DNA Methylation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

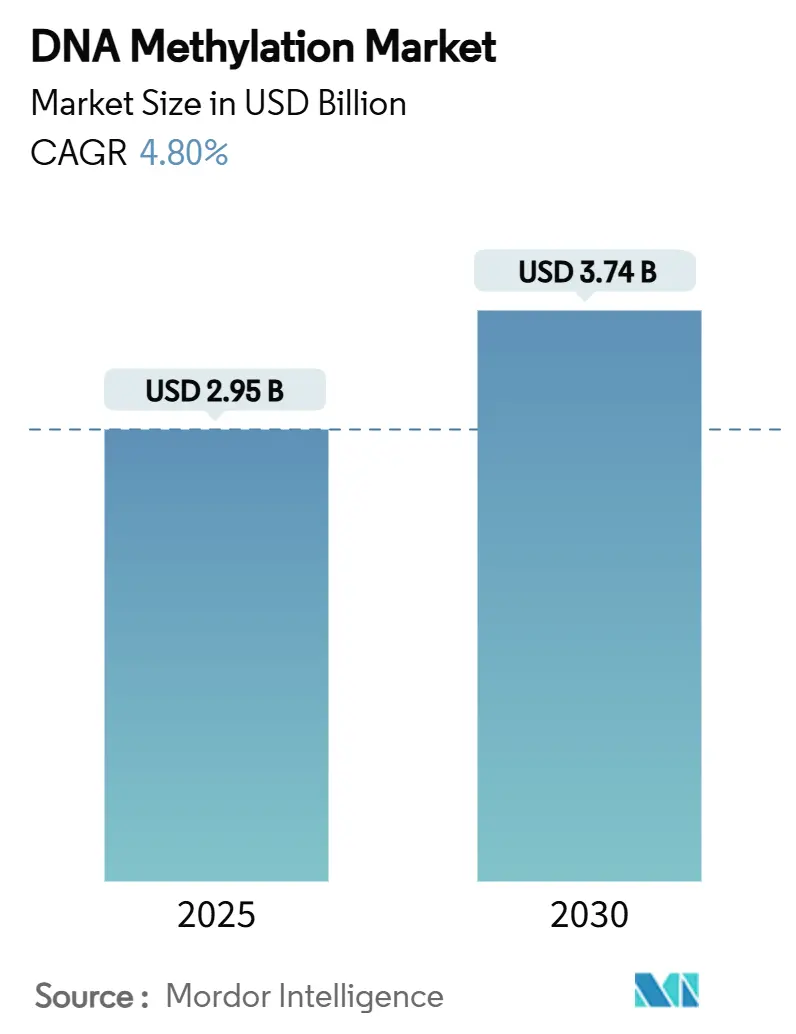

| Market Size (2025) | USD 2.95 Billion |

| Market Size (2030) | USD 3.74 Billion |

| Growth Rate (2025 - 2030) | 4.80% CAGR |

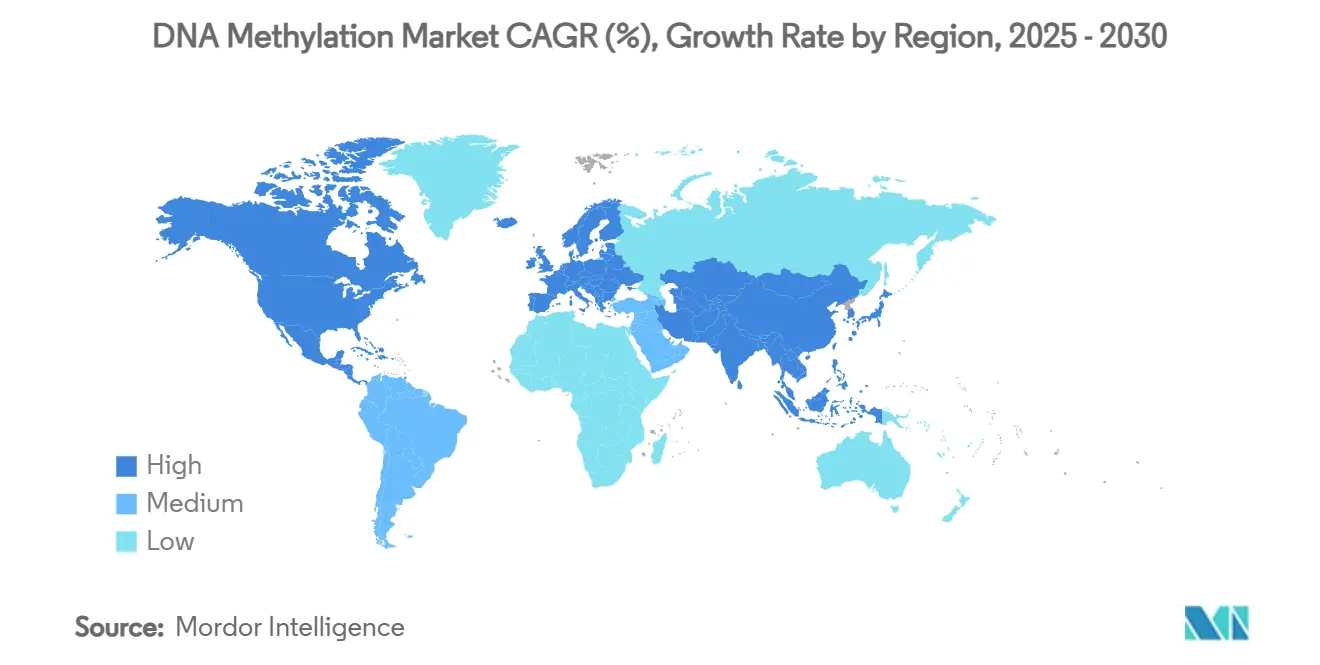

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DNA Methylation Market Analysis by Mordor Intelligence

The DNA methylation market size stands at USD 2.95 billion in 2025 and is forecast to reach USD 3.74 billion by 2030, reflecting a 4.8% CAGR over 2025-2030. Declining sequencing costs, fast platform upgrades, and mounting clinical evidence for liquid-biopsy methylation assays are accelerating adoption in oncology, prenatal testing, and other precision-medicine workflows. Direct detection methods using single-molecule real-time (SMRT) and nanopore technologies are advancing at double-digit growth rates, signaling a shift away from bisulfite conversion workflows toward native DNA analysis. Regional demand is anchored in North America’s strong regulatory framework and clinical-trial infrastructure, while Asia-Pacific registers the fastest uptake owing to national genomics initiatives and expanded healthcare spending. Moderate market consolidation prevails, with integrated platform strategies and data-driven services creating sticky customer relationships, even as disruptive single-cell and AI-powered solutions lower entry barriers for niche providers. Heightened public and private epigenetics funding, coupled with emerging agricultural and environmental use cases, broadens the total addressable DNA methylation analysis market beyond traditional healthcare segments.

Key Report Takeaways

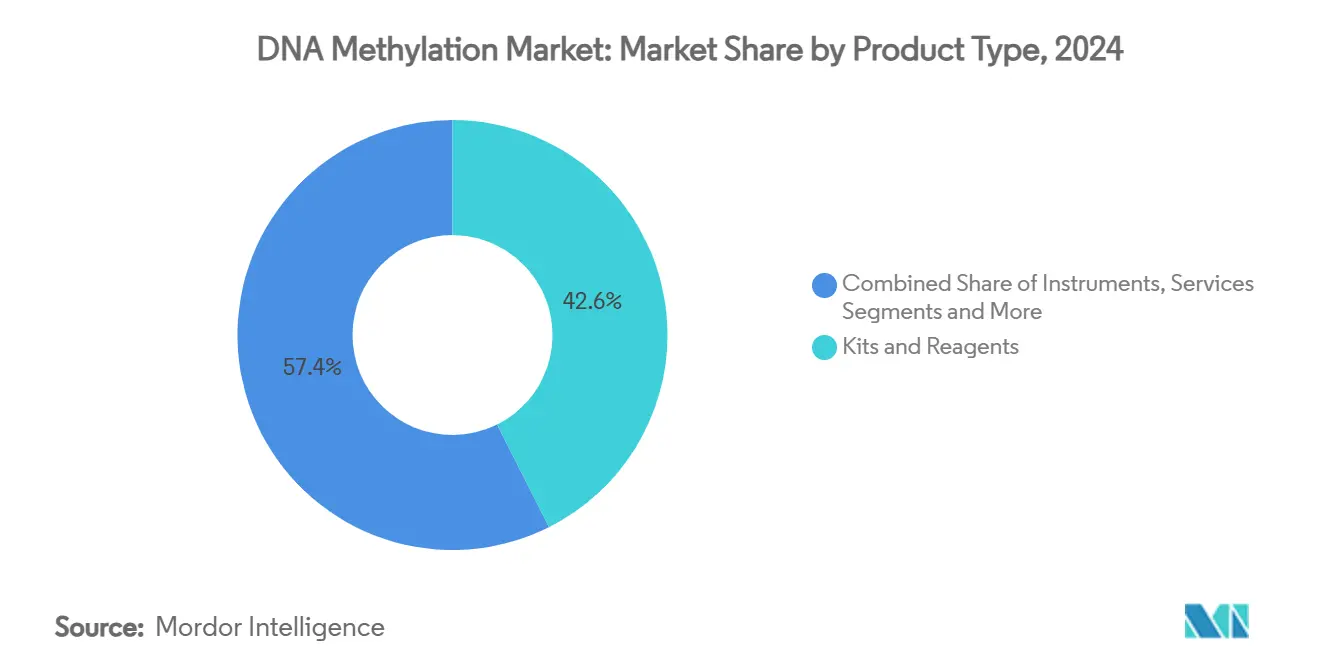

- By product type, kits and reagents held 42.6% DNA methylation analysis market share in 2024, whereas services are projected to record the highest 18.3% CAGR through 2030.

- By technology, bisulfite conversion-based sequencing led with 38.1% revenue share in 2024; SMRT and nanopore sequencing are expected to expand at a 22.1% CAGR to 2030.

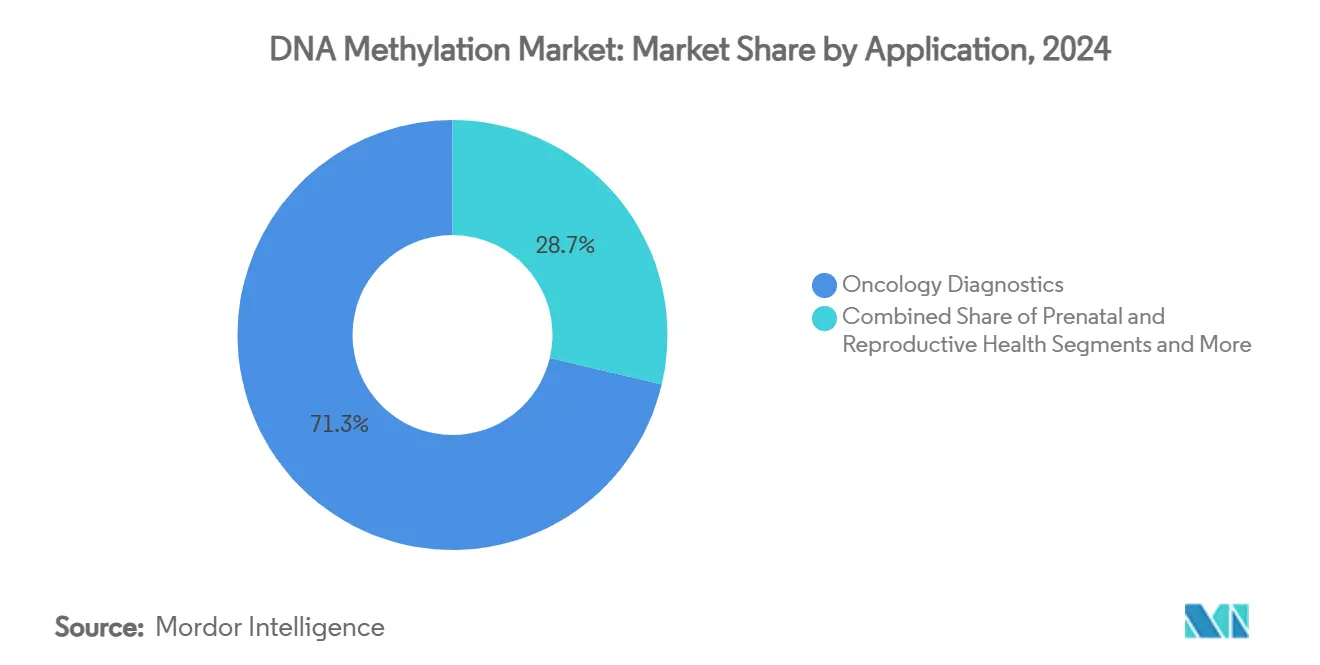

- By application, oncology diagnostics accounted for 71.3% of the DNA methylation analysis market size in 2024, while prenatal and reproductive health is forecast to rise at a 20.5% CAGR over 2025-2030.

- By end user, academic and research institutes commanded a 35.7% share of the DNA methylation analysis market in 2024; clinical and diagnostic laboratories are advancing at a 15.6% CAGR through 2030.

- Geographically, North America led with 44.8% DNA methylation analysis market share in 2024, yet Asia-Pacific is on track for the fastest 16.7% CAGR to 2030.

Global DNA Methylation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Cancer Fuelling Demand For Methylation-Based Diagnostics | +1.20% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Sequencing Cost Decline & Platform Upgrades | +0.80% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Surge In Public & Private Epigenetics Funding | +0.60% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Liquid-Biopsy Methylation Assays Gaining Traction | +1.00% | North America & Europe, clinical validation focus | Medium term (2-4 years) |

| AI-Driven Bioinformatics Accelerating Data Interpretation | +0.70% | Global, with tech hubs leading adoption | Short term (≤ 2 years) |

| Ag-Genomics Use-Cases For Crop Trait Optimisation | +0.30% | Global, with focus on agricultural economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Cancer Fueling Demand for Methylation-Based Diagnostics

Robust clinical evidence indicates methylation signatures detect multiple cancer types with >90% sensitivity and >95% specificity, outperforming protein biomarkers. Multi-cancer early-detection studies have accelerated regulatory milestones, particularly for hepatocellular carcinoma and colorectal cancer, where liquid-biopsy assays recorded 96.7% sensitivity in late-2024 trials.[1]Saverio Candido, “Recent Advances on Gene-Related DNA Methylation in Cancer Diagnosis, Prognosis, and Treatment,” Clinical Epigenetics, clinicalepigenetics.org Oncology clinicians are increasingly integrating methylation panels into routine diagnostics, driving steady laboratory demand and downstream bioinformatics service requirements. Pharma pipelines now include companion diagnostics that use methylation markers to stratify trial cohorts and monitor minimal residual disease, enhancing therapeutic response tracking. Regional reimbursement updates in the United States and Europe are further de-risking adoption pathways.

Sequencing Cost Decline & Platform Upgrades

Whole-genome bisulfite sequencing cost has fallen below USD 1,000 per sample, opening the DNA methylation analysis market to mid-tier clinical labs. Enzymatic conversion methods released in 2025 preserve DNA integrity while delivering >99% conversion efficiency, shortening turnaround time from days to hours. Direct methylation detection via SMRT and nanopore platforms eliminates conversion, enabling real-time data streaming and reducing hands-on processing: miniaturized library-prep workflows and 3-D-printed lab tools further lower consumable costs, democratizing access in resource-constrained settings. Equipment vendors now bundle cloud analytics, reducing capital outlays for local computational infrastructure.

Surge in Public & Private Epigenetics Funding

Government and industry stakeholders poured record sums into epigenetics in 2024, including the UK Biobank’s USD 50 million initiative to build a 50,000-sample epigenetic reference. Canada’s Pan-Canadian Genomics Strategy allocated USD 400 million to the commercialization of precision-medicine applications, a sizeable share earmarked for methylation studies.[2]Innovation, Science and Economic Development Canada, “Pan-Canadian Genomics Strategy: What We Heard Report,” Innovation, Science and Economic Development Canada, ised-isde.gc.caVenture capital flows into epigenetic start-ups surpassed USD 2 billion in 2024, targeting AI-enabled interpretation platforms and clinical-grade assay development. Intensified funding compresses discovery-to-clinic timelines and widens the skill-development pipeline for specialized bioinformatics roles. The influx also fuels global collaborative trials that unify datasets, boosting algorithm performance for cancer, neurological, and metabolic disease biomarkers.

Liquid-Biopsy Methylation Assays Gaining Traction

Methylation-based liquid biopsies are gaining regulatory clearances as non-invasive diagnostics with 96.7% sensitivity for blood-borne cancer detection. AI-assisted pattern recognition now discerns minimal residual disease at sub-0.1% variant allele frequencies, widening clinical utility for treatment monitoring and relapse prediction. Prenatal testing illustrates parallel momentum, with methylation assays achieving 100% concordance against invasive procedures while eliminating fetal-loss risks.[3]Anna Keravnou, Marios Ioannides, Christodoulos Loizides, et al., “MeDIP Combined with In-Solution Targeted Enrichment Followed by NGS: Inter-Individual Methylation Variability of Fetal-Specific Biomarkers and Their Implementation in a Proof-of-Concept Study for NIPT,” PLoS ONE, plos.orgMajor diagnostics suppliers have released cartridge-based methylation workflows compatible with existing high-throughput sequencers, facilitating rapid adoption in community hospitals and reference laboratories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Advanced Kits & Instruments | -0.90% | Global, with greater impact in emerging markets | Short term (≤ 2 years) |

| Scarcity Of Skilled Bioinformaticians | -0.70% | Global, with acute shortages in APAC & emerging markets | Medium term (2-4 years) |

| Data-Privacy / Ownership Concerns On Epigenomes | -0.50% | Europe & North America, GDPR compliance focus | Medium term (2-4 years) |

| Fragmented CfDNA Test Regulations Worldwide | -0.60% | Global, with varying regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Kits & Instruments

Flagship long-read sequencers and high-throughput bisulfite platforms carry list prices of USD 500,000–1 million per unit, putting ownership beyond reach for many regional hospitals. Premium-grade conversion reagents and methylation-specific enzymes add recurring costs that can exceed USD 100 per sample, limiting routine testing volumes. Clinical-grade workflows demand stringent quality controls, specialized cold-chain logistics, and compliant data-analysis pipelines, further raising barriers for small laboratories. Leasing and pay-per-use models partially offset capital constraints but remain nascent in low- and middle-income economies.

Scarcity of Skilled Bioinformaticians

DNA methylation datasets are multi-dimensional, requiring expertise in Python, R, and machine-learning frameworks tuned for epigenetics. Clinical labs, especially in Asia-Pacific, report months-long vacancies for senior bioinformatics roles, slowing test-validation timelines and limiting throughput. Academic curricula still emphasize general genomics, leaving a pipeline gap for methylation-specific analysts. Industry and universities are co-developing micro-credential courses, yet near-term shortages persist, compelling laboratories to outsource data interpretation to specialized service providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Drive Innovation Despite Kits Dominance

Due to consumable-intensive workflows, kits and reagents controlled 42.6% of the DNA methylation market share in 2024, while the services segment is forecast to post an 18.3% CAGR to 2030. Outsourcing to specialized providers appeals to clinical laboratories facing bioinformatics talent shortages and stringent compliance demands. Service firms offer end-to-end packages covering sample logistics, sequencing, data analysis, and clinical reporting, thereby converting capital outlays into operating expenses.

Recurring demand for high-purity enzymes and conversion reagents keeps consumables revenue resilient, and platform vendors bundle reagent-rental agreements to anchor long-term accounts. Instruments register steady replacement cycles as laboratories upgrade to direct-detection platforms that slash turnaround times. AI-embedded software subscriptions create incremental revenue streams, as labs seek automated annotation and decision-support modules. The combined dynamics reinforce a service-oriented DNA methylation analysis vision that complements consumables-driven profitability.

By Technology: Long-Read Sequencing Disrupts Traditional Methods

Bisulfite conversion-based sequencing retained 38.1% revenue share in 2024, yet SMRT and nanopore workflows are set to grow at a 22.1% CAGR, reshaping the DNA methylation analysis market size across all verticals. Direct detection provides longer reads, higher context specificity, and eliminates conversion bias, rendering it well-suited for challenging clinical specimens.

Affinity methods such as MeDIP and enrichment protocols remain advantageous for targeted panels, especially in resource-limited settings seeking cost optimization. Methylation microarrays maintain relevance for population-scale epidemiological studies, benefiting from standardized content and low per-sample pricing. Enzymatic conversion methods bridge cost and integrity gaps for fragmented cfDNA samples, broadening accessibility for prenatal and oncology labs. The technology mix is gradually consolidating toward hybrid platforms that integrate read-length flexibility with tunable cost-performance profiles.

By Application: Prenatal Testing Accelerates Beyond Oncology Dominance

Oncology diagnostics dominated the 2024 revenue pool, claiming 71.3% share of the DNA methylation analysis market size, underscored by the clinical success of liquid biopsies that detect multi-cancer signatures with >90% sensitivity. Repeat-testing workflows for treatment monitoring create annuity-like consumable demand in oncology labs.

Prenatal and reproductive health is projected to outpace all other applications at a 20.5% CAGR through 2030 as non-invasive methylation assays match invasive-test accuracy while mitigating procedure-related miscarriage risks. Neurological, metabolic, and immunological disease research sustains mid-single-digit growth, leveraging methylation profiling for early biomarker discovery. Agricultural and environmental epigenetics, though nascent, registers accelerating contract-research activity as governments prioritize sustainable food production and bio-surveillance.

By End User: Clinical Labs Accelerate Diagnostic Translation

Academic and research institutes captured 35.7% of the 2024 demand, reflecting the foundational role of discovery research in expanding the DNA methylation analysis industry. Clinical and diagnostic laboratories, however, are forecast to grow fastest at 15.6% CAGR as regulatory approvals broaden and reimbursement pathways solidify.

Pharmaceutical and biotech companies intensify their use of methylation assays for patient stratification and companion diagnostic development, while contract research organizations deliver outsourced high-throughput services. Government and non-profit biobanks leverage large-cohort methylation programs to inform public-health strategies, reinforcing the data volume for AI training and reference baselines.

Geography Analysis

North America commanded 44.8% DNA methylation analysis market share in 2024, underpinned by early liquid-biopsy approvals, advanced clinical-trial networks, and precision-medicine reimbursement frameworks. U.S. regulatory guidance for cfDNA assays and strong venture funding bolster domestic innovation pipelines, while Canada’s genomics strategy augments cross-border collaborations. Data-privacy debates and the BIOSECURE Act introduce compliance complexities for multi-national data exchanges, yet market momentum remains robust given the region’s payer dynamics and hospital capacity.

Asia-Pacific exhibits the fastest 16.7% CAGR through 2030 on the strength of national population-genomics initiatives, expanding precision-medicine budgets, and local manufacturing incentives that lower test-pricing thresholds. China, Japan, and South Korea deploy large-scale methylation reference projects, whereas India and Southeast Asian economies pilot public-private programs for prenatal and oncology applications. Regulatory alignment is progressing slowly, but talent-development partnerships aim to mitigate bioinformatics gaps and sustain long-term growth.

Europe maintains steady expansion backed by EU Horizon research grants, pan-European biobanks, and GDPR-aligned governance structures that instill patient trust. While Brexit initially disrupted cross-border data flows, bilateral frameworks restore momentum for UK-EU collaborations. The Middle East, Africa, and South America represent emerging opportunities, particularly in ag-genomics and population health, yet infrastructure and funding constraints temper near-term adoption.

Competitive Landscape

The DNA methylation analysis market is moderately consolidated, with integrated platform players expanding consumables and software ecosystems to lock in customers. Illumina leverages its NovaSeq X sequencer to bundle methylation and multi-omics workflows, emphasizing accuracy gains and reduced run costs. Oxford Nanopore’s alliance with UK Biobank strategically harnesses network effects around a 50,000-sample methylation dataset to enhance clinical-validation capabilities.

Emerging disruptors introduce single-cell methylation profiling and AI-based annotation pipelines, capturing research grants and venture capital that threaten incumbent share. Automated sample-prep partnerships, such as Tecan–Oxford Nanopore, reduce workflow complexity, broadening user bases in hospital labs. Patent portfolios around conversion chemistries, barcoding, and deep-learning algorithms form defensive moats and licensing revenue streams.

Service-oriented models gain prominence as laboratories confront skills shortages and compliance burdens. Guardant Health’s data-as-a-service collaboration with ConcertAI exemplifies a pivot toward longitudinal methylation monitoring fused with electronic health records, enriching real-world evidence for drug-development partners. New entrants often adopt cloud-native analytics and reagent-rental pricing to sidestep capex barriers, intensifying price competition for mid-volume users.

DNA Methylation Industry Leaders

Illumina Inc.

Thermo Fisher Scientific Inc.

QIAGEN N.V.

Merck KGaA (Sigma-Aldrich)

Agilent Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Guardant Health and ConcertAI launched a data-as-a-service platform that integrates clinical records with longitudinal tumor methylation data to accelerate cancer therapy R&D.

- November 2024: Oxford Nanopore Technologies and the UK Biobank initiated a 50,000-sample epigenetic mapping project to elucidate disease mechanisms.

- September 2024: QIAGEN expanded QIAcuity digital PCR with 100+ validated assays, improving lab readiness for DNA methylation analysis.

- August 2024: Illumina unveiled NovaSeq X upgrades, enabling multi-omics runs that incorporate methylation analysis.

Global DNA Methylation Market Report Scope

| Kits & Reagents |

| Instruments |

| Consumables & Accessories |

| Services |

| Software & Bioinformatics Tools |

| Bisulfite Conversion-Based Sequencing |

| Affinity / Enrichment (e.g., MeDIP) |

| Methylation Microarrays |

| Enzymatic Conversion-Based Methods |

| SMRT & Nanopore Sequencing |

| Oncology Diagnostics |

| Non-Oncology Disease Research |

| Prenatal & Reproductive Health |

| Agricultural & Environmental Epigenetics |

| Drug Discovery & Development |

| Academic & Research Institutes |

| Pharma & Biotech Companies |

| Clinical & Diagnostic Laboratories |

| Contract Research Organisations |

| Government & Non-Profit Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Kits & Reagents | |

| Instruments | ||

| Consumables & Accessories | ||

| Services | ||

| Software & Bioinformatics Tools | ||

| By Technology | Bisulfite Conversion-Based Sequencing | |

| Affinity / Enrichment (e.g., MeDIP) | ||

| Methylation Microarrays | ||

| Enzymatic Conversion-Based Methods | ||

| SMRT & Nanopore Sequencing | ||

| By Application | Oncology Diagnostics | |

| Non-Oncology Disease Research | ||

| Prenatal & Reproductive Health | ||

| Agricultural & Environmental Epigenetics | ||

| Drug Discovery & Development | ||

| By End User | Academic & Research Institutes | |

| Pharma & Biotech Companies | ||

| Clinical & Diagnostic Laboratories | ||

| Contract Research Organisations | ||

| Government & Non-Profit Organisations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the DNA methylation analysis market and how fast is it growing?

The market is valued at USD 2.95 billion in 2025 and is projected to grow at a 4.8% CAGR to reach USD 3.74 billion by 2030.

Which application area generates the most revenue for DNA methylation analysis?

Oncology diagnostics commands the largest share, accounting for 71.3% of global revenue in 2024, driven by liquid-biopsy assays for early cancer detection and treatment monitoring.

What technology trends are reshaping the DNA methylation analysis market?

Direct detection platforms such as SMRT and nanopore sequencing are expanding at a 22.1% CAGR, gradually displacing bisulfite conversion methods through faster turnaround times and higher data quality.

Which region is expected to grow the fastest over the forecast period?

Asia-Pacific is forecast to post the strongest 16.7% CAGR to 2030, supported by large-scale genomics initiatives and rising precision-medicine investments in China, Japan, and South Korea.

How are services influencing market dynamics?

Outsourced sequencing and bioinformatics services are the fastest-growing product segment at an 18.3% CAGR, helping laboratories bridge skills gaps and comply with clinical quality standards.

What major challenges could limit wider adoption of DNA methylation testing?

High instrument and reagent costs, a shortage of skilled bioinformaticians, and fragmented regulatory requirements for cfDNA tests remain key barriers to widespread clinical rollout.

Page last updated on: