Popping Boba Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

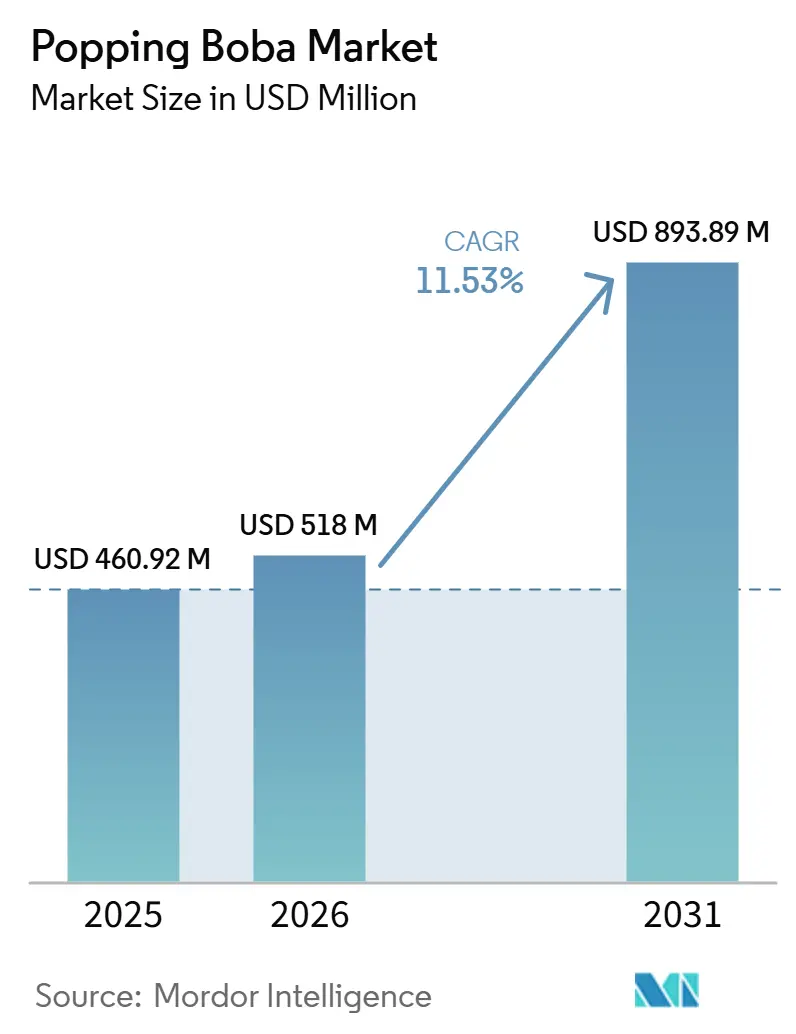

| Market Size (2026) | USD 518 Million |

| Market Size (2031) | USD 893.89 Million |

| Growth Rate (2026 - 2031) | 11.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Popping Boba Market Analysis by Mordor Intelligence

The popping boba market size was USD 460.92 million in 2025 and is expected to reach USD 518.00 million in 2026 and USD 893.89 million by 2031, registering a CAGR of 11.53% between 2026 and 2031. This rapid expansion is propelled by rising social-media visibility, a sharp uptick in beverage customization, and continued roll-outs of bubble tea chains across North America, Europe, and Latin America. Intensifying demand for organic capsules, broader culinary applications in desserts and cocktails, and sustainable packaging breakthroughs are widening commercial opportunities for both large-scale producers and agile niche brands. At the same time, persistent input-cost volatility for sodium alginate and calcium chloride, coupled with tougher U.S. organic-certification rules, keeps supply-side risk at the forefront of boardroom agendas. The popping boba market now sits at the intersection of food science, experiential dining, and retail channel diversification, positioning it for double-digit annual gains over the next five years.

Key Report Takeaways

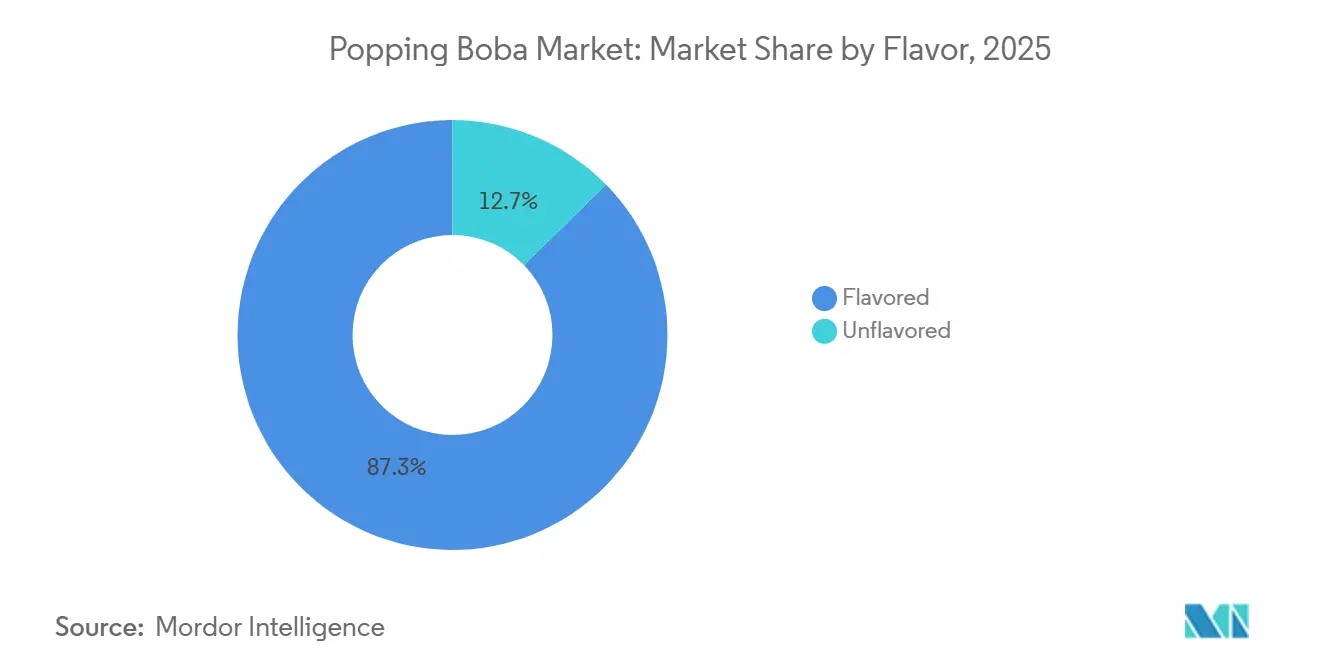

- By flavor, the flavored segment led with 87.14% revenue share in 2025, while it is also projected to post the fastest 11.08% CAGR through 2031.

- By category, conventional products accounted for 82.03% of 2025 sales; the organic segment is forecast to expand at a 12.11% CAGR to 2031.

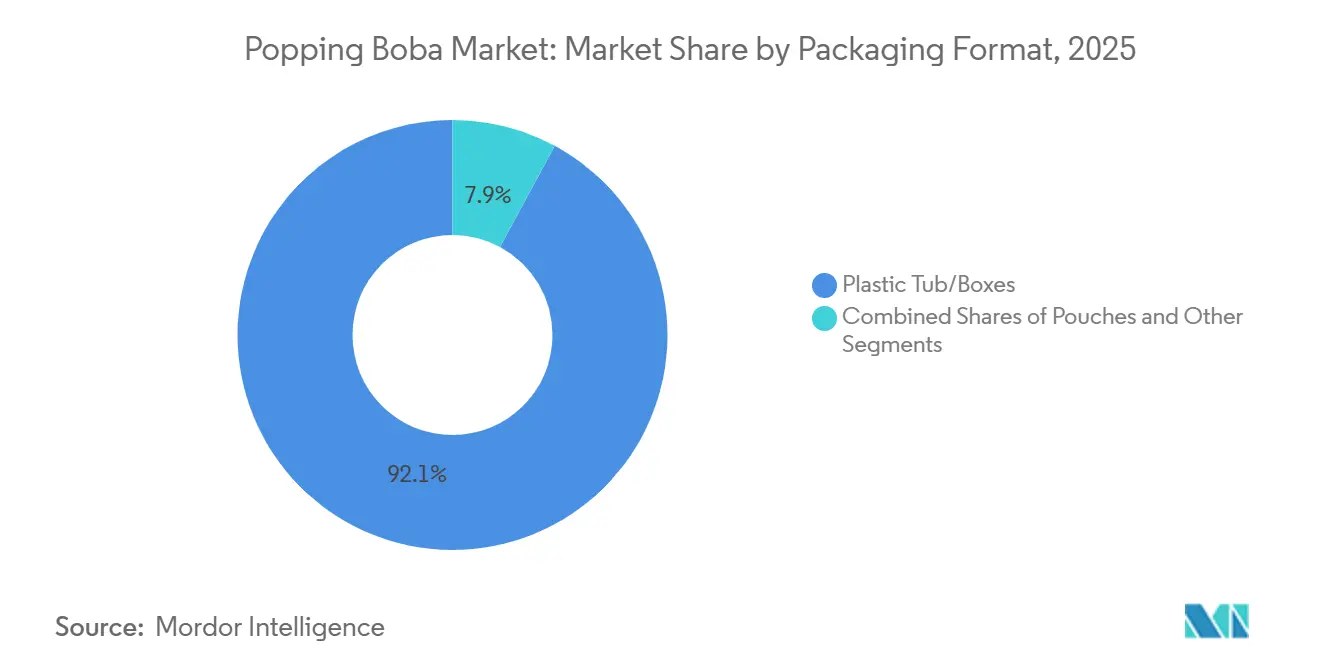

- By packaging format, plastic tubs and boxes held 91.67% of 2025 revenue, whereas cans are advancing at a 12.04% CAGR between 2026 and 2031.

- By distribution channel, on-trade venues generated 58.08% of 2025 revenue, while off-trade retail is poised for a 12.53% CAGR to 2031.

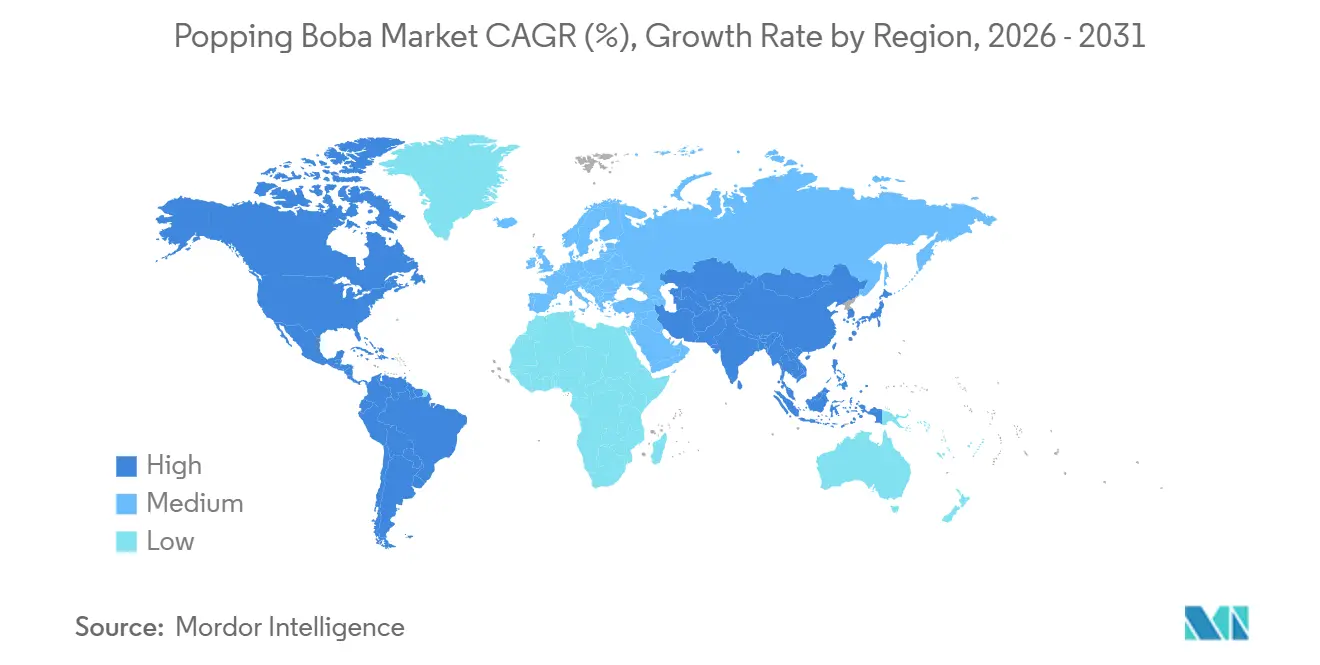

- By geography, Asia-Pacific commanded 41.57% of 2025 revenue, whereas Asia-Pacific is expected to register a 12.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Popping Boba Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global demand for specialty beverages | +2.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion into desserts and beverage formats | +2.1% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Continuous innovation in flavors and formulations | +1.9% | Global, led by North America health trends | Medium term (2-4 years) |

| Social media driving global consumer trends | +1.7% | Global, strongest in urban markets | Short term (≤ 2 years) |

| Growing preference for customizable drink options | +1.4% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Strong appeal among younger consumer segments | +1.2% | Global, particularly Gen Z demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising global demand for specialty beverages

The bubble tea market's expansion beyond traditional Asian strongholds is creating unprecedented demand for popping boba as a premium topping alternative to conventional tapioca pearls. Mixue Bingcheng's recent Hong Kong IPO, raising USD 444 million with shares jumping 40% on the first trading day, demonstrates investor confidence in the sector's global scalability. The chain's 45,000+ outlets worldwide now exceed McDonald's footprint, signaling bubble tea's transition from niche beverage to mainstream food service category. North American market growth in the milk tea category reflects this geographic expansion, with cities like New York and Los Angeles becoming testing grounds for Asian beverage concepts targeting diverse demographics. The proliferation of specialty beverage chains is driving standardization in popping boba specifications, creating economies of scale that benefit both manufacturers and end consumers through improved quality consistency and pricing stability.

Expansion into desserts and beverage formats

Culinary applications beyond traditional beverages represent the most transformative growth vector for popping boba manufacturers, with Kültee Kaviar pioneering smaller-format products specifically designed for dessert and savory dish integration. The company's emphasis on domestic U.S. production addresses both tariff concerns and clean-label demands, leveraging parent company Zentis North America's 130-year food manufacturing expertise. This product diversification strategy aligns with the broader food industry's move toward experiential dining, where visual and textural elements command premium pricing. Ice cream parlors and yogurt shops are increasingly incorporating popping boba as signature toppings, while high-end restaurants experiment with savory applications in molecular gastronomy presentations. The cocktail segment presents promise, as bartenders seek non-alcoholic garnishes that provide both visual appeal and flavor bursts, tapping into the growing mocktail trend among health-conscious consumers.

Continuous innovation in flavors and formulations

Health-conscious formulations are reshaping product development priorities, with organic variants projected to capture increasing market share despite premium pricing. FS Drinks' Simple Boba launch at Expo West 2024 exemplifies this trend, featuring clean-label RTD beverages with konjac-based crystal boba offering a 160-day shelf life without artificial preservatives. Australian oat farmers are developing beta-glucan-enhanced popping boba that reduces sugar content while maintaining flavor profiles, targeting the global bubble tea market with healthier alternatives. Low-sugar and vegan formulations address regulatory pressures and consumer preferences simultaneously, with manufacturers leveraging natural fruit extracts and plant-based gelling agents. The rise of functional beverages creates opportunities for popping boba infused with vitamins, adaptogens, and probiotics. Texture innovations focus on achieving optimal "pop" sensation while extending shelf life, addressing the fundamental challenge of maintaining liquid-filled capsule integrity during distribution and storage.

Social media driving global consumer trends

Visual-first social media platforms are accelerating the adoption rates, particularly among Gen Z consumers who prioritize Instagram-worthy food experiences. The "bursting" texture and vibrant colors create inherently shareable content moments, driving organic marketing reach that traditional advertising cannot replicate. CHAGEE's U.S. expansion strategy explicitly leverages K-pop cultural connections and social media engagement, targeting cities with large Asian populations while building broader cultural appeal. Food influencer partnerships have proven especially effective in introducing popping boba to non-Asian demographics, with viral TikTok videos demonstrating DIY bubble tea recipes driving retail sales of packaged products. The visual appeal factor extends beyond individual consumption to restaurant presentation, where popping boba serves as an affordable way to elevate dessert and beverage aesthetics. This social media amplification effect creates rapid market penetration in new geographic regions, often preceding formal brand expansion by establishing consumer familiarity and demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited shelf life and storage issues affecting freshness | -1.8% | Global, particularly in hot climates | Short term (≤ 2 years) |

| Health concerns related to high sugar content, artificial flavors, and additives | -1.5% | North America and Europe regulatory focus | Medium term (2-4 years) |

| Rising competition from alternative toppings such as jellies, chia balls, and smoothie balls | -1.2% | Global, varying by regional preferences | Long term (≥ 4 years) |

| Variability in raw material availability and price fluctuations | -1.1% | Global, supply chain dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited shelf life and storage issues affecting freshness

Cold-chain logistics requirements and limited shelf stability continue to constrain market expansion, particularly in regions lacking adequate refrigeration infrastructure. The liquid-filled nature of popping boba creates inherent preservation challenges, as the alginate membrane must maintain integrity while preventing bacterial growth in the internal fruit juice or flavoring. Traditional formulations typically require refrigeration and consume within 30-45 days of production, limiting distribution reach and increasing operational costs for retailers. Supply chain disruptions highlighted by KPMG's 2024 analysis, including transportation delays and climate-related logistics challenges, disproportionately impact perishable specialty products like popping boba. Manufacturers are investing in modified atmosphere packaging and natural preservative systems, though these solutions often increase production costs and may affect taste profiles.

Health concerns related to high sugar content, artificial flavors, and additives

Regulatory scrutiny of food additives and sugar content is intensifying across major markets, with particular focus on products targeting younger demographics. The FDA's updated guidance on sodium alginate usage, while generally recognizing it as safe, requires specific labeling and manufacturing compliance that increases operational complexity [1]Source: Code of Federal Regulations, "sodium alginate usage" ecfr.gov. High sugar content in traditional popping boba formulations conflicts with public health initiatives aimed at reducing childhood obesity and diabetes rates, creating pressure for reformulation that may compromise taste and texture characteristics. Artificial coloring restrictions in European markets require manufacturers to develop natural alternatives that maintain visual appeal while meeting regulatory requirements. The challenge intensifies as health-conscious parents increasingly scrutinize ingredient lists, potentially limiting popping boba's appeal in family-oriented food service establishments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Flavored Dominance Drives Innovation

Flavored popping boba maintains commanding market leadership with 87.14% share in 2025, while simultaneously driving the fastest growth at 11.08% CAGR through 2031. This dual dominance reflects both established consumer preferences and ongoing innovation in flavor profiles that extend beyond traditional fruit varieties. Manufacturers are leveraging molecular gastronomy techniques to create complex flavor combinations, including savory options like cucumber-mint and exotic fruit blends that appeal to adventurous consumers seeking novel taste experiences. The unflavored segment, despite its smaller market presence, serves critical applications in premium establishments where chefs prefer to control flavor profiles through external sauces or syrups.

Recent innovations focus on seasonal and limited-edition flavors that create urgency and social media buzz, with companies like CHAGEE incorporating regional taste preferences into their global expansion strategies. The flavored segment's growth trajectory benefits from the broader trend toward experiential dining, where unique taste combinations justify premium pricing. Natural flavor extracts are increasingly replacing artificial alternatives, driven by clean-label demands and regulatory pressures in key markets. This shift toward natural ingredients, while increasing production costs, aligns with the organic segment's growth momentum and creates opportunities for vertical integration with fruit processing operations.

By Category: Organic Segment Captures Health Premium

The organic category emerges as the fastest-growing segment with 12.11% CAGR through 2031, despite conventional products maintaining 82.03% market share in 2025. This growth differential reflects intensifying consumer focus on health and wellness, particularly among millennial and Gen Z demographics who prioritize ingredient transparency and environmental sustainability. The USDA's Strengthening Organic Enforcement rule, effective March 2024, requires enhanced certification and traceability throughout the supply chain, creating barriers to entry that may consolidate the organic segment around established players with robust compliance capabilities [2]Source: U.S. Department of Agriculture, "Strengthening Organic Enforcement rule", ams.usda.gov.

Organic popping boba production faces unique challenges in sourcing certified organic fruit juices and natural gelling agents, often requiring premium pricing that limits mass market penetration. However, the segment benefits from the broader organic beverage market's 12.11% CAGR growth trajectory, with distribution expanding beyond specialty retailers to mainstream grocery chains. Conventional products continue to dominate due to cost advantages and established supply chains, though manufacturers are increasingly offering organic options as premium line extensions. The category split reflects broader food industry trends where organic products capture disproportionate value despite smaller volumes, creating sustainable profit margins for companies willing to invest in certification and specialized sourcing.

By Packaging Format: Plastic Dominance Faces Sustainability Pressure

Plastic tub/boxes command 91.67% market share in 2025, reflecting established supply chain efficiencies and cost advantages in bulk distribution to food service operators. However, cans represent the fastest-growing format at 12.04% CAGR through 2031, driven by sustainability concerns and consumer convenience preferences. This growth trajectory aligns with broader packaging industry innovations, including Amcor's recyclable retort pouch technology that reduces carbon footprints by up to 60% compared to traditional packaging. The shift toward flexible packaging formats addresses both environmental concerns and operational efficiency, as pouches require less storage space and reduce transportation costs.

Accredo Packaging's 100% bio-based resin pouches from sugarcane demonstrate the industry's movement toward sustainable alternatives, though adoption remains limited by higher production costs and performance considerations. Other packaging formats, including sachets and sticks, serve niche applications in retail and single-serve markets, though their growth potential remains constrained by portion size limitations and higher per-unit packaging costs. The packaging format evolution reflects broader consumer preferences for convenience and sustainability, creating opportunities for companies that can balance environmental credentials with functional performance and cost competitiveness.

By Distribution Channel: Retail Transformation Accelerates

The distribution landscape reveals a strategic inflection point, with off-trade retail channels projected to grow at 12.53% CAGR through 2031, significantly outpacing the on-trade foodservice segment that maintains 58.08% market share in 2025. This growth differential reflects changing consumer behavior patterns, including increased home consumption and the rise of DIY bubble tea preparation. Retail expansion benefits from improved packaging technologies that extend shelf life and maintain product quality outside traditional food service cold chains.

Within the on-trade segment, cafés and coffee chains lead adoption as operators seek differentiation through premium toppings and customization options. QSR and fast-casual restaurants represent emerging opportunities, though adoption rates vary by regional taste preferences and operational complexity considerations. The off-trade segment's growth momentum stems from expanding distribution through supermarkets, hypermarkets, and online retail platforms, with convenience stores emerging as key growth drivers due to their accessibility and impulse purchase dynamics. Online retail channels benefit from direct-to-consumer trends and subscription-based models that ensure regular product replenishment. This distribution evolution creates opportunities for manufacturers to develop retail-specific packaging and marketing strategies while maintaining food service relationships that drive brand awareness and trial.

Geography Analysis

Asia-Pacific maintains market leadership with 41.57% share in 2025, reflecting the region's role as both the origin market for bubble tea culture and the primary manufacturing hub for popping boba production. Nevertheless, Asia-Pacific emerges as the fastest-growing region at 12.05% CAGR through 2031, driven by expanding middle-class consumption, urbanization trends, and localized flavor innovations that incorporate regional fruit varieties. The geographic growth pattern reflects bubble tea's cultural diffusion beyond traditional Asian markets, with adaptation to local taste preferences creating new market opportunities.

North America represents a mature but evolving market, with established bubble tea chains expanding and popping boba offerings while new entrants target health-conscious consumers through organic and low-sugar variants. The region benefits from strong purchasing power and openness to food innovation, though market penetration remains concentrated in urban areas with diverse populations. Europe shows steady growth driven by increasing Asian cultural influence and the expansion of specialty beverage concepts, with particular strength in the United Kingdom market, where bubble tea has achieved mainstream acceptance.

The Middle East and Africa region presents long-term growth potential as economic development and urbanization create demand for premium beverage experiences, though current market penetration remains limited by distribution challenges and cultural preferences. Regional growth patterns reflect the global nature of food trend diffusion, with social media and cultural exchange accelerating adoption rates in previously untapped markets. Manufacturing capacity expansion in key regions, including Sirio Pharma's USD 40 million facility in Thailand, demonstrates industry confidence in sustained regional growth momentum.

Competitive Landscape

The popping boba market exhibits moderate fragmentation, reflecting relatively low barriers to entry in manufacturing combined with regional taste preferences that favor localized production capabilities. This competitive structure creates opportunities for both established food ingredient companies and specialized startups to capture market share through differentiation strategies. Technology adoption varies significantly across competitors, with larger players investing in automated spherification equipment and quality control systems while smaller manufacturers rely on traditional batch production methods that limit scalability but enable customization.

Strategic patterns reveal three distinct competitive approaches: cost leadership through scale economies, premium positioning via organic and health-focused formulations, and regional specialization targeting local flavor preferences. Companies like Kültee Kaviar leverage parent company expertise and domestic production advantages to avoid tariffs while positioning products for culinary applications beyond traditional beverages.

Opportunities exist in sustainable packaging solutions, extended shelf-life formulations, and functional ingredient integration that addresses health and wellness trends. Emerging disruptors focus on clean-label alternatives and innovative applications in desserts and cocktails, while established players defend market positions through supply chain efficiency and brand recognition. The FDA's sodium alginate safety assessment and regulatory clarity provide stability for long-term investment planning, though compliance requirements favor companies with established quality management systems [3]Source: Food Standards Agency, "Safety Assessment on Product E 401 (Sodium Alginate) Used as a Surface Treatment in Entire Fruits and Vegetables (RP290)", science.food.gov.uk.

Popping Boba Industry Leaders

-

Nordic Boba ApS

-

BOBAVIDA

-

Pecan Deluxe Candy Company

-

Fanale Drinks

-

Sunnysyrup Food Co, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Twrl Milk Tea, an award-winning food and beverage company inspired by its founders’ Taiwanese and Chinese American heritage, announced the launch of its bestselling low-to-no prep, single serve boba toppings, Brown Sugar Boba and Strawberry Popping Boba, at Andronico’s Community Markets.

- January 2025: Raymond and Harmon Rozycki, CEO and CMO of Unifying Spirits, announced the official launch of Boba POPS™, the only patented alcoholic popping boba in the world. In partnership with RNDC, one of the nation's leading distributors of alcoholic beverages, the brand launched in California, Florida, Texas, Arizona, Georgia, and Louisiana.

- January 2024: What's Hot launched all-new Sour Bursting Boba in 4 flavors: Lemon, Blue Raspberry, Cherry, and Orange. Using molecular gastronomy, the juices were captured in thin bubbles and transformed into juice balls that popped in the mouth, releasing refreshingly sour and delicious juices. Bossen’s Sour Bursting Boba delivered a bright splash of tangy goodness.

Global Popping Boba Market Report Scope

Popping boba is a type of small, juice-filled spherical pearl used in beverages and desserts, which bursts in the mouth when bitten to release flavored liquid. The Popping Boba Market Report is Segmented by Flavor (Flavored and Unflavored), Category (Organic, and Conventional), Packaging Format (Plastic Tub/Boxes, Cans, and Others), Distribution Channel (On-Trade/Foodservice, and Off-Trade/Retail), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Flavored |

| Unflavored |

| Organic |

| Conventional |

| Plastic Tub/Boxes |

| Cans |

| Others |

| On-Trade/Foodservice | |

| Off-Trade/Retail | Supermarkets/Hypermarkets |

| Convenience Stores/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Flavor | Flavored | |

| Unflavored | ||

| By Category | Organic | |

| Conventional | ||

| By Packaging Format | Plastic Tub/Boxes | |

| Cans | ||

| Others | ||

| By Distribution Channel | On-Trade/Foodservice | |

| Off-Trade/Retail | Supermarkets/Hypermarkets | |

| Convenience Stores/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the popping boba market in 2025?

The popping boba market size is USD 460.92 million in 2025 and is on track for USD 893.89 million by 2031.

Which flavor segment leads demand?

Flavored popping boba holds 87.14% of 2025 revenue thanks to continuous innovation in fruit and limited-edition variants.

Why is organic popping boba growing so fast?

USDA traceability rules now reward certified suppliers, helping the organic segment achieve a 12.11% CAGR through 2031.

Which packaging type is gaining momentum?

Cans are rising at a 12.04% CAGR as brands pursue lower carbon footprints and retail convenience.

Page last updated on: