Liquid Packaging Cartons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

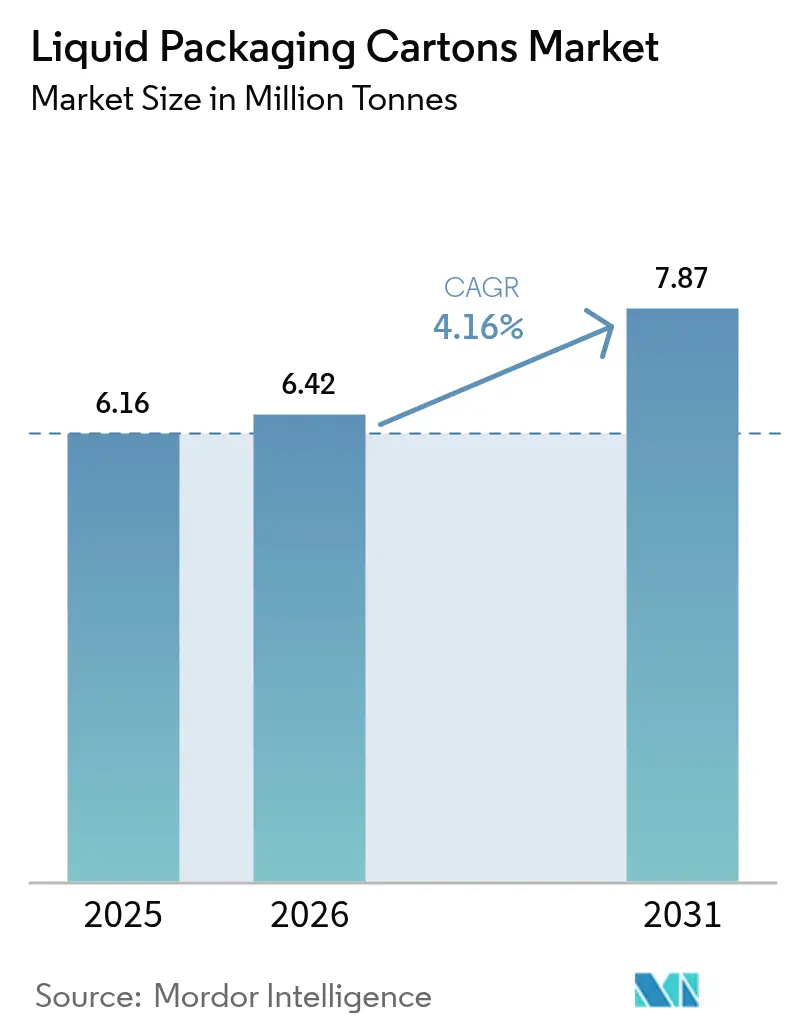

| Market Volume (2026) | 6.42 Million tonnes |

| Market Volume (2031) | 7.87 Million tonnes |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

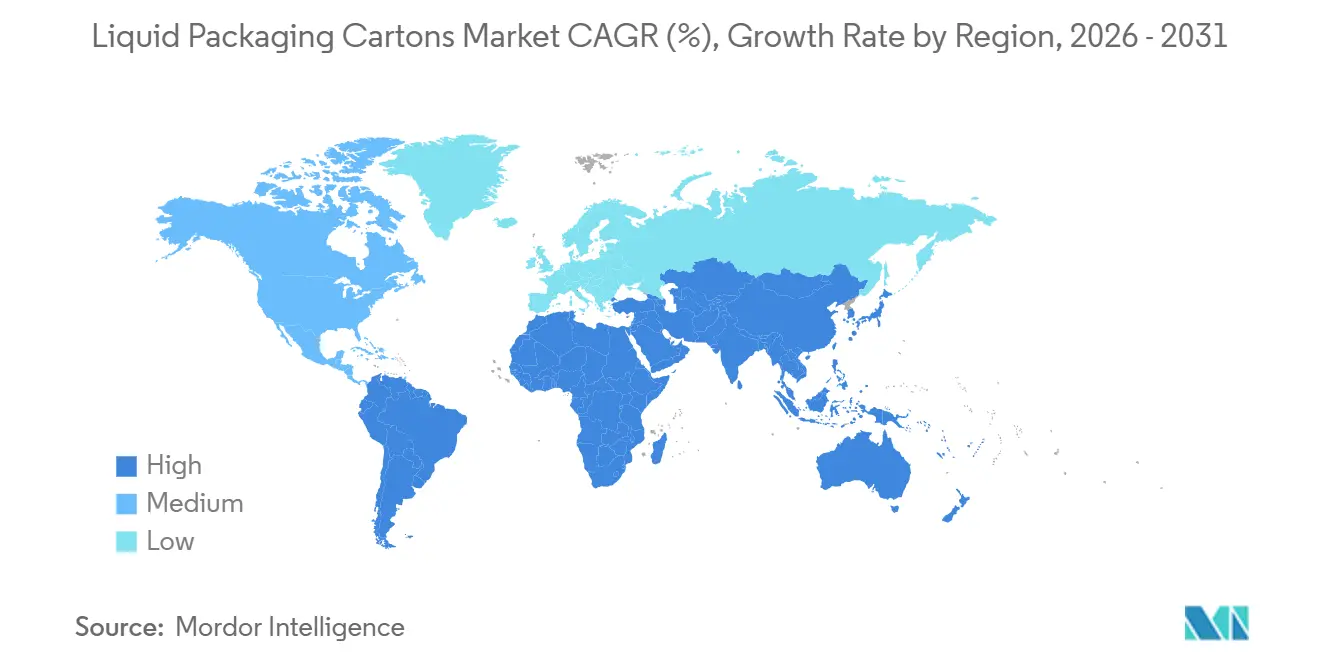

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Packaging Cartons Market Analysis by Mordor Intelligence

The Liquid Packaging Cartons Market size is expected to grow from 6.16 Million tonnes in 2025 to 6.42 Million tonnes in 2026 and is forecast to reach 7.87 Million tonnes by 2031 at 4.16% CAGR over 2026-2031. Strong demand for ambient formats in emerging economies, rising e-commerce grocery volumes, and the European Packaging and Packaging Waste Regulation, which mandates recyclability by 2030, are reshaping capital allocation and material-science priorities. Incumbents are scaling cellulose-based barriers that lift paper content and cut polymer layers, while brand owners pivot toward portion-controlled packs that meet sugar-tax thresholds and reduce cold-chain costs. Investment is tilting toward Asia-Pacific ultra-high-temperature dairy infrastructure and Middle East juice reformulations, even as polyethylene terephthalate bottle lightweighting narrows the life-cycle-assessment gap. Competitive intensity is therefore defined by the race to commercialize mono-material, fiber-dominant designs that secure ESG-linked financing and satisfy extended producer responsibility schemes.

Key Report Takeaways

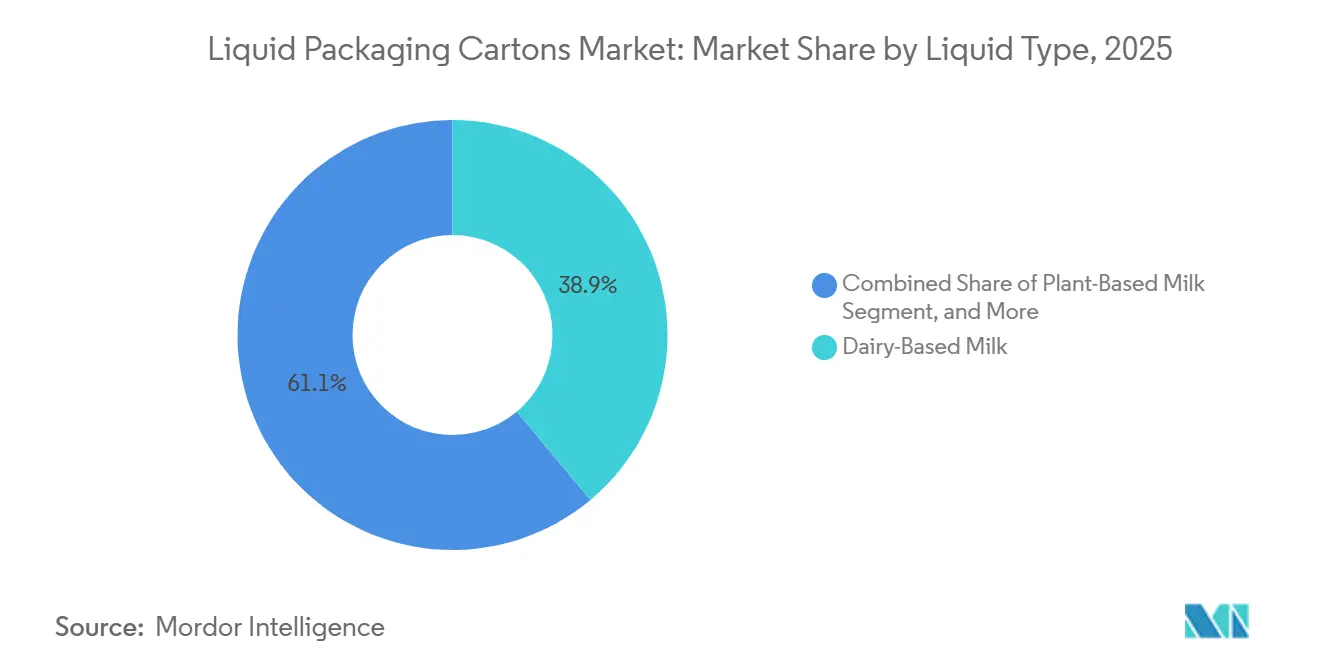

- By liquid type, dairy-based milk held 38.91% of 2025 revenue, while plant-based milk is projected to expand at a 5.39% CAGR to 2031.

- By packaging type, aseptic cartons led with 68.22% of the liquid packaging cartons market share in 2025, whereas retortable formats record the fastest projected CAGR at 4.73% through 2031.

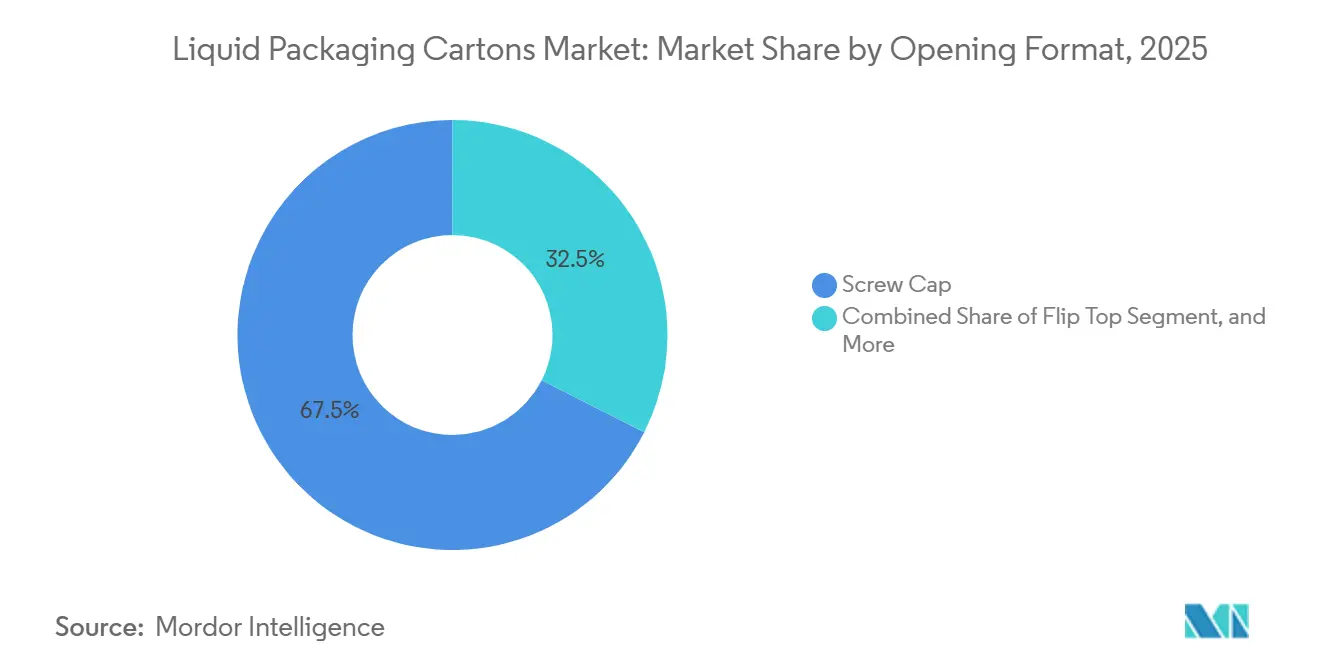

- By opening format, screw-cap closures accounted for 67.54% of 2025 packs; flip-top closures are forecast to grow at a 4.96% CAGR to 2031.

- By carton volume size, formats above 1,000 milliliters commanded 42.83% volume share in 2025, while packs below 250 milliliters advance at a 4.92% CAGR over 2026-2031.

- By geography, Asia-Pacific accounted for 37.62% of the liquid packaging cartons market share in 2025, whereas the Middle East is projected to post the highest 5.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquid Packaging Cartons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UHT Dairy Demand in Emerging Asia | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| E-commerce Grocery Growth Pushing Ambient Formats | +0.9% | Global, with early gains in North America, Europe, China | Medium term (2-4 years) |

| ESG-Linked Financing Favouring Fibre-Based Packs | +0.7% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Sugar-Tax-Led Reformulations Increasing Juice Carton Adoption | +0.5% | Middle East, South America, select Asia-Pacific markets | Short term (≤ 2 years) |

| Cellulose-Based Barrier Breakthroughs Cutting Polymer Layers | +0.4% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Brand Premiumisation in Dairy and Plant-Based Segments Boosting Value-Added Carton Formats | +0.3% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

UHT Dairy Demand in Emerging Asia

Ultra-high-temperature processing economics make aseptic cartons the default in provinces where refrigerated logistics remain cost-prohibitive, and rising protein intake among the middle class sustains multi-year volume visibility.[1]Food and Agriculture Organization, “Dairy Market Review 2025,” FAO.ORG Domestic mega-dairies depend on local filling capacity to avoid import duties, exemplified by a EUR 90 million (USD 94 million) SIG Group plant that came online in Ahmedabad in 2025. Leading carton suppliers also retrofit Asian high-speed lines with fiber-rich barriers so that environmental credentials now influence procurement alongside shelf-life metrics. These shifts cement Asia-Pacific as the growth engine for the liquid packaging cartons market.

E-commerce Grocery Growth Pushing Ambient Formats

Ambient-stable cartons lower energy costs for online fulfilment centres, bypass cold-room zoning, and reduce spoilage during last-mile delivery.[2]Tetra Pak, “Press Release on Lund Pilot Plant,” TETRAPAK.COM The channel, therefore, favors flip-top and screw-cap closures that enable single-hand operation, with flip-tops projected to grow by 4.96% to 2031. In 2025, e-commerce propelled Elopak to its highest quarterly margin, leading the company to greenlight a USD 30 million third line in Arkansas. As online grocery approaches 40% of global retail by 2026, the liquid packaging cartons market gains structural support from warehouse automation that prizes ambient inventory.

ESG-Linked Financing Favoring Fiber-Based Packs

Green bonds and sustainability-linked loans now peg interest-rate spreads to renewable-material thresholds, effectively penalizing polymer-heavy laminates. The European Investment Bank funneled EUR 20 million into dry-molded-fiber pioneer PulPac in 2024, validating investor appetite for mono-material architectures. Brand owners unlock cheaper capital when substrates meet the International Finance Corporation’s 2025 Circular Economy Finance Guidelines' recyclability criteria. Consequently, the liquid packaging cartons market is accelerating upgrades to fiber-dominant structures that meet taxonomy definitions and extend competitive moats.

Sugar-Tax-Led Reformulations Increasing Juice Carton Adoption

Excise regimes that tier levies by sugar content nudge beverage makers toward portion-controlled 180-milliliter packs, boosting demand for small-format cartons. Saudi-based Almarai, holding 50% of the kingdom’s fresh-juice volume, released a 180-milliliter carton in 2024 to mitigate new sugar taxes. World Health Organization data show median tax burdens of 17.8%, reinforcing the economic case for reformulation. These fiscal pressures translate into measurable tailwinds for the liquid packaging cartons market across the Middle East and Latin America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET Bottle Lightweighting Narrowing Carbon Gap | -0.6% | Global, most pronounced in North America and Europe | Medium term (2-4 years) |

| Aseptic Recycling Infrastructure Deficits | -0.5% | Global, acute in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Volatile Liquid Board Prices Tied to Pulp Shortages | -0.4% | Global, supply concentrated in Nordic and North American mills | Short term (≤ 2 years) |

| Labelling and Food-Contact Compliance Costs Rising with Stricter Global Regulations | -0.3% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PET Bottle Lightweighting Narrowing Carbon Gap

Polyethylene terephthalate suppliers have shaved container weight and boosted recycled-resin content, decreasing emissions per bottle by up to 12% and tightening life-cycle parity with fiber-based cartons.[3]The Coca-Cola Company, “Sustainability Report 2025,” COCA-COLACOMPANY.COM Technology such as KHS Loop LITE bottles delivers a 60% footprint reduction versus virgin resin, prompting retailers in Germany and Scandinavia, where collection rates top 90%, to reassess format mixes. Unless carton makers accelerate the elimination of polymer layers, the liquid packaging cartons industry risks losing sustainability differentiation in single-serve applications.

Aseptic Recycling Infrastructure Deficits

Cartons’ multi-layer laminates challenge municipal recovery facilities, as evidenced by a global recycling rate of 28% despite EUR 42 million in supplier-funded collection upgrades. The Alliance for Beverage Cartons and the Environment targets 90% collection by 2030, yet achieving that goal needs EUR 1.5 billion in European sorting enhancements. Persisting infrastructure gaps expose the liquid packaging cartons market to reputational risk and could raise compliance costs under Europe’s 2030 recyclability mandate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Liquid Type: Plant-Based Alternatives Gain Momentum

In 2025, dairy-based milk accounted for 38.91% of the Liquid packaging cartons market share, reflecting entrenched ultra-high-temperature dairy networks in China, India, and the Gulf states. Plant-based milk is projected to grow at a 5.39% CAGR through 2031, widening its revenue footprint as lactose intolerance, environmental messaging, and protein diversification reshape household baskets. Category leaders highlight carton functionality, light-blocking, oxygen-barrier laminates for flavor protection, while regulatory incentives, such as clean-label claims, spur migration from polyethylene terephthalate to fiber-dominant packs. Market participants also leverage allergen-free bases, such as the sunflower-protein ingredient launched in 2025, creating new carton-friendly recipes that bypass soy and nut concerns.

Shelf-stable juices, functional beverages, and liquid foods collectively make up the balance of volumes, each taking advantage of ambient distribution to minimize cold-chain costs. Sugar-tax measures in the Middle East and Latin America accelerate the launch of 180-milliliter juice packs that stay under per-serving sugar thresholds, while functional drinks adopt high-barrier cartons to preserve bioactive ingredients during e-commerce fulfillment. Sauces and ready meals migrate to retortable cartons, trading glass and metal for lighter, stackable formats that extend shelf life to two years. The liquid-type mix, therefore, balances legacy dairy volumes with double-digit growth in plant-based, functional, and culinary applications.

By Packaging Type: Retortable Designs Challenge Aseptic Dominance

Aseptic solutions made the largest contribution to the Liquid packaging cartons market in 2025, accounting for 68.22% of volume across milk, plant-based beverages, and ambient juice. They remain the default when line speeds exceed 24,000 packs per hour, and low-acid formulations require sterile fills. Retortable cartons, however, are expanding at a 4.73% CAGR, propelled by chunky soups, pasta sauces, and ready meals that require in-package sterilization of particulates. Recent barrier innovations now allow retort laminates to match aseptic oxygen transmission rates, reducing flavor scalping and expanding product scope.

Brand owners highlight logistics savings, with cans achieving up to 30% weight reduction and a rectangular footprint that optimizes shelf facings. Gable-top variants, still critical for fresh dairy and chilled juice in North America and Northern Europe, lose relative momentum as retailers prioritize shelf-stable portfolios for e-commerce fulfillment. Material-science convergence means cellulose-based barriers developed for aseptic lines can also be retrofitted to retort formats, enabling suppliers to amortize R&D across both segments and compress time-to-market for low-polymer constructions.

By Opening Format: Flip-Top Convenience Drives Share Shifts

Screw caps dominated 67.54% of 2025 packs, supported by established tooling and ingrained consumer habits. Flip-top closures are gaining fastest, advancing at a projected 4.96% CAGR through 2031 as e-commerce grocers and on-the-go channels demand single-hand operation and resealability. Paper-rich cap prototypes trialed in Spain in 2025 raise renewable content to 87%, helping fillers avoid eco-modulation fees tied to polymer mass. Small-format plant-based lattes and functional drinks showcase flip-tops for spill-proof sipping, with SIG’s DomeMini filling 180- to 350-milliliter packs at 12,000 units per hour.

Straw-hole designs persist in children’s juice boxes, where tamper evidence and portion control outweigh resealing needs, while pull-tabs retain relevance in institutional milk service due to low part counts and fast opening. Closure selection is increasingly a branding lever, with QR-coded lids enabling traceability and loyalty programs. Suppliers that synchronize cap innovation with carton-body material transitions capture incremental value and deepen switching costs for fillers.

By Carton Volume Size: Sub-250 Milliliter Packs Lead Regulatory-Driven Growth

Formats above 1,000 milliliters captured 42.83% of 2025 shipments, catering to multi-person households and bulk pantry restocks in Asia-Pacific and the Middle East. Yet cartons below 250 milliliters are forecast to expand at a 4.92% CAGR through 2031 as sugar tax regimes, vending adoption, and single-serve e-commerce orders proliferate. Brands deploy 180 milliliter juice and functional-shot packs to stay under per-container excise thresholds, while smaller households in urban markets gravitate toward portion-controlled offerings that reduce food waste.

The 250-500 milliliter band captures commuter beverages and ready-to-drink coffees, balancing price-per-liter economics with on-the-go convenience. Meanwhile, the 501-1,000 milliliter segment anchors weekly dairy consumption but faces incremental share pressure from high-protein plant-based lines launching in 750 milliliter sizes. Equipment upgrades that enable quick format changes, down to 0.5 millimeter board-cut tolerance, let fillers switch between family packs and vending-friendly minis on the same line, maximizing asset utilization as demand fragments.

Geography Analysis

Asia-Pacific generated 37.62% of 2025 revenue, the largest regional share of the liquid packaging cartons market, anchored by ultra-high-temperature dairy networks in China and India that rely on ambient distribution. Domestic fillers reduce import tariffs by running local plants such as SIG Group’s Ahmedabad facility, which turns out 4 billion packs a year. Rising household income in tier-three Chinese cities keeps milk demand on a steady upswing, while India’s government school-meal program secures carton volumes for aseptic milk. Japan rounds out regional strength as Nippon Paper Industries expands liquid board capacity to feed premium plant-based launches. This structural demand ensures that Asia-Pacific remains the anchor for growth in the liquid packaging cartons market through 2031.

Europe and North America are mature but far from stagnant. Both regions pivot toward plant-based milk, functional drinks, and regulatory-driven package redesigns that lift recycled-content ratios. The Packaging and Packaging Waste Regulation, active since February 2025, pressures fillers to adopt mono-material cartons that qualify as recyclable, unlocking eco-modulation fee rebates. E-commerce grocery also widens the addressable market because warehouses favor ambient-packaged products that save energy. As a result, Europe and North America sustain mid-single-digit value growth even though per capita consumption has plateaued.

The Middle East holds the fastest projected regional CAGR at 5.11% thanks to sugar-tax-driven juice reformulation and growing ultra-high-temperature dairy penetration. Almarai’s launch of a 180 milliliter juice pack illustrates how portion control sidesteps per-serving sugar levies and spurs small-format uptake. Gulf Cooperation Council retailers now promote deposit-return schemes that raise carton recovery rates, helping the region align with European recyclability targets. Sub-Saharan Africa lags in infrastructure but benefits from bilateral aid programs that fund school milk in aseptic formats. Collectively, these mixed demand drivers position the Middle East and Africa as the fastest-growing region, while Asia-Pacific retains volume leadership in the liquid packaging cartons market.

Competitive Landscape

The liquid packaging cartons arena is moderately concentrated; Tetra Pak, SIG Group, and Elopak together control an estimated 70% to 75% of global volumes, yet each faces localized rivals who chip at price-sensitive niches. Tetra Pak’s EUR 60 million Lund pilot plant brings paper-based barriers closer to commercialization and deepens its proprietary material moat. SIG Group counters with Terra Alu-free cartons that already reach 81% paper content and target 90% by 2030, marketing a 61% carbon-dioxide-equivalent cut to brand owners with science-based climate targets. Elopak leverages its D-Pak launch, which adds post-consumer and bio-circular polyethylene, to court retailers seeking circular-feedstock validation.

Regional producers build share through cost and proximity. Greatview serves Chinese fillers that want dual sourcing, while Graphic Packaging International taps U.S. mills to supply mid-tier dairies that demand Forest Stewardship Council-certified board. Nippon Paper extends downstream into gable-top filling equipment to lock in substrate pull-through, and Pactiv Evergreen’s 2024 divestiture of its Beverage Merchandising unit freed up capital for fiber-barrier R&D. These moves show how vertical integration and portfolio pruning sharpen competitive positioning.

Technology adoption is the decisive lever. Suppliers that retrofit legacy aseptic lines with cellulose barriers help fillers avoid greenfield capex and lock in multi-year contracts. Flip-top paper caps, robotic carton-sorting systems, and digital watermark labeling solutions further differentiate offers, converting sustainability compliance into a revenue-per-pack premium. Start-ups such as PulPac, which won European Investment Bank funding to industrialize dry-molded-fiber bodies, pose a disruptive long-term threat by eliminating multi-layer laminates. Given that the top five players still approach 80% combined share, competitive pressure centers on who can scale next-generation mono-material designs first, a race that will shape margin hierarchy through 2031.

Liquid Packaging Cartons Industry Leaders

Tetra Pak International SA

SIG Group AG

Elopak ASA

Greatview Aseptic Packaging Co. Ltd.

Nippon Paper Industries Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Tetra Pak inaugurated a EUR 60 million pilot plant in Lund, Sweden, to produce paper-based barriers targeting 80% paper content and a 43% carbon-footprint cut versus legacy laminates.

- February 2026: Elopak announced FY 2025 revenue of EUR 1.2 billion with 5.9% organic growth, attributing gains to North American e-commerce volumes and European sustainability demand.

- February 2026: Tetra Pak extended its paper-based barrier to A3/Speed aseptic lines in Asia, with Maeil Dairies as first commercial adopter for soy milk.

- October 2025: Elopak posted Q3 2025 revenue of EUR 289.7 million and approved a USD 30 million third production line at its Little Rock, Arkansas, plant.

Global Liquid Packaging Cartons Market Report Scope

The Liquid Packaging Cartons Market Report is Segmented by Liquid Type (Dairy-Based Milk, Plant-Based Milk, Juices, Energy and Functional Drinks, Sauces and Liquid Food, Other Liquid Types), Packaging Type (Aseptic Cartons, Gable Top Cartons, Retortable Cartons), Opening Format (Screw Cap, Straw Hole, Pull Tab, Flip Top), Carton Volume Size (Less Than 250 ml, 250-500 ml, 501-1,000 ml, Above 1,000 ml), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Dairy-Based Milk |

| Plant-Based Milk |

| Juices |

| Energy and Functional Drinks |

| Sauces and Liquid Food |

| Other Liquid Types |

| Aseptic Cartons |

| Gable Top Cartons |

| Retortable Cartons |

| Screw Cap |

| Straw Hole |

| Pull Tab |

| Flip Top |

| Less Than 250 ml |

| 250-500 ml |

| 501-1,000 ml |

| Above 1,000 ml |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Liquid Type | Dairy-Based Milk | ||

| Plant-Based Milk | |||

| Juices | |||

| Energy and Functional Drinks | |||

| Sauces and Liquid Food | |||

| Other Liquid Types | |||

| By Packaging Type | Aseptic Cartons | ||

| Gable Top Cartons | |||

| Retortable Cartons | |||

| By Opening Format | Screw Cap | ||

| Straw Hole | |||

| Pull Tab | |||

| Flip Top | |||

| By Carton Volume Size | Less Than 250 ml | ||

| 250-500 ml | |||

| 501-1,000 ml | |||

| Above 1,000 ml | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What CAGR is projected for liquid packaging cartons between 2026 and 2031?

The liquid packaging cartons market is projected to grow at a 4.16% CAGR over 2026-2031.

Which region offers the fastest growth opportunity?

The Middle East is expected to post the highest 5.11% CAGR through 2031, driven by sugar-tax-led juice reformulations.

How much of 2025 volume did aseptic cartons represent?

Aseptic designs led the pack with 68.22% of global volume in 2025.

What share did Asia-Pacific hold in 2025 revenue?

Asia-Pacific generated 37.62% of worldwide revenue in 2025.

Which opening format is gaining traction in e-commerce?

Flip-top closures are the fastest-growing opening, advancing at a projected 4.96% CAGR through 2031.

Why are plant-based milks important for future demand?

Plant-based beverages are forecast to rise at a 5.39% CAGR, outpacing dairy and expanding carton usage in premium, sustainability-focused segments.

Page last updated on: