Liquid Food Paperboard Cartons Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

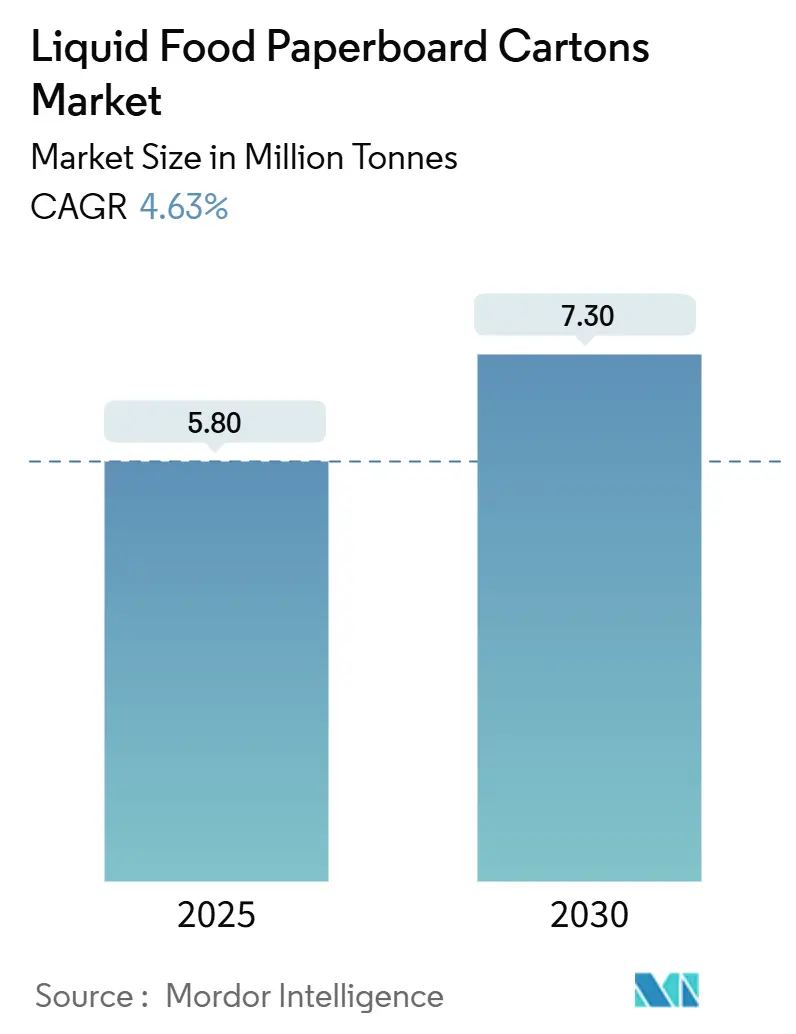

| Market Volume (2025) | 5.80 Million tonnes |

| Market Volume (2030) | 7.30 Million tonnes |

| Growth Rate (2025 - 2030) | 4.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Food Paperboard Cartons Market Analysis by Mordor Intelligence

The liquid food paperboard cartons market size stood at 5.8 million tonnes in 2025 and is forecast to reach 7.3 million tonnes by 2030, translating into a 4.63% CAGR over the period. Robust demand stems from regulatory pressure on single-use plastics, rapid uptake of aseptic technology, and the widening appeal of plant-based and shelf-stable dairy beverages. Brand owners aiming to reduce Scope 3 emissions are standardizing on aluminum-free barriers, while food companies in emerging economies consider paperboard the most cost-effective route to national distribution without a reliable cold chain. At the same time, filler manufacturers are rolling out equipment that handles smaller batch sizes, supporting functional drink launches and private-label expansion. Moderate market concentration gives large integrated suppliers room to protect margins through differentiated substrates and regional production footprints, yet it still leaves space for niche converters that can exploit premium graphics or local language requirements.

Key Report Takeaways

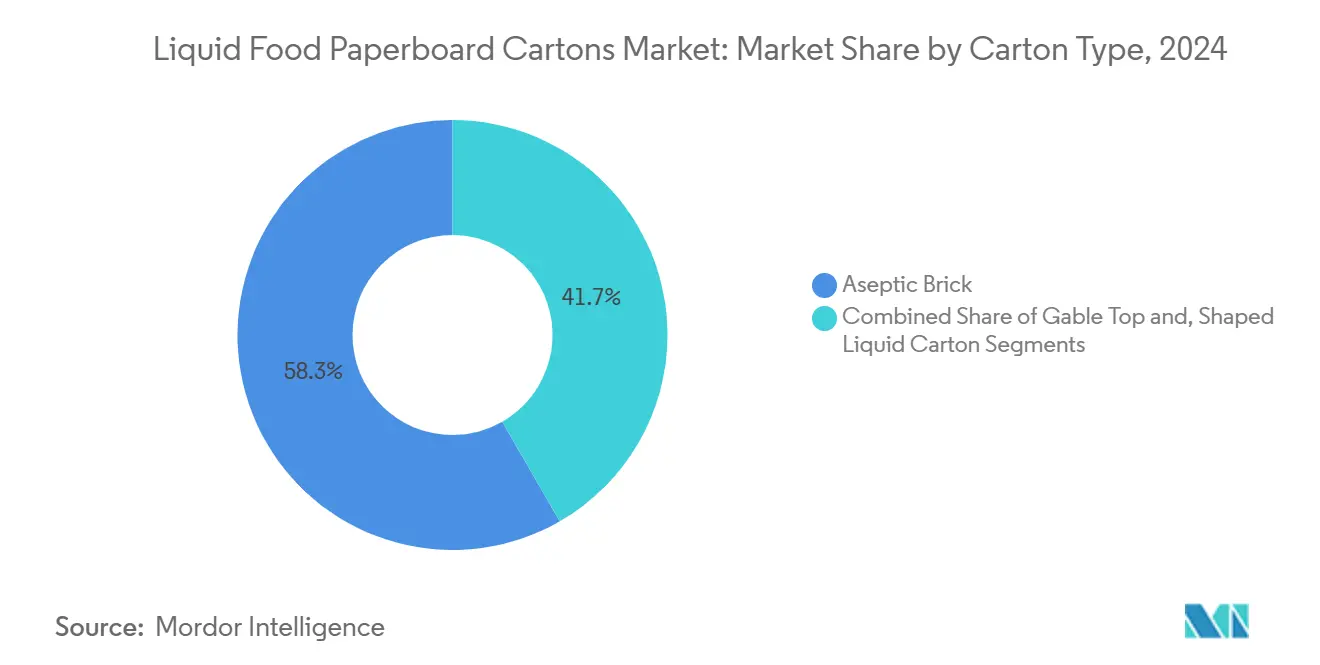

- By carton type, aseptic brick formats captured 58.31% of the liquid food paperboard cartons market share in 2024.

- By end-user, the liquid food paperboard cartons market size for plant-based beverages segment are set to expand at a 7.16% CAGR between 2025-2030.

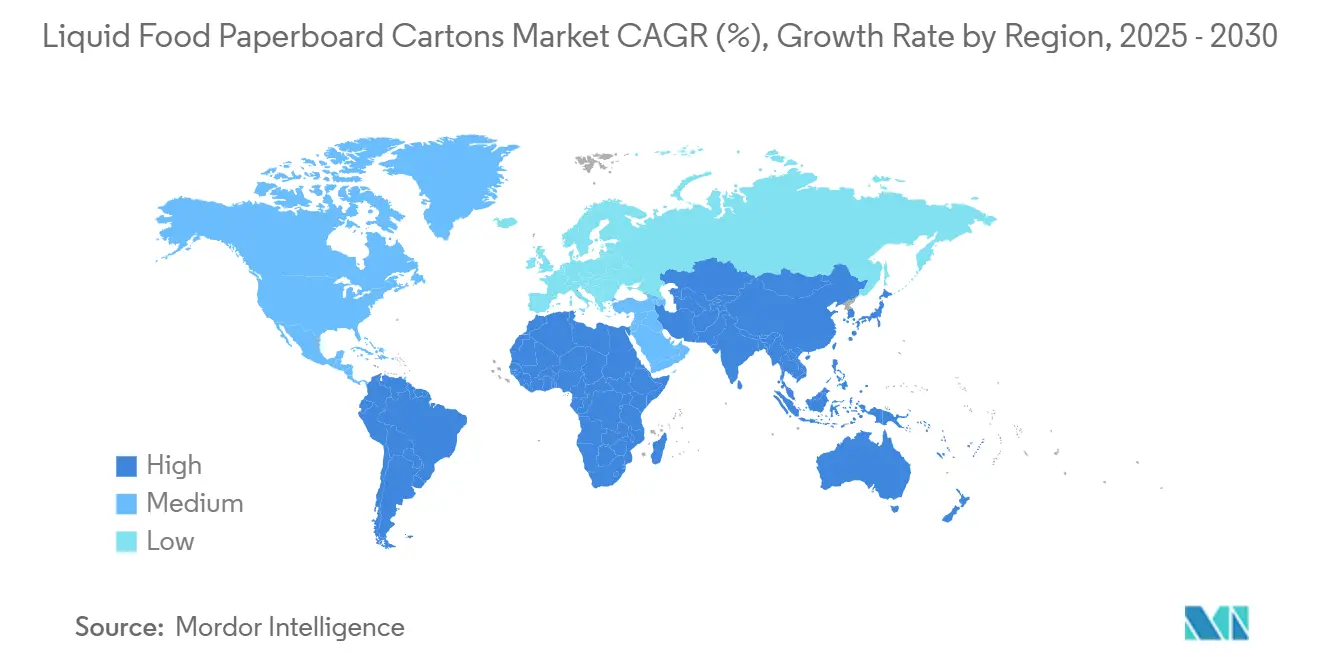

- By Geography, Asia-Pacific Region held 52.04% of the liquid food paperboard cartons market share in 2024.

Global Liquid Food Paperboard Cartons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of shelf-stable dairy beverages in emerging economies | +1.2% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Surge in plant-based “alt-milk” packed in cartons | +0.8% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Plastic-reduction regulations accelerating shift from PET/HDPE | +1.0% | Europe, North America, expanding to APAC | Long term (≥ 4 years) |

| Transition of hot-fill soups and broths from cans to retortable carton bottles | +0.4% | North America, Europe | Medium term (2-4 years) |

| Filler upgrades enabling small-batch functional drink launches | +0.3% | Global, led by North America | Short term (≤ 2 years) |

| Subsidy-eligible paper-based barrier replacing aluminum layers | +0.5% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumption of Shelf-Stable Dairy Beverages in Emerging Economies

Urban migration and rising disposable incomes in Asia, Africa, and parts of Latin America are lifting demand for milk that does not require refrigeration from farm to shelf. Tetra Pak projects global white-milk volumes to rise 2.2% annually through 2027, with Central and East Asia accounting for the bulk of incremental litres. [1]Tetra Laval, “Tetra Pak Facts,” tetralaval.com SIG’s EUR 90 million (USD 105.08 million) Ahmedabad plant, capable of producing 4 billion aseptic packs each year, underscores the upside created by the fact that less than 10% of milk in India is packaged today. In markets where product losses from temperature abuse routinely exceed 5%, retailers gravitate toward carton-based UHT solutions that carry a 6- to 12-month shelf life. Large dairies leverage country-wide distribution without needing expensive chilled fleets, while smaller cooperatives use co-packers to reach urban grocery chains. As governments tighten food-safety rules, carton penetration accelerates further, locking in structural growth for the liquid food paperboard cartons market.

Surge in Plant-Based “Alt-Milk” Packed in Cartons

Global demand for beverages made from oats, almonds, rice, and soy is expanding as consumers link flexitarian diets with lower environmental footprints. Tetra Pak expects plant-based drinks to grow 1.5% annually through 2027, a pace that outstrips traditional dairy in North America and Europe. Danone, whose Essential Dairy and Plant-Based unit generated 52% of company sales in 2024, channels much of this volume through gable-top and slim-brick cartons that showcase sustainability messaging. Paperboard offers superior billboard space and a clear “paper feel” compared with PET bottles, reinforcing brand positioning around carbon savings. Recipe innovation such as protein-fortified oat lattes or calcium-enriched rice drinks demands barrier layers that shield sensitive nutrients from oxygen ingress, a capability that next-generation, aluminum-free cartons now provide at scale. These dynamics foster a premium segment where packaging influences consumer choice almost as strongly as ingredient lists, further enlarging the liquid food paperboard cartons market.

Plastic-Reduction Regulations Accelerating Shift from PET/HDPE

The European Union’s Packaging and Packaging Waste Regulation now obliges producers to place only recyclable packaging on the market by 2030 and bans PFAS in food contact materials.[2]European Parliament, “Packaging and Packaging Waste,” europarl.europa.eu Parallel momentum in the United States includes the General Services Administration’s decision to favor single-use-plastic-free packaging in federal procurement. Compliance costs for PET and HDPE rise as recycled-content mandates tighten and chemical recycling remains expensive. Brand owners of ready-to-drink tea and coffee, once loyal to clear plastic bottles, increasingly view fiber-based cartons as a lower-risk pathway to regulatory alignment. Converters respond with monomaterial caps and high-speed applicators that simplify recycling further. These coordinated policy trends underpin long-duration tailwinds for the liquid food paperboard cartons market.

Transition of Hot-Fill Soups and Broths from Cans to Retortable Carton Bottles

Consumers seeking lighter, microwave-ready packaging are prompting soup and broth manufacturers to reconsider the 150-year-old metal can. Campbell Soup Company’s Meals and Beverages division has singled out packaging innovation as a growth lever within its USD 9.6 billion 2024 portfolio. Retortable cartons withstand hot-fill temperatures yet weigh up to 40% less than steel, trim logistics costs, and offer high-resolution graphics. Supermarket chains appreciate the rectangular geometry that improves case-pack efficiency and shelf utilization. As more brands position premium bone broths and vegetable purées in cartons, the category evolves from a commodity to a differentiated offering, benefiting the liquid food paperboard cartons market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of aseptic filling lines | -0.7% | Global, particularly impacting emerging market players | Medium term (2-4 years) |

| Limited curb-side recycling infrastructure in developing regions | -0.5% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Supply-chain tightness for liquid-packaging-board | -0.4% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| Brand-owner inertia toward incumbent PET bottles in RTD tea/coffee | -0.3% | Global, concentrated in mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Aseptic Filling Lines

State-of-the-art aseptic systems range from USD 10 million to USD 50 million per line, a sum out of reach for many regional dairies and juice blenders. Elopak’s 2024 decision to build a plant in Little Rock, Arkansas, highlights how even established players rely on scale to justify such investments. Complex sterilization protocols require trained technicians, specialized spare parts, and validated cleaning regimes, adding operating expense. Consequently, the pool of converters remains limited, concentrating market power upstream and slowing penetration of cartons in price-sensitive segments.

Limited Curb-Side Recycling Infrastructure in Developing Regions

Cartons consist mainly of paper fiber but also include polyethylene and, in some legacy designs, aluminum. Developing economies often lack mills capable of separating and recovering these layers efficiently. The Asian Development Bank notes that the economics of municipal recycling rely on adequate volumes and organized collection, both still nascent in many cities. Where the informal sector dominates, cartons fetch lower scrap values than PET, dampening recovery rates and raising concerns among policymakers and NGOs. Inadequate end-of-life solutions can blunt the green credentials that underpin demand for the liquid food paperboard cartons industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Carton Type: Aseptic Technology Drives Market Leadership

Aseptic brick cartons delivered 58.31% liquid food paperboard cartons market share in 2024 because their multilayer structure guarantees up to 12 months of ambient shelf life without preservatives. SIG placed 91 new aseptic lines worldwide in 2024, matching its prior-year record and signaling healthy demand for advanced systems. [3]SIG, “Annual Report 2023,” sig.biz The push toward aluminum-free layers further widens the technology gap between cartons and legacy plastic, strengthening the segment’s hold on shelf-stable milk, juice, and plant-based drinks. Gable-top cartons, in contrast, posted the fastest 5.92% CAGR as brands in premium dairy and alt-milk segments favor their wide front panel for clean-label storytelling. The shaped-carton niche thrives on premium juices and functional shots where distinctive silhouettes capture shopper attention. As converters refine forming techniques, shaped variants may capture incremental points of the liquid food paperboard cartons market size, yet aseptic bricks will remain the workhorse format through 2030.

Growth in gable tops also reflects the economics of filling: simpler equipment, lower barrier requirements, and compatibility with pasteurized rather than UHT processes shorten payback for medium-size dairies. Many co-packers in North America retool existing fresh-milk lines to handle oat and almond beverages in the same carton, accelerating time-to-market for brands. Meanwhile, bricks benefit from a new wave of foil-free barriers that cut greenhouse-gas footprints, enabling retailers to meet Scope 3 targets without sacrificing product integrity. These technical upgrades solidify the leadership of bricks while ensuring that the liquid food paperboard cartons market size for gable tops continues to surpass forecast averages.

By End-User: Plant-Based Surge Reshapes Traditional Dairy Dominance

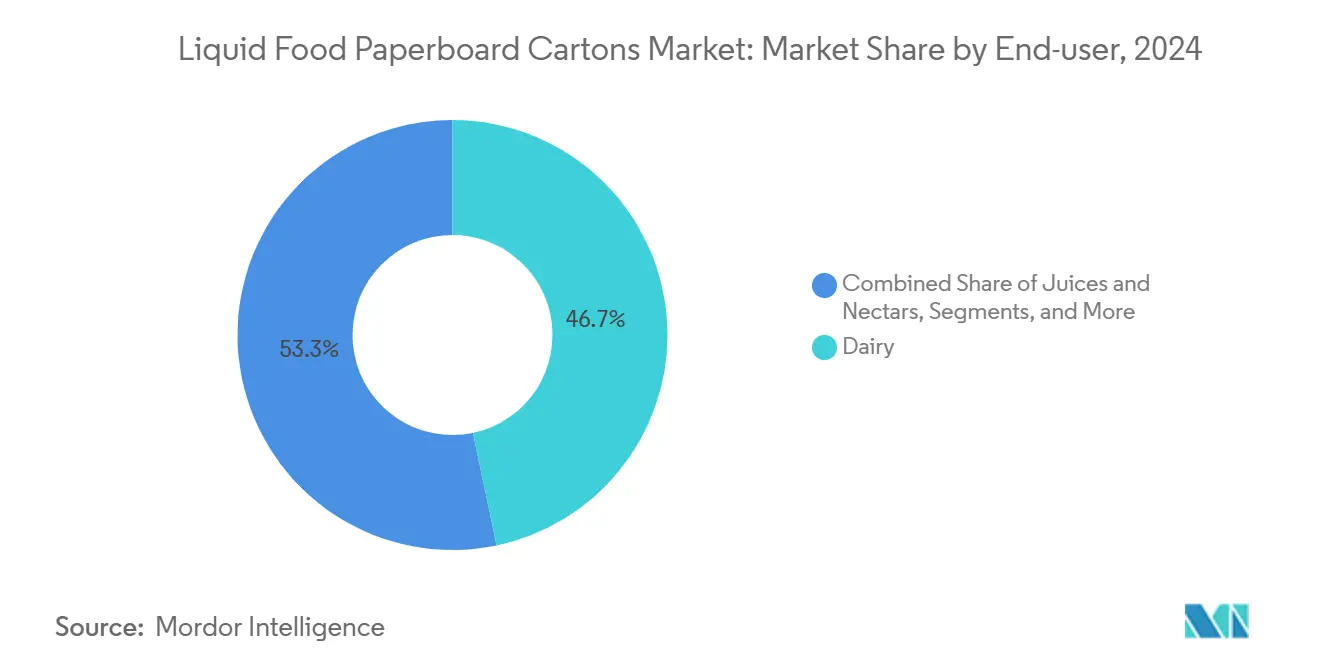

Dairy retained 46.72% of liquid food paperboard cartons market size in 2024 thanks to entrenched consumer habits and the ubiquity of UHT milk across Africa, Latin America, and Southeast Asia. Nonetheless, the plant-based category is on track for a 7.16% CAGR, eroding dairy’s dominance as lactose-intolerant and vegan populations grow in urban centers. Major consumer-goods firms allocate marketing budgets toward oat-milk barista blends and protein-enhanced soy lattes, often priced at a 20% premium to conventional milk. Juices and nectars hold steady but shift toward functional fortification and reduced-sugar recipes. The soups, sauces, and broths segment pivots from cans to retortable cartons, opening fresh shelf-space opportunities. Collectively, these shifts underpin a fertile landscape for brand innovation and protect mid-single-digit growth in the liquid food paperboard cartons market despite maturing dairy demand in Europe and North America.

Specialized nutrition lines—ranging from pediatric formulas to geriatric protein drinks—require ultra-high barrier performance and precise portion sizes. Cartons address both needs and lend themselves to braille embossing, an inclusion feature valued by healthcare regulators. Because this niche commands double-digit gross margins, converters prioritize the segment, reinforcing technology leadership within the liquid food paperboard cartons industry.

Geography Analysis

Asia-Pacific contributed 52.04% of global volume in 2024 and is slated for the fastest 6.62% CAGR through 2030. China’s national dairy revitalization campaigns, India’s packaging penetration gap, and Southeast Asia’s youthful demographics collectively anchor regional momentum. SIG’s new Indian plant exemplifies localization strategies that cut lead times and import duties, improving price competitiveness. Japan and South Korea, though mature, set trends in premium functional beverages and recyclable closures, knowledge that diffuses to other Asian markets over time. North America follows with steady mid-single-digit growth as premiumization and sustainability mandates steer brands to cartons. The General Services Administration’s policy shift signals institutional tailwinds in food-service channels, further entrenching cartons. [4]General Services Administration, “Reduction of Single-Use Plastic Packaging,” gsa.gov

Europe’s sophisticated regulatory environment exerts a dual influence: it accelerates carton adoption but also demands continuous eco-design upgrades. The 2025 ban on PFAS and the 2030 recyclability deadline place fiber-based solutions at the forefront of compliance roadmaps. Within the bloc, Germany and France dominate volume, while Nordic countries boast recycling rates above 70%, validating closed-loop business models. In contrast, the Middle East and Africa grow from a smaller base, constrained by uneven cold-chain coverage and fluctuating oil-linked incomes. Still, young populations and rapid e-commerce uptake favor ambient beverages that require sturdy, lightweight packaging, a combination that enhances prospects for the liquid food paperboard cartons market.

South America presents a mixed picture. Brazil experiences renewed investment in UHT fillers after currency stabilization, while Argentina’s volatile macro environment tempers near-term capacity expansion. Government nutrition programs that distribute school milk in cartons provide a baseline of demand and create familiarity among next-generation consumers, boding well for long-term adoption.

Competitive Landscape

The liquid food paperboard cartons market remains moderately concentrated, with Tetra Pak, SIG Group, and Elopak controlling the majority of installed aseptic filling capacity. Each operates proprietary filling, cap, and barrier systems that lock customers into multiyear service and consumables contracts, generating predictable annuity streams. SIG leverages a strategy of “local for local” manufacturing; its Indian investment cuts import duties and strengthens relationships with regional dairies and juice brands. Tetra Pak focuses on digitalized preventive maintenance and connected packs that enable traceability, while Elopak positions Pure-Pak® as a natural, minimal-plastic solution for both fresh and ambient categories.

Supply-chain integration is a key differentiator. Market leaders co-develop board grades with Nordic mills, ensuring access to scarce high-purity fiber. Their global technical-service networks reduce downtime for customers, reinforcing switching costs. Yet disruption looms from smaller European and Asian fillers marketing compact, lower-pressure aseptic systems at half the traditional capex, targeting craft alt-milk producers and functional drink startups. In substrate innovation, startups explore monomaterial barrier coatings that claim full recyclability in standard paper streams, a breakthrough that could erode the incumbents’ aluminum-free head start.

Strategic moves in 2024-2025 include license-and-produce agreements with corrugated converters seeking to diversify into liquid board, joint ventures between board mills and chemical companies to commercialize bio-based barriers, and acquisitions of regional co-packers by multinationals keen to secure downstream channels. Collectively, these actions illustrate a landscape in flux yet still anchored by technology holders who command the core of the liquid food paperboard cartons market.

Liquid Food Paperboard Cartons Industry Leaders

Tetra Pak International SA

SIG Group AG

Elopak ASA

Pactiv Evergreen Inc.

Greatview Aseptic Packaging Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SIG opened its first aseptic carton plant in India with a €90 million outlay and 4 billion-pack annual capacity, supporting dairy and soft-drink customers as packaging penetration rises.

- February 2025: The European Union’s Packaging and Packaging Waste Regulation took effect, mandating recyclability by 2030 and banning PFAS in food contact materials.

- October 2024: SIG reported 5.1% constant-currency Q3 revenue growth and a 25% adjusted EBITDA margin, reflecting easing capacity constraints in US bag-in-box lines and robust emerging-market demand.

- August 2024: Elopak posted EUR 288.4 million (USD 337.08 million) in Q2 revenue, up 3.7% year on year, buoyed by Pure-Pak growth in Europe and the Americas.

Global Liquid Food Paperboard Cartons Market Report Scope

| Aseptic Brick |

| Gable Top |

| Shaped Liquid Carton |

| Dairy |

| Juices and Nectars |

| Plant-Based Products |

| Soups, Sauces and Broths |

| Other End-user (Ready-to-Drink, Nectar) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Carton Type | Aseptic Brick | ||

| Gable Top | |||

| Shaped Liquid Carton | |||

| By End-user | Dairy | ||

| Juices and Nectars | |||

| Plant-Based Products | |||

| Soups, Sauces and Broths | |||

| Other End-user (Ready-to-Drink, Nectar) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the liquid food paperboard cartons market in 2025?

It reached 5.8 million tonnes in 2025 and is on course for 7.3 million tonnes by 2030.

What CAGR is forecast for liquid food paperboard cartons through 2030?

The market is projected to grow at 4.63% annually between 2025 and 2030.

Which region leads demand for liquid food cartons?

Asia-Pacific accounts for 52.04% of global volume and is expanding at a 6.62% CAGR.

Which carton type has the largest share today?

Aseptic brick formats hold 58.31% of 2024 volume due to extended shelf-life performance.

What is driving the shift from plastic to cartons?

Stringent plastic-reduction regulations, especially in the EU and US, make recyclable paperboard cartons an attractive alternative while meeting brand sustainability goals.

Why are aseptic fillers considered a barrier to entry?

Capital costs of USD 10 millionÐ50 million per line and the need for specialized know-how restrict participation to well-financed players or co-packers.

Page last updated on: