Chocolate Syrup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

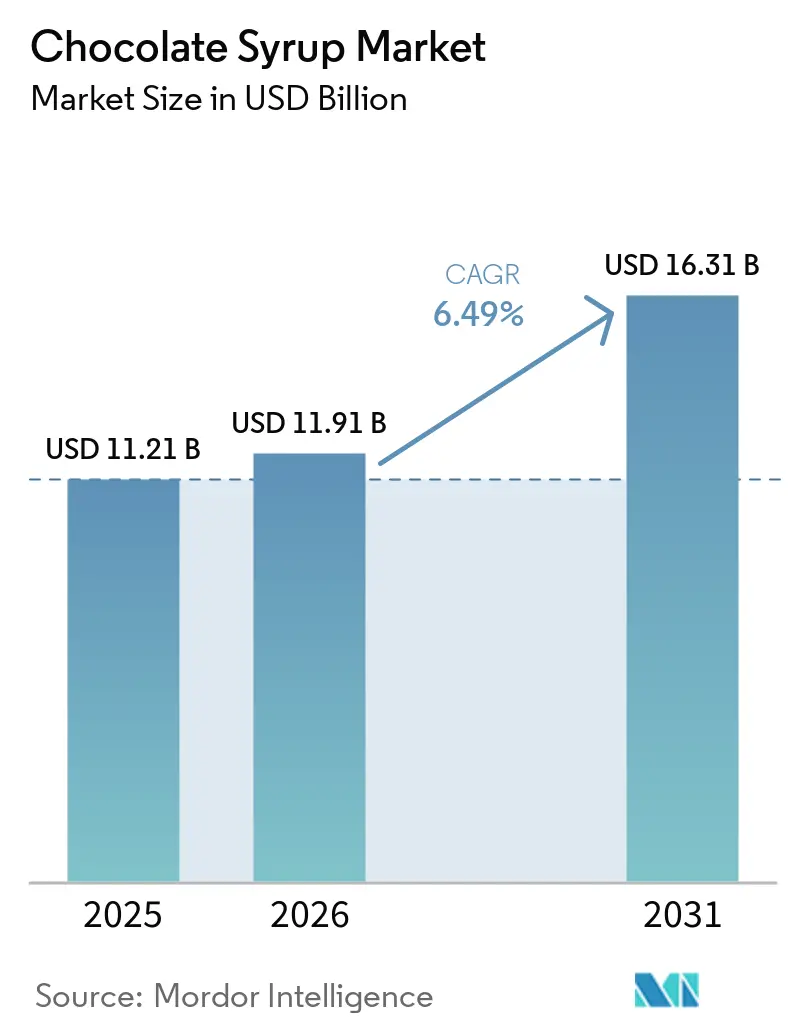

| Market Size (2026) | USD 11.91 Billion |

| Market Size (2031) | USD 16.31 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

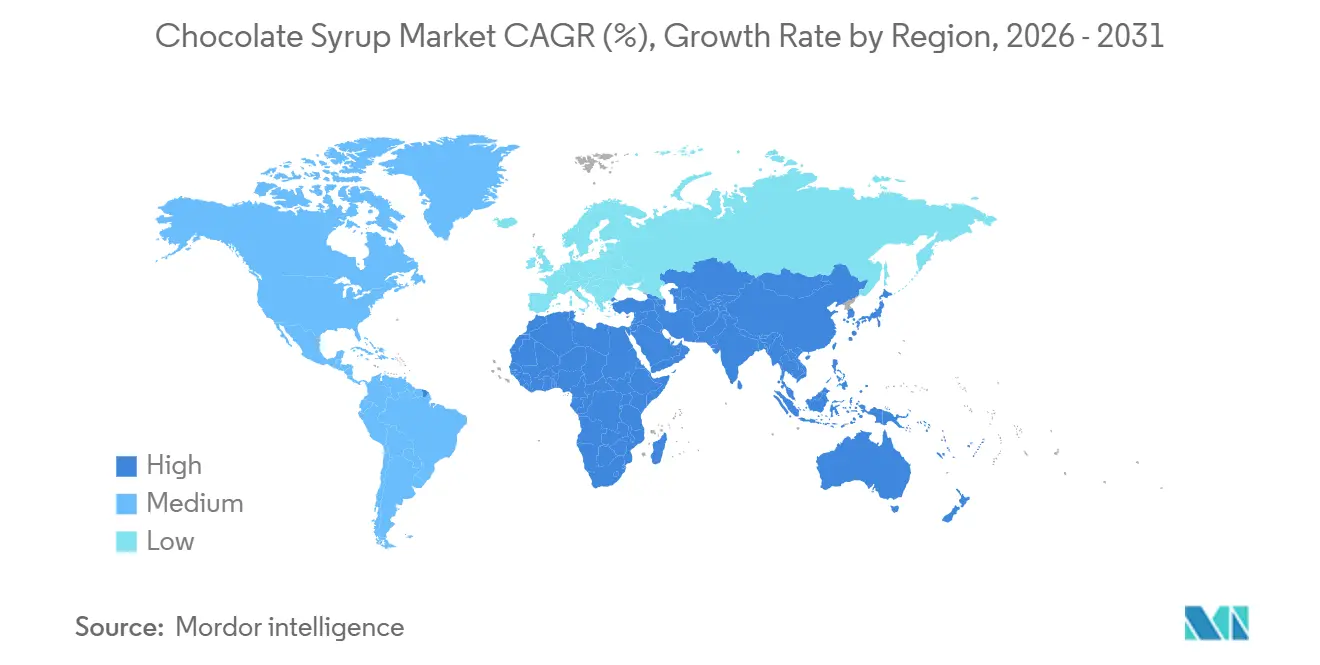

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chocolate Syrup Market Analysis by Mordor Intelligence

The chocolate syrup market size in 2026 is estimated at USD 11.91 billion, growing from the 2025 value of USD 11.21 billion, with 2031 projections showing USD 16.31 billion, growing at a 6.49% CAGR over 2026-2031. This growth trajectory reflects several structural shifts. Cocoa price volatility, which peaked at USD 12,000 per metric ton in March 2025, has driven manufacturers to optimize formulations while maintaining margin discipline. Additionally, the U.S. Food and Drug Administration's updated "Healthy" nutrient-content claim, requiring added sugars to remain below 2.5 grams per reference amount, is compelling reformulation strategies that prioritize premium, reduced-sugar variants over mass-market offerings [1]Source: U.S. Food and Drug Administration (FDA), "Use of the "Healthy" Claim on Food Labeling", fda.gov. Consumer associations of cocoa flavanols with cardiovascular benefits, along with the rise of single-origin, high-cacao-content syrups targeting specialty coffee chains, are further influencing market dynamics. Moreover, there is a growing willingness among consumers to pay a premium for sustainable packaging and clean-label formulations. The interplay between premiumization, health-driven reformulation, and channel diversification will play a critical role in determining which players capture a disproportionate market share over the forecast horizon.

Key Report Takeaways

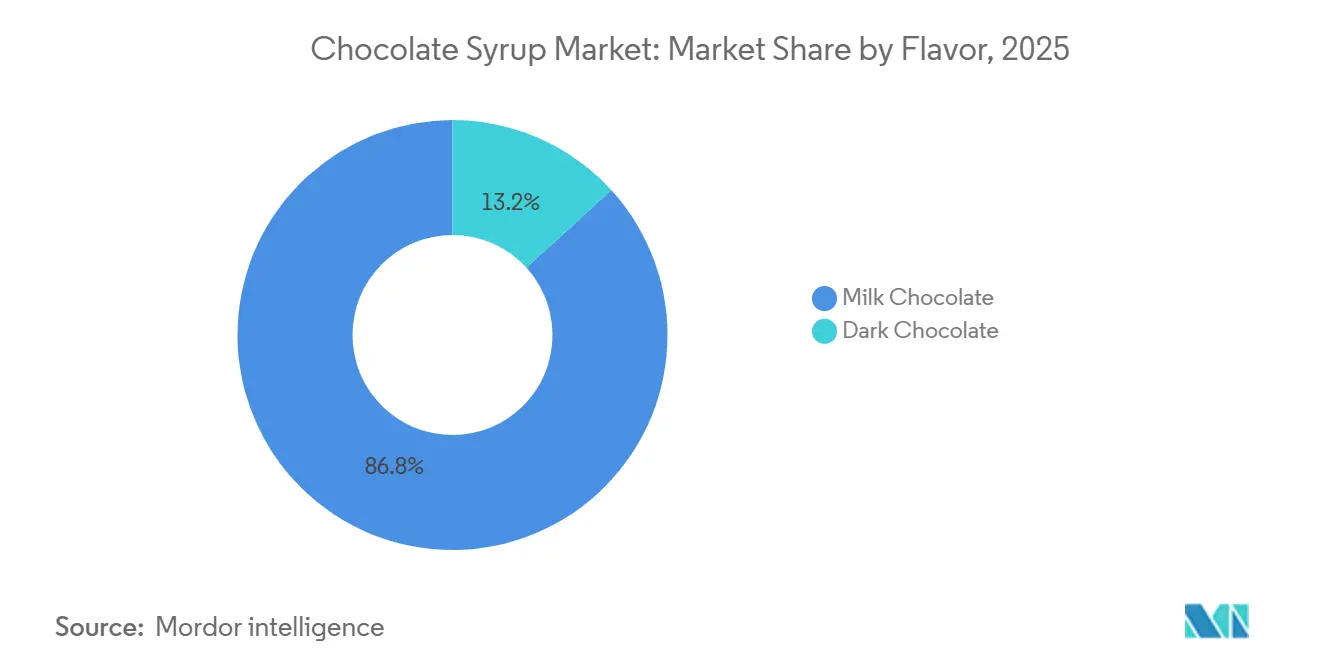

- By flavor, milk chocolate commanded 86.77% market share in 2025, whereas dark chocolate is projected to grow at a 7.24% CAGR during 2026-2031, the highest among flavors.

- By category, mass held 68.23% of the chocolate syrup market share in 2025, while the premium segment is poised to grow at an 8.05% CAGR through 2031.

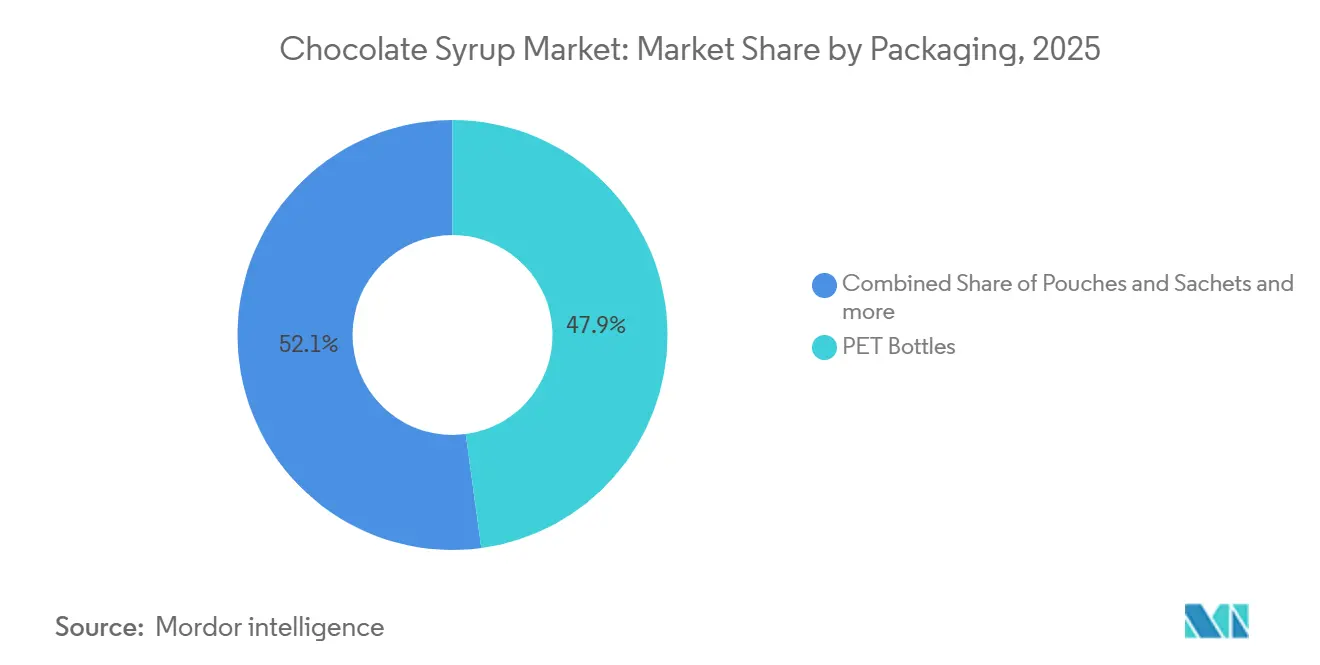

- By packaging type, PET bottles accounted for 47.87% of the market share in 2025; pouches and sachets are set to register a CAGR of 8.22% from 2026 to 2031.

- By end-user, retail channels led with 37.22% of 2025 revenue share, while foodservice/HoReCa is forecast to grow at a 6.89% CAGR through 2031, on the back of beverage chain rollouts.

- By region, North America remained the largest market with 33.04% share in 2025, whereas Asia-Pacific is projected to grow the fastest at a CAGR of 6.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chocolate Syrup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for convenient ready-to-use toppings | +1.2% | Global, with strongest uptake in North America and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Product innovation in flavors and formulations | +1.4% | North America and Europe, spill-over to premium segments in Asia-Pacific | Medium term (2-4 years) |

| Increasing popularity of chocolate-based beverages | +1.1% | Global, led by specialty coffee expansion in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Growing home baking and DIY dessert trends | +0.9% | North America and Europe, with emerging traction in Middle East urban markets | Short term (≤ 2 years) |

| Strong demand from bakery and confectionery sectors | +1.0% | Global, particularly in Asia-Pacific and Middle East where industrial bakery capacity is expanding | Long term (≥ 4 years) |

| Westernization of diets in emerging markets | +0.8% | Asia-Pacific core (China, India, Indonesia), spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for convenient ready-to-use toppings

The shift toward convenience-oriented consumption is reshaping distribution dynamics, favoring squeeze-bottle and single-serve formats. The growing expansion of online grocery channels is significantly benefiting ready-to-use chocolate syrups, as consumers increasingly bundle pantry staples with premium toppings, driving higher ship-to-home average order values. Additionally, foodservice operators have indicated that improved packaging quality could lead to increased orders, highlighting the demand for portion-controlled sachets and tamper-evident closures that minimize waste and enhance food safety. This trend aligns with the broader consumer preference for sustainable and functional packaging solutions. The convergence of omnichannel fulfillment and premiumization is transforming chocolate syrup from a basic commodity to a differentiated product. This shift is particularly evident in quick-service restaurants and coffee chains, where menu innovation increasingly relies on flavor layering to attract customers. Furthermore, the rising consumer interest in clean-label and organic formulations is driving manufacturers to innovate, offering syrups with reduced sugar content and natural ingredients.

Increasing popularity of chocolate-based beverages

Specialty coffee's growth is driving increased demand for premium chocolate syrups in higher-margin applications. Premium coffee platforms are creating pull-through demand for complementary syrups, with mocha beverages blending espresso and chocolate, gaining a larger share of café menus. Operators are leveraging diverse syrup flavor profiles, such as salted caramel, dark chocolate, and hazelnut, to command higher price points per drink. Additionally, the increasing popularity of plant-based and vegan beverages is further boosting the demand for chocolate syrups that cater to these preferences. Suppliers that offer proprietary flavor signatures are gaining a competitive edge, as coffee chains increasingly seek differentiation in a saturated market. Furthermore, the rise of health-conscious consumers and the demand for clean-label, reduced-sugar syrups are expected to further shape product innovation and market dynamics. The integration of functional ingredients, such as protein or adaptogens, into chocolate syrups is also emerging as a key trend, aligning with the growing consumer interest in health and wellness.

Growing home baking and DIY dessert trends

The surge in home baking during the pandemic has normalized the preparation of desserts at home, driving sustained demand for chocolate syrup as a key finishing ingredient. Bakels, a global bakery ingredients supplier, reported in 2025 that consumers increasingly seek "restaurant-quality" results at home, leading to the adoption of professional-grade toppings previously limited to foodservice channels. Social media platforms, such as TikTok and Instagram, have further amplified this trend. Posts showcasing chocolate drizzle techniques have garnered millions of views, encouraging impulse purchases of premium syrups with visually appealing packaging. Brands are capitalizing on this momentum through innovative marketing strategies, including community engagement initiatives. However, as the segment matures, future growth is expected to depend more on premiumization and product differentiation rather than volume expansion.

Strong demand from bakery and confectionery sectors

Industrial bakeries and confectionery manufacturers are scaling production to meet rising demand in Asia-Pacific and the Middle East, driven by rapid urbanization, increasing disposable incomes, and the expansion of modern retail channels. In Brazil, where chocolate confectionery consumption per capita remains below North American levels, industrial bakeries are increasingly adopting chocolate syrup as a cost-effective filling and topping. This adoption is attributed to its shelf stability, ease of application, and versatility in enhancing product appeal. Additionally, the growing trend of convenience foods and ready-to-eat bakery products is further fueling the demand for chocolate syrup in industrial applications. This industrial demand underpins the segment's long-term growth trajectory, as manufacturers prioritize ingredients that streamline production, reduce labor costs, and cater to evolving consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative sweeteners and toppings | -1.30% | Global, strongest in North America & Europe; emerging in Asia-Pacific premium | Medium term (2-4 years) |

| Rising health concerns over high sugar intake | -1.50% | Global, led by North America & Europe; accelerating in China & Asia-Pacific | Short term (≤ 2 years) |

| Fluctuating cocoa and raw material prices | -1.10% | Global supply chain; most acute in North America & Europe | Short term (≤ 2 years) |

| Stringent regulations on sugar and additives | -0.90% | North America (FDA), Europe, China (2030 guidelines); expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health concerns over high sugar intake

Epidemiological evidence linking sugar-sweetened beverages to type 2 diabetes, cardiovascular disease, and obesity is significantly influencing consumer behavior and regulatory frameworks. The International Food Information Council reported in 2025 that 75% of United States consumers are actively limiting or avoiding sugar, signaling a growing shift toward healthier alternatives [2]Source: IFIC: International Food Information Council, "Sugars & Sweeteners", ific.org. Additionally, the FDA's proposed front-of-package labeling rule will mandate high-sugar products to display warning symbols, potentially curbing impulse purchases in retail settings [3]Source: U.S. Food and Drug Administration (FDA), "Front-of-Package Nutrition Labeling", fda.gov. This regulatory push, combined with evolving consumer preferences, is compelling manufacturers to adapt. Companies must either reformulate their products to align with health-conscious trends or face potential margin pressures as demand shifts toward premium, reduced-sugar variants. Furthermore, the rise of plant-based and natural sweeteners, such as stevia and monk fruit, is creating opportunities for innovation.

Competition from alternative sweeteners and toppings

Non-nutritive sweeteners are increasingly impacting the market share of chocolate syrups among health-conscious consumers. Ingredients like stevia, with an acceptable daily intake of 4 milligrams per kilogram of body weight as established by the European Food Safety Authority, and monk fruit, which received Generally Recognized as Safe (GRAS) status from the FDA in 2010, are enabling manufacturers to create zero-calorie syrups that cater to diabetic and weight-management-focused demographics. Additionally, there is a strategic shift toward incorporating mouthfeel-enhancing ingredients that replicate sugar's textural contributions in reduced-calorie formulations. Alternatives such as nut-butter drizzles, tahini-based sauces, and date syrups are gaining traction in specialty retail channels, positioning themselves as "whole-food" substitutes for processed chocolate syrups. Incumbent players face the challenge of reformulating their products to meet these evolving consumer preferences without compromising key sensory attributes like viscosity, glossiness, and cocoa intensity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Dark Chocolate Gains as Cocoa Flavanols Enter Wellness Discourse

Milk chocolate flavor accounted for 86.77% of the market share in 2025. Its dominance continues due to its widespread appeal and lower cocoa content, which shields manufacturers from price fluctuations. Additionally, milk chocolate's versatility in various applications, such as desserts, beverages, and confectionery, further strengthens its market position. Oat milk chocolate syrups, which substitute dairy with oat cream, are gaining popularity in Europe, where Oatly's success has normalized oat-based indulgence categories. This trend is particularly appealing to health-conscious consumers and those with dietary restrictions, as it offers a plant-based alternative without compromising taste. This trend is growing rapidly as foodservice operators seek allergen-free toppings that cater to dietary restrictions while maintaining flavor and quality.

Dark chocolate is projected to grow at an annual rate of 7.24% through 2031, driven by a strategic shift among manufacturers toward higher-cacao formulations that align with functional food trends. The European Food Safety Authority's approval of a health claim linking cocoa flavanols to cardiovascular health, requiring 200 milligrams of flavanols per serving, has positioned dark chocolate syrup as a wellness ingredient. This has enabled brands to command price premiums over milk chocolate variants. Furthermore, the increasing consumer preference for healthier and premium products has fueled innovation in dark chocolate syrups, with manufacturers focusing on clean-label formulations and organic certifications to attract a broader audience. Flavor segmentation is evolving, with mass-market players focusing on defending milk chocolate's volume base, while premium entrants capitalize on margin expansion through dark chocolate innovation.

By Category: Premium Segment Captures Margin as Sustainability Becomes Non-Negotiable

Mass-category products held 68.23% of the market share in 2025. The mass category's resilience is attributed to its strong presence in discount retailers and dollar stores, where affordability takes precedence over sustainability concerns. This segment benefits from economies of scale, enabling manufacturers to offer competitive pricing while maintaining widespread availability. Mass-market players often rely on aggressive promotional strategies and partnerships with large retail chains to sustain their dominance. However, the segment faces increasing margin pressures as private-label brands replicate premium features at competitive price points. This trend is compelling mass-market players to either innovate through reformulation, enhance product packaging, or risk losing market share to these emerging competitors.

Premium chocolate syrup variants are projected to grow at a compound annual growth rate (CAGR) of 8.05% through 2031, driven by evolving consumer preferences for transparency, sustainability, and product provenance. According to the Sustainable Packaging Coalition's 2025 report, 90% of consumers favor eco-friendly packaging, and 43% are willing to pay a premium for products demonstrating environmental responsibility. Premium chocolate syrups are capitalizing on this trend by incorporating sustainable practices such as using glass bottles, compostable pouches, and carbon-neutral certifications. These attributes not only align with consumer values but also justify higher price points compared to mass-market alternatives. Additionally, the premium segment is leveraging digital marketing and direct-to-consumer channels to enhance brand storytelling, further strengthening its appeal among environmentally conscious and quality-focused consumers.

By Packaging: Flexible Formats Disrupt Rigid Incumbents as Circularity Mandates Tighten

PET bottles captured 47.87% share in 2025. PET bottles retain dominance due to their structural integrity, transparency, which signals product quality, and compatibility with existing filling lines. Additionally, PET bottles are lightweight, shatterproof, and cost-effective, making them a preferred choice for manufacturers aiming to balance durability and affordability. Their recyclability also aligns with growing consumer demand for sustainable packaging solutions, particularly in developed markets. However, their share is expected to erode as flexible packaging scales and cost parity is achieved.

Pouches and sachets are projected to grow at 8.22% through 2031, as flexible packaging reduces material use by up to 60% versus rigid formats and aligns with circular-economy mandates in the European Union. Mono-material pouches, which eliminate multi-layer laminates that complicate recycling, are gaining adoption among premium brands seeking to differentiate on sustainability. Pouches also offer logistical advantages as they weigh 70% less than equivalent PET bottles, reducing transportation emissions and costs, a critical consideration as freight rates remain elevated. Single-serve sachets are penetrating emerging markets where affordability and trial are paramount. Tubes, categorized under others, serve niche applications in foodservice, where portion control and ease of dispensing justify higher per-unit costs.

By End-User: Foodservice Recovery Lags Retail, Yet Premiumization Drives Disproportionate Value

Retail channels accounted for 37.22% of the market share in 2025, driven by the growing penetration of e-commerce and the rising popularity of home-baking trends. This dominance is split between two key channels: supermarkets and hypermarkets, which provide a wide range of products and competitive promotional pricing, and online retail, which offers convenience and access to niche brands. Industrial end-users, such as bakeries and confectionery manufacturers, utilize chocolate syrup for its shelf stability and ease of application, streamlining production processes. Specialty stores, while smaller in volume, exert significant influence by curating premium and artisanal syrups that often set trends later adopted by mass-market channels. Other distribution channels, including convenience stores and vending machines, cater to impulse purchases but face structural challenges as consumers increasingly shift toward planned online shopping.

The foodservice/HoReCa segment is projected to grow at a CAGR of 6.89% through 2031, driven by menu innovation and the rise of off-premises consumption. Chocolate syrup has become a cost-effective yet impactful tool for menu customization, enabling operators to enhance beverages and desserts while justifying price increases and maintaining high gross margins. Specialty coffee chains are a key growth driver, incorporating chocolate syrups into seasonal offerings such as pumpkin mocha and peppermint hot chocolate, which encourage trial and repeat visits. The recovery of the foodservice segment depends on operators' ability to justify dine-in premiums through experiential elements, such as tableside dessert preparation and customizable sundae bars, where chocolate syrup plays a pivotal role.

Geography Analysis

North America held a 33.04% market share in 2025, driven by mature consumption patterns and well-established distribution networks. However, growth in the region is slowing due to health-driven reformulations and regulatory pressures impacting volume. In the United States, the largest market in the region, the FDA finalized front-of-package labeling rules in 2026, mandating warning symbols for high-sugar products, which could reduce impulse purchases in retail channels. In Canada, premiumization trends mirror those in the U.S., with consumers increasingly opting for organic and clean-label syrups. Meanwhile, Mexico's price-sensitive market continues to favor mass-market products, despite rising obesity rates and the implementation of sugar taxes. Hershey's opening of a 250,000-square-foot Reese Chocolate Processing facility in the United States in April 2025, as part of a USD 1 billion capital program, reflects confidence in North American demand while also serving as a defensive strategy to mitigate cocoa price volatility through vertical integration.

Europe's market dynamics are shaped by stringent sustainability mandates and sugar-reduction initiatives, with Germany, the United Kingdom, and France leading the premiumization trend. The European Union's Packaging and Packaging Waste Regulation, which requires all packaging to be recyclable or reusable by 2030, is accelerating the adoption of mono-material pouches and compostable formats. Growth in specialty coffee chains in Spain, Italy, and the Netherlands is driving demand for chocolate syrup in higher-margin beverage applications, while industrial bakery expansion in Poland and Belgium supports Central and Eastern European markets. Although population stagnation and mature consumption patterns constrain growth in the region, premiumization and functional innovation present opportunities for value creation.

Asia-Pacific is projected to grow at a rate of 6.74% through 2031, supported by rising disposable incomes, the Westernization of diets, and the expansion of modern retail in countries such as China, India, Indonesia, and Thailand. Monin's September 2025 investment of INR 35 billion in a 40-acre Hyderabad facility highlights confidence in South Asian demand and the strategic benefits of localized production. In China, the quick-service restaurant sector is increasingly using chocolate syrup as a topping for bubble tea and shaved ice, while Japan's specialty coffee culture drives demand for single-origin dark chocolate syrups. Australia and South Korea exhibit consumption patterns similar to North America, with premiumization and e-commerce penetration driving growth. Southeast Asia remains the highest-growth frontier, as urbanization and exposure to Western dessert formats through social media normalize the use of chocolate syrup.

Competitive Landscape

The chocolate syrup market demonstrates moderate fragmentation, with multinational giants such as Hershey, Nestlé, and Smucker's coexisting alongside regional specialists like Monin, Torani, and Hollander Chocolate, each employing distinct strategies to capture market share. Hershey's USD 1 billion capital program, culminating in the April 2025 opening of a 250,000-square-foot Reese Chocolate Processing facility featuring 13 new production lines, highlights the company's efforts to control formulation, enhance production efficiency, and protect margins from commodity price fluctuations. The competitive landscape increasingly favors companies that excel at balancing taste, health, and sustainability, as consumers demand products that combine indulgence with wellness without compromising on quality or ethical considerations.

Flavor innovation remains a key competitive focus as brands strive to differentiate themselves in a crowded market. Torani's launch of Forest Pine as its 2026 Flavor of the Year, with 100% of profits directed to nonprofits, showcases how brands use limited-edition releases to drive consumer interest, create buzz, and encourage trial purchases. Similarly, Monin's introduction of Yuzu Pineapple Syrup, sourced from its 74-acre biodynamic orchard in Portugal, reflects a growing emphasis on provenance-driven differentiation and the rising consumer preference for unique, exotic flavors. These innovations cater to evolving consumer tastes while aligning with sustainability and transparency trends.

Emerging disruptors include plant-based specialists and e-commerce-focused brands that capitalize on incumbents' slower adaptation to dietary and purchasing trends. In North American grocery channels, private-label brands replicate premium features such as organic certification, clean-label formulations, and sustainable packaging at mid-tier prices, thereby compressing margins for mass-market players. Additionally, the rise of direct-to-consumer (DTC) platforms has enabled smaller brands to reach niche audiences more effectively, further intensifying competition. Tate & Lyle's acquisition of CP Kelco for USD 1.8 billion, which added pectin and specialty gums to its portfolio, positions the company to provide integrated sweetening and texture solutions that address reformulation challenges, particularly in the context of sugar reduction and clean-label demands.

Chocolate Syrup Industry Leaders

-

The Hershey Company

-

Nestlé S.A.

-

The J.M. Smucker Company

-

Monin S.A.S.

-

Torani

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Monin launched its highly specialized Ruby Chocolate Syrup across Europe, delivering the naturally fruity, subtly tangy, and creamy flavor of ruby cocoa in a mixologist-friendly format. This innovative syrup combines the smoothness of traditional chocolate with delicate berry notes, boasting a signature vibrant pink color without relying on artificial colorings or berry flavors.

- November 2025: Torani launched Forest Pine as its 2026 Flavor of the Year, with 100% of profits directed to nonprofit organizations. This limited-edition release exemplifies how brands leverage seasonal innovation to generate trial and reinforce brand values.

- September 2025: Monin announced an investment of INR 35 billion in a 40-acre manufacturing facility in Hyderabad, India, operational by Q2 FY 2026 and targeting INR 15 billion in turnover by FY 2026. This expansion reflects confidence in South Asian demand and the strategic advantage of localized production to serve domestic and Middle Eastern markets.

- April 2025: The Hershey Company opened a new 250,000-square-foot Reese Chocolate Processing facility as part of a USD 1 billion capital investment program. The facility features 13 new production lines, enabling vertical integration to insulate against cocoa price volatility.

Global Chocolate Syrup Market Report Scope

Chocolate syrup is a liquid confectionery product with a consistency that ranges from thin to thick, specifically designed to infuse the chocolate flavor in various food items. The chocolate syrup market is segmented by flavor, category, packaging, end-user, and geography. Based on flavor, the market is segmented into milk chocolate and dark chocolate. By category, the market is segmented into premium and mass. By packaging, the market is segmented into PET bottles, pouches and sachets, and others. By end-user, the market is segmented into foodservice/HoReCa, industrial, and retail. By retail, the market has been segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (Tons).

| Milk Chocolate |

| Dark Chocolate |

| Premium |

| Mass |

| PET Bottles |

| Pouches and Sachets |

| Others |

| Foodservice/HoReCa | |

| Industrial | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Flavor | Milk Chocolate | |

| Dark Chocolate | ||

| By Category | Premium | |

| Mass | ||

| By Packaging | PET Bottles | |

| Pouches and Sachets | ||

| Others | ||

| By End-User | Foodservice/HoReCa | |

| Industrial | ||

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current chocolate syrup market size and expected growth?

The chocolate syrup market size is USD 11.91 billion in 2026 and is projected to reach USD 16.31 billion by 2031, reflecting a 6.49% CAGR.

Which flavor segment is expanding the fastest?

Dark chocolate syrup is the fastest-growing flavor, forecast to advance at 7.24% CAGR as consumers seek health-aligned premium options.

Why are pouches and sachets gaining popularity over PET bottles?

EU mandates for recycled content and consumer preference for lighter, recyclable packs drive a 8.22% CAGR for pouches and sachets, even though PET still leads overall share.

Which region offers the strongest growth opportunity?

Asia-Pacific delivers the highest regional CAGR of 6.74% to 2031 due to rapid urbanization, rising incomes and café culture expansion.

Page last updated on: