Injectable Anti-diabetic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

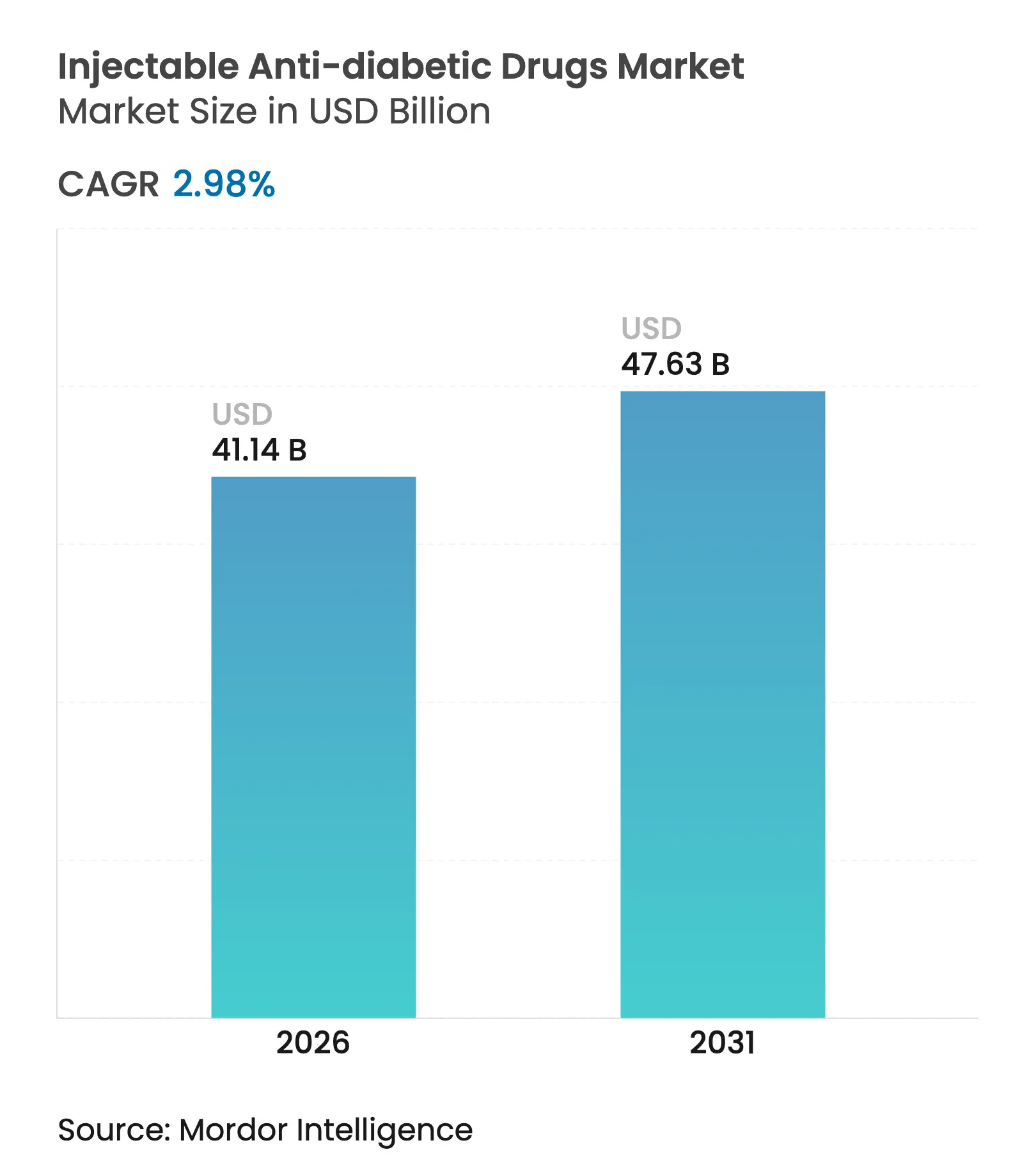

| Market Size (2026) | USD 41.14 Billion |

| Market Size (2031) | USD 47.63 Billion |

| Growth Rate (2026 - 2031) | 2.98 % CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

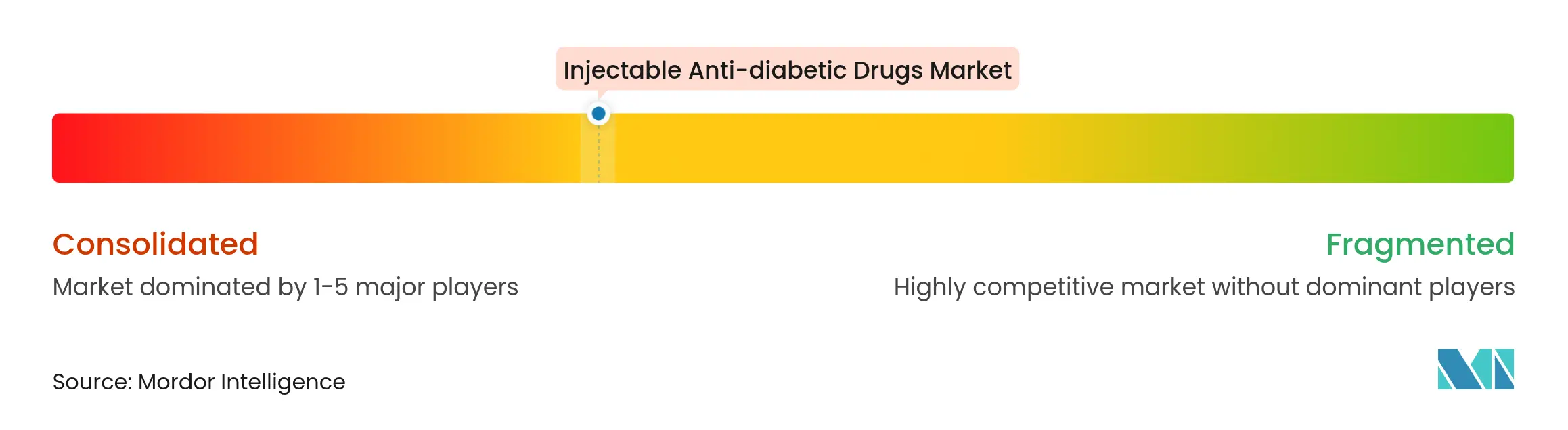

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Injectable Anti-diabetic Drugs Market Analysis by Mordor Intelligence

The injectable anti-diabetic drugs market size is expected to grow from USD 39.95 billion in 2025 to USD 41.14 billion in 2026 and is forecast to reach USD 47.63 billion by 2031 at 2.98% CAGR over 2026-2031. Moderate growth reflects a maturing landscape where next-generation GLP-1 receptor agonists chip away at long-standing insulin dominance, even as over 233 million people in China alone live with diabetes [1]Yu-Chang Zhou, "The national and provincial prevalence and non-fatal burdens of diabetes in China from 2005 to 2023 with projections of prevalence to 2050," Military Medical Research, mmrjournal.biomedcentral.com. Weekly dosing insulins, dual GIP/GLP-1 agonists and connected injectors improve adherence, yet high branded prices and lingering supply chain gaps curb volume-based expansion. Capital spending topping USD 12 billion across leading producers is alleviating prior capacity shortages, while localized manufacturing in India, Venezuela and Pakistan builds regional resilience. The shift toward value-based care, reinforced by Medicare coverage changes for anti-obesity injections, is reshaping treatment decisions toward outcomes and cost-effectiveness, encouraging payers to favor once-weekly regimens with proven cardiometabolic benefits.

Key Report Takeaways

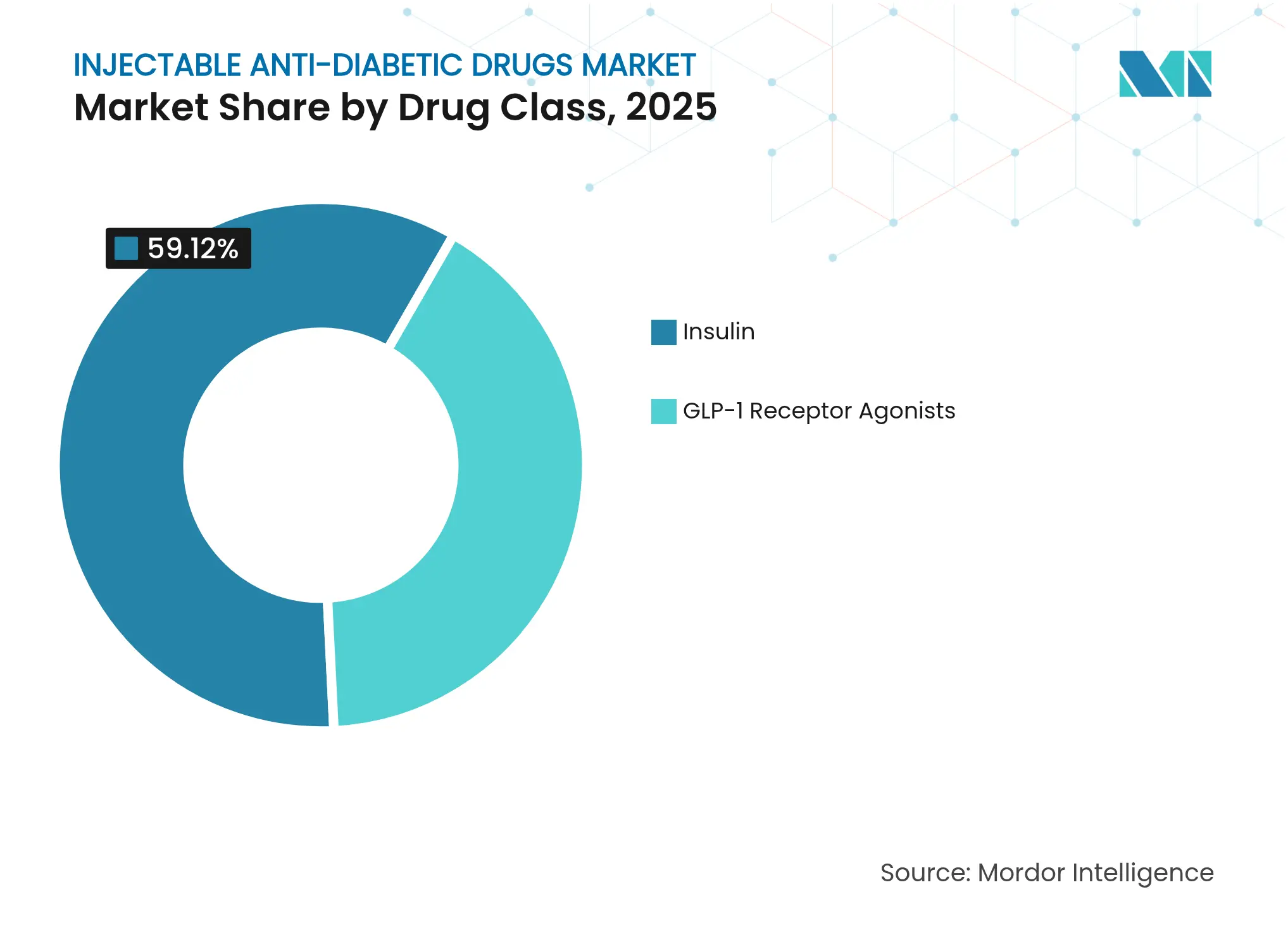

- By drug class, insulin preserved leadership with 59.12% of injectable anti-diabetic drugs market share in 2025; GLP-1 receptor agonists represent the fastest growth at a 3.74% CAGR through 2031.

- By diabetes type, Type-2 patients accounted for 80.05% of the injectable anti-diabetic drugs market size in 2025, while the Type-1 segment is expanding at a 3.79% CAGR to 2031.

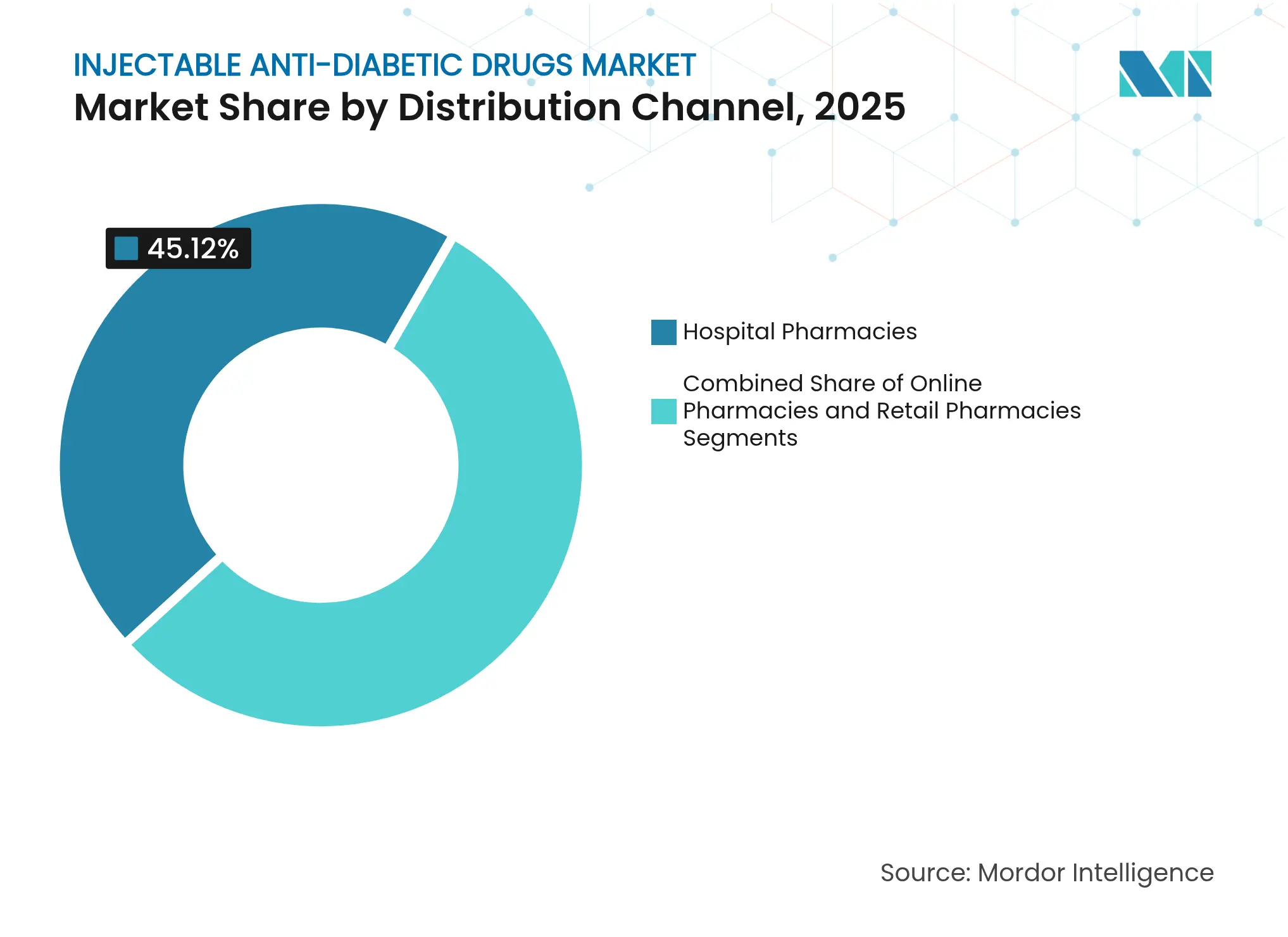

- By distribution channel, hospital pharmacies held 45.12% revenue share of the injectable anti-diabetic drugs market in 2025; online pharmacies post the highest 3.71% CAGR through 2031.

- By age group, adults dominated with 58.02% share of the injectable anti-diabetic drugs market size in 2025, but the geriatric cohort is growing at a 3.43% CAGR.

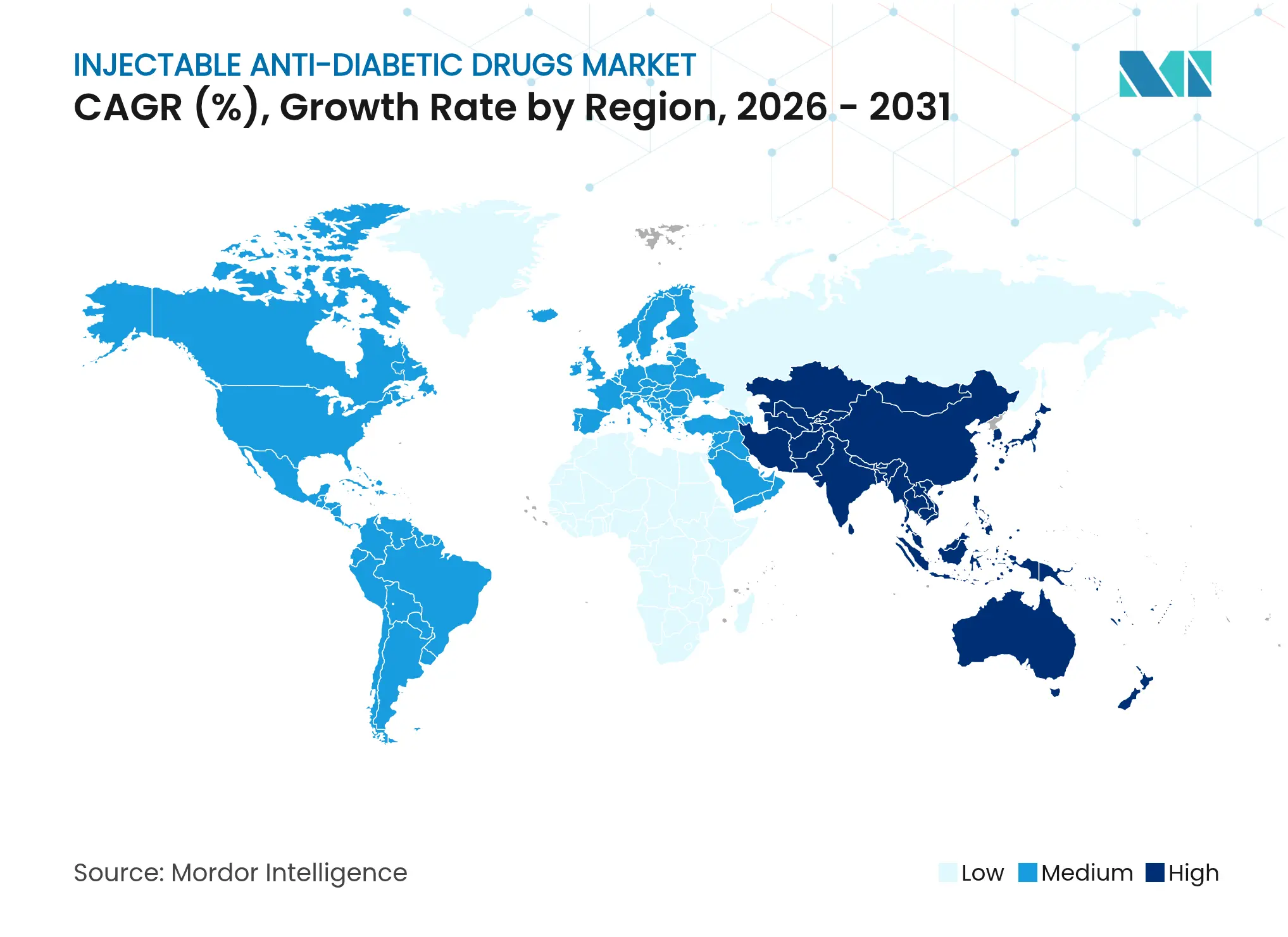

- By geography, North America led with 40.05% share in 2025, whereas Asia-Pacific is the fastest-advancing region at a 3.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Injectable Anti-diabetic Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Diabetes & Obesity Prevalence

Rising Diabetes & Obesity Prevalence

| +0.8% | Global, concentrated in Asia-Pacific and emerging markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+0.8%

|

Geographic Relevance

:

Global, concentrated in Asia-Pacific and emerging markets

|

Impact Timeline

:

Long term (≥ 4 years)

|

Launch Of Once-Weekly Injectable Therapies

Launch Of Once-Weekly Injectable Therapies

| +0.6% | OECD markets, expanding to emerging economies | Medium term (2-4 years) | |||

Favourable Reimbursement in OECD Markets

Favourable Reimbursement in OECD Markets

| +0.4% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) | |||

Dual GIP/GLP-1 Agonist Pipeline Momentum

Dual GIP/GLP-1 Agonist Pipeline Momentum

| +0.5% | Global, led by North America and Europe | Long term (≥ 4 years) | |||

On-Body Wearable/Connected Injector Adoption

On-Body Wearable/Connected Injector Adoption

| +0.3% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) | |||

Localised Insulin Manufacturing in EMs

Localised Insulin Manufacturing in EMs

| +0.4% | Asia-Pacific, Latin America, Middle East | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Diabetes & Obesity Prevalence

Global diabetes prevalence climbed from 6.1% in 2021 to a projected 9.8% by 2050, with 80% of patients living in developing countries. China already reports 233 million diabetics, equating to 15.88% of its population, and that figure could reach 29.1% by mid-century if trends persist. Regional phenotypes in Asia develop diabetes at lower BMI thresholds than Western peers, pushing demand for injectables at earlier disease stages. Southeast Asia alone is expected to see cases rise from 80 million to 151 million by 2045, underscoring sustained volume potential for the injectable anti-diabetic drugs market.

Launch of Once-Weekly Injectable Therapies

Insulin icodec’s approvals in the EU, Canada and Australia introduced a 196-hour half-life basal insulin that matches daily degludec efficacy while trimming injection frequency from seven to one [2]European Medicines Agency (EMA), "Awiqli," ema.europa.eu. Patient satisfaction scores improve, though Type-1 users register higher hypoglycemic episodes, highlighting the need for careful titration. Pipeline assets such as IcoSema and Eli Lilly’s efsitora alfa aim to blend basal insulin with semaglutide-like benefits, while triple-agonists under development promise broader metabolic control. These innovations widen therapeutic choice and spur switch-over growth within the injectable anti-diabetic drugs market.

Favourable Reimbursement in OECD Markets

Medicare rules effective in 2026 allow coverage of anti-obesity injections when prescribed for obesity alone, expanding beyond traditional diabetes indications [3]Federal Register, "Medicare and Medicaid Programs," federalregister.gov. Nevertheless, 83% of U.S. beneficiaries still face prior authorization for Wegovy, and 19 million adults retain no coverage for any GIP/GLP-1 agonist aimed at weight loss. Divergent state legislation creates patchwork access, but patient-assistance programs and pharmacy benefit moves to value-based contracts keep uptake momentum intact.

Dual GIP/GLP-1 Agonist Pipeline Momentum

Tirzepatide posted USD 1.8 billion in Q1-2024 sales, validating dual-target therapy and encouraging rivals. Candidates such as BGM0504 have shown up to 8.3% weight loss in early trials, and Novo Nordisk’s recent USD 2 billion triple-agonist acquisition positions it for next-generation competition. As multi-receptor approaches mature, injectable anti-diabetic drugs market participants anticipate broader cardiometabolic indications.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost of Branded GLP-1 Analogues

High Cost of Branded GLP-1 Analogues

| -0.7% | Global, acute in emerging markets and uninsured populations | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.7%

|

Geographic Relevance

:

Global, acute in emerging markets and uninsured

populations

|

Impact Timeline

:

Short term (≤ 2 years)

|

Cold-Chain & Last-Mile Logistics Gaps

Cold-Chain & Last-Mile Logistics Gaps

| -0.4% | Emerging markets, rural areas globally | Medium term (2-4 years) | |||

Supply Squeeze from Weight-Loss Off-Label Use

Supply Squeeze from Weight-Loss Off-Label Use

| -0.3% | North America, Europe | Short term (≤ 2 years) | |||

Shift Of R&D Capital Toward Oral/Gene Options

Shift Of R&D Capital Toward Oral/Gene Options

| -0.2% | Global, concentrated in developed markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Branded GLP-1 Analogues

GLP-1 receptor agonists list near USD 12,000 annually, creating affordability hurdles even where clinical benefits are clear. Competitive launches have raised rather than lowered prices, and meaningful reductions are unlikely until generics appear after 2031. Brazil is preparing for semaglutide copycats once patents lapse in 2026, while the United States has only just seen its first generic liraglutide approval. Until broader biosimilar penetration materializes, price sensitivity will temper volumes in price-elastic segments of the injectable anti-diabetic drugs market.

Cold-Chain & Last-Mile Logistics Gaps

Maintaining 2 °C–8 °C temperatures across distribution remains challenging in emerging markets where power stability and rural transport limitations raise spoilage risk. Industry investment in dedicated flights, serialization and data-loggers is reducing excursion losses, yet capital-light distributors may struggle to upgrade infrastructure quickly. Cold-chain weakness thus constrains full global reach for the injectable anti-diabetic drugs market, particularly for biologics with narrow thermal windows.

Segment Analysis

By Drug Class: GLP-1 Innovation Disrupts Insulin Dominance

Insulin retained 59.12% of injectable anti-diabetic drugs market share in 2025, reflecting its bedrock role in glycemic control. Revenue, however, advances gently as long-acting analogs cannibalize older human formulations and biosimilar competition spreads across emerging regions. Weekly insulin icodec’s rollout adds a premium niche that may slow volume but raise value. Ultra-rapid prandial insulins now carve share within post-meal management, yet they face overlap with incretin-based weight management options that reduce insulin dose requirements.

The GLP-1 receptor agonist segment represents the growth engine, expanding at 3.74% CAGR through 2031. Semaglutide and tirzepatide lead with strong weight-loss efficacy, driving dual diabetes-obesity adoption despite temporary supply shortages. Second-generation assets targeting multiple receptors aim to elevate efficacy while prolonging dosing intervals. As cardiovascular-label expansions arrive, GLP-1s evolve into broader metabolic solutions, amplifying their influence on the injectable anti-diabetic drugs market.

Note: Segment shares of all individual segments available upon report purchase

By Diabetes Type: Type-2 Prevalence Drives Volume Growth

Type-2 diabetes constituted 80.05% of the injectable anti-diabetic drugs market size in 2025, underlining the pandemic-like scale of adult-onset disease. Incremental prevalence gains and earlier initiation of injectables, especially GLP-1s, underpin volume stability. Automated basal-bolus dosing systems newly cleared for Type-2 users simplify regimens, encouraging uptake among tech-literate populations.

Type-1 diabetes, while smaller, grows marginally faster at 3.79% CAGR as pump-sensor ecosystems, weekly basal insulins and curative cell therapies pipeline create optimism. Clinical trials for islet cell replacement and gene-edited hypo-immune approaches suggest future disruption, yet near-term revenue stems from premium connected devices that extend the injectable anti-diabetic drugs market.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies captured 45.12% of 2025 revenue thanks to cold-chain infrastructure, bedside titration capabilities and integration with endocrinology services. Specialty units within hospital systems coordinate patient education, data capture and adherence for high-cost GLP-1 therapies.

Online pharmacies, however, post the quickest 3.71% CAGR as direct-to-consumer offerings widen access. Manufacturers leverage telemedicine portals, e-prescriptions and insulated parcel shipping to reach patients who seek discretion or convenience. Retail chains adjust through hybrid “click-and-collect” models, but squeezed margins and reimbursement complexity limit share expansion.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Geriatric Segment Drives Future Growth

Adults between 18 and 64 years held 58.02% share of the injectable anti-diabetic drugs market in 2025, reflecting peak incidence years. Employer health plans often cover once-weekly GLP-1s when comorbid obesity or cardiovascular risk is present, reinforcing adult consumption of premium injectables.

The geriatric population, growing at 3.43% CAGR, will underpin incremental gains as seniors live longer with diabetes and require simplified regimens. Medicare’s evolving coverage of anti-obesity treatments dovetails with once-weekly insulin approvals, supporting steady incremental adoption. Pediatric share remains small but benefits from miniaturized pens and new age-extension approvals.

Geography Analysis

North America retained 40.05% of revenue in 2025, bolstered by leading-edge launches, extensive insurance frameworks and domestic production expansion. Insulin icodec secured Health Canada approval ahead of anticipated U.S. entry, while the FDA green-lit automated dosing systems for Type-2 users, reflecting regulatory openness. Investment totaling over USD 9 billion across two states is doubling fill-finish capacity, yet payer scrutiny and prior authorizations dampen growth momentum.

Asia-Pacific is the fastest-growing region at a 3.72% CAGR, a trajectory driven by China’s 233 million diabetics and supportive policy in India that incentivizes local drug makers. Regional manufacturing collaborations, such as Novo Nordisk’s tie-up with Bio Farma in Indonesia, drive cost-down strategies and boost access. Unique phenotypic factors that ignite diabetes at lower BMI thresholds and the expansion of urban middle-income groups further catalyze demand across the injectable anti-diabetic drugs market.

Europe maintains stable expansion as biosimilar insulin approvals and EMA guideline updates foster competitive pricing and technological integration. Coordinated responses to GLP-1 shortages, including production scale-ups and discouragement of cosmetic off-label use, protect therapy availability. Investments by Sanofi and Novo Nordisk in continental facilities anchor supply chains, while emerging Latin American and Middle Eastern markets replicate Asia’s localization model to bridge affordability gaps.

Competitive Landscape

Market Concentration

Intensifying concentration defines the current injectable anti-diabetic drugs industry. Novo Nordisk’s USD 16.5 billion Catalent purchase secures critical fill-finish capacity, while its USD 2.2 billion Septerna tie-in accelerates oral peptide research. Eli Lilly counters with USD 870 million invested in Camurus delivery technology and over USD 5 billion in new U.S. manufacturing, extending its tirzepatide ramp-up. Collectively, these moves reinforce a duopoly holding more than 70% of global revenue.

Technology convergence shapes strategy as pharmaceutical leaders collaborate with device, biotech and digital companies. Vertex and TreeFrog explore cell-derived cures, whereas Ascendis partners with Novo Nordisk for once-monthly TransCon GLP-1 agents. FDA clearance of connected injectors and closed-loop systems positions device makers as critical ecosystem partners, merging software, sensors and biologics into integrated care platforms that expand the injectable anti-diabetic drugs market.

White-space competition centers on emerging markets where government incentives and patent cliffs open entry points. Indian generics firms gear up for semaglutide biosimilars post-2026, and local fill-finish hubs in Venezuela and Pakistan demonstrate technology-transfer models that sidestep earlier cold-chain frictions. Success will depend on meeting stringent biologic quality benchmarks while maintaining low cost structures.

Injectable Anti-diabetic Drugs Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Novo Nordisk acquired UBT251, a GLP-1/GIP/glucagon triple receptor agonist, for USD 2 billion, adding next-generation metabolic capability to its pipeline.

- December 2024: Eli Lilly unveiled a USD 3 billion expansion of its injectable drug plant, creating 750 jobs to support tirzepatide and related products.

- December 2024: FDA approved Hikma’s generic liraglutide injection, signaling the first biosimilar entry into the U.S. GLP-1 space.

- November 2024: Ascendis Pharma and Novo Nordisk agreed to develop a once-monthly GLP-1 receptor agonist using TransCon technology, with milestone payments up to USD 285 million.

Table of Contents for Injectable Anti-diabetic Drugs Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Diabetes & Obesity Prevalence

- 4.2.2Launch Of Once-Weekly Injectable Therapies

- 4.2.3Favourable Reimbursement in OECD Markets

- 4.2.4Dual GIP/GLP-1 Agonist Pipeline Momentum

- 4.2.5On-Body Wearable/Connected Injector Adoption

- 4.2.6Localised Insulin Manufacturing in Ems

- 4.3Market Restraints

- 4.3.1High Cost of Branded GLP-1 Analogues

- 4.3.2Cold-Chain & Last-Mile Logistics Gaps

- 4.3.3Supply Squeeze from Weight-Loss Off-Label Use

- 4.3.4Shift Of R&D Capital Toward Oral/Gene Options

- 4.4Regulatory Landscape

- 4.5Porters Five Forces Analysis

- 4.5.1Bargaining Power of Suppliers

- 4.5.2Bargaining Power of Buyers

- 4.5.3Threat of New Entrants

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Drug Class

- 5.1.1Insulin

- 5.1.1.1Basal/Long-acting

- 5.1.1.2Bolus/Fast-acting

- 5.1.1.3Traditional Human

- 5.1.1.4Combination

- 5.1.1.5Biosimilar

- 5.1.2GLP-1 Receptor Agonists

- 5.1.2.1Dulaglutide

- 5.1.2.2Exenatide

- 5.1.2.3Liraglutide

- 5.1.2.4Lixisenatide

- 5.1.2.5Semaglutide

- 5.2By DiabetesType

- 5.2.1Type-1 Diabetes

- 5.2.2Type-2 Diabetes

- 5.3By Distribution Channel

- 5.3.1Hospital Pharmacies

- 5.3.2Retail Pharmacies

- 5.3.3Online Pharmacies

- 5.4By Age Group

- 5.4.1Adults

- 5.4.2Geriatric

- 5.4.3Pediatric

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Novo Nordisk

- 6.3.2Eli Lilly

- 6.3.3Sanofi

- 6.3.4Biocon

- 6.3.5Pfizer

- 6.3.6Julphar

- 6.3.7AstraZeneca

- 6.3.8Amgen

- 6.3.9Amylin Pharma

- 6.3.10Zealand Pharma

- 6.3.11Boehringer Ingelheim

- 6.3.12Hanmi Pharmaceutical

- 6.3.13Tonghua Dongbao

- 6.3.14Gan & Lee

- 6.3.15Wockhardt

- 6.3.16Celltrion

- 6.3.17Ypsomed

- 6.3.18Insulet Corp

- 6.3.19Medtronic

- 6.3.20BD

- 6.3.21Hikma Pharma

- 6.3.22Mylan-Viatris

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Injectable Anti-diabetic Drugs Market Report Scope

Injectable anti-diabetic Drugs composed of GLP-1 receptor agonists are a type of non-insulin medication that is used in combination with diet and exercise to help treat type 2 diabetes and insulin. The injectable anti-diabetic drugs market is segmented into drugs (dulaglutide, exenatide, ligarglutide, lixisenatide, and semaglutide), brands (byetta, bydureon, victoza, trulicity, lyxumia, and ozempic), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and Latin America). The report offers the value (in USD) and volume (in units) for the above segments.