Wi-Fi Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

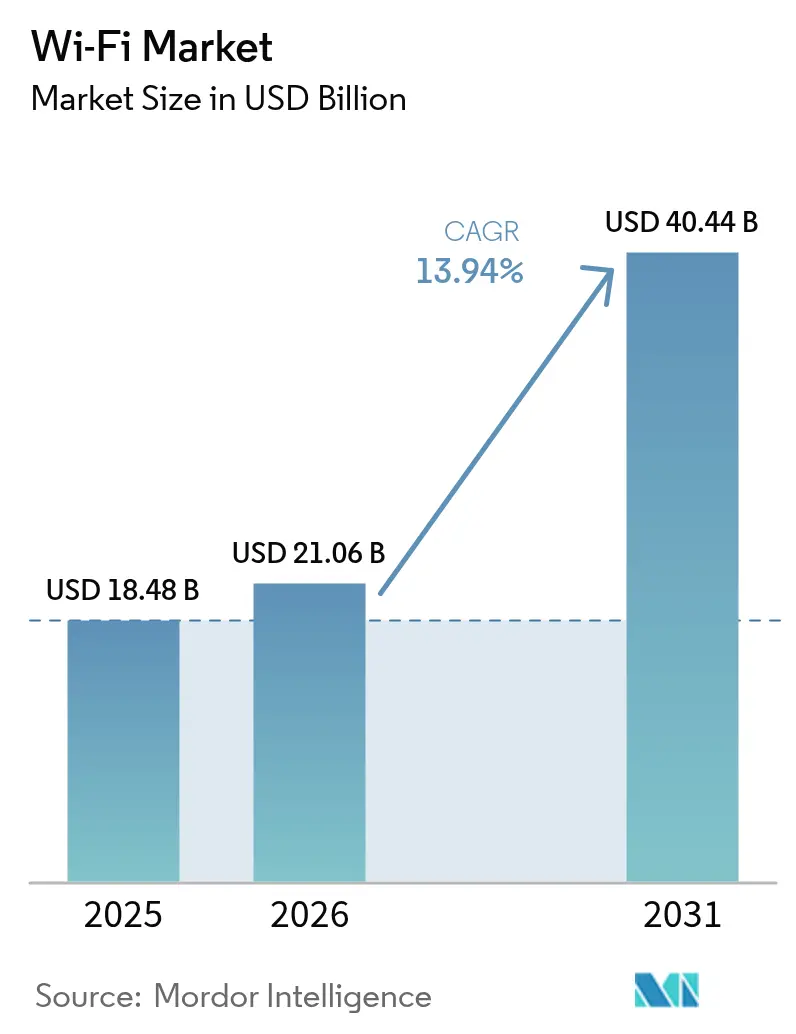

| Market Size (2026) | USD 21.06 Billion |

| Market Size (2031) | USD 40.44 Billion |

| Growth Rate (2026 - 2031) | 13.94% CAGR |

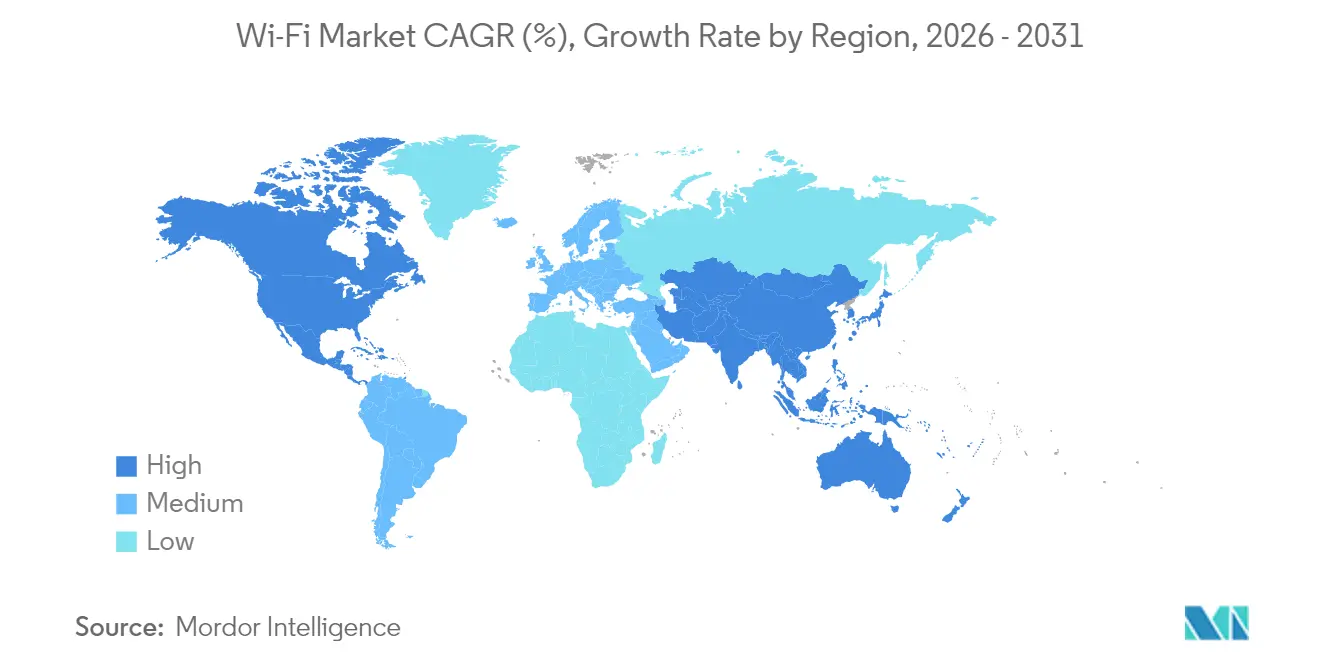

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wi-Fi Market Analysis by Mordor Intelligence

The Wi-Fi Market size was valued at USD 18.48 billion in 2025 and estimated to grow from USD 21.06 billion in 2026 to reach USD 40.44 billion by 2031, at a CAGR of 13.94% during the forecast period (2026-2031). Growing enterprise preference for wireless-first architecture, the commercial debut of Wi-Fi 7, and the adoption of OpenRoaming standards are the primary forces propelling this acceleration [1]Kevin Robinson, “Wi-Fi 7 Momentum in 2025,” Wi-Fi Alliance, wifi.org. Enterprises view high-capacity WLAN as pivotal for hybrid work enablement, edge-hosted artificial intelligence, and real-time industrial automation, prompting refresh cycles that shorten from eight years to five. Rapid mesh penetration in residential and small-office environments further broadens the addressable base, while federal broadband programs in North America stimulate public-sector opportunities. Spectrum allocations in the 6 GHz band supply temporary congestion relief, yet also spark demand for tri-band access points that can assure deterministic latency for robotics, telemedicine, and immersive reality services. The competitive landscape remains open because interoperability requirements prevent lock-in, allowing new service-centric entrants to challenge incumbent hardware vendors.

Key Report Takeaways

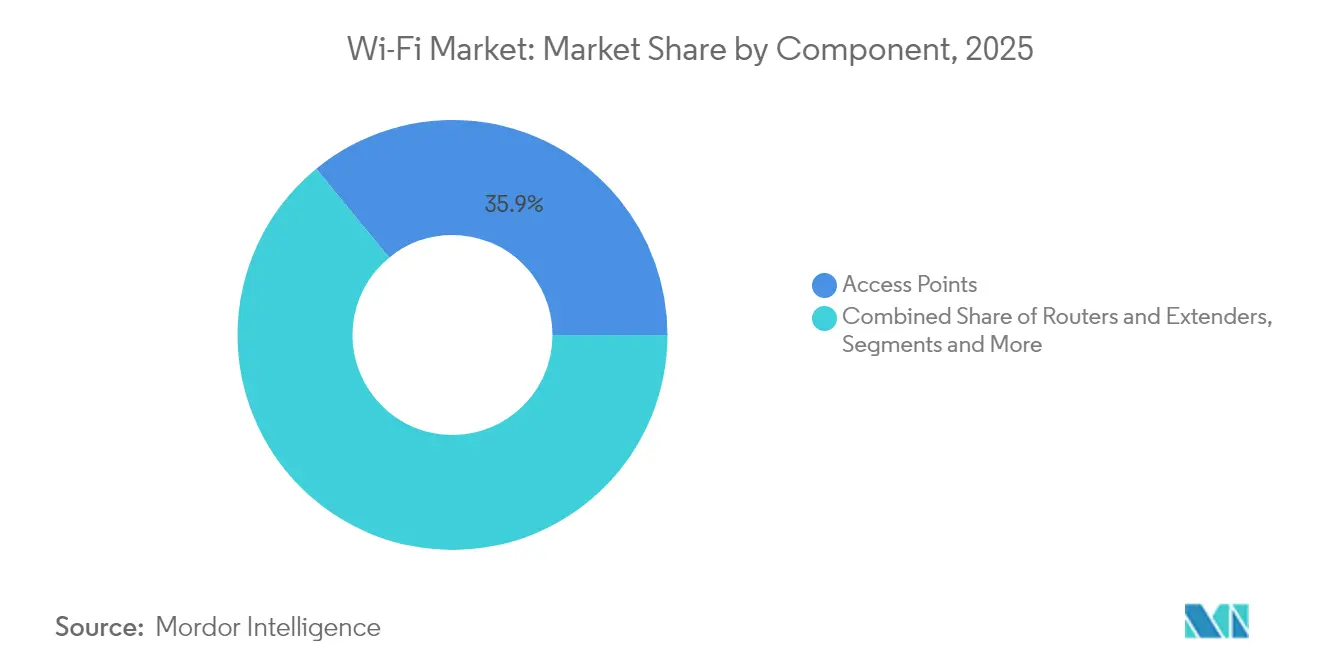

- By component, access points held 35.92% of the Wi-Fi market share in 2025, while the services segment is projected to advance at a 15.98% CAGR through 2031.

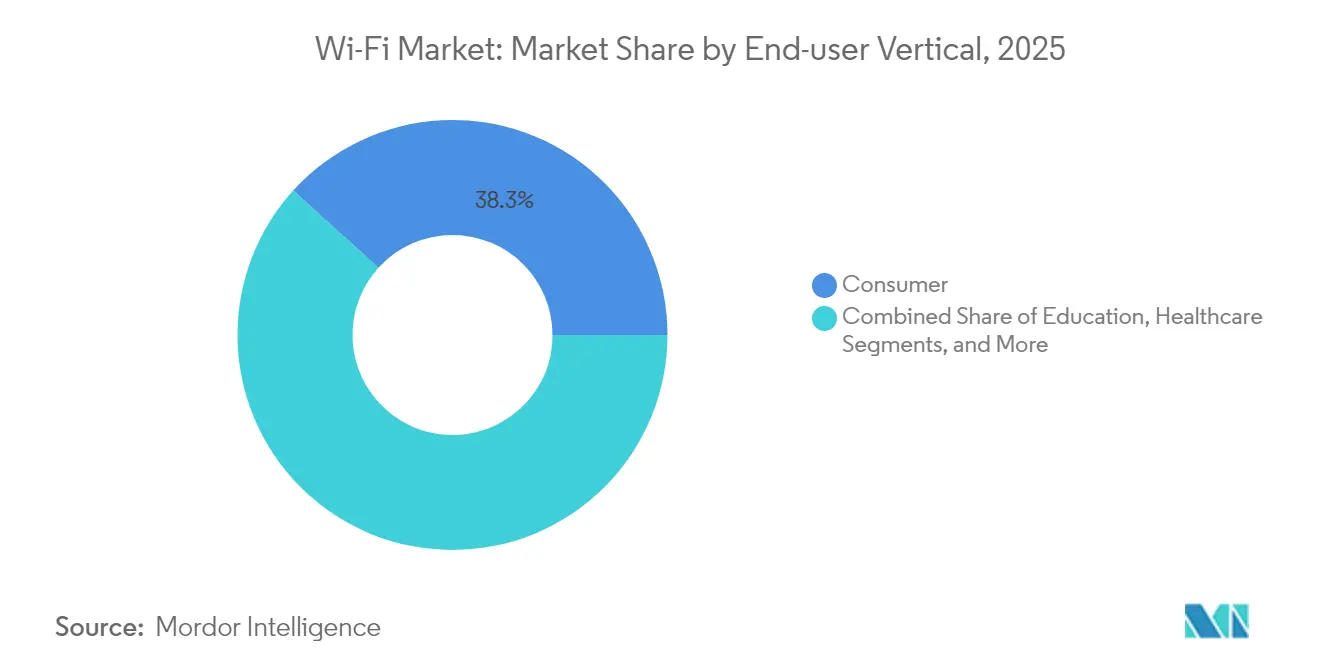

- By end-user vertical, consumer applications led with 38.28% revenue share in 2025; industrial and logistics is forecast to expand at a 17.18% CAGR to 2031.

- By geography, North America commanded a 40.55% share of the Wi-Fi market in 2025, whereas the Asia Pacific is advancing at a 15.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wi-Fi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT and smart devices | +2.8% | Global; strongest in Asia Pacific | Medium term (2-4 years) |

| Smart-city initiatives and public WiFi roll-outs | +2.1% | North America, EU; spreading to APAC | Long term (≥ 4 years) |

| Rapid adoption of WiFi 6/6E and upcoming WiFi 7 | +3.2% | Global; enterprise-led in developed markets | Short term (≤ 2 years) |

| Hybrid/remote work models demanding high-capacity WLAN | +2.5% | North America and EU; spillover to APAC | Medium term (2-4 years) |

| Convergence of WiFi and 5G via OpenRoaming/Passpoint | +1.9% | Global; carrier partnerships pivotal | Long term (≥ 4 years) |

| Energy-efficient TWT features for battery-powered IoT nodes | +1.5% | Global; industrial and smart building | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT and smart devices

Enterprises deploy dense sensor networks that often exceed 100 connected endpoints per access point, a profile economically serviced only by Wi-Fi 6E’s OFDMA scheduling and multi-user MIMO capabilities. Smart-building operators integrate HVAC, lighting, and surveillance over Wi-Fi mesh to cut structured-cabling costs by 40% and enable predictive maintenance analytics. Demand for sub-10 ms response in edge inference workflows makes Wi-Fi 7’s multi-link operation attractive because it sustains jitter-free traffic under load. Industrial automation pilots report 99.9% uptime on dedicated 6 GHz channels versus 97.8% on congested 5 GHz links, validating the migration to new spectrum for mission-critical robotics. These gains encourage organizations to absorb higher capital outlays in return for long-run productivity [2]Qualcomm Incorporated, “FY2025 1st Quarter Earnings Presentation,” Qualcomm, qualcomm.com.

Smart-city initiatives and public Wi-Fi roll-outs

Municipal broadband programs increasingly favor Wi-Fi as the primary medium for digital inclusion because installation is quicker and less capital-intensive than fiber in sprawling rural territories. The Philippines commits USD 1.2 billion to deploy more than 100,000 public hotspots across 17,000 barangays by 2028, a template mirrored by several emerging economies. Europe’s Digital Decade targets gigabit coverage by 2030 and positions Wi-Fi 7 mesh as an affordable last-mile alternative in mountainous and island regions. Cities monetize infrastructure by layering sensor backhaul for traffic, air-quality, and emergency-response schemes that self-fund through efficiency gains. Neutral-host deployments that blend Wi-Fi and 5G radios under OpenRoaming agreements generate fresh revenue as roaming fees while delivering seamless citizen connectivity.

Rapid adoption of Wi-Fi 6/6E and upcoming Wi-Fi 7

Enterprises accelerate refresh cycles because Wi-Fi 7 aggregates 2.4 GHz, 5 GHz, and 6 GHz links to deliver cumulative throughput beyond 40 Gbps, a prerequisite for high-definition collaborative platforms and immersive reality content. Leading silicon suppliers booked record pre-orders for Wi-Fi 7 chipsets in early 2025, highlighting pent-up demand. Hospitals adopt Wi-Fi 7 to support latency-intolerant surgical robotics and telemetry that classical WLAN cannot guarantee. Universities observe a three-fold rise in concurrent 4K streams once Wi-Fi 7 infrastructure is in place, sustaining hybrid classroom models without quality degradation. Backward compatibility smooths migration and protects prior device investments, reinforcing the upgrade imperative.

Hybrid/remote work models demanding high-capacity WLAN

Flexible workspace layouts force IT departments to implement software-defined WLAN that scales bandwidth to shifting occupancy. Video-conference concurrency climbed 250% since 2024, impelling organizations to dedicate 6 GHz spectrum for real-time applications and thereby eliminate interference from legacy 2.4 GHz equipment. Managed Wi-Fi revenue grows at double digits as firms offload network operations to specialists and refocus talent on core initiatives. Productivity studies reveal that workers experiencing sub-50 ms latency achieve 23% higher task completion rates than peers on congested links, reinforcing WLAN investment. Network-as-a-Service contracts trim operating expense swings by matching capacity to actual footfall, with some corporations cutting non-productive spend by 35% [3]Cisco Systems, “Redefining Network Management: The Advantages of Cisco Managed Campus for MSPs,” Cisco, cisco.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion and interference in unlicensed bands | –1.8% | Global; acute in dense cities | Short term (≤ 2 years) |

| Heightened data-privacy/security compliance costs | –1.2% | EU, North America | Medium term (2-4 years) |

| Li-Fi and 60 GHz alternatives cannibalizing dense-WiFi use cases | –0.9% | Niche deployments | Long term (≥ 4 years) |

| Chipset supply constraints delaying WiFi 7 device launches | –1.4% | Global; Asia manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Spectrum congestion and interference in unlicensed bands

Dense urban precincts such as Manhattan experience throughput drops near 60% during peak usage, even when Wi-Fi 6E hardware is present, because legacy devices crowd the 2.4 GHz spectrum. Microwave ovens, Bluetooth handsets, and older routers create overlapping noise that adaptive algorithms cannot fully evade. Enterprises increasingly hire spectrum consultants, a service costing USD 50,000-200,000 on expansive campuses, to engineer channel plans that meet service-level objectives. Regulators consider quasi-licensed regimes akin to CBRS so that critical IoT traffic can operate free of consumer interference. Although the 6 GHz allocation temporarily alleviates pressure, forecasts show saturation within five years as IoT endpoints grow exponentially.

Heightened data-privacy and security compliance costs

Stringent regulations such as GDPR and CCPA obligate encryption, audit trails, and data-sovereignty controls that raise WLAN complexity by 40%. A 500-bed hospital attributes USD 1.5 million to Wi-Fi security upgrades needed for HIPAA compliance, including micro-segmentation and continuous vulnerability scanning. Zero-trust postures mandate integration with identity providers, public-key infrastructure, and real-time analytics, tripling day-to-day operational overhead. Financial firms isolate trading-floor traffic with hardware-enforced segmentation that costs USD 5,000 per access point, a premium many small organizations struggle to justify. Maintaining annual certifications across multi-vendor estates further inflates budgets and slows expansion in cost-sensitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services-led operating models gain momentum

In 2025, access points contributed 35.92% to the Wi-Fi market share, underlining hardware’s continuing relevance even as revenue mix shifts. The services segment, however, is projected to compound at 15.98% through 2031, reflecting the pivot to Network-as-a-Service frameworks that convert upfront capital into recurring operating expense. Cost pressures commoditize standalone routers and range extenders, while cloud-native orchestration platforms take over the policy and analytics roles previously executed by on-premises controllers. Managed service providers leverage artificial intelligence to automate channel allocation, load balancing, and anomaly detection, ultimately delivering 75% fewer unplanned-outage minutes than customer-operated networks. By 2031, the Wi-Fi market size attributed to software and services is expected to eclipse hardware contribution in mature economies as organizations prioritize life-cycle flexibility over asset ownership.

The shift mirrors broader IT procurement trends that favor outcomes over ownership. Consumption-based pricing aligns WLAN costs with occupancy levels, flattening budget spikes and improving CFO visibility. Vendors bundle proactive maintenance, security compliance, and real-time experience scoring to differentiate beyond hardware. Edge gateways and ruggedized IoT bridges constitute a small but fast-rising category, supplying deterministic connectivity in harsh industrial zones where vibration, dust, and temperature extremes invalidate consumer-grade gear. As AI chips embed inside access points, even commodity hardware gains value when offered as a managed experience that abstracts complexity and accelerates time to productivity.

By End-user Vertical: Industrial automation steals the growth spotlight

Consumer deployments accounted for 38.28% of the Wi-Fi market in 2025 because mesh systems proliferated across dense housing and home-office scenarios. Growth nevertheless moderates as penetration nears saturation in developed economies. In contrast, industrial and logistics environments are forecast to post a 17.18% CAGR through 2031, lifted by autonomous guided vehicles, digital twins, and asset-tracking tags that require deterministic latency and rapid handoff. Production lines integrate Wi-Fi robotics and sensor arrays that achieve 99.9% uptime on 6 GHz channels, reinforcing migration to the latest standards. Healthcare facilities adopt Wi-Fi-enabled patient telemetry that improves clinical outcomes by enabling continuous monitoring without tethering, while education systems broaden one-to-one device programs that rely on tri-band WLAN to sustain simultaneous 4K streams for remote learners.

Enterprise campuses modernize to support hybrid work, installing high-density AP clusters and analytics engines that optimize seating usage in real time. Hospitality groups deploy captive portals and loyalty apps over Wi-Fi to personalize guest experiences and upsell services. Retailers integrate point-of-sale, inventory robotics, and customer-facing AR navigation, extracting data that drives price optimization. These cross-sector uses expand the Wi-Fi market size well beyond its original consumer orientation, deepening vendor addressable revenue pools.

Geography Analysis

North America accounts for 40.55% of the Wi-Fi market in 2025, owing to USD 65 billion in broadband incentives and rapid enterprise refresh cycles. Early access to 6 GHz spectrum allows institutions to pioneer tri-band deployments, creating a performance gap over regions still seeking regulatory clearance. Fortune 500 companies refresh their WLAN every five years, two years faster than the global average, to equip smart offices tailored for hybrid work. Healthcare and education pillars represent robust growth nodes as telehealth and distance learning require enterprise-grade reliability.

Asia Pacific records the fastest trajectory with a 15.12% CAGR through 2031, enabled by national digital strategies that treat wireless as primary rather than complementary infrastructure. China’s factory-automation boom, amplified by policy to cultivate domestic chipset capability, translates to bulk orders for industrial-grade Wi-Fi 6E equipment. India’s Digital India mission envisions connecting 600,000 villages via Wi-Fi mesh, making wireless the linchpin of rural inclusion. Southeast Asian economies integrate WLAN across tourism hubs and export-oriented manufacturing parks, while government subsidies shrink payback periods and accelerate deployments. Smart-city funding rounds across Jakarta, Bangkok, and Ho Chi Minh City further elevate regional demand.

Europe’s growth remains orderly as Industry 4.0 uptake and Digital Decade mandates require gigabit household coverage by 2030. Wi-Fi serves as the cost-effective last-mile solution in rugged topographies like the Alps and the Greek islands. OpenRoaming agreements spearheaded by the EU Digital Single Market create frictionless cross-border connectivity, bolstering tourism and remote business travel. Germany leads industrial adoption, whereas Nordic nations focus on smart-grid and sustainability use cases that rely on energy-efficient TWT scheduling. The Middle East and Africa invest in Wi-Fi to diversify economies beyond hydrocarbons and to bridge digital divides in rural deserts and mountainous terrain.

Competitive Landscape

The Wi-Fi market is moderately concentrated. Legacy titans such as Cisco and HPE Aruba leverage extensive channels to defend share, but must contend with service-first entrants that deliver vertically integrated experiences under consumption contracts. Silicon supply is concentrated among Qualcomm, Broadcom, and MediaTek, making chipset availability the gating factor for vendor roadmaps, especially during the Wi-Fi 7 transition. Start-ups position artificial intelligence, zero-trust security, and edge-computing hooks as their levers for differentiation, arguing that the real contest now centers on software efficacy rather than radio specification.

Qualcomm’s FastConnect 7900 introduces AI-powered optimization for power, latency, and throughput, blending Ultra-Wideband for secure ranging and Bluetooth Channel Sounding for positional accuracy. Ubiquiti targets prosumers with simplified cloud dashboards that cut the total cost of ownership for small businesses unable to staff dedicated network teams. Carrier alliances test OpenRoaming to stitch cellular and Wi-Fi authentications, expanding addressable audiences for both camps while blurring traditional demarcations. Meanwhile, industrial specialists secure footholds in hazardous environments with explosion-proof access points that fetch premium margins despite low volume.

Vendor competitiveness thus tilts toward agility in firmware, security orchestration, and consumption-based service bundling. Those slow to integrate AI-driven diagnostics risk relegation to hardware commodity status, underscoring the shrinking window for differentiation during rapid generational shifts. Across segments, the Wi-Fi market size continues to reallocate from one-time equipment sales to recurring software and services, a macro trend that redefines competitive advantage.

Wi-Fi Industry Leaders

Cisco Systems, Inc.

Hewlett Packard Enterprise (Aruba)

Huawei Technologies Co., Ltd.

CommScope Holding Company Inc.(Ruckus Networks)

Telefonaktiebolaget LM Ericsson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: MediaTek and Realtek announce surging orders for Wi-Fi 7 chipsets as enterprises accelerate migration to tri-band WLAN platforms.

- October 2024: MediaTek selects Qorvo to supply front-end modules for the Dimensity 9400 platform, with volume shipments commencing in Q4 2024.

Global Wi-Fi Market Report Scope

Wi-fi is a trademarked term that denotes wi-fi-certified WLAN-based connectivity products that enable communication for various devices over the internet. The recent rise in the number of devices connected over the internet and the demand for external wi-fi communication has significantly driven the need for these connectivity products. The study focuses on tracking the market growth and forecasts for various products, such as access points, gateways, extenders, routers, and services. The study analyzes the evolution of Wi-Fi-based communication that has led to the recent launch of Wi-Fi 6, which is touted as the next-generation standard in the technology.

Wi-Fi market is segmented by product (access points, gateways, routers, and extenders), application (residential, enterprise, and education), outdoor (public services, transportation, and public utilities), and geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, rest of Europe), Asia-Pacific (China, Japan, South Korea, rest of Asia-Pacific) and Latin America and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | Access Points |

| Routers and Extenders | |

| Wireless Controllers | |

| Other Device Types | |

| Solutions | |

| Services |

| Consumer |

| Enterprise/Corporate Campuses |

| Education |

| Healthcare |

| Hospitality and Retail |

| Industrial and Logistics |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | GCC |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware | Access Points |

| Routers and Extenders | ||

| Wireless Controllers | ||

| Other Device Types | ||

| Solutions | ||

| Services | ||

| By End-user Vertical | Consumer | |

| Enterprise/Corporate Campuses | ||

| Education | ||

| Healthcare | ||

| Hospitality and Retail | ||

| Industrial and Logistics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the Wi-Fi market expected to grow between 2026 and 2031?

The Wi-Fi market is projected to expand at a 13.94% CAGR, rising from USD 21.06 billion in 2026 to USD 40.44 billion by 2031.

Which region will see the highest growth in new Wi-Fi deployments?

Asia Pacific leads with a 15.12% CAGR through 2031, driven by smart-city funding, factory automation, and rural connectivity initiatives.

Why are enterprises shifting toward Network-as-a-Service models for WLAN?

NaaS converts capital outlays into predictable operating expense and bundles AI-powered optimization, resulting in 75% fewer unplanned-outage minutes than self-managed networks.

What role does 6 GHz spectrum play in next-generation Wi-Fi?

The 6 GHz band adds contiguous channels that mitigate congestion and enable Wi-Fi 7’s multi-link operation, delivering aggregated throughput beyond 40 Gbps for latency-sensitive applications.

Which end-user vertical will grow the fastest through 2031?

The industrial and logistics vertical is forecast to advance at 17.18% CAGR as autonomous vehicles, asset tracking, and predictive maintenance rely on deterministic Wi-Fi links.

How are security regulations affecting enterprise WLAN budgets?

Compliance with GDPR, CCPA, and sector-specific mandates increases WLAN complexity by around 40% and can add USD 5,000 per access point when micro-segmentation and zero-trust features are required.

Page last updated on: