Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

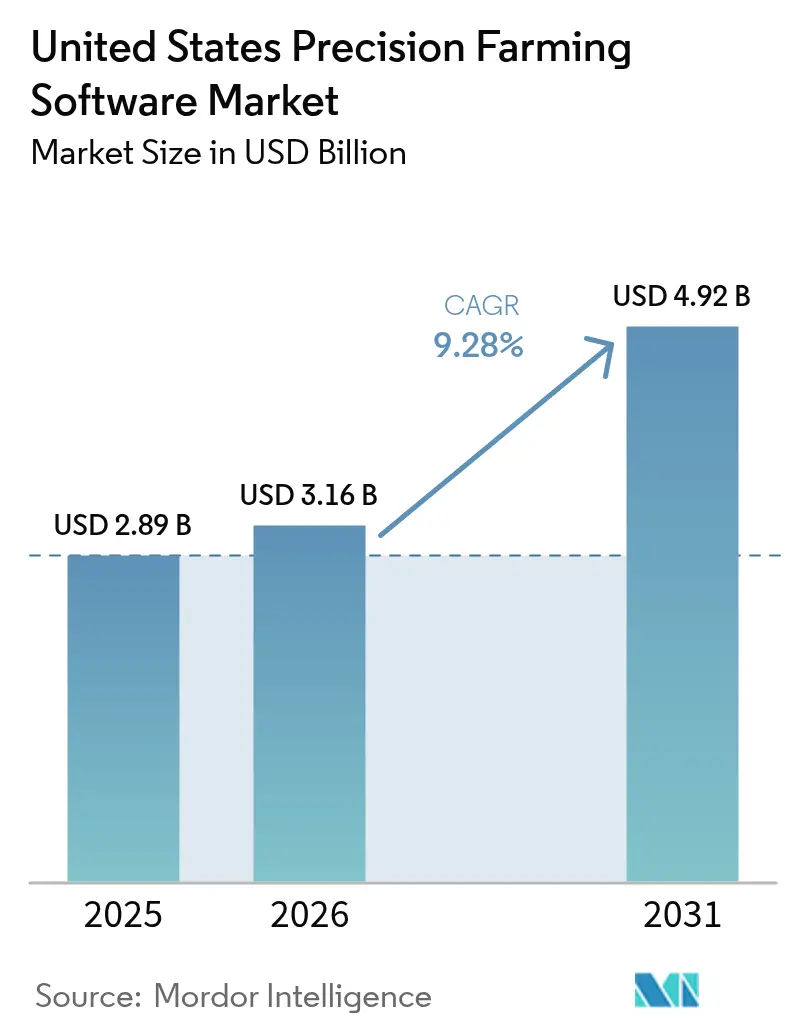

| Base Year Market Size (2025) | USD 2.89 Billion |

| Market Size (2026) | USD 3.16 Billion |

| Market Size (2031) | USD 4.92 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Precision Farming Software Market Analysis by Mordor Intelligence

The United States precision farming software market size was valued at USD 2.89 billion in 2025 and estimated to grow from USD 3.16 billion in 2026 to reach USD 4.92 billion by 2031, at a CAGR of 9.28% during the forecast period (2026-2031). Strong momentum stems from the digitalization of farming practices as operators respond to persistent labor shortages, new climate-smart incentive programs, and expanding rural broadband coverage. Cloud-based platforms, already accounting for most installations, continue to benefit from faster networks that support real-time analytics. Integrated decision-support suites are displacing single-purpose tools because they merge field data, agronomic models, and regulatory reporting into one environment. Meanwhile, artificial intelligence augments software value by raising yield predictions and improving return-on-investment visibility, especially for specialty-crop growers.

Key Report Takeaways

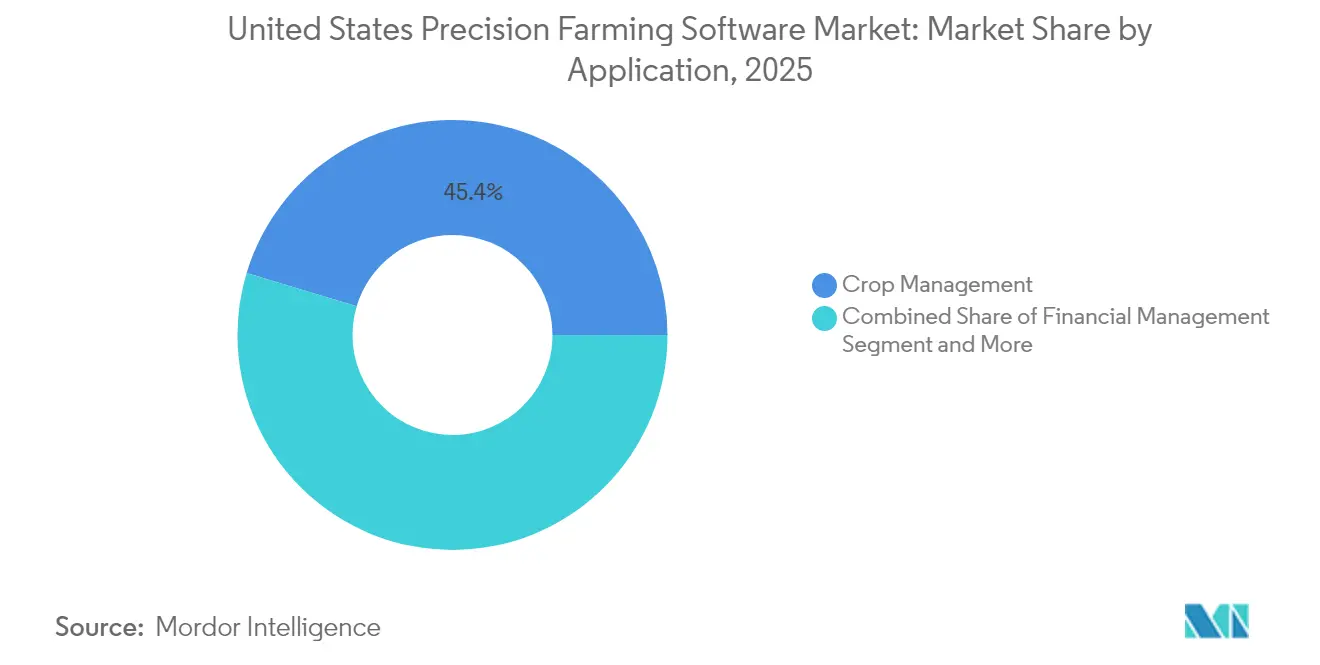

- By application, crop management captured 45.35% of the United States precision farming software market share in 2025, while weather tracking and forecasting is advancing at a 11.35% CAGR through 2031.

- By deployment type, cloud platforms commanded a 60.25% share of the United States precision farming software market size and are growing at an 11.02% CAGR.

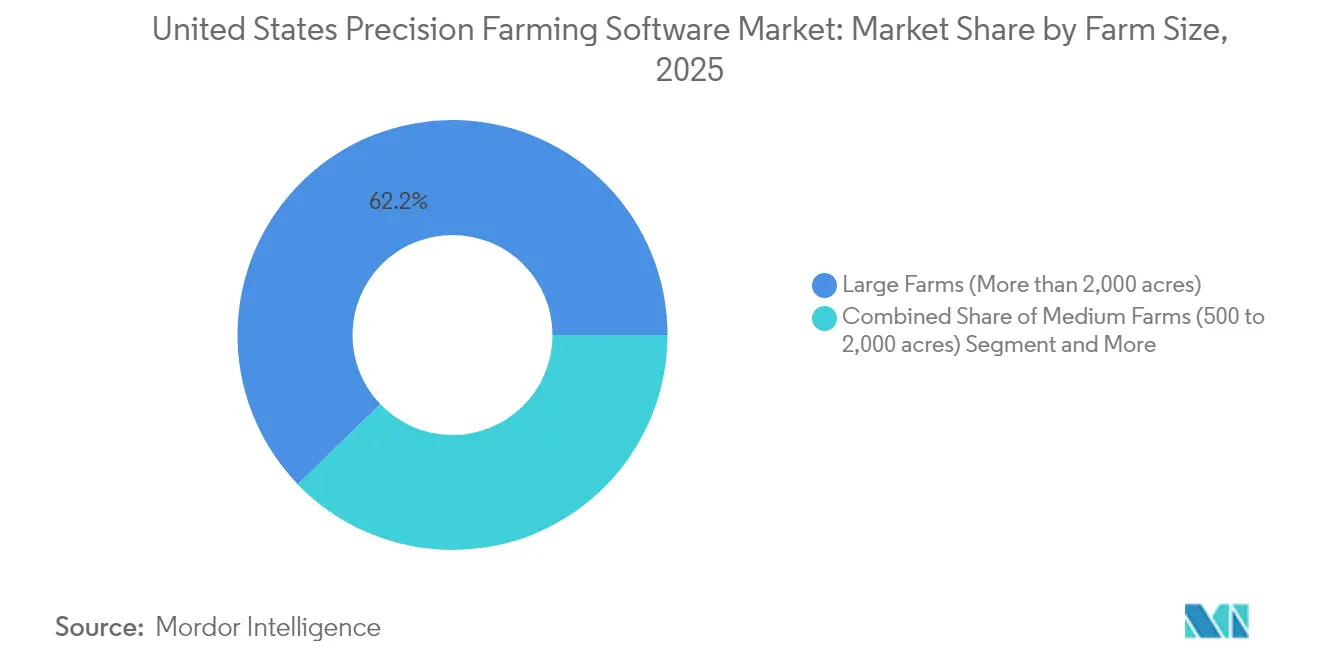

- By farm size, operations larger than 2,000 acres held 62.20% of the United States precision farming software market size in 2025, while the 500–2,000 acre cohort is climbing at a 11.56% CAGR.

- By end-user, row-crop producers controlled 68.10% share of the United States precision farming software market size in 2025, whereas specialty-crop growers represent the fastest rise at 12.78%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Precision Farming Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Farm-labor scarcity and rising average farm size | +2.8% | Global, with the highest impact in North America and Europe | Medium term (2-4 years) |

| Federal cost-share programs for digital tools | +2.1% | North America, with spillover to the European Union through similar programs | Short term (≤ 2 years) |

| Expanding cloud connectivity in rural broadband | +1.9% | Global, with early gains in the Midwest, West, and South regions | Medium term (2-4 years) |

| AI-driven agronomy improving ROI visibility | +1.6% | Global, with advanced adoption in large-scale operations | Long term (≥ 4 years) |

| Carbon-credit revenue models for data-rich farms | +0.8% | North America and the European Union, with emerging opportunities in Asia-Pacific | Long term (≥ 4 years) |

| OEM–software vendor JV activity | +0.6% | Global, concentrated in major agricultural equipment markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Farm-Labor Scarcity and Rising Average Farm Size

Consolidation into larger holdings amplifies these pressures because covering wider acreages intensifies demand for software that synchronizes field operations, labor scheduling, and inventory flows. Medium-scale farms are the most responsive, posting 12.2% CAGR adoption as they strive to match the efficiency of larger peers. Consequently, the United States precision farming software market increasingly targets features that reduce idle equipment time, streamline input allocation, and substitute scarce human labor. These dynamics position workflow automation and fleet coordination modules as core upgrade priorities over the next two planning cycles.

Federal Cost-Share Programs for Digital Tools

Application volume surged to 156,485 in fiscal 2024, signaling unmet demand that is likely to expand program breadth. These incentives stimulate early upgrades to cloud-based packages that capture granular field data needed for compliance reporting. Although funding does not fully cover backlog demand, its continuity reassures lenders and stimulates longer-term financing for integrated platforms. Consequently, the United States precision farming software market experiences a virtuous cycle wherein cost-share capital catalyzes private investment in sensors, connectivity, and subscription services.

Expanding Cloud Connectivity in Rural Broadband

The USDA ReConnect Program has awarded USD 5.55 billion to deliver a minimum of 100 Mbps symmetrical speeds to underserved communities, directly enabling software that depends on continuous telemetry[1]Source: U.S. Department of Agriculture, “ReConnect Loan and Grant Program Awards,” usda.gov. Connectivity upgrades explain why cloud deployments own a 61% share and sustain an 11.5% CAGR, as farmers increasingly prefer platforms accessible on any device. Weather-tracking modules derive a special advantage because low-latency data exchange ensures that frost, drought, or hail advisories instantly trigger software-generated task lists.

AI-Driven Agronomy Improving ROI Visibility

McKinsey projects that artificial intelligence could unlock USD 100 billion in on-farm gains and another USD 150 billion at the enterprise level by minimizing input waste and elevating output quality. Bayer’s E.L.Y. model lifts query-handling accuracy by 40% and saves staff four hours weekly, demonstrating tangible time and cost savings. Specialty-crop operators, whose per-acre margins justify premium analytics, achieve faster paybacks on investment, propelling that segment’s 13.4% CAGR. These successes strengthen the business case for predictive modules, encouraging broader uptake across the United States precision farming software market even among row-crop producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and unclear short-term payback | -1.8% | Global, with the highest impact on small and medium farms | Short term (≤ 2 years) |

| Data ownership and privacy concerns | -1.2% | Global, with heightened concerns in North America and the European Union | Medium term (2-4 years) |

| Integration complexity across heterogeneous machinery | -0.9% | Global, particularly affecting mixed-equipment operations | Medium term (2-4 years) |

| Digital skills gap among aging farm operators | -0.7% | Global, with regional variations in demographic profiles | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Unclear Short-Term Payback

Iowa surveys show 74% of growers label precision technologies expensive, even while acknowledging efficiency benefits, indicating hesitancy to invest absent guaranteed returns. Fragmented hardware ecosystems often force multiple, uncoordinated purchases that lengthen payback periods. Although large farms (>2,000 acres) shoulder these costs more easily and now hold 63% market share, smaller holdings still delay upgrades unless subsidies defray capital expense.

Data Ownership and Privacy Concerns

World Bank studies find growers reluctant to transmit detailed operational records to third parties without contractual safeguards, fearing competitive leakage or unfair monetization. Emerging interoperability standards from the Agricultural Industry Electronics Foundation grant users more control, but mainstream implementation is nascent. Until frameworks mature, privacy concerns will continue constraining some investment in the United States precision farming software market, especially among operators with high-value proprietary genetics or niche production methods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Crop Management Dominance Drives Platform Integration

Crop management solutions controlled 45.35% of the United States precision farming software market share in 2025, underscoring their status as the operating hub for seeding, fertilization, and harvest decisions. The United States precision farming software market size attributed to crop management is projected to expand alongside advanced imaging, sensor fusion, and rate-variable application features. Adding financial and compliance modules converts point solutions into holistic suites that appeal to diversified operations.

Weather-tracking applications, rising at a 11.35% CAGR, exploit high-resolution radar and machine-learning models that predict micro-climate shifts affecting planting windows. Their success illustrates the shift to microservices architecture, where specialized functions bolt onto an overarching platform via open APIs.

By Deployment Type: Cloud Infrastructure Transforms Rural Operations

Cloud offerings accounted for 60.25% of the United States precision farming software market in 2025 because of remote access, automatic updates, and lower upfront hardware outlays. The United States precision farming software market size for cloud deployments is primed for an 11.02% CAGR as rural fiber installations alleviate coverage gaps. Early adopters cite seamless multi-device collaboration, enabling agronomists, equipment operators, and accountants to share one data source as the principal advantage.

Offline-sync capabilities still matter in fringe signal zones, so hybrid configurations combining cloud cores with edge gateways remain popular. Providers differentiate by embedding cybersecurity protocols and contract clauses that guarantee data portability on termination, easing vendor-lock fears. As machine telemetry volumes escalate, pay-per-use storage and compute models will further shift costs from capital to operating expenditure, sustaining cloud momentum within the United States precision farming software market.

By Farm Size: Medium Operations Drive Technology Adoption Growth

Operations larger than 2,000 acres retained 62.20% of the United States precision farming software market in 2025, reflecting their capacity to amortize system costs over extensive acreage. Yet the 500–2,000 acre bracket now posts a 11.56% CAGR, signaling accelerated democratization of digital tools. Autosteering and variable-rate technologies penetrated 52% of midsize operations in 2023, compared with single-digit levels two decades earlier.

Government cost-share grants offset as much as 75% of subscription and hardware expenses, narrowing adoption gaps between midsize and large farms. Equipment vendors like John Deere earmarked USD 20 billion in U.S. investments to develop autonomous solutions tailored for this segment, providing a retrofit pathway that sidesteps large machinery purchases.

By End-User: Specialty Crops Lead Innovation Adoption

Row-crop growers commanded 68.10% of the United States precision farming software market size in 2025 because of vast corn, soybean, and wheat acreages USDA. The specialty-crop enterprises from orchards to vineyards register a blistering 12.78% CAGR as per-acre value grants faster paybacks on precision tools. AI-enabled vision systems from Orchard Robotics can estimate fruit counts and detect disease at the tree level, cutting manual scouting costs while improving quality grades.

Equipment innovation echoes this trend. John Deere’s autonomous 5ML tractor targets orchard spray operations, integrating seamlessly with cloud dashboards that document chemical usage for export compliance. As these high-margin segments refine analytics and autonomous workflows, lessons learned will diffuse to row-crop operations, thereby elevating feature expectations across the United States precision farming software market.

Geography Analysis

The Midwest retained a significant share of the United States precision farming software market revenue in 2025, anchored by large corn and soybean enterprises that historically adopt guidance and rate-control tools first. Ample dealer networks and manufacturer partnerships accelerate product support, while EQIP grants funnel significant climate-smart funds into conservation-oriented digital upgrades. Although the regional CAGR moderates compared with emerging areas, ongoing consolidation and generational turnover sustain steady license renewals and platform expansions.

The West is experiencing remarkable growth in the precision farming software market, driven by the unique demands of high-value specialty crops. These crops require meticulous management of resources such as water, nutrients, and labor, prompting farmers to adopt advanced monitoring and control technologies. The region's ongoing challenges with water scarcity have further accelerated the adoption of solutions that track evapotranspiration and automate irrigation processes. Additionally, infrastructure projects under USDA ReConnect are addressing long-standing connectivity issues in states like North Dakota, South Dakota, and Alaska by expanding fiber networks. This improved broadband access is enabling real-time decision-making capabilities, which were previously limited due to connectivity gaps. As more counties gain access to reliable internet, software providers are prioritizing the West for pilot programs featuring AI-driven irrigation advisory tools. This approach strengthens the connection between technological advancements and the evolving needs of farmers, fostering greater adoption of precision farming solutions.

Southern and Northeastern states show more measured expansion but benefit from crop diversity and proximity to ag-tech research clusters. Cotton and rice growers in the South increasingly adopt variable-rate nitrogen modules to comply with water-quality standards, while Northeast dairy producers combine herd-management data with agronomic records to benchmark environmental footprints.

Competitive Landscape

Competitive intensity is moderately concentrated because no single vendor controls even one-fifth of total revenue, creating room for both conglomerates and start-ups to expand. John Deere leverages strong hardware entrenchment by embedding the Operations Center into every new machine and augmenting it with Sentera’s aerial imaging after the 2025 acquisition. The firm’s USD 20 billion domestic investment pledge underscores a long-range commitment to integrated autonomy and cloud ecosystems.

AGCO formed a USD 2 billion joint venture with Trimble Ag that marries retrofit autonomy kits with mixed-fleet compatibility, positioning the alliance to capture customers who operate equipment from multiple brands. Bayer’s E.L.Y. model showcases how input suppliers extend beyond agronomy services into full-stack decision engines, backed by partnerships such as Azure Data Manager for Agriculture that streamline data interoperability with Microsoft[3]Source: Bayer, “E.L.Y. Generative AI Model Announcement,” bayer.com. New entrants focus on micro-niches, like SWAT VEXA for watershed modeling, before expanding horizontally across modules, using lower customer acquisition costs driven by SaaS delivery.

Data privacy remains a differentiation lever; several providers now offer farmer-controlled encryption keys and explicit data-use clauses to gain the trust of hesitant prospects. Training programs and simplified mobile interfaces tackle the skills gap, an area where only 25% of producers report full digital confidence. As acquisitions concentrate technology under fewer corporate umbrellas, the United States precision farming software market still rewards nimble innovators that solve narrow pain points and then scale through API-first integration.

United States Precision Farming Software Industry Leaders

Corteva Agriscience

Deere & Company

Kubota Corporation

Bayer AG

AGCO Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: John Deere confirmed a USD 20 billion U.S. investment plan to accelerate farm automation and connectivity upgrades.

- May 2025: John Deere acquired Sentera, incorporating SmartScripts weed mapping into the Operations Center to enhance precision spraying.

- February 2025: Texas A&M AgriLife and IBM introduced SWAT VEXA, a generative AI application for water-related agronomic decisions.

- November 2024: Bayer launched the E.L.Y. generative AI model that raises agronomic query accuracy by 40% and frees four staff hours per week.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States precision farming software market as all cloud-based or on-premise digital platforms that ingest machine, sensor, satellite, and financial data to guide in-field decisions, automate record keeping, and optimize crop and resource use.

Scope exclusion: hardware items such as GNSS receivers, drones, and variable-rate controllers are kept outside the revenue pool, so the model tracks only pure-play and bundled software license or subscription fees.

Segmentation Overview

- By Application

- Crop Management

- Financial Management

- Farm Inventory Management

- Personnel Management

- Weather Tracking and Forecasting

- Other Applications

- By Deployment Type

- Local/Web-based

- Cloud-based

- By Farm Size

- Small (Less than 500 acres)

- Medium (500 to 2,000 acres)

- Large (More than 2,000 acres)

- By End-User

- Row-crop Growers

- Specialty-crop Growers

- Livestock and Mixed Operations

Detailed Research Methodology and Data Validation

Primary Research

Interviews with agronomists, mid-western row-crop growers, software integrators, and state extension officers helped us verify typical license fees, average connected-acre ratios, and realistic switching timelines across farm cohorts. Follow-up questionnaires with platform product managers clarified subscriber churn and module-level price bands, which sharpened the sensitivity ranges in the model.

Desk Research

We began with public statistics from the USDA National Agricultural Statistics Service, the ERS farm income tables, and the Census of Agriculture, which anchor planted acreage, input spend, and structural shifts in farm size. Complementary insights came from the American Farm Bureau Federation briefs, academic papers in Agronomy Journal, and patent trends retrieved through Questel that signal emerging decision-support algorithms. Market expansion drivers such as broadband coverage were validated through FCC deployment maps, while tariff and subsidy impacts were traced from White House fact sheets and Congressional Budget Office releases. Subscription databases including D&B Hoovers and Dow Jones Factiva supplied revenue splits and product notes for leading vendors. The sources listed illustrate the range consulted and are not exhaustive.

A second sweep gathered import-export codes via Volza to size U.S. inflows of dedicated farm data terminals and weather service usage metrics from NOAA annual reports to flag downstream user adoption.

Market-Sizing & Forecasting

A top-down construct begins with total planted acres by crop and state, converts these into an addressable digital field-acre pool through precision-tool penetration rates, and multiplies by weighted average software spend per acre. Sampled vendor roll-ups and channel checks act as a selective bottom-up counterpoint, allowing us to adjust outliers before sign-off. Key variables monitored include corn-soy acreage rotation, broadband penetration, average subscription price trends, ag-labor wage inflation, and USDA climate-smart grant outlays. Forecasts run on an ARIMA-enhanced multivariate regression, and we've cross-checked coefficient direction with practitioner consensus before locking the scenario band. Gaps in supplier data, especially for bundled ERP-plus-ag-module suites, are bridged using farm-size specific adoption factors obtained from primary research.

Data Validation & Update Cycle

Outputs face three rings of scrutiny: automated variance flags against historical ratios, peer review within Mordor's analyst pod, and an annual refresh that restarts if a mid-year event, such as a subsidy rule change, shifts the acreage or pricing curve. Clients therefore receive numbers that have cleared statistical, domain, and temporal checks.

Why Mordor's United States Precision Farming Software Baseline Commands Reliability

Published estimates often diverge because firms mix hardware with software, use different planted-acre denominators, or freeze exchange rates months before publication.

Key gap drivers in our space are scope creep into guidance hardware, unvetted price escalation assumptions, and slower refresh cadences that miss USDA grant surges.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.89 B (2025) | Mordor Intelligence | - |

| USD 2.82 B (2024) | Regional Consultancy A | Combines hardware, services, and software under one heading, inflating the base. |

| USD 0.69 B (2024) | Trade Journal B | Tracks only farm management ERP offerings, excluding stand-alone decision-support apps. |

The comparison shows that when scope is either broadened or narrowed, totals swing widely. By keeping a software-only lens, refreshing annually, and triangulating penetrations with both acreage and license counts, Mordor delivers a balanced, transparent baseline stakeholders can trust.

Key Questions Answered in the Report

What is the current size of the United States precision farming software market?

The United States precision farming software market is valued at USD 3.16 billion in 2026 and is projected to reach USD 4.92 billion by 2031.

Which segment holds the largest United States precision farming software market share?

Crop management applications lead with 45.35% share in 2025, reflecting their role in guiding planting, fertilization, and harvest activities.

Why are cloud platforms growing so quickly in the United States precision farming software?

Improved rural broadband under the USDA ReConnect Program enables real-time data transfer, driving an 11.02% CAGR for cloud solutions.

How are medium-sized farms influencing market growth?

Farms between 500-2,000 acres show a 11.56% CAGR as cost-share programs and mid-tier subscription models lower adoption barriers.

What role does artificial intelligence play in the United States precision farming software?

AI enhances yield prediction, input optimization, and compliance reporting, with studies estimating USD 100 billion in potential on-farm value creation.

Which United States region is expanding fastest in adopting precision farming software?

The West region records an 11.12% CAGR, driven by specialty-crop operations and new broadband infrastructure that supports cloud-based analytics.

Page last updated on: