DNA Repair Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

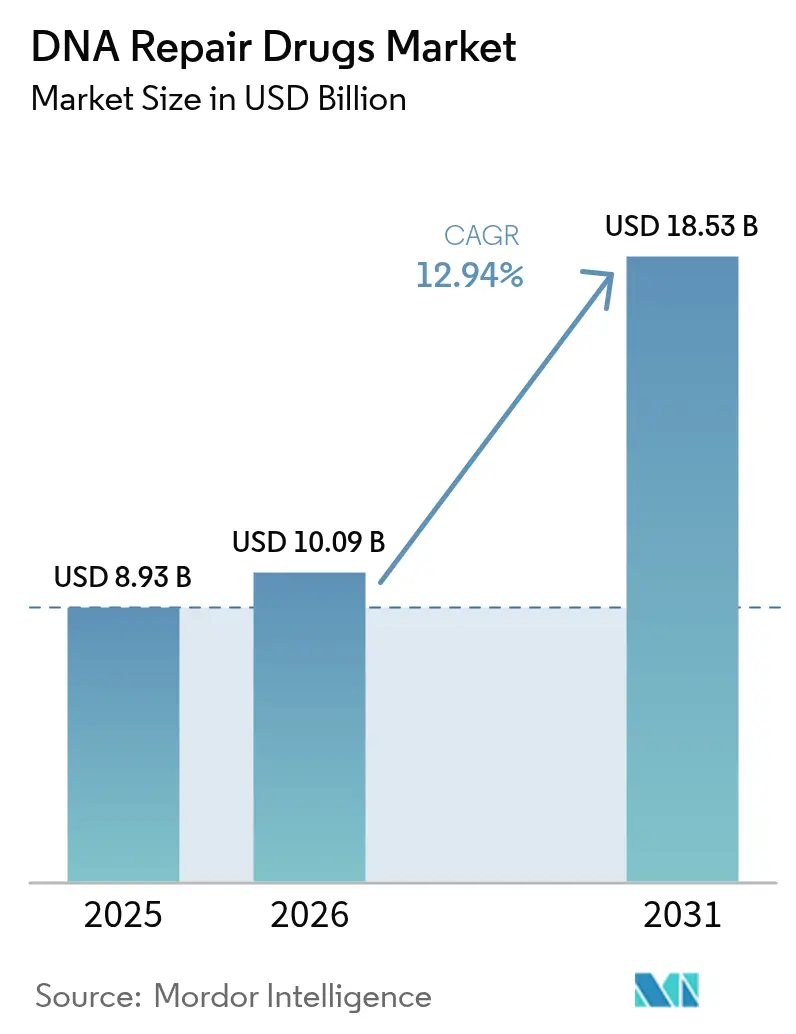

| Market Size (2026) | USD 10.09 Billion |

| Market Size (2031) | USD 18.53 Billion |

| Growth Rate (2026 - 2031) | 12.94% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DNA Repair Drugs Market Analysis by Mordor Intelligence

The DNA repair drugs market size is expected to grow from USD 8.93 billion in 2025 to USD 10.09 billion in 2026 and is forecast to reach USD 18.53 billion by 2031 at 12.94% CAGR over 2026-2031. Clinical success of poly(ADP-ribose) polymerase (PARP) inhibitors, rapid expansion of homologous-recombination-deficient (HRD) testing, and a shift toward oral oncolytics are sustaining double-digit growth. Pipeline diversification into ataxia telangiectasia mutated (ATM), ataxia telangiectasia and Rad3-related (ATR), and DNA-PK inhibitors is broadening the competitive field, while accelerated regulatory designations are shortening launch timelines by almost 2.5 years. First-line maintenance therapy is replacing later-line salvage use across several tumor types, lengthening average treatment duration and boosting per-patient revenue. North America remains the leading revenue contributor, yet Asia Pacific is scaling fastest on the back of government-backed precision-oncology programs that expand access to next-generation sequencing (NGS) and companion diagnostics.

Key Report Takeaways

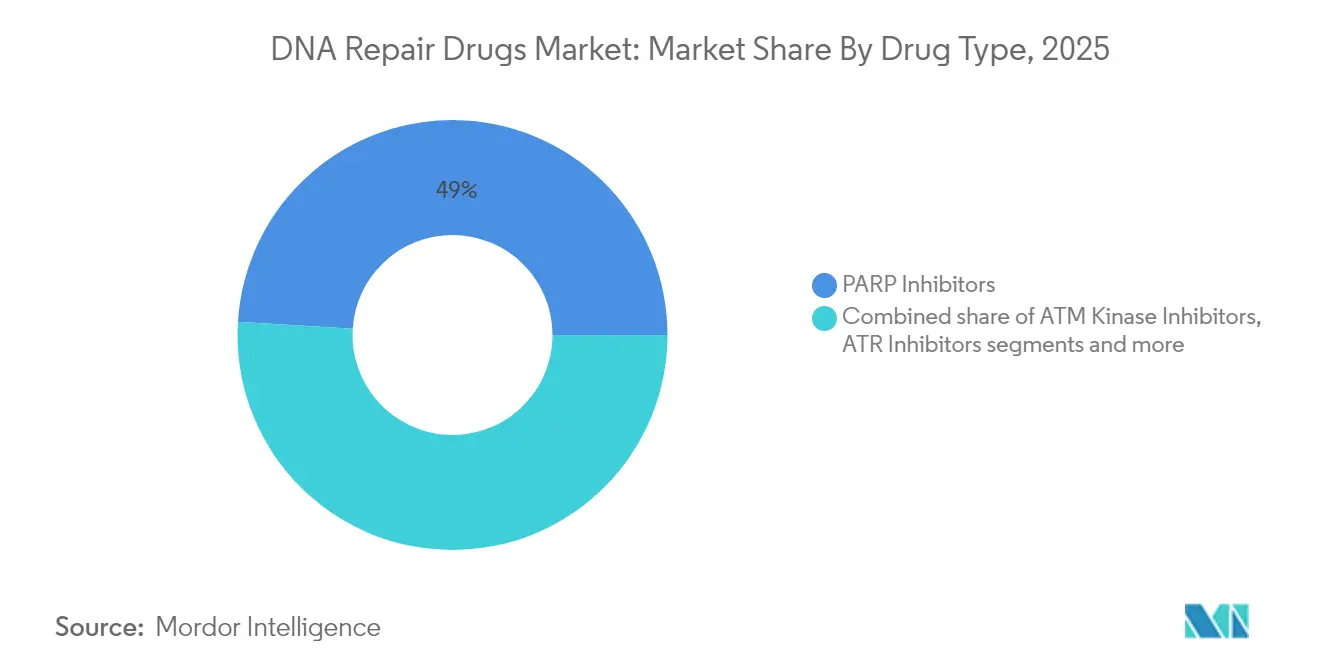

- By drug type, PARP inhibitors led with 49.02% of DNA repair drugs market share in 2025; ATM kinase inhibitors are forecast to post the fastest 18.92% CAGR to 2031.

- By indication, ovarian cancer accounted for 38.72% share of the DNA repair drugs market size in 2025, while prostate cancer is projected to expand at an 17.86% CAGR through 2031.

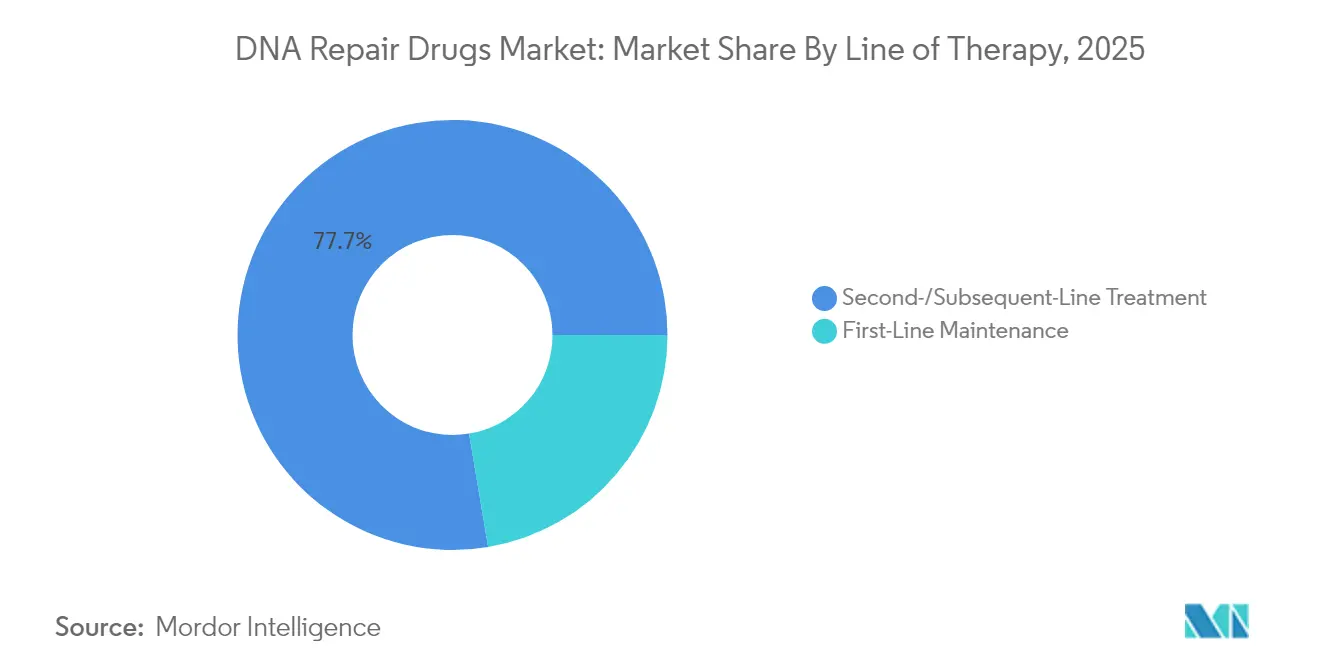

- By line of therapy, second-/subsequent-line treatment accounted for 77.65% share in 2025, yet first-line maintenance is projected to expand at a 17.24% CAGR across the forecast horizon.

- By distribution channel, hospital pharmacies captured 55.18% revenue share in 2025; specialty and retail pharmacies are set to grow fastest at a 15.12% CAGR to 2031.

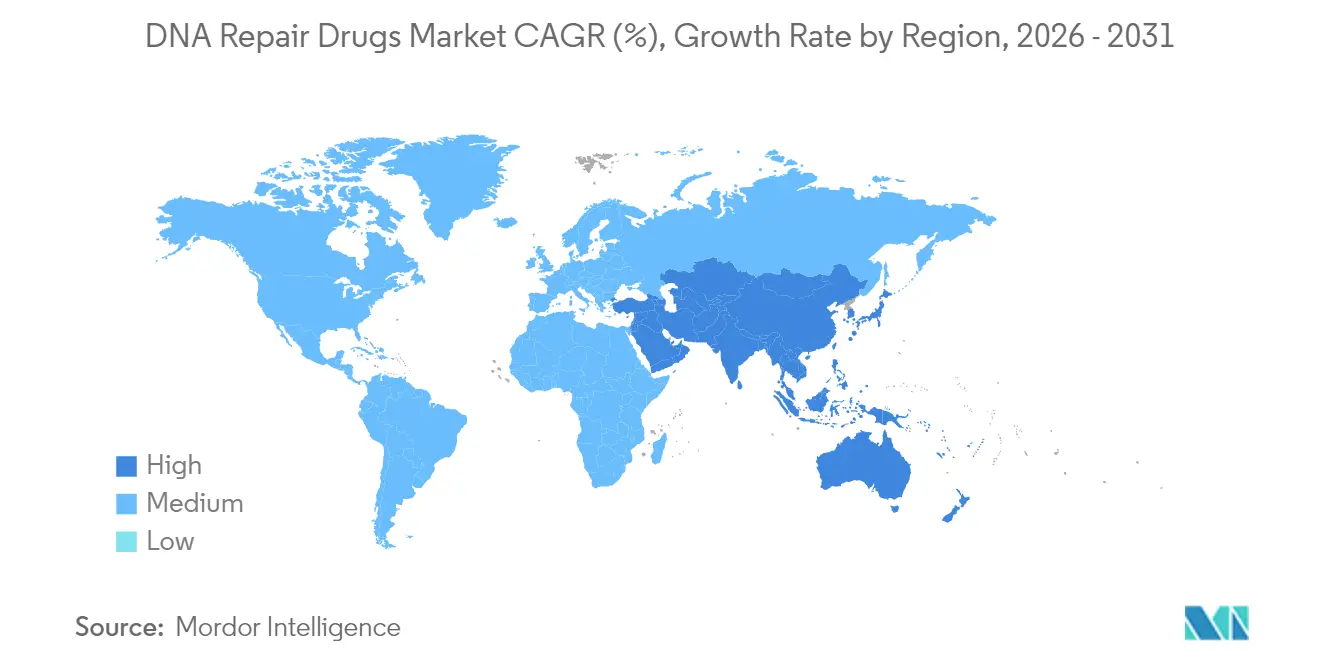

- By geography, North America held 47.35% share of the DNA repair drugs market size in 2025, whereas Asia Pacific is advancing at a 16.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global DNA Repair Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of HR-deficient solid tumors | +2.5% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Label expansion of PARP inhibitors into early-line & maintenance settings | +2.1% | Global, led by North America | Medium term (2–4 years) |

| Adoption of synthetic-lethality combination regimens | +1.8% | North America & Europe; emerging in Asia Pacific | Medium term (2–4 years) |

| Shift toward oral oncolytics in oncology formularies | +1.5% | Global, faster in developed markets | Short term (≤ 2 years) |

| Accelerated regulatory pathways shortening time-to-market | +1.3% | North America & Europe | Short term (≤ 2 years) |

| Public Precision-Oncology Initiatives Driving Companion-Dx Uptake | +1.0% | North America, Europe, and advanced Asian markets | Medium term (~ 3-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of HR-Deficient Solid Tumors

Expanding HRD testing is enlarging the treatable population for the DNA repair drugs market. Around 50% of high-grade serous ovarian tumors and up to 25% of prostate cancers harbor actionable DNA repair defects[1]H.H. Loong et al., “Recommendations for the use of next-generation sequencing in patients with metastatic cancer in the Asia-Pacific region,” ESMO Open, esmoopen.com. Integration of broad NGS panels into routine care, therefore, unlocks new patient pools and sustains prescription growth, especially where payer coverage is mature.

Label Expansion of PARP Inhibitors into Early-Line & Maintenance Settings

Front-line maintenance use is lengthening therapy duration by 10–12 months versus later-line use, as demonstrated in the PRIMA trial where niraparib yielded a 5-year progression-free survival (PFS) rate of 35% in HRD-positive ovarian cancer[2]D.M. Chase et al., “Niraparib as first-line maintenance therapy in patients with stage III ovarian cancer,” Oncol Ther, springer.com. Extended exposure drives higher cumulative sales and strengthens class incumbency.

Adoption of Synthetic-Lethality Combination Regimens

Combining ATR or ATM inhibitors with PARP agents produces synergistic effects that overcome resistance. In Merck’s DDRiver 301 study, ATR inhibitor tuvusertib plus niraparib improved PFS by roughly 35% over monotherapy, broadening eligibility beyond canonical HRD tumors[3]Merck Group, “Merck’s innovative oncology pipeline of DDR inhibitors,” merckgroup.com .

Shift Toward Oral Oncolytics in Oncology Formularies

Oral delivery aligns with outpatient models and specialty-pharmacy integration. A cross-sectional study published in February 2024, which analyzed data from 8 million patients, revealed that Medicare Part D fills for oral anticancer drugs through in-house pharmacies climbed from 10% in 2011 to 34% in 2019, boosting adherence and lowering point-of-sale costs by nearly 20%[4]P. Kakani et al., “Trends in integration between physician organizations and pharmacies,” JAMA Network Open, jamanetwork.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of HRD / BRCA testing limiting eligible patient pool | -1.80% | Global, most severe in emerging markets | Medium term (2–4 years) |

| Myelosuppression & MDS/AML safety signals capping therapy duration | -1.50% | Global | Medium term (2–4 years) |

| Escalating payer scrutiny on overall-survival benefit vs. standard chemotherapy | -1.20% | APAC emerging, Sub-Saharan Africa, parts of South America | Long term (≥ 4 years) |

| Patent cliff 2028–30 for first-wave PARP inhibitors | -0.90% | Global, strongest in price-sensitive markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost of HRD / BRCA Testing Limiting Eligible Patient Pool

Comprehensive genomic profiling costs USD 3,500–5,800 per patient, limiting test uptake to 47% of guideline-eligible ovarian-cancer cases in the United States. The affordability gap is wider in low- and middle-income regions, shrinking the real-world funnel of patients who can access targeted therapies.

Safety Signals—Myelosuppression & MDS/AML—Capping Duration of Therapy

Long-term PARP inhibitor exposure raises the incidence of myelodysplastic syndrome and acute myeloid leukemia, prompting regulators to withdraw certain late-line indications. Clinicians are therefore adopting time-limited regimens rather than continuous dosing, which tempers the total addressable duration per patient.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: ATM Kinase Inhibitors Gaining Momentum

PARP inhibitors retained 49.02% of the DNA repair drugs market share in 2025, underpinned by mature commercial footprints across ovarian, breast, and prostate cancers. The DNA repair drugs market size for this class is projected to expand steadily, although competitive intensity is rising. Momentum is shifting toward ATM kinase inhibitors, forecast to clock a 18.92% CAGR as lartesertib and other pipeline agents enter late-phase trials. Their appeal lies in activity against tumors harboring ATM loss, which encompasses 5–8% of prostate, pancreatic, and gastric cancers.

Early data show objective responses in tumors previously refractory to PARP therapy, positioning the segment as a resistance-management option. Manufacturers are layering ATM inhibitors into frontline trials, accelerating potential uptake. Continuous-dosing oral formulations further align with the health-system trend toward ambulatory oncology, bolstering channel penetration through specialty pharmacies. Collectively, pipeline depth suggests ATM inhibitors may erode the incumbent lead of PARP agents by 2030, when first-generation products face patent expiry.

By Indication: Prostate Cancer Emerges as Growth Leader

Ovarian cancer generated 38.72% of 2025 revenue because of entrenched PARP maintenance protocols and the highest prevalence of HRD. The DNA repair drugs market size attached to this indication remains robust, yet growth is moderating as penetration approaches saturation in developed markets. In contrast, prostate cancer is pacing the field with an 17.86% CAGR owing to compelling overall-survival gains with olaparib-abiraterone doublets that lifted median survival to 42.1 months.

Beyond metastatic castration-resistant prostate cancer, sponsors are now testing combinations in hormone-sensitive and localized settings, potentially quadrupling the eligible patient base. Heightened NGS adoption—spurred by APODDC guidelines—will further raise diagnostic capture rates across Asia Pacific, reinforcing demand growth. Simultaneously, pancreatic and colorectal cancers are moving up the opportunity curve as synthetic-lethal partners magnify PARP activity in tumors without BRCA mutations.

By Line of Therapy: First-Line Maintenance Accelerating

Second-/subsequent-line treatment accounted for the largest cohort in 2025, with 77.65% of market share, reflecting the historical placement of DNA repair agents after platinum exposure. However, first-line maintenance therapy is now the most dynamic slot, anticipated to grow at 17.24% during the forecast period, fuelled by evidence that niraparib doubles median PFS versus placebo in HRD-positive ovarian cancer patients. The extended course pushes cumulative dosing above 17 months on average, nearly tripling drug revenue per patient relative to salvage settings.

Payers are endorsing earlier use as biomarker-selected populations manifest durable benefit, though safety-related caps on total treatment duration could temper upside. Manufacturers are addressing this by designing intermittent-dose schedules and developing next-generation PARP1-selective molecules such as saruparib that promise reduced myelosuppression.

By Distribution Channel: Specialty Pharmacies Gaining Share

Hospital pharmacies still distribute 55.18% of prescriptions, reflecting embedded oncology infusion centers and integrated electronic medical records. Yet specialty and retail pharmacies are projected to climb at a 15.12% CAGR as the DNA repair drugs market pivots to oral dosing. Vertical integration between oncology practices and in-house pharmacies now encompasses more than half of U.S. medical oncologists, shrinking time-to-therapy initiation and raising adherence by 28%.

Online channels are layering on remote medication management tools, expanding reach to rural cohorts and international patients seeking early access. Value-based agreements are emerging, linking reimbursement to patient-reported outcomes and genomic confirmation of target engagement, which may shift economic risk from payers to manufacturers but accelerate formulary inclusion.

Geography Analysis

North America generated 47.35% of 2025 revenue, anchored by early regulatory approvals and payer coverage for HRD testing. Integrated health-system ownership of specialty pharmacies promotes seamless genomic test-to-treatment conversion, propelling steady volume growth. The region also hosts the highest density of combination trials exploring ATR-PARP and PARP-checkpoint inhibitor regimens, ensuring rapid uptake of future approvals.

Asia Pacific is the fastest-growing territory, advancing at 16.35% through 2031 as precision-oncology initiatives unlock pent-up demand. China’s 2025 approval of senaparib for first-line ovarian maintenance—based on the FLAMES Study—illustrates accelerating regulatory momentum. Japan and South Korea are updating reimbursement schedules to include multigene HRD panels, elevating test adoption rates above 60%. India and Southeast Asian markets remain underpenetrated but are trending upward as local contract research organizations bring cost-efficient trials to the region.

Europe holds the second-largest share and is expanding at a steady 12.21% CAGR. National reimbursement bodies increasingly mandate biomarker-driven frameworks, aligning with EMA favorable benefit-risk assessments for new DDR agents. South America and the Middle East and Africa are tracking 12.96% and 14.66% CAGRs, respectively, albeit from lower baselines. Multinational firms are piloting tiered-pricing strategies and public-private diagnostic partnerships to overcome affordability barriers. Expansion of tertiary oncology centers across Brazil, Saudi Arabia and the United Arab Emirates is expected to widen clinical trial participation, bolstering physician familiarity with DDR mechanisms.

Competitive Landscape

The DNA repair drugs market is moderately concentrated. AstraZeneca commands leadership through Lynparza, supported by its alliance with Merck that integrates global co-commercialization. Merck is diversifying beyond PARP with tuvusertib (ATR), lartesertib (ATM), and peposertib (DNA-PK), positioning the firm to offset parity pressure as first-generation patents expire in 2028.

Pipeline entrants emphasize selectivity and tolerability. AstraZeneca’s PARP1-selective saruparib reduced off-target hematologic toxicity in preclinical BRCA1/2 models while extending tumor-free intervals fourfold relative to olaparib. Artios Pharma and Ideaya Biosciences are advancing DNA polymerase theta and PARG inhibitors, respectively, to address PARP resistance.

As exclusivity cliffs near, first-wave agents will face biosimilar competition, likely compressing prices but widening access in cost-sensitive markets. Manufacturers are preparing by bundling companion diagnostics, investing in real-world evidence, and pivoting toward combination regimens that carry premium pricing levers.

DNA Repair Drugs Industry Leaders

AstraZeneca PLC

GlaxoSmithKline PLC

Merck KGaA

Pfizer Inc.

Valerio Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mabwell presented data showing its B7-H3 antibody-drug conjugate plus PARP inhibitors produced tumor regression in B7-H3-positive solid malignancies.

- April 2025: Laekna disclosed preclinical results for LAE122, a selective WRN inhibitor for MSI-H tumors, demonstrating favorable tolerability.

- January 2025: Impact Therapeutics received Chinese marketing authorization for senaparib as maintenance therapy for advanced ovarian cancer.

- November 2024: AstraZeneca and the Global Coalition for Adaptive Research agreed to test ATM inhibitor AZD1390 in newly diagnosed glioblastoma within the GBM AGILE platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the DNA repair drugs market as the global sales value of prescription therapeutics that deliberately inhibit or modulate cellular DNA-damage-response enzymes, most notably PARP, ATM, ATR, and DNA-PK, to exploit synthetic lethality in oncology and, in emerging trials, certain genetic disorders. According to Mordor Intelligence, the market baseline for 2025 stands at USD 8.93 billion.

Scope exclusions include investigational gene-editing tools, over-the-counter nutraceuticals, and manufacturing service revenues, which lie outside this valuation.

Segmentation Overview

- By Drug Type

- PARP Inhibitors

- ATM Kinase Inhibitors

- ATR Inhibitors

- DNA-PK Inhibitors

- Other Drug Types

- By Indication

- Ovarian Cancer

- Breast Cancer

- Prostate Cancer

- Pancreatic Cancer

- Glioblastoma & CNS Tumors

- Other Indications

- By Line of Therapy

- First-Line Maintenance

- Second-/Subsequent-Line Treatment

- By Distribution Channel

- Hospital Pharmacies

- Specialty & Retail Pharmacies

- Online Pharmacies

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed oncologists, hospital pharmacists, CRO scientists, and reimbursement advisors across North America, Europe, and Asia-Pacific. These conversations clarified real-world dosing volumes, emergent use in first-line prostate cancer, typical price erosion after year three on the market, and regional access barriers, letting us verify and fine-tune desk findings.

Desk Research

We began with peer-reviewed clinical journals such as The Lancet Oncology and Nature Reviews Drug Discovery, cancer registries from the WHO and SEER, and regulatory filings published by the US FDA and the European Medicines Agency. Trade associations like PhRMA, IQVIA institute dashboards, and customs shipment records were checked to profile the cross-border flow of leading PARP inhibitors. Company 10-Ks, investor decks, and trusted news feeds from Dow Jones Factiva complemented the public data. Finally, paid datasets, D&B Hoovers for manufacturer revenues and Questel for pipeline patent counts, anchored competitive intensity signals. This list is illustrative; many additional secondary sources informed granular checks.

Market-Sizing & Forecasting

A top-down model starts with regional cancer incidence pools, applies mutation-specific eligibility and treated-patient penetration, and multiplies by weighted annual treatment costs. Results are cross-checked through bottom-up supplier roll-ups of leading PARP inhibitor revenues and sampled average selling price multiplied by volume pulls from specialty pharmacies. Key drivers fed into a multivariate regression forecast include BRCA mutation testing rates, new regulatory approvals, generic entry timing, clinical pipeline success ratios, and oncology spend trends in high-growth Asia. Where bottom-up gaps appeared, we prorated using validated dose-intensity norms from primary interviews.

Data Validation & Update Cycle

Intermediate outputs undergo variance checks against independent import data and quarterly earnings. Senior analysts review anomalies, and we re-contact selected experts if swings exceed set thresholds. The model refreshes every twelve months, with mid-cycle updates triggered by major label expansions or pricing shocks before final sign-off.

Why Mordor's DNA Repair Drugs Baseline Earns Trust

Published market values routinely diverge because providers pick different therapeutic scopes, baseline years, and exchange-rate assumptions.

Our disciplined inclusion criteria, yearly refresh, and dual-path modeling help decision-makers rely on one transparent figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.93 bn (2025) | Mordor Intelligence | - |

| USD 6.80 bn (2023) | Global Consultancy A | Narrow scope excludes ATR and DNA-PK assets and uses static price points |

| USD 5.90 bn (2022) | Industry Journal B | Historical base year, no adjustment for 2023-25 approvals, conservative penetration rates |

In short, Mordor's model triangulates recent approvals, dynamic pricing, and mutation-led patient pools, producing a balanced baseline that clients can trace back to verifiable variables and reproducible steps.

Key Questions Answered in the Report

What is driving the rapid growth of the DNA repair drugs market?

Clinical validation of PARP inhibitors, expanding HRD testing, and strong pipeline progress in ATM, ATR and DNA-PK inhibitors are lifting the market at a 12.94% CAGR.

Which cancer type will add the most incremental revenue through 2031?

Prostate cancer, propelled by survival-boosting combinations such as olaparib plus abiraterone, is forecast to grow at an 17.86% CAGR and add the largest absolute revenue.

How are distribution channels evolving for DNA repair therapeutics?

Shifts toward oral formulations are pushing volume from hospital dispensaries to specialty and retail pharmacies, which are expected to rise at a 15.12% CAGR

What are the main obstacles to broader adoption in emerging markets?

High costs of HRD and BRCA testing and limited reimbursement coverage constrain patient identification and drug access in low- and middle-income regions.

Are safety concerns affecting long-term use of PARP inhibitors?

Yes. Rising incidences of myelosuppression and rare MDS/AML cases are prompting regulators and clinicians to cap treatment duration, especially in late-line settings.

Which novel mechanisms could reshape competition after first-generation PARP patents expire?

Highly selective PARP1 inhibitors, WRN helicase blockers, DNA polymerase theta inhibitors and DDR-based antibody-drug conjugates are poised to diversify therapeutic options and mitigate resistance.

Page last updated on: