MRNA Vaccines And Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

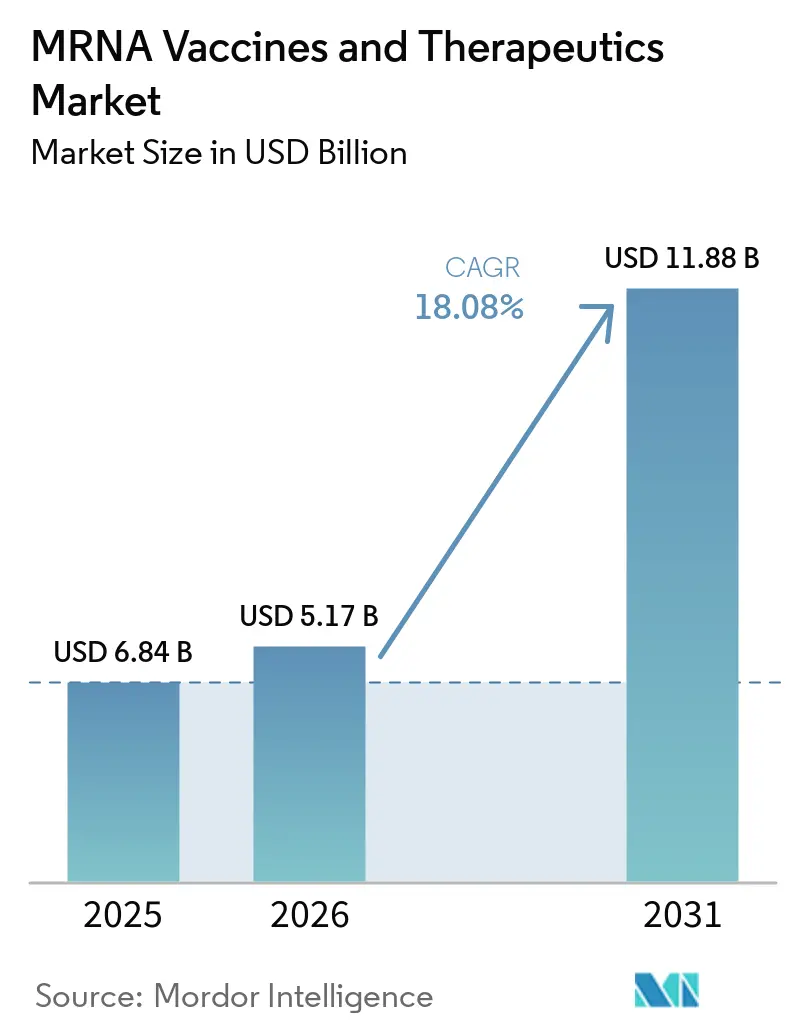

| Market Size (2026) | USD 5.17 Billion |

| Market Size (2031) | USD 11.88 Billion |

| Growth Rate (2026 - 2031) | 18.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

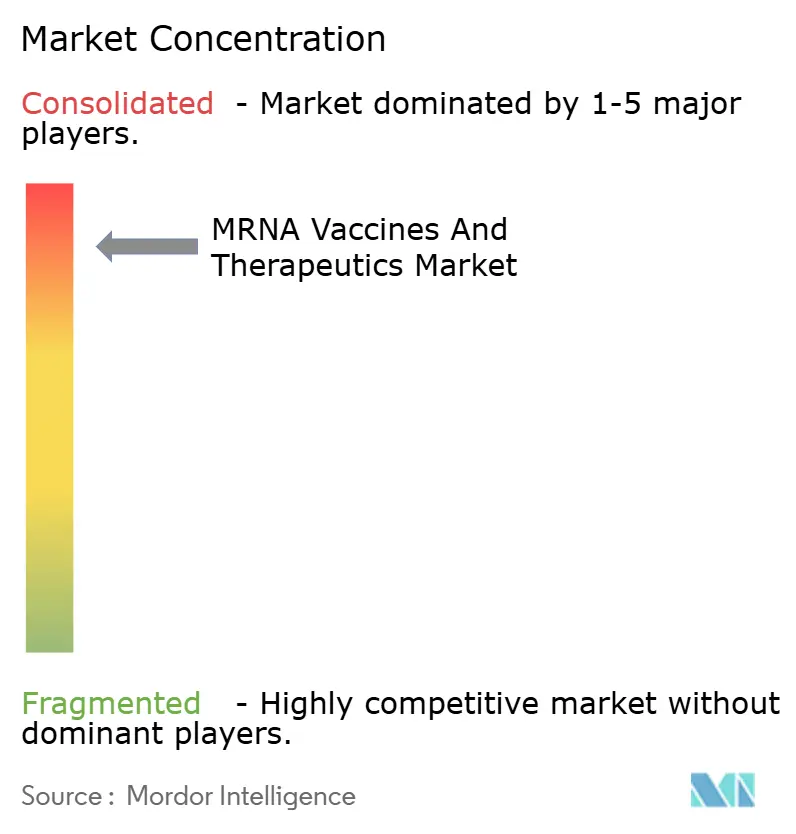

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

MRNA Vaccines And Therapeutics Market Analysis by Mordor Intelligence

The MRNA Vaccines And Therapeutics Market size was valued at USD 6.84 billion in 2025 and is estimated to grow from USD 5.17 billion in 2026 to reach USD 11.88 billion by 2031, at a CAGR of 18.08% during the forecast period (2026-2031).

The mRNA vaccine and therapeutics market is transitioning from an emergency-centric model to a broader platform focused on oncology, rare diseases, and autoimmune disorders as clinical data matures and reimbursement frameworks evolve. This expansion is reinforced by public funding for next-generation modalities, dedicated regulatory pathways that facilitate faster reviews, and rising investment in scalable manufacturing. Developers are strengthening delivery science and antigen design to improve durability and safety while lowering cold-chain exposure in low-resource settings. Private channels are expanding as cancer and rare-disease programs reach late-stage trials and move into hospital networks and specialty pharmacies. The mRNA vaccine and therapeutics market is also benefiting from sovereign manufacturing agendas that reduce supply risk and foster regional resilience.

Key Report Takeaways

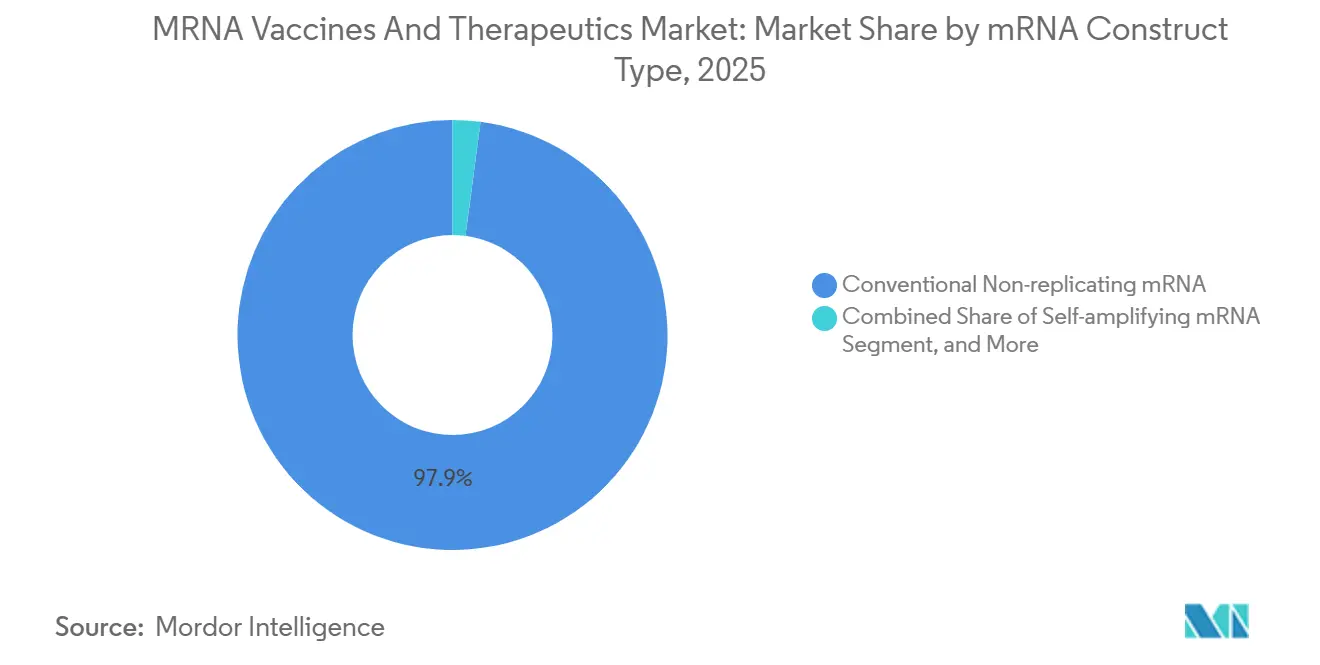

- By mRNA construct type, conventional non-replicating mRNA led with 97.92% of the mRNA vaccines and therapeutics market share in 2025, while circular mRNA is projected to advance at a 130.01% CAGR through 2031.

- By therapeutic area, infectious diseases accounted for 99.42% of the mRNA vaccines and therapeutics market size in 2025, whereas autoimmune disorders is poised for the fastest growth at 171.16% CAGR to 2031.

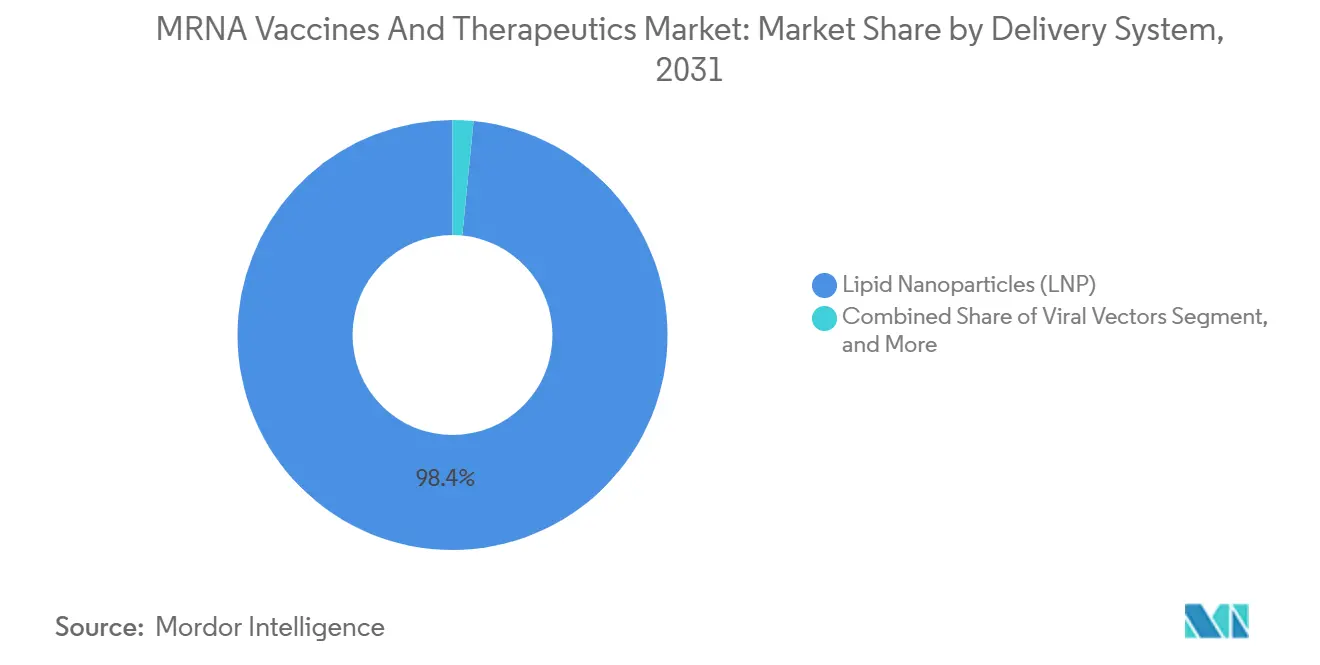

- By delivery system, lipid nanoparticles is expected to hold 98.44% revenue share in 2031; polymer-based nanocarriers exhibit the highest forecast CAGR at 148.64% between 2027 and 2031.

- By distribution channel, public procurement captured 71.52% of 2025 revenue, while the private channel is set to expand at a 32.73% CAGR through 2031.

- By geography, North America commanded 61.11% share in 2025; Asia-Pacific is projected to grow fastest at a 18.71% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global MRNA Vaccines And Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Pandemic-preparedness demand surge | +2.8% | Global, with highest intensity in North America & EU | Medium term (2-4 years) |

| Rising chronic and infectious-disease burden | +3.1% | Global, APAC and MEA showing accelerated growth | Long term (≥ 4 years) |

| Government and venture R&D funding escalation | +2.5% | North America, EU, China | Medium term (2-4 years) |

| Commercial proof-of-concept post-COVID-19 | +3.4% | Global | Short term (≤ 2 years) |

| AI-driven payload design accelerates pipeline | +1.9% | North America, EU, select APAC hubs | Long term (≥ 4 years) |

| Distributed modular manufacturing hubs in lmics | +2.2% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pandemic-Preparedness Demand Surge

Government preparedness funding sustains the mRNA vaccines and therapeutics market as health agencies look beyond COVID-19 to influenza, mpox, and tuberculosis. BARDA’s USD 176 million award to Moderna for an H5 influenza candidate anchors a multiyear procurement roadmap. [1]Moderna, Inc., "Moderna Receives U.S. FDA Approval for RSV Vaccine mRESVIA," modernatx.com CEPI followed with a USD 145 million facility commitment that enables BioNTech to co-locate fill-finish capabilities for malaria antigens in Rwanda. Shifting from reactive procurement to proactive capacity building, governments are now backing platforms that can swiftly adapt to new antigens. In fiscal 2025, the U.S. Biomedical Advanced Research and Development Authority allocated USD 1.2 billion for next-generation vaccine platforms, focusing on mRNA initiatives targeting influenza and other high-consequence pathogens. Meanwhile, the European Health Emergency Preparedness and Response Authority reserved EUR 6 billion for the 2022 to 2027 period. They supported regional mRNA hubs in Poland, Spain, and Romania, each designed to produce 50 million doses within six months of identifying a pathogen.[2]Moderna, Inc., "Moderna Receives Project Award through BARDA's Rapid Response Partnership Vehicle Consortium to Accelerate Development of mRNA-based Pandemic Influenza Vaccine," modernatx.com These strategic moves not only extend planning horizons but also solidify multi-year supply commitments, even as the urgency of COVID-19 volumes begins to wane. Positioned to cater to stockpile strategies and seasonal campaigns against respiratory viruses, the mRNA vaccine and therapeutics market is finding its footing as national agencies refine their pandemic strategies. Furthermore, the framework of advance contracting and readiness funding strengthens early-stage programs, ensuring they can be fast-tracked in response to heightened threat levels.

Rising Chronic and Infectious-Disease Burden

As antimicrobial resistance trends intensify, the urgency for vaccine development against certain bacterial threats grows. Partnerships, including a notable collaboration between BioNTech and the Bill & Melinda Gates Foundation, are stepping up efforts. In 2024, they unveiled a USD 100 million initiative, propelling tuberculosis and malaria mRNA candidates into Phase 1 trials in early 2025, with locations set in Rwanda and Tanzania. Projections from the International Agency for Research on Cancer highlight a burgeoning treatment pool for cancer, underscoring the significance of both personalized and readily available mRNA immunotherapies. Furthermore, interim data from Moderna’s mRNA-4157, when combined with pembrolizumab, showcased a promising 44% reduction in the risk of recurrence or death for high-risk melanoma patients. This finding not only validates the therapeutic potential of mRNA beyond infectious diseases but also signals a broader expansion in the mRNA vaccine and therapeutics market. Developers are now keenly focusing on preventive vaccines for persistent pathogens and therapeutic solutions for prevalent cancers.

Government and Venture R&D Funding Escalation

Sovereign funds and blue-chip investors are amplifying early-stage capital flows. The UK pledged GBP 129 million to BioNTech for genomic-driven cell therapies, while Australia’s RNA Blueprint estimates an USD 8 billion GDP contribution by 2033, backed by state grants to Aurora Biosynthetics. Private placements remain robust; Exsilio Biotech launched with USD 82 million, and RNAimmune has raised USD 39.35 million to date. This blended financing model shortens cash runway constraints that often impede first-in-class programs. In 2025, public research funding for mRNA science saw a significant boost, with the U.S. National Institutes of Health (NIH) disbursing a substantial USD 450 million. This funding, channeled through an mRNA Research Network, focuses on areas like circular mRNA, trans-amplifying designs, and innovative carriers. These NIH-backed programs are designed to bridge the gap between academic laboratories and biotech firms, accelerating the journey from discovery to first-in-human studies. Thanks to this enhanced infrastructure, the timeline from selecting an antigen to achieving clinical proof has been notably shortened, especially in fields like oncology and infectious diseases.

Commercial proof-of-concept post-COVID-19

Regulators are issuing record numbers of breakthrough and priority-review designations for mRNA products, converting scientific promise into reliable commercial cashflows. The FDA cleared Moderna’s RSV vaccine for adults 18-59 in June 2025, extending the brand family beyond its original 60+ indication. Japan’s approval of ARCT-154, the first self-amplifying mRNA for SARS-CoV-2, signaled Asia’s willingness to adopt novel constructs. These milestones give payers and investors tangible reference points for reimbursement, accelerating pipeline valuation upgrades across the mRNA vaccines and therapeutics market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cold-chain and stringent regulatory compliance | -1.4% | Global, acute in APAC and MEA | Medium term (2-4 years) |

| Elevated production cost & scale-up complexity | -1.6% | Global | Short term (≤ 2 years) |

| Imminent expiry of pandemic APAs creates demand cliff | -2.1% | North America, EU | Short term (≤ 2 years) |

| Public scrutiny of LNP toxicity profiles | -0.9% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain and Stringent Regulatory Compliance

Deep-freeze distribution still demands −20 °C to −80 °C storage for many formulations, stressing logistics in equatorial climates. Japanese developers are testing thermostable excipients that hold potency for 14 days at 8 °C, yet commercial rollout remains nascent. On the regulatory front, the FDA’s updated CMC guidance mandates granular reporting on process analytics and critical quality attributes, thereby extending dossier preparation timelines. While the agency’s Platform Designation label offers accelerated reviews, only a handful of applicants have secured it to date, limiting near-term relief. [3]Matthew O’Brien Laramy, "Chemistry, manufacturing and controls strategies for using novel excipients in lipid nanoparticles," Nature Nanotechnology, nature.com

Elevated Production Cost & Scale-Up Complexity

Cap-intensive facilities and bespoke raw materials keep cost of goods above USD 2 per dose for newer constructs, compared with sub-USD 1 for traditional vaccines. Continuous manufacturing can trim unit cost by 32%, but the upfront automation expense deters mid-tier entrants. Emerging-market plants also grapple with talent shortages in analytical development, prompting reliance on costly expatriate expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By mRNA Construct Type: Self-Amplifying Variants Gain Traction

The mRNA vaccines and therapeutics market size for construct types remains dominated by conventional non-replicating formats. This conventional non-replicating mRNA retained 97.92% share in 2025 because existing facilities, regulatory precedents, and validated analytical assays minimize scale-up friction. Demand continues in RSV and influenza boosters, preserving baseline revenue even as competitive pressure mounts. Circular mRNA is expected to accelerate at 130.01% CAGR between 2027 and 2031 owing to its lower dose requirement and improved antigen persistence, which collectively lower per-patient treatment cost. Japan’s approval of ARCT-154 created a regulatory template that other jurisdictions are now studying, reducing the perceived development risk for startups.

Second-generation circular mRNA is gathering momentum despite limited commercial exposure. Industry observers expect circular modalities to supplant linear templates within a decade because they resist exonuclease degradation and therefore prolong protein expression windows. Parallel academic research at Nagoya University presents disease-cell-selective translation initiation, hinting at oncology applications with minimal off-target toxicity. Collectively, these innovations diversify the mRNA vaccines and therapeutics market and attract platform licensing deals from companies that lack internal RNA chemistry expertise.

By Therapeutic Area: Oncology Pipelines Accelerate

Infectious diseases remained the primary revenue pillar, securing 99.42% of 2025 turnover as COVID-19 boosters, RSV shots, and pediatric combination vaccines filled public-sector procurement pipelines. Beyond respiratory viruses, norovirus and cytomegalovirus programs are progressing toward late-stage trials, reinforcing the volume outlook. Yet the autoimmune disorders segment is expected to register the fastest expansion at 171.16% CAGR, catalyzed by the milestone 49% reduction in melanoma recurrence achieved by mRNA-4157 plus pembrolizumab. FDA Breakthrough Therapy Designation for that regimen accelerated trial enrollment in lung and bladder cancers, broadening addressable patient pools.

The oncology wave is also geo-diversifying. Likang Life Sciences received FDA IND clearance for a personalized neoantigen vaccine manufactured at one-tenth the cost of comparable Western protocols. Chinese hospitals are piloting these regimens under private payment models, signaling payer flexibility when efficacy endpoints are compelling. Autoimmune research is following a similar trajectory; Cartesian Therapeutics’ Descartes-08 reached Phase 3 in myasthenia gravis, and OSE Immunotherapeutics is advancing IL-35 tolerizing constructs for autoimmune hepatitis. Each success story builds confidence that the mRNA vaccines and therapeutics market can sustain growth outside its infectious-disease origins.

By Delivery System: Viral Vectors Emerge for In-Vivo Applications

Lipid nanoparticles are expected to command 98.44% share in 2031 because existing approval dossiers and established raw-material supply chains simplify regulatory filings. Formulation scientists are optimizing ionizable lipid pKa values to bias distribution toward lymph-node resident dendritic cells, thereby enhancing vaccine potency. Blood-brain barrier-penetrating LNPs have achieved 12-fold higher central nervous system transfection compared with first-generation materials, opening neurology indications. The Polymer-based Nanocarriers segment, despite historical safety concerns, is expected to exhibit 148.64% CAGR (2027 - 2031) through engineered capsids that evade preexisting immunity and deliver mRNA cargo efficiently to solid tumors.

Concurrently, polymeric nanoparticles and “naked” mRNA delivered via needle-free jet devices are gaining research traction for chronic indications. Early data reveal comparable antigen expression with reduced systemic reactogenicity, an attribute valuable for repeat dosing schedules envisioned in oncology maintenance therapies. Continuous-flow microfluidics is further standardizing particle size and encapsulation efficiency at scale, lowering batch-failure risk. These advances sustain competitive differentiation, ensuring sustained capital inflows into delivery technologies within the broader mRNA vaccines and therapeutics market.

By Distribution Channel: Private Networks Scale for Specialty Therapeutics

Public channels captured 71.52% of 2025 revenue because national immunization programs bulk-procure pandemic stockpiles and seasonal boosters. The United States’ Vaccines for Children program now covers mRNA influenza shots, further entrenching public volume dominance. However, the private segment is projected to grow at 32.73% CAGR as personalized cancer vaccines and rare-disease therapeutics require specialist infusion centers outside public infrastructure. Oncology networks such as Memorial Sloan Kettering are integrating point-of-care sequencing with rapid mRNA synthesis to deliver individualized vaccines within six weeks of tumor biopsy. This workflow aligns poorly with public tender cycles.

Asia-Pacific private insurers are beginning to reimburse mRNA vaccines against endemic diseases like dengue, particularly in Singapore and Malaysia, where out-of-pocket expenditure is high. Meanwhile, Chinese private clinics market personalized neoantigen cocktails at pricing that undercuts Western equivalents by 99%, reshaping competitive pricing benchmarks. These developments suggest that the mRNA vaccines and therapeutics market will see channel diversification that mirrors the precision-medicine shift evident in other biologics segments.

Geography Analysis

North America accounted for 61.11% of global revenue in 2025, driven by robust federal funding, dense contract manufacturing networks, and a regulatory environment that first validated mRNA technology. BARDA’s influenza contract and Blackstone’s multibillion-dollar R&D support underscore institutional confidence. Ongoing investment in modular plants across Texas and Massachusetts keeps capacity flexible for both pandemic surges and therapeutic rollouts, sustaining the regional leadership position.

Asia-Pacific is expected to register a 18.71% CAGR from 2026 to 2031, the fastest across all regions. Regulatory agility is a key driver: Japan approved the first self-amplifying mRNA vaccine, and Singapore has issued guidance treating circular RNA as an incremental modification rather than a brand-new modality, thereby shortening review cycles. Governments are also funding domestic supply chains. Australia’s RNA Blueprint forecasts an AUD 8 billion contribution to GDP, and South Korea’s GC Biopharma is co-developing autoimmune candidates with Immetas. Cost-innovation dynamics are particularly acute in China, where localized manufacturing is delivering individualized cancer vaccines at prices 99% below Western benchmarks, effectively expanding patient access and challenging incumbent pricing strategies across the mRNA vaccines and therapeutics market.

Europe maintains steady mid-teens growth, supported by strategic industrial policy. BioNTech committed GBP 1 billion for two UK R&D hubs specializing in genomics and regenerative medicine, a project subsidized by GBP 129 million in government grants. CEPI’s USD 145 million facility in Rwanda, although located in Africa, employs European process technology and quality-management protocols, extending the continent’s influence. Meanwhile, Latin America is leveraging PAHO’s capacity-building program, which equips plants in Argentina and Brazil with modular cleanrooms and knowledge-transfer packages funded by Canada. These initiatives collectively diffuse manufacturing know-how and reduce single-region supply dependence, boosting resilience across the mRNA vaccines and therapeutics market.

Competitive Landscape

Dominance by Moderna and Pfizer/BioNTech persists, yet recent PTAB invalidations of key Moderna claims have eroded patent fortifications, inviting fresh competition. GSK’s entry into litigation over Novartis-originated patents signals the incumbent's ambition to capture share. Market strategies have shifted from single-asset development to platform monetization, exemplified by Moderna’s plan to launch ten products by 2027 across respiratory, oncology, and rare-disease segments. Merck’s co-development deal on mRNA-4157 affirms the value of combination immuno-oncology approaches.

Emerging players are filling technology gaps. Exsilio Biotech focuses on bespoke genetic-medicine payloads using proprietary circular mRNA backbones. Radar Therapeutics is engineering structure-based design algorithms that marry AI with high-throughput screening to shorten construct iteration cycles. Outsourcing specialists such as Vernal Biosciences offer GMP-grade plasmid and mRNA cartridges, easing entry barriers for virtual biotech firms and academic spinouts. Delivery-system differentiation is another battleground; companies developing blood-brain barrier-crossing LNPs or synthetic ssRNA+ virus vectors gain privileged access to central nervous system or solid-tumor indications not readily achievable with first-generation particles.

Cost leadership is emerging as a decisive competitive variable, especially in oncology, where treatment courses can exceed USD 100,000 in Western markets. Chinese manufacturers achieve 99% cost reductions by integrating continuous manufacturing with local raw-material sourcing, compelling incumbents to revisit their pricing models. Continuous manufacturing and AI-driven optimization, therefore, play dual roles, improving margins for established players and offering disruptive entry points for new challengers, reshaping the medium-term trajectory of the mRNA vaccines and therapeutics market.

MRNA Vaccines And Therapeutics Industry Leaders

-

Arcturus Therapeutics Holdings Inc.

-

BioNTech SE

-

Daiichi Sankyo Company Ltd.

-

Moderna Inc.

-

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The UK Medicines and Healthcare products Regulatory Agency (MHRA) has approved Moderna's updated COVID-19 mRNA vaccine, Spikevax, targeting the SARS-CoV-2 LP.8.1 variant. This approval applies to adults and children aged six months and older.

- February 2026: Ethris GmbH, a clinical-stage biotechnology company specializing in next-generation RNA therapeutics and vaccines, has partnered with the German Center for Infection Research (DZIF). This collaboration aims to combine Ethris' mRNA technology with DZIF's expertise in vaccine research to address a wide range of pathogens, including viruses, bacteria, and parasites.

- January 2026: Insight Therapeutics announced the "Next-generation mRNA Vaccines Against Complex Pathogens: From Antigen Selection to Clinical Translation" conference, scheduled for March 25–26, 2026, in Leuven, Belgium.

- February 2026: BioNTech has received Fast Track designation from the U.S. Food and Drug Administration (FDA) for its investigational mRNA cancer immunotherapy, BNT113.

- November 2025: Moderna has expanded its U.S. manufacturing capabilities by onshoring Drug Product manufacturing to its Moderna Technology Center (MTC) in Norwood, Massachusetts.

Global MRNA Vaccines And Therapeutics Market Report Scope

As per the scope of the report, mRNA vaccines and therapeutics enable the combination of desirable immunological properties. These are prepared in laboratories using mammalian cells and injected into the target's body to trigger virus-detecting immune sensors and produce viral antigen proteins within the cells. This enhances the body's immune system by improving B- and T-cell responses.

The mRNA vaccines and therapeutics market is segmented by mRNA construct type, application, delivery system, distribution channel, and geography. mRNA construct type, the market is segmented by self-amplifying mRNA-based vaccines and conventional non-amplifying mRNA-based vaccines. By application, the market is segmented by cancer, infectious diseases, autoimmune diseases, and other applications. By delivery system, the market is segmented into lipid nanoparticles (LNP), polymer-based nanocarriers, cationic nanoemulsions, viral vectors, physical methods, and others. By distribution channel, the market is segmented into public and private. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Conventional Non-replicating mRNA |

| Self-amplifying mRNA |

| Circular mRNA |

| Trans-amplifying mRNA |

| Others |

| Infectious Diseases |

| Oncology |

| Autoimmune Disorders |

| Rare & Genetic Disorders |

| Others |

| Lipid Nanoparticles (LNP) |

| Polymer-based Nanocarriers |

| Cationic Nano-emulsions |

| Viral Vectors |

| Physical Methods |

| Others |

| Public |

| Private |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By mRNA Construct Type | Conventional Non-replicating mRNA | |

| Self-amplifying mRNA | ||

| Circular mRNA | ||

| Trans-amplifying mRNA | ||

| Others | ||

| By Therapeutic Area | Infectious Diseases | |

| Oncology | ||

| Autoimmune Disorders | ||

| Rare & Genetic Disorders | ||

| Others | ||

| By Delivery System | Lipid Nanoparticles (LNP) | |

| Polymer-based Nanocarriers | ||

| Cationic Nano-emulsions | ||

| Viral Vectors | ||

| Physical Methods | ||

| Others | ||

| By Distribution Channel | Public | |

| Private | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the mRNA vaccines and therapeutics market?

The mRNA vaccines and therapeutics market size reached USD 5.17 billion in 2026 and is forecast to grow to USD 11.8 billion by 2031.

Which mRNA construct type is growing fastest?

Circular mRNA leads growth with a projected 130.01% CAGR through 2031, thanks to its lower dose requirement and robust immune response profile.

Why is oncology attracting so much attention in mRNA pipelines?

Breakthrough results such as the 49% reduction in melanoma recurrence from mRNA-4157 plus pembrolizumab have validated the modality, lifting oncology to a 17.20% CAGR.

How are manufacturing innovations influencing market expansion?

Modular closed-system and continuous-flow plants cut validation timelines and reduce batch costs, enabling more countries to build local production and supporting global market growth.

Which region will grow fastest over the next five years?

Asia-Pacific is expected to expand at a 18.71% CAGR owing to supportive regulation, state funding, and cost-efficient manufacturing models.

What are the main barriers facing new entrants?

The most significant hurdles are cold-chain logistics, complex regulatory compliance, and ongoing lipid-nanoparticle patent disputes that can delay freedom-to-operate decisions.

Page last updated on: