Market Overview

| Study Period | 2020 - 2031 |

|---|---|

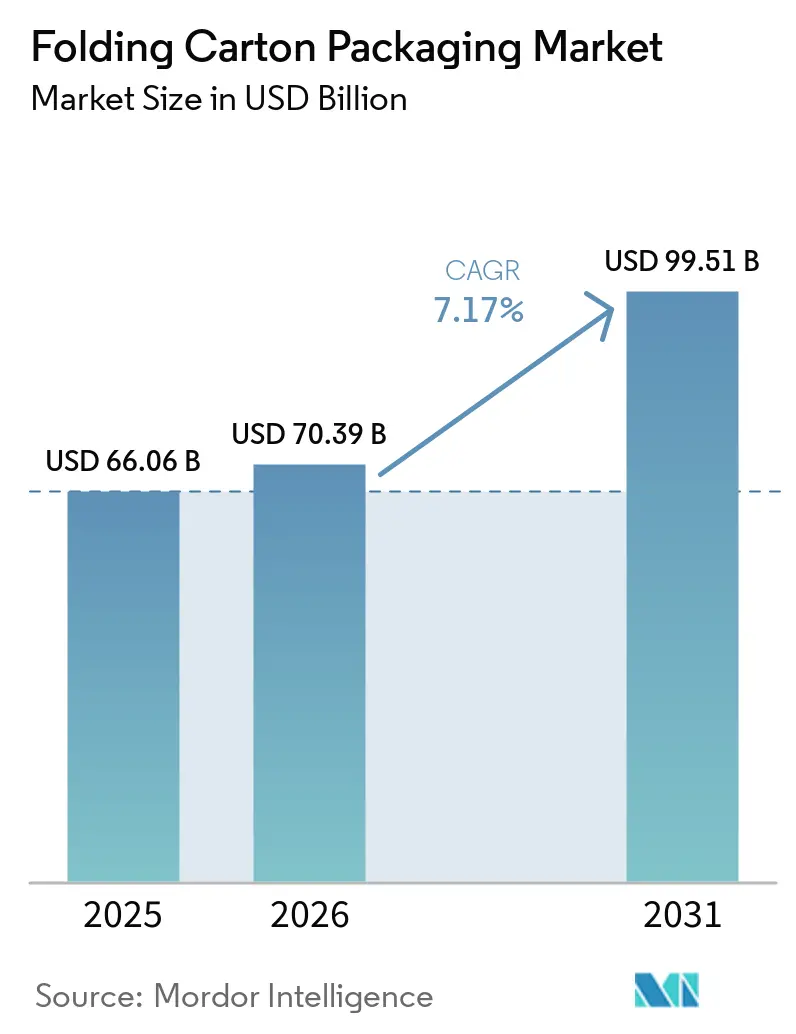

| Market Size (2026) | USD 70.39 Billion |

| Market Size (2031) | USD 99.51 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

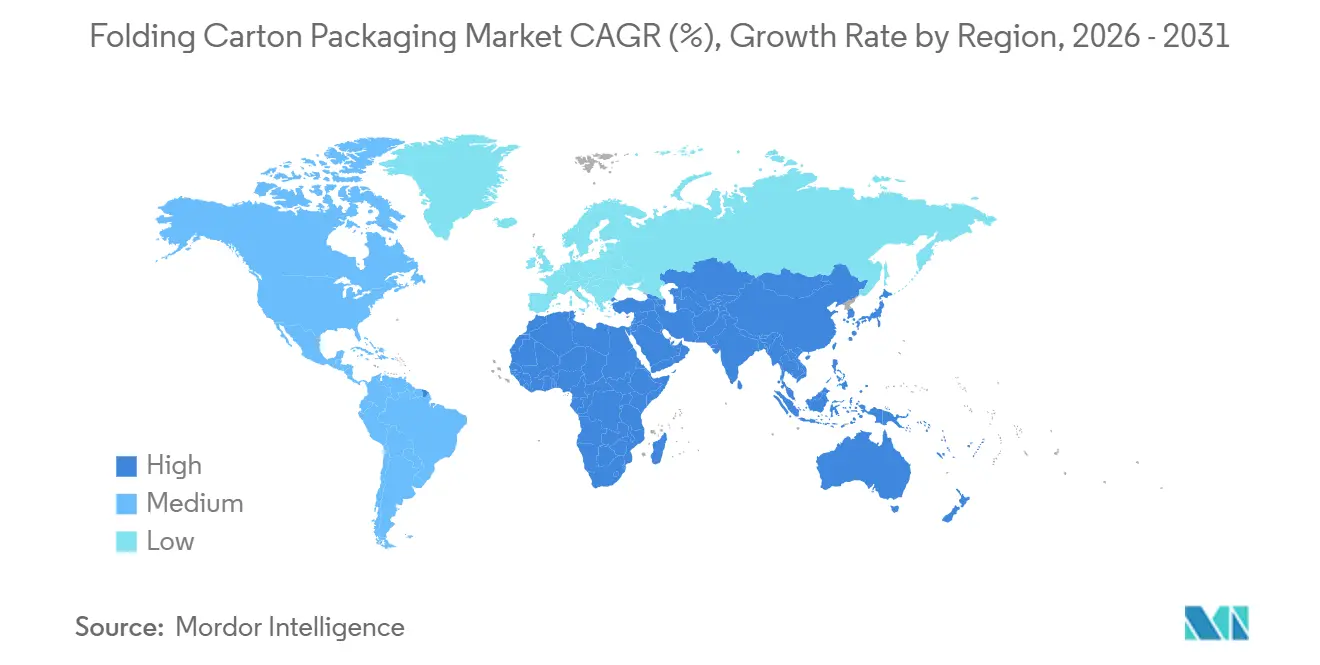

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Folding Carton Packaging Market Analysis by Mordor Intelligence

The folding carton packaging market size is expected to increase from USD 66.06 billion in 2025 to USD 70.39 billion in 2026 and reach USD 99.51 billion by 2031, growing at a CAGR of 7.17% over 2026-2031. Capacity additions across Asia-Pacific and Europe are supporting this rise in supply, while food processing industrialization and retail-ready distribution formats are supporting steady offtake. The folding carton packaging market is also benefiting from brand-owner efforts to replace single-use plastics with recyclable paperboard formats, which is shifting specification choices in favor of cartons across several packaged goods categories. Competitive conditions remain active because large integrated board producers are investing in automation, digital workflows, and certified supply chains, while smaller converters continue to face margin pressure from raw material volatility. Over the forecast period, the folding carton packaging market is likely to reward producers that can combine scale, compliance readiness, and short-run customization without losing cost discipline.

Key Report Takeaways

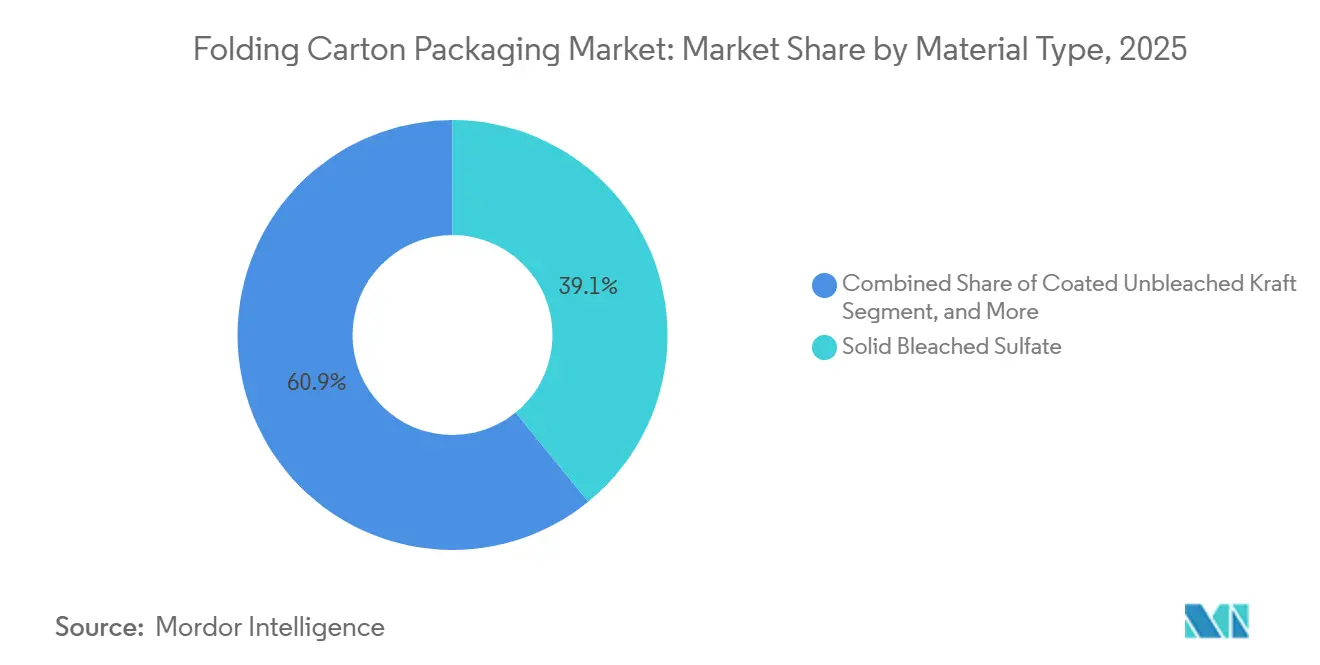

- By material type, solid bleached board captured with 39.13% of the folding carton packaging market share in 2025.

- By printing technology, the folding carton packaging market size for digital printing is projected to grow at a 8.34% CAGR to 2031.

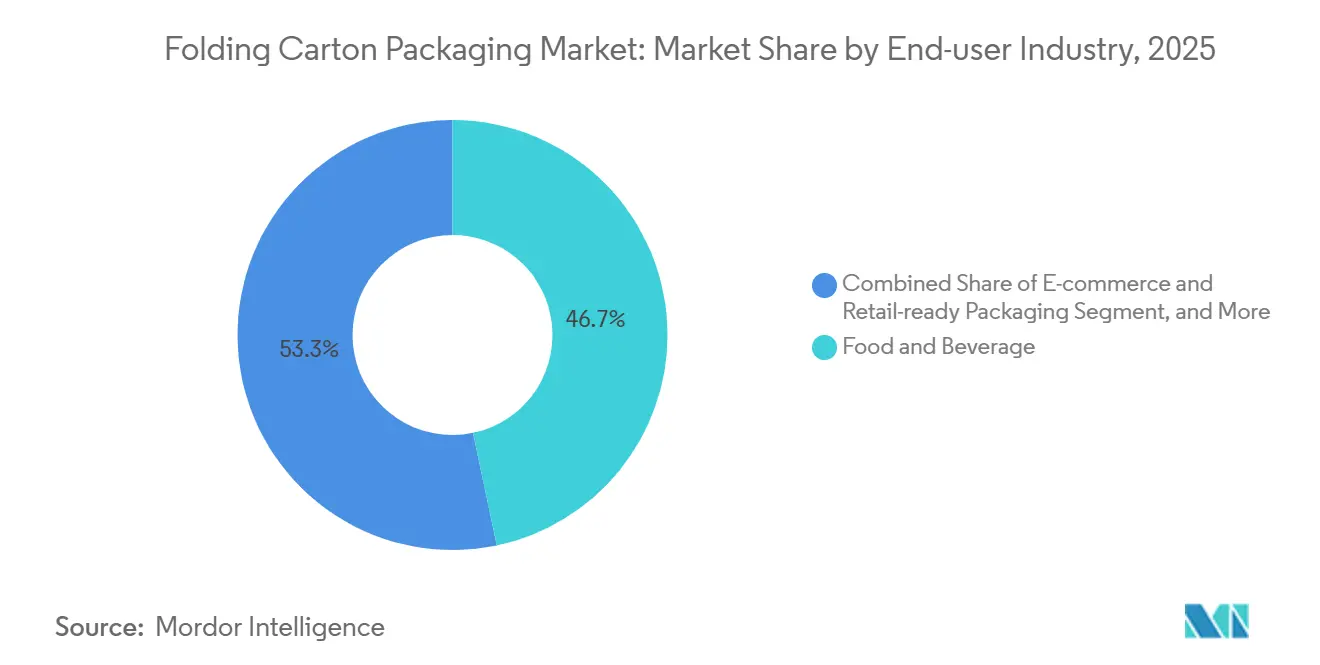

- By end-user industry, the food and beverage industry captured 46.71% of the folding carton packaging market share in 2025.

- By geography, the folding carton packaging market size for Asia-Pacific is projected to grow at a 8.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Folding Carton Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Food and Beverage Processing Sector | +2.0% | Global | Short term (≤ 2 years) |

| Growth Of E-commerce Packaging Demand | +1.6% | Global, Asia-Pacific-led | Short term (≤ 2 years) |

| Rising Demand for Sustainable Packaging Solutions | +1.2% | Europe and North America | Medium term (2-4 years) |

| Increased Adoption of Digital Printing for Short-run Cartons | +0.8% | North America and Europe | Medium term (2-4 years) |

| Government Excise Tax on Plastic Packaging Spurring Shift Toward Paperboard | +0.5% | Europe and North America | Short term (≤ 2 years) |

| Rapid Growth of Cloud Kitchen and Meal-kit Start-ups Requiring Small-batch Cartons | +0.3% | Asia-Pacific and Middle East, and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of the Food and Beverage Processing Sector

The food and beverage processing sector remains the largest demand anchor for the folding carton packaging market. Capacity additions across Southeast Asia, India, and sub-Saharan Africa are driving fresh carton procurement demand rather than simply replacing existing volumes. Demand is also moving toward barrier-coated and aseptic formats, which means the folding carton packaging market is seeing a stronger pull toward higher-value substrates rather than just standard bleached board. Smurfit WestRock plc reported FY2025 net sales of USD 31.18 billion, with food and beverage conversion volumes continuing to support its scale in paper-based packaging, which reinforces the sector's central role in carton demand.[1]Smurfit WestRock plc, “Annual Report And Financial Statements 2025,” Smurfit WestRock, smurfitwestrock.com Emerging-market processors are still buying more mid-tier grades with basic barrier properties, while European and North American brand owners are specifying certified recyclable premium grades to meet sustainability-related procurement rules.

Growth of E-commerce Packaging Demand

E-commerce logistics are changing packaging requirements across the folding carton packaging market, especially for lightweight cartons that still need enough strength for automated fulfillment handling. Retail-ready packaging is becoming a standard specification in many online and omnichannel supply chains, and this favors converters that can manage multiple SKUs with short production runs. The folding carton packaging market is also being reshaped by the fact that brands now want more design variants in smaller batches, which weakens the old link between high complexity and high volume. Graphic Packaging International LLC launched the Boardio multipack machine in December 2025 to replace plastic multi-can ring holders with paperboard alternatives, a move that aligned directly with brand-owner demand for recyclable and channel-ready formats. Converters that lack digital print capability or short-run economics are at risk of losing share in the folding carton packaging market even when their conventional print quality remains competitive.

Rising Demand for Sustainable Packaging Solutions

Sustainability has moved from brand messaging into formal vendor selection criteria across the folding carton packaging market. Large consumer goods companies now require recyclability thresholds, recycled-content levels, and carbon footprint disclosure when reviewing packaging suppliers, which has improved the position of fiber-based carton formats. The EU Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, requires packaging on the EU market to be recyclable by 2030 and restricts PFAS-containing functional barriers from August 12, 2026, which is accelerating material conversion programs in Europe. Metsä Board published a lifecycle analysis in March 2025 showing that a shift from white-lined chipboard to folding boxboard can reduce the carbon footprint by more than 60% in food packaging applications, providing procurement teams with a quantified basis for moving toward higher-grade paperboard. Stora Enso Oyj inaugurated its Oulu packaging board line in August 2025 as part of a USD 1.3 billion investment, equal to USD 1.24 billion, which shows that integrated producers are building capacity around low-carbon substrate positioning rather than treating compliance as a side issue.

Increased Adoption of Digital Printing for Short-run Cartons

Digital printing is improving short-run carton economics across the folding carton packaging market by eliminating plate costs and making variable-data jobs easier to execute. This matters in categories where brand owners need personalization, regional versions, or serialized packs without committing to long runs. BOBST Group SA reported that its inkjet carton printing platforms are tracking an installation growth rate of 11% through 2030, suggesting that equipment deployment is outpacing the headline growth rate of the digital segment. Smurfit WestRock unveiled its ActiBlu prototype in May 2026, and the system used 60% less adhesive than conventional hot-melt closure methods, demonstrating that digital innovation is now extending into assembly, not just the print stage. Pharmaceutical track-and-trace requirements in the United States and Europe are also supporting the folding carton packaging market by creating steady demand for variable-data carton printing that is less dependent on changing consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Paperboard Prices | -0.9% | Global | Short term (≤ 2 years) |

| Competition From Flexible Packaging Alternatives | -0.7% | Asia-Pacific and Global | Long term (≥ 4 years) |

| Limited Domestic Pulp Production Increasing Import Dependence | -0.4% | Asia-Pacific and South America | Medium term (2-4 years) |

| Power Supply Interruptions Elevating Production Costs For Converters | -0.3% | Africa and South Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility In Paperboard Prices

Input cost volatility remains the most immediate operating risk for the folding carton packaging market. Packaging Corporation of America said North American containerboard prices rose by USD 50 per ton in April 2026, with another announced increase of USD 50-70 per ton for mid-2026, which continued to pressure converting margins. Contract pricing often lags spot input changes by one or two quarters, creating an earnings gap for converters without supply protection or backward integration. Even though NBSK pulp prices in the United States eased by 7.6% to USD 790-860 per metric ton in Q3 2025, rising finished board prices meant that the relief at pulp level did not fully restore downstream margins. Mayr-Melnhof Karton AG reported that its Fit-for-Future program delivered EUR 70 million in savings in FY2025, equivalent to USD 79.1 million, showing that efficiency programs can soften cost shocks but are harder to replicate for fragmented regional converters. As a result, the folding carton packaging market still favors large-scale operators when raw material prices become volatile.

Competition From Flexible Packaging Alternatives

Flexible packaging continues to compete with folding carton packaging in the snacks, dairy, and personal care categories, where barrier performance and pack efficiency drive buying decisions. This substitution pressure is strongest in Asia-Pacific, where flexible film infrastructure is well established, and the pack-cost gap versus heavier paperboard formats still matters. At the same time, the recycling disadvantage of multilayer films is shifting from a weak point in brand perception to a real cost issue under extended producer responsibility systems. Regulation (EU) 2025/40 and related eco-modulation trends are gradually changing the economics of packaging selection by linking regulatory cost more directly to recyclability performance. That change will take time to flow through into purchasing decisions, but the folding carton packaging market is positioned to benefit as compliance costs make comparisons with flexible alternatives less favorable over the longer term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: SBS Anchors Premium Carton Applications

Solid Bleached Sulfate accounted for 39.13% of the folding carton packaging market in 2025 and is projected to grow at a 7.76% CAGR from 2026 to 2031. That combination of scale and above-market growth is unusual in the folding carton packaging market because the leading material also remains one of the most specification-sensitive grades. SBS continues to lead in food-contact and pharmaceutical applications because brightness, print quality, and certification remain essential in those categories. Its surface smoothness supports high-resolution graphics, while its established compliance profile helps multinational brand owners standardize carton specifications across markets.

Folding Boxboard held the second-largest material position in the folding carton packaging market and remained especially important in European tobacco and premium cosmetics applications. Metsä Board stated in March 2025 that folding boxboard can cut the carbon footprint by more than 60% compared with white-lined chipboard in food packaging, which is influencing material selection among brands with climate targets.[2]Metsä Board, “Lifecycle Assessment, Folding Boxboard Vs. White-lined Chipboard In Food Packaging,” Metsä Board, metsaboard.com Coated Unbleached Kraft played a strong role in fast-food and retail-ready packaging due to its stiffness-to-weight ratio and natural look. White Line Chipboard stayed present in price-sensitive cartons such as cereals and detergents, but it is gradually losing ground where coatings reduce recyclability classification.

By Printing Technology: Digital Printing Redefines Short-run Economics

Flexographic Printing held a 39.53% share in 2025, making it the leading production format in the folding carton packaging market. Its position rests on cost efficiency in medium- and high-volume runs, especially in food and beverage cartons, where repeat jobs still dominate plant utilization. Lithographic offset printing also remained important in prestige cosmetics and luxury personal care because it continues to support strong color fidelity and complex embellishment. Gravure printing remained concentrated in high-volume tobacco and food applications, where the cost of cylinder preparation can still be justified by scale.

Digital Printing is forecast to grow at a 8.34% CAGR from 2026 to 2031, placing it ahead of the overall folding carton packaging market. BOBST Group SA said its inkjet-based carton platforms are seeing 11% installation growth through 2030, indicating that adoption at the equipment level is accelerating. Smurfit WestRock's ActiBlu prototype, shown in May 2026, illustrates how digital workflows are now extending into closure and assembly as well as printing. Brand owners in pharmaceutical, luxury, and fast-moving consumer goods applications are increasingly valuing variable-data capability in packaging contracts, and this is giving digitally enabled converters a higher-value position within the folding carton packaging industry.

By End-user Industry: Food And Beverage Drives Volume, E-commerce Fuels Growth

Food and Beverage held 46.71% of the folding carton packaging market share in 2025, which reflected the category's steady consumption base and its high reliance on printed paperboard packaging. The segment also benefits from the global spread of processed foods, ready-to-eat meals, and organized retail distribution, all of which reinforce demand for cartons. Healthcare and Pharmaceuticals remained the second-largest end-user segment as reshoring programs in North America and Europe increased local procurement of serialized, tamper-evident SBS cartons. Personal Care and Cosmetics also supported the folding carton packaging market, especially across South Korea, Japan, and China, where outer packaging remains a visible part of brand presentation.

E-commerce and Retail-ready Packaging is projected to grow at 7.96% CAGR from 2026 to 2031, making it the fastest-growing end-user category in the folding carton packaging market. Retail-ready formats are being adopted because they reduce in-store handling while preserving shelf visibility for fast-moving consumer goods brands. Graphic Packaging International LLC introduced the Boardio multipack machine in December 2025 to support the shift from plastic ring holders toward paperboard-based alternatives, which fits both e-commerce and shelf-ready use cases. Electrical and Electronics, Household and Industrial Goods, and Tobacco still provide a stable base of demand, although tobacco volumes are weakening in Western markets under standardized packaging policies. Household and industrial packaging is also seeing incremental value from QR-code and NFC-enabled carton designs, which adds functionality beyond simple containment and supports broader relevance for the folding carton packaging market.

Geography Analysis

Asia-Pacific accounted for 42.89% of the folding carton packaging market share in 2025 and is forecast to grow at a 8.03% CAGR through 2031. China accounted for 49% of Asia-Pacific demand, supported by food processing modernization, the growth of modern retail, and an e-commerce system that has made retail-ready formats a common requirement. India is the second-largest regional growth engine for the folding carton packaging market, as urbanization, packaged food penetration, and domestic FMCG expansion are all supporting durable demand. Demand in India is also shifting from imported substrates toward more locally supplied mid-grade SBS and FBB grades, reflecting improving domestic packaging capabilities. Sonoco Products Company opened a paper can manufacturing plant in Thailand in March 2026, with a capacity of 200 million units per year, indicating that multinational producers are directing investment toward the region's stronger demand outlook.

North America remained the second-largest region in the folding carton packaging market, but it is currently experiencing softer demand and supply rationalization. Graphic Packaging International LLC announced a global workforce reduction of more than 500 positions in April 2026, signaling an operating adjustment tied to overcapacity and weaker near-term demand rather than a structural decline in carton relevance.[3]Graphic Packaging International LLC, “Workforce Restructuring Announcement,” Graphic Packaging International, graphicpkg.com The region's pharmaceutical and healthcare base still provides consistent demand for higher-value SBS cartons and helps stabilize the mix. International Paper Company completed its USD 7.2 billion acquisition of DS Smith plc in January 2026, which is reshaping paper-based packaging scale and board supply relationships across North America and Europe. South America is benefiting from restrictions on single-use plastics and from rising investment in local food processing, while Brazil continues to anchor the region through its strong fiber base and the scale position of Klabin S.A.

Europe retained a structurally important position in the folding carton packaging market because Germany, France, and the United Kingdom remain core centers for carton demand and converting capacity. Regulation (EU) 2025/40 comes into force from August 12, 2026, and its recyclability and PFAS provisions are strengthening the long-term case for fiber-based cartons across European FMCG supply chains. Stora Enso Oyj inaugurated its Oulu line in August 2025 with a target of 750,000 tonnes per year of near carbon-neutral folding boxboard capacity by 2027, positioning it to capture substitution demand linked to plastic-to-paperboard conversion. The Middle East is still smaller in absolute terms, but retail formalization in the UAE and Saudi Arabia and food processing projects linked to broader economic diversification are supporting new carton demand. Africa remains constrained by import dependence, infrastructure gaps, and unstable power supply, though regional FMCG expansion is still creating incremental opportunities for the folding carton packaging market.

Competitive Landscape

The folding carton packaging market shows moderate concentration at the integrated board level. No single converter holds a dominant global position, but large vertically integrated producers continue to shape pricing, technology standards, and procurement expectations. Smurfit WestRock plc remained in the top tier following the earlier merger of Smurfit Kappa and WestRock, reporting FY2025 net sales of USD 31.18 billion, merger-related sales above USD 400 million, and a USD 7 billion EBITDA target by 2030.[4]Smurfit WestRock plc, “Investor Day Presentation, Medium-term Financial Plan,” Smurfit WestRock, smurfitwestrock.com That scale matters in the folding carton packaging market because large customers increasingly want broad geographic coverage, compliance documentation, and supply assurance from the same vendor.

International Paper's acquisition of DS Smith and Packaging Corporation of America's USD 1.8 billion deal for Greif's containerboard business show that larger players are still using consolidation to improve board access and supply-chain control. At the same time, the folding carton packaging market is not closing off opportunities for specialized converters. Edelmann GmbH and Autajon Group remain relevant in pharmaceutical and luxury carton markets because technical qualification, print quality, and regulatory compliance raise switching costs in those niches. This keeps the folding carton packaging market open to smaller but highly capable firms even as the broad supply base becomes more demanding on cost and compliance.

Automation and digital printing are changing competitive differentiation across the folding carton packaging market because they improve responsiveness for short runs, reduce setup waste, and help converters manage SKU complexity. Brand owners are also embedding recyclability thresholds and carbon disclosure rules into vendor selection, which raises the value of certified supply chains and audited material sourcing. Smurfit WestRock's ActiBlu prototype, unveiled in May 2026, showed how digital assembly and lower adhesive use can improve both recyclability and plant efficiency at the same time. BOBST platform deployment trends also suggest that digitally equipped converters can challenge established players in short-run formats without having to mirror their full production footprint. The folding carton packaging market is therefore becoming harder for new entrants that lack capital, compliance systems, and technology depth, even though fragmentation at the regional level is still visible.

Folding Carton Packaging Industry Leaders

Smurfit WestRock plc

Graphic Packaging International LLC

Mayr-Melnhof Karton AG

International Paper Company

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Smurfit WestRock earmarked USD 150 million for HP Indigo 100K presses at 12 North American and European plants, targeting 20% digital folding-carton share by 2028.

- March 2026: Sonoco Products Company opened a new paper can manufacturing plant in Thailand with a capacity of 200 million units per year, targeting the Asian stacked-chip and snack-food market to support regional demand growth.

- February 2026: Smurfit WestRock plc presented its medium-term financial plan at its investor day, setting a USD 7 billion EBITDA target by 2030 and reporting Q4 2025 net sales of USD 7.5 billion, reflecting continued post-merger integration progress.

- January 2026: International Paper Company completed the acquisition of DS Smith plc for USD 7.2 billion, creating one of the largest paper-based packaging companies globally and materially expanding International Paper's European board supply footprint.

Global Folding Carton Packaging Market Report Scope

The scope of the report covers the analysis of the folding carton packaging market, focusing on its current trends, growth drivers, challenges, and opportunities. These cartons are lightweight, recyclable, and customizable, making them a preferred choice for packaging. The report provides insights into market dynamics, competitive landscape, and key developments shaping the folding carton packaging market.

The Folding Carton Packaging Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and More), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and More), and Geography (North America, South America, Europe, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

By Printing Technology

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

By End-User Industry

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Material Type | Solid Bleached Sulfate | |

| Folding Boxboard | ||

| Coated Unbleached Kraft | ||

| White Line Chipboard | ||

| Other Material Types | ||

| By Printing Technology | Lithographic Printing | |

| Flexographic Printing | ||

| Digital Printing | ||

| Gravure Printing | ||

| Other Printing Technologies | ||

| By End-User Industry | Food and Beverage | |

| Healthcare/Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Electrical and Electronics | ||

| Household and Industrial Goods | ||

| Tobacco | ||

| E-commerce and Retail-ready Packaging | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of folding carton packaging?

The folding carton packaging market size stands at USD 70.39 billion in 2026 and is projected to reach USD 99.51 billion by 2031, growing at a CAGR of 7.17% over 2026-2031.

Which region leads global demand for folding cartons?

Asia-Pacific led with a 42.89% share in 2025 and is also the fastest-growing region with an 8.03% CAGR through 2031, supported by China and India.

Which material type has the strongest position in carton conversion?

Solid Bleached Sulfate led with a 39.13% share in 2025 and is still projected to grow at 7.76% CAGR, reflecting strong demand in food-contact and pharmaceutical cartons.

Why is digital printing gaining ground in carton converting?

Digital printing is expanding because it supports short runs, variable-data printing, and e-commerce customization, and the segment is projected to grow at 8.34% CAGR through 2031.

Which end-user group drives the largest carton volumes?

Food and Beverage remained the largest end-user segment with a 46.71% share in 2025 because processed foods and organized retail continue to require large volumes of printed paperboard packaging.

What is the biggest near-term challenge for carton converters?

Raw material volatility remains the key operating issue, especially rising board prices and margin pressure for converters without backward integration or long-term supply contracts.

Page last updated on: