Seaweed-Based Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

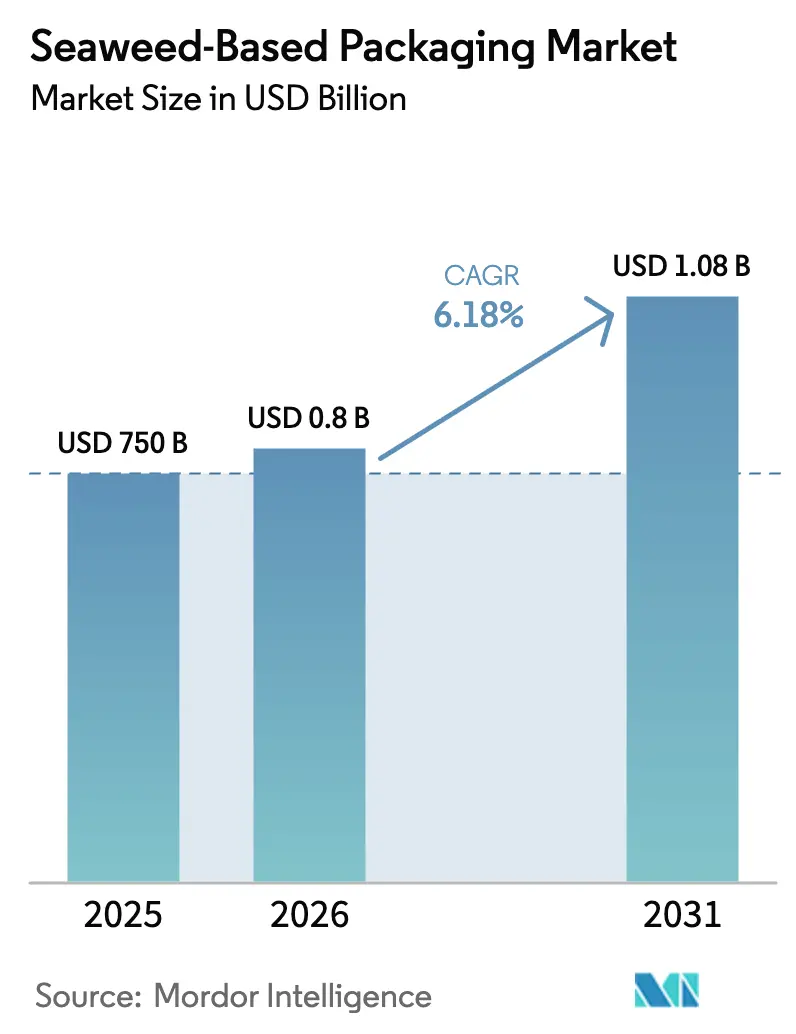

| Market Size (2026) | USD 0.8 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

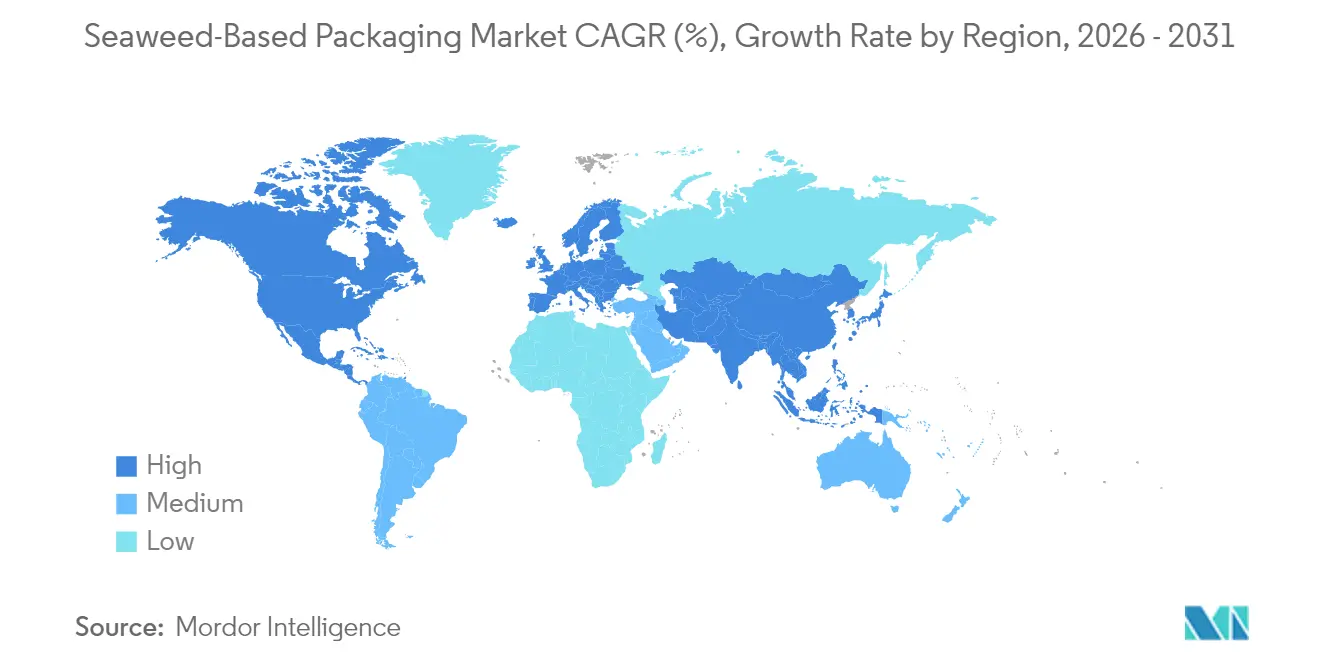

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

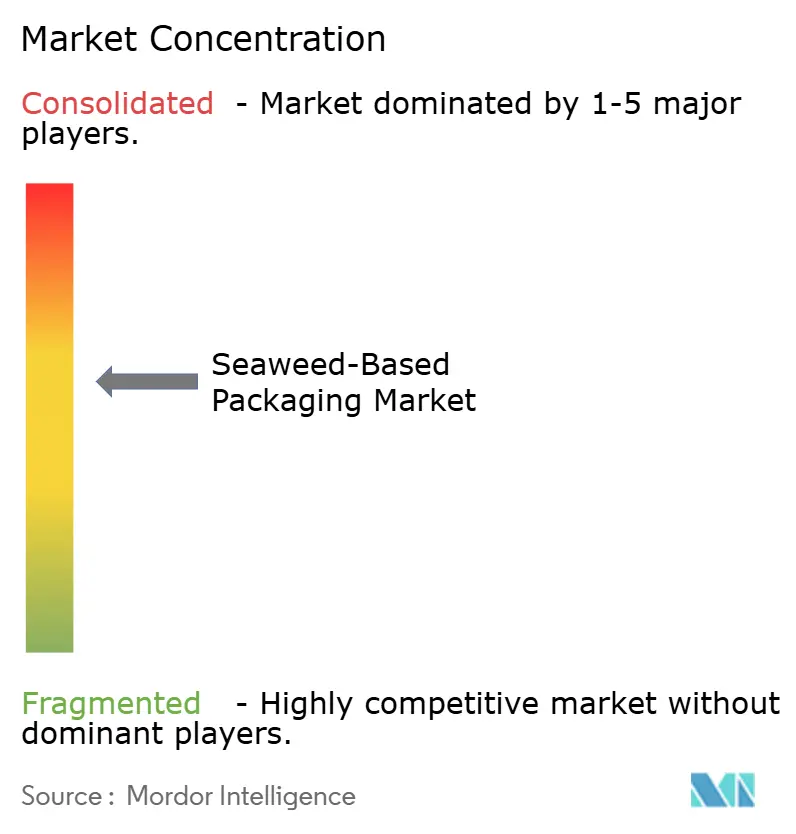

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Seaweed-Based Packaging Market Analysis by Mordor Intelligence

The Seaweed-Based Packaging Market size was valued at USD 750 million in 2025 and estimated to grow from USD 796.35 million in 2026 to reach USD 1.08 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031). Strong regulatory pressure to phase out single-use plastics, rapid progress in seaweed-based resin technology, and monetization of blue-carbon credits together fuel steady demand. Brand owners view marine-derived materials as a route to meet Scope 3 carbon targets, while co-location of offshore wind and aquaculture assets lowers production costs. Films remain the largest application, but pouches are scaling quickly as e-commerce accelerates the shift from rigid to flexible formats. In parallel, blended bio-polymer pellets are gaining traction because they run on existing plastics machinery, shortening buyers’ transition timelines.

Key Report Takeaways

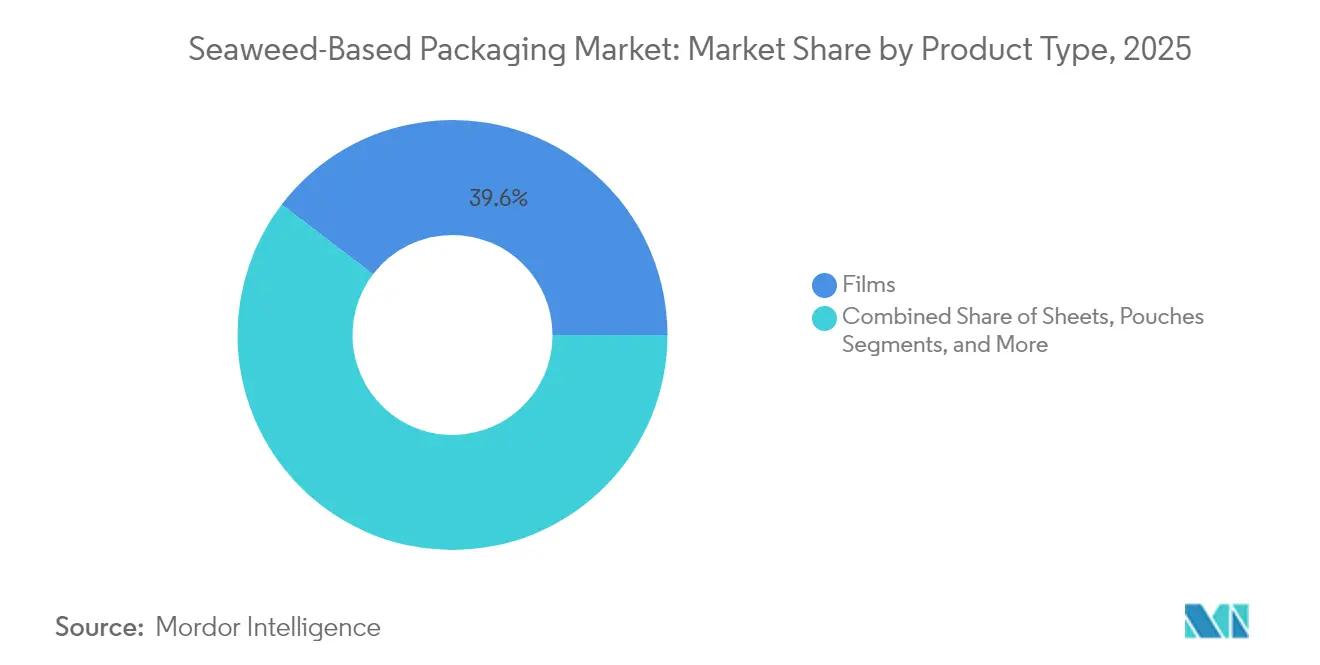

- By product type, films led with 39.62% of seaweed packaging market share in 2025; pouches are projected to expand at a 9.05% CAGR to 2031.

- By material composition, alginate captured 35.05% revenue share in 2025, while blended pellets are advancing at an 8.3% CAGR through 2031.

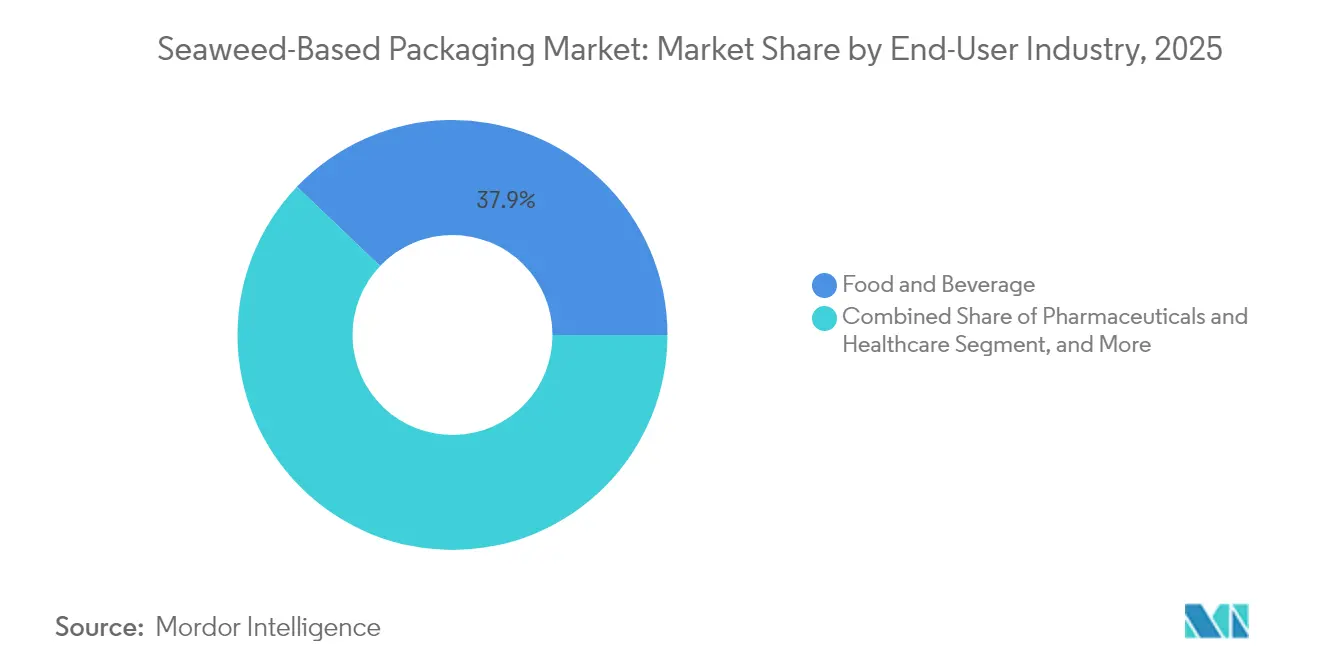

- By end-user industry, food and beverage held 37.88% of the seaweed packaging market size in 2025; pharmaceuticals and healthcare post the fastest CAGR at 9.1% to 2031.

- By distribution channel, direct sales commanded 58.02% revenue share in 2025 and are growing at 7.65% CAGR as suppliers prioritise controlled fulfilment.

- By geography, Asia-Pacific dominated with 37.94% revenue share in 2025 and is set to expand at a 9.63% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Seaweed-Based Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid bans on single-use plastics worldwide | +1.8% | Global, with early adoption in EU and APAC | Short term (≤ 2 years) |

| Brand-owner shift to science-based carbon targets | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Cost-down breakthroughs in seaweed resin compounding | +0.9% | Global, led by North America innovation hubs | Medium term (2-4 years) |

| Co-location of seaweed farms with offshore wind assets | +0.7% | Europe & North America coastal regions | Long term (≥ 4 years) |

| Retailer EPR fees favour bio-sourced packaging | +0.6% | EU, UK, expanding to North America | Short term (≤ 2 years) |

| Blue-carbon credits monetisation for seaweed suppliers | +0.4% | Global coastal regions with carbon markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid bans on single-use plastics worldwide

Nation-level restrictions that entered force in 2025, including New South Wales’ comprehensive ban on designated disposable formats, have moved buyers to seek immediately compliant alternatives.[1]Environment Protection Authority, “Plastics bans and packaged food and drinks,” epa.nsw.gov.auThe European Union’s prohibition of Bisphenol A in food-contact materials adds further urgency for converters that depend on regulated chemicals to shift toward naturally derived solutions. Russia’s upcoming 2025 constraints on specific PET structures heighten global supply disruption, encouraging procurement teams to lock in seaweed based supply contracts. As authorities extend enforcement to the entire value chain, the seaweed packaging market gains a compliance advantage that outweighs price premiums, particularly in quick-service food and retail applications. Short transition windows compress innovation cycles, favouring vendors already equipped with scalable capacity.

Brand-owner shift to science-based carbon targets

Major consumer brands linked executive compensation to Scope 3 emissions reduction in 2024, making low-carbon packaging procurement a board-level priority. Standardised life-cycle assessment frameworks for marine materials now enable precise carbon reporting, and suppliers that document cultivation-level sequestration win preference in tenders. Packaging intensity scores integrated into on-pack labelling strengthen the business case for seaweed solutions because shoppers reward credible climate claims. The ability to generate future blue-carbon credits positions seaweed-based formats as a two-way value lever: instant footprint cuts plus potential offset revenue.

Cost-down breakthroughs in seaweed resin compounding

Thermoplastic resins such as TPSea™ exhibit melt behaviour compatible with commodity extrusion and moulding lines, eliminating the need for dedicated kit and cutting switchover risk. Enzyme-assisted extraction improves alginate quality while lowering energy input, and zero-waste biorefining monetises side streams from the same biomass. AI-enabled process control boosts yield and labour efficiency, narrowing today’s price gap to fossil plastics. These converging innovations set the seaweed packaging market on a path to volume economics in high-throughput segments by the second half of the decade.

Co-location of seaweed farms with offshore wind assets

The Netherlands commissioned the first commercial seaweed farm inside a wind array in 2024, proving dual-use of ocean infrastructure.[2]About Amazon, “World's first commercial-scale seaweed farm located between offshore wind turbines is now open in the Netherlands,” aboutamazon.eu Shared mooring, vessels, and renewable power lower cultivation and processing costs, while regulators begin issuing integrated licences that streamline project approvals. As more North Sea and US Atlantic leases adopt this template, cultivation capacity could expand without pushing into ecologically sensitive near-shore zones—creating long-term supply security for the seaweed packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for commercial-scale seaweed biorefineries | -1.4% | Global, particularly acute in Western markets | Medium term (2-4 years) |

| Price volatility of carrageenan and alginate feedstocks | -0.8% | Global supply chains, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Regulatory uncertainty on "edible packaging" labelling | -0.6% | North America & EU regulatory jurisdictions | Short term (≤ 2 years) |

| Biofouling and disease risks in open-ocean farms | -0.5% | Coastal cultivation regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capex for commercial-scale seaweed biorefineries

Integrated plants that extract carrageenan and alginate require investments above USD 50 million, a threshold difficult to finance without government guarantees or anchor offtake contracts. Specialised equipment cannot be retrofitted from existing plastic plants, raising barriers for start-ups. Facility siting near both coastal biomass sources and end-user hubs often forces dual-site strategies that compound capital. Wastewater systems must handle saline organic effluent, adding further cost layers. The funding gap slows capacity additions and could delay economies of scale in the seaweed packaging market.

Price volatility of carrageenan and alginate feedstocks

Storm-driven crop losses in Indonesia and the Philippines caused 20-30% price swings in 2024, squeezing converters’ margins and complicating long-term agreements. Potential Indonesian export curbs introduce regulatory risk, while limited hedging instruments expose buyers to currency shifts. Unpredictable input costs deter large brands from locking in multi-year supply, moderating near-term volume growth. Vertical integration and blended-material strategies are emerging as hedges but require investment and technical resources that smaller players lack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: films remain core while pouches gain momentum

Films held 39.62% of seaweed packaging market share in 2025, underscoring their compatibility with standard form-fill-seal lines and their balanced barrier performance. Brands in snack foods and fresh produce favour film because it can be down-gauged without compromising visibility. Pouches, however, are projected to deliver a 9.05% CAGR as e-commerce pushes demand for lightweight, protective formats that cut freight emissions.

The wider shift toward flexible solutions aligns with the move to lower-carbon logistics, and TPSea™ resins specifically target pouch and sachet applications with drop-in processing ability. Edible sachets for condiments in quick-service restaurants illustrate how functionality plus compostability wins regulatory approval and consumer acceptance. Other product groups such as trays and cutlery continue to see incremental gains, but growth skews to flexible formats where seaweed’s water-soluble or home-compostable traits solve end-of-life challenges that haunt rigid bioplastics.

By Material Composition: alginate leads yet blended pellets accelerate

Alginate retained 35.05% revenue share in 2025 on the strength of proven food-contact safety and mature extraction infrastructure. Nevertheless, blended pellets are advancing at an 8.3% CAGR as processors mix seaweed polysaccharides with starches or plant oils to fine-tune melt flow and lower costs. These hybrid inputs decrease dependence on any single feedstock and broaden processing windows on legacy plastics lines.

The seaweed packaging market size for blended materials is forecast to capture wider adoption in cosmetics and personal-care sachets that need both barrier and seal strength. Cellulose–seaweed composites move the technology toward semi-rigid containers, opening opportunities in dry goods and pharmaceuticals. Continuous R&D in enzymes and green solvents is expected to enhance purity and stability, reinforcing alginate’s role while supporting a multi-material future.

By Packaging Function: flexible films set the pace as barrier coatings rise

Compostable flexible films generated 44.71% of 2025 revenues, positioning them as the anchor function for the seaweed packaging market. Their dominance stems from the clear route to establish municipal compost collection in many cities and successful pilot programmes in hospitality chains. Barrier coatings on fibre substrates, posting a 7.28% CAGR, let converters use existing paperboard while replacing fluorinated coatings now under regulatory scrutiny.

Edible films open premium niches in pre-measured beverage powders and seasoning packets, eliminating secondary waste entirely. Rigid bioplastics lag in growth because injection moulding requires higher thermal stability; however, process tweaks using seaweed-cellulose blends are closing that gap for small medical devices. Over the forecast period, dual-layer constructions that pair seaweed-derived barriers with recycled fibre are likely to enter high-volume snack markets.

By End-User Industry: food leads yet healthcare surges

Food and beverage generated 37.88% of seaweed packaging market revenue in 2025 as brand owners embraced materials that allow edible or home-compostable disposal. Quick-service chains adopted sauce pods and wrap film to meet plastic-ban deadlines, locking in baseline volume. Pharmaceuticals and healthcare are forecast to rise at a 9.1% CAGR thanks to alginate’s biocompatibility and regulatory familiarity from drug-delivery uses.

The sector shift reflects hospital procurement policies that target reduced plastic waste in sterile packaging and wound-care components. Cosmetic brands also test seaweed sachets for single-dose creams, using the narrative of ocean-positive sourcing to capture sustainability-minded consumers. Across categories, clear chain-of-custody data on cultivation origin is becoming a prerequisite, giving vertically integrated suppliers a commercial edge.

By Distribution Channel: direct relationships dominate in an emerging market

Direct sales accounted for 58.02% of revenue in 2025 and continue to grow at 7.65% CAGR because converters require hands-on technical guidance during initial trials. Close collaboration shortens qualification cycles and lets suppliers collect performance feedback that feeds product iterations.

As the seaweed packaging market scales, indirect distribution will expand, particularly for standard grades with published technical data sheets. Even so, leading suppliers are expected to maintain hybrid models, using direct engagement for complex, high-margin applications and channel partners for commodity SKU rollouts. This approach mirrors specialty-chemical industry evolution and balances reach with application know-how.

Geography Analysis

Asia-Pacific generated 37.94% of global revenue in 2025 and is forecast to grow at 9.63% CAGR. China’s Jiangsu coast remains the largest cultivation zone, though disease pressures are nudging farmers toward disease-resistant breeds and offshore lines. South Korea set a new export record of KRW 1 trillion in 2024 and plans to reach KRW 1.3 trillion by 2027, signalling state-level backing for seaweed-based value chains. Indonesia and the Philippines continue to supply most carrageenan feedstock, yet potential export barriers keep buyers cautious.

Europe combines innovation leadership with regulatory incentives. The Netherlands’ wind-farm-integrated acreage validates a scalable cultivation model, and UK EPR fees in 2025 give financial preference to compostable formats. France’s decision to expand EPR to fishing gear opens a marine-application niche that favours ocean-origin polymers. Venture funding into Notpla and Kelpi underscores investor confidence that European innovators can capture premium market segments.

North America positions itself as a technology hub. Sway’s Department of Energy grant and National Science Foundation award advance drop-in resin chemistry, while state-level EPR schemes in Maine, Oregon, and California add demand pull. Domestic cultivation remains modest, but the USDA projects a USD 733 million seaweed sector by 2030, providing feedstock security for local processors.Strategic partnerships between US resin developers and Asian growers already bridge the supply gap while technology transfer initiatives aim to localise farming on both Atlantic and Pacific coasts.

Competitive Landscape

Competition is moderaltely consolidated and dynamic, with venture-backed start-ups attracting more than USD 40 million in equity during 2024. Established processors focus on high-volume alginate and carrageenan, but face margin compression when feedstock prices spike. Start-ups such as Notpla, Sway, Kelpi, and B’ZEOS use patent-protected extraction or compounding technologies to differentiate on performance and traceability.

Two strategic camps are forming. Legacy suppliers leverage existing scale, distribution, and long-term supply agreements, while newcomers integrate vertically, handle cultivation trials, and partner directly with brand owners for co-development pilots. The latter pathway accelerates learning loops and guides resin design around real-world performance criteria.

Mergers or capacity-sharing alliances are likely as manufacturing costs rise. Potential tie-ups would let scale-curious start-ups access proven extraction assets without committing to full plant builds, and would provide established processors with intellectual-property inflow. Over the next five years, cost-down progress and brand adoption rates will determine which business models create sustainable competitive moats in the seaweed packaging market.

Seaweed-Based Packaging Industry Leaders

Notpla Limited

Sway Innovation Co.

B'ZEOS Switzerland SA

Zerocircle Alternatives Pvt. Ltd.

Evoware

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sea Vegetable launched the “Delicious Suji Aonori Project” to expand culinary seaweed use and fund aquaculture research.

- January 2025: Notpla raised more than EUR 25 million to scale home-compostable seaweed packaging into North America.

- November 2024: B’ZEOS secured EUR 5 million to upscale compostable packaging production in partnership with multinational food manufacturers.

- November 2024: Sway and Umaro won a USD 1.5 million US Department of Energy grant to convert alginate by-products into thermoplastic resins.

Global Seaweed-Based Packaging Market Report Scope

Seaweed-derived plastic is 100% biodegradable and ecologically friendly, providing a viable solution to the environmental crisis caused by single-use plastics. Seaweed based biodegradable packaging is gaining popularity in the food industry as a sustainable alternative to traditional packaging materials. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The seaweed-based packaging market is segmented by product type (Sheets, Films, Pouches, Boxes and Other Products), by end- user industry (Food, Personal Care & Cosmetics, Pharmaceuticals, Retail and Other End-User Industries) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Sheets |

| Films |

| Pouches |

| Boxes and Trays |

| Straws and Cutlery |

| Other Product Type |

| Alginate-based |

| Carrageenan-based |

| Agar-based |

| Cellulose–Seaweed Composites |

| Blended Bio-polymer Pellets |

| Edible Films and Coatings |

| Compostable Flexible Films |

| Rigid Bio-Plastics |

| Barrier Coatings for Paper/Card |

| Food and Beverage |

| Foodservice and Hospitality |

| Personal Care and Cosmetics |

| Pharmaceuticals and Healthcare |

| Retail and E-commerce |

| Other End-User Industry |

| Direct Sales |

| Indirect Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Sheets | ||

| Films | |||

| Pouches | |||

| Boxes and Trays | |||

| Straws and Cutlery | |||

| Other Product Type | |||

| By Material Composition | Alginate-based | ||

| Carrageenan-based | |||

| Agar-based | |||

| Cellulose–Seaweed Composites | |||

| Blended Bio-polymer Pellets | |||

| By Packaging Function | Edible Films and Coatings | ||

| Compostable Flexible Films | |||

| Rigid Bio-Plastics | |||

| Barrier Coatings for Paper/Card | |||

| By End-User Industry | Food and Beverage | ||

| Foodservice and Hospitality | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals and Healthcare | |||

| Retail and E-commerce | |||

| Other End-User Industry | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the seaweed packaging market?

The seaweed packaging market is valued at USD 796.35 million in 2026 and is projected to reach USD 1.08 billion by 2031.

Which region generates the highest revenue for seaweed-based packaging?

Asia-Pacific leads with 37.94% revenue share in 2025 and is expanding at a 9.63% CAGR through 2031.

What application segment is growing fastest within the market?

Pouches show the quickest rise, registering a 9.05% CAGR as brands pivot to flexible formats suitable for e-commerce shipping.

Why are pharmaceutical companies adopting seaweed-derived packaging?

Regulatory familiarity with alginate and its proven biocompatibility enable safe contact with medical products, driving a 9.1% CAGR in the healthcare segment.

How do single-use plastic bans influence market demand?

Nation-level bans create immediate compliance gaps, prompting brands to substitute restricted materials with seaweed-based alternatives that meet both safety and compostability standards.

What is the main obstacle to rapid capacity expansion?

High upfront investment—often exceeding USD 50 million per integrated biorefinery—slows large-scale build-outs and delays economies of scale for new entrants.

Page last updated on: