Sterile Injectable Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

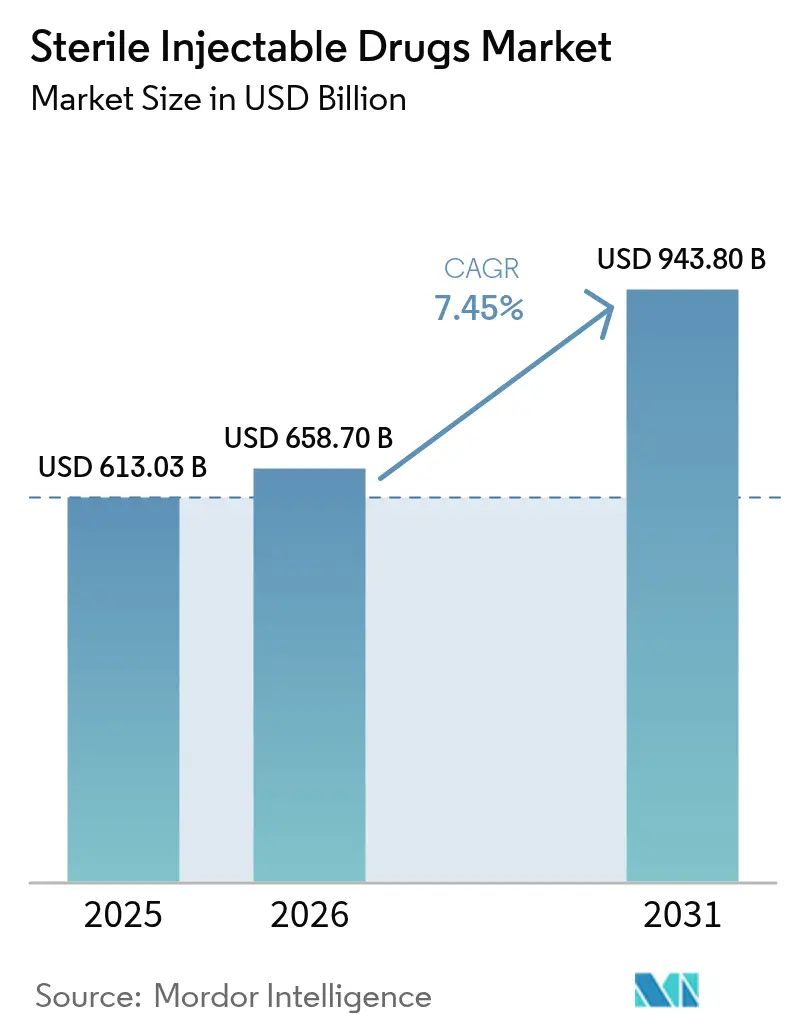

| Market Size (2026) | USD 658.70 Billion |

| Market Size (2031) | USD 943.80 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

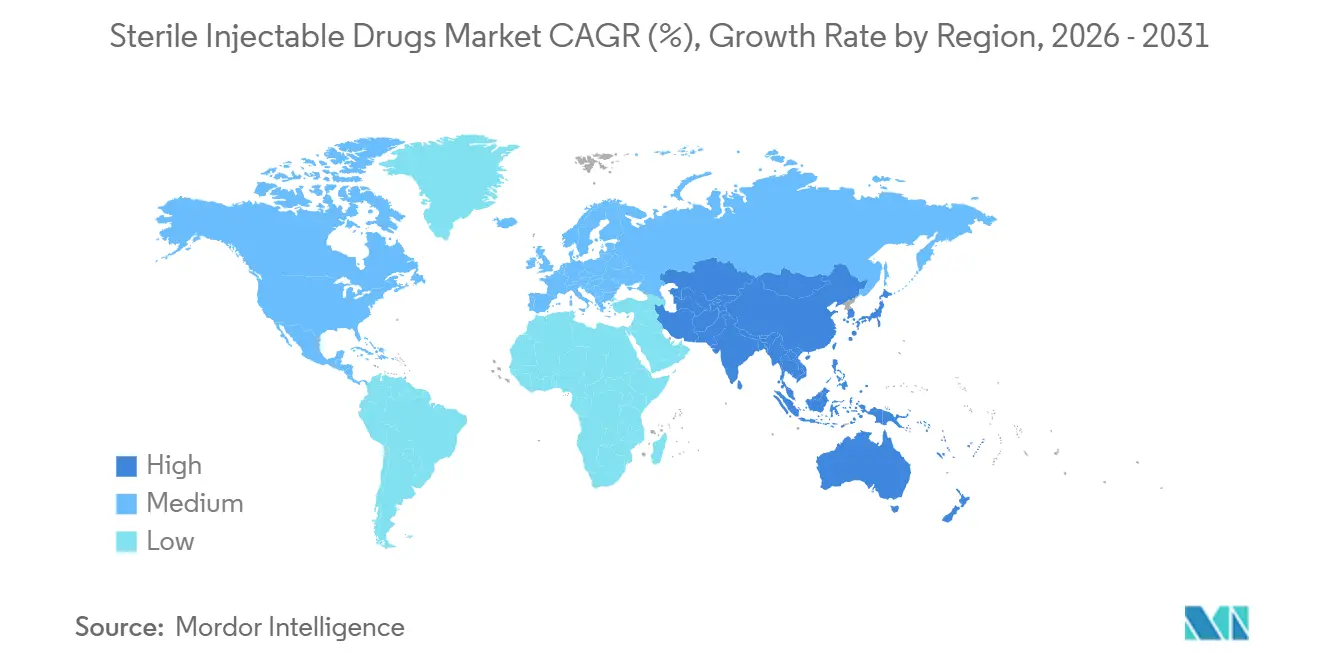

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterile Injectable Drugs Market Analysis by Mordor Intelligence

The Sterile Injectable Drugs Market size is projected to expand from USD 613.03 billion in 2025 and USD 658.70 billion in 2026 to USD 943.80 billion by 2031, registering a CAGR of 7.45% between 2026 to 2031.

The competitive focus tilts toward biologics, where large-molecule formats have scaled quickly on the back of oncology, autoimmune, and rare disease pipelines. At the same time, small molecules regain momentum through complex injectables and acute-care use cases. Monoclonal antibodies extend their lead due to new indications and biosimilar entry, which broaden access and accelerate adoption in community settings. Packaging and delivery are shifting toward ready-to-administer and home-use formats as hospitals prioritize error reduction and, when clinically appropriate, payers move therapies out of high-cost infusion sites. Regionally, North America has the most significant revenue base, while Asia-Pacific is advancing through capacity expansion and export-ready manufacturing that support regulated markets.

Key Report Takeaways

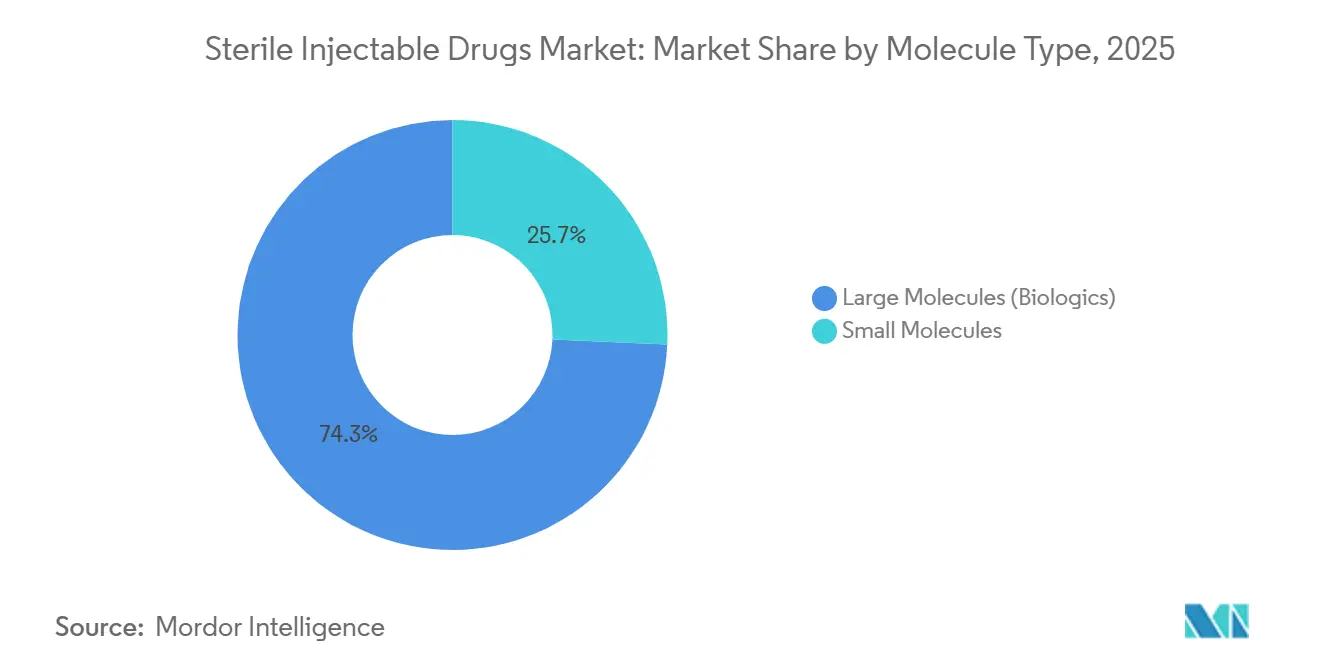

- By molecule type, large-molecule biologics led with 74.30% revenue share in 2025, while small molecules are projected to expand at an 8.30% CAGR through 2031.

- By drug class, monoclonal antibodies accounted for 38.00% of revenue in 2025 and are forecast to grow at an 8.00% CAGR through 2031.

- By application, oncology accounted for a 44.40% share in 2025, while neurology is set to record an 11.10% CAGR through 2031.

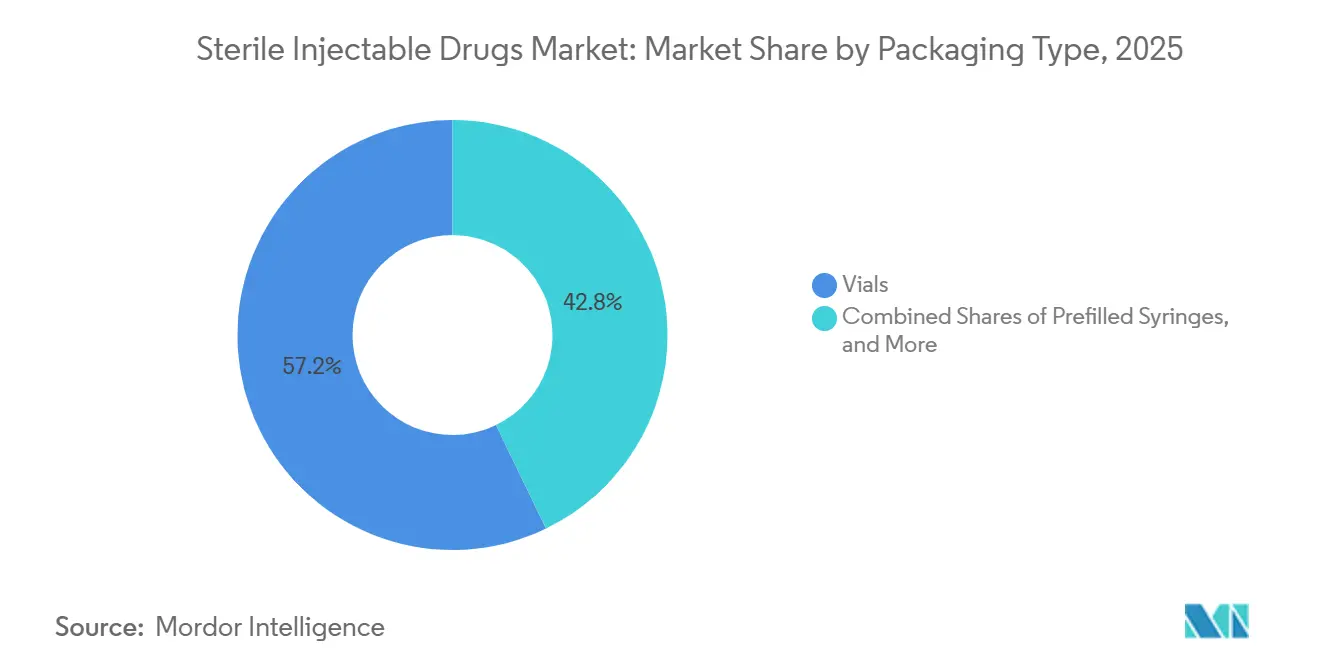

- By packaging type, vials held a 57.16% share in 2025, and prefilled syringes are expected to post a 9.60% CAGR to 2031.

- By route of administration, intravenous accounted for 63.20% of the 2025 volume, while subcutaneous is projected to grow at a 12.40% CAGR through 2031.

- By distribution channel, hospital pharmacies held 68.60% in 2025, while retail pharmacies are advancing at a 15.00% CAGR through 2031.

- By geography, North America captured 38.40% of the regional share in 2025, while Asia-Pacific is set to expand at an 8.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sterile Injectable Drugs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising R&D focus on biotechnology-engineered anti-cancer drugs | +1.2% | Global, with North America and Europe leading clinical-trial density | Medium term (2-4 years) |

| Rapid growth in pre-filled syringes for biologics | +0.9% | North America, Europe, and Japan; emerging adoption in urban China and India | Short term (≤ 2 years) |

| Increased outsourcing across the injectable value-chain | +1.1% | Global, with CDMO hubs in Asia-Pacific and Eastern Europe | Medium term (2-4 years) |

| Growing chronic-disease burden demanding parenteral therapies | +1.5% | Global, especially aging populations in OECD countries and rising diabetes prevalence in Asia-Pacific | Long term (≥ 4 years) |

| Closed-system robotics cutting contamination & batch failures | +0.8% | North America and Europe, with gradual diffusion to Asia-Pacific greenfield sites | Medium term (2-4 years) |

| Lyophilized nano-suspensions enabling room-temperature shipping | +0.7% | Emerging markets in Africa, Latin America, and Southeast Asia with limited cold-chain infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising R&D Focus on Biotechnology-Engineered Anti-Cancer Drugs

Pipeline investment in oncology biologics continues to reshape the injectable drugs market, with immuno-oncology and targeted modalities requiring parenteral delivery to reach therapeutic exposure. FDA approvals of novel cancer agents remained active in 2025, reflecting ongoing advances in antibody-drug conjugates and bispecifics that align with sterile fill-finish and high-containment operations.[1]U.S. Food and Drug Administration, “Biosimilar Product Information,” U.S. Food and Drug Administration, fda.gov

Pfizer’s acquisition of Seagen for USD 43 billion underscored the premium for ADC platforms and strengthened its larger oncology franchise, anchored in targeted parenteral therapies. Manufacturing strategies increasingly favor smaller batch sizes and higher potency, which drives demand for closed isolators and single-use systems to mitigate cross-contamination risks without lengthening validation timelines. The trend expands the addressable base for specialized CDMOs that combine conjugation chemistry and sterile packaging at commercial scale for sponsors navigating complex analytical comparability. FDA approvals of additional conjugate constructs through late 2024 signaled continued maturation of linker and payload innovation, pointing to sustained commercial launches over the next several years.[2]U.S. Food and Drug Administration, “Biosimilar Product Information,” U.S. Food and Drug Administration, fda.gov

Rapid Growth In Pre-Filled Syringes for Biologics

Prefilled platforms continue to displace vials as hospital systems and ambulatory providers reduce reconstitution steps and dosing errors while seeking to standardize administration at the bedside and in the home. Safety-engineered needles, connectivity features, and integrated autoinjector formats are improving usability and adherence for chronic biologic therapies. Regulators in the European Union and Japan emphasize extractables-and leachables controls for prefilled components, which extend development lead times but reinforce quality in real-world use. Device-data capture is creating feedback loops that support value-based reimbursement, as dose timing and persistence become measurable in routine care. In parallel, high-viscosity formulations with smaller volumes are expanding the scope of self-administration, making prefilled systems central to therapy delivery in the injectable drugs market.

Increased Outsourcing Across the Injectable Value-Chain

CDMOs are capturing a larger part of the fill-finish and lyophilization workload as sponsors opt for modular capacity without the burden of large capital projects. Catalent expanded lyophilization at its Bloomington, Indiana site to support biologics and next-wave modalities, and it secured multi-year programs that reflect sustained demand for end-to-end sterile services. Sponsors benefit from established regulatory track records with agencies such as the FDA, EMA, and PMDA, which can streamline pre-approval inspections and reduce the risk of launch delays. Leaders in biologics manufacturing add capacity in North America, Europe, and Asia, reinforcing global supply redundancy for high-value injectables. The outsourcing momentum is most visible among mid-sized biotechs that scale quickly on the back of positive clinical data. Still, even large pharmas are reshaping site networks to prioritize discovery and commercialization over legacy sterile operations.

Growing Chronic-Disease Burden Demanding Parenteral Therapies

Diabetes prevalence reached 537 million adults in 2025, with projections rising to 783 million by 2045, which sustains demand for insulins and incretin therapies commonly administered subcutaneously.[3]International Diabetes Federation, “IDF Diabetes Atlas 2025,” International Diabetes Federation, diabetesatlas.org

GLP-1 and dual-incretin therapies saw strong 2025 revenue contributions from Novo Nordisk and Eli Lilly, highlighting continued supply scaling and device optimization in self-administered formats. Acute settings maintain steady use of injectable anticoagulants and other cardiovascular agents as hospital caseloads for procedures and coronary events remain high. Autoimmune diseases are increasingly shifting toward subcutaneous biologics, which reduce the burden on infusion centers and enable consistent dosing at home for better persistence. The aging population, combined with the rising incidence of chronic conditions, underpins steady growth in ophthalmology, osteoporosis, and pain-management injectables that rely on parenteral routes for efficacy.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High expenses in sterile-inventory management | -0.6% | Global, with acute pressure in North America and Europe due to regulatory compliance costs | Short term (≤ 2 years) |

| Availability of alternative drug-delivery routes | -0.5% | North America and Europe, where oral and transdermal technologies are most advanced | Medium term (2-4 years) |

| Global shortage of pharma-grade vials & stoppers | -0.8% | Global, with bottlenecks concentrated in Asia-Pacific and Europe supply chains | Short term (≤ 2 years) |

| Tariff-driven volatility in sterile API import costs | -0.4% | North America and Europe importing from China and India; reverse impact on exporting nations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Expenses in Sterile-Inventory Management

Sterile inventory management elevates costs across warehousing, validated transport, and temperature monitoring, all of which must meet stringent compliance requirements. Just-in-time practices help reduce carrying costs but increase the risk of stockouts for small-volume orphan and oncology products subject to variable demand. Cold-chain investments are extending into last-mile delivery and home-based care, which increases the complexity of serialization and chain-of-custody controls for high-value biologics. Digital track-and-trace solutions offer better visibility but require data standards and interoperability that are still evolving across networks. Overall, these factors weigh on margins and complicate fulfillment strategies in the injectable drugs market, where sterility and temperature control are non-negotiable.

Availability of Alternative Drug-Delivery Routes

Oral technologies that feature permeation enhancers and nanoparticle carriers continue to expand into categories historically dominated by injectables, particularly in chronic conditions where ease of use matters. Transdermal systems for pain and hormone therapy deliver steady-state exposure and reduce the peaks and troughs associated with injections, which can improve patient satisfaction. Inhaled therapies have regained attention with modern devices, and mealtime control options such as inhaled insulin show the potential for faster onset in select cases. Pediatric and geriatric populations, where needle aversion and dexterity constraints are common, tend to prefer non-invasive routes when efficacy is equivalent. At the same time, many biologics still face bioavailability limits with oral and transdermal formats, so the core indications that require rapid onset and precise dosing continue to rely on parenteral delivery. The balance of convenience and clinical performance keeps competitive pressure on the injectable drugs market while preserving a firm role for injectables across acute and specialty care.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule Type: Biologics Dominance Masks Small-Molecule Revival

Large-molecule biologics held 74.30% of the injectable drugs market share in 2025, while small molecules are projected to grow faster at an 8.30% CAGR through 2031 as complex injectables see broader use. Small molecules benefit from shorter development cycles and lower capital intensity for sterile filtration and filling compared to mammalian cell culture and downstream purification. Biologics continue to command premium pricing due to clinical differentiation, but biosimilar entry is broadening access and accelerating formulary shifts. Many hospital-driven indications still rely on small-molecule injectables for rapid onset and predictable pharmacokinetics in critical care. Pipeline diversity across both categories ensures a two-speed market in which high-value biologics coexist with high-volume generics in hospital and retail channels.

By Drug Class: Monoclonal Antibodies Lead, Insulin Faces Disruption

Monoclonal antibodies accounted for 38.00% of the injectable drugs market share in 2025 and are set to grow at an 8.00% CAGR through 2031, driven by expanded adoption in oncology and immunology. Gene therapies have begun to displace routine prophylaxis in select hematology indications, including hemophilia A, where a one-time treatment has been approved. Peptide hormones maintain use in specialty endocrinology and fertility, while GLP-1 and dual-incretin agents reshape diabetes care pathways toward weight and cardiometabolic outcomes. Insulin use patterns are evolving as incretins take on a larger role in type 2 diabetes, with device and formulation innovation advancing on both fronts. Originators and biosimilar developers face an environment that rewards differentiated delivery, improved persistence, and a clear value proposition in outcomes.

By Application: Oncology Leads, Neurology Surges

Oncology accounted for 44.40% of revenue in 2025, driven by targeted biologics and combination regimens that rely on intravenous and subcutaneous routes for systemic exposure. Leading oncology agents are now available in neoadjuvant and adjuvant settings to improve event-free survival and reduce relapse, broadening the treatment-eligible population. Neurology advances at an 11.10% CAGR through 2031 as disease-modifying therapies in multiple sclerosis and new approaches in Alzheimer’s and migraine favor parenteral delivery for reliable central nervous system exposure. Cardiovascular care stabilizes demand with anticoagulants and other injectables tied to procedural settings and acute events.

By Packaging Type: Vials Hold, Prefilled Syringes Accelerate

Vials held 57.16% of the 2025 packaging share, based on their compounding flexibility and economics for multi-dose use in hospital pharmacies. Ready-to-use vials and standardized concentrations are gaining traction to reduce pharmacy workload and minimize contamination risk during preparation. Prefilled syringes are growing at a 9.60% CAGR to 2031 as manufacturers seek to reduce dosing steps and support self-administration without sacrificing dose accuracy. Cartridges and ampoules remain important in insulin, epinephrine, and anesthesia, where portability and reliability are vital.

By Route of Administration: Intravenous Dominates, Subcutaneous Climbs

Intravenous routes accounted for 63.20% of the administration volume in 2025, reflecting established clinical protocols in emergency medicine, surgery, oncology, and intensive care. The infrastructure built around infusion pumps, centers, and staffing creates inertia for incumbent IV formulations. Subcutaneous delivery is the fastest-growing route, with a 12.40% CAGR through 2031, enabled by high-concentration formulations and hyaluronidase co-formulations that expand the feasible dose volume. On-body injectors and spring- or motor-driven autoinjectors help patients manage chronic regimens at home without clinic visits.

By Distribution Channel: Hospital Pharmacies Lead, Retail Expands

Hospital pharmacies accounted for 68.60% of distribution in 2025 due to demand concentration in acute-care injectables, chemotherapy, and inpatient biologics requiring immediate clinical oversight. Group purchasing standardizes pricing and ensures supply continuity for formularies that manage high-volume classes such as antibiotics and anesthetics. Retail and specialty pharmacies are the fastest-growing segment, with a 15.00% CAGR to 2031, as payers shift care to the pharmacy for select biologics and expand home administration where clinically appropriate. Cold-chain support, patient education, and adherence programs are extending beyond specialty providers into broader retail networks.

Geography Analysis

North America captured 38.40% of the regional share in 2025, driven by higher per-capita spending, strong specialty uptake, and a favorable reimbursement environment for innovative injectables. United States utilization patterns and coverage for physician-administered products support the growth of originator and biosimilar products across oncology and immunology. Canada applies more restrictive health-technology assessments that lengthen time-to-access for new therapies, while still enabling meaningful biosimilar uptake province by province. Mexico’s hospital investments and expanded coverage continue to broaden access to sterile injectables across essential therapeutic categories.

Europe maintains the second-largest share with coordinated pathways that enable biosimilar entry, competitive tendering, and broad patient access over time. EMA’s experience with biosimilars has helped normalize switching and price competition in oncology and immunology classes. Asia-Pacific is forecast to grow at an 8.03% CAGR through 2031, driven by capacity build-outs and export-oriented manufacturing that feed regulated markets. India and China expand fermentation and fill-finish capabilities to support CDMO contracts and local access to oncology and chronic therapies.

Japan’s aging demographic sustains high biologics use, although conservative prescribing and longer review timelines slow adoption of novel classes. The Middle East and Africa, including GCC countries, invest in local manufacturing and hospital capacity to reduce import dependency and improve supply resilience. South America sees concentration in Brazil and Argentina, with public procurement emphasizing vaccines and essential antimicrobials and evolving pathways for specialty biologics. Across regions, policy and procurement structures shape price and access, yet the global pipeline and manufacturing investments continue to support steady adoption in the injectable drugs market.

Competitive Landscape

The injectable drugs market shows moderate consolidation, with the top 10 companies holding a majority share in 2025, while a large tail of generics, biosimilar entrants, and CDMOs compete on cost, speed, and flexibility. Innovators are adding or securing fill-finish capacity and investing in process analytics for more consistent quality and real-time release. CDMOs expand lyophilization, high-speed filling, and conjugation to support both emerging biotechs and large pharma, anchoring global redundancy for high-value sterile products. Biosimilar competition remains strong in monoclonal antibodies and other classes, supported by maturing regulatory frameworks and broader payer acceptance in major markets.

Signature moves define the current cycle. Pfizer acquired Seagen to deepen its antibody-drug conjugate capabilities and integrate linker technology into a broader oncology portfolio. Halozyme’s enzyme-enabled subcutaneous platforms enable large-volume dosing and expand self-administration options for biologics traditionally confined to infusion suites. Leading device and component suppliers are prioritizing safety-engineered and connected platforms to enhance usability and support adherence tracking. Quality remains a key competitive differentiator, as manufacturing observations and enforcement actions can disrupt market supply and open windows for competitors.

Sterile Injectable Drugs Industry Leaders

Novo Nordisk A/S

Amgen Inc.

Gilead Sciences Inc.

GSK plc

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: PAI Pharma has strategically acquired California-based Nivagen Pharmaceutical, including its portfolio of ready-to-use (RTU) sterile injectables, to enhance its injectable drug production capabilities. This acquisition reflects PAI's strategic evolution and commitment to strengthening domestic pharmaceutical manufacturing.

- January 2026: Eli Lilly announced a USD 5.3 billion investment to expand manufacturing capacity for tirzepatide in North Carolina, adding robotic aseptic processing and new fill-finish lines to serve expected growth.

- September 2025: Apiject Systems, Corp. has announced the submission of its New Drug Application (NDA) to the Food and Drug Administration (FDA) for the world's first injectable medicine, leveraging Apiject's proprietary single-dose, single-use prefilled plastic syringe technology.

Global Sterile Injectable Drugs Market Report Scope

As per the scope of the report, sterile injectable drugs are introduced into the body with a syringe and needle. These drugs are used to treat various diseases and disorders. The sterile injectable drugs market is gaining importance in hospitals and clinics, with an increasing number of biologics, antibody-drug conjugates, and monoclonal antibodies in development, as well as several injectable drugs in clinical trials globally.

The sterile injectable drugs market is segmented by molecule type, drug class, application, packaging type, route of administration, distribution channel, and geography. By molecule type, the market is segmented into small molecules and large molecules. By drug class, the market is segmented into blood factors, cytokines, peptide hormones, immunoglobulin, monoclonal antibodies (mAbs), insulin, and other drug classes. By application, the market is segmented into oncology, neurology, cardiovascular diseases, autoimmune diseases, infectious diseases, pain, and other applications. By packaging type, the market is segmented into vials (RTU/bulk), prefilled syringes, cartridges & ampoules, and ready-to-use blow-fill-seal containers. By route of administration, the market is segmented into intravenous (IV), subcutaneous (SC), intramuscular (IM), and intravitreal /other specialty routes. By distribution channel, the market is segmented into hospital pharmacies and retail pharmacies. and online & specialty pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Small Molecule |

| Large Molecule (Biologics) |

| Blood Factors |

| Cytokines |

| Peptide Hormones |

| Immunoglobulins |

| Monoclonal Antibodies (mAbs) |

| Insulin |

| Other Classes |

| Oncology |

| Neurology |

| Cardiovascular Diseases |

| Autoimmune Diseases |

| Infectious Diseases |

| Pain Management |

| Other Applications |

| Vials (RTU/Bulk) |

| Prefilled Syringes |

| Cartridges & Ampoules |

| Ready-to-Use Blow-Fill-Seal Containers |

| Intravenous (IV) |

| Subcutaneous (SC) |

| Intramuscular (IM) |

| Intravitreal / Other Specialty Routes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online & Specialty Pharmacies |

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Molecule Type | Small Molecule | ||

| Large Molecule (Biologics) | |||

| By Drug Class | Blood Factors | ||

| Cytokines | |||

| Peptide Hormones | |||

| Immunoglobulins | |||

| Monoclonal Antibodies (mAbs) | |||

| Insulin | |||

| Other Classes | |||

| By Application | Oncology | ||

| Neurology | |||

| Cardiovascular Diseases | |||

| Autoimmune Diseases | |||

| Infectious Diseases | |||

| Pain Management | |||

| Other Applications | |||

| By Packaging Type | Vials (RTU/Bulk) | ||

| Prefilled Syringes | |||

| Cartridges & Ampoules | |||

| Ready-to-Use Blow-Fill-Seal Containers | |||

| By Route of Administration | Intravenous (IV) | ||

| Subcutaneous (SC) | |||

| Intramuscular (IM) | |||

| Intravitreal / Other Specialty Routes | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online & Specialty Pharmacies | |||

| By Geography | By Geography | North America | United States |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the injectable drugs market size in 2026 and its 2031 outlook?

The injectable drugs market size is USD 658.70 billion in 2026 and is projected to reach USD 943.45 billion by 2031 at a 7.45% CAGR.

Which drug class leads global revenue among injectables?

Monoclonal antibodies lead with 38.00% of revenue and are projected to grow at 8.00% CAGR through 2031, supported by expanding oncology and immunology indications.

Which route of administration is growing the fastest and why?

Subcutaneous delivery is the fastest at a 12.40% CAGR, driven by high-concentration formulations, hyaluronidase-enabled large-volume dosing, and wearable injectors that support home administration.

Which application area contributes most to revenue today?

Oncology holds the largest share at 44.40%, reflecting widespread adoption of targeted biologics and perioperative use in neo-adjuvant and adjuvant settings.

How are packaging preferences changing across providers?

Vials still lead by share at 57.16%, but prefilled syringes are expanding at 9.60% CAGR as providers and payers favor ready-to-administer and self-injection formats that improve safety and adherence.

Which regions are set to contribute most to growth through 2031?

North America remains the largest by share at 38.40%, while Asia-Pacific is the fastest-growing region at an 8.03% CAGR due to capacity expansion and export-focused manufacturing.

Page last updated on: