Generic Injectables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

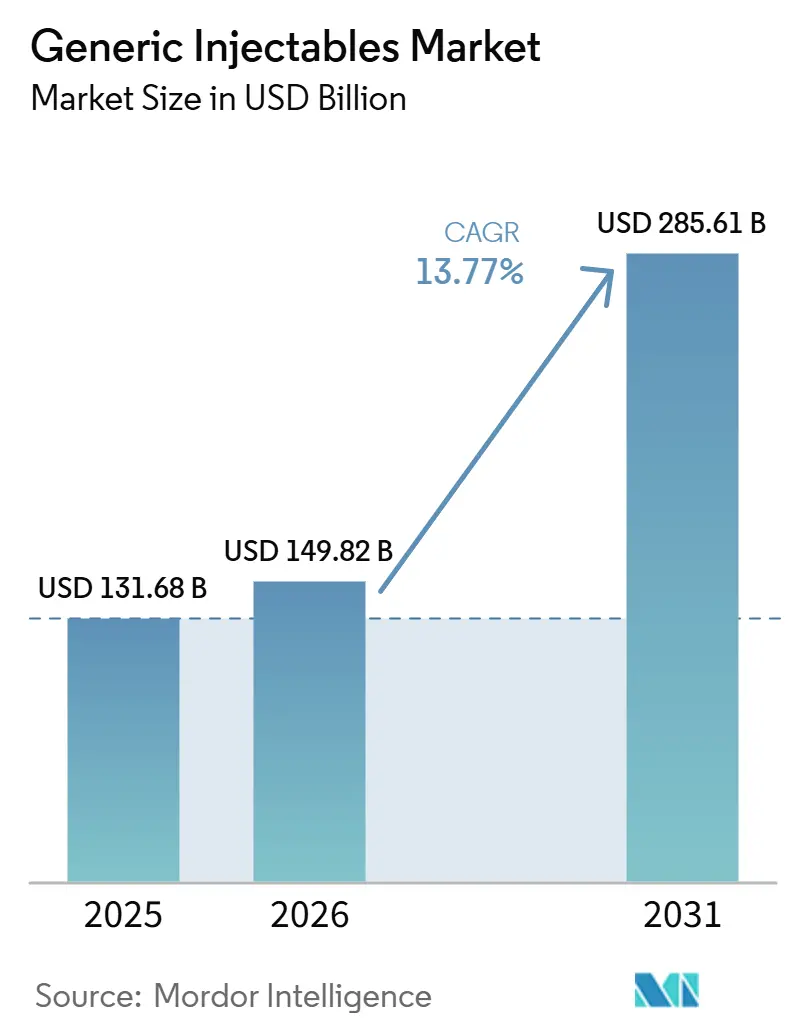

| Market Size (2026) | USD 149.82 Billion |

| Market Size (2031) | USD 285.61 Billion |

| Growth Rate (2026 - 2031) | 13.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Generic Injectables Market Analysis by Mordor Intelligence

The Generic Injectables Market size was valued at USD 131.68 billion in 2025 and is estimated to grow from USD 149.82 billion in 2026 to reach USD 285.61 billion by 2031, at a CAGR of 13.77% during the forecast period (2026-2031).

Growth remains tied to a broad loss-of-exclusivity cycle in branded injectable therapies and to payer pressure that keeps approved generic substitution central to hospital and formulary purchasing. The Generic Injectables Market is also being shaped by stricter procurement standards, because buyers are no longer focused only on unit price and now place more weight on supply continuity, sterile compliance, and operational ease in care settings. Competitive positions are separating between large sterile manufacturing groups with integrated fill-finish assets and lower-cost portfolio builders that serve regulated export markets from efficient production bases. Capacity constraints, compliance upgrades, and tender-led price pressure still limit how quickly suppliers can convert demand into revenue, especially in mature hospital categories. Even so, the Generic Injectables Market continues to offer room for expansion in biosimilars, complex injectables, ready-to-use formats, and home-administered products that fit the shift toward more flexible care delivery.

Key Report Takeaways

- By therapeutic area, oncology accounted for 33.26% share of the Generic Injectables Market size in 2025 and is forecast to grow at a 16.55% CAGR through 2031.

- By distribution channel, hospital pharmacies held 62.52% of revenue in 2025, while online pharmacies are projected to record the highest CAGR at 18.25% through 2031.

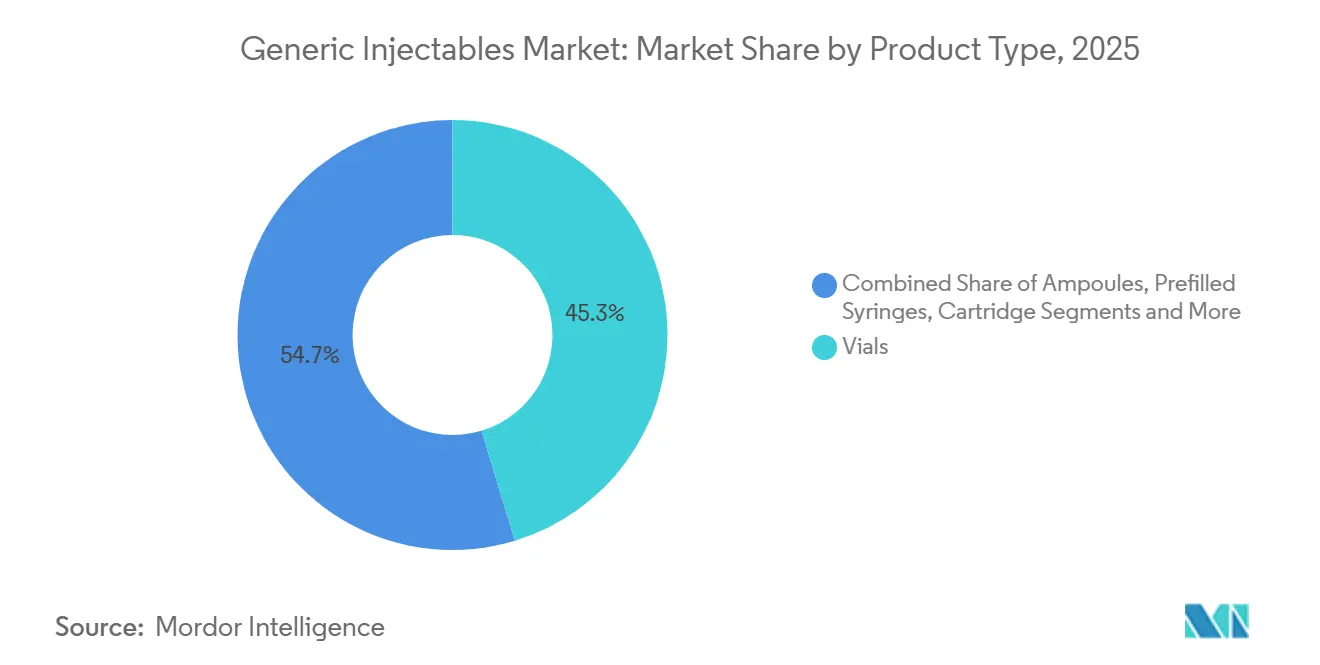

- By product type, vials held 45.31% of revenue in 2025, while prefilled syringes are projected to advance at a 16.38% CAGR through 2031.

- By molecule type, small-molecule generics held 58.24% of revenue in 2025, while large-molecule injectables and biosimilar generics are projected to grow at a 15.52% CAGR through 2031.

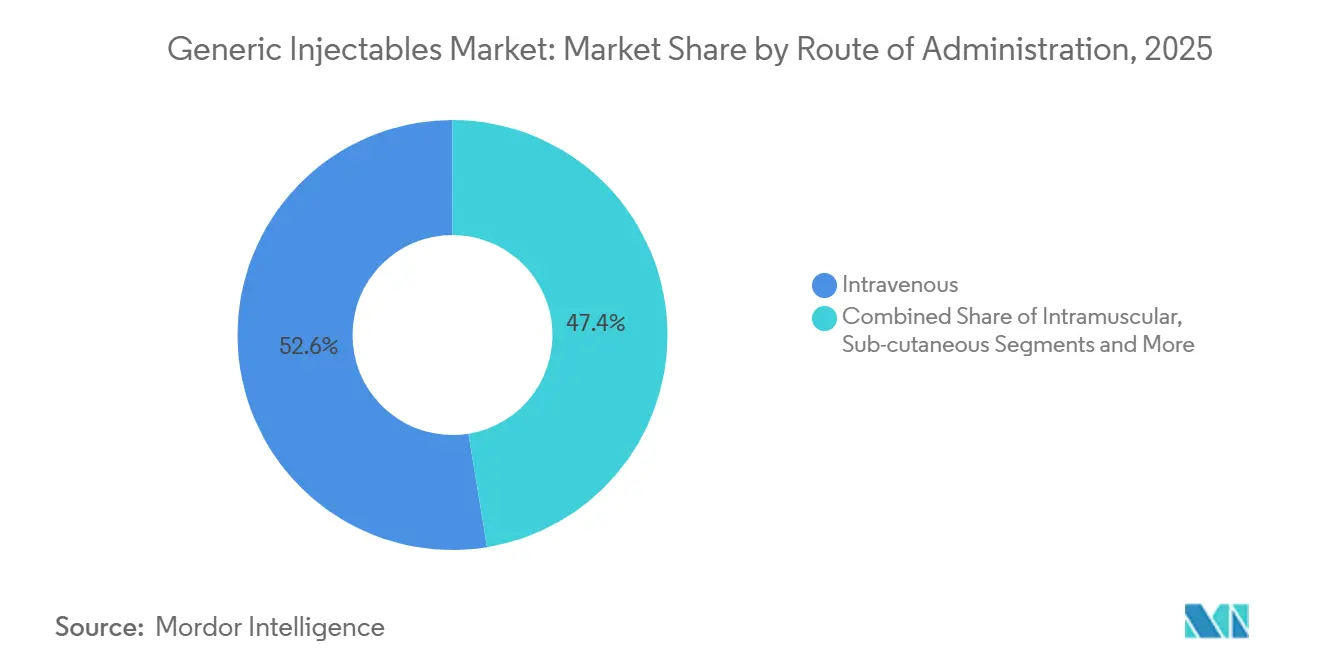

- By route of administration, intravenous delivery held 52.56% of revenue in 2025, while subcutaneous delivery is projected to grow at a 17.65% CAGR through 2031.

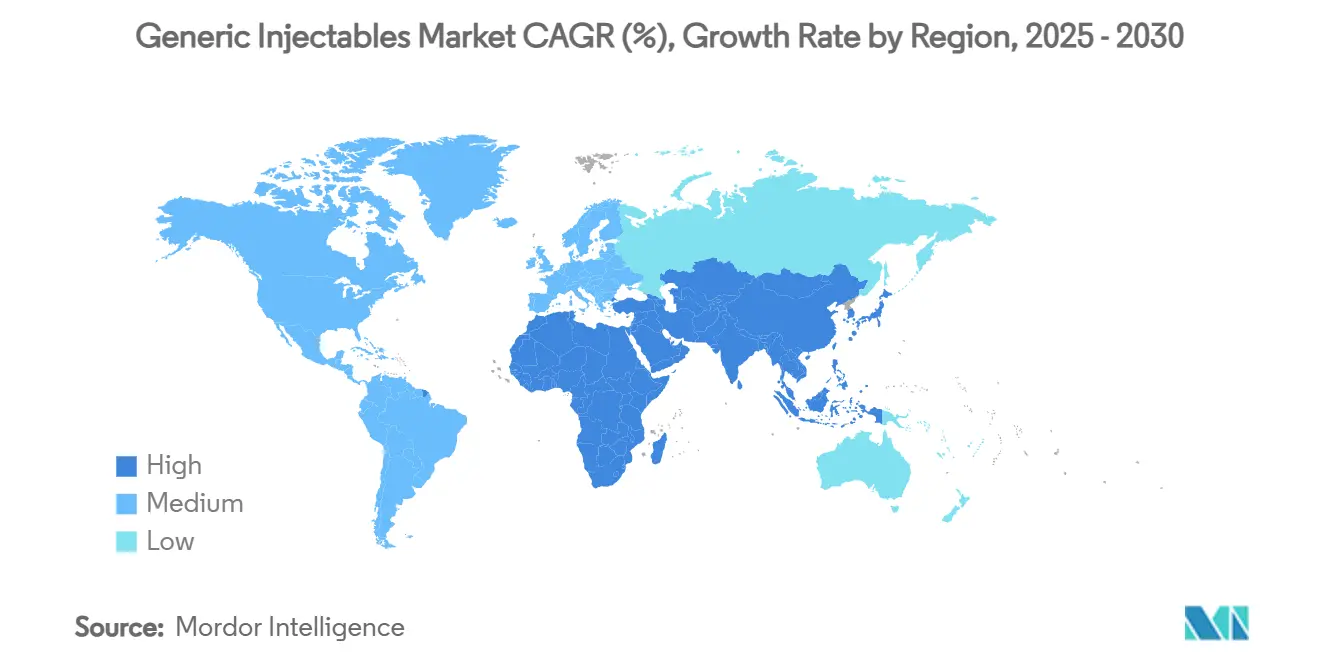

- By geography, North America held 36.62% of Generic Injectables Market share in 2025, while Asia-Pacific is projected to expand at a 16.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Generic Injectables Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent Cliff Wave Accelerating Generic Launches | +3.5% | Global, peak impact in North America and Europe | Short term (≤ 2 years) |

| Rising Demand for Sterile Affordable Oncology and Anti-Infective Therapies | +2.8% | Global, concentrated in North America, Europe, APAC | Long term (≥ 4 years) |

| Hospital Preference for Ready-to-Use and Pre-Administration Formats | +1.8% | North America and EU, with spill-over to APAC core | Medium term (2-4 years) |

| Biosimilar and Complex Injectable Approvals Broadening Addressable Demand | +2.5% | Global, led by North America and EU with spill-over to APAC | Medium term (2-4 years) |

| AI-Assisted Formulation and Analytical Development Shortening Development Cycles | +1.2% | Global, strongest in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Lyophilized-to-Liquid Conversion Lowering Cold-Chain and COGS Burden | +0.8% | North America and EU, emerging in APAC core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patent Cliff Wave Accelerating Generic Launches

The Generic Injectables Market is benefiting from a broad wave of branded injectable exclusivity losses that is opening more room for abbreviated approvals and faster portfolio turnover. This matters most in hospital drugs, because a single loss of exclusivity can unlock multiple follow-on launches across oncology, supportive care, and acute care categories. The FDA approved 4 first generic injectable drugs in the first quarter of 2026, including bortezomib powder for injection and aprepitant injection, which shows that the sterile approval pipeline remains active and responsive to launch windows. The Generic Injectables Market also gains from the fact that technical barriers in sterile development are higher than in oral solids, so many entrants still target products where fewer qualified competitors can launch at the same time. That supports a more durable volume base during the early phase of competition, especially when hospitals want approved alternatives ready as branded products lose protection. The result is a launch environment where timing, regulatory readiness, and sterile capacity matter as much as the molecule itself.

Rising Demand for Sterile Affordable Oncology and Anti-Infective Therapies

The Generic Injectables Market continues to draw support from hospital demand for lower-cost oncology and anti-infective products that still meet strict quality and supply standards. Oncology already held 33.26% of revenue in 2025 and is projected to post a 16.55% CAGR through 2031, which keeps it at the center of both present volume and future growth. In anti-infectives, hospitals still need broad-spectrum injectable coverage across carbapenems, beta-lactams, antifungals, and other acute care therapies where treatment delays are not acceptable. That need changes purchasing behavior, because buyers often prefer a wider approved supplier list in shortage-prone or clinically sensitive categories instead of relying on only the lowest bidder. The Generic Injectables Market therefore benefits from a procurement model that rewards continuity, approved manufacturing quality, and dependable replenishment in addition to price. This is especially important in hospital formularies where the cost of disruption can be greater than the savings from a narrow sourcing strategy.

Biosimilar and Complex Injectable Approvals Broadening Addressable Demand

The Generic Injectables Market is also expanding through complex injectable products and biosimilars, where regulatory progress is opening a larger pool of addressable therapies. FDA biosimilar product information showed 90 approved biosimilars in the United States as of early 2026, and 25 of them had interchangeability status that can support pharmacy-level substitution in eligible settings. The FDA also approved 18 injectable biosimilars in 2025 across products such as denosumab, insulin aspart, aflibercept, bevacizumab, omalizumab, pegfilgrastim, pertuzumab, ranibizumab, and tocilizumab. This part of the Generic Injectables Market has a different economic profile from commodity generics, because biologic manufacturing, analytical characterization, and development requirements narrow the set of capable competitors. Companies that build these capabilities can move into categories where competition starts later and operating margins are less exposed to immediate price collapse. That is why complex sterile formats and biosimilar injectables are becoming a larger share of investment plans across the Generic Injectables Market.

Hospital Preference for Ready-to-Use and Pre-Administration Formats

The Generic Injectables Market is seeing a steady format shift toward products that reduce bedside preparation and lower handling complexity in pharmacies and care units. Hospital pharmacies held 62.52% of distribution revenue in 2025, which gives hospital procurement teams strong influence over whether vials, ready-to-dilute products, premixed bags, and prefilled syringes gain share. A 2025 economic evaluation in ClinicoEconomics and Outcomes Research found that ready-to-dilute thiotepa reduced hospital pharmacy costs through lower compounding time, less drug waste, and fewer preparation-related consequences compared with the lyophilized alternative. This means buyers are increasingly comparing total operating burden, not only list price, when they decide which injectable format to prefer. The Generic Injectables Market therefore rewards suppliers that can combine sterile compliance with formats that fit routine hospital workflows. Over time, that can shift contract wins toward companies that offer ready-to-use portfolios across multiple treatment categories.

Restraints Impact Analysis of Generic Injectables Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sterile Fill-Finish Capacity Bottlenecks | -2.2% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Tender-Led Price Compression and GPO Consolidation | -1.9% | North America, dominant, and Europe | Long term (≥ 4 years) |

| Annex 1 and Sterility Compliance Cost Escalation | -1.6% | EU primarily, with spill-over to APAC export manufacturers | Medium term (2-4 years) |

| Volatile Supply of Type I Glass and COP Components | -0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sterile Fill-Finish Capacity Bottlenecks

The Generic Injectables Market still faces a hard operational limit in sterile fill-finish capacity, because demand can rise faster than compliant commercial lines can be expanded. This issue is more serious in injectables than in simpler dosage forms, since aseptic production needs specialized equipment, strict validation, and longer ramp-up periods before output becomes usable for regulated sales. The 2024 PDA survey on Annex 1 implementation showed that 40% of responding facilities needed timeline extensions and 30% reported upgrade investments above USD 2 million, which indicates that available compliant capacity is tighter than simple facility counts suggest[1]Parenteral Drug Association, “GMP Annex 1 Implementation,” PDA Letter Portal, pda.org. The Generic Injectables Market is therefore vulnerable when several launch windows, shortage categories, and capacity upgrades overlap in the same planning period. New capacity additions help, but they do not remove the short-term pressure on scheduling, validation, and regulatory readiness. As a result, some suppliers may hold approvals yet still struggle to convert them into timely commercial supply.

Tender-Led Price Compression and GPO Consolidation

The Generic Injectables Market also remains exposed to price pressure from hospital contracting systems that concentrate buying power in a small number of procurement organizations or national tender frameworks. In the United States, this pressure is strongest in mature injectable categories where multiple approved suppliers compete for large multi-year contracts and where price often becomes the deciding factor once supply reliability is assumed. The same pattern appears in Europe, where reference pricing, rebates, and volume-linked tenders can pull net selling prices down even when sterile compliance costs are rising. This creates a difficult position for mid-tier manufacturers, because losing one major contract can weaken line utilization and reduce the economic case for keeping lower-margin products in production. The Generic Injectables Market therefore does not reward scale evenly, and it tends to favor producers that can absorb margin pressure across broader portfolios and larger manufacturing networks. Over time, that tension can remove weaker suppliers from some categories and leave buyers with fewer financially stable options than the tender process first appears to create.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Generic Injectables Market Segment Analysis

By Product Type:

Vials Lead, Prefilled Formats Redefine Volume DynamicsVials held 45.31% of revenue in 2025, while prefilled syringes are projected to grow at a 16.38% CAGR through 2031, which shows how the Generic Injectables Market is balancing legacy hospital use with newer delivery preferences. Vials still fit entrenched oncology infusion and anti-infective protocols, especially in institutional settings where dose flexibility and existing administration systems remain important. Prefilled syringes are gaining ground because they reduce preparation steps, support safer handling, and match the wider shift toward subcutaneous biologics and ready-to-use care models. The June 2026 positive CHMP opinion for Nylaspeg, a pegfilgrastim biosimilar in a 6 mg prefilled syringe presentation, reflected how new biosimilar launches are increasingly entering the market in ready-to-use formats from the start. In the Generic Injectables Market, that matters because it shortens the gap between molecule approval and real-world adoption in the format hospitals and patients already prefer.

Ampoules still have a role in anesthesia and emergency medicine, especially in settings where closed-system alternatives are not yet the default requirement. IV bags and large-volume parenterals keep stable institutional demand in critical care, electrolyte replacement, and parenteral nutrition, where high-volume administration remains routine. Cartridges serve a narrower but relevant part of the Generic Injectables Market tied to insulin and GLP-1 pen delivery systems, where convenience and device compatibility matter. Manufacturers that can move between vial and prefilled syringe output on flexible lines are better positioned when procurement contracts ask for both traditional and ready-to-use presentations under one supply relationship. That flexibility can help suppliers hold share in established categories while still participating in the faster migration toward newer delivery formats.

By Molecule Type:

Biosimilar Generics Redefine the Competitive CeilingSmall-molecule generics held 58.24% share of the Generic Injectables Market size in 2025, while large-molecule injectables and biosimilar generics are projected to expand at a 15.52% CAGR through 2031. Small molecules remain the core of present revenue because they include deep hospital categories such as IV antibiotics, cytotoxic chemotherapy, analgesics, and cardiovascular injectables with broad procurement demand. Their regulatory pathways are more established, and that supports a large installed base of approved products across many health systems. By contrast, the faster growth in large-molecule injectables shows where the Generic Injectables Market is moving, because fewer companies can support biologic process development, analytical work, and sterile manufacturing at commercial scale. FDA biosimilar records also show a steady buildout in this opportunity set, including 18 injectable biosimilar approvals in 2025 and 90 approved biosimilars in total as of early 2026.

This transition is changing investment priorities across the Generic Injectables Market, because the most attractive long-cycle opportunities now sit in complex biologics rather than only in commodity molecules. Aurobindo Pharma’s June 2026 launch of the TheraNym biologics contract manufacturing facility in Telangana, with 15 KL bioreactors and aseptic fill-finish capability, showed how Indian producers are building infrastructure for this shift[2]Aurobindo Pharma Limited, “Q4 FY26 Investor/Earnings Presentation,” Aurobindo Pharma Limited, aurobindo.com. The move toward biosimilar injectables also raises the competitive threshold, since companies need a broader operating model that links biologic manufacturing, sterile finishing, and regulatory execution. That means the future leadership pattern in the Generic Injectables Market will depend less on the breadth of simple generic filings alone and more on whether suppliers can scale high-complexity sterile assets. Manufacturers that begin this transition now are preparing for a period when more large biologic injectables lose exclusivity and create a wider competitive field.

By Therapeutic Area:

Oncology Commands Both Volume and VelocityOncology held 33.26% of revenue in 2025 and is projected to expand at a 16.55% CAGR through 2031, making it the clearest example of simultaneous volume leadership and growth leadership in the Generic Injectables Market. This position reflects steady hospital use of cytotoxic agents, supportive care injectables, and a rising biosimilar substitution window for expensive oncology biologics. Anti-infectives remained the second-largest therapeutic block, supported by hospital demand for IV antibiotics, antifungals, and antivirals in acute care settings where treatment continuity is essential. Cardiovascular injectables continued to provide a stable base through emergency cardiac drugs, antithrombotic infusions, and antiarrhythmics that move through institutional procurement with predictable demand. Together, these segments keep the Generic Injectables Market closely tied to inpatient care, formulary compliance, and shortage management.

Diabetes and metabolic disorders are also becoming more visible in the Generic Injectables Market as insulin biosimilars gain regulatory ground and fit broader substitution pathways. FDA biosimilar records showed multiple insulin products cleared by 2025 and 2026, including cases with interchangeability designations that can support automatic substitution where permitted. CNS disorders add another stable layer through injectable antiepileptics, depot antipsychotics, and sedation agents used in hospital and intensive care settings. Oncology still stands apart, because buyers in shortage-sensitive cancer categories often place more value on supply assurance and procurement continuity than they do in more commoditized injectable classes. That helps preserve a stronger commercial position for qualified suppliers even when the wider Generic Injectables Market remains exposed to pricing pressure.

By Route of Administration:

Subcutaneous Surges as Biologic Delivery Migrates HomeIntravenous administration held 52.56% of revenue in 2025, while subcutaneous delivery is projected to grow at a 17.65% CAGR through 2031, showing a clear route shift inside the Generic Injectables Market. IV delivery remains essential for oncology infusion, anti-infective therapy, and critical care because these settings still need rapid onset, dose control, and institutional supervision. Intramuscular products keep a moderate position in hormonal therapies, depot antipsychotics, and selected preventive care applications. Subcutaneous growth is stronger because more biologics are moving toward self-administration models that reduce hospital visits and fit home-based treatment patterns. This route is becoming one of the main structural growth engines in the Generic Injectables Market, especially where the product can be paired with a device or a simplified delivery presentation.

Aurobindo Pharma’s 2026 plan for clinical studies on trastuzumab 600 mg in a subcutaneous presentation shows how this migration is extending into oncology, not only into immunology or metabolic therapy. Suppliers that invest in subcutaneous formulation work, autoinjector partnerships, and user-friendly presentations are aligning with a part of the Generic Injectables Market that is growing faster than traditional institutional routes. The link between subcutaneous delivery and biosimilar expansion is especially important, because many of the products best suited for home administration also sit in higher-value biologic categories. Other routes such as intrathecal and intra-articular delivery remain small, but they still represent less crowded pockets where approved supplier counts can stay limited. That leaves room for specialized entrants that can manage complex sterile development without competing directly in the largest commodity classes.

By Distribution Channel:

Hospital Dominance Meets Accelerating Digital DisruptionHospital pharmacies held 62.52% of revenue in 2025, while online pharmacies are projected to record an 18.25% CAGR through 2031, which captures the split between present control and future acceleration in the Generic Injectables Market. Hospitals still dominate because supervised IV therapy, oncology administration, and institutional bulk buying keep most injectable volume inside organized care settings. Retail and mail-order pharmacies are gaining a larger role where products are suited to home administration, especially for insulin biosimilars and other self-administered injectables. Online channels are moving even faster as telehealth prescribing, direct-to-consumer refill models, and expanded logistics improve patient access across a broader geographic base. In the Generic Injectables Market, the rise of online dispensing depends less on traditional IV products and more on formats that are stable, portable, and practical for self-use.

This channel shift reinforces the route shift already visible in the Generic Injectables Market, because subcutaneous biologics and insulin products are better matched to home storage and remote dispensing than institution-bound infusions. FDA interchangeability designations also support this trend by making substitution easier at the pharmacy level for qualifying biosimilar products. Institutional wholesalers and specialty distributors still remain relevant, especially in regions where direct hospital purchasing infrastructure is less developed. Their role is more visible in parts of APAC and the GCC, where intermediary networks still connect manufacturers to hospital demand. Over time, the Generic Injectables Market will likely show a wider gap between channels that serve acute-care infusion products and channels that serve home-administered injectables with device support.

Geography Analysis

North America Generic Injectables Market

North America retained leadership with 36.78% of the generic injectables market revenue share in 2024, supported by sophisticated hospital infrastructure, advanced compounding automation, and a clear regulatory framework that speeds complex generic approvals. Health systems continue to invest in robotic preparation platforms and gravitate to ready-to-administer presentations that curb medication errors and nursing workload. Reimbursement policies accommodate premium pricing for device-enabled generics that cut downstream care costs.

APAC Generic Injectables Market

Asia-Pacific generates the fastest CAGR at 16.43% through 2030 as India scales its Production Linked Incentive (PLI) scheme, channeling USD 2 billion into sterile capacity expansions and technology upgrades. China aligns its National Medical Products Administration standards with ICH guidelines, enhancing export credibility. Manufacturing clusters leverage lower labor costs and accelerating regulatory harmonization to capture global contract fill-finish work. Japan, South Korea, and Australia lift regional value through early adoption of biosimilars and supportive pricing frameworks.

Western Europe Generic Injectables Market

Europe remains pivotal thanks to its stringent quality standards, entrenched pharmaceutical manufacturing base, and single-payer reimbursement that broadens patient access. Implementation of the revised EU GMP Annex 1 raises compliance costs yet ultimately strengthens supply reliability.[3]European Medicines Agency, “EU GMP Annex 1 Revision Guidelines,” ema.europa.eu Germany and France lead automated fill-finish adoption, while Eastern European nations attract contract work through competitive tax regimes. The generic injectables market size in Western Europe edges upward as biosimilar adoption deepens across oncology and immunology indications.

Competitive Landscape

The Generic Injectables Market remains fragmented across product lines, but competitive leadership is still concentrated among a relatively small group of large sterile manufacturers with scale, compliance depth, and hospital access. Fresenius Kabi, Teva Pharmaceutical, Hikma Pharmaceuticals, Baxter International, and Sandoz Group sit close to the center of this structure, while Indian manufacturers such as Aurobindo Pharma, Dr. Reddy’s Laboratories, Cipla, Sun Pharmaceutical, and Lupin remain important through cost-efficient integration and regulated export supply. In practice, the strongest positions belong to companies that can link API sourcing, sterile fill-finish, regulatory execution, and dependable replenishment across more than one geography. The Generic Injectables Market therefore rewards operating breadth as much as product breadth, because hospital buyers increasingly assess resilience and execution under shortage-sensitive conditions. Competitive advantage is no longer defined only by low cost, since compliance readiness and format relevance now shape who can scale profitable volume.

Recent strategic moves show how companies are responding to these demands in the Generic Injectables Market. Fresenius Kabi and Phlow Corp. announced an end-to-end United States manufacturing collaboration for Epinephrine Injection, USP in February 2026, combining domestic API production with finished-dose manufacturing across multiple states to strengthen supply reliability in an essential injectable category. Hikma’s USD 1 billion U.S. investment plan through 2030 showed a similar intent to deepen sterile capacity and R&D around essential generic medicines. Teva added another example in March 2026 when it received FDA approval for PONLIMSI, a denosumab biosimilar, and also secured dual filing acceptances for an omalizumab biosimilar candidate.

The next layer of competition in the Generic Injectables Market is forming around complexity access rather than basic scale alone. Companies with biologics infrastructure, ready-to-use format capabilities, and route-specific delivery know-how are better placed to move beyond heavily commoditized injectable classes. Aurobindo’s TheraNym facility is one example of how suppliers are preparing for more biologic and biosimilar work inside the sterile injectable space. White-space opportunities still exist in niche sterile formats such as orphan oncology injectables, intrathecal delivery, and extended-release injectable systems where the number of capable competitors remains limited. That means the Generic Injectables Market is likely to stay broad and fragmented overall, while a smaller set of technically stronger companies capture the more complex and less crowded profit pools.

Generic Injectables Industry Leaders

Fresenius Kabi

Pfizer Inc.

Viatris Inc.

Hikma Pharmaceuticals PLC

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Generic Injectables Market Companies Covered in this Report

- Accord Healthcare Limited

- Apotex

- Aurobindo Pharma

- Baxter

- Cipla

- Dr. Reddy’s Laboratories

- Endo International

- Fresenius

- Glenmark Pharmaceuticals

- Hikma Pharmaceuticals

- Intas Pharmaceutical

- Lupin

- Pfizer

- Sandoz Group AG

- Sawai Pharmaceutical Group

- Stada Arzneimittel

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Viatris

- Zydus Lifesciences Limited

Recent Industry Developments in Generic Injectables Market

- March 2026: Teva Pharmaceutical received FDA approval for PONLIMSI (denosumab-adet), an injectable biosimilar to Prolia (denosumab), and received dual filing acceptances from both the FDA and EMA for a proposed omalizumab biosimilar candidate, expanding Teva's injectable biosimilar portfolio under its "Pivot to Growth" strategy and confirming dual-regulatory market access.

- February 2026: Fresenius Kabi and Phlow Corp. announced the first-ever end-to-end US manufacturing collaboration for Epinephrine Injection, USP, with API production at Phlow's advanced manufacturing campus in Virginia and finished-dose manufacturing at Fresenius Kabi's facilities in Illinois, New York, and North Carolina. Domestically produced Epinephrine is targeted for availability to US hospitals by 2027, pending FDA approval, as part of a broader pharmaceutical sovereignty initiative.

Global Generic Injectables Market Report Scope

As per the scope of the report, generic injectables are affordable, equivalent versions of brand-name injectable drugs, containing the same active ingredients and used for medical treatments.

The generic injectables market is segmented by product type into vials, ampoules, prefilled syringes, cartridges, and IV bags and large-volume parenterals; by molecule type into small-molecule generics and large-molecule injectables and biosimilar generics; by therapeutic area into oncology, anti-infectives, cardiovascular, diabetes and metabolic disorders, central nervous system disorders, and other therapeutic areas; by route of administration into intravenous, intramuscular, subcutaneous, and other routes of administration; by distribution channel into hospital pharmacies, retail and mail-order pharmacies, online pharmacies, and other distribution channels; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

Segmentation Overview

| Vials |

| Ampoules |

| Prefilled Syringes |

| Cartridges |

| IV Bags and Large Volume Parenterals |

| Small-Molecule Generics |

| Large-Molecule Injectables and Biosimilar Generics |

| Oncology |

| Anti-Infectives |

| Cardiovascular |

| Diabetes and Metabolic Disorders |

| Central Nervous System Disorders |

| Other Therapeutic Areas |

| Intravenous |

| Intramuscular |

| Subcutaneous |

| Other Routes of Administration |

| Hospital Pharmacies |

| Retail and Mail-Order Pharmacies |

| Online Pharmacies |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Vials | |

| Ampoules | ||

| Prefilled Syringes | ||

| Cartridges | ||

| IV Bags and Large Volume Parenterals | ||

| By Molecule Type | Small-Molecule Generics | |

| Large-Molecule Injectables and Biosimilar Generics | ||

| By Therapeutic Area | Oncology | |

| Anti-Infectives | ||

| Cardiovascular | ||

| Diabetes and Metabolic Disorders | ||

| Central Nervous System Disorders | ||

| Other Therapeutic Areas | ||

| By Route of Administration | Intravenous | |

| Intramuscular | ||

| Subcutaneous | ||

| Other Routes of Administration | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail and Mail-Order Pharmacies | ||

| Online Pharmacies | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the Generic Injectables Market?

The Generic Injectables Market is valued at USD 149.82 billion in 2026 and is projected to reach USD 285.61 billion by 2031 at a 13.77% CAGR.

Which therapeutic area leads generic injectables demand?

Oncology leads with 33.26% of revenue in 2025 and is also the fastest-growing therapeutic area with a 16.55% CAGR through 2031.

Which product format is growing fastest in generic injectables?

Prefilled syringes are the fastest-growing product format, with a projected 16.38% CAGR through 2031, while vials still led revenue with 45.31% in 2025.

Why are hospital pharmacies still the main channel for injectable generics?

Hospital pharmacies held 62.52% of revenue in 2025 because supervised IV therapy, oncology administration, and bulk institutional purchasing still dominate injectable use.

Which region is expanding fastest for generic injectables?

Asia-Pacific is the fastest-growing region, with a projected 16.15% CAGR through 2031, supported by sterile capacity expansion and stronger export compliance.

What is changing competition in this space the most?

Competition is shifting toward biosimilars, complex sterile products, and reliable compliant capacity, rather than only low-cost supply in commodity injectables.

Page last updated on: