Enterprise Imaging Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

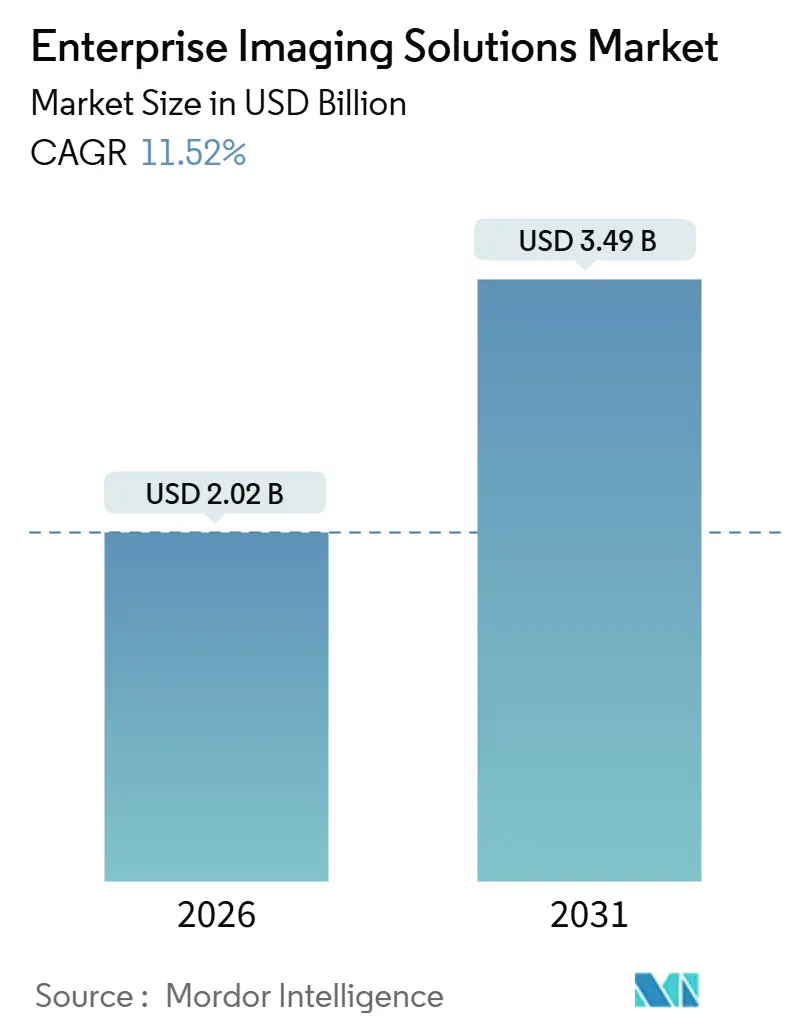

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 3.49 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Imaging Solutions Market Analysis by Mordor Intelligence

The Enterprise Imaging Solutions Market size is estimated at USD 2.02 billion in 2026, and is expected to reach USD 3.49 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

Growth is being shaped by the maturing cloud backbone that now supports elastic DICOM workloads, a surge of FDA-cleared imaging AI models, widening regional image-exchange mandates, and mounting cybersecurity spending that has become a prerequisite for modernization. Heightened value-based reimbursement pressure is steering buyers toward platforms that can embed clinical decision support at the point of order, while large, multi-year “value partnerships” demonstrate that competitive edge now flows from lifecycle AI orchestration rather than hardware refresh cycles. Cloud hyperscalers have entered the field with managed DICOM web services, changing the purchasing calculus for health systems that once defaulted to radiology-centric PACS. At the same time, public-sector funding programs in North America and Asia-Pacific, coupled with workforce shortages, are accelerating the adoption of vendor-managed services to offset limited in-house informatics capacity.

Key Report Takeaways

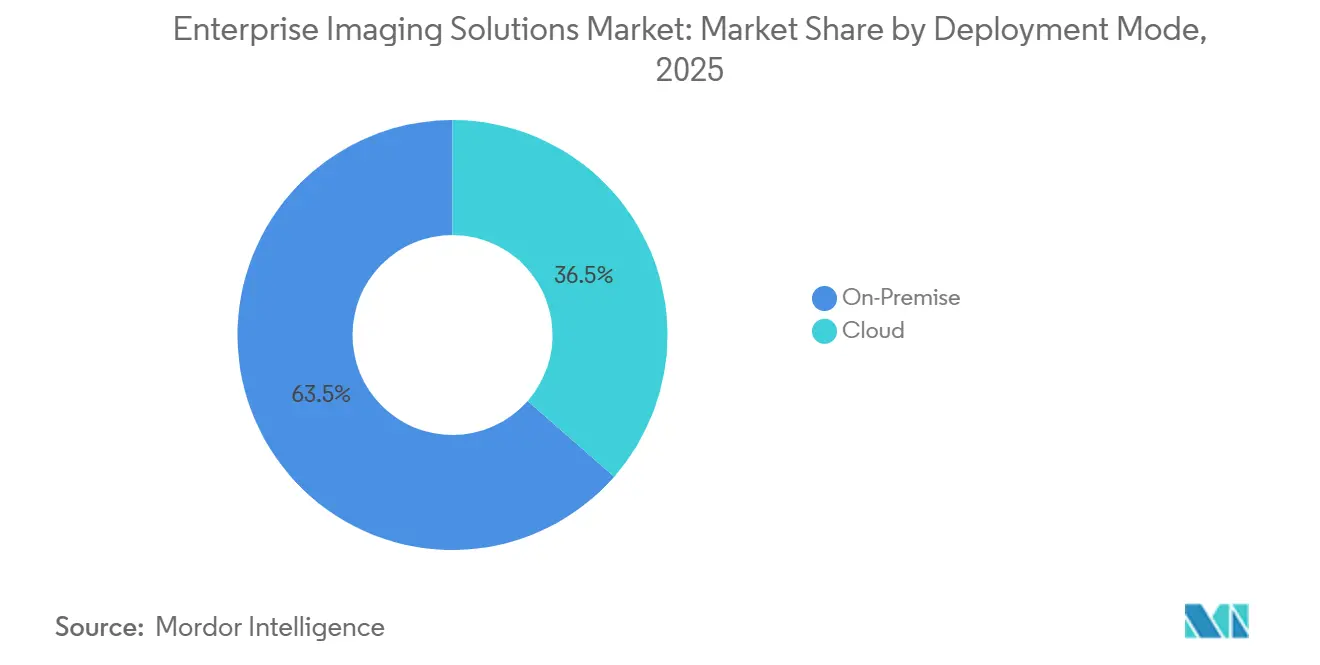

- By deployment mode, cloud captured 63.54% of the enterprise imaging solutions market share in 2025, and its 13.65% CAGR keeps it the fastest-advancing option to 2031.

- By solution type, vendor-neutral archives led with 36.76% revenue share in 2025, while image-exchange platforms recorded the top growth trajectory at a 13.82% CAGR through the end of the decade.

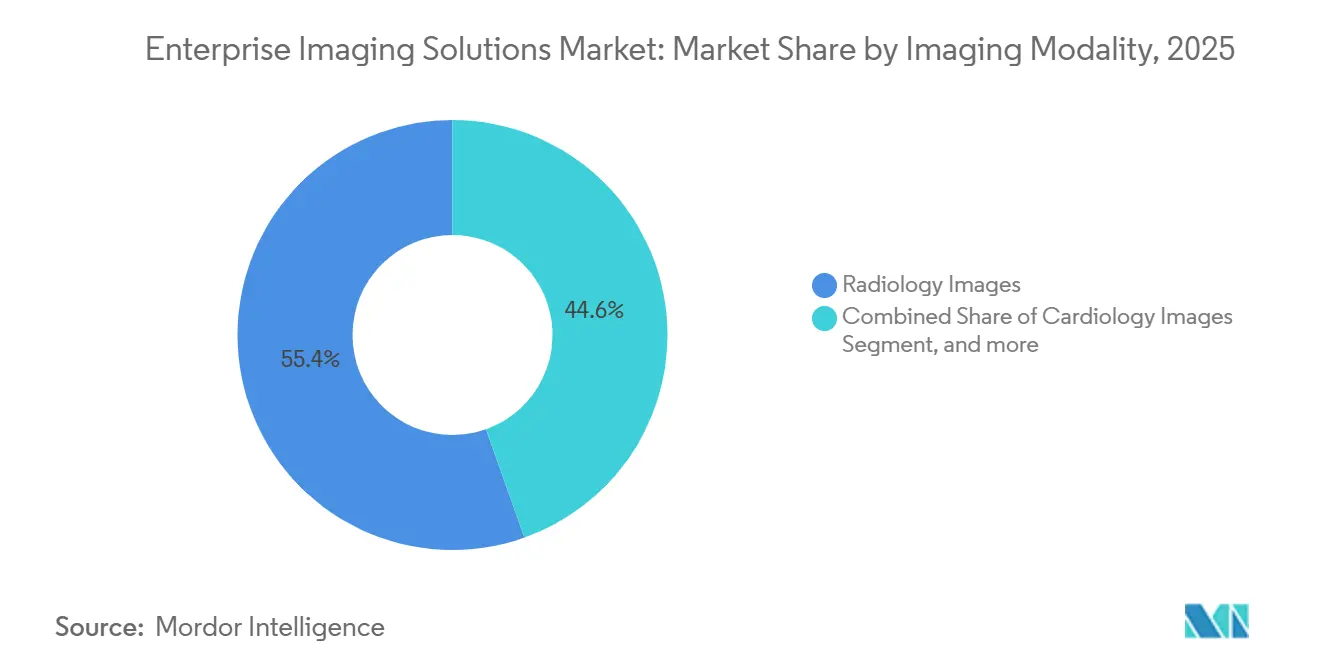

- By imaging modality, radiology accounted for 55.43% of the enterprise imaging solutions market in 2025, whereas point-of-care ultrasound is expanding at the highest 14.11% CAGR, driven by rising handheld adoption.

- By end user, hospitals held a 52.43% share in 2025; ambulatory surgical centers posted the strongest 14.65% CAGR, mirroring procedural migration to outpatient venues.

- By geography, North America accounted for a 42.78% share in 2025, yet Asia-Pacific shows the most rapid 12.54% CAGR through 2031, underpinned by large-scale government digital-health programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise Imaging Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Digital Transformation Of Healthcare Ecosystems | +2.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Cloud Adoption In Enterprise Health IT | +2.5% | Global, particularly North America and Asia-Pacific | Short term (≤ 2 years) |

| Population Health Management Initiatives | +1.4% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Growing Investments In Artificial Intelligence For Medical Imaging | +2.1% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Shift Toward Value-Based Care And Integrated Imaging Workflows | +1.6% | North America, Europe | Long term (≥ 4 years) |

| Government Incentives And Funding For Healthcare IT Modernization | +1.3% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Digital Transformation of Healthcare Ecosystems

Large networks are collapsing siloed departmental PACS into enterprise platforms that span radiology, cardiology, pathology, and point-of-care imaging, unifying longitudinal records across care venues[1]CMS Analysts, “Optimizing Care Delivery Framework,” cms.gov. Federal modernization contracts such as the Veterans Affairs EHR program extend this push by stipulating imaging interoperability alongside clinical data unification. Regional EHR rollouts—North West London being a notable example—require imaging backbones that can span multiple trusts, driving demand for vendor-neutral archives and federated query frameworks. Standards bodies have codified this shift: the August 2025 IHE Radiology Framework added profiles for FHIR-indexed imaging, ensuring algorithmic and clinical systems can locate studies without proprietary hooks. Together, these forces ensure that the enterprise imaging solutions market continues to consolidate disparate image silos into governance-driven, system-wide platforms that serve population-level analytics.

Cloud Adoption in Enterprise Health IT

Elastic cloud storage eliminates capital outlays for on-premise arrays and offers geo-redundant DICOMweb endpoints with built-in encryption, prompting buyers to redirect budgets from hardware to analytics and AI. National policies, including Germany’s Digitalisation Strategy and the UK NHS Cloud Framework, certify cloud as a compliant location of record for clinical imaging, reducing procurement risk for health systems. Google and Oracle have matched Microsoft with managed DICOM services that integrate with native AI tooling, allowing customers to chain imaging archives to analytics pipelines without bespoke interfaces. Hybrid rollouts remain common: real-time acquisition sits on site while long-term retention lives in the cloud, letting hospitals phase migration and control network expenditure. Cybersecurity leaders, spurred by the 2024 Change Healthcare incident, insist on stringent IAM, immutable backups, and API throttling, reinforcing the case for cloud security investment as a baseline rather than an elective add-on.

Population Health Management Initiatives

Aggregated imaging cohorts help systems monitor screening adherence, quantify disease progression, and report quality metrics under Medicare’s MIPS Value Pathways, fostering a direct financial link between enterprise imaging adoption and reimbursement. Multi-society guidance stresses standardized terminologies and structured reporting so that images can feed outcomes dashboards without manual curation. Chinese regional centers such as Shenzhen Longgang illustrate how shared reading hubs deliver consistent protocols across multiple facilities, lowering diagnostic variance. These initiatives elevate the role of imaging metadata pipelines that anonymize, tag, and mirror data into population registries. As analytics move upstream, the enterprise imaging solutions market embeds de-identification and cohort-builder tools, enabling providers to address value-based metrics without exporting datasets to third parties.

Growing Investments in Artificial Intelligence for Medical Imaging

Over 1,000 FDA-cleared imaging AI devices exist, with radiology the prime focus, converting enterprise archives from passive stores into algorithm-routing engines. Health systems now evaluate platforms based on how well they deploy, monitor, and manage AI, rather than on viewer ergonomics alone. Regulators are hardening post-market surveillance obligations, requiring continuous performance tracking that demands tight integration among PACS, VNA, and AI inference engines. Vendor partnerships—GE with Sutter Health and Siemens Healthineers with Tower Health—exemplify deals where AI governance is integral to contract value. As adaptive algorithms proliferate, platforms that fail to expose standardized orchestration hooks risk relegation to commodity storage in an enterprise imaging solutions industry that increasingly prizes AI agility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost Of Ownership And Budgetary Constraints | -1.8% | Global, acute in resource-limited markets | Short term (≤ 2 years) |

| Data Privacy Regulations And Cybersecurity Risks | -1.2% | Global, stringent in Europe and North America | Medium term (2-4 years) |

| Interoperability Challenges Across Legacy Systems | -0.9% | Global, particularly fragmented health systems | Medium term (2-4 years) |

| Workforce Skill Gaps In Advanced Imaging IT | -0.7% | Global, pronounced in smaller facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Budgetary Constraints

Licensing, storage, bandwidth, and professional services quickly swell lifetime costs beyond initial capital budgets, placing smaller hospitals at a disadvantage. The National Academy of Medicine warns that procurement teams rarely account for migration and integration expenses, triggering overruns that delay go-lives. Tiered retention strategies help, yet higher-resolution modalities inflate storage faster than cost curves decline. Cloud egress fees introduce a new line item that finance teams must monitor, eroding perceived savings. These dynamics temper adoption rates in resource-limited markets, even as high-income systems push ahead.

Data Privacy Regulations and Cybersecurity Risks

Ransomware gangs increasingly target PACS archives, exfiltrating DICOM files for double extortion, compelling CIOs to divert budgets to segmentation, MFA, and immutable backups[2]HHS Cybersecurity Program, “Ransomware Threat Brief,” hhs.gov. GDPR fines and U.S. breach-notification liabilities heighten the financial stakes of any compromise. Industry advisories highlight vulnerabilities in legacy DICOM viewers and unmanaged ultrasound probes, pressuring vendors to harden devices by default. Insurance premiums for cyber coverage have also spiked, further inflating total ownership costs. Heightened scrutiny may slow cloud migrations where data-residency assurances remain opaque.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Drives Elastic Scalability

Cloud deployments accounted for a dominant 63.54% enterprise imaging solutions market share in 2025, and the segment is projected to post a 13.65% CAGR to 2031. The enterprise imaging solutions market size for on-premises systems is leveling off as CIOs weigh refresh costs against subscription-based cloud alternatives. Early movers report faster study retrieval for distributed clinicians and simplified disaster recovery once images reside in geo-redundant buckets. Hybrid options are popular: real-time acquisitions stay on site, while legacy data trickles to the cloud, limiting bandwidth spikes and egress fees. Health systems also leverage cloud AI toolchains for inference, avoiding on-premise GPU clusters and thereby compressing deployment cycles. Security remains under scrutiny, yet converged IAM and native audit logging help satisfy regulators. As framework contracts from bodies like the NHS lock in multi-vendor cloud compliance, even data-sovereign markets grow more receptive.

On-premise deployments persist where strict data-residency statutes or sunk infrastructure costs prevail. Many academic centers still favor local GPU farms for research agility, and latency-sensitive modalities such as fluoroscopy may remain tethered to in-house servers. Nonetheless, hardware replacement cycles and higher insurance premiums for physical data centers pressure boards to revisit total cost models. The growing availability of sovereign cloud regions promises to dissolve some residency objections, paving the way for further cloud penetration in the enterprise imaging solutions market.

By Solution: Image Exchange Gains Momentum

Vendor-neutral archives led the enterprise imaging solutions market, accounting for 36.76% of revenue in 2025, reflecting their role as foundational repositories across modalities. Yet image-exchange platforms boast the sharpest 13.82% CAGR, fuelled by regional collaboration mandates that prioritize federated query over bulk migration. In shared-reading networks, a study can remain on site yet be viewable anywhere, slashing duplicate storage. The XDS-I and DICOMweb protocols underpin these transactions, enabling zero-footprint viewers to present studies within EHR launch contexts. As accountable-care contracts reward continuity, clinicians value one-click access to external priors, nudging procurement toward exchange-oriented products.

Picture archiving and communication systems remain indispensable for worklist management and advanced visualization, but growth is flatter as enterprise initiatives stretch beyond radiology. Universal viewers bundle multi-specialty toolsets, reducing the number of thick clients a clinician must master. Vendors increasingly collapse archive and exchange features into single licenses, simplifying SKUs but complicating category labels in the enterprise imaging solutions industry. Meanwhile, cloud hyperscalers position their managed DICOM stores as neutral brokers, eroding the moat historically enjoyed by VNA incumbents.

By Imaging Modality: Point-of-Care Ultrasound Surges

Radiology images still constitute 55.43% of the enterprise imaging solutions market size because CT and MR remain storage-heavy. Point-of-care ultrasound, however, is rising fastest at a 14.11% CAGR as handheld scanners proliferate outside imaging suites. Governing the influx requires standardized credentialing and metadata capture to ensure clips integrate seamlessly into VNA archives. The HIMSS-SIIM-AIUM January 2025 guidance has become a de facto blueprint, defining quality checkpoints that mitigate variable operator skill. Pathology and dermatology images are next in line, though whole-slide imaging tax bandwidth and viewer performance, slowing uptake. Cardiology remains a specialty silo due to hemodynamic data dependencies, yet converged platforms are beginning to normalize echocardiography workflows within enterprise viewers.

As photon-counting CT and 7T MRI deliver larger datasets, compression algorithms and tiered storage strategies grow critical. Workflow engines now direct large cine loops into secondary tiers after clinical review, balancing instant availability against cost. AI triage tools flag critical head CTs or large-vessel occlusions, reinserting findings into the worklist and reducing manual routing. These innovations bolster the case for imaging platforms that can coordinate modality diversity without spawning new silos, reinforcing vendor emphasis on cross-disciplinary governance.

By End User: Ambulatory Settings Accelerate Adoption

Hospitals retained 52.43% enterprise imaging solutions market share in 2025 thanks to expansive modality rosters and 24/7 services, yet ambulatory surgical centers deliver the swiftest 14.65% CAGR as payers redirect elective procedures to lower-cost venues. Imaging in outpatient centers must sync with pre-operative planning tools and post-procedure follow-ups, driving demand for web-based viewers accessible from ORs and consultation rooms. Diagnostic imaging centers value instant report delivery to referring physicians, making FHIR endpoints and mobile-ready links prime buying criteria. Subscription-priced cloud archives spare these smaller operators the need for large capital outlays, aligning costs with exam volumes.

Hospitals leverage economies of scale for enterprise licenses and specialist informatics teams, yet their multi-campus setups intensify governance complexity. Teaching institutions often pilot AI models, pushing vendors to accommodate research sandboxes alongside production workflows. Rural facilities, lacking on-site radiology coverage, are relying on teleradiology providers that connect directly to the VNA, raising expectations for seamless multi-tenant credentialing. Collectively, these trends widen the enterprise imaging solutions market, but they also fragment user personas, spurring vendors to diversify support models.

Geography Analysis

North America commanded 42.78% of the 2025 enterprise imaging solutions market share, buoyed by integrated delivery networks like Sutter Health, which inked a USD 1 billion AI-centric imaging pact with GE HealthCare in January 2025. U.S. regulatory levers, including ONC’s HTI-2 and CMS’s imaging-heavy MIPS pathways, strengthen platform replacement cycles as providers race to prove compliance. Canada’s momentum stems from multi-year value partnerships such as Siemens Healthineers’ collaboration with Hamilton Health Sciences, which bundles modality refresh with cloud archives and analytics subscriptions. Heightened ransomware activity, notably the 2024 Change Healthcare compromise, continues to push North American buyers toward immutable backups and zero-trust architectures, inflating security line items within total project budgets.

Asia-Pacific is projected to clock the fastest 12.54% CAGR through 2031. China leads with regional imaging hubs exemplified by Shenzhen Longgang District’s Huawei-backed consolidation, which showcases how centralized reading curbs diagnostic disparities across urban and suburban catchments. India’s national digital health mission encourages imaging data exchange, yet fragmented hospital ownership prolongs procurement cycles outside the top private chains. In Japan, an aging populace and radiologist scarcity fuel teleradiology and AI triage uptake, although stringent evaluation norms slow cloud adoption. Australia’s state health systems are co-funding VNAs to enable cross-state sharing, guided by national VNA standards updated in April 2025[3]Digital VA Office, “PACS Modernization PIA,” digital.va.gov.

Europe’s growth hinges on outcome-based value partnerships. Siemens Healthineers struck multi-year deals with Manchester University NHS Foundation Trust, Assistance Publique–Hôpitaux de Paris, and University Hospital Nantes, each bundling software, modalities, and services under performance-linked clauses. The UK deploys centralized frameworks such as the January 2026 PACS & VNA agreement that allow trusts to bypass individual tendering, speeding uptake. Germany’s digital-health funding mechanisms require FHIR-ready interfaces, nudging even conservative buyers toward next-generation platforms. Southern Europe faces tighter capital ceilings, favoring cloud-hosted subscriptions over outright purchases, while the Middle East and Gulf regions invest aggressively in smart-hospital projects that embed enterprise imaging from day one. South American growth clusters in Brazil and Argentina, where private hospital chains seek differentiation via AI-enabled imaging.

Competitive Landscape

Competition is moderate, with traditional PACS incumbents—GE HealthCare, Siemens Healthineers, Philips, Fujifilm—sharing space with enterprise-first players like Sectra, Intelerad, and Hyland, while hyperscalers Microsoft, Google, and Oracle layer in managed DICOM stores. Multi-year value partnerships have redefined the sales cycle, shifting emphasis from standalone equipment bids to outcome-aligned contracts that bundle software, AI suites, and life-cycle services. AI orchestration has become a decisive battlefield: platforms lacking native model governance risk marginalization as health systems rank algorithm deployment agility above viewer aesthetics. Cyber-resilience is another differentiator post-ransomware crises; vendors offering embedded immutable backups and granular zero-trust IAM now score higher in RFPs.

Cloud hyperscalers leverage scale to undercut storage costs and attach native analytics, pressuring legacy vendors to open APIs or risk customer attrition. Partnerships are proliferating: Sectra’s Azure-based SaaS offering lets hospitals offload infrastructure management, while Intelerad’s Google Cloud alliance wraps image-exchange and advanced AI pipelines under a single SLA. Emerging disruptors include handheld ultrasound firms that auto-upload exams to cloud VNAs, re-shaping acquisition pathways and elevating governance considerations flagged by HIMSS-SIIM-AIUM in early 2025. Standards engagement remains a strategic lever; companies chairing DICOM or IHE workgroups often see their preferred implementations crystallize in the specifications that buyers embed in tenders.

Enterprise Imaging Solutions Industry Leaders

GE HealthCare

Siemens Healthineers

Koninklijke Philips N.V.

Agfa-Gevaert Group

Carestream Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: he university hospital TUM Klinikum Rechts der Isar (TUM Klinikum) in Germany expands its enterprise imaging solution from international medical imaging IT and cybersecurity company Sectra (STO: SECT B) by adding the modules for pathology and ophthalmology. This will provide their clinicians with tools for enhanced efficiency, helping them enhance diagnostic speed, as well as foster collaboration within and between departments.

- December 2025: GE HealthCare announced the latest advancements of Imaging 360, now enhanced with artificial intelligence (AI), designed to help improve efficiency in the radiology department. AI-driven Discoveries helps to balance device utilization, optimize slot times, and identify opportunities to standardize protocols – all with the intent of giving back time and energy to healthcare providers so they can deliver optimal care to more patients with existing resources.

- November 2025: Fujifilm Healthcare Americas Corp. launched Synapse One, a comprehensive, tailor-made workflow solution for outpatient imaging, in North America. This all-inclusive enterprise imaging solution enables providers to address everything from a patient engagement portal, self-scheduling of exams, RIS (Radiology Information System), advanced scheduling capability, RCM options, PACS, advanced 3D imaging, a physician portal, and more, all within the Synapse platform in the secure Amazon Web Services (AWS) cloud.

- November 2025: DeepHealth, one of the global leaders in AI-powered health informatics and a wholly owned subsidiary of RadNet, Inc., unveiled an expanded portfolio at RSNA 2025, introducing next-generation imaging informatics and clinical AI solutions. The company is announcing new offerings and major enhancements across its portfolio, spanning disease detection, assessment and monitoring, remote scanning, image management and interpretation, center operations and AI orchestration—all designed to transform the imaging experience and advance population health.

Global Enterprise Imaging Solutions Market Report Scope

As per the scope of the report, enterprise imaging solutions are comprehensive systems that enable healthcare providers to store, manage, and access medical images and associated data across various departments. They facilitate seamless integration, improving diagnostic accuracy and patient care. These solutions support efficient workflow and data sharing within healthcare organizations.

The Enterprise Imaging Solutions Market is Segmented by Deployment Mode (On-Premise and Cloud), Solution (Vendor Neutral Archive, Picture Archiving & Communication System, Image Exchange, and Universal Viewer / Enterprise Viewer), Imaging Modality (Radiology Images, Cardiology Images, Pathology & Microscopy Images, and Point-Of-Care & Ultrasound Images), End-User (Hospitals, Diagnostic Imaging Centers, and Ambulatory Surgical Centers & Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| On-Premise |

| Cloud |

| Vendor Neutral Archive (VNA) |

| Picture Archiving & Communication System (PACS) |

| Image Exchange |

| Universal Viewer / Enterprise Viewer |

| Radiology Images |

| Cardiology Images |

| Pathology & Microscopy Images |

| Point-Of-Care & Ultrasound Images |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By Solution | Vendor Neutral Archive (VNA) | |

| Picture Archiving & Communication System (PACS) | ||

| Image Exchange | ||

| Universal Viewer / Enterprise Viewer | ||

| By Imaging Modality | Radiology Images | |

| Cardiology Images | ||

| Pathology & Microscopy Images | ||

| Point-Of-Care & Ultrasound Images | ||

| By End-User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers & Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the 2026 value of enterprise imaging solutions worldwide?

The market stands at USD 2.02 billion in 2026.

How fast will spending on enterprise imaging platforms expand over the next five years?

Revenue is projected to climb at an 11.52% CAGR, reaching USD 3.49 billion by 2031.

Which deployment option is seeing the greatest uptake among health systems?

Cloud-based implementations lead with a 63.54% share in 2025 and maintain the fastest 13.65% CAGR.

Which region shows the highest growth momentum?

Asia-Pacific posts the quickest 12.54% CAGR through 2031, supported by large-scale government digital-health initiatives.

Which imaging modality is projected to accelerate the most?

Point-of-care ultrasound grows at a 14.11% CAGR as handheld devices move into emergency, critical-care, and outpatient settings.

How are artificial-intelligence investments influencing platform selection?

Buyers increasingly favor solutions that streamline AI model deployment, monitoring, and versioning, making orchestration capabilities a top differentiator during procurements.

Page last updated on: