Mobile Signal Booster Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

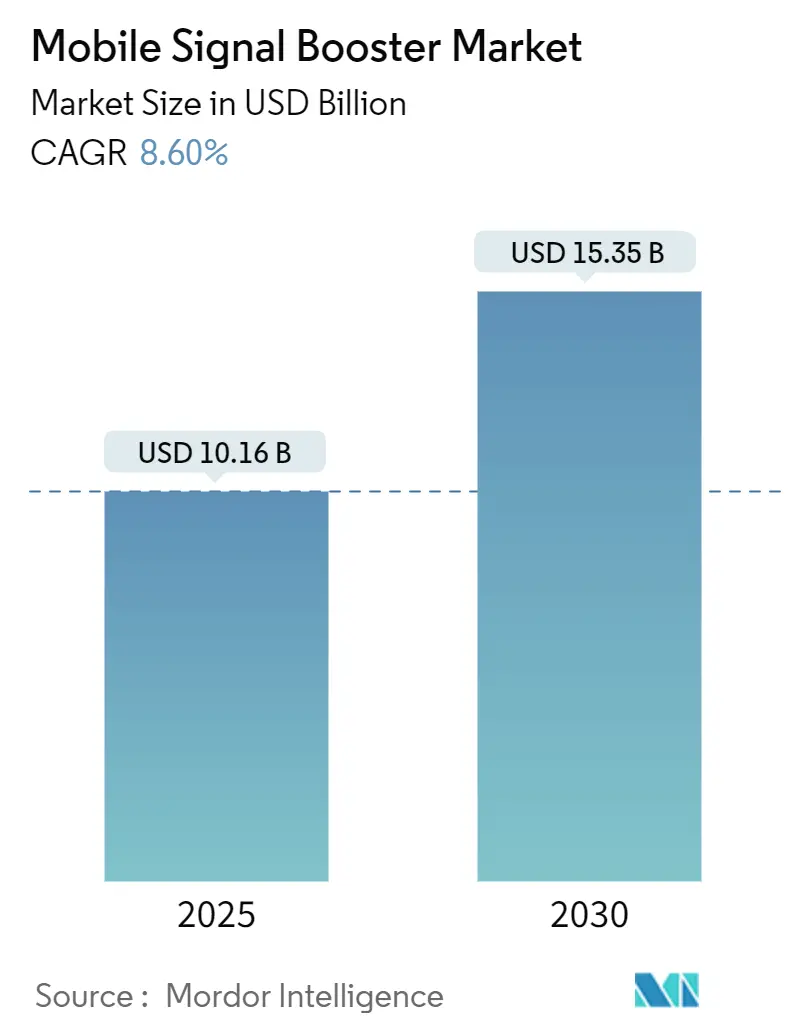

| Market Size (2025) | USD 10.16 Billion |

| Market Size (2030) | USD 15.35 Billion |

| Growth Rate (2025 - 2030) | 8.60% CAGR |

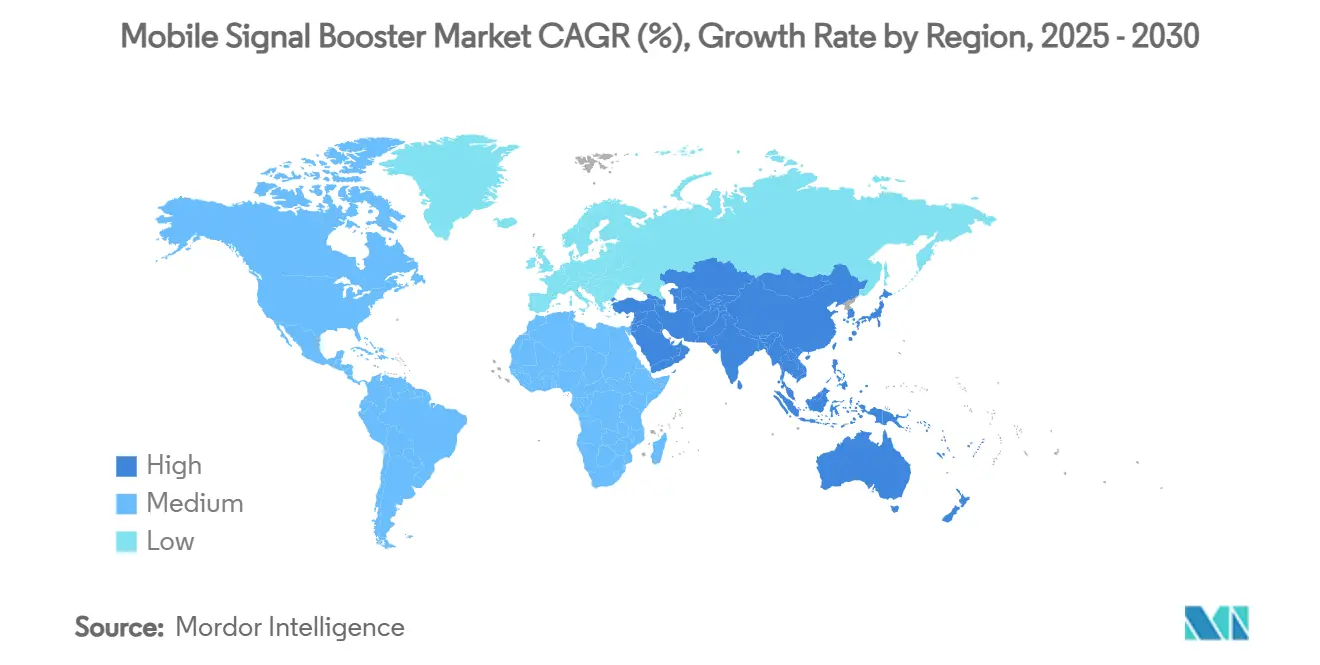

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Signal Booster Market Analysis by Mordor Intelligence

The mobile signal booster market size stands at USD 10.16 billion in 2025 and, at an 8.60% CAGR, is forecast to reach USD 15.35 billion by 2030. Heightened demand for always-on mobile data, the densification of 5G networks, and government-funded rural-connectivity programs are expanding addressable volumes across residential, commercial, and heavy-industry environments. Smart boosters equipped with AI-driven gain control now temper interference concerns while cutting deployment time for carriers and enterprises alike. Concurrent spectrum policies-from streamlined FCC Part 20 rules to nationwide coverage mandates, are lowering ownership barriers, especially for first-time consumers and rural internet service providers. Meanwhile, capital spending on factory automation and private 5G is turning industrial facilities into the fastest-growing customer group, reinforcing double-digit growth projections for the mobile signal booster market.

Key Report Takeaways

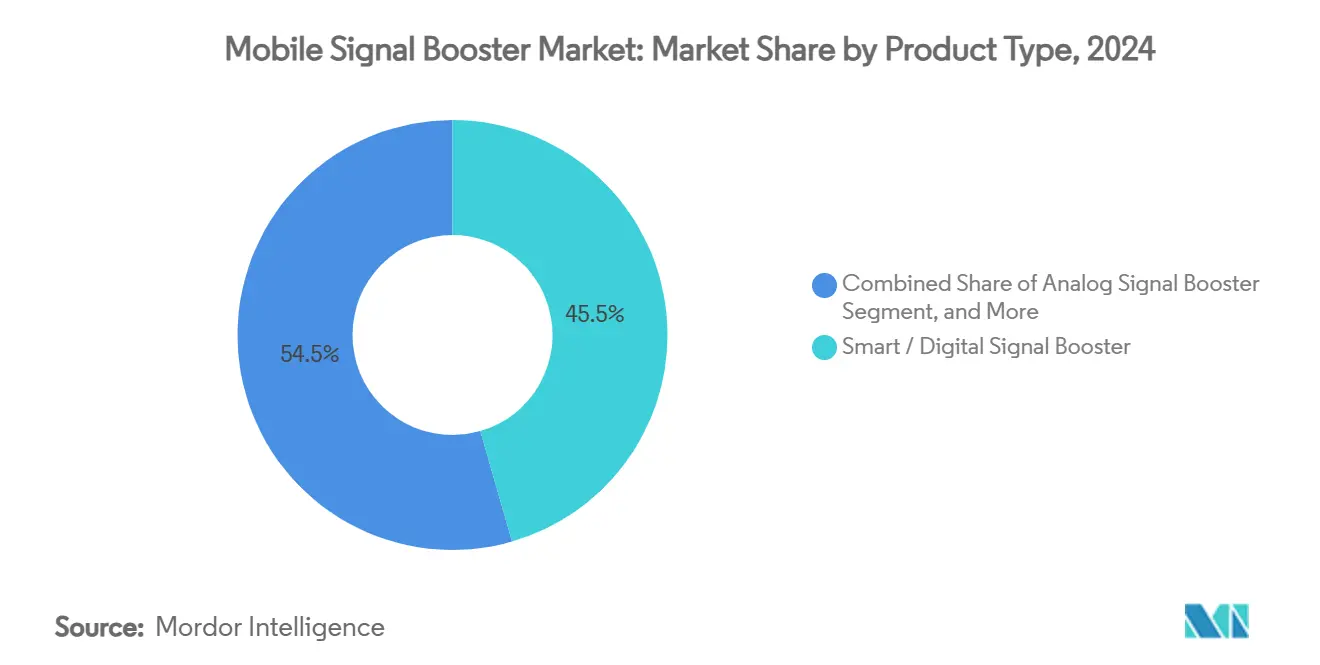

- By product type, smart/digital boosters captured 45.53% share of the mobile signal booster market in 2024.

- By technology, the mobile signal booster market for 5G-NR Sub-6 GHz is projected to capture a 10.63% CAGR between 2025 to 2030.

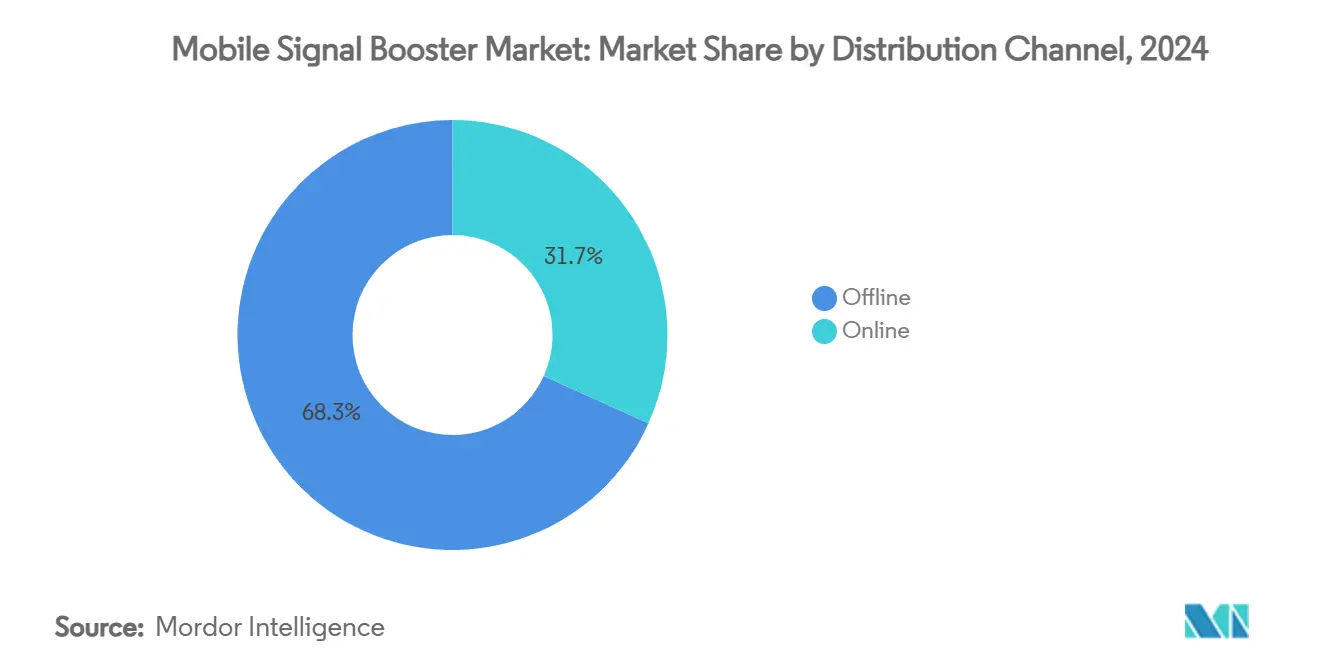

- By distribution channel, offline sales captured 68.26% share of the mobile signal booster market in 2024.

- By end-user, the mobile signal booster market for industrial facilities is projected to capture a 10.64% CAGR between 2025 to 2030.

- By geography, North America captured a 37.73% share of the mobile signal booster market in 2024.

Global Mobile Signal Booster Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G densification and indoor coverage mandates | +2.1% | Global, concentration in North America and EU | Medium term (2-4 years) |

| Rapid growth of data-heavy IoT devices in factories | +1.8% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Eased FCC Part 20 regulations on consumer boosters | +1.3% | North America, regulatory influence on global standards | Short term (≤ 2 years) |

| Government rural-broadband subsidy programs | +1.5% | Global, emphasis on North America and emerging markets | Medium term (2-4 years) |

| AI-enabled remote-monitoring “smart” boosters | +0.9% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| Private-network rollout by enterprises (LTE/5G) | +1.4% | Global, concentrated in industrial regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Densification and Indoor Coverage Mandates

Indoor attenuation at mid-band and mmWave frequencies forces operators to complement small-cell investments with cost-effective repeaters that accelerate compliance with population-coverage obligations. Smart boosters can reuse licensed spectrum without heavy fiber backhaul, closing service gaps in offices, hospitals, and campuses. Building owners increasingly favor these devices because they avoid lengthy zoning processes tied to traditional base-station expansion. In large venues, gain-controlled boosters lessen network planning complexity by auto-adjusting to traffic loads. This alignment of regulatory goals and building-owner economics secures a multiyear pull for the mobile signal booster market.

Rapid Growth of Data-Heavy IoT Devices in Factories

Factories running thousands of sensors and mobile robots now treat wireless uptime as a production KPI. Private LTE and 5G outperform Wi-Fi in spectral efficiency, yet concrete walls and metal machinery still create shadow zones. Signal boosters extend on-premise coverage without additional spectrum licenses, cutting deployment timelines for manufacturers. Demand is most acute in Asia-Pacific mega-industrial parks that mix assembly, warehousing, and logistics facilities. As predictive-maintenance workloads rise, low-latency links via boosted mid-band spectrum become central to digital-twin rollouts, reinforcing adoption inside the mobile signal booster market.

Eased FCC Part 20 Regulations on Consumer Boosters

The 2024 Part 20 update simplified device certification and required automatic gain control, which boosted retailer confidence and slashed grey-market leakage. Consumers can now self-register boosters with their carrier online, accelerating time to service. Carriers gain network-wide visibility, mitigating interference fears and opening joint marketing programs with certified vendors. The rule set also clarifies licensing for industrial boosters, giving plant operators a predictable path to legal high-gain systems. These changes collectively enlarge the addressable U.S. slice of the mobile signal booster market.

Government Rural-Broadband Subsidy Programs

Funding such as the USD 9 billion 5G Fund for Rural America subsidizes infrastructure in low-density zones where standalone cell-site economics falter. USDA ReConnect loans treat boosters as eligible capital, encouraging WISPs to bundle signal amplification with fixed-wireless service.[1]U.S. Department of Agriculture, “ReConnect Loan and Grant Program,” usda.govCommunity Connect grants target dead-spot remediation around schools and clinics, channeling public dollars toward carrier-approved repeaters. These schemes accelerate unit shipments while validating boosters as mainstream broadband tools rather than niche accessories. Resulting volume growth materially lifts the mobile signal booster market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from small-cell and DAS alternatives | -1.7% | Global, concentrated in urban markets | Medium term (2-4 years) |

| Interference concerns and grey-market devices | -1.2% | Global, regulatory enforcement varies | Short term (≤ 2 years) |

| Up-front cost for mmWave-compatible boosters | -0.8% | Global, early 5G deployment markets | Medium term (2-4 years) |

| Uncertain 6G migration road-maps dampening CAPEX | -0.6% | Global, technology leadership regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Small-Cell and DAS Alternatives

Urban carriers favor managed small-cell grids and fiber-fed DAS to assure multi-operator capacity and quality of service. Falling vRAN costs further narrow the price gap with boosters. Venue owners often bundle neutral-host DAS into leasing contracts, sidelining DIY booster installs for malls and stadiums. Despite these pressures, boosters keep an edge in installation speed and permit simplicity for mid-size offices, preserving a resilient albeit contested share of the mobile signal booster market.

Interference Concerns and Grey-Market Devices

Non-certified repeaters sold through overseas e-commerce generate harmful oscillations that degrade macro-cell performance. The FCC’s USD 34.9 million jammer fine exemplifies the crackdown, yet enforcement resources remain finite, particularly outside the United States. Network operators sometimes blanket-block unknown IMEIs, inconveniencing legitimate users and curbing word-of-mouth adoption. Manufacturers must therefore invest in education and traceable supply chains, which raises go-to-market spend and tempers short-term gains in the mobile signal booster market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Boosters Drive Innovation

Smart/digital models accounted for 45.53% of 2024 revenue within the mobile signal booster market share. The feature set includes automatic gain control, self-diagnostics, and AI-enabled interference mitigation, and supports a 9.57% CAGR through 2030. Analog units continue serving budget-conscious households, but shrinking ASP differentials hasten migration to intelligent solutions. Femtocell-based hybrids offer carrier-grade voice hand-off yet require backhaul, limiting traction primarily to enterprises.

Manufacturers increasingly embed cloud APIs, letting IT teams integrate booster telemetry into existing NOC dashboards. This convergence of RF hardware and software services captures value beyond simple amplification, reinforcing premium pricing power inside the mobile signal booster market.

By Technology: 5G Transition Accelerates

4G/LTE held 47.38% of 2024 revenue, marking it the single-largest protocol layer inside the mobile signal booster market size. Nonetheless, shipments tuned for 5G-NR Sub-6 GHz bands are climbing 10.63% annually as carriers sunset 3G and divert 4G spectrum refarming budgets. mmWave-ready SKUs remain niche due to coverage economics but are indispensable for arenas and dense CBD districts.

Regulators unlocking mid-band blocks such as C-band in the United States spur OEM roadmaps toward wideband, multi-service repeaters that auto-detect band combinations. These technical shifts intensify competition yet expand TAM, sustaining double-digit expansion for the mobile signal booster market.

By Distribution Channel: Digital Transformation Accelerates

Offline wholesalers and value-added resellers captured 68.26% of the 2024 turnover across the mobile signal booster market. Their edge lies in site surveys and turnkey installation services for enterprises. E-commerce, however, is gaining momentum at an 11.34% CAGR on the back of improved DIY kits and regulator-curated device lists that reassure buyers about compliance.

Online portals also leverage user reviews and how-to videos to demystify antenna placement, reducing perceived complexity among homeowners. Hybrid click-and-collect models are emerging, letting consumers order online yet pick up units at local installers for same-day support, expanding reach for the mobile signal booster market.

By End-User: Industrial Adoption Surges

Residential premises delivered 39.24% of 2024 revenue, confirming their foundational role in the mobile signal booster market share. Yet industrial facilities are expanding at 10.64% CAGR, outpacing all other segments as factories digitize processes and deploy private 5G. Commercial buildings retain a sizeable slice led by office towers undergoing post-pandemic workplace upgrades.

In mines and ports, boosters aboard autonomous vehicles maintain telemetry links despite metallic reflections. These mission-critical applications justify higher-gain, ruggedized enclosures, raising overall ASPs and profit pools within the mobile signal booster market.

Geography Analysis

North America’s 37.73% revenue share reflects mature telecom infrastructure, FCC-aligned compliance pathways, and rural-broadband subsidies that funnel orders toward certified repeaters.[2]Federal Communications Commission, “Establishing a 5G Fund for Rural America,” fcc.govCarrier partnerships with U.S. fire departments also drive booster installs inside critical-communications networks.

Asia-Pacific, registering a 11.74% CAGR, absorbs shipments into sprawling factory complexes and rapidly expanding metro rail systems that struggle with sub-surface coverage. Aggressive 5G rollouts in China and network densification in India underpin multi-year momentum despite stricter consumer-device rules in Australia and Hong Kong.

Europe enjoys consistent growth as enterprise customers retrofit historical structures where macro signals falter. EU spectrum harmonization simplifies cross-border product SKUs, encouraging OEM investment. Eastern European markets, meanwhile, benefit from structural funds targeting digital infrastructure, further enlarging the region’s slice of the mobile signal booster market.

Competitive Landscape

Competitive intensity remains moderate as top vendors differentiate via AI firmware, regulatory pedigree, and channel breadth. Amphenol’s USD 2.1 billion acquisition of CommScope’s outdoor and DAS units signals consolidation toward end-to-end connectivity portfolios.[3]Amphenol Corporation, “To Acquire Mobile Networks Businesses from CommScope,” amphenol.comWilson Electronics, SureCall, and Nextivity battle on peak gain, band agility, and remote-management UX to secure enterprise contracts.

OEMs increasingly bundle SaaS dashboards, creating sticky subscription revenues that augment hardware margins inside the mobile signal booster market. Carriers co-label certified models, easing consumer device selection while locking out grey-market imports. Entrants focusing on integrated edge compute plus booster modules could reshuffle share in logistics and fleet verticals.

Barriers to entry include multi-jurisdictional certification costs and patent estates covering adaptive echo cancellation. As 5G shifts demand toward wideband designs, legacy analog specialists face either rapid reinvention or niche retreat, accelerating concentration within the mobile signal booster market.

Mobile Signal Booster Industry Leaders

Wilson Electronics, LLC

SureCall

Nextivity, Inc.

TESSCO Technologies Incorporated

Stella Doradus Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sonim Technologies posted 13% revenue growth on rugged hotspot launches and international expansion.

- May 2025: The FCC barred non-compliant test labs from the U.S. approval process, safeguarding certification integrity.

- November 2024: Airgain launched the next-generation Airgain Connect Fleet gateway, expanding mobile-platform coverage for transportation clients.

- October 2024: Mobix Labs recorded 44% sequential quarterly revenue growth, driven by 5G IC and wireless-system solutions complementary to boosters.

Global Mobile Signal Booster Market Report Scope

| Analog Signal Booster |

| Smart/Digital Signal Booster |

| Femtocell-Based Booster |

| Residential |

| Commercial Buildings |

| Industrial Facilities |

| Transportation and Vehicles |

| 3G / UMTS |

| 4G / LTE |

| 5G-NR Sub-6 GHz |

| 5G-NR mmWave |

| Online |

| Offline |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Analog Signal Booster | ||

| Smart/Digital Signal Booster | |||

| Femtocell-Based Booster | |||

| By End-User | Residential | ||

| Commercial Buildings | |||

| Industrial Facilities | |||

| Transportation and Vehicles | |||

| By Technology | 3G / UMTS | ||

| 4G / LTE | |||

| 5G-NR Sub-6 GHz | |||

| 5G-NR mmWave | |||

| By Distribution Channel | Online | ||

| Offline | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the mobile signal booster market in 2025?

The mobile signal booster market size is USD 10.16 billion in 2025 and is projected to expand to USD 15.35 billion by 2030.

Which product category grows fastest through 2030?

Smart/digital boosters post the highest 9.57% CAGR as AI features and remote management become must-have capabilities.

Why are industrial facilities adopting boosters so quickly?

Thousands of IoT sensors and private 5G networks inside factories require deterministic coverage, driving a 10.64% CAGR for industrial deployments.

Which region offers the highest growth potential?

Asia-Pacific leads with a 11.74% CAGR, supported by rapid 5G rollout, mega-factory construction, and urban-rail expansion.

How do government subsidies affect market demand?

Programs such as the USD 9 billion 5G Fund for Rural America finance coverage in underserved areas, directly boosting unit volumes.

What is the main competitive threat to signal boosters?

Managed small-cell and DAS installations offer carriers tighter network control, especially in dense urban venues, pressuring booster share.

Page last updated on: