Picture Archiving Communications Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

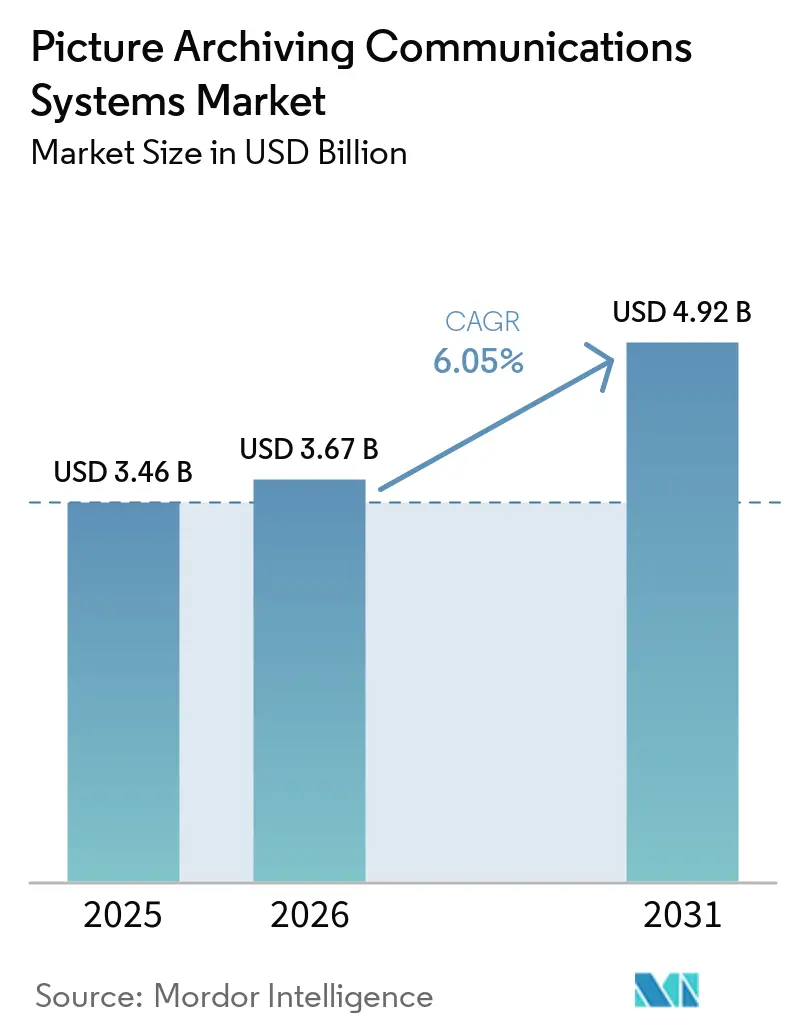

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 4.92 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

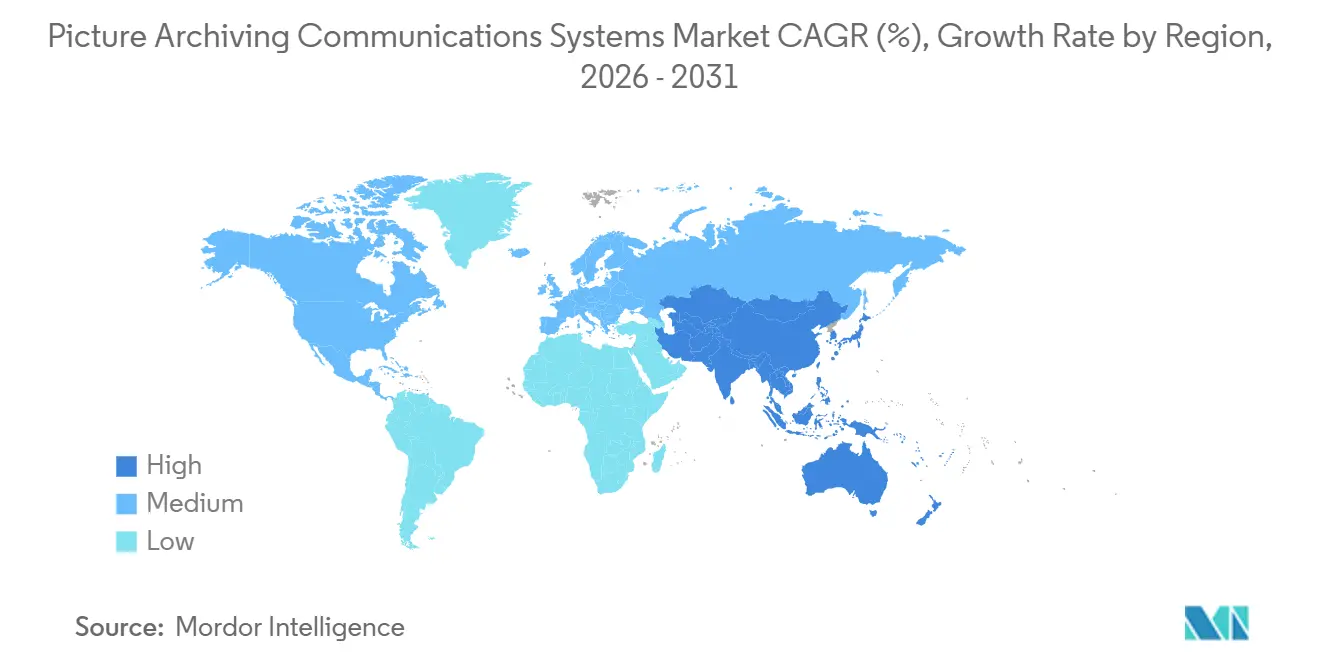

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Picture Archiving Communications Systems Market Analysis by Mordor Intelligence

The Picture Archiving Communications Systems Market size is expected to increase from USD 3.46 billion in 2025 to USD 3.67 billion in 2026 and reach USD 4.92 billion by 2031, growing at a CAGR of 6.05% over 2026-2031.

The market is growing as health systems move away from department-based imaging repositories and adopt enterprise imaging platforms that connect radiology, cardiology, and oncology workflows through a shared architecture, and large multihospital deployments continue to reinforce that direction. The Picture Archiving Communications Systems market is also being shaped by cloud and hybrid delivery, which lower hardware management needs, support remote reading, and make cross-site standardization easier for providers facing staffing pressure. Demand is also rising because imaging volumes continue to expand, cancer care workflows are becoming more data intensive, and providers need scalable storage and orchestration tools that can support higher exam throughput without slowing clinical use. Competition is tightening as leading vendors use acquisitions, large enterprise contracts, and workflow automation features to widen their installed base and deepen platform dependence across health networks. The main constraints remain legacy integration friction, long-term storage economics, and stricter privacy and cybersecurity obligations, all of which can slow deployment and reduce the financial appeal of full cloud migration for some providers.

Key Report Takeaways

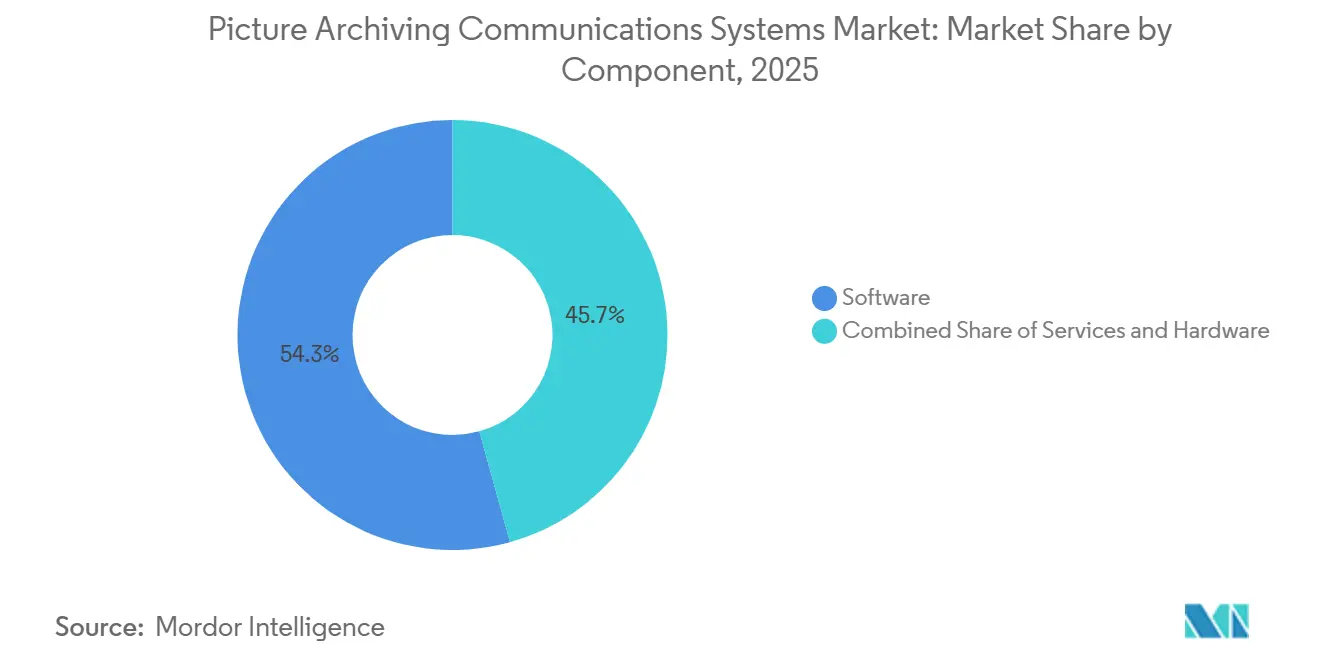

- By component, software led with 54.31% revenue share in 2025, while services is forecast to expand at a 7.38% CAGR through 2031.

- By deployment mode, cloud-based held 56.24% revenue share in 2025, while hybrid is projected to record the highest CAGR of 8.52% through 2031.

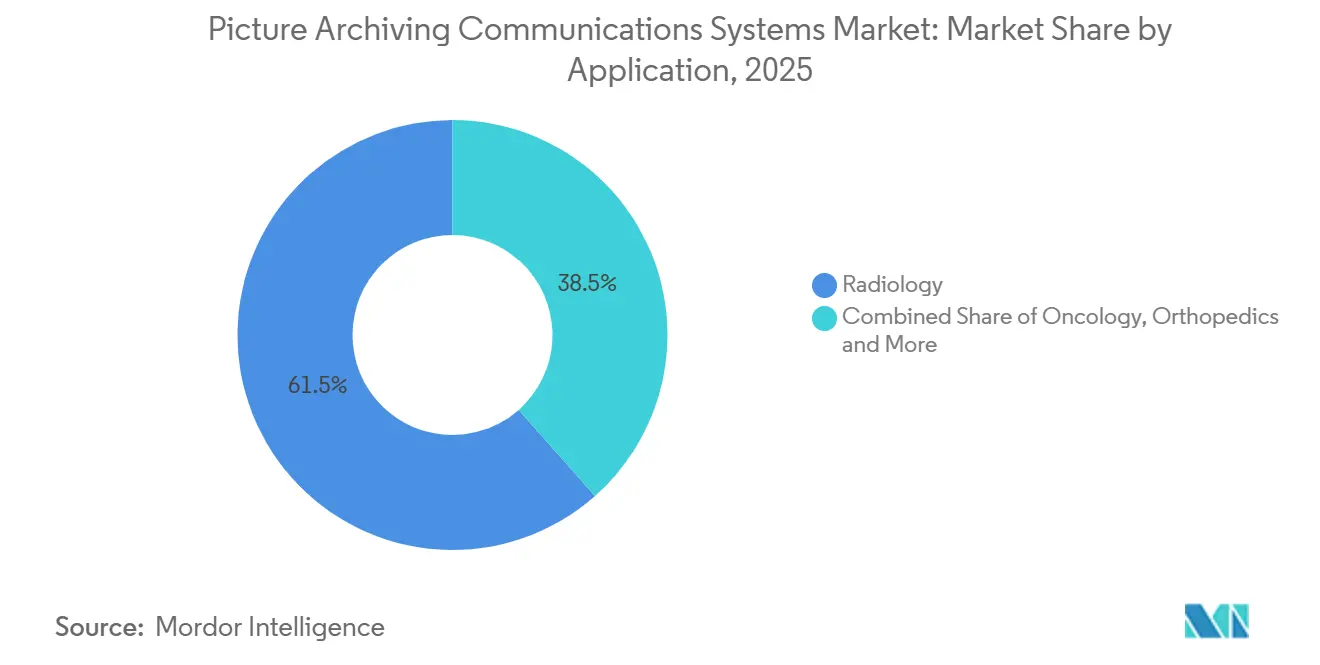

- By application, radiology accounted for 61.52% revenue share in 2025, while oncology is expected to advance at an 8.25% CAGR through 2031.

- By end user, hospitals and clinics captured 68.52% revenue share in 2025, while diagnostic imaging centers are forecast to grow at an 8.25% CAGR through 2031.

- By geography, North America held 40.22% of revenue in 2025, while Asia-Pacific is projected to expand at a 7.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Picture Archiving Communications Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Enterprise Imaging And Cross-Department Workflow Standardization | +1.2% | North America and Europe | Medium term (2-4 years) |

| Cloud Migration To Reduce Infrastructure Burden And Enable Remote Reading | +1.5% | Global | Short term (≤ 2 years) |

| Growing Imaging Volumes From Chronic Disease And Aging Populations | +0.9% | Global, concentrated in Asia-Pacific and North America | Long term (≥ 4 years) |

| Interoperability Demand Across RIS, EHR, VNA, And AI Tools | +0.7% | North America and Europe | Medium term (2-4 years) |

| AI-Assisted Triage, Routing, And Worklist Optimization | +0.8% | North America, early Asia-Pacific | Medium term (2-4 years) |

| Rising Teleradiology And Multi-Site Health System Consolidation | +0.6% | North America, with spillover to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud Migration To Reduce Infrastructure Burden And Enable Remote Reading

The Picture Archiving Communications Systems market is seeing its clearest shift in deployment, as providers move from on-premise systems to cloud-delivered platforms that are easier to scale across locations. In this market, cloud software reduces upfront hardware spending, avoids repeated server refresh cycles, and turns backup and recovery into a managed service instead of a long internal project. The Picture Archiving Communications Systems market is also benefiting from consolidation across multihospital systems, because adding acquired facilities to a cloud architecture is often simpler than building separate local infrastructure at each site. Philips had already migrated more than 150 sites in North America and Latin America to HealthSuite Imaging on Amazon Web Services before it extended the service across 13 European markets in February 2025, and the company tied that expansion to staffing pressure and AI-enabled workflow improvement. That pattern matters for the Picture Archiving Communications Systems market because it links cloud adoption to workforce and network management rather than to storage alone. It also explains why hybrid models are rising quickly, since providers often move long-term archive and advanced processing first while keeping time-sensitive reading functions close to local workflows.

AI-Assisted Triage, Routing, And Worklist Optimization

The Picture Archiving Communications Systems market is increasingly tying growth to workflow intelligence, because AI is moving from a stand-alone add-on into the core of image routing and reading prioritization. Research covering 62 hospitals and 2.2 million radiology studies found that rule-based worklists created 17.7-minute delays for expedited cases and generated annual costs of USD 2.1 million to USD 4.2 million per hospital network, which makes automation a practical purchasing issue rather than a trial feature[1]Amazon Web Services, “Intelligent Radiology Workflow Optimization With AI Agents,” AWS Machine Learning Blog, aws.amazon.com. Vendors in the Picture Archiving Communications Systems market are now using AI to direct studies by urgency, radiologist specialty, live workload, and case complexity, which improves throughput where reading teams are spread across sites. A large peer-reviewed analysis of 46.4 million U.S. radiology examinations also showed that high-volume radiologists were carrying much heavier reading loads by 2024, which supports demand for workload balancing tools within enterprise imaging environments. That detail matters in the Picture Archiving Communications Systems market because providers are not only seeking faster triage, they are also trying to distribute work more evenly across networks. As those capabilities mature, PACS selection is likely to depend more on orchestration quality and less on image storage alone.

Growing Imaging Volumes From Chronic Disease And Aging Populations

The Picture Archiving Communications Systems market continues to draw support from a steady rise in imaging demand, and that demand is tied to aging populations and higher chronic disease burden across health systems. A peer-reviewed study of 46.4 million examinations across 167 radiology facilities showed that U.S. radiology exam volume in Q1 2024 stood 31% above the earlier study baseline, which confirms sustained pressure on storage, retrieval, and reading workflows. Separate research projected that population aging alone will account for 12% to 27% of future imaging utilization growth in the United States, while population growth will contribute a much larger share, which points to a broad volume base rather than a short-lived surge[2]Mythreyi Bhargavan-Chatfield, “Projected US Imaging Utilization, 2025 to 2055,” Radiology, pubmed.ncbi.nlm.nih.gov. Cancer care adds to that burden, since annual U.S. case volumes are projected to rise from 2.4 million to 3.4 million by 2045, and that trend supports heavier oncology imaging use and larger multiphase image archives. NHS England reported 49.9 million imaging tests in the year to March 2025, up 5.9% year over year, which shows that the same pressure is visible in another major health system. For the Picture Archiving Communications Systems market, this means capacity planning is becoming a continuing operational need rather than a periodic infrastructure decision.

Rising Enterprise Imaging And Cross-Department Workflow Standardization

The Picture Archiving Communications Systems market is moving beyond radiology-only deployments, as health systems standardize imaging across radiology, cardiology, pathology, and point-of-care workflows. This shift matters because a shared archive and viewer can reduce duplicate exams, support tumor board collaboration, and give clinicians access to imaging across departments without switching between several systems. In the Picture Archiving Communications Systems market, that creates longer implementation programs and deeper platform dependence, since a single deployment increasingly touches many departments and many years of archived images. FUJIFILM announced in May 2026 that Ardent Health selected Synapse Enterprise Imaging across 30 acute care hospitals and more than 280 sites of care in 6 U.S. states, covering radiology and cardiology under a unified viewer integrated with Epic EHR. The Picture Archiving Communications Systems market therefore gains from a broader buying scope, because each enterprise imaging project extends beyond storage into workflow design, interoperability, governance, and clinical collaboration. It also raises switching barriers, since replacing a cross-department system is much harder than replacing a single radiology archive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Data Egress, Archival Storage, And Long-Term Retention | -0.8% | Global | Long term (≥ 4 years) |

| Legacy DICOM, HL7, And Workflow Integration Friction | -0.6% | North America and Europe | Medium term (2-4 years) |

| Cybersecurity, Privacy, And Data Residency Compliance Burden | -0.5% | Global, acute in Europe and Asia-Pacific | Medium term (2-4 years) |

| Cloud Vendor Lock-In And Migration Complexity | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity, Privacy, And Data Residency Compliance Burden

The Picture Archiving Communications Systems market handles some of the most sensitive patient data in the clinical setting, so compliance requirements carry real weight in product selection and rollout timing. The U.S. Department of Health and Human Services issued a proposed HIPAA Security Rule amendment on December 27, 2024, that would require encryption of electronic protected health information at rest and in transit, multifactor authentication, regular vulnerability scanning, and network segmentation[3]HHS Office for Civil Rights, “HIPAA Security Rule Notice of Proposed Rulemaking to Strengthen Cybersecurity for Electronic Protected Health Information,” U.S. Department of Health and Human Services, hhs.gov. For the Picture Archiving Communications Systems market, that means providers can no longer delay many security upgrades that were once treated with more flexibility. In Europe, data sovereignty obligations add another layer because vendors often need regional hosting and country-specific processing arrangements, which makes cloud design more complex. These burdens slow the Picture Archiving Communications Systems market most in mid-sized providers, where IT security staffing is limited and procurement cycles stretch when legal and technical reviews grow. They also reinforce the advantage of vendors that can package compliance support as part of a managed imaging platform.

High Cost Of Data Egress, Archival Storage, And Long-Term Retention

The Picture Archiving Communications Systems market gains from cloud migration, but the cost structure changes once retrieval activity and long retention periods are considered. NHS England reported 49.9 million imaging tests in the year to March 2025, and that 5.9% annual increase shows how fast retrieval-heavy archives can grow when imaging demand keeps rising. A 2025 European Radiology study found that long-term CT data storage creates substantial cost and environmental burden, and it noted that cloud archival can lower emissions by 40% to 80% while also shifting providers toward retrieval-based pricing. In the Picture Archiving Communications Systems market, that tradeoff is especially important for outpatient imaging operators that retrieve studies often and must keep them for many years. Long medical record retention obligations keep adding to that exposure, which can weaken the financial case for full cloud migration even when the operational case is strong. This is why the Picture Archiving Communications Systems market is showing growing interest in tiered storage, with active studies kept in warmer environments and older data moved into lower-cost archive layers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue While Services Extend Platform Value

Software commanded 54.31% of revenue in 2025, and it represented the largest share of the Picture Archiving Communications Systems market share because vendors have shifted value toward subscriptions, analytics modules, AI functions, and enterprise workflow tools. The Picture Archiving Communications Systems market has moved away from hardware-led setups, and cloud-native vendors now generate more revenue from recurring platform access than from physical infrastructure. That transition is visible in GE HealthCare’s March 2026 disclosure on Intelerad, where the acquired business was described as having approximately USD 270 million in annual revenue with more than 90% recurring revenue and more than 30% EBITDA margin. Hardware still matters for high-throughput workstations and modality-adjacent devices, but its role is more supportive in the Picture Archiving Communications Systems market as browser-based viewing and remote access tools improve. This keeps software at the center of differentiation, because image management alone no longer defines vendor value.

Services is the fastest-growing component at a 7.38% CAGR through 2031, and that part of the Picture Archiving Communications Systems market is expanding as providers seek outside help for implementation, integration, migration, and managed operations. Longer enterprise imaging programs have turned one-time deployment work into multiyear service revenue, especially where radiology, cardiology, and other departments are being brought onto a common platform. In the Picture Archiving Communications Systems industry, services also deepen vendor stickiness because much of the work involves linking PACS with EHR, RIS, VNA, and AI tools across several sites. That means service contracts do more than support go-live activities, they also shape the success of later workflow changes and archive expansion. As enterprise rollouts become broader and more complex, services should keep gaining importance as both a revenue stream and a retention tool.

By Deployment Mode: Cloud-Based Crosses The Majority Threshold, Hybrid Grows Fastest

Cloud-based deployment captured 56.24% of revenue in 2025, and it accounted for the largest share of the Picture Archiving Communications Systems market size because SaaS delivery reduced hardware buying friction and supported distributed reading models. The Picture Archiving Communications Systems market has favored cloud deployment where providers want automatic upgrades, security patching, compliance support, and easier expansion across facilities. Philips positioned its HealthSuite Imaging model in that way, noting that the service handles ongoing updates and security needs as part of the managed offering. That proposition has become more relevant as imaging directors deal with staff shortages and older server environments. Cloud leadership in the Picture Archiving Communications Systems market therefore reflects both financial and operational preferences, not just a change in hosting location.

Hybrid is the fastest-growing deployment mode at an 8.52% CAGR through 2031, and that growth shows how providers are balancing newer cloud tools with existing local investments. In the Picture Archiving Communications Systems market, hybrid models let health systems move long-term archive and AI processing into the cloud while retaining low-latency reading flows for high-priority studies on site. This approach fits multihospital networks that already own useful infrastructure and want a gradual migration path instead of a single large cutover. On-premise deployments still remain in settings with strict sovereignty rules, including some academic, defense, and national healthcare environments, though their share is declining across the forecast period. Web-based access also plays a bridging role in the Picture Archiving Communications Systems market because it gives clinicians lighter image review access through broader clinical systems without requiring full workstation licensing.

By Application: Radiology Leads Volume, Oncology Reshapes Strategic Value

Radiology retained 61.52% of revenue in 2025, and it remained the largest application in the Picture Archiving Communications Systems market because it has the highest exam volumes and the deepest DICOM workflow standardization. The Picture Archiving Communications Systems market still leans heavily on radiology as its installed base, and that makes radiology the anchor for most enterprise imaging contracts. Even so, vendor strategy is widening, because the same archive and viewer layers are now being used to bring cardiology, orthopedics, and other image-rich specialties onto shared infrastructure. FUJIFILM and Siemens Healthineers have both advanced cross-department imaging strategies that support this broader positioning, which reflects the market’s move toward platform consolidation rather than specialty isolation. Radiology’s lead should therefore remain durable, but the use case around it is becoming much broader.

Oncology is the fastest-growing application at an 8.25% CAGR through 2031, and that growth reflects a more strategic role for imaging in cancer screening, treatment planning, and response tracking. In the Picture Archiving Communications Systems market, oncology workflows require integrated handling of PET, CT, and MRI studies across repeated treatment cycles, which raises the value of structured retrieval, annotation, and longitudinal comparison. Springer Nature reported that radiomics pipelines are increasingly being embedded into PACS and RIS infrastructure, which helps automate feature extraction, image retrieval, and clinical workflow steps inside existing systems. This makes oncology different from a simple volume story, because procurement often becomes part of a clinical strategy discussion rather than only a radiology IT choice. Smaller specialty areas such as ophthalmology and veterinary imaging are also opening room for niche growth, but oncology is the segment that most clearly changes how enterprise value is defined.

By End User: Hospital Anchor Meets Imaging Center Acceleration

Hospitals and clinics generated 68.52% of revenue in 2025, and they held the largest share of the Picture Archiving Communications Systems market because they need multidepartment image management, broader modality coverage, and longer enterprise contracts. The Picture Archiving Communications Systems market continues to depend on hospitals as its core customer base, since large systems can justify major archive consolidation and integration programs. FUJIFILM’s May 2026 agreement with Ardent Health shows that scale clearly, as the deployment covers 30 acute care hospitals and more than 280 sites of care across 6 U.S. states with radiology and cardiology under one viewer integrated with Epic EHR. These contracts matter because they combine image storage, workflow standardization, and long-term platform dependence in one buying decision. The hospital segment therefore remains the main revenue anchor even as delivery models evolve.

Diagnostic imaging centers are the fastest-growing end-user segment at an 8.25% CAGR through 2031, and that pace reflects the ongoing movement of advanced imaging into lower-cost outpatient settings. In the Picture Archiving Communications Systems market, these centers often prefer cloud-delivered tools with limited on-site IT requirements, because that supports faster expansion across distributed locations. Their operating model also benefits from remote reading, centralized administration, and lighter deployment requirements than hospital campuses usually need. Ambulatory surgery centers are increasing PACS use in orthopedic and ophthalmic workflows, while other end users such as research centers and veterinary networks are gaining access through subscription pricing that lowers upfront barriers. This means the Picture Archiving Communications Systems market is broadening beyond hospital walls, even though hospitals still generate the largest revenue base.

Geography Analysis

North America held 40.22% of revenue in 2025, and it accounted for the largest regional share of the Picture Archiving Communications Systems market share because the region combines mature payer systems, large integrated delivery networks, and strong cloud adoption capacity. The Picture Archiving Communications Systems market in North America is also being pushed by multihospital consolidation, since acquired community facilities are often folded into larger enterprise imaging plans. Sectra signed a five-year Sectra One Cloud enterprise imaging contract in June 2026 with four Ontario healthcare providers across 16 sites and an estimated 3.6 million imaging exams, which shows how city-wide and regional standardization models are now moving into larger network settings. The American College of Radiology also pressed in March 2026 for FHIR ImagingStudy and ImagingSelection resources to be treated as core interoperability tools, which supports deeper integration between imaging systems and EHR environments. These conditions make North America the most established region in the Picture Archiving Communications Systems market, while still leaving room for replacement cycles and broader enterprise rollouts.

Asia-Pacific is the fastest-growing region at a 7.15% CAGR through 2031, and it is the main growth engine for the Picture Archiving Communications Systems market over the forecast period. The region is being supported by hospital digitization in China, rapid scaling of diagnostic center networks in India, and a replacement cycle in Japan that is tied more closely to compliance and system integration needs. In the Picture Archiving Communications Systems market, these drivers favor vendors that can support multistage deployment, remote administration, and lower infrastructure burden across mixed provider environments. Asia-Pacific also stands out because many providers are building or upgrading imaging networks while still deciding how much infrastructure to keep local and how much to shift into managed environments.

Europe is positioned for stable growth in the Picture Archiving Communications Systems market, supported by hospital modernization programs and procurement structures that can favor enterprise-scale imaging platforms. The region also has a tougher compliance setting, and that tends to benefit larger vendors with stronger regulatory and hosting capabilities. The Middle East and Africa represent an emerging opportunity in the Picture Archiving Communications Systems market because medical tourism investment, cross-border care ambitions, and radiologist shortages all raise the value of cloud-enabled image sharing and teleradiology support. South Africa and select West African markets are adopting cloud PACS to improve access across dispersed networks, which mirrors earlier teleradiology-led adoption patterns seen in other regions. South America, led by Brazil and Argentina, is also moving forward as private hospital groups upgrade legacy imaging environments, though currency volatility and import costs continue to slow the pace of investment in some cases.

Competitive Landscape

The Picture Archiving Communications Systems market is moderately concentrated, with a leading group that includes GE HealthCare, Siemens Healthineers, Koninklijke Philips, FUJIFILM, Agfa HealthCare, and Sectra, while a longer tail of cloud-native and specialty vendors competes for mid-market and ambulatory accounts. The Picture Archiving Communications Systems market is not controlled by a single dominant vendor, but scale still matters because enterprise imaging contracts depend on integration depth, hosting capability, clinical workflow breadth, and long support commitments. GE HealthCare materially changed the competitive picture in March 2026 when it completed the USD 2.3 billion acquisition of Intelerad, combining a hospital-focused PACS base with a cloud-first teleradiology platform that had approximately USD 270 million in annual revenue and more than 90% recurring revenue. That move increased pressure on mid-market cloud specialists, because one of the largest imaging vendors now has stronger cloud credibility and a broader installed base. It also pushed the Picture Archiving Communications Systems market further toward competition based on platform breadth rather than storage alone.

Another clear pattern in the Picture Archiving Communications Systems market is the effort to package AI inside the core enterprise imaging offering instead of leaving it to outside marketplaces. FUJIFILM has emphasized workflow orchestration through Synapse Worklist Orchestrator, which supports diagnostic workload balancing and reflects how incumbents are trying to defend workflow territory with proprietary tools. Siemens Healthineers has pursued an open data management approach with Syngo Carbon, bringing PACS, VNA, digital pathology, cardiology, and advanced visualization together under a broader enterprise data layer, which keeps competition centered on connected imaging ecosystems. Sectra has also stayed active in large-scale cloud deployments, and its Ontario contract shows that the company is using network-wide standardization projects to reinforce its position in the enterprise segment. These moves show that the Picture Archiving Communications Systems market is rewarding vendors that combine cloud delivery, workflow intelligence, and enterprise integration under one commercial model.

The Picture Archiving Communications Systems market still leaves room for specialists in outpatient ophthalmology, orthopedics, veterinary imaging, and cross-border teleradiology where lighter cloud-native models can solve narrower workflow problems. Even so, the larger vendors keep gaining leverage because hospitals prefer partners that can cover more departments and more integration points over time. This means new entrants in the Picture Archiving Communications Systems market usually need a very specific clinical, workflow, or deployment advantage to win share. Competitive pressure will likely remain high, but it is most intense around enterprise accounts where long contracts, migration complexity, and archive depth make each replacement decision harder to reverse.

Picture Archiving Communications Systems Industry Leaders

GE HealthCare

Koninklijke Philips N.V.

FUJIFILM Holdings Corporation

Agfa-Gevaert Group

Sectra AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Sectra signed a five-year Sectra One Cloud enterprise imaging contract with four Ontario, Canada healthcare providers, Hamilton Health Sciences, St. Joseph's Healthcare Hamilton, Norfolk General Hospital, and West Haldimand General Hospital, consolidating 16 sites previously operating on 2 separate PACS solutions into a single cloud instance and covering an estimated 3.6 million imaging exams over the contract term. The agreement extends Sectra's city-wide cloud model into a new North American regional health network.

- May 2026: FUJIFILM Healthcare Americas Corporation announced a strategic partnership with Ardent Health to deploy Synapse Enterprise Imaging solutions across Ardent's 30 acute care hospitals and more than 280 sites of care spanning 6 U.S. states, covering radiology and cardiology under a unified Synapse Diagnostic PACS viewer integrated with Epic EHR. The contract represents one of the largest enterprise imaging deployments announced in 2026.

Global Picture Archiving Communications Systems Market Report Scope

As per the scope of the report, Picture Archiving and Communications Systems (PACS) are medical imaging technology systems that securely store and electronically transmit electronic images and associated data. They enable healthcare providers to access and share images such as X-rays, MRIs, CT scans, and ultrasound images quickly and efficiently, improving diagnosis, treatment planning, and patient care.

The Picture Archiving Communications Systems Market is segmented by component into software, hardware, and services. By deployment mode, the market is categorized into on-premise, cloud-based, web-based, and hybrid. By application, it is divided into radiology, cardiology, oncology, orthopedics, ophthalmology, and veterinary medicine. By end user, the market includes hospitals and clinics, diagnostic imaging centers, ambulatory surgery centers, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software |

| Hardware |

| Services |

| On-Premise |

| Cloud-Based |

| Web-Based |

| Hybrid |

| Radiology |

| Cardiology |

| Oncology |

| Orthopedics |

| Ophthalmology |

| Veterinary Medicine |

| Hospitals and Clinics |

| Diagnostic Imaging Centers |

| Ambulatory Surgery Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Deployment Mode | On-Premise | |

| Cloud-Based | ||

| Web-Based | ||

| Hybrid | ||

| By Application | Radiology | |

| Cardiology | ||

| Oncology | ||

| Orthopedics | ||

| Ophthalmology | ||

| Veterinary Medicine | ||

| By End User | Hospitals and Clinics | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgery Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for the Picture Archiving Communications Systems market?

The Picture Archiving Communications Systems market is projected to reach USD 4.92 billion by 2031 from USD 3.67 billion in 2026, growing at a 6.05% CAGR over 2026 to 2031.

Which deployment model currently leads adoption in Picture Archiving Communications Systems?

Cloud-based deployment led with 56.24% of revenue in 2025, showing that providers are favoring managed, scalable imaging environments over hardware-heavy setups.

Which application is growing fastest in Picture Archiving Communications Systems?

Oncology is the fastest-growing application at an 8.25% CAGR through 2031, supported by screening expansion and deeper use of quantitative imaging in treatment workflows.

Why do hospitals remain the main buyers of Picture Archiving Communications Systems platforms?

Hospitals and clinics generated 68.52% of revenue in 2025 because they need multidepartment coverage, enterprise integration, and long-term archive consolidation across many sites.

Which region offers the strongest growth opportunity for vendors?

Asia-Pacific is projected to expand at a 7.15% CAGR through 2031, driven by hospital digitization, diagnostic center expansion, and replacement demand tied to compliance and integration.

What are the main risks slowing Picture Archiving Communications Systems adoption?

The main risks are legacy integration friction, stricter cybersecurity and privacy obligations, and the long-term cost of cloud storage retrieval and retention.

Page last updated on: