Germany Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.45 Billion |

| Market Size (2026) | USD 6.57 Billion |

| Market Size (2031) | USD 7.12 Billion |

| Growth Rate (2026 - 2031) | 1.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Containerboard Market Analysis by Mordor Intelligence

The Germany containerboard market size is expected to increase from USD 6.45 billion in 2025 to USD 6.57 billion in 2026 and reach USD 7.12 billion by 2031, growing at a CAGR of 1.62% over 2026-2031. Germany remained the largest corrugated board economy in Europe, and output reached 7.414 billion m² in 2024 even as industry revenue fell 8.2% after price normalization from the 2022 energy shock. The Germany containerboard market is holding up because online retail, food logistics, and retail replenishment still require high-repeat corrugated supply, which is limiting the effect of softer industrial ordering. The Germany containerboard market is also being shaped by stronger recycled-fiber acceptance, wider use of fiber-based transport formats, and growing adoption of lighter grades on automated corrugator lines. Pricing and mill margins remain under pressure because German producers still face elevated gas and recovered-fiber costs, and several mills continued to seek price increases through 2025 and early 2026. The Germany containerboard market is therefore moving toward growth led by specification complexity, food and parcel formats, and scale-driven integration rather than a broad industrial rebound.

Key Report Takeaways

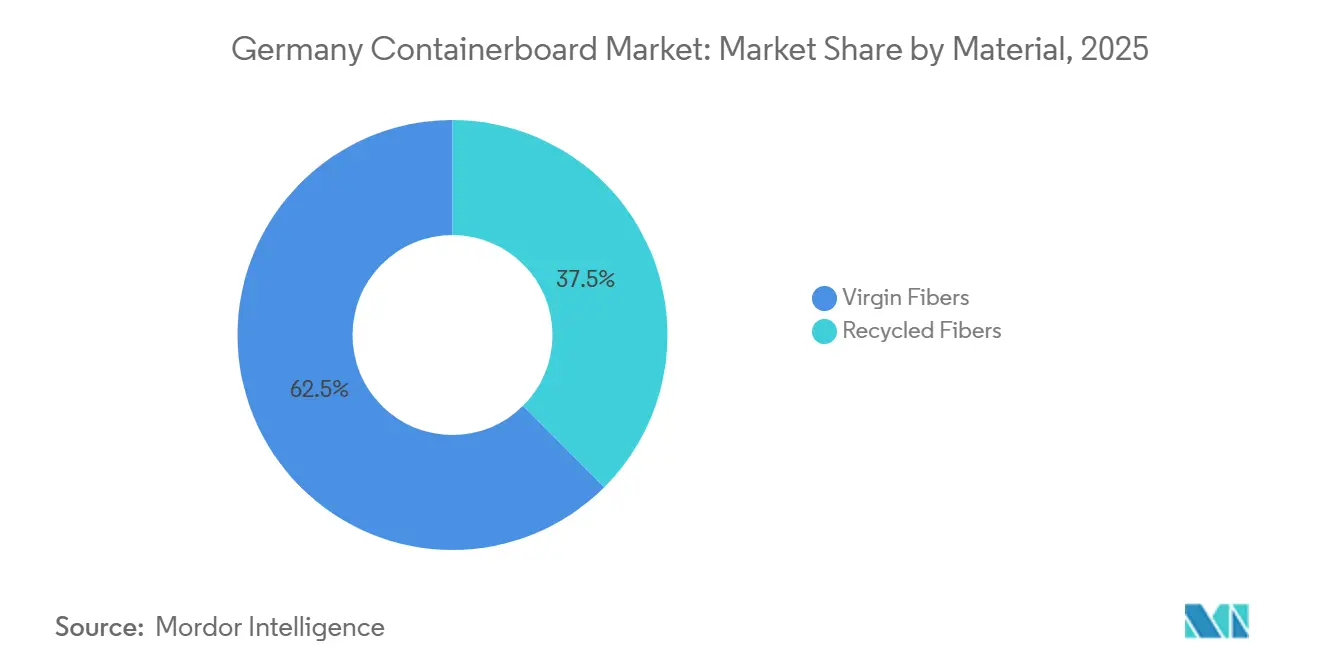

- By material, virgin fibers captured with 62.48% of the Germany containerboard market share in 2025.

- By product type, the Germany containerboard market size for testliners is projected to grow at a 2.25% CAGR to 2031.

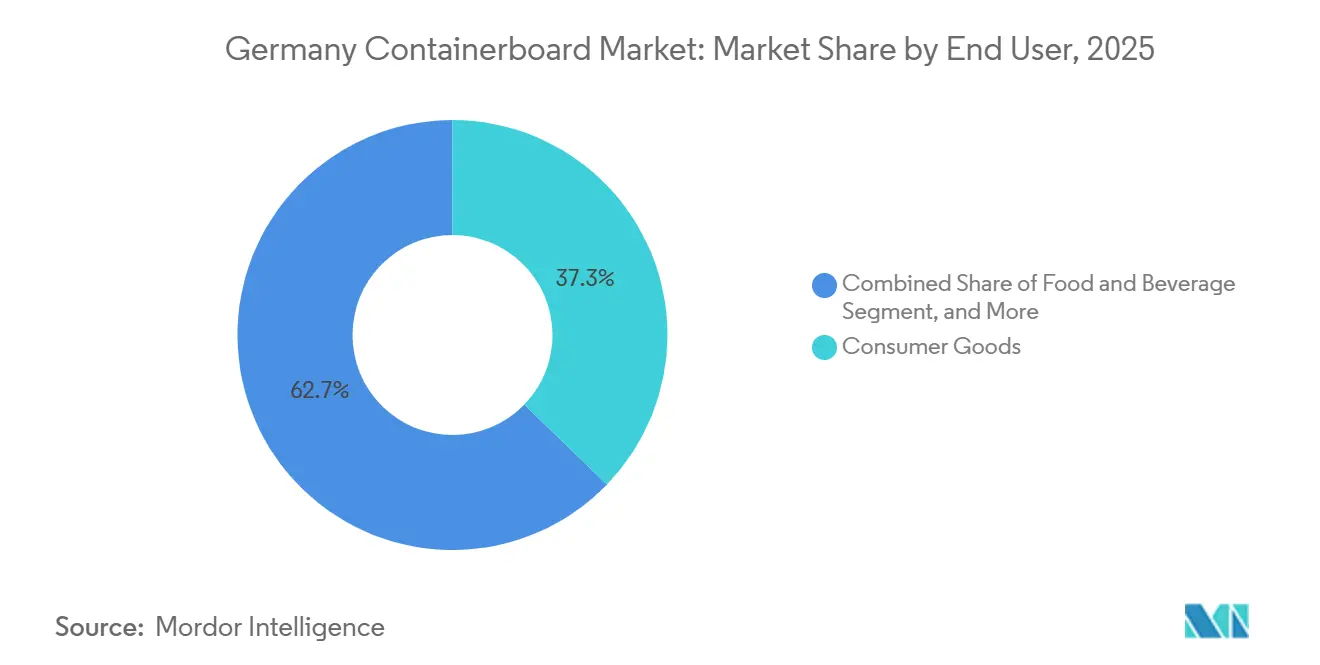

- By end user, consumer goods captured with 37.25% of the Germany containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce and Omnichannel Fulfillment Demand | +0.5% | National, with concentration in Rhine-Ruhr, Munich, Hamburg, and Frankfurt metropolitan logistics zones | Short term (≤ 2 years) |

| Plastic-To-Paper Substitution in Secondary and Transit Packaging | +0.4% | National and Western Europe, Germany as a lead adoption market with spillover to France, Benelux, and Nordic markets | Medium term (2-4 years) |

| Food and Beverage Shipment Hygiene and Shelf-Ready Needs | +0.3% | National, with spillover to DACH and Benelux export markets | Short term (≤ 2 years) |

| High Recycled-Fiber Acceptance in German Packaging Procurement | +0.2% | National, with early adoption visible in Frankfurt, Düsseldorf, and Hamburg logistics hubs | Medium term (2-4 years) |

| Lightweight Sub-100 Gsm Grade Adoption on Automated Corrugators | +0.2% | National and Western Europe, strongest in automated warehousing and parcel processing clusters | Medium term (2-4 years) |

| Alternative-Fiber Blending for White-Top and Specialty Liner Innovation | +0.1% | National, with early R&D activity at Schwedt/Oder and Schrobenhausen production sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce and Omnichannel Fulfillment Demand

Germany's online retail sector rose to EUR 92.4 billion (USD 100 billion) in 2025, up 4% from 2024, with marketplace platforms driving growth while non-marketplace channels declined on average by 5.4%. This pattern is concentrating corrugated demand around a smaller set of large logistics operators, which raises the value of short lead times and tightly configured lightweight formats in the German containerboard market. Corrugated board held a 90% share of German e-commerce packaging in 2024 because it remained strong in protection, recyclability, and automation compatibility. Germany's e-commerce penetration reached 87% in 2024, average parcel deliveries were 54 per resident, and the courier, express, and parcel segment is projected to expand at a 3.4% CAGR through 2031. The German containerboard market is therefore seeing a stronger pull for right-size recycled medium and testliner formats than for heavier parcel grades used in earlier shipping models.

Plastic-to-Paper Substitution in Secondary and Transit Packaging

The move from plastic transport formats to paper-based alternatives is advancing in Germany as commercial buyers and regulators both push for easier recycling and lower compliance costs. Across Europe, paper and cardboard reached a 87% recycling rate in 2023, while plastics stood at 42.1%, strengthening the economic case for fiber-based packaging under EPR systems. The Heidelberger Druckmaschinen AG and DHBW Heilbronn study on packaging to 2030 projected that flexible paper packaging will grow by more than 4.5% annually through the decade. Hugo Beck and Mondi showcased a commercial example at Interpack 2026 featuring the Paper S sleeve wrapper, which uses 70 gsm kraft paper instead of plastic shrink film for secondary packaging. In the German containerboard market, this shift supports greater demand for medium-weight kraft and specialty fluting grades than for heavyweight linerboard in transit applications.

Food and Beverage Shipment Hygiene and Shelf-Ready Needs

Food and beverage packaging in Germany now has to perform across cold-chain transit, automated distribution, and shelf-ready display without repacking, which is tightening corrugated specifications. FMCG was Germany's fastest-growing online category in 2024, with 7.3% year-on-year growth, underscoring the need for durable yet presentation-ready corrugated formats. Mondi expanded its food packaging offer in November 2025 following the integration of Schumacher Packaging sites, and the portfolio included digital printing with white ink on a brown corrugated substrate. THIMM's shelf-ready systems for brands such as Deli Reform and Staropramen show how converters are prioritizing surface consistency, stacking strength, and clean perforation performance.[1]THIMM Group, “Shelf-Ready Packaging Solutions,” THIMM, thimm.com The German containerboard market is benefiting from rising food-grade white-top and premium testliner demand, which is outpacing total market volume, as retailers focus on shelf efficiency and packaging visibility.

High Recycled-Fiber Acceptance in German Packaging Procurement

Germany has one of Europe's strongest closed-loop systems for packaging fiber, and corrugated board made up 88% by mass of commercial transport packaging collected as paper, paperboard, and cardboard in the country. The same collection stream achieves recycling rates above 90%, providing domestic mills with a stable recovered-fiber base for testliner, fluting, and corrugating medium output. A 2024 survey of 58 German paper industry practitioners found that 80% saw virgin fibers from packaging as a high-value input to the recycling stream, and 90% expected greater challenges from fiber-based composites in standard recycling processes. LEIPA's launch of LEIPA Nova in 2025 and the planned straw fiber facility with OutNature at Schwedt both show how German producers are pushing recycled and alternative fibers into more demanding applications. The Germany containerboard market is therefore seeing faster acceptance of recycled-furnish grades in consumer and logistics uses than many Southern and Eastern European markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Energy, Gas, And OCC Costs | -0.4% | National and Western Europe, particularly acute in gas-dependent Rhineland and Hamburg mill clusters, with regulatory influence from EU ETS carbon pricing beginning in 2026 | Short term (≤ 2 years) |

| Weak Industrial Production and Cautious Ordering | -0.3% | National, strongest in automotive and mechanical engineering clusters in Munich, Stuttgart, and Wolfsburg corridors | Short term (≤ 2 years) |

| Recovered-Fiber Export Disruptions Distorting Domestic Supply Economics | -0.2% | National and European, influenced by Red Sea routing disruptions and fluctuating Asian OCC import demand | Medium term (2-4 years) |

| PPWR Compliance and Documentation Costs Ahead of Full Monetization | -0.1% | EU-wide, with cost concentration in Germany and France as the lead PPWR implementation markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Energy, Gas, and OCC Costs

Energy cost volatility is still the clearest structural restraint on the Germany containerboard market because German recycled grades remain highly exposed to natural gas costs. Fastmarkets reported that testliner production draws 68% of its energy from natural gas, while white-lined chipboard can reach 92%. German natural gas prices rose 18% in Q2 2025 versus Q2 2024, and producers were still pursuing further hikes in early 2026 as energy pressure persisted. The German containerboard market feels this most sharply at non-integrated converters and recycled-grade mills, as they have less room to hedge costs or absorb concurrent spikes in energy and fiber input prices.

Weak Industrial Production and Cautious Ordering

Germany's industrial sector posted a third straight year of decline in 2025, with full-year output down 1.1% from 2024. Energy-intensive branches remained 17.8% below 2021 peak levels, suggesting a lower industrial base rather than a short pause in production. The automotive sector fell 1.7% in full-year 2025, and machinery and equipment dropped 2.6%, both of which directly weaken demand for high-caliper industrial corrugated grades. EUWID described 2025 as largely disappointing for German paper and board companies, as softer industrial volumes coincided with price normalization in corrugated board. The German containerboard market has remained more durable than German industry as a whole, but producers that still depend on heavy industrial demand are facing a slower, less certain recovery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Grades Close the Gap on Virgin Fiber Dominance

Virgin fibers held 62.5% of the Germany containerboard market share in 2025, while recycled grades are projected to grow at a 2.1% CAGR through 2031. Recycled-furnish growth is strongest in consumer goods, retail logistics, and FMCG applications where procurement teams are comfortable with high-quality recovered fiber. Germany's closed-loop collection structure supports this shift because corrugated board makes up 88% by mass of commercial transport packaging collected as paper, paperboard, and cardboard. The move is especially visible in parcel and shelf-ready formats where automated corrugators favor improved dimensional consistency from better stock preparation and cleaner OCC streams.

Virgin-fiber board still keeps a structural role in pharmaceutical secondary packaging, fresh produce, and heavy-wall industrial corrugated because those uses still value burst strength, print surface, and moisture resistance. The 2024 German practitioner survey showed that 80% of respondents see virgin fiber in incoming packaging as a positive input to recycled pulp quality. That is why the German containerboard market is moving toward a more balanced raw-material mix rather than a full shift to mono-recycled fiber.

By Product Type: Kraftliner Scale Anchored as Testliner Momentum Builds

Kraftliners accounted for 44.1% of the Germany containerboard market size in 2025, while testliners are forecast to expand at a 2.3% CAGR through 2031. Kraftliner leadership still reflects its role in heavy-wall industrial formats, export boxes, and food-contact packaging, where surface regularity and tear strength remain important. Testliner growth is faster because more corrugated volume is moving toward lighter, print-receptive grades designed for retail-ready and e-commerce fulfillment. This leaves the Germany containerboard market with a wider mix of applications where premium process control matters as much as raw material choice.

The quality gap in testliner is increasingly shaped by automation performance, not just by fiber source, because converters want flatness, moisture uniformity, and stiffness that stays consistent on high-speed lines. Klingele's Weener project with Valmet supports this direction through added automation at a mill producing testliner, flute paper, and flexliner from recycled waste paper. Progroup's newer corrugated sheet feeder assets in Cessalto and Petersberg were designed for low-grammage production and high running speeds, underscoring how lighter grades are becoming central to converting economics.

By End User: Consumer Goods Lead While Food and Beverage Accelerates

Consumer goods accounted for 37.3% of the Germany containerboard market in 2025, while food and beverage is projected to grow at a 2.4% CAGR through 2031. Consumer goods remained the largest because Germany has a dense retail and logistics base, and corrugated remains the primary transit format for household goods, personal care, and consumer electronics. Food and beverage is growing faster because the same shipper now has to work in cold-chain transit, automated picking, and shelf presentation. This is pushing converters toward tighter tolerances and lifting demand for better-performing liner and medium grades.

Industrial end users continue to consume significant volumes of containerboard for automotive parts, machinery subassemblies, and hazardous goods packaging, even after the recent industrial downturn. Those applications still depend on heavy-wall corrugated, where transit protection requirements leave little room for substitution. At the same time, THIMM's tray and shelf-ready systems and Mondi's white-ink digital printing show how food packaging is pulling the value mix upward in the German containerboard market.[2]Mondi Group, “Mondi Launches Extended Corrugated and Solid Board Portfolio for the Food Packaging Industry,” Mondi Group, mondigroup.com Other end users tied to parcel delivery and e-commerce packaging are also expanding faster than the market average as Germany's delivery network deepens its use of corrugated packaging.

Geography Analysis

Germany sits at the center of the European supply chain for corrugated base paper, and the German containerboard market continues to be supported by strong domestic demand and robust exports to nearby converting markets. CEPI's preliminary statistics for 2025 showed European corrugated board production up 1.7%, while demand was almost flat at -0.2%, keeping price competition elevated across the region.[3]Cepi, “Preliminary Statistics 2025, European Pulp and Paper Industry,” Cepi, cepi.org That environment put German mills under pressure from lower-cost Eastern European capacity, especially in commodity recycled grades. Germany still holds an advantage in supply security because the country reported a 95.3% corrugated recycling rate and an organized collection system, where corrugated board accounts for 88% by mass of industrial transport packaging.

Recovered-fiber export shifts also affect domestic economics because longer Asia routes and changing Asian demand can periodically tighten OCC availability in Europe. Within Germany, capacity is concentrated in a few industrial corridors, shaping freight costs and customer service. The Rhineland and southwest remain important because they connect major mills and converting demand in a short logistics loop. Northern and eastern sites also matter because they tie into collection flows and distribution routes serving domestic and export customers. Progroup's packaging park model in Schüttorf shows how co-location can reduce truck movements and create a tighter mill-to-converter service structure.

Western European neighbors remain important outlets for German-linked groups, and this cross-border structure influences both pricing discipline and converting strategy. Palm's acquisition of International Paper corrugated plants in France, Spain, and Portugal in 2025 widened the reach of a German mill-integrated group into Western European converting operations. The EU packaging regulation also changes geography because PPWR becomes fully applicable on August 12, 2026 and introduces harmonized recyclability grading and declarations of conformity across member states. That gives Germany an early standard-setting role because buyers and producers operating in the Germany containerboard market are preparing for certification and documentation that can later support sales into France, Benelux, and the Nordic countries.

Competitive Landscape

The German containerboard market shows moderate concentration, with a limited group of integrated producers holding the strongest positions in mills, collection, and converting. Smurfit Westrock has the largest single-ownership production footprint in Germany through its recycled containerboard mills in Zülpich, Hoya, and Wrexen. The 2024 merger of Smurfit Kappa and WestRock gave the combined company greater scale across Europe, and the group followed that with plant rationalization and new investments in higher-quality printed packaging. Progroup remains one of the most expansion-focused competitors, with paper mills, sheet feeder plants, waste-to-energy assets, and a long-term plan for Stockstadt. Palm also used 2025 to expand its geographic scale through acquisitions and new construction rather than waiting for a broad demand rebound.

Two strategies stand out in the German containerboard market: scale integration and technology-led specialization. Large integrated groups are consolidating mills and corrugators, investing in energy resilience, and using design and data tools to deepen customer relationships. Smurfit Westrock's network of customer experience centers and digital packaging development tools shows how the biggest companies are moving beyond paper supply into packaging solution design.[4]Smurfit Westrock, “2025 Annual Report,” Smurfit Westrock, smurfitwestrock.com Mid-tier players are responding with focused automation and process intelligence, as shown by Klingele's AI Research Hub and its Weener automation project with Valmet.

Competitive moves in 2025 and 2026 also show a clear push into downstream converting and higher-value formats. Mondi's integration of Schumacher Packaging sites expanded its European corrugated footprint and strengthened its offer in food packaging and retail-ready applications. Saica's acquisition of THIMM in May 2026 points in the same direction because it links recycled containerboard scale with a recognized German shelf-ready packaging network. The Germany containerboard market still leaves room for differentiation in white-top liner, food-contact grades, and alternative-fiber blends, but the companies best placed to capture that value are those with both technical mill capability and direct converter or brand relationships.

Germany Containerboard Industry Leaders

Mondi plc

Smurfit Westrock plc

VPK Group NV

International Paper Company

Billerud AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Smurfit Westrock reported Q1 2026 results, noting that containerboard prices in the EMEA and APAC regions increased during March and April 2026, driven by higher energy costs and improving demand.

- April 2026: Palm initiated the first phase of its Wörth containerboard warehouse modernization, deploying two automated crane systems and a new crane runway from Konecranes, a project expected to increase loading capacity by 30% upon completion in spring 2027.

- March 2026: Progroup started joint operations with Akarton at its PW05 corrugated sheetfeeder plant in Schüttorf, Germany, restoring a full converting value chain at the site through a packaging park co-location model and reducing daily transport movements via direct intralogistics integration.

- February 2026: LEIPA Group signed a Power Purchase Agreement with Statkraft, Europe's largest renewable energy producer, to supply both German LEIPA production sites with onshore wind power from 2026, supporting the group's decarbonization strategy and providing cost stability against gas price volatility.

Germany Containerboard Market Report Scope

The scope of the report includes an in-depth analysis of the containerboard market in Germany. Containerboard refers to the material used in the production of corrugated boxes, primarily consisting of linerboard and corrugating medium. This report examines market trends, growth drivers, challenges, and opportunities within the containerboard market in Germany, providing insights into the supply chain, demand dynamics, and competitive landscape.

The Germany Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End User (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End Users |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End User | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End Users |

Key Questions Answered in the Report

What is the expected value of Germany containerboard demand by 2031?

The Germany containerboard market is forecast to reach USD 7.12 billion by 2031 from USD 6.57 billion in 2026, which reflects a 1.62% CAGR over 2026-2031.

Which material segment leads current demand in Germany?

Virgin fibers lead current demand with 62.5% share in 2025, mainly because food-contact, pharmaceutical, and heavy industrial applications still need their strength and consistency.

Which product type is growing fastest through 2031?

Testliner is the fastest-growing product type with a 2.3% CAGR through 2031 because parcel, FMCG, and retail-ready packaging are shifting toward lighter and more automation-friendly grades.

Why are food and beverages becoming more important for corrugated demand?

Food and beverage are projected to grow at a 2.4% CAGR because omnichannel supply chains require packaging that supports cold-chain transit, automated picking, and shelf-ready presentation.

How is weak German industry affecting corrugated base paper suppliers?

Industrial output fell 1.1% in 2025, and automotive and machinery also declined, which is reducing demand for high-caliper industrial corrugated grades even though consumer and parcel channels remain more resilient.

What is the biggest cost risk for producers in 2026?

Energy and OCC volatility remains the main risk because gas dependency is high in recycled grades and some producers continued seeking price increases in early 2026 to offset cost pressure.

Page last updated on: