Precision Planting Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.06 Billion |

| Market Size (2031) | USD 9.77 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

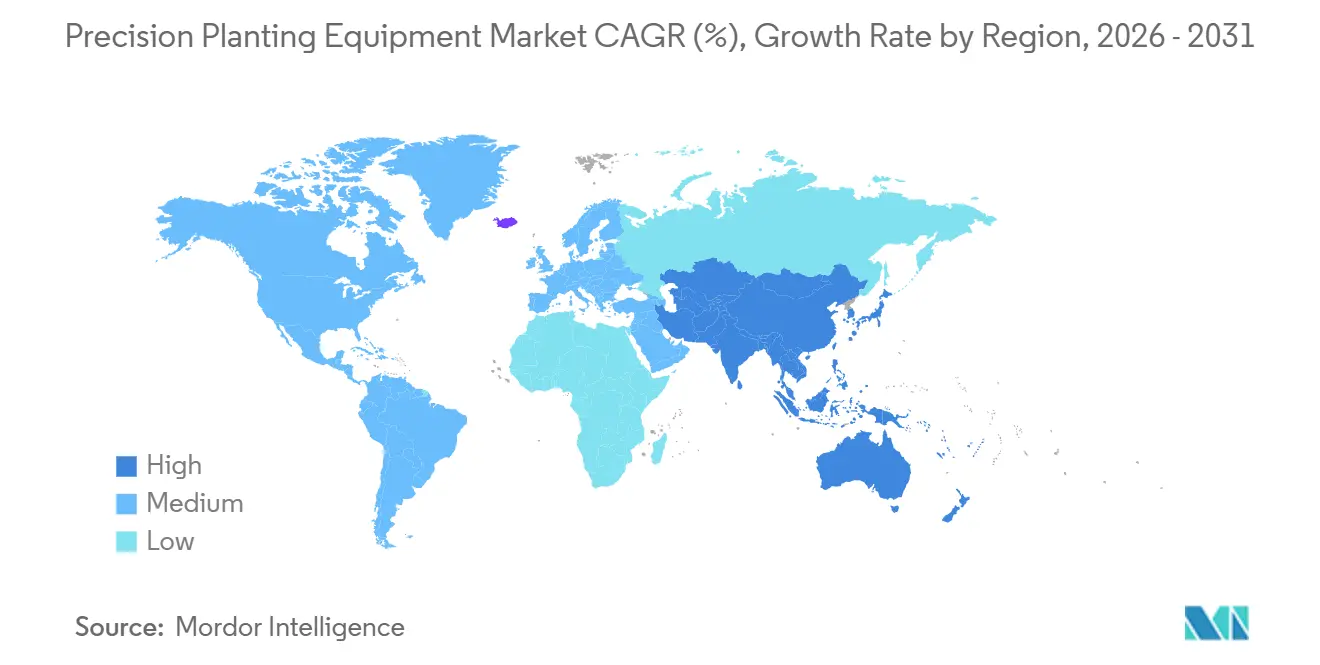

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

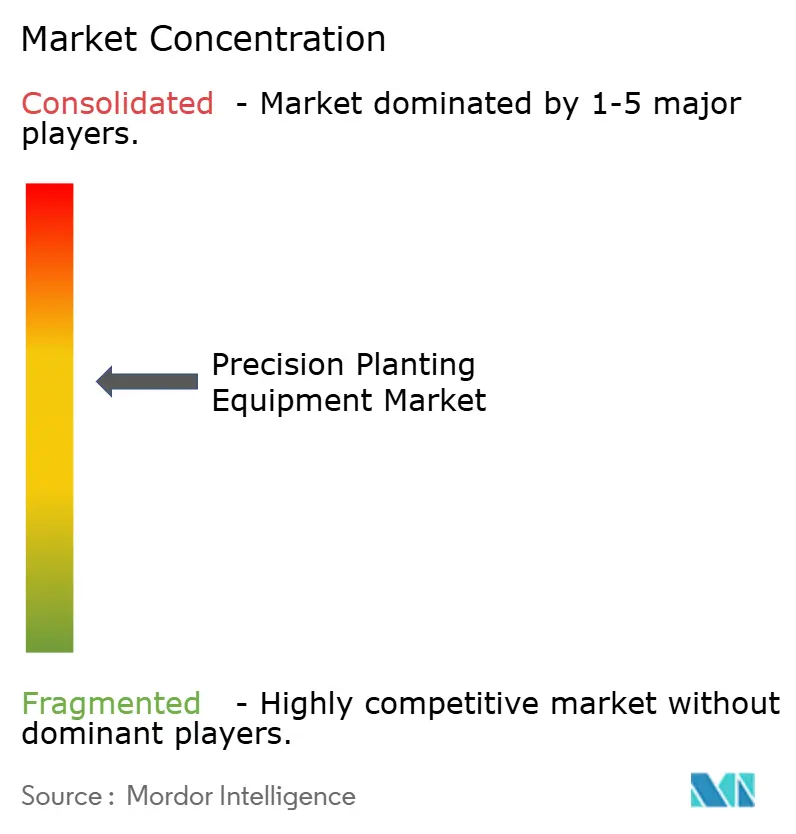

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precision Planting Equipment Market Analysis by Mordor Intelligence

The precision planting equipment market size is projected to expand from USD 5.51 billion in 2025 to USD 6.06 billion in 2026, and to USD 9.77 billion by 2031, registering a CAGR of 10.02% between 2026 and 2031. The precision planting equipment market is moving higher because grain demand is rising faster than usable cropland, which keeps yield per acre at the center of farm investment decisions[1]Source: Y. A. Zereyesus et al., “Global Food Assessment, 2025–35,” USDA Economic Research Service, ers.usda.gov. The precision planting equipment market is also benefiting from a clear shift toward electric metering, row-level control, and retrofit kits that improve planting accuracy without forcing full planter replacement. Growth remains strongest where policy support and digitization goals are becoming more explicit, especially in the Asia-Pacific, while North America continues to anchor current revenue because of its large installed base and faster upgrade cycles. Competition is active but not closed, since leading OEMs still face pressure from retrofit specialists and European manufacturers that are pushing electric architectures, software integration, and mixed-fleet compatibility. The main limits remain financing pressure, operator training needs, and connectivity dependence in rural areas, which means adoption will continue to vary widely by farm income, dealer support, and network quality.

Key Report Takeaways

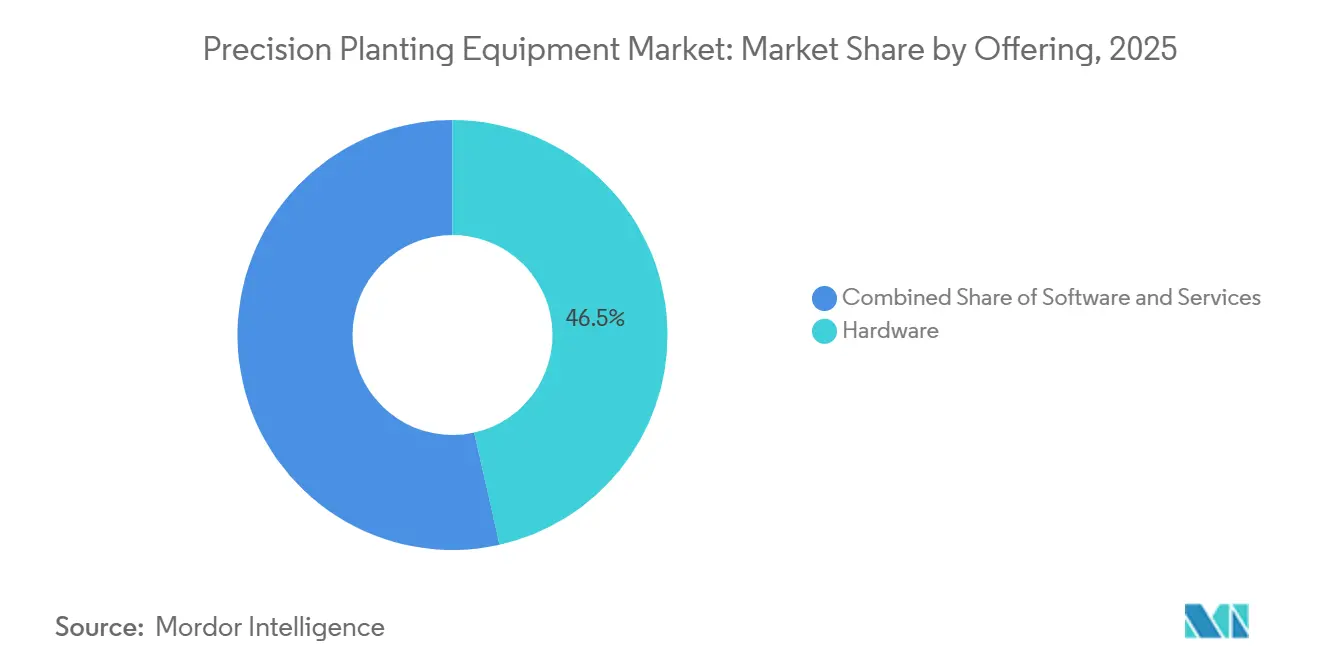

- By offering, hardware led with 46.5% market share in 2025, while services is forecast to expand at an 11.4% CAGR through 2031.

- By equipment type, planters held 58% share in 2025, while drones and autonomous seeding equipments recorded the highest projected CAGR at 13.4% through 2031.

- By drive type, electric drive held 55% market size in 2025 and also represents the fastest-growing segment with an 11.6% CAGR through 2031.

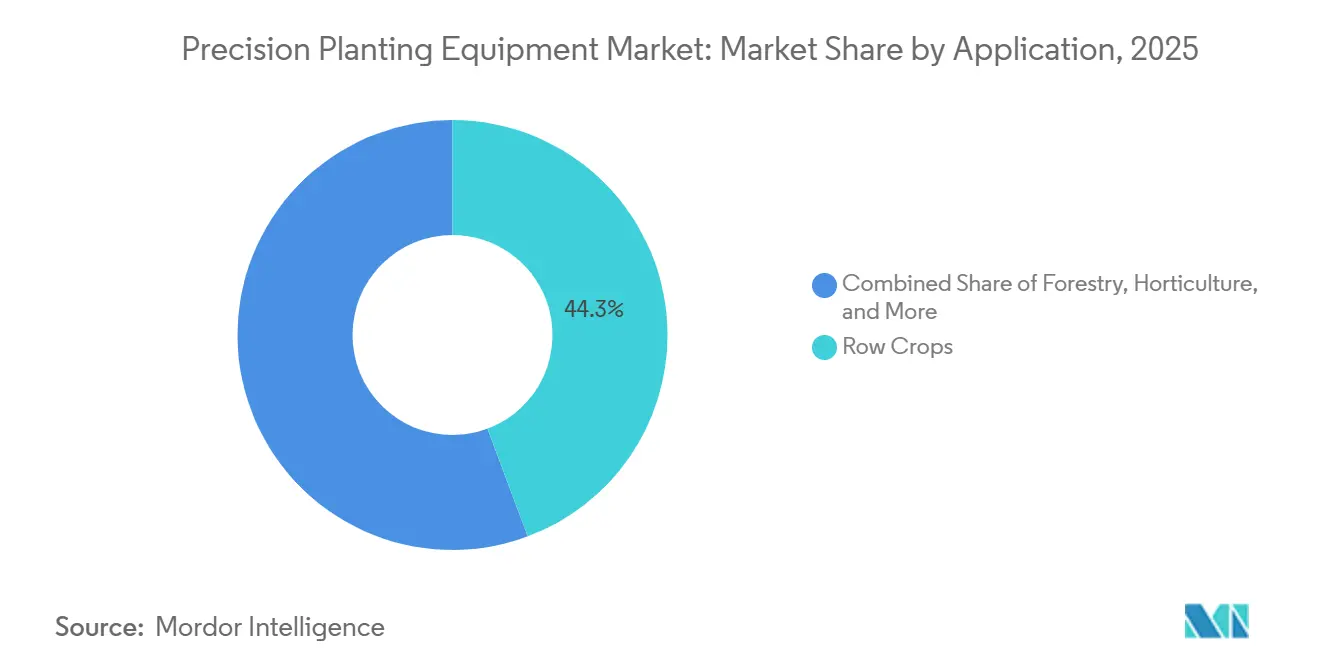

- By application, row crops accounted for 44.3% share of the precision planting equipment market size in 2025, while forestry is projected to expand at a 12.7% CAGR through 2031.

- By farm size, below 400 hectares held 55% share in 2025, while above 400 hectares posted the highest projected CAGR at 11.0% through 2031.

- By geography, North America held 44% of the precision planting equipment market share in 2025, while Asia-Pacific is forecast to grow at a 12.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Precision Planting Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield maximization and food security pressure | +2.5% | Global, highest in Asia-Pacific and South America | Medium term (2-4 years) |

| Input cost reduction through seed and fertilizer efficiency | +2.0% | North America and South America, concentrated in the United States, Brazil, Argentina, and Canada | Short term (≤ 2 years) |

| Labor shortages and compressed planting windows | +1.5% | North America and Oceania, concentrated in the United States, Canada, and Australia | Short term (≤ 2 years) |

| Government support and sustainability-linked mechanization | +1.0% | Europe and Asia-Pacific, concentrated in Germany, France, India, and China | Medium term (2-4 years) |

| Premium seed economics favor singulation and row-level control | +1.2% | North America and South America, concentrated in the United States, Brazil, and Argentina | Medium term (2-4 years) |

| Retrofit economics extend the installed planter base | +1.0% | North America and Oceania, concentrated in the United States, Canada, Brazil, and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Yield Maximization and Food Security Pressure

The precision planting equipment market is influenced by the growing demand for food, while crop producers face limitations in expanding arable land. USDA ERS projected total grain demand across 83 low and middle-income countries to grow at 2.2% annually through 2035, which keeps output pressure elevated across major cropping systems. The same assessment showed the grain demand shortfall rising from 271.4 million metric tons in 2025 to 394.3 million metric tons by 2035 across Asia and Sub-Saharan Africa, which points to a sustained need for higher field productivity. That pressure matters at planting because emergence uniformity, seed placement, and seed-to-soil contact set the ceiling for later crop performance. A 2025 systematic review in Frontiers in Agronomy found that precision agriculture raised yields by 10% to 15% in European Union (EU) trials while reducing fertilizer use by 25% and water use by 30%. The precision planting equipment market, therefore, benefits from a structural demand signal rather than a short-lived equipment cycle. This is especially relevant in Asia-Pacific and South America, where export crops and food security goals both raise the value of each planted acre. As growers face tighter land, water, and nutrient constraints, planting accuracy becomes one of the earliest and most controllable ways to protect final yield.

Input Cost Reduction through Seed and Fertilizer Efficiency

The precision planting equipment market is also advancing because every missed seed, double drop, or overlap now carries a clearer financial penalty. Electric metering systems improve population control and reduce maintenance exposure compared with older mechanical layouts, which directly supports better use of expensive seed inputs. Alabama Cooperative Extension reported that electric drives can deliver population accuracy advantages of up to 20% over mechanical predecessors while removing chain and shaft maintenance. Deere states that its ExactShot liquid fertilizer system can reduce in-furrow nutrient use by up to 60% by applying fertilizer only where seed is present, which turns row-level control into a direct cost-saving tool. Deere also reported a 23% reduction in overpopulation on curved rows through its AccuRate meter design, which shows how section control and curve compensation protect seed economics in irregular field shapes. These operating gains support the case for higher-spec planters and upgrade kits even when crop prices are uneven. The precision planting equipment market gains from this driver because growers no longer view planting precision only as a yield tool. It is increasingly treated as an input cost control tool that protects seed, fertilizer, and operating time in the same pass.

Labor Shortages and Compressed Planting Windows

The precision planting equipment market is being driven by ongoing labor constraints that are reshaping how growers define a workable planting window. With increasing weather variability, reduced labor availability, and tighter timing for optimal soil conditions, farmers are under pressure to complete planting more efficiently. As a result, there is a growing demand for equipment that enables faster operations without compromising seed placement accuracy, allowing more acreage to be covered within a limited timeframe using fewer workers. Manufacturers are responding by enhancing the speed and efficiency of existing equipment through upgrade kits, reflecting strong demand for performance improvements that maintain precision. At the same time, autonomous seeding technologies are beginning to transition from pilot stages to real-world field applications, signaling a shift toward greater automation in planting operations. Overall, the market benefits from this trend as it drives both investments in new machinery and incremental upgrades. With seasonal labor becoming harder to secure, growers increasingly prioritize solutions that allow a single operator to manage larger areas while maintaining consistent planting quality.

Government Support and Sustainability-Linked Mechanization

The precision planting equipment market is receiving help from public policy that links farm modernization to food security, digitization, and resource efficiency. China's National Smart Agriculture Action Plan for 2024 to 2028 set a target for agricultural informatization rates above 30% by the end of 2026 and identified Beidou-assisted digital operations as a national priority. China also expanded its agricultural machinery replacement subsidy program in 2025 and added new equipment categories that include plant protection drones, which strengthens the broader digital mechanization environment[2]Source: Government Action Plan, “National Smart Agriculture Action Plan Published,” USDA Foreign Agricultural Service, apps.fas.usda.gov. This policy backdrop matters because it reduces hesitation around equipment purchases that improve data capture and application accuracy. In Europe, compliance needs tied to input-use efficiency and sustainability reporting continue to support interest in systems that document field operations with greater precision. India is also moving in the same direction through broader mechanization and digital agriculture efforts, even if adoption remains uneven across regions. The precision planting equipment market benefits from these programs, as they soften cyclical weakness in farm cash flow and align digital upgrades with public policy goals. Over time, the value of planting systems that support traceability, reduce overlap, and improve documentation becomes increasingly evident in both developed and emerging farm economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront investment and financing pressure | -1.5% | India, Brazil, South Africa, Turkey, and wider developing Asia-Pacific markets | Long term (≥ 4 years) |

| Technical complexity and training gaps | -1.0% | India, South Africa, Brazil, Turkey, and broader developing market dealer networks | Medium term (2-4 years) |

| Interoperability friction across mixed fleets and data standards | -0.8% | North America, Germany, Brazil, and Australia | Medium term (2-4 years) |

| Connectivity dependence and electronics cost inflation | -0.7% | India, South Africa, Saudi Arabia, and other rural RTK-sparse geographies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Investment and Financing Pressure

The precision planting equipment market still faces a basic capital barrier, especially outside the most mature farm machinery regions. The United States Government Accountability Office (US GAO) reported that variable-rate technology applicators carry a premium of USD 5,600, and replacement yield monitors cost around USD 8,000, demonstrating that even single components can raise the total ownership burden. When full planter upgrades include electric drive systems, monitors, controllers, and downforce components, total spending can quickly exceed what many growers can finance during a weak income cycle. This issue is more pronounced in developing markets, where interest costs are higher, and subsidy coverage is incomplete. Smaller farms may still see the agronomic value, but they often delay adoption because the savings arrive over several seasons while the cash outlay is immediate. The precision planting equipment market, therefore, grows unevenly across regions, with stronger uptake in areas where retrofit paths, dealer financing, or policy support reduce the entry hurdle. This restraint also affects product mix, since growers may favor partial upgrades over fully integrated precision packages. As long as farm incomes stay cyclical, financing pressure will continue to slow adoption at the lower end of the customer base.

Technical Complexity and Training Gaps

The precision planting equipment market is also limited by the skill required to install, calibrate, and operate advanced planting systems correctly. The US GAO identified knowledge barriers and data-related challenges as material limits on broader precision agriculture adoption, which remains relevant for planting technologies that rely on multiple displays, sensors, and prescription layers. A planter can now involve row-unit electronics, guidance interfaces, section control, data export settings, and software updates that must work together in the field. If operators are not confident with setup and troubleshooting, the perceived risk of downtime rises during the most time-sensitive days of the season. Dealer support becomes critical, yet training quality varies by region and by brand coverage. AGCO's push to expand its PTx Trimble dealer footprint highlights how vendor networks are responding to the need for stronger setup and service capabilities. The precision planting equipment market cannot convert product capability into full adoption unless growers and dealers can use these systems reliably. In many emerging markets, the technical gap is not about interest in precision. It is about whether the local support ecosystem is deep enough to make the technology dependable at planting time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Revenue Rising on Connected Agronomy Momentum

Hardware accounted for 46.5% of the precision planting equipment market size in 2025, which kept it as the largest offering segment while services moved ahead as the fastest-growing segment at an 11.4% CAGR through 2031. The hardware lead reflects the continued importance of row units, meters, controllers, sensors, and guidance components that still define the main capital purchase in the precision planting equipment market. Even so, the growth profile is shifting because growers increasingly expect setup, calibration, data interpretation, and software support to come with the machine rather than after the sale. AGCO stated that its PTx platform is targeting USD 2 billion in precision agriculture revenue by 2029, which shows how major suppliers are building a larger recurring revenue layer around connected solutions[3]Source: AGCO CORPORATION “AGCO Accelerates PTx Dealership Expansion Across North America,” AGCO CORPORATION, news.agcocorp.com . This pattern suggests that future value capture will depend less on standalone hardware margins and more on how effectively suppliers attach services to field operations.

The services segment is gaining momentum because the installed base of connected equipment now needs more dealer-led support, data handling, and agronomic guidance. Growers are asking for help with prescription execution, seasonal optimization, and mixed-fleet integration, not only with equipment delivery. That creates a larger role for subscription software, seasonal consulting, and managed planting programs within the precision planting equipment market. The stronger this service layer becomes, the more durable customer retention tends to be because the relationship extends beyond the original equipment sale. This also favors suppliers with large dealer networks and digital platforms that can support growers over multiple seasons. Hardware will remain foundational, but the segment mix is clearly moving toward bundled solutions where software and support rise faster than steel and iron.

By Equipment Type: Planters Lead as Drones Redefine the Growth Ceiling

Planters captured 58% of the precision planting equipment market share in 2025, which confirms that most spending still sits inside row-crop planting systems. That lead reflects the central role of planter accuracy in stand establishment, emergence uniformity, and row-level input control across corn, soybean, and similar cropping systems. Kinze's 5000 Series lineup is now electric-drive only, which shows how leading manufacturers have turned electric metering from a premium feature into a core specification. Vaderstad AB has also positioned its Tempo line around individual electric drives and wireless control, reinforcing the same design direction in the precision planting equipment market. This concentration around planters explains why OEM innovation still focuses so heavily on row-unit architecture, speed, singulation, and upgrade compatibility.

Drones and autonomous seeding equipment are forecast to grow at a 13.4% CAGR through 2031, which makes them the fastest-growing equipment type, even from a smaller base. Their growth reflects wider interest in unmanned field operations, lighter deployment models, and direct seeding use cases that were once treated as experimental. The rise of this segment does not reduce the importance of planters, but it does widen the technology ceiling for the precision planting equipment market. Autonomous and drone-enabled systems are especially relevant where labor availability is tight or terrain makes conventional coverage harder. They also fit well with policy support for agricultural digitization and the growing comfort level around autonomous operations. Over time, this segment is likely to stay smaller than conventional planters in revenue, but it will keep influencing how manufacturers think about seeding, control, and fleet design.

By Drive Type: Electric Drive Consolidates Its Majority Share

Electric drive systems held 55% share in 2025 and represented the fastest-growing drive segment at an 11.6% CAGR through 2031, which gives them a clear majority position in the precision planting equipment market. This rise has been driven by row-by-row shutoff, curve compensation, variable-rate capability, and lower maintenance exposure compared with chain and shaft systems. Alabama Cooperative Extension confirmed that electric drives reduce hydraulic lag, lower vibration-related spacing errors, and enable higher meter speeds, which helps explain why adoption has moved quickly. Once growers experience cleaner control across individual rows, the step back to older architectures becomes harder to justify. That is why electric drive is no longer a niche feature in the precision planting equipment market.

Hydraulic drives still retain a place in certain retrofit cases and lower-cost configurations where growers want incremental gains without full electrical conversion. Even so, the product pipeline remains pointed toward electricity, with Monosem's ValoTerra platform using a 56V architecture and row-by-row motor control. Kinze's all-electric 5000 Series planters and the broader move toward fully controlled row units show how quickly supplier investment has consolidated around this approach. Electric drive also fits better with software-led planting because it enables finer prescription execution and faster response on each row unit. That makes it the natural base for future automation, autonomy, and service diagnostics in the precision planting equipment market. Hydraulic systems will not disappear immediately, but their role is becoming more selective as platform expectations rise.

By Application: Row Crops Lead, Forestry Demonstrates the Highest Growth Potential

Row crops accounted for 44.3% of the precision planting equipment market size in 2025, which kept them as the largest application segment by a wide margin. This dominance reflects the fact that precision planting technologies were first built around crops where seed spacing, emergence timing, and plant population have a direct effect on yield. Corn and soybean systems in North America, Brazil, Argentina, and China continue to shape global planter design, dealer capability, and upgrade demand. That keeps row crops at the center of the precision planting equipment market even as new applications broaden the addressable base. The segment also benefits from the strongest retrofit economics because row-crop growers have the clearest path to measurable gains from meter, drive, and guidance upgrades.

Forestry is forecast to expand at a 12.7% CAGR through 2031, making it the fastest-growing application even though it starts from a smaller base. This growth reflects rising interest in afforestation, restoration programs, and planting systems that can support better survivability and species placement. The segment broadens the role of the precision planting equipment market beyond mainstream grain production and into long-cycle land management use cases. Horticulture and controlled environment settings are also becoming more relevant as seed costs rise and spacing precision becomes more valuable in high-value crops. A 2025 study in Frontiers in Plant Science on potato precision planter metering systems highlights the growing research effort behind specialty crop applications. That research pipeline suggests that non-row-crop uses will keep expanding the market's technology range even if row crops stay dominant in revenue.

By Farm Size: Below 400 Hectares Dominates, Larger Operations Drive the Growth Curve

Below 400 hectares accounted for 55% of 2025 revenue, which shows that the precision planting equipment market is not limited to very large farms. This segment leads because mid-sized farms are more numerous globally and because retrofit products have lowered the practical entry point for precision adoption. Deere designed its meter upgrade kits to fit older planter platforms, while Ag Leader continues to market upgrade paths that improve existing row units rather than forcing full replacement. That matters because many growers want step-by-step modernization instead of a full new machine decision. The result is a broader customer base for the precision planting equipment market than its large-farm image might suggest.

Above 400 hectares is forecast to grow at an 11.0% CAGR through 2031, making it the fastest-growing farm-size group because scale intensifies the value of speed, integration, and documentation. Large operations benefit more quickly from full-system precision because small efficiency gains are multiplied across a much larger acre base. Bourgault's large-width ParaLink hoe drill platform reflects how equipment design changes when farms need consistent depth control and digital management across very wide working spans. These farms are also better placed to absorb training, software, and connectivity investments that smaller operators may postpone. That is why the growth curve is steeper at the top end even though the revenue base remains larger below 400 hectares. In effect, the precision planting equipment market is broadening downward through retrofits while deepening upward through fully integrated systems.

Geography Analysis

North America held 44% of the precision planting equipment market share in 2025, and the region is projected to grow at a 9.2% CAGR through 2031. The United States and Canada remain the core of regional demand because large row-crop operations continue to invest in electric drive planters, real-time monitoring, and retrofit programs. Deere's upgrade strategy for planters dating back to 2005 illustrates how the region supports both new sales and installed-base monetization at the same time. This combination of scale, dealer depth, and upgrade readiness keeps North America at the center of the precision planting equipment market. Mexico remains smaller, but it adds incremental demand in irrigated corn and sorghum areas where precision gains are becoming more attractive.

Asia-Pacific is the fastest-growing regional block at a 12.5% CAGR through 2031, which makes it the main expansion engine for the precision planting equipment market. China is the largest policy anchor in the region because its smart agriculture plan set explicit informatization targets and backed wider use of digital operations across major crops. China's 2025 subsidy expansion for agricultural machinery replacement further strengthens the adoption environment for digitally enabled equipment categories. Australia also contributes a mature precision seeding base because large farm structures support high-capacity systems and wider digital integration. Across the region, the growth pattern combines policy support, food production pressure, and an expanding commercial-scale farming segment.

South America is experiencing steady growth, led by Brazil and Argentina, where large soybean and corn farming operations sustain strong demand for planting equipment. The region continues to attract technology providers due to its importance as a mixed-fleet precision agriculture market. Europe is also expanding, supported by sustainability-driven farming practices and demand for adaptable precision equipment suited to smaller and more fragmented fields. The Middle East and Africa are developing more gradually, with growth concentrated in specific markets supported by food security initiatives and mechanization programs. However, broader adoption remains constrained by cost and connectivity challenges. Overall, the precision planting equipment market is advancing most rapidly in regions where agronomic needs, supportive policies, and strong distribution networks align.

Competitive Landscape

The precision planting equipment market shows moderate concentration, with Deere and Company, AGCO Corporation, CNH Industrial N.V., Kinze Manufacturing, and Ag Leader Technology together holding significant revenue share in 2025. This structure gives the leading group real scale advantages, but it still leaves meaningful room for retrofit specialists and regional manufacturers. Deere remains strong because it can sell into a large installed base and then deepen customer value through upgrades such as the ExactEmerge Meter Upgrade Kit and MaxEmerge 5e Meter Upgrade Kit. AGCO changed the competitive map when it closed the PTx Trimble joint venture in 2024, combining AGCO's precision assets with Trimble's capabilities to strengthen both factory-fit and mixed-fleet retrofit channels. These moves show that scale in the precision planting equipment market now depends on digital reach and installed-base access as much as on new equipment sales.

The next layer of competition comes from specialists who are narrowing the gap through focused technology choices. Kinze has leaned into all-electric planters, which supports a clear product identity around speed, row control, and modern meter architecture. Vaderstad AB has continued to improve the Tempo platform and announced its next-generation row unit with updated electronics and prescription-map-controlled planting depth, which keeps it competitive in high-performance planting systems. Monosem is taking a similar path through 56V electric architectures and row-by-row rate modulation across multiple inputs. These companies matter because they push the precision planting equipment market toward deeper row-unit functionality rather than only broader machine size. Their presence also limits how much the top tier can rely on legacy brand loyalty alone.

Competitive strategies are increasingly focused on three key areas retrofits, fully electric platforms, and software-integrated service layers. AGCO's dealership expansion for PTx Trimble in North America shows how distribution itself has become part of the strategic playbook. Deere's retrofit-first approach targets growers who want faster and more accurate planting without buying a whole new planter, while European suppliers continue to compete through multi-crop versatility and compact platform design. That combination keeps the precision planting equipment market moderately concentrated rather than tightly closed. The leaders are clear, but product innovation and mixed-fleet demand still give challengers room to take share.

Precision Planting Equipment Industry Leaders

Deere and Company

AGCO Corporation

CNH Industrial N.V.

Kinze Manufacturing, Inc.

Ag Leader Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AGCO accelerated PTx dealership expansion across North America, with PTx Trimble integrated into over 50 additional Fendt and Massey Ferguson dealers in the US and Canada within one year of launch, and all AGCO North American production agriculture dealerships are targeted for the PTx Trimble portfolio by the end of 2025.

- February 2025: Deere and Company launched the ExactEmerge Meter Upgrade Kit and MaxEmerge 5e Meter Upgrade Kit, enabling existing planter owners from 2015 onward to access 10 mph planting speed and up to 20% improved population accuracy without replacing row units; this retrofit-first approach extends precision capability across a legacy installed base dating to 2005.

- February 2024: Kinze Manufacturing, Inc. launched the 5900 and 5700 all-electric 5000 Series planters for MY2024, offering True Speed meters up to 12 mph, with the 5670 pivot-fold split-row planter announced for MY2025, and all models use the Kinze 5000 Series row unit and Blue Vantage display with FieldView integration. This product innovation enhances planting speed, thereby improving operational efficiency and supporting increased adoption in the precision planting equipment market

Global Precision Planting Equipment Market Report Scope

The Precision Planting Equipment Market refers to the industry encompassing advanced machinery, systems, and technologies used to optimize seed placement during planting operations. These solutions are designed to improve accuracy in seed spacing, depth, timing, and population, thereby enhancing crop yields and input efficiency.

The Precision Planting Market Report is Segmented by Offering (Hardware, Software, and Services), Equipment Type (Planters, Seed Drills and Air Seeders, Planting Attachments and Add-Ons, and Drones and Autonomous Seeding Equipments), Drive Type (Electric Drive and Hydraulic Drive), Application (Row Crops, Cereals, Oilseeds, and Pulses, Forestry, Horticulture, Greenhouse and Controlled Environment Farming), Farm Size (Below 400 Ha and Above 400 Ha), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Report Offers the Market Size and Forecasts in Terms of Value (USD).

| Hardware | Automation and Control Systems |

| Sensing and Monitoring Systems | |

| Software | Farm Management and Mapping Software |

| Prescription and Analytics Software | |

| Services | System Integration and Consulting |

| Managed and Connected Services | |

| Training and Support Services |

| Planters |

| Seed Drills and Air Seeders |

| Planting Attachments and Add-Ons |

| Drones and Autonomous Seeding Equipments |

| Electric Drive |

| Hydraulic Drive |

| Row Crops |

| Cereals, Oilseeds, and Pulses |

| Forestry |

| Horticulture |

| Greenhouse and Controlled Environment Farming |

| Below 400 Hectares |

| Above 400 Hectares |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Offering | Hardware | Automation and Control Systems |

| Sensing and Monitoring Systems | ||

| Software | Farm Management and Mapping Software | |

| Prescription and Analytics Software | ||

| Services | System Integration and Consulting | |

| Managed and Connected Services | ||

| Training and Support Services | ||

| By Equipment Type | Planters | |

| Seed Drills and Air Seeders | ||

| Planting Attachments and Add-Ons | ||

| Drones and Autonomous Seeding Equipments | ||

| By Drive Type | Electric Drive | |

| Hydraulic Drive | ||

| By Application | Row Crops | |

| Cereals, Oilseeds, and Pulses | ||

| Forestry | ||

| Horticulture | ||

| Greenhouse and Controlled Environment Farming | ||

| By Farm Size | Below 400 Hectares | |

| Above 400 Hectares | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of precision planting equipment in 2026?

The precision planting equipment market stands at USD 6.06 billion in 2026 and is projected to reach USD 9.77 billion by 2031 at a 10.02% CAGR.

Which region is growing fastest through 2031?

Asia-Pacific is projected to be the fastest-growing region, registering a CAGR of 12.5% during 2026–2031, supported by smart agriculture policies, digitization goals, and rising food production pressure.

Why do electric drive systems lead adoption?

Electric drive held a 55% market share in 2025 because it improves row-by-row control, reduces maintenance requirements, and supports variable-rate planting and curve compensation capabilities.

Which product areas are expanding the fastest?

Drones and autonomous seeding equipment are projected to register the highest CAGR of 13.4% during 2026–2031, driven by increasing interest in autonomous farming operations and labor-saving technologies.

What is the biggest application area today?

Row crops remain the largest application with 44.3% share in 2025 because precision planting has the clearest agronomic and economic payoff in corn and soybean systems.

What is holding adoption back in some regions?

High upfront cost, operator training needs, mixed-fleet interoperability issues, and uneven connectivity still slow rollout, especially in developing markets.

Page last updated on: