Handheld Imaging Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

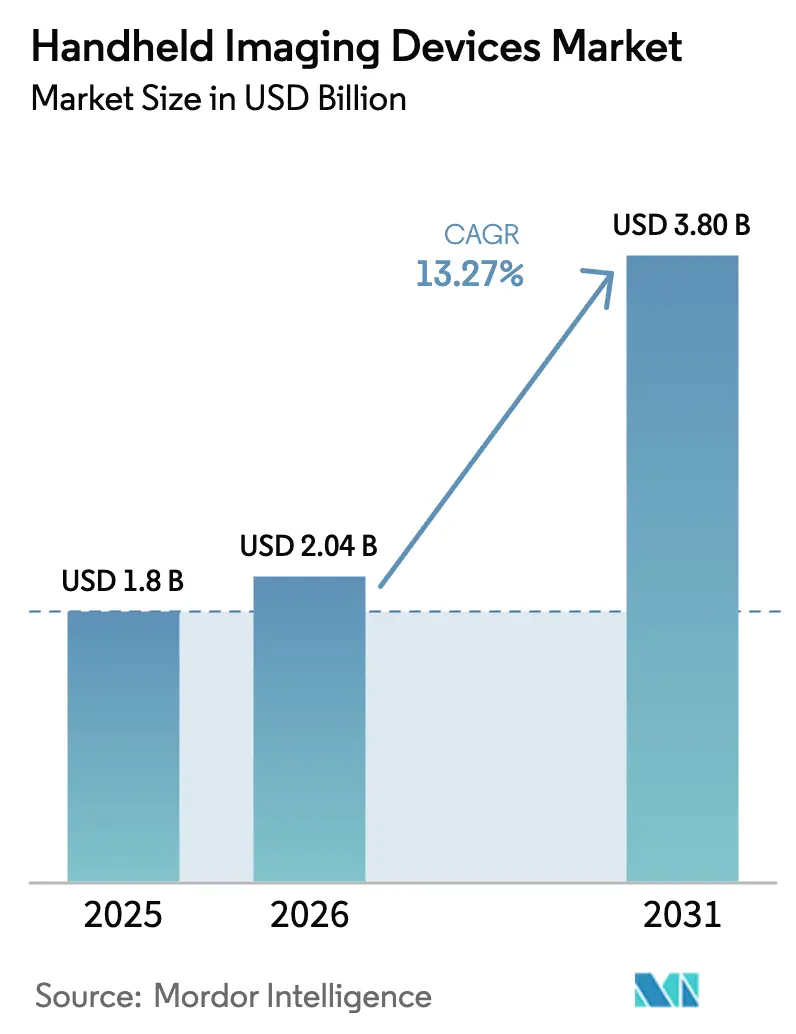

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 3.80 Billion |

| Growth Rate (2026 - 2031) | 13.27% CAGR |

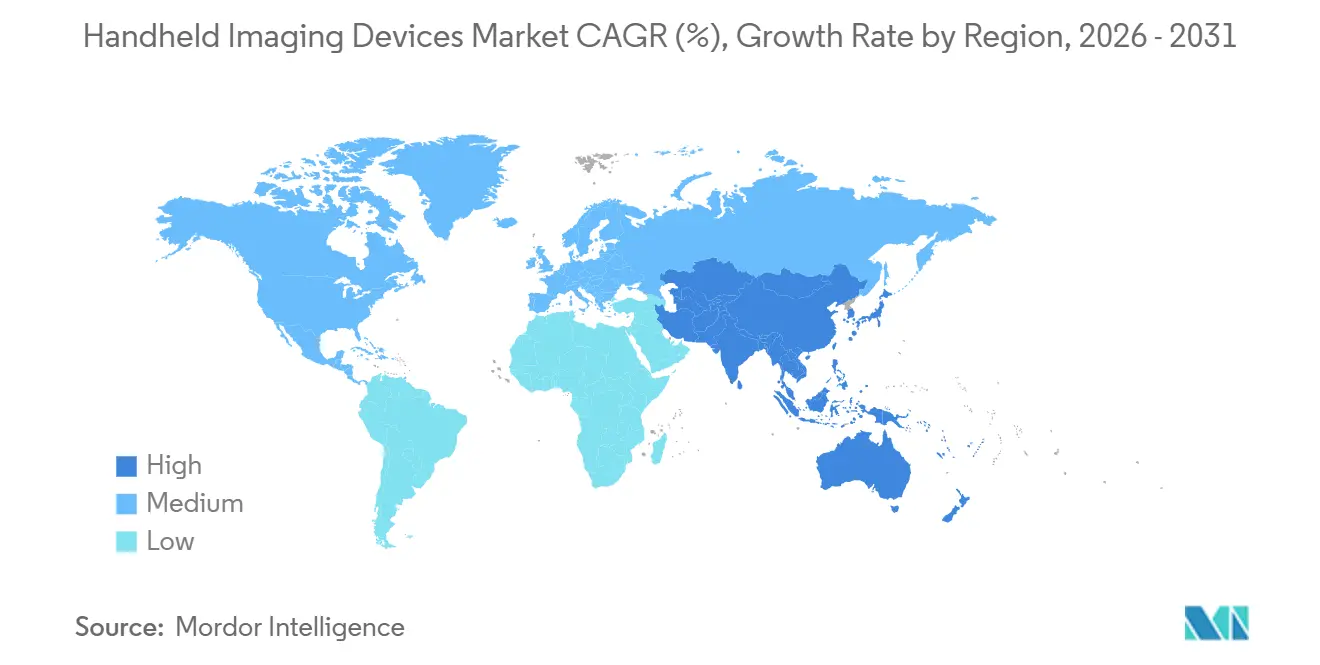

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Handheld Imaging Devices Market Analysis by Mordor Intelligence

Handheld Imaging Devices Market size in 2026 is estimated at USD 2.04 billion, growing from 2025 value of USD 1.8 billion with projections showing USD 3.80 billion, growing at 13.27% CAGR over 2026-2031.

This robust trajectory reflects hospitals and specialty clinics shifting diagnostic workflows from centralized radiology suites to the bedside, ambulance, or factory floor as telemedicine networks mature and AI-guided image acquisition reduces operator dependency. Enterprise spending on imaging IT, which reached USD 10.96 billion in 2024, is now prioritizing seamless ingestion of point-of-care data, further propelling the handheld imaging devices market. Vendor competition around single-probe ultrasound, wireless X-ray generators, and pocket-sized optical coherence tomography (OCT) cameras confirms that hardware miniaturization and sensor innovation are no longer future prospects but present-day differentiators. Geopolitical shocks to semiconductor supply chains and heightened cybersecurity scrutiny continue to temper near-term margins, yet the addressable clinical and industrial user base continues to expand every quarter, sustaining capital investment appetite across North America, Europe, and Asia-Pacific.

Key Report Takeaways

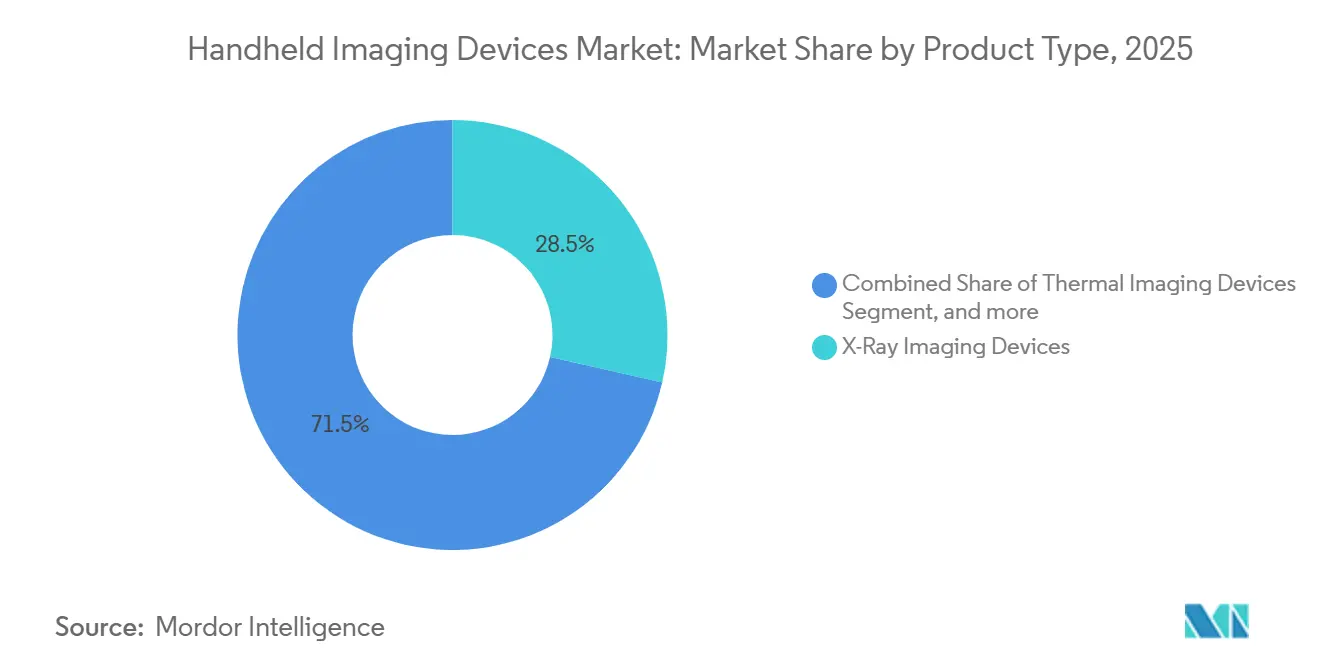

- By product type, X-ray systems captured 28.54% handheld imaging devices market share in 2025, while optical and OCT platforms are projected to advance at a 15.76% CAGR to 2031.

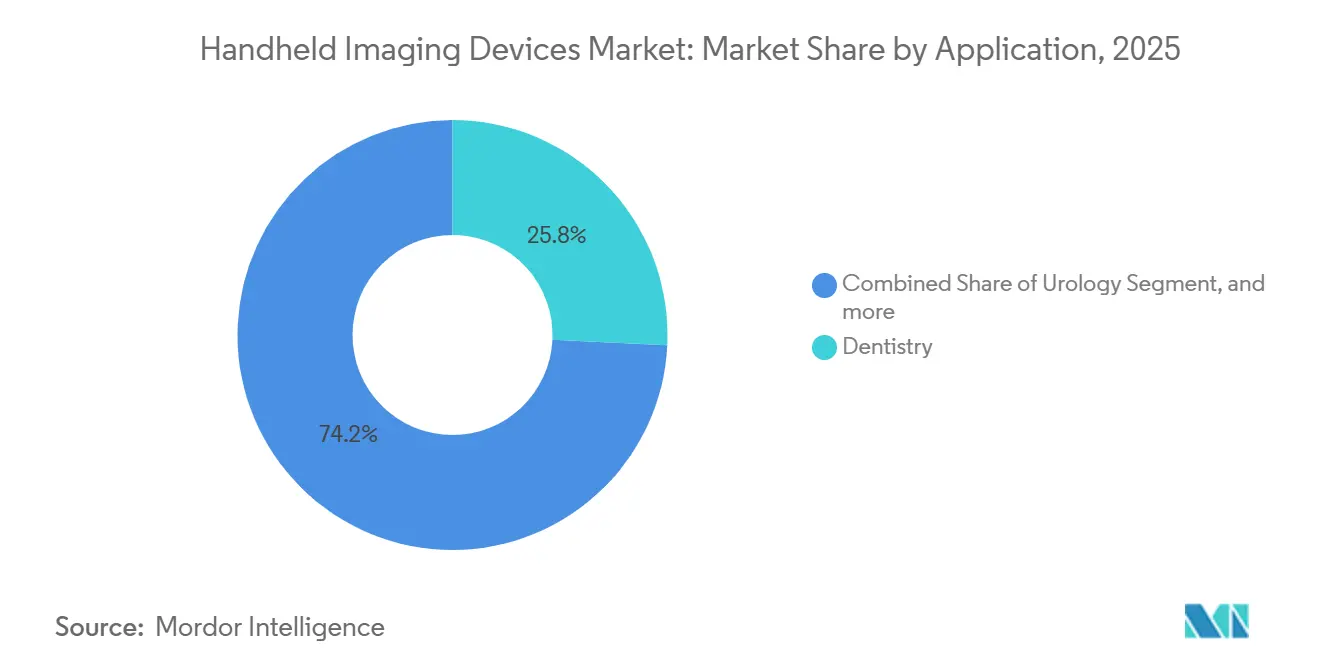

- By application, dentistry led revenue with a 25.76% share of the handheld imaging devices market in 2025; orthopedics is set to grow the fastest at a 16.22% CAGR through 2031.

- By end user, hospitals accounted for 55.63% of 2025 revenue, whereas specialty clinics are forecast to expand at a 16.43% CAGR over 2026-2031.

- By geography, North America held 43.21% of 2025 revenue; Asia-Pacific is on track for a 14.65% CAGR, the fastest among all geographies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Handheld Imaging Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Point-of-Care Diagnostics | +2.8% | Global (North America, Western Europe early adopters) | Medium term (2-4 years) |

| Growing Industrial Demand for Real-Time NDT | +1.4% | APAC manufacturing hubs, North America defense sectors | Medium term (2-4 years) |

| Increasing Defense & Homeland Security Spend | +1.1% | North America, Europe, Middle East GCC | Long term (≥4 years) |

| Sensor Miniaturization & Wireless Advances | +2.5% | R&D hubs in North America, Japan, South Korea | Short term (≤2 years) |

| Expanding Telemedicine Infrastructure | +2.2% | APAC emerging markets, rural North America | Short term (≤2 years) |

| Government Funding & Reimbursement Clarity | +1.6% | North America, Europe, Japan, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Point-of-Care Diagnostics Across Healthcare Settings

Point-of-care ultrasound has evolved from a niche emergency medicine adjunct into a standard tool across cardiology, critical care, and obstetrics. In a January 2024 head-to-head evaluation of six handheld probes, 35 clinicians ranked image quality and intuitive workflows as top purchase criteria. GE Healthcare’s April 2024 launch of Caption AI on the Vscan Air SL added automated ejection-fraction and B-line quantification, enabling non-cardiologists to perform bedside echocardiography with specialist-level accuracy. CMS finalized audio-only telehealth reimbursement for 2025, permitting handheld ultrasound billing when video links fail, a change that broadens access in bandwidth-constrained rural areas. Hospitals now embed handheld imaging in nurse-led triage, shaving minutes off diagnosis of pneumothorax or deep vein thrombosis, while specialty clinics capture both professional and technical components under Medicare’s Physician Fee Schedule. Combined with AI guidance, cloud DICOM integration, and stable reimbursement, this creates a self-reinforcing cycle that fuels double-digit growth for the handheld imaging devices market in the medium term.

Growing Industrial Demand for Real-Time Non-Destructive Testing

Factory managers and field engineers increasingly rely on handheld thermal and X-ray devices to detect hidden corrosion, voids, or counterfeit electronics without halting production. Teledyne FLIR cameras pinpoint electrical hotspots and insulation failure in milliseconds, and compact computed-tomography scanners like Lumafield Neptune visualize multi-die semiconductor stacks for supply-chain assurance. Demand clusters in Chinese, Japanese, and South Korean auto-electronics plants and in North American aerospace and defense maintenance depots. Condition-based maintenance supported by portable imaging reduces downtime and extends asset life, resulting in a quantifiable return on investment that sustains procurement cycles.

Increasing Defense and Homeland Security Procurement of Portable Imaging

Explosive ordnance teams deploy ruggedized X-ray units to visualize device internals without direct manipulation, while thermal imagers support perimeter security and disaster search-and-rescue. U.S. Department of Defense guidelines now specify wireless data links, sub-3 kg total weight, and extreme-temperature operation for field imaging gear. GCC countries invest in handheld ultrasound for combat casualty care, and NATO members modernize battalion aid stations with pocket devices that feed images into secure tactical networks. Long contracting timelines lock in revenue visibility for four-plus years even though unit volumes trail civilian healthcare orders.

Technological Advances in Sensor Miniaturization and Wireless Connectivity

Backside-illuminated CMOS sensors, wafer stacking, and capacitive micromachined ultrasound transducers (CMUT) have narrowed the quality gap between handheld and cart-based systems. Butterfly Network’s 2024 Prix Galien-winning iQ3 uses a single CMUT array for multiple scan modes, eliminating costly probe swaps. Samsung’s R20, unveiled at RSNA 2025, melds ultrasound with low-dose X-ray in one portable chassis. Yet the supply chain remains fragile: state-of-the-art CMOS sensor fabrication is concentrated in Taiwan and China, with no comparable Western capacity[1]National Institute of Standards & Technology, “Semiconductor Supply Chain Report,” nist.gov. Wireless upgrades to Bluetooth Low Energy and Wi-Fi 6 relieve cable fatigue but leave battery runtimes hovering around 80 minutes, prompting engineering races around power management[2]American College of Emergency Physicians, “Handheld Ultrasound Battery Performance Guidance,” acep.org. Short-term, feature differentiation—AI overlays, longer battery life, automated presets—will spur device refresh cycles across the handheld imaging devices market.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership and Maintenance | -1.8% | Global, acute in APAC & South America | Medium term (2-4 years) |

| Stringent Multi-Region Regulatory Approval Pathways | -1.2% | Global, extended MDR timelines in Europe | Long term (≥4 years) |

| Data Security & Cyber-Compliance Challenges | -1.4% | North America & Europe heightened scrutiny | Short term (≤2 years) |

| Supply-Chain Constraints for High-Performance Sensors | -1.1% | Dependence on Taiwan & China semiconductor fabs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Maintenance

Acquisition prices run from USD 1,999 for Butterfly iQ+ to north of USD 10,000 for premium Sonosite probes, yet annual software, maintenance, and probe-replacement charges pile another USD 3,000-10,000 on top. Batteries degrade after roughly 400 cycles, and replacement packs cost USD 500-1,000. Smaller clinics in Southeast Asia or South America struggle to amortize these outlays when fees are predominantly out of pocket. Leasing spreads payments over 3-5 years but embeds 4-8% interest, locking practices into vendor ecosystems and boosting lifetime expense. Medium-term, elevated ownership costs will cap volume growth in price-sensitive segments of the handheld imaging devices market.

Data Security and Cyber-Compliance Challenges for Connected Devices

Health-ISAC flagged 11 CISA advisories for medical devices in 2024 and counted 5,100 public DICOM servers lacking proper authentication, a 246% jump since 2017[3]Health-ISAC, “Medical Device Cyber Vulnerability Landscape 2024,” h-isac.org . Fifty-three percent of analyzed vulnerabilities could directly harm patients. Windows 10’s October 2025 end-of-life forces providers to upgrade firmware or expose endpoints. Manufacturers sink rising budgets into secure-by-design engineering and coordinated disclosure programs; providers divert 7-20% of IT spend to cybersecurity hardening. Heightened scrutiny, especially in the U.S. and EU, makes risk-averse buyers delay purchases, trimming near-term unit sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Optical Devices Outpace Traditional Modalities

Optical, near-infrared, and portable OCT units are projected to log a 15.76% CAGR through 2031, the speediest among all product categories. X-ray systems dominated revenue, accounting for 28.54% of the handheld imaging devices market share in 2025, propelled by intraoral dental units and mobile radiography carts used in skilled nursing facilities. The handheld imaging devices market size attached to optical platforms should exceed USD 1 billion by 2031 as dermatologists and ophthalmologists replace traditional film with non-ionizing solutions. Ultrasound remains the most installed modality: GE’s Vscan Air tops clinician ease-of-use ratings, while Mindray TE Air wins cardiac accuracy honors. Thermal cameras, though niche, gain momentum for industrial predictive maintenance and defense reconnaissance, where Teledyne FLIR holds sway.

Handheld OCT now achieves sub-10-micron axial resolution, empowering primary-care physicians to screen diabetic retinopathy without specialist referral. Smartphone-linked fundus cameras and dermatoscopes, often priced below USD 3,000, extend imaging into retail clinics and mobile vans. Konica Minolta’s Bone Suppression Imaging, FDA-cleared in December 2024, showcases software-led X-ray innovation that enhances lung detail without adding dose. Future differentiation will migrate from hardware to firmware, with vendors deploying cloud-delivered upgrades that inject new imaging modes overnight. As platform convergence accelerates—Samsung’s R20 bundles ultrasound and low-dose X-ray—buyers will increasingly weigh AI-driven interpretation speed and cybersecurity posture over pure image resolution.

By Application: Orthopedics Surges as MSK Ultrasound Gains Traction

Orthopedics is slated for a 16.22% CAGR, the fastest of any application, as musculoskeletal ultrasound enters sports medicine clinics, emergency rooms, and primary care workflows. Dentistry commanded 25.76% of 2025 revenue thanks to rapid chairside diagnostics, yet its growth moderates amid saturated penetration in developed markets. Cardiology workflows have mainstreamed handheld ejection fraction estimation and pericardial effusion screening, trimming echo wait times in congested emergency departments. Ophthalmology and dermatology usage leaps as portable OCT and high-resolution dermoscopy expand retinal and skin cancer screening to community settings.

Point-of-care ultrasound for fracture detection, guided joint injections, and soft-tissue injury assessment reduces orthopedic referral delays. Medicare now reimburses ultrasound-guided injections at roughly USD 180 per episode, buoying clinic economics. Urology leverages handheld scanners for bladder scans and renal stone triage, while gynecology uses portable imaging for early pregnancy dating and labor triage. Although endocrinology and vascular access niches remain small, AI-driven needle guidance tools may spur wider utilization. As sports participation and an aging population increase injury incidence, orthopedics’ share of the handheld imaging devices market will continue to widen.

By End-User: Specialty Clinics Gain Share as Care Disaggregates

Hospitals owned 55.63% of the handheld imaging devices market revenue in 2025, but specialty clinics will chalk up a 16.43% CAGR through 2031. Distributed care models let orthopedic, cardiac, and obstetric practices retain both technical and professional fees, a dual-capture incentive absent when imaging is outsourced to hospital radiology. Diagnostic imaging centers remain focused on MRI and CT, with handheld devices serving as a minor adjunct, outside portable X-ray services for homebound seniors. Industrial NDT firms, defense forces, and veterinarians add steady but smaller volume streams.

CMS’s 2025 policy permitting virtual direct supervision allows medical assistants to run handheld probes under remote physician oversight, stretching staffing models in outpatient settings. Multi-specialty groups increasingly embed ultrasound during same-visit consults, elevating downstream procedure capture. Hospitals still dominate emergency, ICU, and labor ward use, but capital budgets lean toward robotics and radiation oncology, slowing the refresh rates of handheld devices. Ambulatory surgery centers and urgent-care chains will be the fastest adopters, viewing portable imaging as a patient-engagement and revenue-generation lever.

Geography Analysis

North America retained 43.21% of 2025 revenue, anchored by Medicare’s clear payment codes and FDA’s lean 510(k) pathway that helped Konica Minolta and Fujifilm clear novel devices within 12 months. U.S. integrated delivery networks such as Sutter Health standardized on Vscan Air in early 2025, deploying more than 5,000 units and linking images to Epic electronic records. Canada equips remote clinics in the Yukon and Nunavut with pocket ultrasound to avoid USD 10,000 medevac flights, while Mexico’s private hospitals expand obstetric handheld imaging despite limited public-sector funding.

Asia-Pacific will post a brisk 14.65% CAGR, the highest regional pace for the handheld imaging devices market. China’s Healthy China 2030 plan funds township clinics to buy ultrasound from domestic champions Mindray and Chison at 30-40% discounts to Western list prices. India’s Ayushman Bharat Digital Mission co-finances tele-echocardiography hubs that slash rural diagnostic gaps. Japan’s greying population spurs home-visit doctors to carry lightweight probes, and South Korea’s semiconductor capability shortens R&D cycles for sensor-intensive modalities. Australia enforces AS/NZS 3540 safety norms but allocates rural health grants for mobile imaging procurement.

Europe exhibits replacement demand in Germany, France, and the UK, where stringent Medical Device Regulation audits slow novel modality rollouts but favor established OEMs with deep compliance budgets. Eastern European nations direct EU cohesion funds toward modernizing district hospitals with portable ultrasound and digital X-ray equipment. GCC states, led by Saudi Arabia and the UAE, procure handheld devices for border control and mass-event medicine. Sub-Saharan Africa relies on NGO donations, while Latin America’s growth is constrained by currency volatility; nevertheless, private Brazilian maternity hospitals are adopting handheld fetal scanners to differentiate their patient experience.

Competitive Landscape

The handheld imaging devices market encompasses diversified imaging giants—GE Healthcare, Philips, Siemens Healthineers—alongside pure-play innovators including Butterfly Network, Clarius Mobile Health, and EchoNous. GE’s USD 2.3 billion Intelerad takeover in November 2025 deepened its cloud PACS stack, letting the firm bundle software subscriptions with Vscan hardware and lock health systems into multi-year enterprise deals. The July 2024 USD 51 million purchase of Intelligent Ultrasound folded Caption AI and ScanNav automation into GE’s portfolio, enabling automated cardiac and obstetric measurements that shrink operator variability.

Butterfly’s USD 1,999 iQ3 disrupted pricing and forced incumbents to release competitive single-probe models. Philips Lumify and Siemens Acuson Pocket rely on subscription-tied presets to defend premium gross margins. In industrial NDT, Teledyne FLIR and Varex Imaging dominate, but new entrants such as Lumafield market office-friendly CT scanners for supply-chain assurance. Samsung’s R20 underscores modality convergence, marrying ultrasound and X-ray in a carry-on-sized unit and shifting differentiation toward firmware upgrades and AI analytics.

Cybersecurity posture has emerged as a selling point: Health-ISAC’s rising alert volume is pressuring providers to favor vendors with dedicated security operations centers and coordinated disclosure programs. FDA’s ISO 13485 harmonization raises compliance barriers for startups without mature quality systems. The competitive field thus remains moderately fragmented, with top five players controlling near-60% of global revenue.

Handheld Imaging Devices Industry Leaders

GE Healthcare

Teledyne FLIR

Koninklijke Philips N.V.

Siemens Healthineers

Butterfly Network

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Optomed USA launched its latest innovation: Optomed Lumo, a next-generation handheld fundus camera designed to bring high-quality retinal imaging into primary care and beyond.

- March 2025: Planmeca launched its first handheld intraoral X-ray device. Planmeca ProX GO offers space and time-saving chairside efficiency to both traditional clinics and radiology rooms, as well as mobile dental clinics, nursing homes, and emergency situations.

Global Handheld Imaging Devices Market Report Scope

As per the scope of the report, handheld imaging devices are portable medical tools used to capture real-time images of the body's internal structures. They are compact, easy to use, and provide quick diagnostic insights at the point of care. These devices enhance mobility and efficiency in healthcare settings.

The Handheld Imaging Devices Market Report is Segmented by Product Type (Thermal, Ultrasound, X-Ray, Optical/NIR/OCT, and Other Product Types), Application (Ophthalmology, Endocrinology, Urology, Gynecology & Obstetrics, Dermatology, Dentistry, Orthopedics, Cardiology and Vascular, and Other Applications), End-User (Hospitals, Diagnostic Imaging Centers, Specialty Clinics, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Thermal Imaging Devices |

| Ultrasound Imaging Devices |

| X-Ray Imaging Devices |

| Optical / NIR / OCT Devices |

| Other Product Types |

| Ophthalmology |

| Endocrinology |

| Urology |

| Gynecology & Obstetrics |

| Dermatology |

| Dentistry |

| Orthopedics |

| Cardiology and Vascular |

| Other Applications |

| Hospitals |

| Diagnostic Imaging Centers |

| Specialty Clinics |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Thermal Imaging Devices | |

| Ultrasound Imaging Devices | ||

| X-Ray Imaging Devices | ||

| Optical / NIR / OCT Devices | ||

| Other Product Types | ||

| By Application | Ophthalmology | |

| Endocrinology | ||

| Urology | ||

| Gynecology & Obstetrics | ||

| Dermatology | ||

| Dentistry | ||

| Orthopedics | ||

| Cardiology and Vascular | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Specialty Clinics | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the handheld imaging devices market in 2026?

The handheld imaging devices market size stands at USD 2.04 billion in 2026, with a 13.27% CAGR projected through 2031.

Which product type is expanding fastest?

Optical and OCT devices lead growth at a 15.76% CAGR, driven by non-ionizing, high-resolution needs in ophthalmology and dermatology.

Why are specialty clinics adopting handheld imaging so quickly?

They can capture both professional and technical fees while offering same-visit diagnostics, fueling a 16.43% CAGR for this end-user segment.

What is the primary regional growth engine after North America?

Asia-Pacific, especially China and India, will expand at 14.65% CAGR due to rural healthcare investments and domestic low-cost manufacturing.

How will supply-chain risks affect future device availability?

Heavy reliance on Taiwanese and Chinese CMOS fabs means geopolitical or natural disruptions could extend lead times and raise component costs, pressuring vendors to maintain higher inventory.

Which recent corporate move most reshaped competition?

GE Healthcare's USD 2.3 billion purchase of Intelerad in 2025 integrated cloud PACS with handheld devices, deepening enterprise lock-in and intensifying platform competition.

Page last updated on: