Plant-based Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

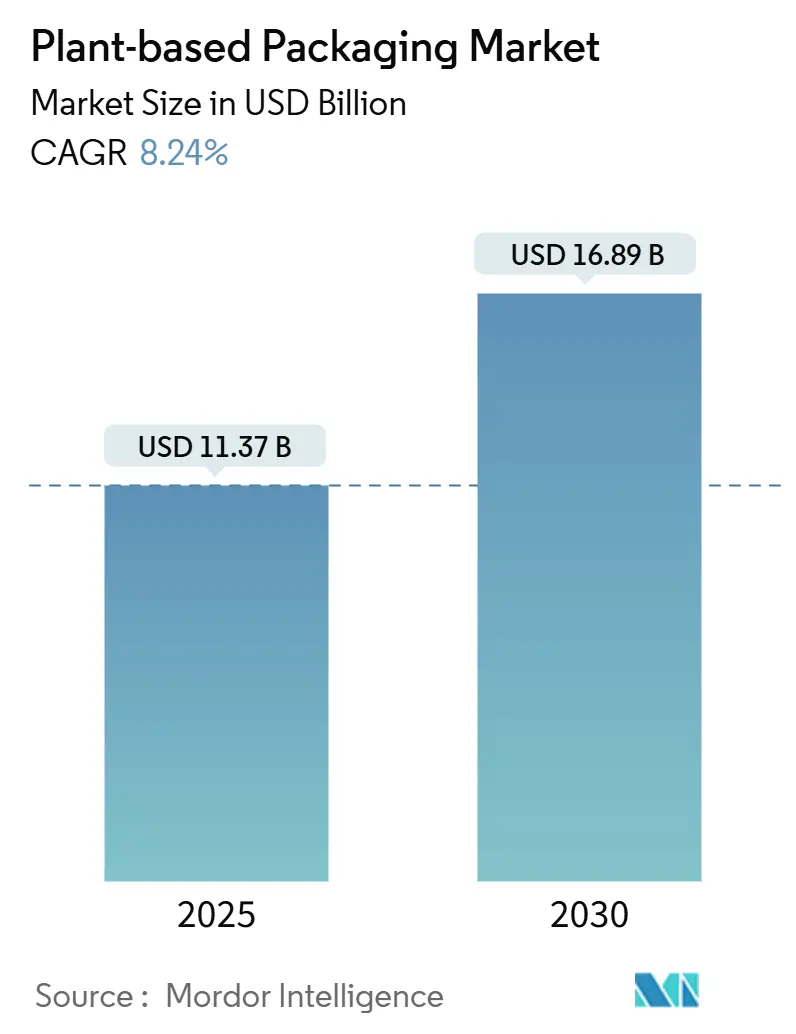

| Market Size (2025) | USD 11.37 Billion |

| Market Size (2030) | USD 16.89 Billion |

| Growth Rate (2025 - 2030) | 8.24% CAGR |

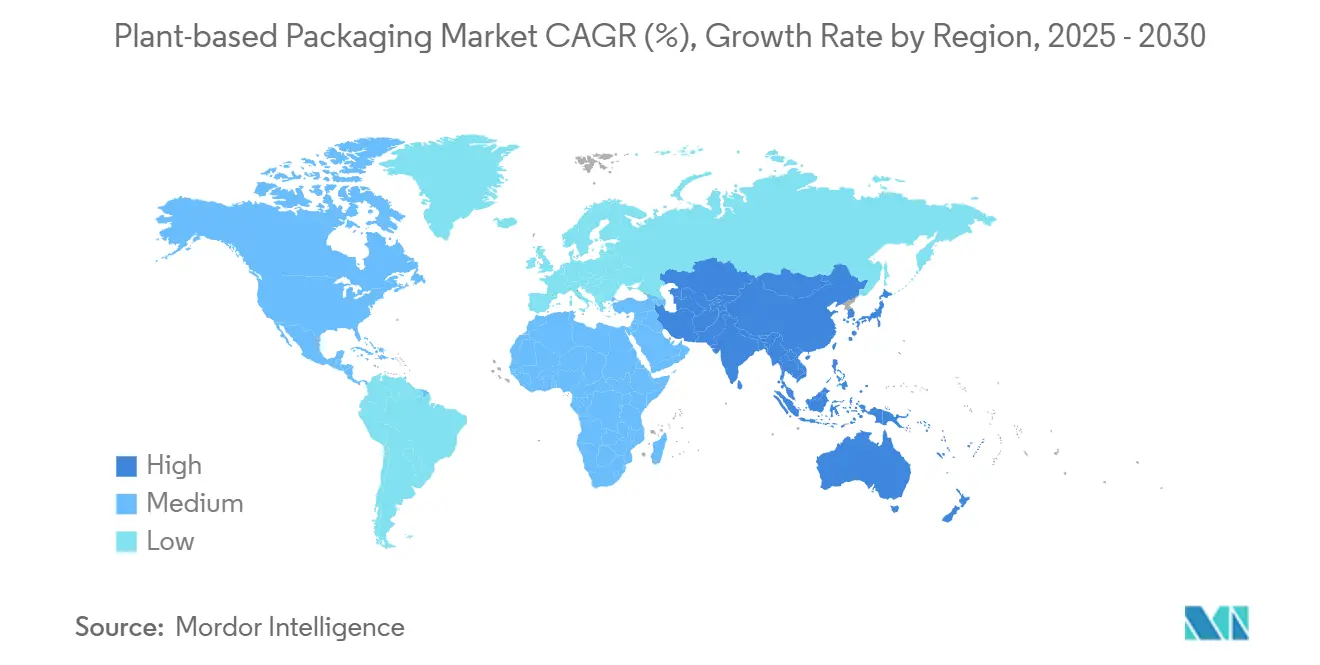

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plant-based Packaging Market Analysis by Mordor Intelligence

The Plant-Based Packaging Market size is valued at USD 11.37 billion in 2025 and is projected to reach USD 16.89 billion by 2030, advancing at an 8.24% CAGR. Growing legislative pressure, brand decarbonization pledges, and cost convergence between bio-based resins and PET are steering procurement teams toward low-carbon materials. Europe continues to enforce some of the world’s most stringent extended producer responsibility rules, while the Asia-Pacific region accelerates capacity additions to serve regional bans on virgin plastics. Cost drops in PHA and PLA production, carbon pricing on fossil polymers, and the rise of e-commerce fulfillment programs that reward compost-ready packaging have combined to give the plant-based packaging market traction in both premium and mass segments. Parallel growth in industrial composting capacity further strengthens the value chain, reducing the infrastructure hurdle that once limited commercial uptake.

Key Report Takeaways

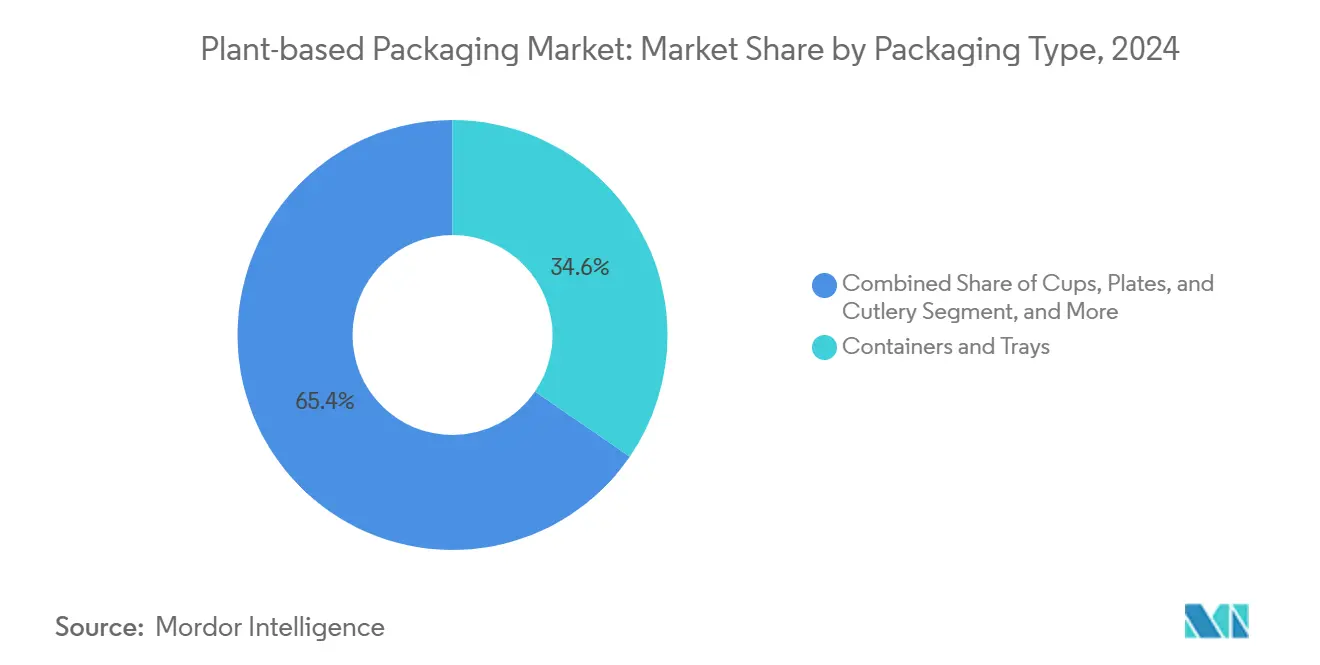

- By packaging type, the containers and trays segment captured 34.58% of the Plant-Based Packaging Market share in 2024.

- By material, the Plant-Based Packaging Market size for Polyhydroxyalkanoates (PHA) is projected to grow at a 9.98% CAGR between 2025–2030.

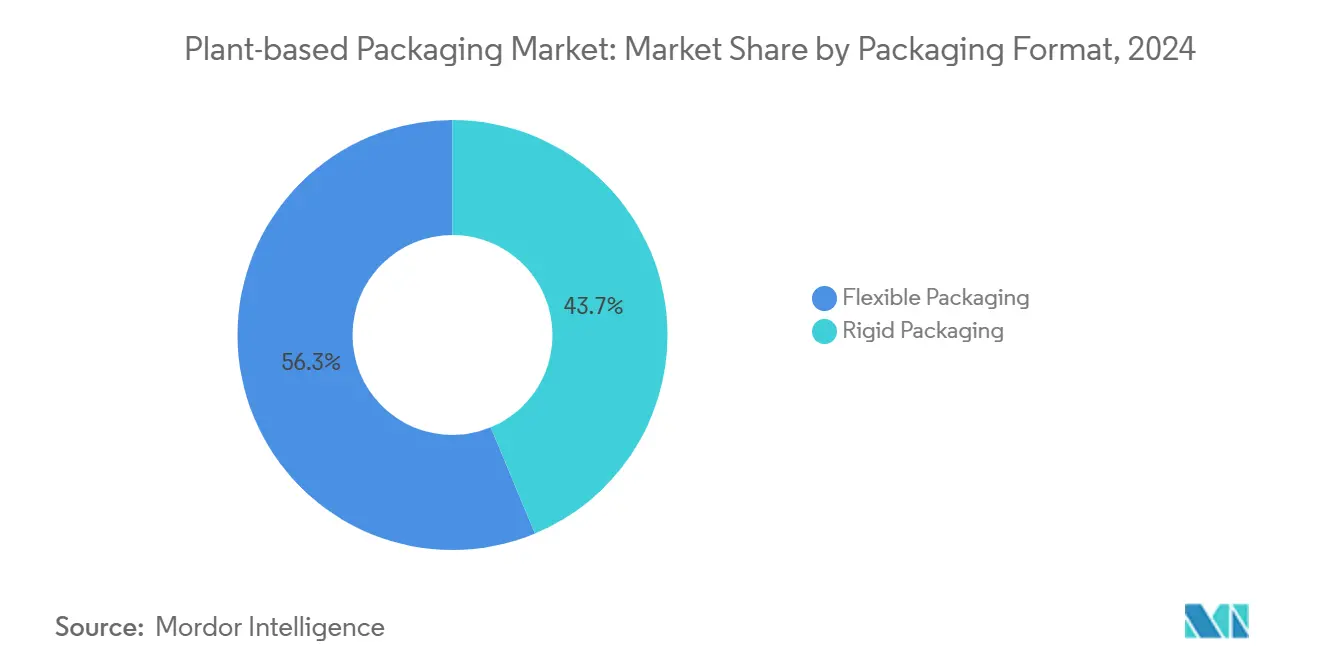

- By format, the rigid solutions segment captured 43.74% of the Plant-Based Packaging Market revenue share in 2024.

- By end-user industry, the Plant-Based Packaging Market size for pharmaceuticals is projected to grow at a 9.63% CAGR between 2025–2030.

- By geography, the Europe segment captured 33.17% of the Plant-Based Packaging Market share in 2024.

Global Plant-based Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food and Beverage brand decarbonization targets | +1.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Extended producer-responsibility (EPR) roll-outs | +2.1% | Europe and North America core, expanding to APAC | Short term (≤ 2 years) |

| Bio-based resin cost convergence with PET | +1.5% | Global, with manufacturing hubs in Asia-Pacific | Long term (≥ 4 years) |

| Millennial and Gen-Z ethical purchasing power | +1.2% | North America and Europe primary, emerging in APAC urban centers | Medium term (2-4 years) |

| Compost-ready e-commerce fulfilment demand | +0.9% | Global, concentrated in major e-commerce markets | Short term (≤ 2 years) |

| Advance purchase agreements for novel fibres | +0.7% | North America and Europe, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food and Beverage brand decarbonization targets

Global consumer goods leaders have imposed strict deadlines for reducing packaging emissions. Firms such as Unilever aim to reduce virgin plastic use by half within the next two years, creating a predictable shift toward bio-based formats.[1]Unilever plc, “Sustainable Packaging Commitments Update 2025,” unilever.com Packaging can account for up to one-fifth of a brand’s total carbon footprint, so shifting to plant-based substrates represents a measurable step toward achieving science-based targets. High-volume contracts signed by multinational bottlers give resin makers the confidence to invest in larger fermenters and downstream equipment. As production scales, price gaps with petro-polymers narrow and the plant-based packaging market gains further momentum. Capital expenditure decisions now factor in the shadow cost of carbon, rendering renewable materials economically rational even in mainstream SKUs.

Extended producer-responsibility roll-outs

European and North American lawmakers have transferred collection and recycling costs from taxpayers to brand owners. The EU Packaging and Packaging Waste Regulation obliges producers to finance the full end-of-life chain, while California’s SB 54 applies a USD 0.02 per-gram fee on non-recyclable plastics. These rules reveal the true lifecycle cost of conventional polymers and shift procurement toward alternatives with lower disposal costs. Dedicated EPR funds also bankroll municipal composting lines, solving a critical bottleneck for biodegradable formats. As EPR frameworks spread into the Asia-Pacific, suppliers with certified compostable products occupy a stronger competitive position.

Bio-based resin cost convergence with PET

PLA and PHA producers have lowered their cost curves through feedstock optimization and continuous fermentation technology. Average PLA manufacturing expense fell from USD 3.50 kg in 2020 to USD 2.80 kg in 2024, while PHA costs dropped by 35% in the same period. Carbon pricing schemes that add up to USD 0.30 per kilogram of virgin polymers accelerate parity. Machinery manufacturers have introduced extruders optimized for biopolymer rheology, which can boost yield by up to 15%. As operating margins improve, converters allocate more line time to renewable resins, further anchoring the plant-based packaging market.

Millennial and Gen-Z ethical purchasing power

Young consumers show a willingness to pay double-digit premiums for environmentally responsible products. Surveys reveal that three-quarters of shoppers under 40 actively consider packaging sustainability when making purchasing decisions. This demographic trend extends into B2B procurement as younger managers adopt climate-positive sourcing policies. Online marketplaces now badge plant-based packaging solutions, nudging algorithms to rank them higher in search results. Brands that comply win shelf space and digital visibility, reinforcing volume growth across categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited food-contact certifications for some biopolymers | -0.8% | Global, with strictest impact in North America and Europe | Medium term (2-4 years) |

| Supply-chain volatility for agricultural residues | -0.6% | Global, with highest impact in agricultural regions | Short term (≤ 2 years) |

| Under-developed industrial composting infrastructure | -1.1% | Global, most severe in developing markets | Long term (≥ 4 years) |

| Competitive pricing pressure from recycled plastics | -0.9% | Global, intensifying in cost-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited food-contact certifications for some biopolymers

The FDA and EFSA require extensive migration testing before new materials are used in direct food contact. PHA approvals remain limited to narrow molecular-weight windows, leaving fatty or hot-fill items outside the current scope. The approval process can take more than two years and cost over USD 1 million, potentially delaying commercialization. Startups often need to focus on secondary packaging first, which can slow down payback periods and deter investors. Brands with multipack portfolios may postpone their plant-based transitions until certification hurdles are eased.

Competitive pricing pressure from recycled plastics

Rapid advances in chemical recycling have lowered post-consumer PET prices to nearly USD 1/kg in 2024, widening the gap with PLA. Major beverage companies pledge to use 50% recycled content, securing large supply contracts that keep r-PET demand robust. Legislators sometimes grant fee reductions or tax credits to recycled-content packaging, creating a preferential treatment that compostables seldom enjoy. In cost-sensitive categories, such as bottled water, the price delta can outweigh the gains from sustainability marketing, thereby restraining the addressable slice of the plant-based packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Foodservice Drives Rigid Alternatives

Containers and trays accounted for a 34.58% share of the plant-based packaging market in 2024, as quick-service restaurants replaced polystyrene with bio-based rigid packaging. Several U.S. cities have banned foam clamshells, prompting national chains to revise their supplier contracts. The segment benefits from setup efficiencies because most filler lines require minimal retooling when shifting from PET to PLA variants. Clear, tamper-evident lids fashioned from plant-derived resins also support the growth of fresh-meal delivery, adding incremental tonnage. Regulatory support remains strong, with 250 local jurisdictions incentivizing the use of compostable takeout containers through waste-hauler fee rebates.

Growth in cups, plates, and cutlery outpaces every other category at a 9.76% CAGR. Music festivals, sports arenas, and university campuses have adopted closed-loop composting programs that favor single-use fiberware. Product innovation now includes hot-cup linings made from water-based dispersions that eliminate traditional polyethylene barriers. Films and pouches retain relevance where oxygen and moisture control are mission-critical, especially in snack foods and ready-to-eat produce. Retail bag mandates in regions such as New York have revived interest in compostable carrier bags that meet ASTM D6400 standards. Niche items, including plant-based bottle caps and engineered closure systems, round out the portfolio, giving brands a full suite of renewable options.

By Material Type: Paper Dominance Faces Biopolymer Challenge

Paper and paperboard secured 44.68% of the plant-based packaging market size in 2024 by leveraging mature forestry supply chains and an expanding network of curbside compost facilities. The material meets migration standards without requiring complex re-registration and integrates seamlessly with existing print-and-form equipment. Pulp mills have begun applying novel barrier coatings that withstand high grease and moisture environments, thus encroaching on territory once reserved for multilayer plastics. Investor funding for pulping capacity remains stable, supported by consistent feedstock forecasts across Scandinavia and North America.

PHA leads material innovation with a 9.98% CAGR, the fastest among its peers. Its marine-biodegradable nature aligns with coastal policy objectives, especially in Southeast Asia, where plastic pollution harms fisheries. Manufacturers like Danimer have blended PHA with natural fibers to improve stiffness, allowing lightweight thermoform applications. Starch blends are used in cost-sensitive outlets, including agricultural mulch film and single-day eventware, where the functional lifespan is inherently short. PLA advances in high-heat grades unlock applications such as microwaveable ready meals and hot-fill beverage liners. Cellulose composites and seaweed-based films occupy premium niches, differentiating upscale cosmetic and electronics packaging through tactile and visual cues.

By Packaging Format: Flexibility Gains Ground

Rigid packaging achieved a 43.74% revenue share in 2024 due to its structural rigidity and compatibility with legacy filling lines. Transparent clamshells display produce while offering drop protection, satisfying both aesthetic and logistical needs. Rigid jars made with plant-based resin help nut-butter brands hit recycled-content goals that glass cannot meet, given weight considerations. Recycling systems also recognize rigid shapes more readily, minimizing contamination concerns in mixed collection streams.

Flexible formats achieve a faster 9.37% CAGR, fueled by e-commerce. Lightweight mailers reduce shipping emissions and cut dimensional-weight fees. Multilayer biofilms now incorporate moisture and oxygen barriers that rival those of petroleum laminates, extending the shelf life of pantry staples. Pouch-based refills enable bulk sales, reducing the use of unit-dose plastics in personal care. Some suppliers introduce drop-in bio-based EVOH replacements, solving historical seal-strength issues. Hybrid formats blend rigid shells with flexible lids, optimizing cost and disposal paths. Format decisions often trace back to available end-of-life options: rigid items are sent to mechanical recyclers, while flexibles are routed to composters or anaerobic digesters.

By End-user Industry: Healthcare Accelerates Adoption

The food and beverage sector represented 46.67% of demand in 2024. Fast-casual chains rely on certified compostables to meet municipal zero-waste targets, and grocers utilize plant-based trays to reduce scope-3 emissions in fresh produce. Shelf-ready designs feature QR codes linking to disposal instructions, enhancing consumer compliance. Thermal resistance upgrades allow chilled ready-meal trays to endure conventional reheating cycles, broadening category coverage.

Pharmaceuticals emerge as the fastest climber at a 9.63% CAGR. Regulators now encourage blister packs with bio-based films and fiber-based inserts that replace PVC. Child-resistant paper-PHA composites receive FDA 510(k) clearance, reducing landfill load without sacrificing barrier integrity. Consumer electronics buyers expect eco-labels, motivating handset makers to abandon plastic trays inside gift boxes. High-end cosmetics incorporate molded-fiber shells lined with plant-based wax for water resistance, appealing to luxury buyers who are keen on plastic-free, premium experiences. Automotive and industrial components explore pallet footprint reduction via foldable biofilm wraps that cut reverse logistics costs.

Geography Analysis

Europe retained 33.17% of global revenue in 2024, underscored by the legally binding Packaging and Packaging Waste Regulation. France accelerated its exit from single-use plastics by mandating reusable dinnerware for on-premise dining as early as 2025, forcing quick-service chains to adopt compostable lines. Germany’s Green Dot fees penalize hard-to-recycle plastics, making biopolymers financially attractive in chilled convenience foods. A dense network of 5,000 municipal composting plants supports post-consumer collection, minimizing leakage into mixed waste streams. However, stiff competition from low-cost recycled PET and limited domestic biomass feedstock creates supply tensions that could moderate growth velocity.

Asia-Pacific posts the highest 9.45% CAGR through 2030. China’s latest Five-Year Plan lists the scale-up of biodegradable materials as a strategic objective, enabling local producers to access preferential financing.[2]Ministry of Ecology and Environment of China, “Five-Year Plan for Biodegradable Materials,” mee.gov.cn India’s Plastic Waste Management Rules impose producer responsibility certificates, rewarding companies that deploy certified compostables in sachets and courier pouches. Japan pilots enzymatic depolymerization of PLA, bolstering the reuse of monomers for a closed-loop supply chain. Proximity to sugarcane and cassava feedstocks lowers variable costs, making the region a logical export base for multinational converters serving the plant-based packaging market. Variability in national standards remains a hurdle, yet trade associations push for harmonization to facilitate intra-Asian flows.

North America shows steady but diversifying demand. California’s SB 54 drives state-level momentum, mirrored by Washington and Oregon. The United States FDA maintains a rigorous food-contact notification pathway, pushing converters toward established PLA and paper formulations to speed market entry. Canada’s federal ban on specific single-use items extends uptake into quick-service chains nationwide. Mexico leverages free-trade corridors and abundant agricultural residues such as agave bagasse to add bio-polymer capacity for both domestic and export sales. The continent’s composting infrastructure lags Europe, but capital commitments from private waste haulers signal a turning point.

Competitive Landscape

The market balances scale and specialization. Amcor and Huhtamaki possess global sales footprints and substantial R&D budgets, investing more than USD 400 million annually in circular-economy projects. Recent acquisitions, such as Huhtamaki’s takeover of BioPak, plugged regional portfolio gaps and granted immediate access to foodservice clients in Asia.

Amcor’s alliance with Stora Enso on fiber-based barrier packs attacks the flexible-laminate stronghold of petro-plastics, targeting multibillion-dollar run rates over the next five years.[3]Amcor plc, “Sustainability Report 2025: Advancing Circular Economy Solutions,” amcor.com On the specialist front, TIPA and Evoware compete on innovation speed rather than brute capacity. TIPA’s latest Series C round allocates capital to scale its home-compostable film lines beyond Europe. Evoware taps Indonesian seaweed farmers, hedging against price swings in corn and sugar feedstocks commonly used in mainstream PLA.

Patent filings cluster around extrusion screw designs and enzymatic degradation accelerants, forming IP moats that complicate fast-follower strategies. Contract manufacturing deals between agricultural processors and resin firms shorten supply chains and lower landed costs. The competitive narrative increasingly pivots on end-of-life credibility, as marine degradability and circular-traceability apps become tipping points in RFP scoring.

Plant-based Packaging Industry Leaders

Amcor plc

Huhtamäki Oyj

Sealed Air Corporation

Mondi plc

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Danimer Scientific announced a USD 120 million expansion in Kentucky to triple PHA capacity by 2027, targeting 25% cost reduction once the line is fully automated.

- September 2025: Amcor partnered with Stora Enso to commercialize plastic-free barrier packaging projected to generate USD 2 billion in annual revenue across North America and Europe.

- August 2025: Huhtamaki completed an USD 85 million acquisition of BioPak Australia, adding compostable foodservice ranges to its Asia-Pacific footprint.

- July 2025: TIPA closed a USD 70 million Series C to scale compostable film production and accelerate EU food-contact approvals.

Global Plant-based Packaging Market Report Scope

| Containers and Trays |

| Films and Pouches |

| Cups, Plates,and Cutlery |

| Bags and Sacks |

| Other Packaging Types |

| Paper and Paperboard |

| Starch-based Biopolymers |

| Polylactic Acid (PLA) |

| Cellulose and Plant-Fibre Composites |

| Polyhydroxyalkanoates (PHA) |

| Other Material Types |

| Rigid Packaging |

| Flexible Packaging |

| Food and Beverage |

| Consumer Electronics |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| E-commerce and Retail |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Containers and Trays | ||

| Films and Pouches | |||

| Cups, Plates,and Cutlery | |||

| Bags and Sacks | |||

| Other Packaging Types | |||

| By Material Type | Paper and Paperboard | ||

| Starch-based Biopolymers | |||

| Polylactic Acid (PLA) | |||

| Cellulose and Plant-Fibre Composites | |||

| Polyhydroxyalkanoates (PHA) | |||

| Other Material Types | |||

| Packaging Format | Rigid Packaging | ||

| Flexible Packaging | |||

| By End-user Industry | Food and Beverage | ||

| Consumer Electronics | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| E-commerce and Retail | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the plant-based packaging market in 2030?

The market is forecast to reach USD 16.89 billion by 2030.

Which region will expand the fastest in plant-based packaging between 2025 and 2030?

Asia-Pacific is expected to post a 9.45% CAGR, the highest among all regions.

Which packaging type holds the largest share in the plant-based format market today?

Containers and trays lead with 34.58% share in 2024.

Why are pharmaceuticals adopting plant-based packaging rapidly?

Regulatory guidance encourages lower-impact drug delivery systems, helping the category grow at a 9.63% CAGR.

How does cost convergence with PET influence adoption?

Falling PLA and PHA production costs, combined with carbon pricing on fossil plastics, narrow the price gap and strengthen economic viability.

What is the top restraint slowing wider uptake?

Limited food-contact certifications for emerging biopolymers extend approval timelines and increase compliance costs.

Page last updated on: