Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

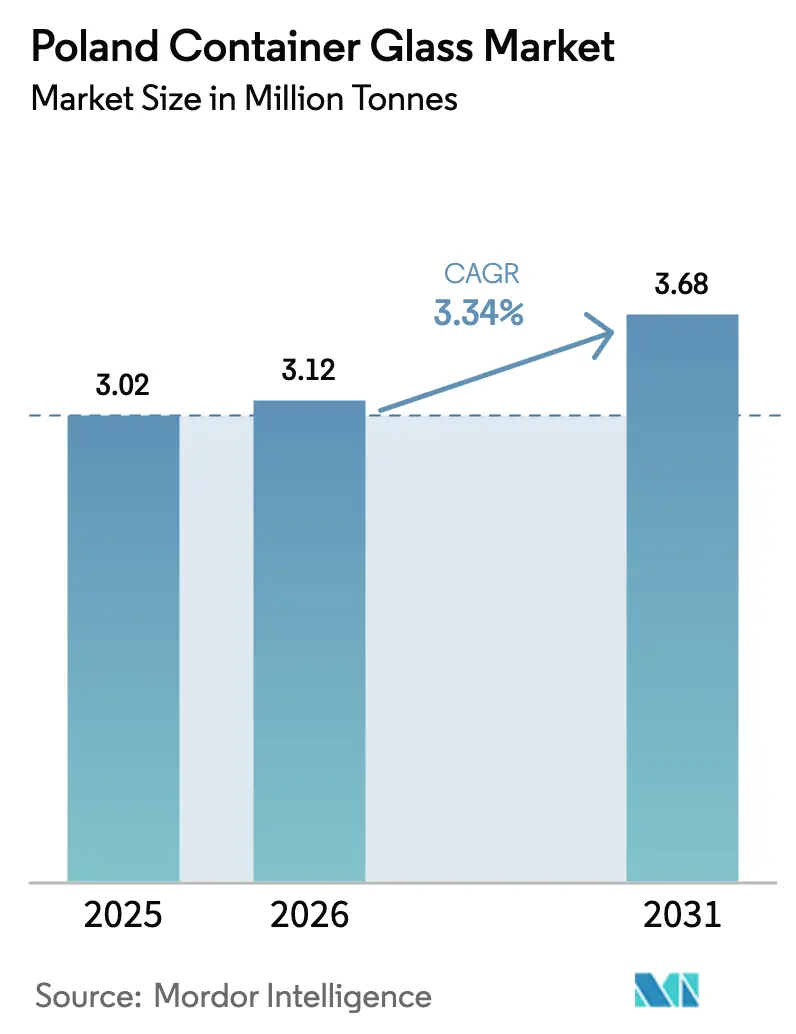

| Base Year Market Size (2025) | 3.02 Million tonnes |

| Market Volume (2026) | 3.12 Million tonnes |

| Market Volume (2031) | 3.68 Million tonnes |

| Growth Rate (2026 - 2031) | 3.34% CAGR |

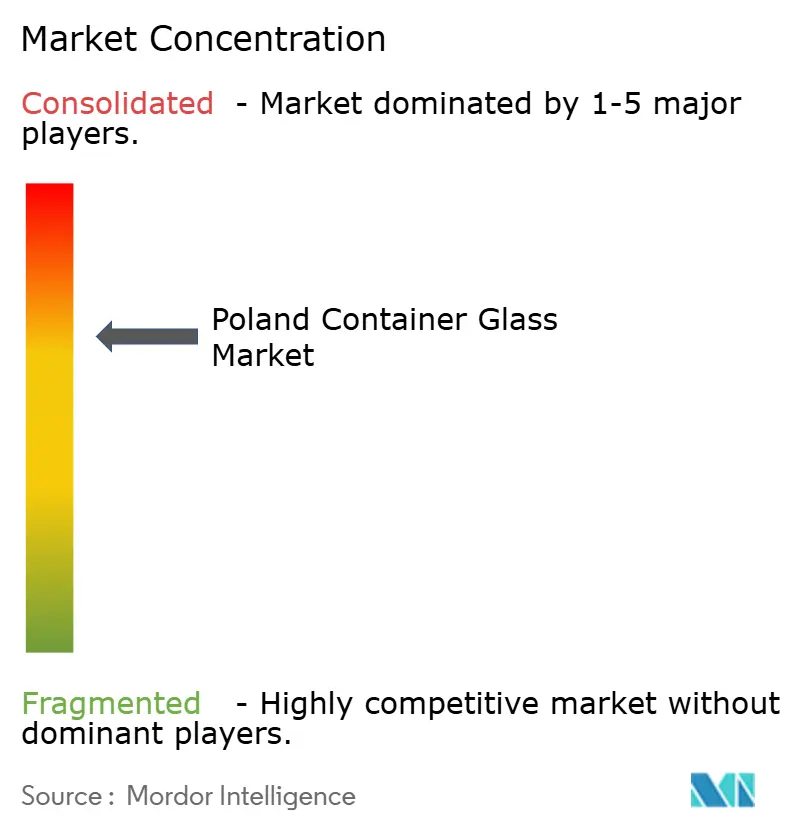

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Container Glass Market Analysis by Mordor Intelligence

The Poland Container Glass Market size was valued at 3.02 million tonnes in 2025 and estimated to grow from 3.12 million tonnes in 2026 to reach 3.68 million tonnes by 2031, at a CAGR of 3.34% during the forecast period (2026-2031). Poland’s position as Europe’s second-largest container glass producer, with more than 1.8 million tonnes of annual capacity, enables domestic manufacturers to serve both the local beverage industry and regional export demand efficiently. The recent implementation of the national deposit return system (DRS) in January 2025 created a PLN 1.00 deposit on refillable glass versus PLN 0.50 on plastic or metal, strengthening structural demand for glass packaging in alcoholic and non-alcoholic beverages. Manufacturers benefit from abundant domestic silica sand, limestone, and soda ash, most notably the Quarzwerke Biała Góra deposit, which reduces raw-material procurement risks and transportation costs. Technological investment in hybrid and fully electric furnaces is improving energy efficiency by 15-20% while cutting emissions up to 60%, partially cushioning the impact of volatile natural-gas prices.

Key Report Takeaways

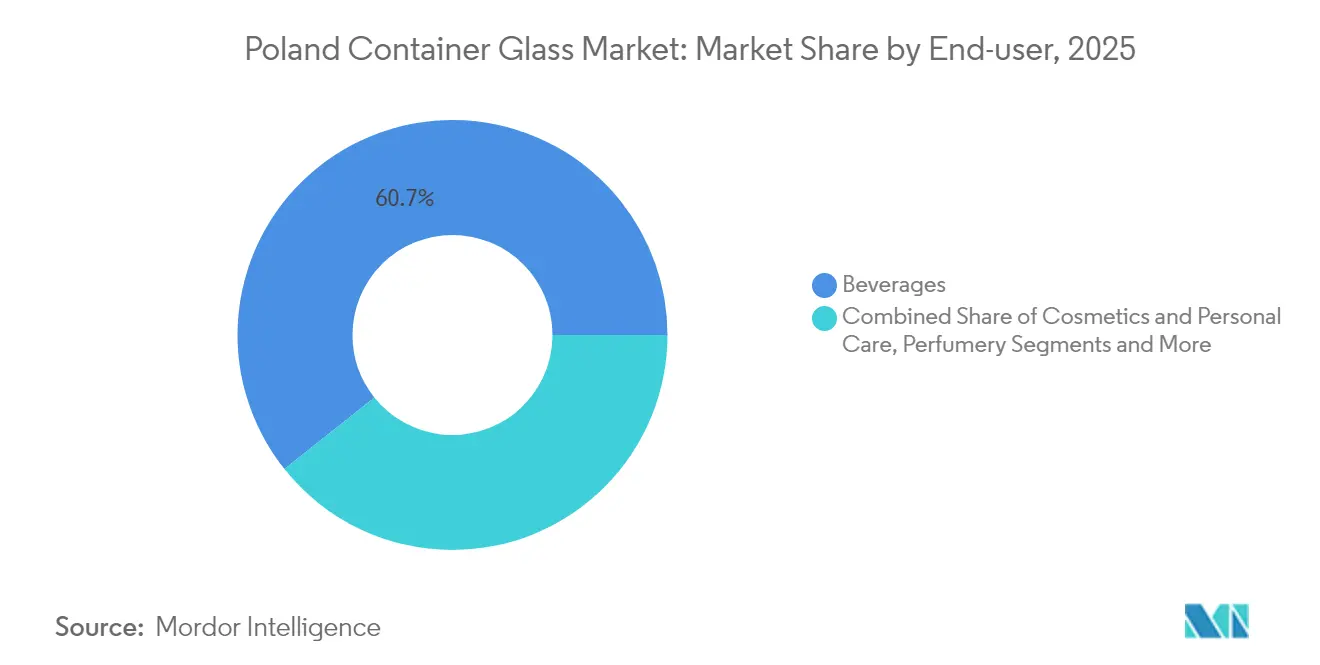

- By end-user, beverages captured 60.72% of the Poland container glass market share in 2025.

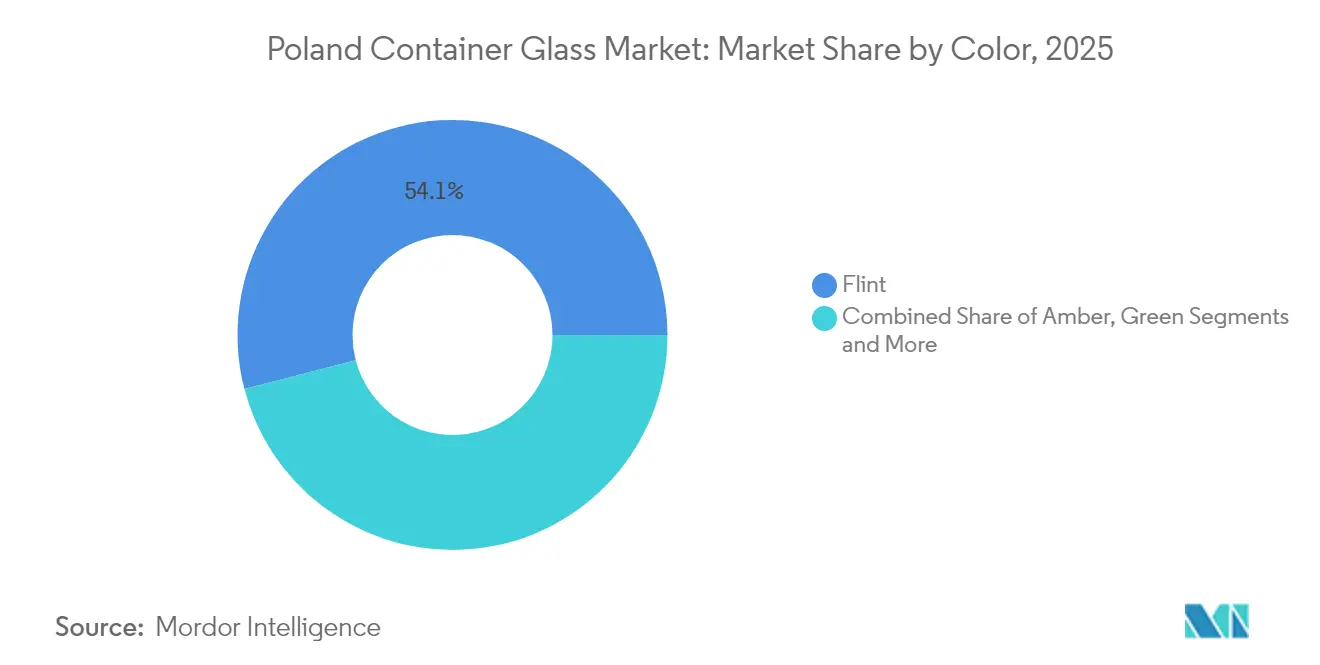

- By color, the Poland container glass market size for amber glass is projected to grow at a 3.84% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export Potential and EU Market Integration | +0.8% | Poland, with spillover to Germany, Czech Republic, and broader EU markets | Medium term (2-4 years) |

| Technological Advancements in Glass Manufacturing | +0.6% | National, with early adoption in Silesia and Greater Poland regions | Long term (≥ 4 years) |

| Government Regulations Supporting Recycling | +0.9% | National, with enhanced impact in major urban centers | Short term (≤ 2 years) |

| Rising Demand for Sustainable Packaging | +0.7% | Global, with concentrated effects in Warsaw, Kraków, and Gdańsk metropolitan areas | Medium term (2-4 years) |

| Growth in Beverage Industry | +0.5% | National, with particular strength in wine-consuming regions | Medium term (2-4 years) |

| Expansion of Cosmetics and Pharmaceuticals | +0.4% | National, with clustering around pharmaceutical manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export Potential and EU Market Integration

Polish producers ship 27.77% of container-glass exports to Germany, benefiting from tariff-free EU trade and lower labor costs that narrow delivered-price gaps with German and Italian rivals. The integrated market gives local plants shorter lead times to large German bottlers, a key advantage as European buyers rebuild inventories after 2024 destocking cycles. O-I’s European revenue fell 7% in Q1 2024, opening share opportunities for cost-competitive Polish suppliers. Alignment with the EU Emissions Trading System simplifies compliance paperwork, allowing Polish exporters to avoid duplicate carbon-accounting costs when shipping within the bloc. OEM proximity also reduces empty-container mileage, cutting freight emissions and logistics spend.

Technological Advancements in Glass Manufacturing

Hybrid melters that combine electric boosting and oxygen-fired burners became operational in Jarosław and Poznań in 2024, delivering 15-20% specific energy savings and enabling flexible batch runs that suit Poland’s growing craft-beverage segment. MAGMA modular furnaces shorten rebuild downtime from 120 days to fewer than 60 days, extending asset life and smoothing cash-flow requirements. Plants now use closed-loop controls to push cullet ratios above 70%, a milestone made possible by the January 2025 DRS surge in returned glass. Energy-efficiency gains translate into CO₂ reductions nearing 60%, supporting corporate net-zero roadmaps and easing ETS credit costs. Automation upgrades, including hot-end inspection cameras, are improving quality yield by 2-3 percentage points and reducing spoilage.

Government Regulations Supporting Recycling

The DRS grants a PLN 1.00 deposit on refillable glass compared with PLN 0.50 on plastic or metal, instantly making refillable glass the most economical choice on a total-cost-of-ownership basis for beverage brand owners. Parallel EU Packaging and Packaging Waste Regulation rules force minimum recycled-content thresholds that favor cullet-rich glass over virgin-plastic packaging.[1]European Commission, “Packaging and Packaging Waste,” europa.eu Energy-cost mitigation delivered through state-subsidized electricity and gas tariffs smooths furnace-fuel bills for qualifying high-usage plants. Environmental fee structures charge PLN 0.64 per kg of particulate and PLN 0.44 per kg of NOₓ released, further incentivizing low-emission furnace retrofits.

Rising Demand for Sustainable Packaging

Poland’s USD 5.48 billion cosmetics market is pivoting to recyclable containers as global beauty conglomerates impose Scope 3 emissions targets on regional sourcing teams. Craft breweries and premium spirits brands opt for glass because of its infinite recyclability and premium shelf appeal, which together strengthen brand storytelling around sustainability. EU eco-design mandates require clear labeling and single-material construction, disqualifying many layered plastic films; glass passes these tests naturally. Retailers in Warsaw, Kraków, and Gdańsk report double-digit growth in private-label SKUs that switched from plastic to glass ahead of new eco-score labeling rules. Corporate ESG frameworks using ISO 14001 certification are now embedding supplier glass-content thresholds in procurement bids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy and Production Costs | -0.7% | National, with concentrated impact in energy-intensive production regions | Short term (≤ 2 years) |

| Competition from Alternative Materials | -0.5% | Global, with particular pressure in dairy and juice packaging segments | Medium term (2-4 years) |

| Environmental Compliance Costs | -0.3% | National, with higher impact in industrial zones subject to stricter emissions monitoring | Long term (≥ 4 years) |

| Volatility in Raw Material Supply | -0.4% | National, with supply chain dependencies on regional sand and soda ash suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy and Production Costs

Energy can account for up to 30% of container-glass manufacturing overhead, and natural-gas spot prices remained volatile in 2024, eroding margins for plants locked into long-term supply contracts. Ardagh Glass Packaging Europe and Africa saw adjusted EBITDA fall 55% in Q1 2024 because fixed-cost absorption declined as throughput fell. EU ETS allowances cost major producers an estimated USD 37 million annually, translating to several euro-cent increases per bottle. Capital expenditure for a single furnace rebuild ranges from USD 10 million to USD 15 million, limiting flexibility to curtail production if demand slips. Although state fuel-price stabilization partially offsets the burden, energy input remains the most significant variable cost.

Competition from Alternative Materials

Fiber-based cartons gained share in German dairy, and Elopak is marketing similar conversions in Polish juice and milk sectors, targeting cost-sensitive mass-market SKUs that traditionally used returnable glass. Metal cans are also pressuring beer and energy-drink volumes thanks to lightweighting and improved recycling logistics. Beauty-category trials with refillable aluminum pods introduce uncertainty for single-use fragrance glass. Meanwhile, polymer suppliers have introduced rPET bottles with enhanced barrier layers that extend shelf life, removing one of glass’s historic advantages in food preservation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Extend Leadership as Cosmetics Accelerate

The beverages segment accounted for 60.72% of Poland's container glass market share in 2025, underpinned by Poland’s thriving beer culture and a wine market that reached 13.1 million 9-liter cases after ten years of 3.7% annual expansion.Non-alcoholic producers, especially regional juice cooperatives, are returning to refillable glass to benefit from the PLN 1.00 deposit, protecting margins as PET resin prices rise. Key breweries in Poznań and Żywiec forged long-term supply contracts with nearby glass plants, locking in cullet supply and smoothing furnace loads. Food processors remain steady buyers of jars for preserved products, benefiting from Poland's container glass market size economies in standard neck-finish formats that support line-speed efficiency.

The cosmetics and personal-care category represents the fastest-growing end-user, forecast at a 3.91% CAGR through 2031, as both domestic and export-oriented beauty brands integrate eco-claims into packaging briefings. Luxury skincare launches in Warsaw department stores feature thick-walled flint glass that accentuates premium textures, while indie brands favor amber for natural-ingredient protection. Pharmacist-owned dermocosmetic lines distributed through apotek channels increasingly specify small-format amber glass that fits shelf-ready packaging dimensions. Poland's container glass industry innovators offer decoration services, including ink-jet printing and acid-etch finishes, meeting rising personalization needs without compromising recyclability. Export-oriented perfumery producers in Kraków capitalize on the market’s integrated logistics to ship filled bottles quickly to German and Scandinavian distributors.

By Color: Dominance of Flint, Momentum in Amber

Flint retained 54.05% of Poland's container glass market size in 2025 as premium liquor and clear-label wine APIs demand transparency for branding. High-clarity flint glass leverages advanced batch recipes with low iron content sourced from Biała Góra sand. Spirits producers often select heavyweight shapes, relying on flint’s sparkle to project quality. Machine upgrades at Jarosław now enable rapid mold changeovers, allowing glasshouses to service both high-volume vodka SKUs and low-volume craft distillates without long downtime. Flint cullet availability improved sharply after DRS launch, stabilizing batch consistency and lowering furnace energy demand by up to 2% per percentage-point cullet gain.

Amber glass is growing at a 3.84% CAGR, with pharmaceutical and craft-beer applications valuing its UV-barrier up to 400 nm that guards against vitamin degradation and hop spoilage. Poland’s life-sciences clusters near Łódź and Poznań are scaling OTC syrup lines that require 125-ml amber bottles. Craft brewers deploy long-neck amber bottles that align with global category cues and help differentiate from aluminum can competitors. Process optimization has pushed amber colorant dosing accuracy to sub-ppm ranges, minimizing off-tone rejects and boosting line yield. Green glass remains significant for traditional Riesling and Veltliner wines aimed at the Central European market, but usage is flat as bag-in-box gains share among price-conscious consumers. Specialty tints such as cobalt blue occupy niche skincare markets and command higher margins, yet volumes are too small to influence furnace scheduling beyond opportunistic runs.

Geography Analysis

Poland lies at the center of European supply chains, and 27.77% of Poland's container glass market exports head to Germany, leveraging zero tariffs and one-day truck transit times to Munich, Berlin, and Hamburg bottlers. Czech, Slovak, and Baltic beverage fillers make up another sizeable share, attracted by competitive Polish freight rates and flexible order quantities. The Silesia region hosts a dense cluster of sand quarries and natural-gas pipelines that feed high-capacity furnaces, giving the area a cost-of-production edge. Meanwhile, Greater Poland’s proximity to Baltic ports enables direct containerized shipments of filled products to Scandinavian markets within 48 hours.

Domestically, the DRS that started in January 2025 improves glass collection logistics nationwide, underpinning rising cullet ratios that reduce energy intensity at furnaces from Kraków to Szczecin. Major retail chains provide 20,000 reverse-vending machines, enhancing post-consumer return rates and slashing inbound-raw-material trucking distances. Urban centers such as Warsaw and Wrocław observe higher cosmetics-package throughput, consistent with income-driven demand for premium skincare housed in glass. Pharmaceutical glass demand is strongest near the Łódź-Poznań corridor, where contract-manufacturing organizations operate GMP-compliant lines.

Poland container glass market participants also benefit from government energy-support schemes granting discounted tariffs to energy-intensive plants, easing the shock of natural-gas price spikes that battered Western European peers in late 2024. EU border-adjustment carbon mechanisms do not apply to intra-EU trade, so Polish shipments circumvent taxes facing Turkish or Ukrainian competitors, sustaining volume momentum into 2026. Infrastructure enhancements, including a new east-west highway spur, will cut lead times to the Czech border by 90 minutes when fully opened in 2027, further strengthening export competitiveness.

Competitive Landscape

Poland's container glass market features O-I Glass, Verallia, and Ardagh Glass as anchor multinationals, supplemented by regional specialists such as BA Glass Poland and CP Glass. O-I operates Jarosław and Poznań plants with a combined capacity topping 800 kt, and its EUR 400 million senior notes offering in May 2024 earmarks funds for furnace electrification and MAGMA pilot lines.[3]O-I Glass, “€400 Million Senior Notes Offering,” o-i.comVerallia invested EUR 34.6 million in H1 2024 to upgrade Northern and Eastern Europe operations, signaling a long-term commitment to the Polish asset base despite volume softness. Ardagh’s 55% EBITDA drop in Q1 2024 triggered efficiency reviews of Polish furnaces, accelerating digital controls to improve pull-rate utilization.

Local manufacturers are carving out niches via advanced decoration technologies. Dekorglass in Działdowo operates multi-pass screen-printing lines capable of producing 8-color designs at 450 bottles per minute for craft-gin exporters. Stoelzle Częstochowa specializes in perfumery bottles with proprietary engraving molds, capturing high margins by supplying French luxury houses. Forglass, a domestic furnace-engineering firm, licenses oxy-fuel combustion chambers to regional plants, deepening local value capture in capex spend. BA Glass Poland improves flint-glass clarity through continuous oxygen-bubble removal systems, appealing to vodka brands that demand pristine transparency.

Strategic directives revolve around decarbonization and supply-chain agility. Producers prioritize cullet procurement contracts linked to DRS flows, ensuring stable quality and pricing. Hybrid furnace pilots target production of smaller lot sizes, matching demand variability in seasonal craft-beverage and limited-edition cosmetics packaging. ESG metrics influence buyer scorecards; hence, glassmakers publicize annual sustainability reports detailing. Simultaneously, portfolio rationalization sees multinationals shutter under-utilized European furnaces and concentrate output in efficient Polish hubs, raising Poland’s share of group production over the forecast horizon.

Poland Container Glass Industry Leaders

Ardagh Glass S.A.

Stoelzle Glass Group

O-I Glass, Inc.

Gerresheimer AG

Verallia Polska Sp. z o.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TricorBraun agreed to acquire Euroglas and Glaspack, broadening DACH-region distribution coverage that could channel additional order volumes toward Polish glassmakers.

- January 2025: Poland’s DRS took effect, setting PLN 1.00 deposits on refillable glass versus PLN 0.50 on plastic and metal containers.

- May 2024: O-I European Group issued EUR 400 million (USD 432 million) in senior notes to fund technology upgrades across its European plants, including Polish facilities.

- April 2024: Ardagh Glass Packaging Europe and Africa reported USD 644 million revenue in Q1 2024, down 7% YoY, with EBITDA tumbling 55% as input-cost pass-through lagged.

Poland Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

The poland container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large will Poland’s container-glass volume be in 2031?

Forecasts indicate 3.68 million tonnes by 2031, reflecting a 3.34% CAGR from 2026.

Which end-user generates the most demand?

Beverages remain dominant, delivering 60.72% of 2025 volume and benefiting most from the deposit return system.

Why is amber glass growing faster than other colors?

Pharmaceutical UV-protection needs and the craft-beer boom drive amber demand, underpinning its 3.84% CAGR outlook.

How does the national DRS influence glass demand?

The PLN 1.00 deposit on refillable bottles materially lowers lifecycle costs, boosting refillable-glass orders for beverage producers.

Which companies lead furnace-modernization investments?

O-I, Verallia and Ardagh are investing in hybrid and electric furnaces to trim energy use and meet EU decarbonization targets.

Page last updated on: