Bean-to-Bar Chocolate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.65 Billion |

| Market Size (2031) | USD 6.56 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bean-to-Bar Chocolate Market Analysis by Mordor Intelligence

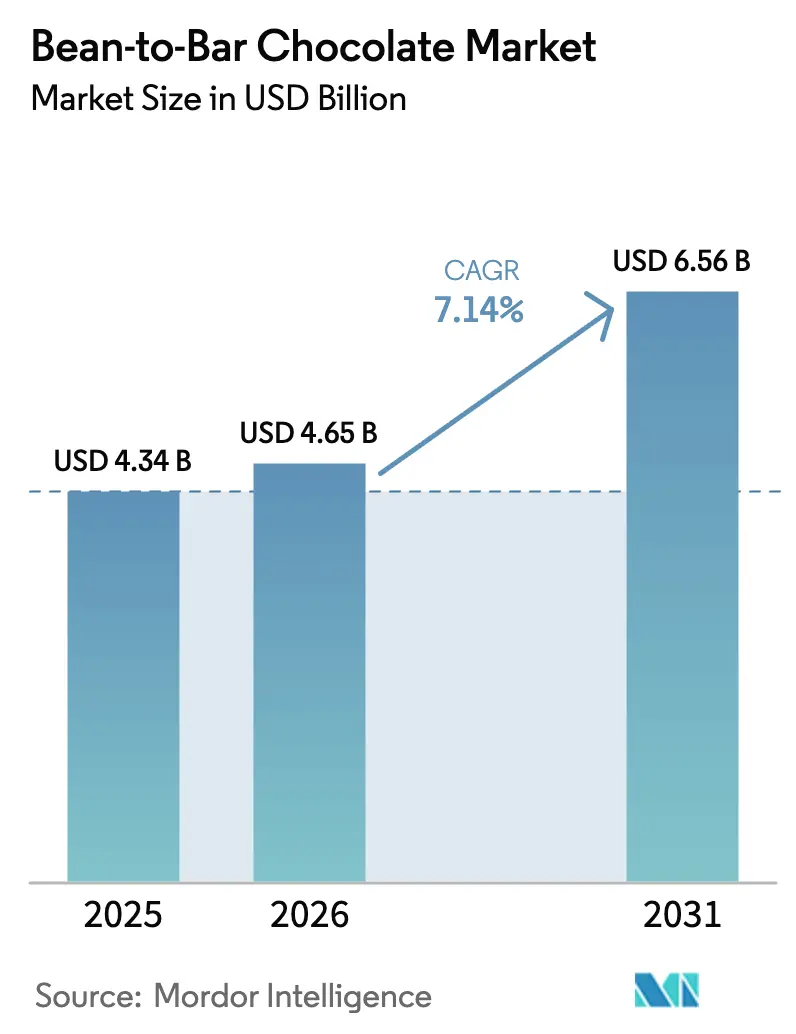

The Bean-to-Bar chocolate market size was valued at USD 4.34 billion in 2025 and estimated to grow from USD 4.65 billion in 2026 to reach USD 6.56 billion by 2031, at a CAGR of 7.14% during the forecast period (2026-2031). Consumers are increasingly gravitating towards transparent supply chains, ethical sourcing, and premium flavor profiles, which distinctly set artisanal makers apart from commodity producers. These preferences reflect a growing demand for products that align with personal values, such as sustainability and quality. Despite rising cocoa prices, growth in the market remains robust as buyers view single-origin bars as affordable luxuries that fulfill dual motives of wellness and indulgence. This trend highlights the willingness of consumers to pay a premium for products that offer both superior taste and ethical assurance. A strong e-commerce backbone has further facilitated access to these premium offerings, while innovative flavor developments continue to attract a broader audience. Additionally, Europe's stringent sustainability regulations are shaping purchasing decisions, encouraging brands to adopt environmentally responsible practices that reinforce their premium positioning. Competitive strategies in the market are increasingly centered on direct-trade models, which not only ensure consistent bean quality but also help stabilize margins in the face of price volatility, thereby strengthening the overall value proposition for both producers and consumers.

Key Report Takeaways

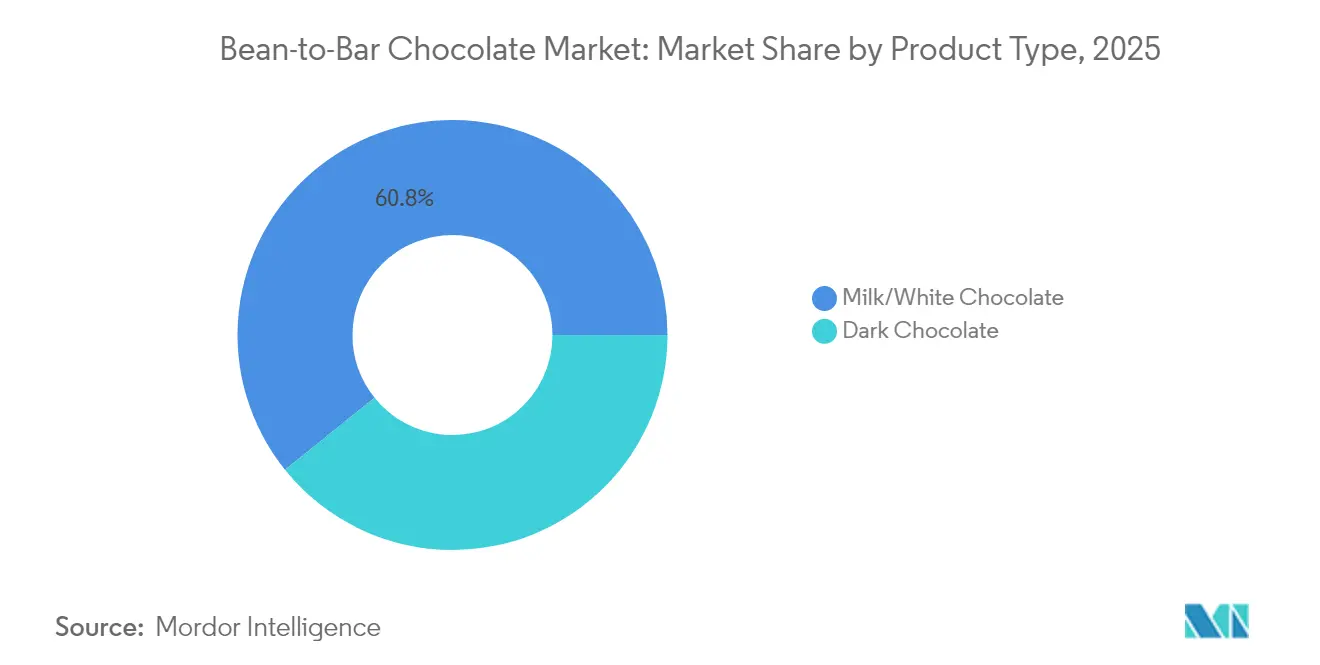

- By product type, Milk/White Chocolate held 60.78% of the Bean-to-Bar chocolate market share in 2025, while Dark Milk Chocolate is forecast to expand at a 7.28% CAGR through 2031.

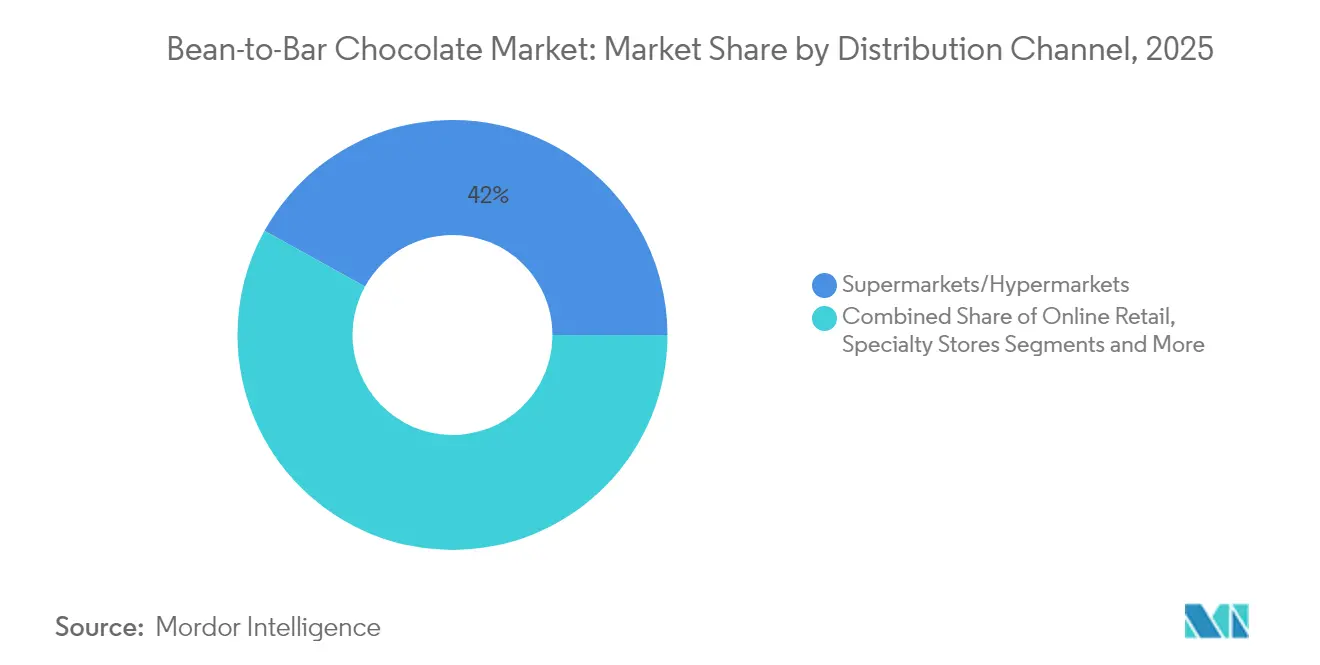

- By distribution channel, Supermarkets/Hypermarkets commanded 41.95% of the Bean-to-Bar chocolate market size in 2025, and Online Retail records the fastest 7.78% CAGR to 2031.

- By geography, Europe captured 31.02% revenue share in 2025; Asia-Pacific advances at a 7.32% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bean-to-Bar Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for dark, high-cocoa chocolate | +1.2% | Global, with stronger adoption in Europe and North America | Medium term (2-4 years) |

| Premiumisation trend in confectionery and gifting | +1.8% | Europe, North America, Asia-Pacific urban centers | Long term (≥ 4 years) |

| E-commerce expansion for micro-brands | +1.5% | Global, with acceleration in Asia-Pacific and North America | Short term (≤ 2 years) |

| Demand for ethical and traceable sourcing | +1.1% | Europe, North America, with emerging influence in Asia-Pacific | Medium term (2-4 years) |

| Emergence of cocoa-free fermentation technologies | +0.4% | Europe, North America (early adoption markets) | Long term (≥ 4 years) |

| Corporate sustainability in gifting programs | +0.6% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing preference for dark, high-cocoa chocolate

Health-conscious consumers are increasingly associating higher cocoa content with antioxidant benefits and reduced sugar intake, which is accelerating the migration toward dark chocolate varieties and driving market premiumization. The National Confectioners Association has reported a significant rise in fine chocolate consumption, with younger, urban demographics actively driving this shift. This growing demand is enabling bean-to-bar producers to command premium margins on single-origin, high-percentage cacao bars. European specialty cocoa markets are expected to grow annually by 8.7% through 2028, with single-origin chocolates gaining strong traction among discerning consumers who value unique offerings [1]Source: Centre for the Promotion of Imports from Developing Countries, "The European market potential for speciality cocoa", www.cbi.eu. This shift in consumer preference is also allowing smaller producers to differentiate themselves by emphasizing terroir expression and crafting unique flavor profiles that mass-market milk chocolate cannot replicate. Additionally, FDA regulations under 21 CFR 163.123 mandate a minimum of 15% chocolate liquor content for sweet chocolate, providing a clear regulatory framework to uphold quality standards.

Premiumisation trend in confectionery and gifting

The premiumisation trend is a significant driver in the Bean-to-Bar Chocolate Market. Consumers are increasingly seeking high-quality, artisanal products that offer unique flavors and superior ingredients. This shift reflects a change in purchasing behavior, where individuals prioritize value and experience, even in everyday treats. Premium chocolate brands are capitalizing on this demand by offering products that balance luxury and affordability, appealing to a broader audience. The emphasis on unique flavors, sustainable sourcing, and artisanal craftsmanship further enhances the appeal of premium chocolates as an accessible luxury option. Additionally, the gifting culture has amplified the demand for premium confectionery, as consumers prefer to present items that reflect sophistication and exclusivity. Supporting this trend, Jordbruksverket reported that Sweden's per capita consumption of chocolate and confectionery increased to 16.4 kg in 2023, up from 15.8 kg in 2021 [2]Source: Jordbruksverket, "Per capita consumption of chocolate and confectionery in Sweden", statistik.sjv.se. This rise in consumption highlights the growing demand for chocolate products, including premium offerings, as consumers increasingly view chocolate as a means of affordable indulgence. The data underscores the expanding market potential for premium chocolate, driven by evolving consumer preferences for products that combine quality, taste, and an element of luxury.

E-commerce expansion for micro-brands

Micro-brands are expanding their reach through e-commerce, which is emerging as a significant driver in the Bean-to-Bar Chocolate Market. Digital commerce platforms eliminate traditional retail barriers, enabling micro-chocolate brands to reach global audiences without significant capital investment in physical distribution networks. Chinese e-commerce platforms like JD.com and Taobao facilitate market entry for international artisanal brands, with the Chinese chocolate market showing strong growth momentum despite foreign brand dominance. This direct-to-consumer approach allows micro-brands to showcase their unique offerings, such as premium-quality, ethically sourced, and artisanal chocolates, to a broader audience. This channel expansion allows producers to maintain higher margins by eliminating intermediary markups while building direct customer relationships that support premium pricing. The model particularly benefits single-origin and limited-edition products that traditional retailers might not stock due to inventory constraints or unfamiliar flavor profiles. Additionally, the convenience of online shopping and the ability to target niche consumer segments through digital marketing strategies are further fueling the growth of micro-brands in the e-commerce space.

Demand for ethical and traceable sourcing

The increasing consumer preference for ethically sourced and traceable products is a significant driver in the Bean-to-Bar Chocolate Market. Consumers are becoming more conscious of the environmental and social impact of their purchases, leading to a higher demand for transparency in the supply chain. Ethical sourcing ensures that cocoa farmers receive fair compensation and work under humane conditions, while traceability allows consumers to verify the origins and production processes of the chocolate they consume. This trend is compelling manufacturers to adopt sustainable practices and provide detailed information about their sourcing and production methods. As a result, companies focusing on ethical and traceable sourcing are gaining a competitive edge in the market. Furthermore, regulatory bodies and certifications, such as Fair Trade and Rainforest Alliance, are playing a pivotal role in promoting ethical sourcing practices. These certifications not only assure consumers of the product's authenticity but also encourage manufacturers to adhere to stringent ethical standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cocoa prices and sensitivity to consumer pricing | -2.1% | Global, with acute impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Costs associated with forced-labour compliance | -0.8% | Europe, North America (strict regulatory enforcement) | Medium term (2-4 years) |

| Limitations of artisanal production scale | -1.2% | Global, particularly affecting micro-producers | Long term (≥ 4 years) |

| High failure rate for start-ups among micro-makers | -0.7% | North America, Europe (high concentration of new entrants) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile cocoa prices and sensitivity to consumer pricing

Unprecedented cocoa price volatility poses the most significant threat to the stability of the Bean-to-Bar Chocolate Market. Prices fluctuated from USD 2,000 per ton in 2023 to peaks exceeding USD 12,000 in 2024, before declining by over 30% in early 2025[3]Source: Anadolu Agency (AA), "Cocoa prices drop over 30% in 2025 after last year's record high", www.aa.com.tr. This extreme volatility, driven by factors such as supply chain disruptions, weather conditions, geopolitical issues, and speculative trading in commodity markets, directly impacts production costs. Such fluctuations create uncertainty for manufacturers, making it challenging to plan long-term strategies and manage budgets effectively. Additionally, the rising costs are often passed on to consumers, which can lead to reduced demand, especially among price-sensitive segments. The premium nature of bean-to-bar chocolate further amplifies this issue, as consumers may opt for more affordable alternatives during periods of economic uncertainty. Such market dynamics make it difficult for manufacturers to maintain consistent profit margins while ensuring competitive pricing and catering to evolving consumer preferences.

Limitations of artisanal production scale

The limitations of artisanal production scale act as a significant restraint in the Bean-to-Bar Chocolate Market. Artisanal producers often operate on a small scale, which restricts their ability to meet growing consumer demand. This limited production capacity can lead to supply shortages, especially during peak demand periods. Additionally, the high costs associated with small-scale production, including sourcing premium-quality cocoa beans and maintaining traditional manufacturing processes, further constrain their scalability. These producers also face challenges in achieving economies of scale, which larger industrial manufacturers can leverage to reduce costs and improve profit margins. Furthermore, the lack of advanced machinery and technology in artisanal setups often results in longer production times and higher labor costs, impacting overall efficiency. As the market continues to grow, these limitations may hinder the ability of artisanal producers to compete effectively with larger players, thereby affecting their market share and growth potential. Moreover, artisanal producers frequently encounter difficulties in establishing a robust supply chain for high-quality cocoa beans, as they often rely on smallholder farmers who may face their own production constraints. This dependency can lead to inconsistencies in raw material availability and quality, further complicating production processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Drives Premium Migration

Milk and white chocolate continue to dominate the bean-to-bar chocolate market, collectively maintaining the largest market share at 60.78% in 2025. The popularity of these chocolate varieties can be attributed to their widespread appeal and milder, sweeter taste profiles, which resonate strongly with a broad segment of consumers. These products are often favored for their creamy texture and versatility in both confectionery and cooking applications, making them staples in households and commercial establishments alike. The enduring popularity of milk and white chocolate also reflects their accessibility, as they are commonly available across varied price points and retail formats, ensuring broad market penetration. Brand loyalty and established consumer preferences continue to reinforce the dominance of these segments, especially in established markets. As a result, milk and white chocolates remain central to the revenue streams of leading bean-to-bar chocolate manufacturers.

In contrast, dark milk chocolate has emerged as the fastest-growing segment within the bean-to-bar chocolate market, projected to achieve a compound annual growth rate (CAGR) of 7.28% through 2031. This rapid growth reflects a shift in consumer attitudes toward more sophisticated and health-conscious chocolate options. Dark milk chocolate bridges the gap between traditional milk chocolate and rich dark chocolate, appealing to consumers who seek complex flavors with moderate sweetness and enhanced cacao content. The rise of this segment is fueled by increasing awareness of the potential health benefits associated with higher cocoa content, including antioxidant properties and reduced sugar intake. Artisanal chocolate makers are responding with innovative dark milk chocolate products that highlight single-origin cacao and unique production techniques. As consumers become more discerning and adventurous, the dark milk chocolate segment is poised to capture an expanding share of the premium and specialty chocolate market.

By Distribution Channel: Digital Commerce Transforms Access

Supermarkets and hypermarkets continue to be the dominant distribution channels in the bean-to-bar chocolate market, maintaining a substantial market share of 41.95% in 2025. Their strength lies in their wide accessibility, established infrastructure, and unparalleled reach to diverse consumer segments. These large-format retailers offer consumers the convenience of one-stop shopping, enabling them to access a broad range of premium and artisanal chocolates alongside everyday grocery items. In addition, supermarkets often provide ample shelf space and prominent visibility for bean-to-bar chocolate brands, enhancing both impulse and planned purchases. Their ability to run targeted promotions, offer discounts, and partner with chocolate manufacturers for in-store engagement further cements their importance in the market. As a result, supermarkets and hypermarkets continue to be the primary revenue channels for bean-to-bar chocolate producers and play a decisive role in market penetration.

Meanwhile, online retail is achieving the highest growth rate among all distribution channels, with an impressive CAGR of 7.78% through 2031. This rapid expansion reflects evolving consumer shopping behaviors that increasingly prioritize convenience, product variety, and direct engagement with brands. The digital marketplace allows consumers to explore a global assortment of bean-to-bar chocolates, including limited-edition or single-origin bars that may not be widely available in physical stores. Online platforms provide an ideal setting for small-scale chocolatiers and artisanal brands to share their stories and establish direct connections, fostering brand loyalty through personalized experiences. The rise of online retail is bolstered by advancements in e-commerce technologies, efficient delivery networks, and the growing popularity of direct-to-consumer sales models. As these trends intensify, online retail stands out as the fastest-growing channel, driving substantial transformation within the bean-to-bar chocolate market landscape.

Geography Analysis

In 2025, Europe solidifies its dominance in the Bean-to-Bar Chocolate market, holding a 31.02% share. This is largely due to the continent's discerning consumers and stringent sustainability regulations, which favor artisanal producers with transparent supply chains. The region's long-standing tradition of chocolate consumption, coupled with increasing awareness of ethical sourcing, has created a fertile ground for the growth of the bean-to-bar segment. The United Kingdom spearheads regional consumption, bolstered by rising imports of specialty cocoa and a surge in craft chocolate manufacturers catering to the refined local palate. The growing number of small-scale producers in the UK reflects a broader trend across Europe, where consumers are increasingly drawn to high-quality, handcrafted products. European consumers show a pronounced preference for organic and single-origin products, often paying a premium for those that emphasize environmental and social responsibility. Additionally, the region's regulatory environment, which prioritizes sustainability and transparency, has encouraged producers to adopt practices that align with these values, further strengthening the market.

Asia-Pacific is on a rapid ascent, projected to grow at a 7.32% CAGR through 2031, fueled by swift economic progress and a shift in consumer preferences towards premium, health-focused products. The region's expanding middle class, particularly in countries like China, India, and Japan, is driving demand for high-quality chocolate products. Rising disposable incomes and increased exposure to global food trends have led to a growing appreciation for artisanal and premium chocolates. Health-conscious consumers in the region are also gravitating toward products with natural ingredients and lower sugar content, creating opportunities for bean-to-bar producers to cater to these preferences. Furthermore, the region's younger demographic, with its openness to experimenting with new flavors and formats, is contributing to the market's rapid growth. The increasing presence of international and local players investing in the region further underscores its potential as a key growth driver in the global bean-to-bar chocolate market.

North America boasts a well-established craft chocolate infrastructure, bolstered by consumer education. This region is home to around 480 global specialty chocolate makers. The United States stands out with its robust consumption, thanks to direct-trade ties with cacao producers in Central and South America. These relationships foster transparent sourcing narratives, appealing to the region's conscious consumers. Meanwhile, Canada and Mexico play pivotal roles in regional growth, both in consumption and production. Notably, Mexico's rich cacao heritage lends authenticity to its bean-to-bar ventures. South America is carving a niche with its tree-to-bar operations, allowing cacao-producing nations to enhance their value chain margins through local processing and subsequent international export. In the Middle East and Africa, burgeoning economic development and urbanization are birthing new consumer segments. However, certain nations grapple with political instability and infrastructure challenges, tempering their growth potential.

Competitive Landscape

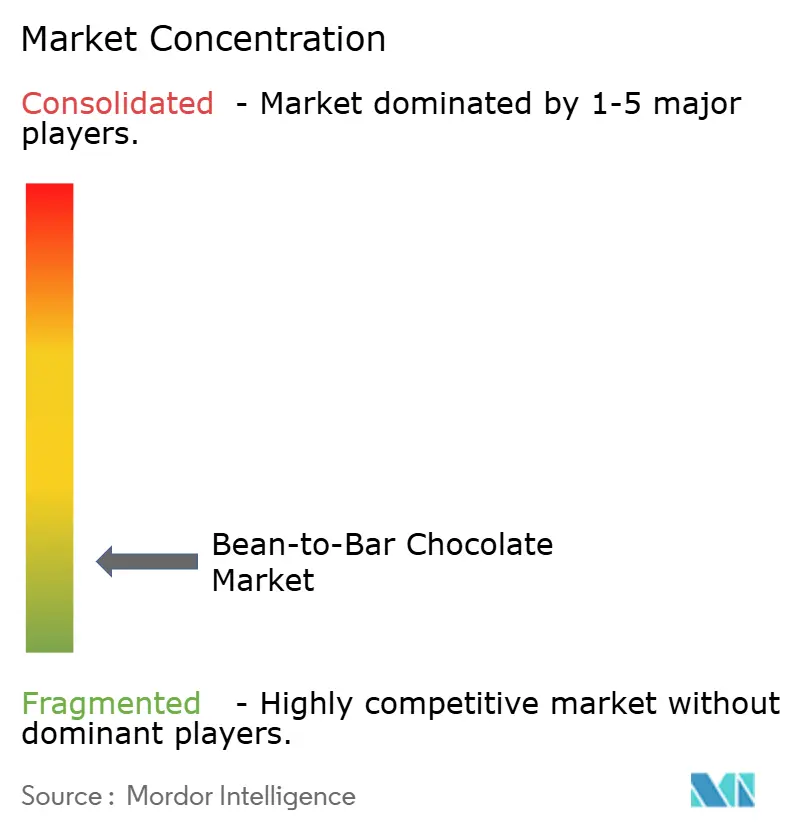

The Bean-to-Bar Chocolate market demonstrates moderate fragmentation, with a concentration score of 2. This score reflects the coexistence of well-established artisanal brands and emerging micro-producers. These players compete primarily through differentiation strategies rather than leveraging scale advantages. The market's competitive dynamics are shaped by the unique value propositions offered by these producers, which cater to a growing consumer demand for high-quality, ethically sourced, and premium chocolate products. Established artisanal brands in the market focus on maintaining their reputation by emphasizing craftsmanship, quality, and authenticity.

These companies often invest in direct-sourcing relationships with cocoa farmers, ensuring traceability and sustainability throughout the supply chain. By fostering such relationships, they not only secure high-quality raw materials but also build a compelling transparency narrative that resonates with ethically conscious consumers. This approach enables them to justify premium pricing and maintain a competitive edge over mass-market chocolate manufacturers. Additionally, these brands leverage their expertise in chocolate-making techniques and their ability to tell a compelling brand story, further solidifying their position in the market.

Emerging micro-producers, on the other hand, bring innovation and creativity to the market. These smaller players often experiment with unique flavors, limited-edition offerings, and locally sourced ingredients to differentiate themselves. Their agility allows them to quickly adapt to changing consumer preferences and trends. Despite their smaller scale, these producers leverage storytelling and branding to create a strong emotional connection with their target audience. Together, the established brands and micro-producers contribute to the dynamic and evolving nature of the Bean-to-Bar Chocolate market, driving competition and innovation within the industry.

Bean-to-Bar Chocolate Industry Leaders

-

Goodnow Farms

-

Maui Kuʻia Estate Chocolate

-

Raaka Chocolate Ltd

-

Salgado Chocolates

-

Askinosie Chocolate

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Love Cocoa, the sustainable chocolate brand, unveiled two new additions to its lineup: a creamy 35% Blonde Chocolate Bar and a rich 85% Dark Chocolate Bar. Crafted in the UK, these contemporary bars, with their signature luxe appearance and eco-friendly packaging, utilized sustainably sourced, single-origin Colombian cocoa. They were designed to cater to consumers seeking a more indulgent and sophisticated chocolate experience.

- June 2024: Raaka Chocolate reintroduced a new collection featuring six limited-edition bars from its First Nibs series. The collection included unique flavors such as Salted Cherry Wood 70%, Porcini Mushroom 67%, Cranberry Pink Peppercorn 70%, Matcha Swirl, Vanilla Rooibos 68%, and Hojicha & Bitter Orange 70%, offering a diverse range of taste experiences for chocolate enthusiasts.

- September 2023: Dandelion Chocolate expanded its direct trade program by establishing partnerships with cocoa farmers in Belize and the Philippines. This initiative aimed to promote fair pricing and support sustainable farming practices.

Global Bean-to-Bar Chocolate Market Report Scope

Bean-to-bar chocolates are produced by processing cacao beans into chocolate bars. These products can be produced in-house and have many small-scale players operating in this business. Most chocolate-making companies just melt ready-made chocolates, but bean-to-bar chocolate manufacturers have control over the whole process and produce chocolates from cocoa beans. The global bean-to-bar chocolate market (henceforth referred to as the market studied) is segmented by product type, distribution channel, and geography. By type, the market is segmented into dark chocolate, and milk/white chocolate.

Based on the distribution channel, the market studied is segmented into supermarkets/ hypermarkets, convenience stores, online stores, and other distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, Middle-East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Dark Chocolate |

| Milk/White Chocolate |

| Supermarkets/Hypermarkets |

| Specialty and Gourmet Stores |

| Online Retail |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Dark Chocolate | |

| Milk/White Chocolate | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Gourmet Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Bean-to-Bar chocolate market?

The Bean-to-Bar chocolate market size is USD 4.65 billion in 2026.

How fast is the market expected to grow through 2031?

It is forecast to post a 7.14% CAGR and reach USD 6.56 billion by 2031.

Which region is expanding quickest?

Asia-Pacific records the fastest 7.32% CAGR due to rising incomes and premiumization.

Which product segment is gaining momentum?

Dark Milk Chocolate leads growth with a 7.28% CAGR as consumers shift toward higher cocoa content.

How are cocoa-price swings affecting producers?

Volatile prices squeeze margins for small makers, causing some to reduce volumes or exit despite stable demand.

Page last updated on: