Precision Irrigation Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.16 Billion |

| Market Size (2031) | USD 14.15 Billion |

| Growth Rate (2026 - 2031) | 9.08% CAGR |

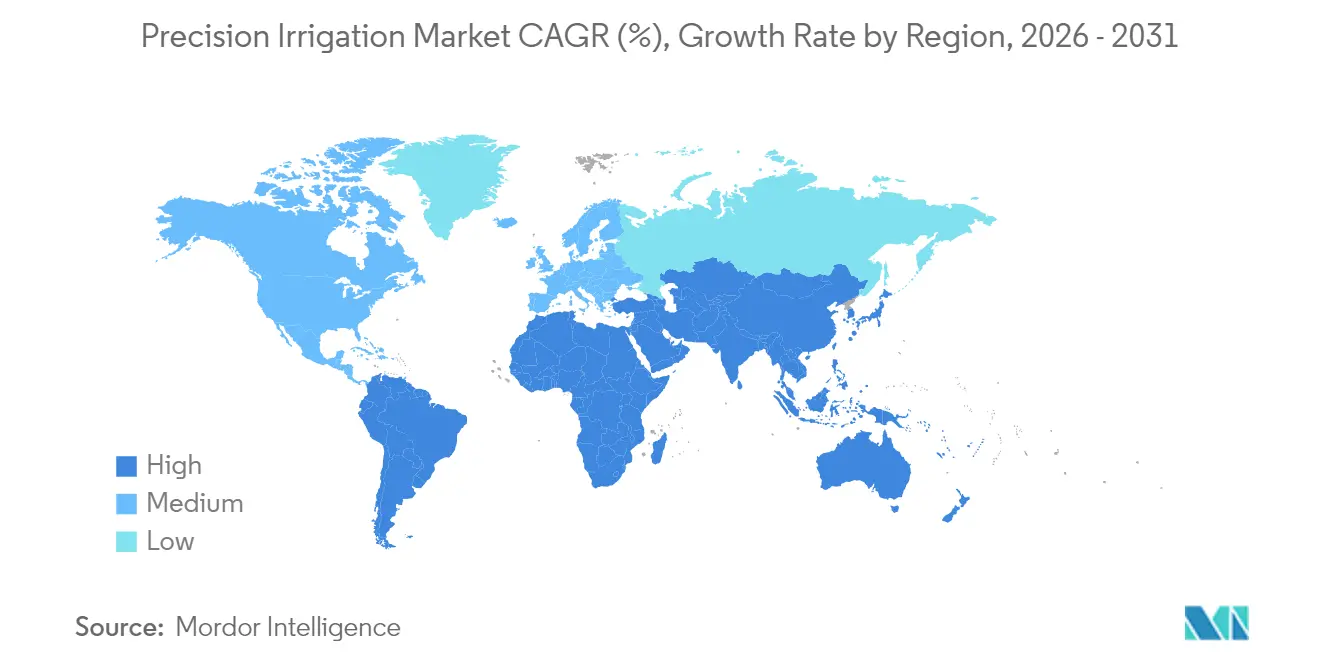

| Fastest Growing Market | Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precision Irrigation Market Analysis by Mordor Intelligence

The precision irrigation market size was valued at USD 8.4 billion in 2025 and estimated to grow from USD 9.16 billion in 2026 to reach USD 14.15 billion by 2031, at a CAGR of 9.08% during the forecast period (2026-2031). Climate-driven water scarcity, stricter groundwater allocations, and subsidy programs that defray up-front costs are accelerating equipment replacement cycles and tilting capital toward drip and variable-rate platforms. Mid-size farms continue to dominate the installed base, yet larger enterprises are scaling automation fastest as labor constraints and centralized water management push them toward sensor-driven scheduling. Hardware margins are compressing as commoditized Internet of Things (IoT) sensors enter the channel, redirecting supplier focus toward subscription software that bundles telemetry, analytics, and compliance reporting. Competitive intensity remains moderate, with major players still controlling a majority of global revenue, while sensor-agnostic software entrants are unbundling legacy stacks and capturing growers that refuse to scrap functional pivots.

Key Report Takeaways

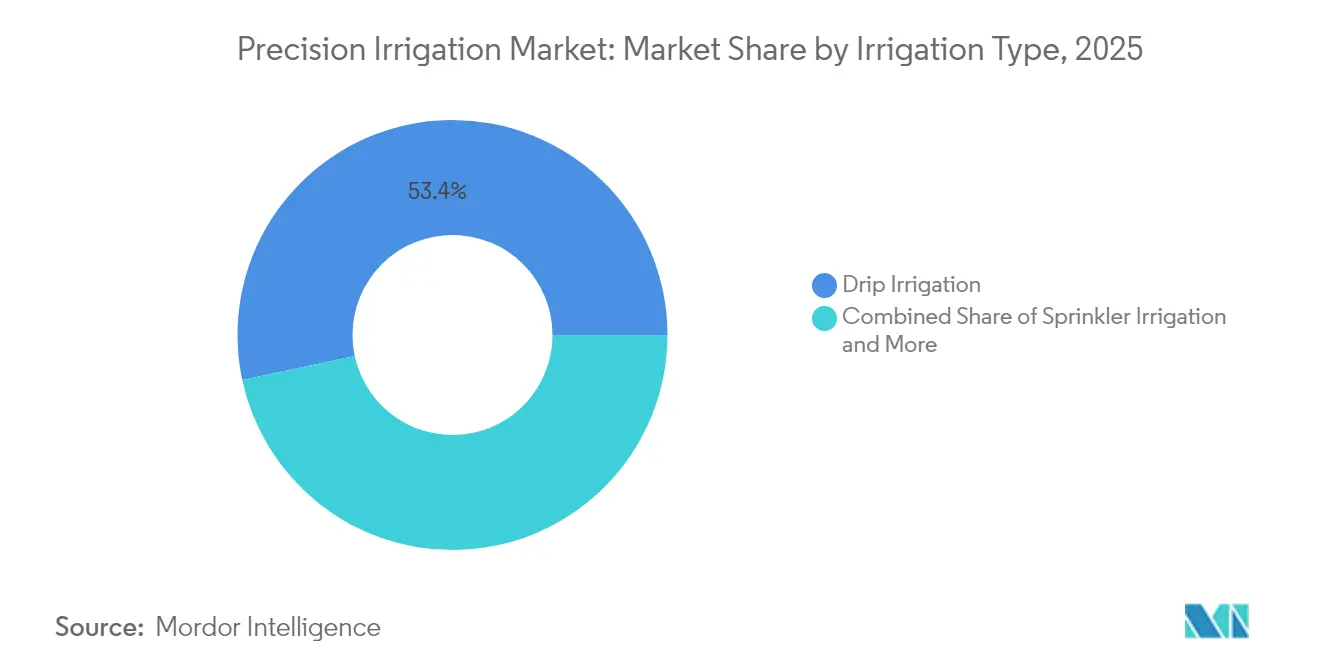

- By irrigation type, drip irrigation led with a 53.35% share of the precision irrigation market in 2025 and is also projected to expand at a 10.42% CAGR through 2031.

- By component, controllers and timers held a 31.40% market share in the precision irrigation market in 2025, while software and services are poised to grow at a 11.57% CAGR through 2031.

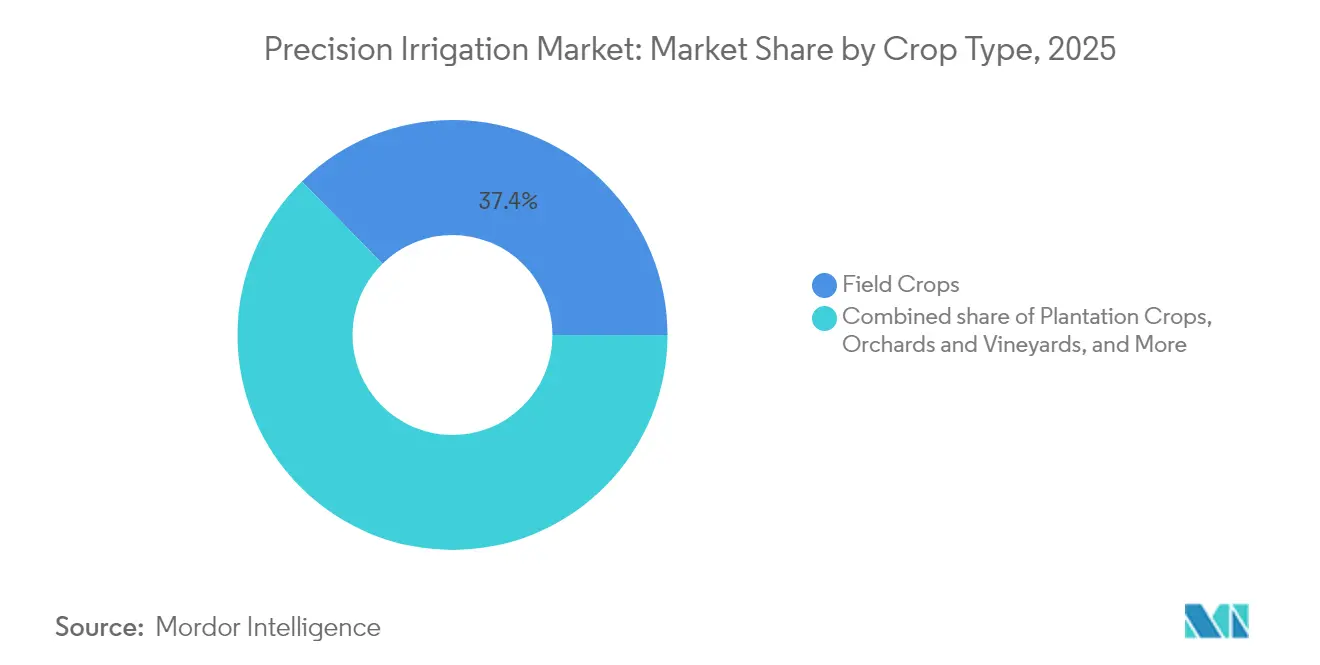

- By crop type, field crops accounted for 37.35% of the precision irrigation market share in 2025, whereas orchards and vineyards are set to advance at an 10.82% CAGR through 2031.

- By geography, North America commanded a 31.55% market share in the precision irrigation market in 2025, while Africa is the fastest-growing region, with a 10.05% CAGR projected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Precision Irrigation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy Expansions for Water-Efficient Farming | +1.8% | North America, Europe, India, and Australia | Medium term (2–4 years) |

| Rising Adoption of Drip Systems in Horticulture Clusters | +1.5% | Asia-Pacific, South America, and Mediterranean Europe | Medium term (2–4 years) |

| Integration of Soil-Moisture IoT (Internet of Things) Sensors | +1.3% | North America, Europe, Australia, and select Asia-Pacific | Short term (≤ 2 years) |

| Pivot-Retrofit Kits Lowering CAPEX for Mid-Size Farms | +0.9% | North America, South America, and Australia | Short term (≤ 2 years) |

| Corporate Net-Zero Pledges Driving Water-Use KPIs | +0.7% | Global, led by North America, and Europe | Long term (≥ 4 years) |

| Surge in Agri-Venture Capitalist Funding for Water-Stress Regions | +0.6% | Middle East, Africa, and South Asia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Subsidy Expansions for Water-Efficient Farming

Rebate programs are cutting payback periods on drip and pivot upgrades from seven to fewer than four years, lifting adoption among cash-constrained growers. Arizona and California disbursed a combined USD 75 million in 2024 to cotton, dairy, and specialty-crop producers, reducing net capital outlays by up to 50% [1]Source: State of California Department of Food and Agriculture, “State Water Efficiency and Enhancement Program,” Cdfa.ca.gov. Australia extended its On-Farm Emergency Water Infrastructure Rebate Scheme through 2025, covering half of sensor and controller costs to counter drought pressure in the Murray-Darling Basin. India’s Pradhan Mantri Kisan Urja Suraksha Evam Utthan Mahabhiyan Yojana (PM-KUSUM) initiative paired solar pumps with drip kits for 180,000 farmers, effectively solving energy and water challenges in one bundle. Carbon-credit linkages embedded in many of these programs let growers monetize water savings, further improving project economics for early adopters.

Rising Adoption of Drip Systems in Horticulture Clusters

High-value fruit and vegetable belts are switching from flood to drip at rates surpassing broader row-crop trends. California’s Central Valley reached 78% drip penetration in almond acreage during 2024, a surge tied to groundwater caps under the Sustainable Groundwater Management Act. Spain’s Almería greenhouses operate nearly exclusively on recirculating drip networks that exceed 90% water-use efficiency, a benchmark now influencing Morocco and Turkey. India’s Nashik grape belt posted 22% annual growth in drip installations, cutting system costs to USD 800 per hectare after subsidies. Chile’s export-oriented blueberry growers adopted subsurface drip to mitigate salt stress, lifting yields 18% while trimming water use by 35%.

Integration of Soil-Moisture IoT (Internet of Things) Sensors

Bundling sensors with drip equipment trims water application by as much as 30% versus timer-based schedules, easily offsetting the USD 150–300 per-hectare sensor premium where volumetric pricing exists. Reinke’s 2024 partnership with CropX embeds telemetry in pivot panels, letting growers vary rates every 10 meters and cut usage by 18% on average. Valmont logged 42,000 FieldNET Advisor subscriptions in 2024, up 28% year on year, at annual fees near USD 10 per hectare. Australia’s cotton farms, operating under water-trading markets, reached 34% sensor adoption, showing that pricing signals accelerate digital upgrades. The Environmental Protection Agency (EPA) WaterSense label now certifies smart controllers that deliver at least 20% water savings, opening new municipal rebate channels.

Pivot-Retrofit Kits Lowering CAPEX for Mid-Size Farms

Retrofit modules turn legacy pivots into variable-rate systems for USD 18,000–25,000 per tower, a level mid-size growers can finance within three to four years. Nebraska and Kansas recorded 1,200 such retrofits in 2024, with state cost-share programs funding 40% of expenses. Brazil’s Cerrado growers favor retrofits because short land-lease terms discourage full system replacement; adoption climbed to 8% of installed pivots in 2024. Variable-rate fertigation delivered through these retrofits boosted nutrient-use efficiency 15% in Kansas trials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Cost Versus Flood Irrigation | −1.2% | Asia-Pacific, Africa, and South America | Medium term (2–4 years) |

| Fragmented Landholding in Emerging Economies | −0.9% | South Asia, Sub-Saharan Africa, and Southeast Asia | Long term (≥ 4 years) |

| Limited After-Sales Service Networks in Africa | −0.5% | Sub-Saharan Africa, and parts of the Middle East | Medium term (2–4 years) |

| Data-Privacy Concerns Around Connected Irrigation Controllers | −0.3% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Cost Versus Flood Irrigation

Precision systems still cost more than 200% above flood infrastructure, which deters growers without access to low-interest credit. A 40-hectare subsurface drip install in India ranges from USD 2,500 to USD 3,200 per hectare after subsidy, while flood canals need only USD 800, so many vegetable producers delay upgrades until water caps force action. In Kenya, drip kits priced near USD 1,200 per hectare equal roughly 60% of rural household income, leaving adoption almost entirely dependent on donor grants [2]Source: World Bank, “Irrigation Projects in Sub-Saharan Africa,” Worldbank.org. Annual filtration and emitter maintenance add 15–20% to operating budgets, which weakens the water-savings argument when energy prices remain low.

Fragmented Landholding in Emerging Economies

Small plot sizes amplify per-hectare costs because fixed expenses for controllers and sensors do not scale down smoothly. India’s mean holding fell to 1.08 hectares in 2024 and 86% of farms now sit below the two-hectare mark where automation begins to pay off. Sub-Saharan Africa shows a similar pattern, with 80% of farms smaller than 2 hectares, which limits dealer interest and raises service call distances [3]Source: Food and Agriculture Organization, “Smallholder Farming in Sub-Saharan Africa,” Fao.org. Collective procurement has made little headway because only 12% of India’s Farmer Producer Organizations bought irrigation equipment together in 2024, mainly due to governance and credit hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Irrigation Type: Mobile Drip Enhances Portability

Drip irrigation held a 53.35% market share in the precision irrigation segment in 2025 and is projected to grow at a 10.42% CAGR through 2031, making it both the largest and fastest-growing segment. Subsurface drip irrigation is gaining popularity in row crops such as cotton and corn, as buried lines reduce evaporation and deliver nutrients directly to the root zone, resulting in water use reductions of up to 60% compared to sprinklers. Surface drip remains the workhorse in orchards, vineyards, and high-value vegetable crops; California almond growers, facing extraction caps under the state's groundwater law, increased drip penetration to 78% in 2024. A hybrid called precision mobile drip mounts tape on moveable frames so one system can serve several fields, a cost-saving approach now spreading through Israel, Kenya, and India. Spain’s 31,000-hectare Almería greenhouse hub showcases the cutting edge of technology, operating almost entirely on recirculating drip irrigation that utilizes more than 90% of the applied water.

Sprinkler formats, including traditional, center-pivot, and lateral-move units, comprise the remainder of the precision irrigation market size, yet their growth pace lags behind that of drip as regulators favor low-evaporation options. Center pivots still dominate the Great Plains and Brazil’s Cerrado, but many owners are adding variable-rate retrofit kits that bring drip-like precision to existing hardware. Lateral-move systems, which run straight instead of pivoting, expanded 9% in 2024 because they cover rectangular edges and irregular parcels where pivots fall short. Traditional solid-set and hand-move sprinklers persist in areas with fragmented land tenure, while micro-sprinklers and bubblers fill nursery niches that need gentle delivery. Drip’s edge also comes from fertigation automation, which raised nutrient efficiency 15% in Kansas trials and works on sloped terrain where pivots face engineering limits.

By Component: Recurring Software Revenues Rise

Controllers and timers delivered 31.40% of 2025 component sales, yet their growth is slowing as Internet of Things (IoT) variants commoditize and prices fall. The software and services slice of the precision irrigation market size is projected to climb at an 11.57% CAGR, eclipsing hardware on recurrent subscription value. Flow meters and telemetry valves, now 24.30% of spend, benefit from rules in Australia and California that require real-time reporting. Soil-moisture sensor adoption is strongest in premium crops, capturing 21.10% of revenue after wireless models removed wiring costs.

Suppliers favor hybrid models that bundle low-margin sensors with higher-margin analytics. CropX charges USD 10 per hectare annually for scheduling algorithms that integrate satellite imagery and weather forecasts. The Enviornmental Protection Agency (EPA) WaterSense badge has crossed from turf into agriculture, pushing smart controllers into broad-acre row crops. Attach rates should keep rising as sustainability audits and International Organization for Standardization (ISO) 14046 drive traceable water-footprint reporting.

By Crop Type: Perennial Plantings Justify Higher Capex

Field crops held a 37.35% market share in the precision irrigation segment in 2025, anchored by mechanized cereal and oilseed acres across the Americas and Australia. Orchards and vineyards will outpace all other segments at an 10.82% CAGR to 2031, leveraging premium crop economics that support USD 3,000–5,000 per-hectare subsurface drip. Plantation crops such as sugarcane are adopting drip to raise yield and cut fertilizer losses 22% in Brazilian trials. Turf and ornamentals, influenced by municipal water caps, are using smart sprinklers certified under WaterSense guidelines.

California’s almond sector shows subsurface drip paying back in less than five years through 35% water savings and 8% yield gains. Spain’s olive groves employ deficit irrigation guided by sensors to protect oil quality while shaving 25% off water use. Wine regions in Australia and California use granular irrigation to fine-tune vine stress, a practice tied to higher price points in premium bottlings.

Geography Analysis

North America is projected to lead the precision irrigation market with a 31.55% revenue share in 2025, driven by a substantial center-pivot infrastructure and the United States Department of Agriculture (USDA) programs that subsidize up to 50% of retrofit costs. Additionally, stricter groundwater regulations in California and the Ogallala Aquifer region are increasing the demand for drip irrigation systems and variable-rate pivots. Africa is anticipated to be the fastest-growing market, with a CAGR of 10.05% through 2031, supported by World Bank and African Development Bank loans aimed at financing smallholder drip irrigation projects. Increased donor support and government subsidies in countries such as Kenya, Ethiopia, and Morocco are facilitating the transition of pilot projects into large-scale commercial farming operations.

Europe benefits from Common Agricultural Policy grants that cover half of precision upgrades, while national groundwater caps in Spain and Italy make drip the default choice for fruit and vegetable belts. Asia-Pacific demand is anchored by India’s PM-KUSUM solar-pump bundles and China’s mandatory precision standards on new farmland, creating the world’s largest pipeline of subsidized installations. The Middle East relies on state-backed financing under Saudi Vision 2030 and the United Arab Emirates food-security plan, which require precision systems for new agricultural projects. South America’s growth stems from Brazil’s Cerrado and Argentina’s Pampas, where pivots extend cropping into marginal zones subject to erratic rainfall.

North America is projected to add variable-rate technology to legacy pivots, shortening payback periods as energy costs rise and water allocations tighten. Europe will intensify sensor adoption to meet the European Union’s water-footprint reporting rules, driving software subscriptions that layer onto existing drip networks. Asia-Pacific should see sustained momentum as state subsidies expand to mid-size farms and local manufacturers cut system costs with domestic drip-tape production. Africa’s next challenge is building spare-parts depots and technician networks to keep newly installed systems running, a service gap that forward-looking vendors are racing to fill.

Competitive Landscape

The precision irrigation market remains moderately concentrated, with the top five suppliers accounting for a majority of global revenue in 2024 following a new wave of consolidation. Netafim Ltd (Orbia Advance Corporation), Valmont Industries, Inc., and Lindsay Corporation continue to dominate the market, supported by vertically integrated manufacturing, proprietary technology stacks, and extensive dealer networks that span all major irrigated regions. Rivulis Pte. Ltd. (Temasek Holdings Pte. Ltd.) has increased its market share significantly after acquiring Jain Irrigation’s international assets, highlighting the role of mergers and acquisitions as a fast track to scale in a market where growers typically replace hardware only once every decade. The Toro Company has also entered the top tier, leveraging its expertise in turf-focused smart controllers to expand into agriculture, with notable success in water-scarce regions such as California and Australia.

Technological innovation remains a critical area of competition. Valmont’s FieldNET Advisor reached 42,000 paying subscriptions in 2024, integrating evapotranspiration models with in-field sensors to achieve an average water savings of 18%. Lindsay Corporation expanded its FieldNET platform to include satellite-based crop health imagery, covering 1.2 million hectares and enabling growers to synchronize variable-rate irrigation prescriptions with real-time vegetation indices. Patent activity underscores the emphasis on technology: Netafim secured seven patents related to pressure-compensating emitters and fertigation automation, while Toro obtained five patents for weather-adaptive controller logic and wireless valve communication.

Growth opportunities are emerging in areas such as after-sales services in Africa, small-farm financing in South Asia, and sensor-agnostic analytics that separate software functionality from hardware dependency. Companies like CropX and Semios offer cloud-based dashboards priced at USD 8–15 per hectare, appealing to growers who prefer to retain existing functional equipment. In February 2024, Reinke demonstrated this modular approach by integrating CropX telemetry into its control panels, maintaining pivot sales while generating recurring revenue from data services. Vendors that adopt open data architectures and establish efficient repair networks are well-positioned to capture market share, especially as regulatory requirements and carbon-credit programs make real-time water usage tracking a standard feature rather than an optional upgrade.

Precision Irrigation Industry Leaders

Netafim Ltd (Orbia Advance Corporation)

Valmont Industries, Inc.

Lindsay Corporation

Rivulis Pte. Ltd. (Temasek Holdings Pte. Ltd.)

The Toro Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Precision irrigation demand continues to move toward platforms that make water application measurable and auditable, which supports connected controllers, sensor integration, and software subscriptions that bundle telemetry, analytics, and reporting. Valmont's FieldNET Advisor reached 42,000 paying subscriptions in 2024, and Lindsay expanded FieldNET to include satellite-based crop health imagery across 1.2 million hectares, indicating room for sensor-agnostic, interoperable analytics that add onto existing drip and pivot assets rather than requiring full replacement.

A second opportunity is supply-chain localization and capacity additions that reduce lead times in water-stressed regions and support faster deployment of thin-wall drip, drippers, and retrofit kits. Orbia Netafim opening a 30,000-square-meter manufacturing plant in Hermosillo, Sonora, Mexico in June 2026 strengthens regional availability for the Americas. Large project wins, including Lindsay Corporation's USD 80 million Zimmatic and FieldNET agreement in MENA announced in December 2025, also point to continued procurement of turnkey packages, covering hardware plus digital management, for new irrigated area buildouts. On the demand side, public cost-share and conservation program mechanics, alongside corporate water stewardship, continue to widen adoption channels for monitoring and verification services, including Orbia Netafim's partnership with Amazon India to save about 325 million liters of water annually.

Recent Industry Developments

- June 2026: Orbia Netafim opened a 30,000-square-meter manufacturing plant in Hermosillo, Sonora, Mexico, to produce thin-wall drip irrigation solutions for the Americas. The added regional capacity supports faster fulfillment and lowers logistics friction for drip deployments as growers shift from flood and sprinkler systems toward more water-efficient micro-irrigation.

- December 2025: Lindsay Corporation announced a USD 80 million irrigation project in the Middle East and North Africa to supply Zimmatic systems along with FieldNET technology, with revenue realization extending through fiscal year 2026. Packaging pivots with digital management strengthens Lindsay's recurring software footprint while advancing irrigation modernization programs in water-constrained markets.

- February 2024: Netafim unveiled a hybrid dripline that embeds a pressure-compensating emitter inside a disposable tape to cut installation time while maintaining uniform flow on uneven terrain. This design extends drip applicability in row crops and sloped fields by reducing labor intensity and improving distribution uniformity, supporting faster conversion from less efficient sprinkler or flood practices.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the precision irrigation market is defined as the revenue generated from equipment, software, and services that help apply water at the right time and in the right quantity, using control and sensing to improve farm water efficiency.

Scope exclusions: It excludes conventional flood and non-automated irrigation hardware that does not support measured, controlled, or sensor- or controller-led water application.

Segmentation Overview

- By Irrigation Type

- Sprinkler Irrigation

- Traditional Sprinklers

- Center Pivot Sprinklers

- Lateral / Linear Move Sprinklers

- Drip Irrigation

- Surface Drip Irrigation

- Sub-surface Drip Irrigation

- Precision Mobile Drip Irrigation

- Other Types

- Sprinkler Irrigation

- By Component

- Controllers and Timers

- Flow Meters and Valves

- Soil-Moisture Sensors

- Software and Services

- By Crop Type

- Field Crops

- Plantation Crops

- Orchards and Vineyards

- Turf and Ornamentals

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to map the demand pool and the supply landscape in a way that can be explained and checked. We relied on public agriculture and water data series such as USDA and NASS datasets, FAO databases, World Bank indicators, and irrigation and water management statistics from national ministries and agencies, along with technical papers indexed in peer-reviewed journals.

Next, the model inputs were grounded using practical sources like company annual reports, investor presentations, product catalogs, and association websites covering irrigation and farm mechanization. Where needed, we used paid database subscriptions for company financials, news tracking, patents, and shipment-level trade reads to validate import intensity for irrigation components in key countries. These are illustrative examples, and many other public sources were also referenced for data collection, validation, and clarification during research.

Primary Interviews and Surveys

Primary work was used to convert broad indicators into market-ready assumptions that match how systems are actually purchased and installed. We spoke with a mix of manufacturers, distributors, installers, agronomists, and large farm operators across major regions, so adoption timing, typical system sizing, and price changes could be cross-checked before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 18% | APAC: 48% |

| Mid tier: 49% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 19% | Managers: 51% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction where irrigated acreage, crop mix, and the share of farms adopting drip, sprinkler, and sensor- or controller-based upgrades are translated into an annual demand pool. To keep the math realistic, the model uses practical drivers such as irrigated area trends, subsidy and incentive intensity, water scarcity signals, on-farm labor availability, and typical replacement cycles for emitters, valves, controllers, and sensors.

After that, selective bottom-up approximations are used to corroborate totals, including sampled ASP x volume checks for key components and channel feedback on installation intensity by crop and farm size. Where coverage is incomplete, gaps are handled by using proxy adoption rates from comparable agronomy zones, then adjusting with primary feedback on affordability and availability.

For forecasting, scenario analysis is applied with a base case anchored to expected acreage growth and adoption acceleration, followed by sensitivity checks on pricing progression, subsidy continuity, and drought-year volatility. The final forecast is then aligned to what primary respondents consider realistic for near-term demand and for longer-cycle farm capex decisions.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including irrigated area movement, trade flow direction for key parts, and on-ground channel sentiment about order books. When a variance looks large, assumptions are rechecked, and follow-up outreach is triggered so the driver causing the deviation is understood before sign-off.

A multi-step internal review follows, where the math, unit logic, and region totals are reviewed separately to reduce carryover errors. Reports are refreshed annually, with interim updates when major events change farm economics or policy, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's Precision Irrigation Market Sizing Compared With Other Published Estimates

It is normal to see different published market sizes for precision irrigation because the boundary is not always the same, and the build-up logic can change by source. Differences usually come from what is counted as precision irrigation, the year used as the base, and whether pricing is treated as installed system value or just equipment shipments.

By tracking installed-area adoption and refreshing average system pricing by component and crop, Mordor Intelligence keeps the 2026 total focused on precision enabling hardware, software, and services, instead of folding in broader irrigation machinery or general farm equipment spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.16 B (2026) | |

| Industry Publisher A | USD 8.40 B (2025) | Uses a different base year and a longer horizon, and it can treat smart control layers and advanced analytics as part of the core market even when bundled, which changes the revenue boundary. |

| Syndicated Platform B | USD 5.36 B (2025) | Often relies on a narrower definition closer to irrigation equipment sales, with limited visibility on services and software attachment rates, which tends to reduce the modeled value. |

Overall, the spread mainly comes down to scope boundaries and how adoption and pricing are translated into revenue by year. Our approach stays traceable to irrigated area, technology penetration, and component pricing checks, which makes the estimate easier to reproduce and to update when farm economics shift.

Key Questions Answered in the Report

What was the precision irrigation market size in 2026?

It reached USD 9.16 billion and is projected to hit USD 14.15 billion by 2031.

Why are software and services gaining share?

Growers prefer subscription analytics that bundle sensors, weather data, and compliance reporting, supporting an 11.57% CAGR for this component.

Which region is growing fastest?

Africa leads at a projected 10.05% CAGR, supported by multilateral financing but challenged by service-network gaps.

What restrains adoption among smallholders?

High initial capital, fragmented landholdings, and weak after-sales support raise per-hectare costs and risk.

Page last updated on: