North America Automatic Carton Erector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

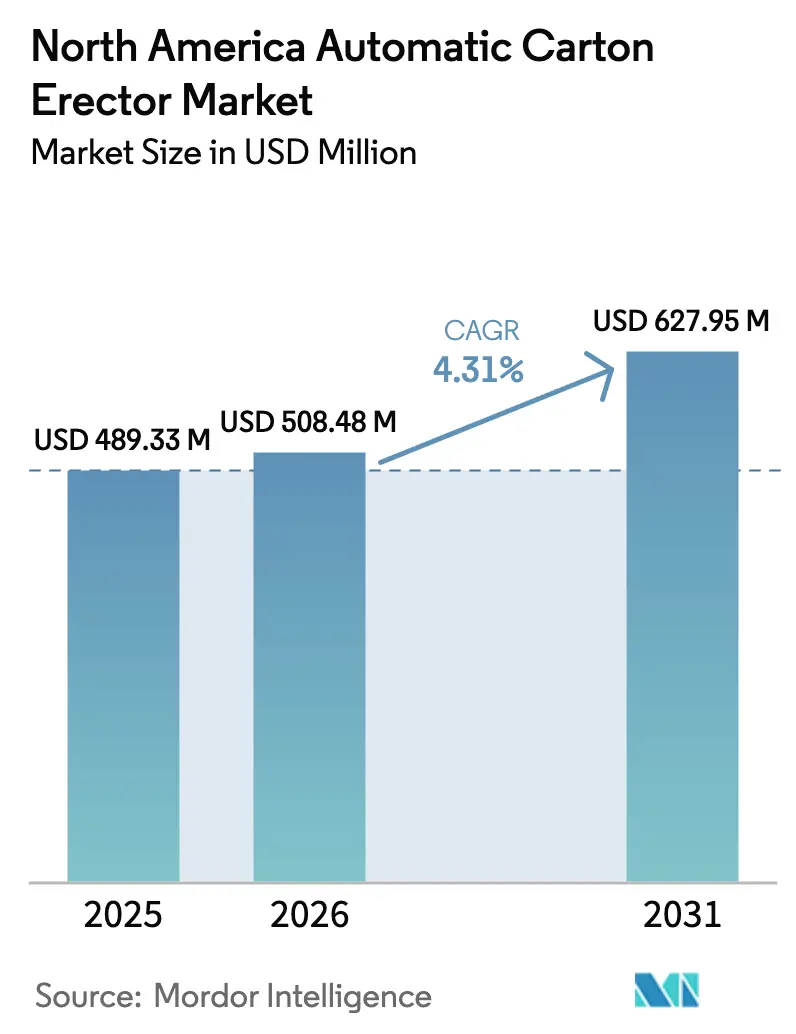

| Base Year Market Size (2025) | USD 489.33 Million |

| Market Size (2026) | USD 508.48 Million |

| Market Size (2031) | USD 627.95 Million |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

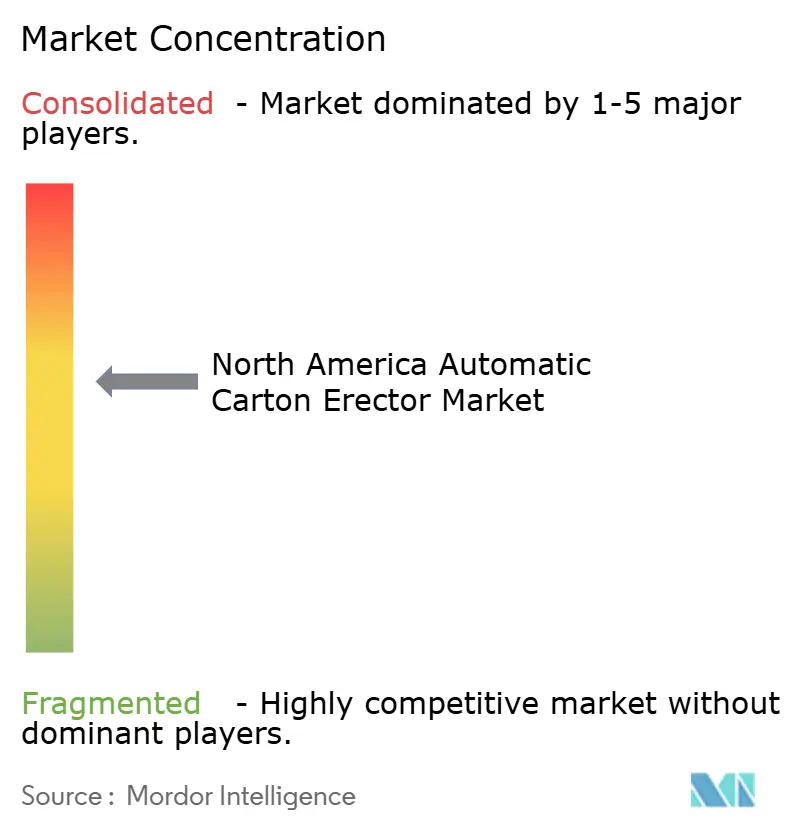

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automatic Carton Erector Market Analysis by Mordor Intelligence

The North America automatic carton erector market size is expected to increase from USD 489.33 million in 2025 to USD 508.48 million in 2026 and reach USD 627.95 million by 2031, growing at a CAGR of 4.31% over 2026-2031. Expanding e-commerce footprints, double-digit rises in warehouse wages, and stricter food-safety mandates collectively steer procurement budgets toward automated case forming. Finance teams now calculate 18- to 24-month payback horizons as labor represents nearly one-third of end-of-line packaging cost, while 40%–50% wage inflation since 2019 accelerates automation justification. Vendors face fewer technology barriers because vision-guided robotics, servo motion, and modular frames have become standard offerings, so competitive advantage shifts to pre-wired, quick-install packages that minimize engineering lead time. Deeper capital scrutiny inside legacy food plants tempers the overall growth pace because electrical upgrades, floor-leveling, and fire-code retrofits can double installed cost when retrofitting 30-year-old buildings. Key adoption differentials surface across segments. Regular slotted case (RSC) formats still dominate because they handle 70%–80% of corrugated shipping volume, yet retailers’ dimensional-weight surcharges spur faster uptake of tray formers and wraparound styles. Mid-tier 20-40 carton-per-minute (CPM) machines account for two-fifths of 2025 revenue because they match throughput on most frozen food, pharma, and contract-packaging lines; however, >40 CPM systems are gaining share in beverage and snack operations that now run three shifts during seasonal peaks. Fully automatic platforms comprise almost two-thirds of 2025 installations, but their growth is gated by the scarcity of technicians who can maintain servo drives, vision cameras, and PLC code. Geography again shapes ROI; the United States controls more than four-fifths of 2025 sales, Canada emerges as the fastest grower through 2031 on the back of greenfield fulfillment hubs, and Mexico is a nearshoring wild card whose upside depends on service-network reach and wage-cost trajectories.

Key Report Takeaways

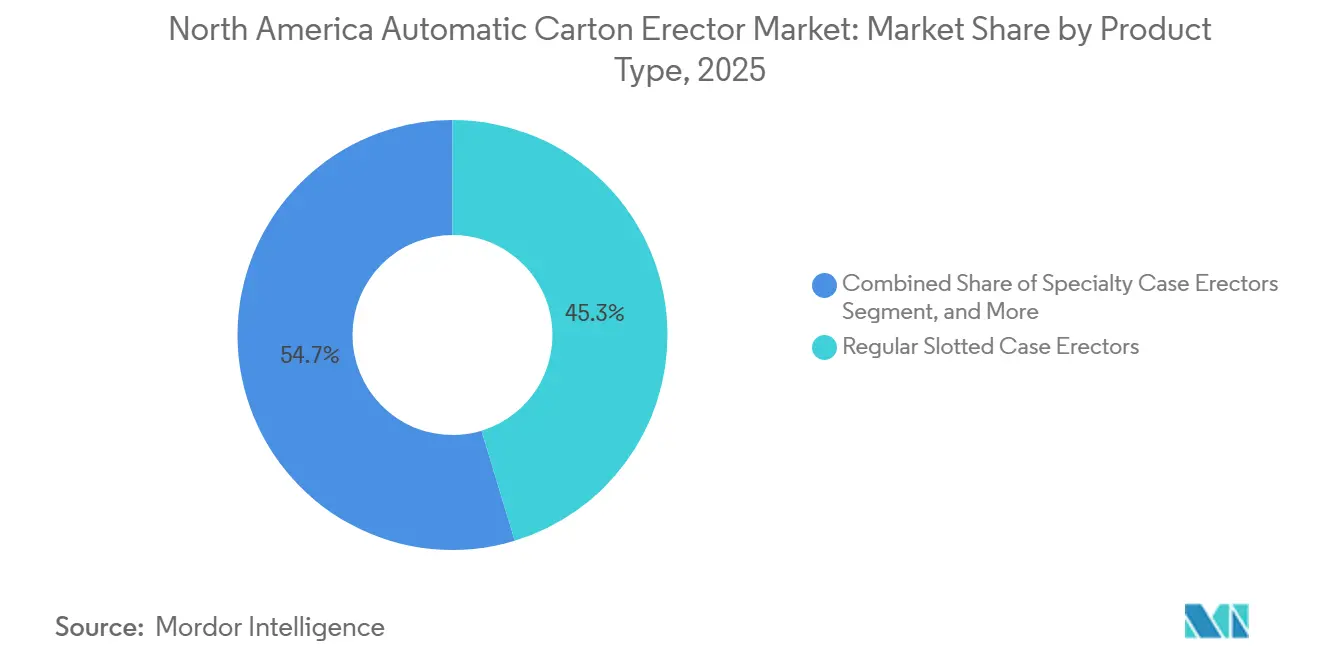

- By product type, regular slotted case erectors led with 45.32% of the North America automatic carton erector market share in 2025, while specialty formats are forecast to expand at a 5.34% CAGR through 2031.

- By speed band, 20-40 CPM systems captured 40.21% of the North America automatic carton erector market size in 2025; machines exceeding 40 CPM are projected to grow at 5.53% between 2026-2031.

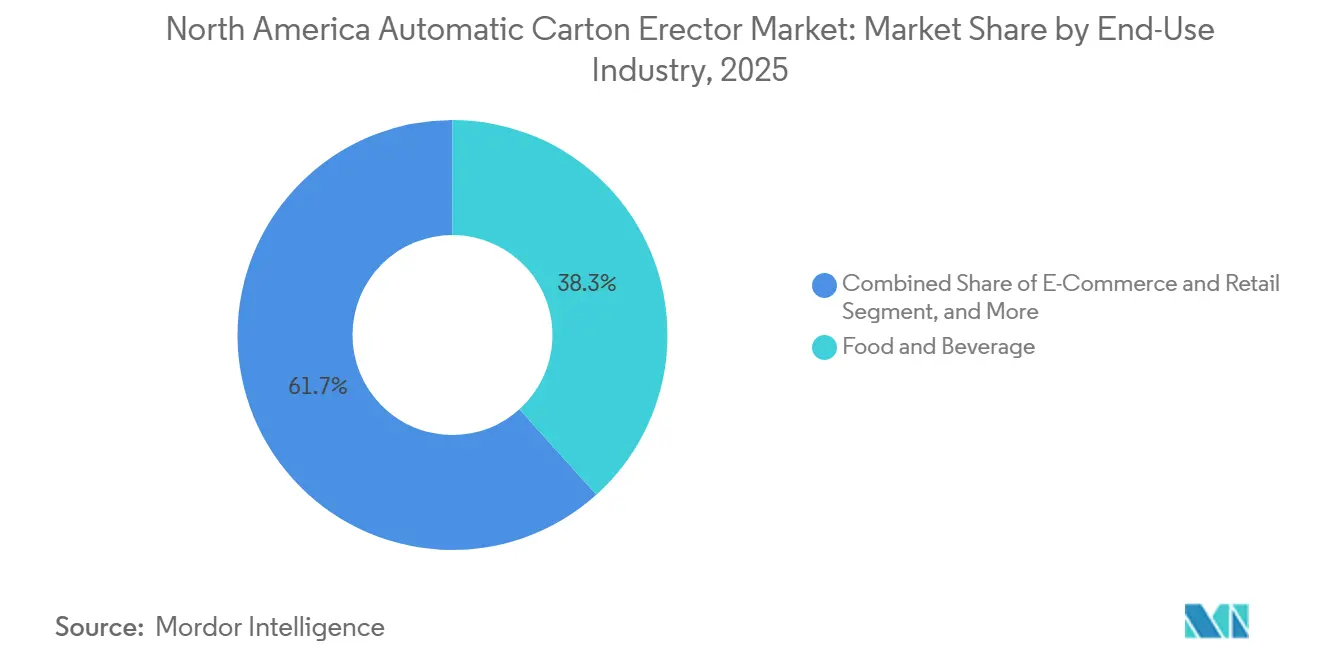

- By end-use industry, food and beverage dominated with 38.34% of the market share in 2025, whereas e-commerce and retail applications are advancing at a 5.88% CAGR through 2031.

- By automation level, fully automatic units held 64.43% of the North America automatic carton erector market share in 2025, and this segment is on track for a 5.71% CAGR through 2031.

- By country, the United States accounted for 80.32% of the market share in 2025, and Canada is forecast to register the highest country-level CAGR of 5.98% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Automatic Carton Erector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in E-Commerce Fulfillment Centers | +1.2% | United States and Canada, spillover into Mexico | Medium term (2-4 years) |

| Rising Labor Costs Prompting Automation | +1.0% | North America-wide, high-wage metro areas | Short term (≤ 2 years) |

| Stricter Food Safety Packaging Regulations | +0.8% | United States and Canada, FDA and CFIA jurisdictions | Long term (≥ 4 years) |

| Integration of Vision-Guided Robotics | +0.7% | United States, early automotive and pharma clusters | Medium term (2-4 years) |

| Shift Toward Recyclable Corrugated Materials | +0.6% | North America-wide | Long term (≥ 4 years) |

| Adoption of Plug-and-Play Modular Machines | +0.5% | United States and Canada, small and medium enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Boom in E-Commerce Fulfillment Centers

Online retailers embed automatic erectors inside greenfield distribution hubs to eliminate 8- to 12-second manual case assembly steps, sustaining throughput targets above 1,000 units per hour.[1]Walmart Canada, “Supply Chain Investment Announcement,” WALMARTCANADA.CA Walmart Canada’s USD 6.5 billion Vaughan and Calgary nodes integrate carton forming with high-density storage, while Amazon’s 2.8 million square-foot YYC4 site runs robotic picking that depends on pre-erected cartons.[2]Amazon, “Calgary Fulfillment Center YYC4 Opening,” ABOUTAMAZON.COM Micro-fulfillment specialists such as Metro Supply Chain pair AutoStore cubes with compact erectors, pushing order-to-ship cycles under 30 minutes.[3]Metro Supply Chain, “Brampton AutoStore Installation,” METROSUPPLYCHAIN.COM Distributed networks multiply the number of required machines even when single-site volumes drop, favoring modular, plug-and-play formats that forklift into position and wire up in hours rather than days.

Rising Labor Costs Prompting Automation Adoption

Average warehouse wages reached USD 18.99 per hour in Q2 2024, a 40%-50% jump since 2019, compressing carton-erector payback periods to 18-24 months. High turnover magnifies savings; each replacement costs firms USD 3,500 in recruiting and onboarding, repeating every 8-12 months in many distribution centers. Contract logistics providers reshoring operations from Asia enter labor-scarce markets where unemployment hovers near record lows, leaving automation as the only scalable path. Nonetheless, only 13% of surveyed warehouses report full packaging automation because upstream palletizing and downstream labeling must be modernized in parallel.

Stricter Food Safety Packaging Regulations

The U.S. FDA Food Safety Modernization Act requires stainless-steel frames, tool-free teardown, and IP69K-rated motors on any equipment in indirect food contact. Health Canada mirrors these rules, mandating materials that neither leach contaminants nor alter organoleptic properties. Compliance lifts unit prices by 15%-20% yet shields suppliers that invested early in sanitary design. Recalls linked to listeria or salmonella can exceed USD 50 million in direct cost, making incremental capital negligible versus brand-protection value. Vendors now bundle NSF-certified lubricants and adhesive systems, further tightening supply chains but raising switching costs for end users.

Integration of Vision-Guided Robotics

3D cameras and machine-vision software let erectors accept mixed-size blanks without mechanical changeovers, slashing setup from 45 minutes to under 10 minutes. Delkor’s V Series tray former hits 35 units per minute, a 40% lift over pneumatic predecessors, while simultaneously self-correcting ±2 mm board-tolerance drift. Pharmaceutical contract packagers use embedded vision to verify 2D matrix codes at erection, eliminating downstream inspection stations. The obstacle remains cost; vision packages add USD 30,000-USD 50,000 per machine, and many plants still run legacy erectors with a decade of service life.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure | -0.6% | North America-wide, acute for small and medium enterprises | Short term (≤ 2 years) |

| Skilled Technician Shortage for Maintenance | -0.5% | United States and Canada, rural manufacturing regions | Medium term (2-4 years) |

| Limited Floor Space in Legacy Facilities | -0.4% | United States, older Northeast and Midwest plants | Long term (≥ 4 years) |

| Supply Chain Volatility of Corrugated Board | -0.3% | North America-wide, kraft-paper disruptions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

Entry-level semi-automatic units start near USD 15,000, while fully automatic, vision-equipped platforms exceed USD 100,000, a hurdle for food processors operating on single-digit margins. Total installed cost doubles after accounting for blank feeders, downstream sealers, and system integration, stretching ROI beyond 36 months when plants run only one shift. Leasing models remain nascent in packaging machinery, forcing firms to draw on working-capital lines priced above 7% interest in 2024. Contract manufacturers with variable volume commitments hesitate to lock in fixed costs, and many postpone automation until private-equity consolidators roll up multiple sites to achieve scale.

Skilled Technician Shortage for Maintenance

PMMI’s 2024 workforce survey shows 95% of consumer-goods companies cannot find qualified packaging technicians, while only 17% succeed in retraining legacy mechanics. Unplanned downtime on an erector can idle an entire filler-packer-palletizer train, burning USD 5,000-USD 10,000 per hour in lost throughput for beverage lines. Vendors embed remote diagnostics, but these features add USD 10,000-USD 15,000 and require reliable broadband that many rural plants lack. Community colleges have not scaled curricula fast enough, and oil-and-gas salaries often lure away the limited talent pool even in apprenticeship-friendly Canada.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Formats Gain Traction Amid E-Commerce Demands

Regular slotted case erectors accounted for 45.32% of the market share in 2025, underscoring their entrenched role in pallet-optimized shipping lanes, yet their growth aligns with the overall North America automatic carton erector market. Specialty case erectors is projected to outpace the baseline at 5.34% because right-sized packaging trims dimensional-weight fees that erode digital-retail margins. Tray formers serve fresh produce and ready-meal sectors that need airflow and shelf visibility, while tablock designs remove adhesive, lowering consumables budgets and improving curbside recyclability. Wraparound styles offer billboard-quality graphics for warehouse-club aisles, but they require precision product loading and intolerance for SKU variances, increasing the importance of integrated robotics.

Vision-guided systems now enable sub-10-minute tool-free changeovers, making mixed-format production economical at batch sizes below 500. Combi’s Ergopack 2.0, capable of switching between RSC and tray within minutes, answers multi-SKU demands in grocery e-commerce fulfillment. Pharmaceutical and nutraceutical contract packers add tamper-evident inserts during erection, leveraging specialty formats for compliance as well as marketing. The shift toward sustainability reinforces the trend, since wraparounds and trays often reduce corrugated usage by 10%-15%, supporting corporate ESG scorecards.

By Speed Band: High-Throughput Systems Address Labor Scarcity

Systems rated 20-40 CPM captured 40.21% of the market share in 2025, aligning with the North America automatic carton erector market size requirements of frozen food, OTC pharma, and contract-packaging lines that balance volume with frequent changeovers. Sub-20 CPM machines persist in artisan and clinical-trial environments where manual assembly still pencils out. Equipment above 40 CPM is forecast to grow 5.53%, driven by beverage, snack, and same-day-delivery fulfillment centers whose uptime economics demand automated forming.

Schneider’s servo-driven platform hits 60 CPM while still fitting a 12-foot footprint, enabling Labor Day beverage promotions without adding temporary workers. The ROI accelerates in continuous 2- or 3-shift plants; a 60 CPM erector running 20 hours daily erects 72,000 cases, eliminating four to five operators and recouping capital in 12-15 months. The constraint lies upstream, and downstream case sealers, packers, and palletizers must match speed, often bumping system budgets toward USD 0.5-0.75 million.

By End-Use Industry: E-Commerce Outpaces Traditional Segments

The food and beverage segment accounted for 38.34% of the market share in 2025, driven by sanitary design regulations and line speeds above 40,000 bottles per hour, which create a natural pull for automation. Dairy and ready-meal plants favor stainless-steel IP69K frames that tolerate caustic washdown cycles mandated by FDA preventive controls. Conversely, the e-commerce and retail segment grows fastest at 5.88%, as grocery, apparel, and electronics sellers deploy multi-node fulfillment networks that require right-sized cartons per order. Each percentage-point rise in e-commerce penetration translates to millions of additional cartons annually, cementing the segment’s outperformance.

Pharmaceutical contract packers adopt high-spec machines with integrated serialization, driving premium pricing but lower volume share. Industrial goods lag because reusable totes replace one-way corrugated shipments, though nearshored electronics assembly may spark incremental demand. Overall, end-use appetite traces back to throughput variability; high-volume lines value speed, whereas high-mix operations prioritize changeover flexibility.

By Automation Level: Fully Automatic Systems Dominate Despite Skills Gap

Fully automatic erectors represented 64.43% of the market share in 2025 and is projected to grow at 5.71%, eclipsing semi-automatic alternatives in the North America automatic carton erector market. A single technician can monitor two to three fully automatic machines erecting 40-50 cases per minute each, whereas semi-automatic options peak at half that speed and require dedicated operators. Yet skill shortages mute adoption velocity; facilities lacking PLC-savvy mechanics hesitate to introduce servo-laden equipment they cannot easily maintain.

Suppliers respond with augmented-reality maintenance glasses and predictive dashboards that forecast failures 72 hours early, but connectivity and cost remain hurdles. Semi-automatic platforms stay relevant for short-run co-packers and seasonal operations where labor can be redeployed when lines stop. Over the forecast period, workforce development programs and remote-support ecosystems will dictate how quickly fully automatic penetration accelerates versus plateauing near current two-thirds share.

Geography Analysis

The United States held 80.32% of the market share in 2025, reflecting its dense concentration of food processors in the Midwest, beverage bottlers in the Southeast, and more than 1,500 e-commerce fulfillment centers across major metros. Plant footprints routinely exceed 500,000 square feet, run three shifts, and therefore justify six-figure investments in fully automatic equipment that elevate overall equipment effectiveness above 85%. FDA sanitary-design rules create a nationwide compliance baseline that simplifies vendor qualification but raises entry-level prices, thereby reinforcing preference for suppliers with deep after-sales networks. Moderate fragmentation persists among domestic OEMs; however, consolidation is noticeable at the top where ProMach, Syntegon, and Pearson capture multi-line turnkey projects through bundled warranties and integrated controls.

Canada is forecast to expand at 5.98% CAGR from 2026-2031, the fastest rate within the North America automatic carton erector market. Walmart’s USD 6.5 billion supply-chain expansion and Amazon’s YYC4 mega-site anchor a greenfield wave free from legacy floor-space constraints, permitting line layouts optimized for robotics and quick-changeover carton forming. Labor costs in Toronto and Vancouver now rival many U.S. metros, accelerating automation ROI, while Health Canada imposes packaging-material rules mirroring FDA language, ensuring U.S.-spec machinery fits seamlessly north of the border. The country’s challenge is geographic dispersion; a population of 40 million spread over 10 provinces forces retailers into distributed micro-fulfillment nodes, each demanding compact, plug-and-play erectors rather than one mega-plant.

Mexico captures a modest slice today yet enjoys tailwinds from nearshoring electronics, automotive, and appliance assembly. Cross-border suppliers transplant U.S. packaging standards to Monterrey, Querétaro, and Tijuana corridors to secure duty-free status under the United States-Mexico-Canada Agreement. Wage inflation along border maquiladoras narrows the historical labor-cost gap, but eight-day ocean voyages from Asia versus two-day trucking from Mexico preserve the strategic logic. OEMs must expand Spanish-language technical service and stock local spares to unlock faster growth, decisions that tilt in favor of global players with regional hubs.

Competitive Landscape

At the value end, the North America automatic carton erector market remains moderately fragmented, with Econocorp, ADCO Manufacturing, and EndFlex pushing USD 15,000-USD 35,000 semi-automatic units into single-shift bakeries and co-packers. Higher up, the field consolidates as ProMach, Syntegon, Pearson, and Schneider bundle erectors with case packers, sealers, stretch wrappers, and palletizers under one PLC, de-risking system integration for buyers and locking in aftermarket parts streams that exceed equipment margin over a decade. Moderate overall concentration allows niche brands to win share through specialized footprints or tray-forming expertise, yet scale players increasingly deploy M&A to fill technology gaps.

ProMach’s December 2024 acquisition of Zalkin widened its capping and sealing bench, enabling turnkey wet-line cells commissioned in under two weeks, while Syntegon’s January 2025 purchase of Harro Höfliger imported European serialization know-how into North American pharma accounts. Schneider integrates 3D vision on fold bars to auto-tune glue-lap angles on the fly, a feature that resonates with snack makers running mixed board suppliers. Delkor’s V Series leverages vision-guided pick-and-place arms to erect trays at 35 CPM, a 40% jump over pneumatic predecessors and a differentiator for fresh-cut produce packhouses.

Skill shortages create a services battleground; 95% of consumer-goods producers report hiring challenges, so OEMs that embed remote diagnostics, AR goggles, and subscription-based predictive maintenance win mindshare. Compliance adds another vector; machines surpassing PMMI ANSI B155.1 by adding light curtains and two-hand controls fetch premiums in pharma and infant-formula factories. Ultimately, market power flows to vendors that compress design-to-ship lead times, arrive with pre-wired skids, and commission in days rather than months.

North America Automatic Carton Erector Industry Leaders

ProMach Inc.

Syntegon Technology GmbH

Combi Packaging Systems LLC

Pearson Packaging Systems LLC

Lantech LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Schneider Packaging Equipment unveiled an AI-enabled predictive maintenance suite that analyzes vibration, temperature, and cycle-time data, forecasting component failures 72 hours in advance; beta trials begin Q2 2026 with beverage customers.

- February 2026: ADCO Manufacturing secured a USD 3.2 million order from a Canadian frozen-food producer for cold-room-rated automatic erectors designed to operate at -10 °F.

- January 2026: Econocorp launched the Econocaser EC-50, a USD 28,000 compact erector producing 25 cases per minute within a 48-inch-by-36-inch footprint, aimed at artisan food companies.

- November 2025: Lantech committed USD 15 million to expand its Louisville campus, adding lines that integrate stretch wrapping with case forming on a single chassis.

North America Automatic Carton Erector Market Report Scope

The North America Automatic Carton Erector Market refers to the industry focused on the production, distribution, and utilization of machines designed to automatically form and erect cartons or boxes for packaging purposes. These machines are widely used across various industries to enhance efficiency and reduce manual labor in packaging operations.

The North America Automatic Carton Erector Market Report is Segmented by Product Type (Regular Slotted Case Erectors, Tablock Case Erectors, Tray Forming Erectors, and Specialty Case Erectors), Speed Band (Up to 20 CPM, 20-40 CPM, and Above 40 CPM), End-Use Industry (Food and Beverage, E-Commerce and Retail, Pharmaceuticals, Industrial Goods, and Other End-Use Industries), Automation Level (Semi-Automatic, and Fully Automatic), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Regular Slotted Case Erectors |

| Tablock Case Erectors |

| Tray Forming Erectors |

| Specialty Case Erectors |

| Up to 20 CPM |

| 20-40 CPM |

| Above 40 CPM |

| Food and Beverage |

| E-Commerce and Retail |

| Pharmaceuticals |

| Industrial Goods |

| Other End-Use Industries |

| Semi-Automatic |

| Fully Automatic |

| United States |

| Canada |

| Mexico |

| By Product Type | Regular Slotted Case Erectors |

| Tablock Case Erectors | |

| Tray Forming Erectors | |

| Specialty Case Erectors | |

| By Speed Band (Cartons per Minute) | Up to 20 CPM |

| 20-40 CPM | |

| Above 40 CPM | |

| By End-Use Industry | Food and Beverage |

| E-Commerce and Retail | |

| Pharmaceuticals | |

| Industrial Goods | |

| Other End-Use Industries | |

| By Automation Level | Semi-Automatic |

| Fully Automatic | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How fast is the North America automatic carton erector market expected to grow to 2031?

It is forecast to rise from USD 508.48 million in 2026 to USD 627.95 million by 2031, reflecting a 4.31% CAGR.

Which product style is gaining share the quickest?

Specialty formats such as trays, tablock, and wraparound cases are projected to expand at 5.34% annually through 2031, outpacing RSC styles.

Why are Canadian installations growing faster than U.S. ones?

Canada is adding greenfield e-commerce and grocery fulfillment centers that adopt automation from day one, driving a 5.98% CAGR for the period.

What is the biggest obstacle to wider adoption of fully automatic erectors?

A shortage of technicians skilled in PLC, servo, and vision systems limits deployment even when ROI metrics are favorable.

How do labor costs influence payback periods?

Warehouse wages that climbed 40%-50% since 2019 cut payback horizons for automatic erectors to 18-24 months in many high-wage metro areas.

Which speed class offers the highest growth outlook?

Platforms exceeding 40 CPM are set for a 5.53% CAGR as beverage, snack, and same-day-delivery operations pursue high throughput with limited labor.

Page last updated on: