Packaging

The printed cartons market is seeing its strongest structural push from the shift away from plastic to fiber-based packaging. Europe recorded a 82% recycling rate for paper and cardboard in 2025, improving the availability of secondary fiber and reducing the cost gap with virgin grades in many carton applications. The EU Packaging and Packaging Waste Regulation entered into force in February 2025 and became applicable in August 2026, raising pressure on brand owners to place recyclable packaging on the market.[1]Department for Environment, Food and Rural Affairs, “PackUK Extended Producer Responsibility for Packaging Producer Disposal Fees Modulation Statement,” GOV.UK, gov.uk This shift is not only about material replacement because brands are also finding that printed fiber cartons offer stronger graphic quality and better shelf visibility than many plastic alternatives. Groupe Bel’s plan to move all cheese-portion packs to folding cartons by 2027, eliminating 4,200 tonnes of plastic each year, shows how sustainability commitments are driving significant, visible demand for printed folding cartons across the market.

Pharmaceutical Serialization and Tamper-Evident Carton Requirements

The printed cartons market is also benefiting from pharmaceutical compliance rules that have elevated carton packaging to a more technical, recurring category. In the United States, DSCSA requirements have increased the need for cartons that can support unique identification and reliable print placement for regulated packs. In Europe, prescription medicine cartons also require a unique identifier and tamper-evident features, which strengthens demand for consistent board quality, precise converting, and dependable print performance. These rules are pushing converters toward digital and hybrid workflows because variable-data handling is now closely tied to contract retention in pharmaceutical packaging. The result is that pharmaceutical cartons carry higher technical requirements and longer qualification cycles, which supports premium pricing and more stable demand in the printed cartons market.

Premiumization and Shelf-Ready Branding Demand

Premium finishing demand is raising the value of carton output even in categories where volume growth is more measured. Consumer research cited for the French market showed that packaging influenced nearly 70% of purchase decisions, and 64% of consumers said packaging design led them to try a new product in 2025. Techniques such as foil effects, embossing, and textured finishes are gaining traction because they enhance shelf impact while still aligning with recycling goals for fiber packaging. Shelf-ready packaging adds another layer of value because retailers want formats that reduce store labor while still providing a branded display surface at the point of sale. That combination is helping specialty converters move away from low-margin commodity work and into accounts that reward design support, finishing capability, and retail execution within the printed cartons market.

E-Commerce And Omnichannel Secondary Packaging Demand

E-commerce continues to reshape the specification of cartons used in shipping, retail-ready presentation, and fulfillment operations. Major retailers and platforms introduced stricter carton requirements in 2025, and some of these requirements extend to RFID-linked workflows in 2026, increasing the need for pre-printed, machine-readable packaging. In Europe, online retail activity supported demand for cartons in lighter board ranges that reduce shipping weight while still holding up through last-mile handling. The printed cartons market is benefiting because secondary packaging now carries a larger data and branding function than it did in traditional wholesale distribution. At the same time, short inventory buffers at large e-commerce operators are raising the value of converters that can produce and replenish cartons on demand with limited setup time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material and Energy Cost Volatility | -0.9% | Global, Most Acute in Europe and South Asia | Short term (≤ 2 years) |

| Competition From Flexible Packaging Formats | -0.7% | Global, Strongest in North America and Europe | Long term (≥ 4 years) |

| EPR Fee Modulation Penalizing Hard-to-Recycle Structures | -0.5% | Europe, Expanding to North America | Medium term (2-4 years) |

| Barrier-Coating Qualification and Recyclability Trade-Offs | -0.3% | Global, Most Acute in Developed Markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material and Energy Cost Volatility

Raw material and energy inflation remains the most immediate pressure point for converters in the printed cartons market. North American containerboard prices rose by USD 50 per tonne net in Q1 2026, and producers followed with another planned round of increases in June 2026 in the USD 50-70 per tonne range. In Europe, natural gas prices moved above EUR 68 per MWh (USD 77 per MWh) in early 2026, raising the cost base for paperboard production across the region. Non-integrated converters bear the heaviest burden because they lack protection from long-term fiber contracts, internal mill capacity, or energy hedging. This pressure is feeding consolidation in the printed cartons market because smaller operators are less able to absorb repeated cost swings without losing margin or customer share.

Competition from Flexible Packaging Formats

Flexible formats remain a steady threat to substitution, where weight, transport efficiency, and low-cost pack formats matter most. Recyclable mono-material pouches and related film formats are improving their sustainability profile, especially in snacks, frozen foods, and condiments, thereby reducing one of the strongest arguments that had favored cartons. In North America, flexible pouches in snacks created a measurable drag on folding carton growth during the modeled period, showing that the risk is already affecting category performance. The printed cartons market also faces competition in logistics because flexible mailers and paper-based wraps are moving into some e-commerce use cases once reserved for corrugated formats. Producers that do not differentiate on print quality, structure, barrier performance, or regulatory compliance remain more exposed to substitution than suppliers operating in higher-value carton applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Folding Cartons Lead in Both Scale and Momentum

Folding cartons accounted for 43.36% of the printed cartons market size in 2025, making them the largest product type by a clear margin over corrugated cartons and rigid cartons. Their leadership stems from a blend of print quality, recyclability, and structural flexibility that suits food, pharmaceuticals, cosmetics, and many consumer goods applications. In the printed cartons market, folding cartons are used as primary packs in healthcare and beauty, secondary packs in food and beverage, and retail-ready packs in omnichannel distribution. The same segment is projected to expand at a 6.84% CAGR through 2031, making it the largest and fastest-growing category in the current market structure. That pattern reflects a broader shift toward mono-material fiber packaging, stronger retail presentation, and upgrades to pharmaceutical packaging specifications across the printed cartons market.

Corrugated cartons still hold a central role in shipping-heavy and industrial applications where crush resistance, stacking strength, and cost control matter most. They are also benefiting from the expansion of e-commerce networks, especially in Asia-Pacific and South America, where parcel volumes and warehousing activity continue to widen the addressable base for printed cartons market suppliers. Rigid cartons remain the smallest category by volume, but they preserve a strong position in luxury cosmetics, premium spirits, and high-end electronics where tactile quality and structural stiffness support higher unit pricing. Competition between product types is also shifting because micro-flute corrugated formats are moving into display and shelf-ready roles that once sat more firmly with folding cartons. That overlap is pushing converters in the printed cartons industry to sharpen design capability, substrate selection, and press flexibility rather than compete only on output volume.

By Printing Technology: Lithography Stays Central While Digital Changes the Cost Logic

Lithographic printing captured 38.62% of the printed cartons market size in 2025, confirming its leading position in long-run, high-definition carton production. Its advantage remains rooted in unit economics because high-volume work still favors offset once run lengths move beyond short promotional or regional batches. For much of the printed cartons market, lithography remains the preferred choice for food, beverage, and personal care cartons where visual consistency and efficient scale matter most. Flexographic printing continues to play a strong role in corrugated and retail-ready applications, and in North America, it accounted for 51.91% of its core use base in 2025. Gravure also retains value in specialized cosmetic and tobacco work, where very high print fidelity still carries a premium.

Digital printing is projected to expand at a 7.32% CAGR through 2031, making it the fastest-growing technology in the printed cartons market. Its growth is being driven less by full replacement of offset and more by the need for short runs, regional SKUs, seasonal packs, and variable data content. Packaging Dive described 2026 as a more mature stage for digital packaging printing, with adoption moving from experimentation into mainstream production decisions. This shift matters because brand teams now want packaging cycles measured in weeks, and converters with hybrid setups can serve both volume orders and high-agility work without forcing customers to choose between speed and quality. That is steadily changing how contracts are awarded across the printed cartons market.

By End-User Industry: Food Provides Scale While Electronics Adds Upside

Food and beverage accounted for 37.45% of the market value in 2025 and remained the largest end-user base in the printed cartons market. The category’s strength lies in daily consumption, strict food-contact requirements, and the need for branded primary and secondary packs across cereals, confectionery, dairy, frozen meals, and multipack beverages. Healthcare and pharmaceuticals represent the next major use case because tamper-evident features, serialized codes, and qualified production environments raise both technical requirements and pricing stability. Personal care and cosmetics keep demand strong for high-graphic SBS and rigid carton formats, while tobacco remains a narrower but still quality-sensitive outlet where the pack often carries much of the remaining brand communication. Together, these categories keep the printed cartons market anchored in applications that value both compliance and visual presentation.

Electrical and electronics is projected to record the fastest growth, with a 6.86% CAGR through 2031, as OEMs replace plastic clamshells and EPS inserts with fiber-based carton solutions. That change reflects both sustainability goals and rising producer responsibility costs, which are making paper-based alternatives more attractive despite some upfront material trade-offs. The e-commerce and retail-ready subsegment is also expanding because retailers want frustration-free, scannable, and tamper-evident formats that can move cleanly from fulfillment to store display. These shifts create new room for suppliers that can combine protection, anti-static coatings, branding, and efficient cube utilization in one carton design. As a result, the printed cartons market is gaining a more diverse growth base than it had when food and healthcare carried a larger share of total momentum.

Geography Analysis

Asia-Pacific held 39.14% of the printed cartons market share in 2025 and is projected to grow at a 7.13% CAGR through 2031, making it the largest and fastest-growing regional market. China remains the anchor because its restrictions on single-use plastics have supported demand for folding cartons and corrugated products across retail and e-commerce channels. Capacity additions by large local suppliers also show that domestic demand is being met by a long-term supply response rather than solely by short-term trade flows. India adds another major layer of growth, as organized retail, FMCG expansion, and packaging regulations are pushing more brand owners toward fiber-based formats. Japan, South Korea, Australia, and New Zealand have distinct demand mixes centered on higher-value cartons, digital printing adoption, and packaging formats that support traceability and premium brand presentation.

North America and Europe together represent the largest value pool outside Asia-Pacific in the printed cartons market. North America is being driven by e-commerce fulfillment growth, tighter retailer packaging specifications, and the need for pharmaceutical cartons that support serialization and tamper-evident packaging. Europe’s outlook is shaped by recyclability rules under PPWR and by EPR systems that increasingly tie packaging design to cost outcomes for producers.[2]Markku Björkman, “EU Clears Paper Industry Mega Merger,” PULPAPERnews, pulpapernews.com The United Kingdom’s move toward modulated disposal fees in 2026-2027 shows how quickly carton design decisions are becoming financial decisions rather than optional sustainability choices. Germany remains a large national center because of its scale, recycling discipline, and links to multinational packaging buyers, while lower-cost converting locations in Eastern Europe continue to gain relevance for cost-sensitive production.

South America and Middle East and Africa are smaller in total size, but they remain strategically important to the printed cartons market because they offer space for regional capacity expansion and category-specific growth. Brazil anchors South American demand through food and beverage exports, organized retail growth, and a broad FMCG packaging base. Smurfit Westrock’s acquisition of Cartomanabí in Ecuador in March 2026 showed that major suppliers still see South America as an active corrugated growth platform.[3]Simon Matthis, “Smurfit Westrock Expands Its Presence in Ecuador,” PULPAPERnews, pulpapernews.com In Middle East and Africa, Gulf markets are investing in modern retail-ready packaging, while pharmaceutical traceability and compliance demands are raising the need for higher-specification cartons in parts of Africa.

Competitive Landscape

The printed cartons market remains moderately consolidated, with Smurfit Westrock, International Paper, Mayr-Melnhof Karton, Mondi, and Graphic Packaging together accounting for 40-45% of global revenue. That level of concentration gives leading groups meaningful scale advantages, but it still leaves a large share of the printed cartons market in the hands of regional converters and niche specialists that compete on speed, depth of certification, and customer proximity. International Paper’s USD 9.9 billion acquisition of DS Smith marked one of the clearest consolidation moves in the sector, and the European Commission approved the deal in April 2026, subject to divestitures in France, Portugal, and Spain. International Paper also announced plans to create 2 independent public companies, with an EMEA entity expected to operate under the DS Smith name after separation.[4]International Paper, “International Paper to Create Two Independent Public Companies,” Nasdaq, nasdaq.com These moves show that fiber integration, geographic fit, and regulatory positioning now matter as much as plant count in shaping leadership across the printed cartons market.

Graphic Packaging provided another example of how large suppliers are defending their position through innovation and scale. The company reported Q1 2026 net sales of USD 2,156 million, recorded USD 42 million in innovation sales growth, and filed 13 new patents, expanding its active patent base to nearly 3,100. Smurfit Westrock’s expansion in Ecuador also reflected a regional strategy built around corrugated strength, geographic density, and access to growing demand in South America. Stora Enso’s board investments and product launches point in a different direction, with a focus on premium cartonboard grades for pharmaceutical, food, and personal care converters. Together, these moves show that the printed cartons market is not consolidating around one playbook, but around a mix of integration, innovation, regional expansion, and higher-value substrate capability.

Open opportunities remain meaningful despite this consolidation because no small group of companies controls a dominant majority of the printed cartons market. One area of opportunity is turnkey pharmaceutical serialization support, where converters can combine carton production with data aggregation and compliance services for regulated customers. Another is e-commerce packaging development, where buyers increasingly want cartons designed around scannability, RFID readiness, and reduced fulfillment friction. A third is food packaging conversion using PFAS-free barrier systems, where suppliers such as Amcor, Metsä Group, and other material developers are supporting fiber-based formats that can meet food performance needs without losing recyclability. Barriers to entry remain real because certifications such as ISO 15378 and ISO 22000, along with customer qualification cycles in regulated applications, continue to favor established operators with proven systems and long-standing customer trust.

Printed Cartons Industry Leaders

Smurfit Westrock plc

Graphic Packaging Holding Company

International Paper Company

Stora Enso Oyj

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Graphic Packaging Holding Company reported Q1 2026 net sales of USD 2,156 million, filed 13 new patents, expanding its portfolio to approximately 3,100 patents, and committed to USD 60 million in structural cost reductions including a workforce reduction of over 500 roles.

- April 2026: Prinzhorn Group acquired Stora Enso's corrugated packaging businesses in Germany, Gaster Wellpappe, Wellpappe Sausenheim, and PTI, comprising 350 employees and EUR 74 million (USD 84 million) in 2025 revenue.

- April 2026: The European Commission approved International Paper's acquisition of DS Smith, subject to divestitures of box plants in France, Portugal, and Spain to address competition concerns.

- March 2026: Smurfit Westrock acquired Cartomanabí, an Ecuadorian corrugated packaging producer with annual capacity exceeding 50,000 tonnes, reinforcing its position as the largest corrugated packaging supplier in South America and extending geographic reach across the region.

Global Printed Cartons Market Report Scope

The scope of the report includes an analysis of the printed cartons market, which refers to the industry that produces and distributes cartons with printed designs, logos, or information. The study examines market trends, growth drivers, challenges, and opportunities, providing insights into the forecast period and the competitive landscape.

The Printed Cartons Market Report is Segmented by Product Type (Folding Cartons, Printed Corrugated Cartons, and Rigid Setup Cartons), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and More), End-User (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and More), Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Folding Cartons |

| Printed Corrugated Cartons |

| Rigid Setup Cartons |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Folding Cartons | ||

| Printed Corrugated Cartons | |||

| Rigid Setup Cartons | |||

| By Printing Technology | Lithographic Printing | ||

| Flexographic Printing | |||

| Digital Printing | |||

| Gravure Printing | |||

| Other Printing Technologies | |||

| By End-User Industry | Food and Beverage | ||

| Healthcare/Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Electrical and Electronics | |||

| Household and Industrial Goods | |||

| Tobacco | |||

| E-commerce and Retail-ready Packaging | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and forecast for printed cartons?

The printed cartons market size was USD 417.61 billion in 2025 and is forecast to reach USD 598.71 billion by 2031, growing at a 6.19% CAGR during 2026-2031.

Which product category leads demand for printed cartons?

Folding cartons led the market with a 43.36% share in 2025 and are also expected to be the fastest-growing product type through 2031 at a 6.84% CAGR.

Why is pharmaceutical demand important for carton converters?

Pharmaceutical packaging requires serialization, tamper evidence, and dependable print quality, which supports demand for higher-specification cartons and more stable long-term supply relationships.

Which region is expected to grow the fastest for printed cartons?

Asia-Pacific is both the largest regional market and the fastest-growing one, with a 39.14% share in 2025 and a projected 7.13% CAGR through 2031.

What is driving digital printing adoption in carton packaging?

Brands are launching more regional variants, seasonal packs, and variable-data formats, which makes digital printing more attractive for short runs and faster turnaround than traditional long-run methods.

What are the main risks affecting carton suppliers?

Raw material and energy volatility, competition from flexible packaging, and changing EPR-linked packaging costs are the main pressures shaping margins and design decisions.

Page last updated on: