Lollipop Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

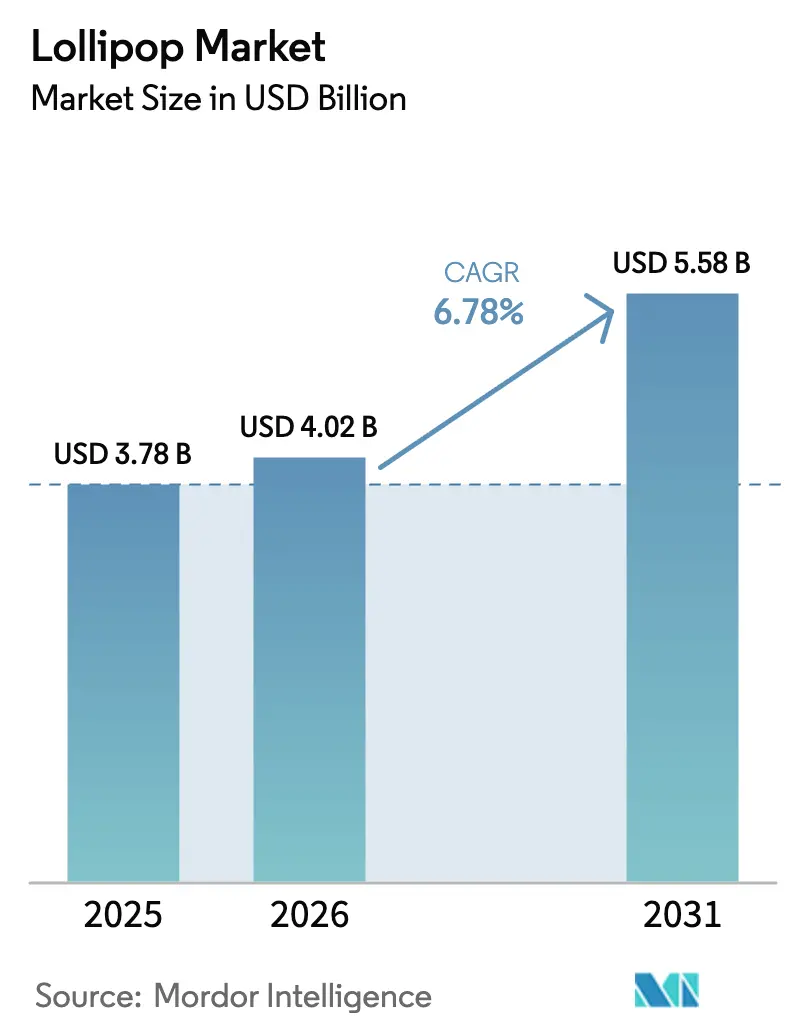

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 5.58 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

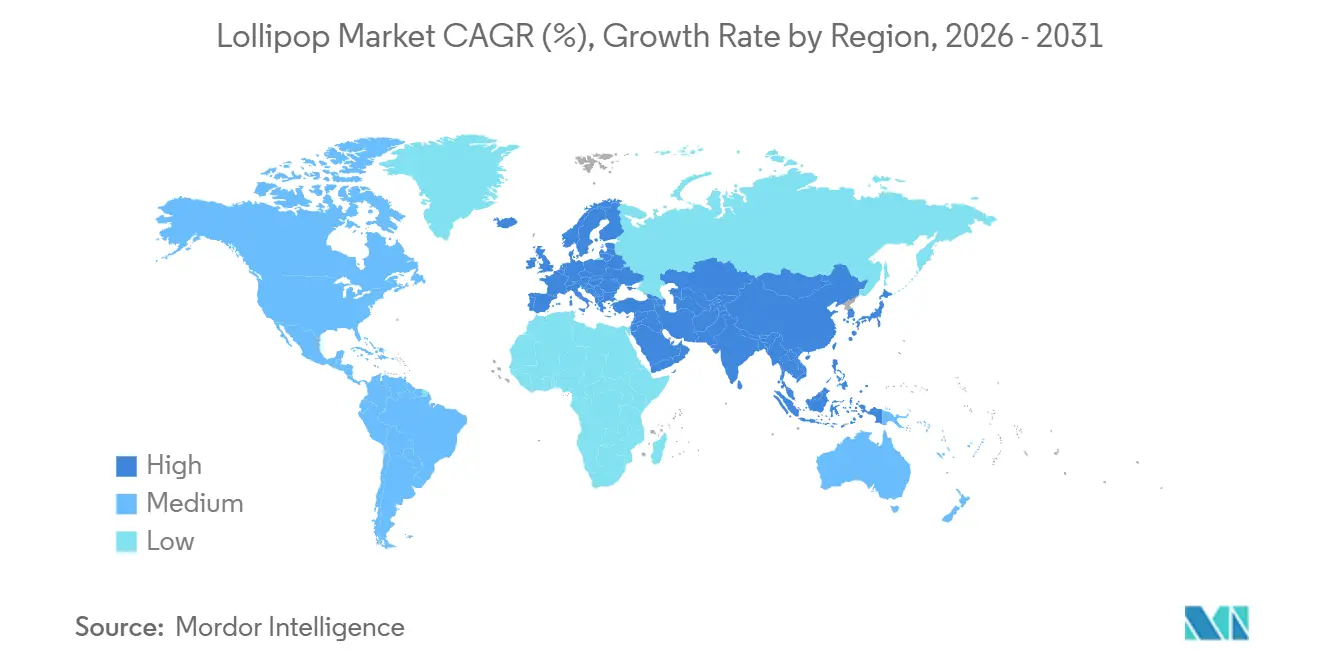

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lollipop Market Analysis by Mordor Intelligence

The Lollipop Market size is projected to expand from USD 3.78 billion in 2025 and USD 4.02 billion in 2026 to USD 5.58 billion by 2031, registering a CAGR of 6.78% between 2026 to 2031. Despite challenges faced by other confectionery categories due to commodity volatility, the lollipop market remains strong. This stability is driven by high demand for affordable indulgences, consistent sugar input costs, and the industry's rapid shift toward sugar-free and artisanal products. E-commerce is expanding the market's accessibility, enabling direct-to-consumer brands to overcome traditional shelf-space constraints and scale personalized gifting. Premiumization continues to gain momentum, with botanical flavors and design-focused sticks achieving double-digit price premiums and supporting profit margins. Additionally, sugar-free options made with stevia, erythritol, and allulose are becoming mainstream, increasing their appeal among diabetic, keto, and health-conscious consumers.

Key Report Takeaways

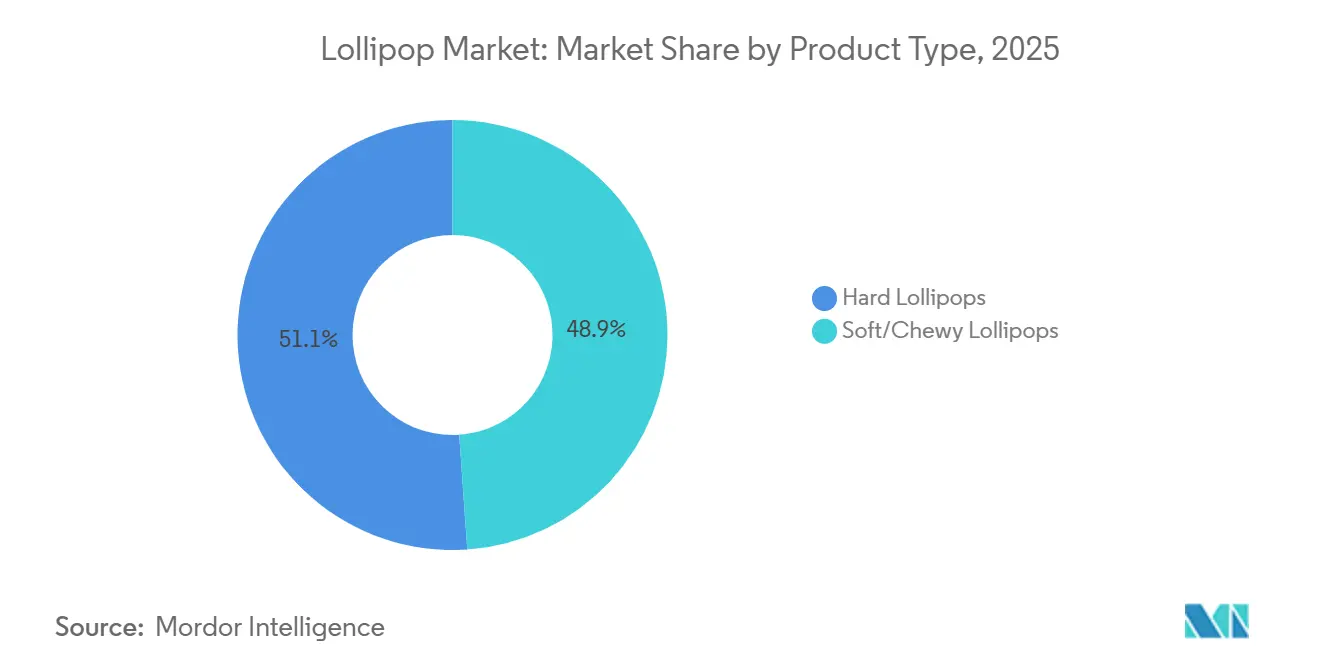

- By product type, hard lollipops led with 51.09% of lollipop market share in 2025, while soft/chewy variants are advancing at a 7.28% CAGR through 2031.

- By category, conventional sugar-based items held 86.74% of the lollipop market size in 2025, but sugar-free alternatives are growing at a 7.45% CAGR to 2031.

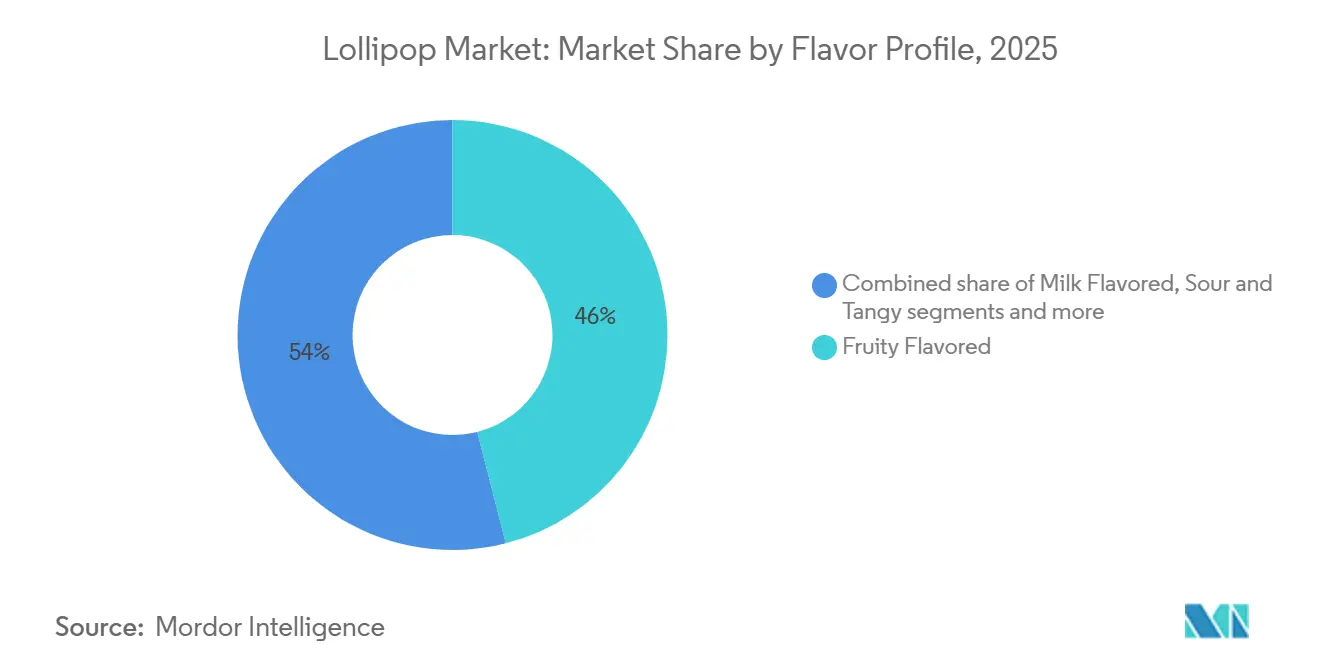

- By flavor profile, fruity flavors accounted for 46.02% of the lollipop market size in 2025; sour and tangy offerings are the fastest mover at a 7.11% CAGR.

- By distribution, supermarkets and hypermarkets delivered 42.33% of the 2025 value, yet online retail is rising at a 7.98% CAGR, topping every other channel.

- By geography, Asia-Pacific captured 36.23% of 2025 revenue, while Europe is the fastest-growing region at a 7.68% CAGR on the back of sour innovation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lollipop Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for confectionery among children and adults | +1.2% | Global, with concentration in Asia-Pacific (China, India, Southeast Asia) and North America | Medium term (2-4 years) |

| Impulse purchase behavior at point-of-sale | +1.0% | Global, strongest in North America and Europe convenience channels | Short term (≤ 2 years) |

| Seasonal and festive demand spikes | +0.9% | North America and Europe (Halloween, Easter, Valentine's, winter holidays); emerging in Latin America | Short term (≤ 2 years) |

| Gourmet and premium positioning | +0.8% | North America, Western Europe, urban centers in Asia-Pacific | Long term (≥ 4 years) |

| Sustainable, eco-friendly packaging | +0.7% | Europe (EU Packaging Directive), North America, Australia | Medium term (2-4 years) |

| Custom and personalized gifting | +0.6% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for confectionery among children and adults

In 2025, the National Confectioners Association revealed that confectionery products were present in 99.8% of U.S. households[1]Source: National Confectioners Association, “Confectionery Sales Climb to USD 55 Billion in 2025,” candyusa.com . Lollipops, with prices ranging from USD 0.25 to USD 0.75, have established a distinct position. This pricing enables them to perform well even during inflationary periods, unlike premium chocolate bars priced above USD 3.00. In the Asia-Pacific region, where confectionery plays a key role in snacking, manufacturers are adapting products to suit local preferences. For instance, in 2025, Mars Wrigley launched a half-sugar Snickers variant, and Lotte increased production in Thailand to meet Southeast Asian demand. Adult consumption of confectioneries is growing faster than pediatric consumption, fueled by nostalgia and a demand for healthier options. Consumers are increasingly opting for variants fortified with vitamins, probiotics, and adaptogens. This widespread appeal protects lollipops from regulatory scrutiny over children's sugar intake and allows manufacturers to shift marketing efforts toward adult consumers without altering the product's core formulation.

Impulse purchase behavior at point-of-sale

Retailers leverage the affordability, compact size, and extended shelf life of lollipops, which ranges from 12 to 18 months, to strategically position them in high-traffic checkout areas. This approach minimizes inventory risks while maximizing impulse purchases. In Europe, convenience confectionery sales have experienced significant growth as consumer behavior normalizes post-pandemic. Countries such as Italy, France, and Singapore have particularly reflected this trend, driven by the resurgence of on-the-go consumption habits. The introduction of innovative formats, including freeze-dried candies, lollipops featuring licensed characters, and the increasingly popular "swicy" (sweet-spicy) flavors, has further fueled incremental sales. Licensed products, in particular, contribute to higher basket values compared to generic stock-keeping units (SKUs), highlighting their appeal to consumers. Among retail channels, convenience stores have emerged as the fastest-growing segment, surpassing supermarkets and hypermarkets. This growth is attributed to their ability to cater to spontaneous indulgence moments, which are less likely to occur during planned grocery shopping trips.

Seasonal and festive demand spikes

In the four major seasonal events, Valentine's Day, Easter, Halloween, and the winter holidays, contribute 62% to 63% of annual confectionery sales. Winter holidays alone account for over 18% of these seasonal sales. During Halloween, lollipops lead sales due to their suitability for trick-or-treating. Brands like YummyEarth and Zolli Candy offer individually wrapped, allergen-friendly options that command premium pricing. Valentine's Day drives demand for gourmet lollipops featuring intricate designs, custom logos, and botanical flavors. Small-batch producers leverage this demand, pricing wedding favors and corporate gifts between USD 3.00 and USD 5.00 per unit. Mint-flavored confections see a sales peak in December, aligning with holiday gifting trends, while fruity and sour flavors dominate spring and summer. Manufacturers begin production 6 to 9 months before peak seasons. Although this approach creates cash-flow volatility, it enables price premiums, as seasonal SKUs typically deliver higher margins than year-round products. The concentration of sales into four distinct periods heightens the importance of retail shelf space negotiations and promotional planning, with late entrants often excluded from prime checkout placements.

Gourmet and premium positioning

Premium and specialty candies are experiencing significant growth. Gourmet lollipops are branching into two primary categories: design-led formats, featuring visual crafts, embedded art, and QR codes, and ingredient-led formats, focusing on honey-forward flavors, natural colorings, and botanical tastes. Design-focused producers utilize small-batch, hand-poured methods to create custom lollipops for weddings, corporate events, and hostess gifts, priced between USD 3.00 and USD 5.00 per unit, 10 to 20 times higher than mass-market alternatives. In contrast, ingredient-driven brands emphasize transparency by showcasing organic certifications, non-GMO verifications, and single-origin honey sourcing, appealing to consumers willing to pay a premium for superior quality and sustainability. In February 2026, Perfetti Van Melle's Chupa Chups collaborated with New Era in Japan to reposition lollipops as fashion accessories rather than just confectionery. Similarly, in March 2026, Sweet Venture Group launched Gummi Popz, a popping gummy candy priced at USD 2.49, blending the characteristics of lollipops and novelty candies. The expansion of this segment not only drives its own growth but also enhances the brand perception of mass-market SKUs within the same portfolio.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Childhood obesity and sugar-intake concerns | -0.8% | Global, most acute in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Sugar taxes and tightening regulations | -0.6% | Europe (108 countries with SSB taxes), Latin America (Mexico, Chile), Middle East (Saudi Arabia, UAE) | Short term (≤ 2 years) |

| Competition from chocolates and alternatives | -0.5% | Global, strongest in North America and Europe where chocolate holds 60%+ confectionery share | Long term (≥ 4 years) |

| Pressure for natural and clean-label input | -0.4% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Childhood obesity and sugar-intake concerns

The World Health Organization (WHO) advises that both adults and children should limit free sugars to less than 10% of their total energy intake. They even suggest a further reduction to below 5% in certain cases, highlighting the association between sugar intake and issues like childhood obesity, type 2 diabetes, and dental problems. In 2024, WHO's Regional Office for Europe released a policy brief pinpointing sugar-sweetened beverages (SSBs) as a major factor in childhood obesity. They advocate for evidence-backed measures like taxing SSBs and implementing specific school food policies. WHO data from 2024 reveals that 35 million children under 5 were classified as overweight[2]Source: World Health Organization, "Obesity and overweight", who.int. Lollipops are coming under heightened scrutiny: a single 15-gram lollipop packs about 10 grams of sugar—roughly 2.5 teaspoons. This amount can account for 20% to 25% of a child's daily added-sugar limit. In response to these health concerns, there's a noticeable shift towards reformulating products with sugar-free alternatives like stevia, erythritol, and allulose. However, these substitutes come at a premium, costing 3 to 5 times more than traditional sucrose, which tightens profit margins for mainstream brands. Notably, 47% of candy purchasers are now on the lookout for healthier options. This shift has spurred interest in functional lollipops, those enriched with vitamins or probiotics. Yet, it's worth noting that while there's a market for these, regulatory bodies have been cautious, limiting health claim approvals.

Sugar taxes and tightening regulations

As of July 2024, at least 116 countries have implemented national excise taxes on sugar-sweetened beverages (SSBs), with 114 of them specifically targeting sugar-sweetened carbonated drinks, the most widely consumed type, according to the World Health Organization[3]Source: World Health Organization, “Global report on the use of sugar-sweetened beverage taxes,” who.int. Lithuania introduced a confectionery tax in 2026. Chile has adopted a broader strategy by requiring front-of-pack warning labels on high-sugar products and restricting advertisements directed at children. These measures aim to increase cognitive friction at the point of sale, thereby reducing impulse purchases. Venezuela mandates warning labels on products containing more than 10% added sugars, while several U.S. states are considering similar front-of-pack labeling requirements. The FDA has prioritized the removal of synthetic dyes from confectionery products. California's AB 2316 legislation bans Red Dye 3 and other additives in foods sold within the state, potentially setting a national precedent. These regulatory changes bring dual challenges: the cost of reformulating products (natural colorants are 50% to 100% more expensive than synthetic ones) and potential declines in sales volumes due to higher retail prices driven by taxes. Manufacturers are addressing these challenges by diversifying their product portfolios. In 2025, Ferrero launched its sugar-free 'Tic Tac Two' and 'Nutella Plant-based'. Similarly, YummyEarth introduced 'Sour Littles' and 'Duo Pops', marketed as organic and allergen-free. However, sugar-free lollipops face issues with taste and texture: erythritol can create a cooling effect, and allulose lacks the crystalline structure of sucrose, complicating the production of hard candies. Smart Sweets, tackling these challenges, replaced allulose with isomalto-oligosaccharides (IMO) in their formulation to enhance mouthfeel, highlighting the iterative process of reformulation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Soft Variants Gain Through Center-Fill Innovation

In 2025, hard lollipops, supported by their extended shelf life and the presence of well-established brands like Chupa Chups and Dum Dums, dominated the lollipop market, contributing 51.09% to its size. The industry's confidence in the sustained demand for hard lollipops is evident from recent capacity expansions, including a USD 97.7 million investment by Tootsie Roll in Tennessee and a USD 5 million investment by Spangler in Ohio. These established players experience heightened demand during Halloween, as the durable shells of hard lollipops withstand the rigors of bulk handling, making them a preferred choice for the season.

Conversely, soft and chewy lollipops are experiencing significant growth, with a compound annual growth rate (CAGR) of 7.28%. This growth is driven by advancements in center-fill depositing systems, which have significantly reduced changeover times to less than an hour, enabling the inclusion of creamy or fruit-jam fillings. Mid-scale producers are capitalizing on technologies such as GEA’s Aquarius FlexFormer and Suzhou Harmo’s one-shot moulding lines, which allow them to produce multiple stock-keeping units (SKUs) per shift without incurring substantial labor costs. Positioned as gentler alternatives suitable for young children and seniors, these soft variants command a 10-15% price premium. This premium not only enhances profitability but also provides additional margin opportunities as the lollipop market continues to mature and diversify.

By Category: Sugar-Free Acceleration Driven by Sweetener Innovation

In 2025, conventional sugar-based SKUs maintain a dominant 86.74% share of the lollipop market. This dominance is largely attributed to retailers' preference for affordable seasonal bag formats and the continued use of sucrose, which remains the most cost-effective crystallizing agent available. The affordability and widespread availability of sucrose make it a staple ingredient in conventional lollipops, ensuring its stronghold in the market. On the other hand, the sugar-free segment is experiencing significant growth, with a robust 7.45% CAGR. This growth is driven by advancements in erythritol and stevia technologies, which effectively replicate the sweetness of sugar while offering the added benefit of negligible calorie content. These innovations are reshaping consumer preferences and expanding the appeal of sugar-free lollipops.

Brands like Zolli Candy and YummyEarth, despite being priced at USD 1.50-2.00 per stick, double the cost of conventional lollipops, have successfully carved out a niche in pharmacies and health-food aisles. Their premium positioning is further bolstered by United States regulatory approvals for allulose, which provide an additional competitive advantage. However, the adoption of allulose comes with challenges, as its ingredient cost is 16-24 times higher than that of sucrose. To address these challenges and capture incremental market share, the lollipop industry is expected to intensify its research and development efforts. These efforts will likely focus on optimizing mouthfeel, managing production costs, and ensuring compliance with evolving regulatory standards.

By Flavor Profile: Sour Profiles Surge on Gen Z Demand

In 2025, fruity flavors continued to dominate the lollipop market, accounting for 46.02% of the total market share. Popular flavors such as strawberry, cherry, and grape remained consumer favorites, often associated with seasonal themes like Easter pastels and summer tropical assortments. Perfetti Van Melle capitalized on its economies of scale to maintain retail prices below USD 0.50 per unit, a critical strategy for catering to price-sensitive consumers in Asian markets.

On the other hand, sour and tangy flavor profiles experienced significant growth, registering a robust 7.11% CAGR. These flavors have gained popularity, particularly among Gen Z consumers, who favor bold and extreme taste experiences. In the United Kingdom, sour confectionery products grew 4.5 times faster than the overall confectionery category, now holding a notable 12% market share. The increasing mainstream appeal of sour flavors is evident through products like Mentos Sour Tones and Hershey’s acquisition of Sour Strips in 2024. Additionally, innovative layered flavor combinations, such as mango-chili-lime and raspberry-hibiscus-ginger, are transitioning from the beverage sector into the lollipop market. However, these high-acid formulations present a unique challenge, as they require more durable and costlier packaging solutions to ensure product integrity.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets are expected to contribute 42.33% of sales in 2025, primarily due to the popularity of bulk seasonal packs and the influence of checkout impulse purchases. In the U.K., Price-Marked Packs (PMPs) play a significant role, accounting for 62% of sugar confectionery sharing bags. This prevalence of PMPs reinforces consumer confidence in receiving value for their money.

Online retail is emerging as the fastest-growing channel, with a Compound Annual Growth Rate (CAGR) of 7.98%, surpassing all other distribution routes by 20 basis points. This growth is fueled by Direct-to-Consumer (DTC) brands capitalizing on subscription-based models and personalized gifting options. The trend is further validated by a 70% increase in e-commerce lollipop sales between 2021 and 2024. Although higher summer freight costs and the need for protective packaging add 15-20% to delivery expenses, the online channel compensates by acting as an experimental platform for niche flavors. These niche offerings, often overlooked by brick-and-mortar retailers, contribute to expanding the lollipop market's long-tail variety and cater to evolving consumer preferences.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 36.23% of the market value, driven by increasing disposable incomes and the confectionery sector's significant 33.4% share of snacking occasions in both China and India. Manufacturers in the region are leveraging Thailand's cost-effective production capabilities and benefiting from preferential ASEAN tariffs to enhance their export activities across Asia-Pacific. In Japan, consumer preferences lean heavily towards novelty products; for example, Chupa Chups' collaboration with New Era fashion has transformed their lollipops into lifestyle symbols. In India, the market is distinctly segmented, catering to both budget-conscious consumers with INR 20 value SKUs and urban consumers seeking premium organic options. However, infrastructure challenges, such as inadequate cold-chain systems in rural South Asia, continue to exacerbate spoilage rates. This has led brands to focus on producing more durable products like hard lollipops to mitigate losses.

Europe is experiencing robust growth, with the region projected to expand at the fastest rate, achieving a 7.68% CAGR through 2031. In the U.K., innovations in sour-flavored confectionery are driving sales, growing 4.5 times faster than the overall confectionery market. Post-pandemic recovery is evident in Italy and France, where convenience stores are witnessing a resurgence due to increased consumer mobility. Additionally, the European Union's stringent packaging regulations are accelerating the adoption of paper-based wrapping materials, providing early adopters with a competitive advantage in terms of brand reputation. Germany continues to dominate as a leading export hub, while Rotterdam serves as a critical re-export center, facilitating the movement of goods across Europe and beyond.

North America contributed an estimated 28-30% to the 2025 sales figures, reflecting the maturity of the lollipop market in the region, where household penetration is nearing saturation. Seasonal demand patterns significantly influence supply-chain planning and inventory management. Key domestic players, such as Tootsie Roll and Spangler, are expanding their production capacities to meet demand and mitigate risks associated with supply disruptions. In Latin America and the Middle East and Africa, these regions collectively represent a 15-18% market share. In 2024, the Middle East and Africa imported approximately 880,000 tonnes of confectionery, valued at USD 4.6 billion. The UAE plays a pivotal role as a re-export hub, channeling confectionery products into African markets. Furthermore, certifications such as Halal and Fairtrade are becoming increasingly important in these emerging markets, reflecting growing consumer demand for ethically and culturally aligned products.

Competitive Landscape

The lollipop market remains moderately fragmented, providing opportunities for smaller brands to establish unique positions through innovative flavors, clean-label initiatives, and localized strategies tailored to specific consumer preferences. Prominent players such as Perfetti Van Melle, Ferrero, and Tootsie Roll Industries leverage their well-established brand equity and expansive distribution networks to maintain a stronghold in the market. On the other hand, niche producers are gaining traction by offering premium and artisanal products, which are particularly appealing in rapidly urbanizing regions and the growing online retail segment.

With consumers increasingly prioritizing health and wellness, manufacturers are actively introducing healthier lollipop options to meet this demand. Regional companies, in particular, are focusing on launching health-oriented lollipops targeted at children. For example, in June 2025, Beekeeper’s Naturals launched its 'Kids’ Fiber Lollipops', designed to address the fiber deficiency affecting approximately 95% of children's diets. The company has established a significant presence in over 18,000 retail outlets, including major retailers such as Whole Foods, Target, Walmart, CVS, and Walgreens. Additionally, both local and global players are diversifying their product portfolios by shifting from traditional hard candies to center-filled or sugar-free variants. This strategic move aims to attract a broader consumer base while effectively addressing challenges posed by increasing sugar-related regulations.

Technological advancements are playing a transformative role in the lollipop industry, particularly in improving manufacturing efficiency and developing sustainable packaging solutions. Key differentiators in the market now include the adoption of automation, enhanced ingredient traceability, and the use of eco-friendly materials. These innovations align with regulatory requirements and cater to the evolving preferences of environmentally conscious consumers. Moreover, there is a growing emphasis on sugar-free alternatives, personalized gifting options, and direct-to-consumer (DTC) business models, which are reshaping the competitive landscape of the industry.

Lollipop Industry Leaders

-

Perfetti Van Melle Group B.V.

-

Tootsie Roll Industries, Inc.

-

Spangler Candy Company

-

Colombina S.A.

-

Ferrero International S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Glucovita introduced India's first glucose lollipop, supported by the 'Energy Ka Power Bank' campaign. Enriched with glucose and Vitamin C, this lollipop provides a quick energy boost for children, helping them manage their busy schedules of school, play, sports, and daily activities.

- April 2025: Bon Bon Bum launched its first U.S. campaign “Suck at Something,” partnering with Miami FC and rolling out bubblegum-filled lollipops nationwide via Amazon, Walmart, CVS, and TikTok Shop.

- March 2025: Mars Wrigley India introduced Boomer Lollipop, extending its iconic gum brand into the lollipop format through Indian retail and e-commerce channels.

- December 2024: Mondelez International explored the potential acquisition of Hershey Company, a move that could create a confectionery group with near-USD 50 billion in annual sales.

Global Lollipop Market Report Scope

A lollipop is A large, flat, rounded boiled sweet on the end of A stick. The lollipop market report is segmented by product type, category, flavor profile, distribution channel, and geography. By product type, the market is segmented into hard lollipops and soft/chewy lollipops. By category, the market is segmented into conventional and sugar-free. By flavor profile, the market is segmented into fruity flavored, sour and tangy, milk flavored, and chocolate flavored. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, specialty confectionery stores, online retail stores, and others. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. For each segment, the market forecasts are provided in terms of value (USD) and volume (Tons).

| Hard Lollipops |

| Soft/Chewy Lollipops |

| Conventional |

| Sugar-Free |

| Fruity Flavored |

| Sour and Tangy |

| Milk Flavored |

| Chocolate Flavored |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Specialty Confectionery Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hard Lollipops | |

| Soft/Chewy Lollipops | ||

| By Category | Conventional | |

| Sugar-Free | ||

| By Flavor Profile | Fruity Flavored | |

| Sour and Tangy | ||

| Milk Flavored | ||

| Chocolate Flavored | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty Confectionery Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the lollipop market expected to be by 2031?

The lollipop market size is projected to reach USD 5.58 billion by 2031, reflecting a CAGR of 6.78% from 2026-2031.

Which region is growing fastest for lollipops?

Europe leads growth at a projected 7.68% CAGR, propelled by sour-flavor innovation and premium positioning.

What share do hard lollipops hold?

Hard variants captured 51.09% of 2025 revenue, maintaining the largest slice of lollipop market share.

How quickly are sugar-free lollipops expanding?

Sugar-free formulations are advancing at a 7.45% CAGR, outpacing the overall category by 67 basis points.

Page last updated on: