Genitourinary Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.69 Billion |

| Market Size (2031) | USD 33.19 Billion |

| Growth Rate (2026 - 2031) | 1.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Genitourinary Drugs Market Analysis by Mordor Intelligence

genitourinary drugs market size in 2026 is estimated at USD 30.69 billion, growing from 2025 value of USD 30.21 billion with 2031 projections showing USD 33.19 billion, growing at 1.58% CAGR over 2026-2031. Ongoing demographic aging in high-income economies, rising diagnosis rates for prostate disorders and incontinence, and faster regulatory approvals for specialty therapeutics sustain demand even as volume growth remains muted. Companies protect revenues by shifting from expiring blockbusters to precision medicines, device–drug combinations, and long-acting formulations that justify premium pricing. Digital prescribing and telemedicine are broadening patient access and reshaping fulfillment economics, while innovation pipelines address unmet needs in bladder cancer, multidrug-resistant urinary tract infections, and hormone-related urological problems. Patent cliffs, antibiotic resistance, and therapy-compliance gaps temper the trajectory but do not alter the fundamental direction of the genitourinary drugs market.

Key Report Takeaways

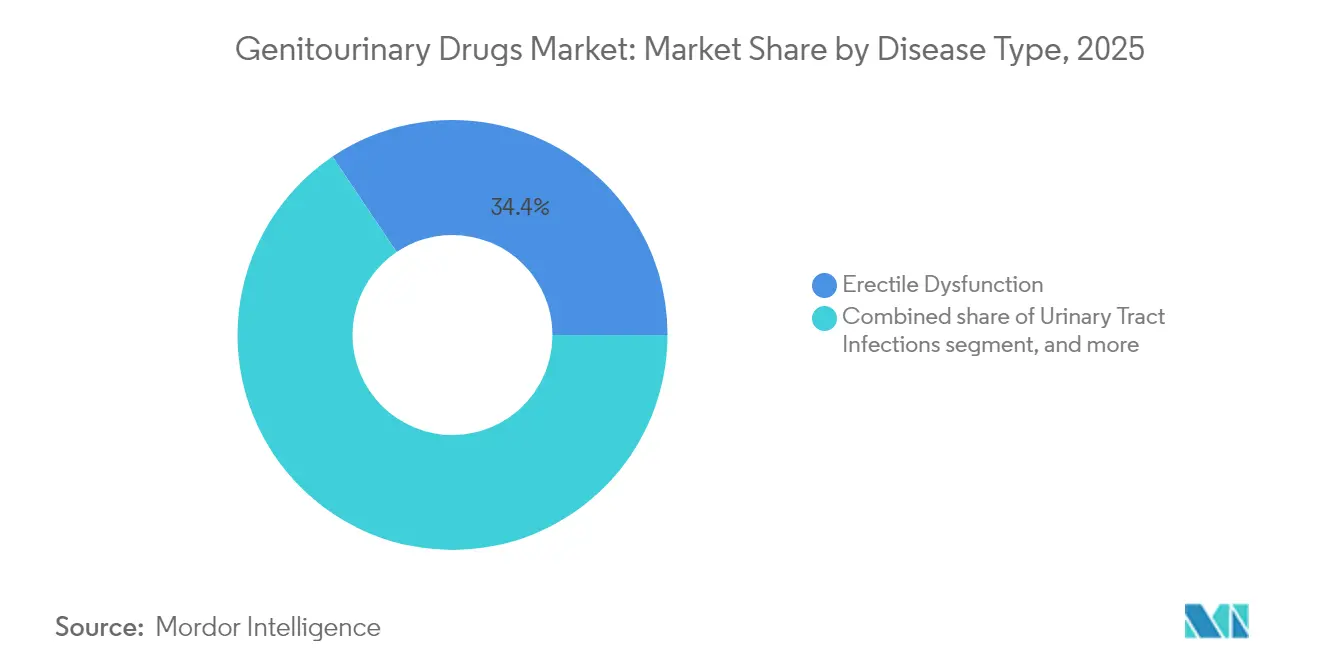

- By disease type, erectile dysfunction led with 34.42% of genitourinary drugs market share in 2025, while urinary incontinence is advancing at a 3.42% CAGR to 2031.

- By drug class, phosphodiesterase-5 inhibitors held 29.12% share of the genitourinary drugs market size in 2025; β-3 adrenergic agonists are expanding at a 3.6% CAGR through 2031.

- By route of administration, oral medicines accounted for 70.78% revenue share in 2025, whereas injectables are forecast to grow at 4.75% CAGR.

- By gender, male-focused therapeutics represented 55.26% of the genitourinary drugs market size in 2025, while female therapeutics are set to post a 4.55% CAGR.

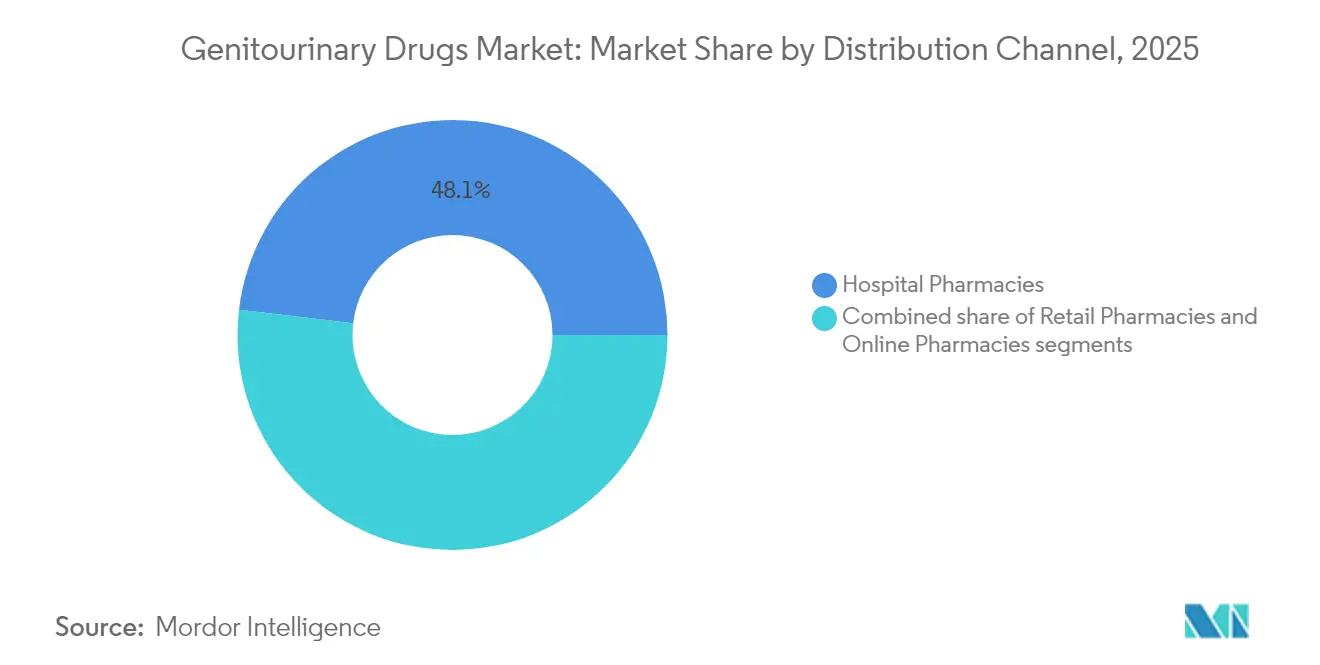

- By distribution channel, hospital pharmacies controlled 48.12% of 2025 revenues, but online pharmacies are rising at 4.14% CAGR.

- By molecule, small molecules commanded 58.21% share of the genitourinary drugs market in 2025; biologics and peptides are projected to rise at a 3.84% CAGR.

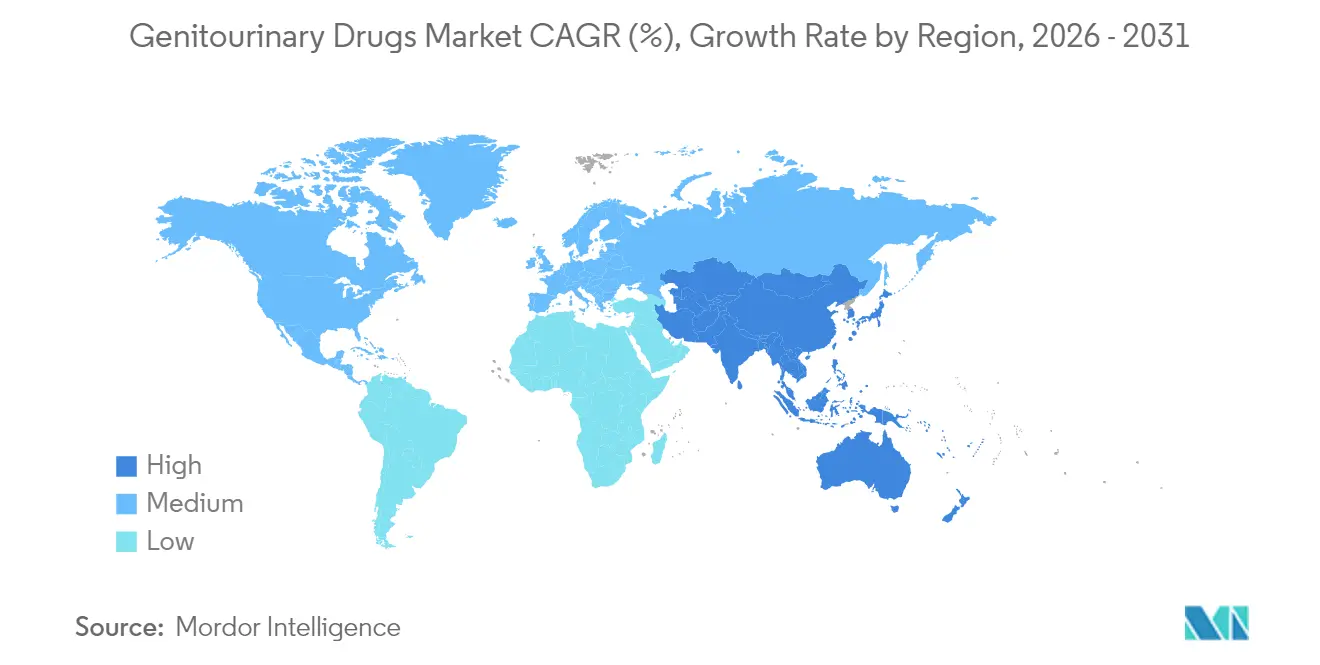

- By geography, North America held 42.10% of genitourinary drugs market share in 2025, whereas Asia-Pacific is the fastest-growing region at 2.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Genitourinary Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of genitourinary disorders | +0.4% | North America, Europe, Japan | Long term (≥ 4 years) |

| Growing aging male population with urological issues | +0.3% | North America, Europe | Long term (≥ 4 years) |

| Rising adoption of generic PDE5 inhibitors post patent expiry | +0.2% | Global, stronger in emerging markets | Medium term (2-4 years) |

| Expanding pipeline of novel genitourinary therapeutics | +0.3% | North America, Europe, spillover to APAC | Medium term (2-4 years) |

| Microbiome-modulating urotherapeutics entering clinical trials | +0.1% | Global, pilot programs in North America & Europe | Long term (≥ 4 years) |

| Telemedicine-based sexual-health platforms boosting prescription rates | +0.2% | North America, Europe, selected APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Genitourinary Disorders

Benign prostatic hyperplasia affects more than 50% of men aged 60–69 and up to 90% by age 85, prompting higher diagnostic and treatment rates. The FDA’s 2025 clearance of the Optilume BPH system illustrates how device-assisted interventions can improve maximum urinary flow from 7.9 mL/s to 16.4 mL/s while protecting sexual function. Urinary incontinence already impacts 25-45% of women over 65, fueling demand for β-3 adrenergic agonists that avoid anticholinergic side effects. The MyProstateScore 2.0 urine assay detects 94% of high-grade prostate cancers, reinforcing early-stage therapeutic demand[1]University of Michigan, “MyProstateScore 2.0 Clinical Validation,” umich.edu. Health systems increasingly classify genitourinary disorders as quality-of-life priorities, which strengthens reimbursement coverage and underpins the long-term resilience of the genitourinary drugs market.

Growing Aging Male Population with Urological Issues

Testosterone deficiency touches 20% of men over 60 and 50% above 80. In February 2025, the FDA revised testosterone labels to reflect the TRAVERSE trial, removing longstanding age-related hypogonadism warnings and easing prescriber concerns. Prostate cancer incidence doubles every decade after 50; Bayer’s Nubeqa treated nearly 100,000 patients in 2024 with an ultra-low PSA response of 42.6% versus 7.8% for placebo in the ARANOTE study. Longer lifespans coupled with higher expectations for sexual wellness elevate demand for erectile dysfunction therapies and related combination regimens, reinforcing the revenue base of the genitourinary drugs market.

Rising Adoption of Generic PDE5 Inhibitors Post Patent Expiry

Generic sildenafil captured more than 80% of major markets after Viagra’s loss of exclusivity, cutting average treatment costs and unlocking demand in price-sensitive economies. Similar dynamics shadow tadalafil as generic entries proliferate. Direct-to-consumer telehealth providers leverage these generics to offer discreet, low-cost programs that are resonating with younger cohorts. The model helped Hims & Hers exceed USD 1.48 billion in 2024 revenue. Formulation tweaks such as orally disintegrating tablets and rapid-onset films provide competitive differentiation beyond price, broadening therapeutic options in the genitourinary drugs market.

Expanding Pipeline of Novel Genitourinary Therapeutics

Johnson & Johnson’s TAR-200 intravesical gemcitabine system delivered an 82.4% complete response in BCG-unresponsive bladder cancer and received FDA Breakthrough Therapy Designation. GSK’s gepotidacin, branded Blujepa, became the first new oral antibiotic for urinary tract infections in three decades, maintaining potency against fluoroquinolone-resistant E. coli. UroGen Pharma’s UGN-102, with a June 2025 PDUFA date, targets a USD 5 billion bladder cancer opportunity. These advances point to durable innovation that offsets mature category erosion and fuels incremental value in the genitourinary drugs market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of therapy compliance | -0.2% | Global, more acute in low-resource settings | Short term (≤ 2 years) |

| Escalating antibiotic resistance in UTI pathogens | -0.3% | Global, higher where antibiotic stewardship is weak | Medium term (2-4 years) |

| Proliferation of counterfeit erectile-dysfunction drugs | -0.2% | Global, pronounced in unregulated online channels | Short term (≤ 2 years) |

| Emerging GLP-1-related sexual dysfunction confounding treatment uptake | -0.1% | North America, Europe, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack Of Therapy Compliance

Adherence rates range from 40–70% across genitourinary conditions. Overactive bladder drugs suffer from anticholinergic side effects that drive 50% discontinuation inside six months. Long-acting β-3 agonists such as vibegron offer better tolerability. Erectile dysfunction regimens face behavioral barriers tied to partner dynamics and performance anxiety. Telemedicine firms attempt to improve persistence through monthly refill services and ongoing counseling, but robust longitudinal data are still emerging. Digital reminders and implant-based delivery systems are under study to close the adherence gap and safeguard value leakage from the genitourinary drugs market.

Escalating Antibiotic Resistance In UTI Pathogens

E. coli resistance now tops 20% for trimethoprim-sulfamethoxazole and 10% for ciprofloxacin across multiple geographies. ESBL-producing organisms often require intravenous carbapenems, increasing costs and inpatient stays. The CDC links resistant UTIs to over 10,000 US hospitalizations each year[2]Nature Publishing Group, “Gepotidacin Overcomes Fluoroquinolone Resistance,” nature.com. Gepotidacin’s dual-target mechanism preserves efficacy against fluoroquinolone-resistant strains[3]Centers for Disease Control and Prevention, “Antibiotic Resistance Threats Report,” cdc.gov. Experimental bacteriophage and microbiome therapies are also in development. Until such solutions scale, resistance dampens treatment success rates and imposes additional stewardship constraints on the genitourinary drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Erectile Dysfunction Dominance Faces Incontinence Challenge

The genitourinary drugs market size for erectile dysfunction stood at a leading 34.42% share in 2025, benefiting from telemedicine penetration and generic PDE5 affordability. Yet growth is slowing as the segment approaches therapeutic saturation and faces emerging GLP-1-induced dysfunction complications. Urinary incontinence, with a 3.42% CAGR outlook, is narrowing the gap as aging populations and improved diagnosis accelerate demand for β-3 agonists and minimally invasive device–drug hybrids.

Urinary tract infection therapeutics retain stable revenue streams despite resistance issues, while prostate cancer drugs capture premium pricing through precision androgen-receptor targeting. Bladder cancer interventions such as TAR-200 demonstrate how localized delivery can redefine outcomes, drawing R&D investment toward high-risk, non-muscle-invasive disease niches. Together, these shifts recalibrate portfolio priorities within the genitourinary drugs market.

By Drug Class: PDE5 Inhibitors Lead Despite β-3 Agonist Innovation

Phosphodiesterase-5 inhibitors contributed 29.12% of genitourinary drugs market revenue in 2025, upheld by broad clinical familiarity and strong oral preference. Patent expiries, however, compress price points and spur a migration toward differentiated formulations and combination therapies. β-3 adrenergic agonists, growing at 3.6% CAGR, are winning share in overactive bladder by limiting anticholinergic adverse events.

Hormone therapies gain momentum after the FDA’s labeling clarification, while α-blocker/5α-reductase inhibitor fixed-dose regimens improve adherence. Neurokinin antagonists and microbiome-modulating agents populate early pipelines, highlighting diversification themes that support the long-term expansion of the genitourinary drugs market.

By Route Of Administration: Injectable Growth Challenges Oral Dominance

Oral products commanded 70.78% of 2025 revenue, anchored in erectile dysfunction, overactive bladder, and antimicrobial therapies. Convenience, privacy, and self-administration secure continued primacy. Nonetheless, injectables are forecast to post a 4.75% CAGR as depot testosterone, on-demand GnRH antagonists, and intravesical oncology products scale.

Johnson & Johnson’s TAR-200 underscores the therapeutic gain from localized, sustained drug exposure. Transdermal patches and topical gels add non-invasive options, whereas nanogel carriers from the University of Colorado promise higher tissue penetration. Collectively, these modalities extend choice and cement patient-centric care as a core differentiator in the genitourinary drugs market.

By Gender: Male Market Size Contrasts Female Growth Acceleration

Men accounted for 55.26% of 2025 sales, propelled by entrenched erectile dysfunction and prostate cancer lines that lend scale to the genitourinary drugs market size. Bayer’s Nubeqa blockbuster trajectory exemplifies the revenue heft of precision oncology. Women, however, are fueling the fastest category growth at 4.55% CAGR as industry focus finally addresses overactive bladder, recurrent UTIs, and menopausal urogenital atrophy.

Higher female UTI incidence—and new agents like gepotidacin—creates upside, as do hormone-based treatments that concurrently address vasomotor and genitourinary symptoms. Telehealth providers split service lines by gender, lowering access barriers and normalizing care-seeking, which will gradually rebalance the genitourinary drugs market.

By Distribution Channel: Hospital Pharmacies Lead as Online Surges

Hospital pharmacies retained 48.12% of 2025 turnover thanks to oncology infusions and controlled-distribution hormone therapies. Yet online pharmacies, rising at 4.14% CAGR, are redefining convenience and privacy for sensitive indications. Discrete packaging, auto-refills, and integrated teleconsultations reduce friction points and convert stigma-affected patients into consistent users.

Retail outlets face intensified margin pressure from generics and must compete on in-store clinical services. Regulatory harmonization around e-prescribing, especially in Europe and North America, will determine the extent to which digital channels cannibalize institutional dispensing within the genitourinary drugs market.

By Molecule Type: Small-Molecule Dominance Faces Biologics Innovation

Small molecules held 58.21% share of 2025 revenue due to cost-effective synthesis, oral bioavailability, and robust generic ecosystems. Genitourinary drugs market share leadership persists, but biologics and peptides are pacing at a 3.84% CAGR. Checkpoint inhibitors, antibody–drug conjugates, and depot peptide formulations meet complex urological needs that small molecules rarely solve.

Biosimilar pathways remain longer and costlier than generic filings, protecting originator economics for an extended period. At the same time, antibody-drug conjugates and engineered peptides blur category lines, indicating a future roadmap where precise targeting coexists with affordability imperatives in the genitourinary drugs market.

Geography Analysis

North America generated 42.10% of 2025 revenue, leveraging mature reimbursement systems and pioneering telehealth penetration. FDA fast-track pathways enable swift uptake of innovations such as TAR-200, and patient demand is reinforced by demographic aging and high prostate-cancer screening rates. Generic PDE5 erosion tempers pricing but expands volume, stabilizing overall regional growth for the genitourinary drugs market.

Asia-Pacific, advancing at 2.55% CAGR, benefits from expanding insurance coverage, urbanization, and policy reforms that shorten the regulatory lag behind Western approvals. China’s centralized procurement lowers costs yet enlarges access, while Japan’s super-aging society propels incontinence and BPH therapeutics. India’s generics expertise supplies both domestic and export demand, strengthening regional self-sufficiency. Although pricing pressure is intense, absolute patient volumes position the region as a long-run growth engine for the genitourinary drugs market.

Europe delivers consistent though slower expansion. EMA centralization simplifies submissions, and countries such as Germany sustain premium prices for novel agents like vibegron. Nonetheless, austerity measures in certain markets and fragmented national reimbursement rules complicate launch sequencing. Eastern Europe offers incremental upside as healthcare modernization aligns with EU standards. Brexit forces isolated UK filings, marginally raising costs but not altering demand fundamentals for the genitourinary drugs market.

Competitive Landscape

The competitive field shows moderate consolidation. Bayer, Johnson & Johnson, GSK, and AstraZeneca leverage deep pipelines and global footprints to hedge patent expiries. Bayer’s Q1 2025 report highlighted 81% Nubeqa sales growth and 89% Kerendia growth, offsetting Xarelto’s decline. Johnson & Johnson’s 82.4% TAR-200 response rate exemplifies breakthrough outcomes that command premium pricing. GSK’s Blujepa introduces a new antibiotic class after a 30-year drought, underscoring first-in-class advantage.

Strategic moves include Boston Scientific’s USD 3.7 billion Axonics acquisition, adding sacral neuromodulation expertise to manage incontinence. Ferring’s USD 500 million royalty deal spreads risk while securing prostate oncology upside. Generic challengers employ formulation innovation to stand out, and biosimilar entrants prepare to chip away at mature biologics. Digital alliances with telemedicine firms provide direct-to-consumer distribution muscles that traditional detailing cannot match. Overall, firms that combine innovative science with digitally enabled market access are positioned to outperform in the genitourinary drugs market.

Genitourinary Drugs Industry Leaders

Pfizer Inc.

Eli Lilly and Company

Bayer AG

Merck & Co., Inc.

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: UroGen Pharma released positive 18-month data for UGN-102 in recurrent low-grade bladder cancer ahead of the 13 June FDA PDUFA date, supporting a USD 5 billion opportunity.

- May 2025: Bayer announced Q1 2025 pharmaceutical revenue up 4.4%, propelled by Nubeqa and Kerendia growth.

- April 2025: Johnson & Johnson disclosed SunRISe-1 Phase 2b results, with TAR-200 achieving an 82.4% complete response in BCG-unresponsive bladder cancer.

- March 2025: FDA approved GSK’s gepotidacin (Blujepa) for uncomplicated UTIs, the first new oral class in nearly 30 years.

- March 2025: University of Colorado reported a nanogel platform that eliminated 90% of bacteria in recurrent-UTI models.

Global Genitourinary Drugs Market Report Scope

As per the scope of the report, genitourinary drugs are used to treat disorders affecting the kidneys, bladder, ureters, and urethra. Patients suffering from diseases and infections related to genitourinary systems have been depending on steroids and immunosuppressants, which are chemically synthesized and may reciprocate with severe side effects such as insomnia, acne, nausea, vomiting, and diarrhea.

The Genitourinary Drugs Market is Segmented by Disease Type (Erectile dysfunction, Gonorrhoea, Genital Herpes, Urinary Tract Infections, Urinary Incontinence, Glomerulonephritis, Chronic renal failure, Other Disease Types), Drug Type (Hormonal Therapy, Impotence Agents, Uterine Relaxants, Urinary Antispasmodics, Urinary pH Modifiers, Uterine Stimulants, Miscellaneous Genitourinary Tract Agents), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| Erectile Dysfunction |

| Urinary Tract Infections |

| Urinary Incontinence |

| Gonorrhoea |

| Genital Herpes |

| Glomerulonephritis |

| Chronic Renal Failure |

| Other Disease Types |

| Hormonal Therapy |

| Phosphodiesterase-5 Inhibitors |

| ?-Blockers & 5-? Reductase Inhibitors |

| Uterine Relaxants & Stimulants |

| Urinary Antispasmodics |

| Urinary pH Modifiers |

| Miscellaneous Genitourinary Agents |

| Oral |

| Injectable |

| Topical / Transdermal |

| Vaginal / Rectal Suppository |

| Male |

| Female |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Small-Molecule Drugs |

| Biologics & Peptides |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| APAC | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of APAC | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Disease Type | Erectile Dysfunction | |

| Urinary Tract Infections | ||

| Urinary Incontinence | ||

| Gonorrhoea | ||

| Genital Herpes | ||

| Glomerulonephritis | ||

| Chronic Renal Failure | ||

| Other Disease Types | ||

| By Drug Class | Hormonal Therapy | |

| Phosphodiesterase-5 Inhibitors | ||

| ?-Blockers & 5-? Reductase Inhibitors | ||

| Uterine Relaxants & Stimulants | ||

| Urinary Antispasmodics | ||

| Urinary pH Modifiers | ||

| Miscellaneous Genitourinary Agents | ||

| By Route Of Administration | Oral | |

| Injectable | ||

| Topical / Transdermal | ||

| Vaginal / Rectal Suppository | ||

| By Gender | Male | |

| Female | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Molecule Type | Small-Molecule Drugs | |

| Biologics & Peptides | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| APAC | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of APAC | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the genitourinary drugs market?

The market stands at USD 30.69 billion in 2026 and is projected to reach USD 33.19 billion by 2031.

Which disease area holds the largest share within the genitourinary drugs market?

Erectile dysfunction leads with 34.42% share in 2025, supported by widespread telehealth prescribing and generic PDE5 availability.

Which drug class is growing the fastest?

Β-3 adrenergic agonists for overactive bladder are expanding at a 3.6% CAGR through 2031.

How are online pharmacies influencing market growth?

Online pharmacies are forecast to grow at 4.14% CAGR by offering discreet, cost-effective access, particularly for erectile dysfunction and incontinence treatments.

Why is Asia-Pacific the fastest-growing region?

Healthcare reforms, large aging populations, and increasing insurance coverage drive a 2.55% CAGR across Asia-Pacific.

What novel therapies could reshape the market in the near term?

Johnson & Johnson’s TAR-200 for bladder cancer and GSK’s gepotidacin for antibiotic-resistant UTIs represent high-impact innovations expected to gain traction after 2025.

Page last updated on: