Wireless Intraoral Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

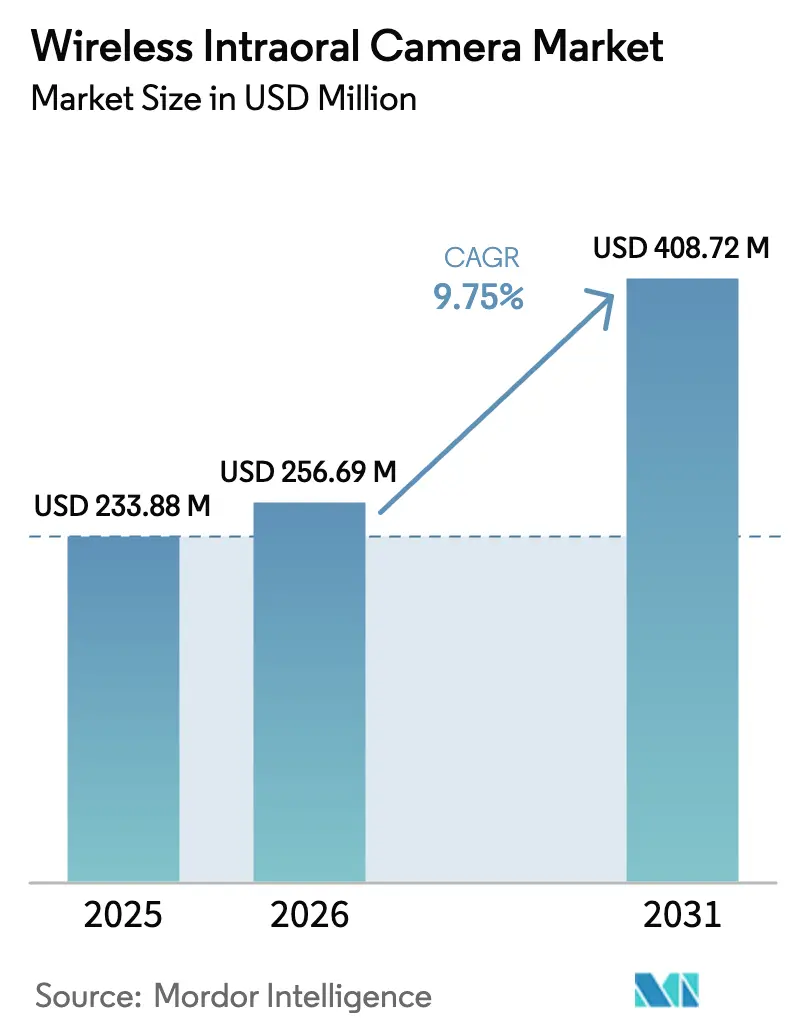

| Market Size (2026) | USD 256.69 Million |

| Market Size (2031) | USD 408.72 Million |

| Growth Rate (2026 - 2031) | 9.75% CAGR |

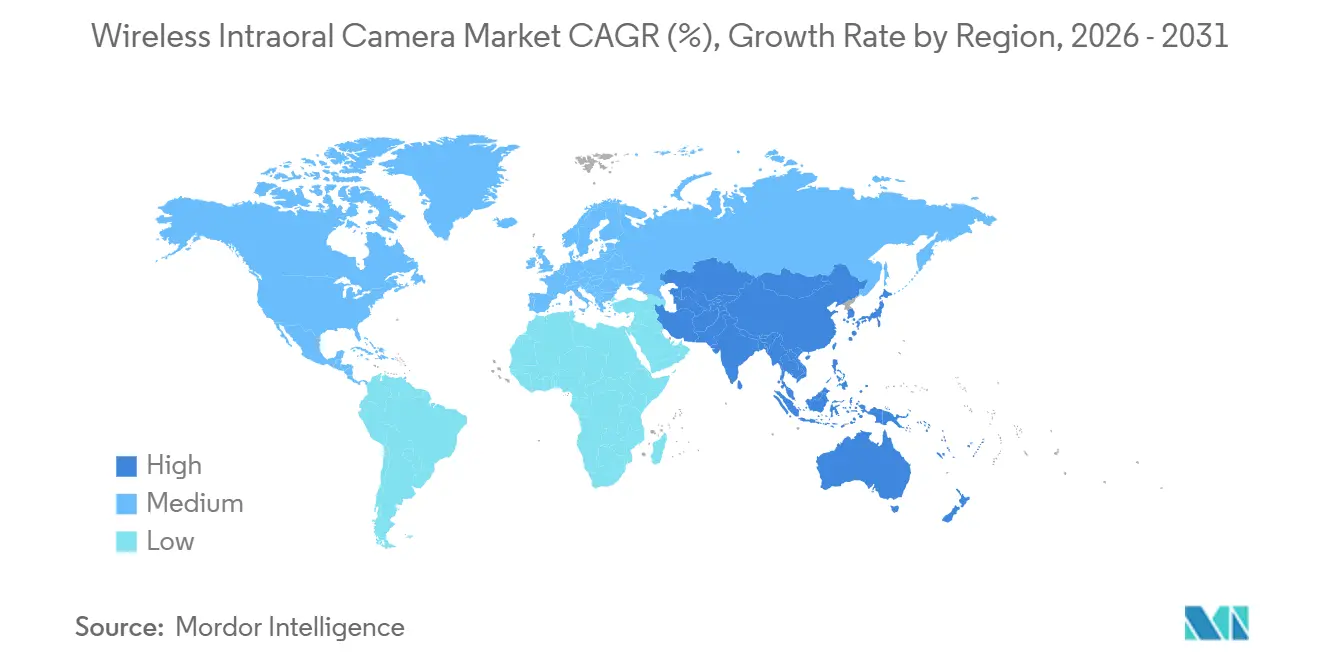

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Intraoral Camera Market Analysis by Mordor Intelligence

Wireless Intraoral Camera Market size in 2026 is estimated at USD 256.69 million, growing from 2025 value of USD 233.88 million with projections showing USD 408.72 million, growing at 9.75% CAGR over 2026-2031.

This trajectory reflects a structural pivot toward cloud-native, AI-ready imaging that links chairside capture to practice-management software and teledentistry platforms. Practices are retiring 1-5 meter USB systems because untethered handpieces move effortlessly between operatories, stream live images to remote specialists, and align with reimbursement mandates for photographic documentation. High-definition devices dominate shipments, yet full-HD and edge-AI upgrades are accelerating refresh cycles, while battery endurance and cybersecurity remain gating constraints. Regionally, North America benefits from dense dentist coverage and broad insurance penetration, whereas Asia-Pacific is expanding fastest as public and private stakeholders use wireless imaging to offset specialist shortages.

Key Report Takeaways

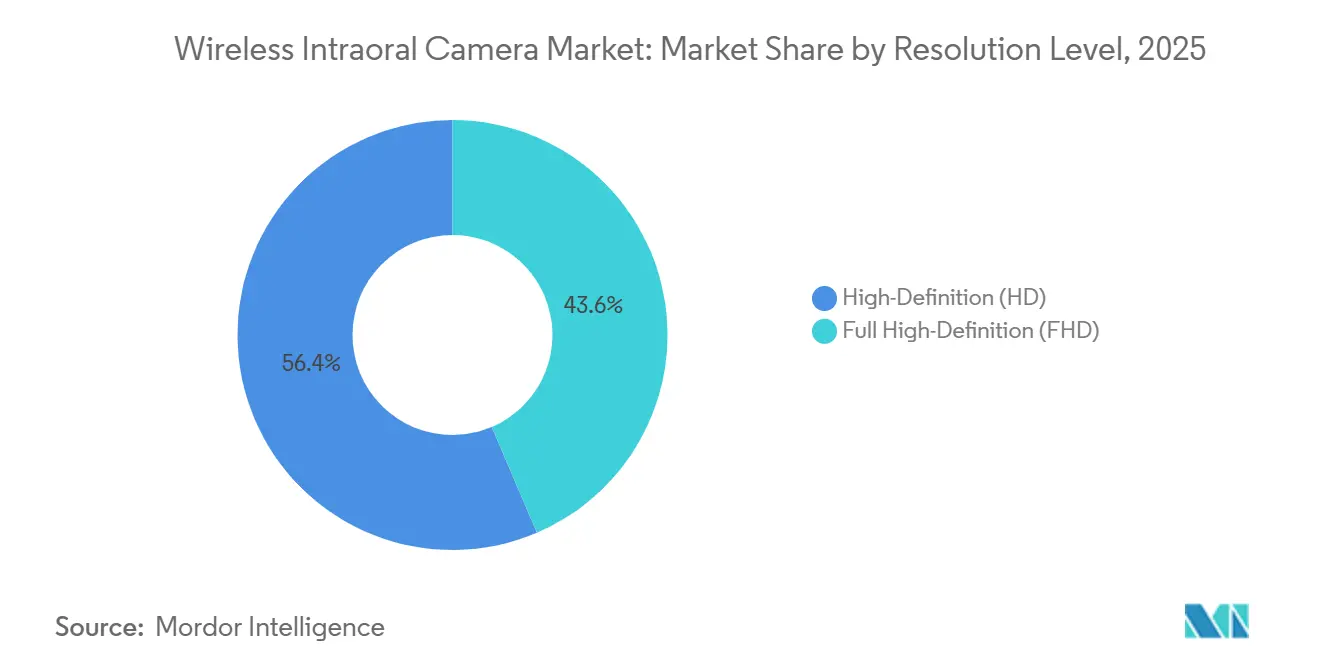

- By resolution, high-definition models commanded 56.43% of revenue share in 2025; full high-definition cameras are forecast to expand at a 11.54% CAGR through 2031.

- By sensor technology, CMOS held 71.54% of the wireless intraoral camera market share in 2025, while its segment is projected to grow at 11.12% CAGR through 2031.

- By connectivity, Wi-Fi led with 48.76% share in 2025; Bluetooth is expected to post the highest 11.84% CAGR to 2031.

- By application, implantology accounted for 27.65% of the wireless intraoral camera market size in 2025, and orthodontics is advancing at a 12.65% CAGR through 2031.

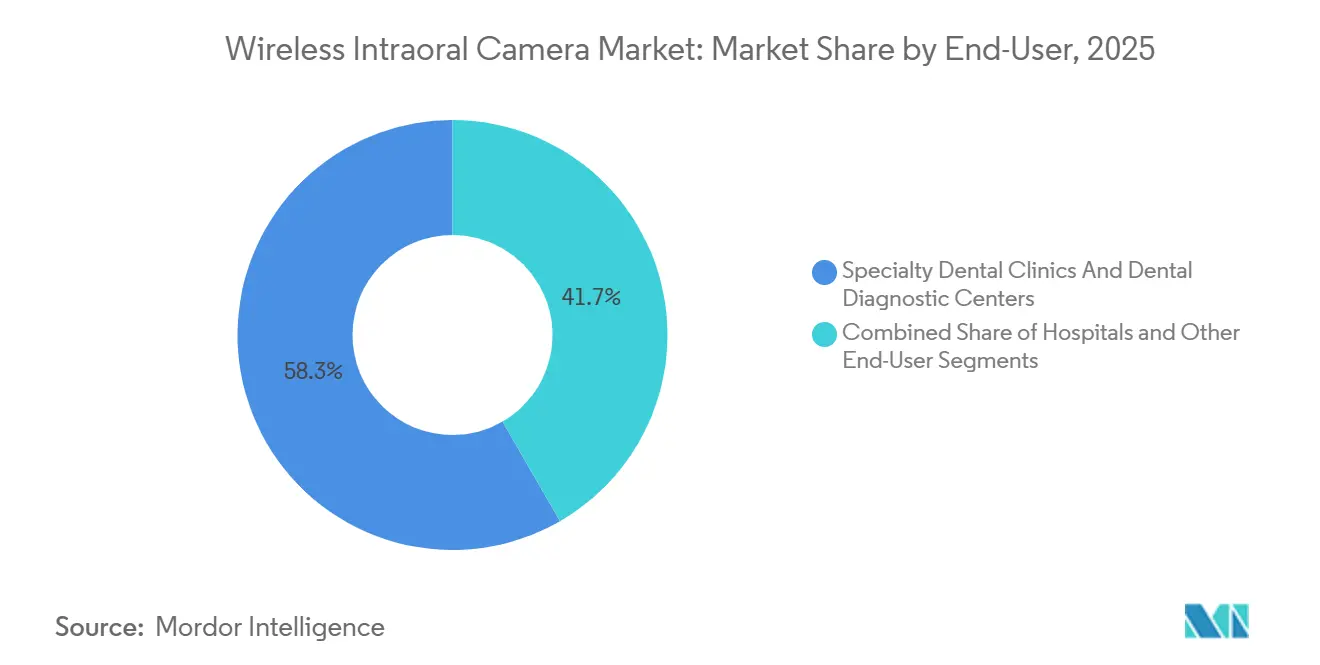

- By end user, specialty dental clinics and diagnostic centers captured a 58.33% share in 2025, whereas hospitals are set to grow at a 11.78% CAGR to 2031.

- By distribution, direct sales represented 55.87% share in 2025; online channels are predicted to climb at a 12.43% CAGR to 2031.

- By geography, North America led with 44.76% share in 2025 and Asia-Pacific is poised for a 10.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wireless Intraoral Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift Toward Digital Dentistry Workflows | +2.8% | North America, Europe, Asia-Pacific urban hubs | Medium term (2-4 years) |

| Integration of Intraoral Cameras with AI Platforms | +2.3% | North America, Europe, Asia-Pacific metros | Medium term (2-4 years) |

| Continuous Advancements in Wireless Imaging Technology | +1.9% | Global, faster uptake in tech-mature markets | Short term (≤2 years) |

| Growing Adoption of Teledentistry in Rural Areas | +1.6% | Asia-Pacific, Latin America, MENA, rural U.S. | Long term (≥4 years) |

| Rising Burden of Dental Caries and Periodontal Diseases | +1.4% | Higher prevalence in emerging markets | Long term (≥4 years) |

| Expansion of Dental Insurance Coverage in Emerging Markets | +1.2% | Asia-Pacific, Latin America, MENA | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift Toward Digital Dentistry Workflows

Between 2023 and 2024, the share of fully digital practices rose from 48% to 57%, positioning wireless cameras as the on-ramp to paperless records. Cord-free handpieces simplify chairside consultations by allowing clinicians to annotate lesions on ceiling-mounted screens while patients watch in real time, increasing treatment acceptance. Dealer data show practices diverting budgets from single-purpose hardware to integrated subscriptions that bundle cameras, imaging software, and cloud storage. The FDA’s 2023 recognition of ISO 23450:2021 shortened 510(k) clearances and sped product refreshes[1]FDA, “Recognition of ISO 23450:2021,” fda.gov. As workflows converge on cloud architecture, vendors pairing wireless optics with practice-management APIs gain a defensible edge.

Integration of Intraoral Cameras with Artificial Intelligence Platforms

AI use in dentistry doubled to 18% of practices in 2024 after studies showed 72–95% accuracy in caries detection using intraoral camera datasets. Edge-enabled handpieces, such as DEXIS Ti2, highlight suspect areas during capture, reducing diagnostic variance across multi-location groups. Vatech’s partnership with Pearl AI allows clinics to subscribe to niche algorithms without replacing hardware, anchoring long-term software revenue. Patient surveys reveal AI-flagged visuals elevate case acceptance by more than 20%, reframing imaging from a cost center to a revenue catalyst.

Continuous Advancements in Wireless Imaging Technology

Full-HD sensors now equal wired systems for diagnostic accuracy, with 84.62% sensitivity in caries detection versus 79.52% for smartphone photography. Multi-mode devices like KaVo’s DIAGNOcam Vision combine transillumination, fluorescence, and photography in a single 12-millimeter handpiece, trimming per-exam setup time by 40%. Bluetooth 5.0 handpieces deliver sub-100 millisecond latency across 10 meter ranges, while Wi-Fi units handle 1080p video at 60 fps for complex cases. Battery life remains a concern, prompting vendors to ship inductive charging cradles that double as infection-control stations.

Growing Adoption of Teledentistry in Rural Areas

Wireless intraoral images reviewed asynchronously now achieve 95% sensitivity and up to 93% specificity, rivaling chairside exams. Virtual Dental Home programs let hygienists capture footage in schools and transmit it to supervising dentists, lowering per-patient costs by up to 40%. In India the dentist-to-population ratio sits at 1:10,000, well below WHO guidance, making wireless cameras central to access expansion. Regulatory lag persists; only 23 U.S. states compel private insurers to pay for asynchronous consultations. Sub-USD 500 devices on e-commerce sites often lack HIPAA-compliant encryption, exposing practices to breach penalties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Wireless Systems | -1.8% | Emerging Asia-Pacific, Latin America, MENA | Short term (≤2 years) |

| Limited Battery Life and Connectivity Issues | -1.3% | Global, especially high-volume practices | Short term (≤2 years) |

| Lack of Standardized Imaging Protocols | -0.9% | Highest fragmentation in emerging markets | Medium term (2-4 years) |

| Cybersecurity Concerns Over Patient Images | -0.7% | GDPR and HIPAA jurisdictions in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Wireless Systems

Professional-grade handpieces priced between USD 1,909 and USD 5,495 consume up to 25% of a start-up clinic’s capital budget. Leasing and subscription bundles partially offset sticker shock by converting capex to opex; MouthWatch offers USD 299 hardware with a USD 49 monthly software fee that spreads cash outflow across 36-plus months. Yet practices in markets where annual per-capita dental spend is below USD 50 still favor wired USB cameras at sub-USD 799 price points.

Limited Battery Life and Connectivity Reliability Issues

Typical lithium-polymer cells power only two hours of continuous imaging, forcing midday charging in clinics that see 30 patients daily. Metal cabinetry and lead-lined radiography walls can attenuate Bluetooth signals, while a single 1080p video stream consumes 15-20 Mbps, saturating small-office Wi-Fi. Manufacturers respond with dual-protocol designs that switch between Wi-Fi and Bluetooth based on signal strength, albeit at higher bill-of-materials cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resolution Level: FHD Gains Ground on Specialist Demand

Full-HD cameras are growing at an 11.54% CAGR, nearly two percentage points faster than the broader Wireless Intraoral Camera market. Sub-millimeter precision is vital for implant site assessment and orthodontic bracket positioning, where 0.5 millimeter errors can derail outcomes. KaVo’s DIAGNOcam Vision shows how bundled modalities justify its USD 4,500 premium because clinicians toggle between fluorescence and transillumination without swapping devices.

High-Definition systems still dominate with 56.43% share because 1080p sensors capture and compress images 30% faster, maximizing throughput in volume-driven Medicaid practices. MouthWatch’s Plus+ camera at USD 999 integrates with 50-plus software platforms, easing adoption for clinics migrating from film. 4K sensors remain niche given 100 MB file sizes that strain cloud storage and rural bandwidth. ISO 23450:2021 sets baseline resolution requirements but stops short of mandating FHD, so clinical necessity, not regulation, will dictate upgrade speed.

By Sensor Technology: CMOS Dominance Reflects Physics and Economics

CMOS sensors captured 71.54% share in 2025 and are forecast to grow 11.12% annually. On-chip analog-to-digital conversion cuts power draw by up to 60%, extending battery runtime in wireless handpieces[2]IEEE, “Low-Power CMOS Sensors for Medical Imaging,” ieeexplore.ieee.org. DEXIS Ti2 uses CMOS to achieve 20 lp/mm spatial resolution, enabling clinicians to detect early enamel lesions before they become radiographically visible.

CCD retains a small niche for ultra-low-light fluorescence imaging but loses ground as CMOS backside-illumination matches its quantum efficiency. Smartphone and automotive camera demand push CMOS wafer costs below USD 15, allowing Chinese OEMs to underprice Western incumbents by up to 70%. As hardware commoditizes, vendors differentiate through AI software bundles and service contracts rather than sensor spec sheets.

By Connectivity Technology: Bluetooth Surges on Multi-Device Pairing

Bluetooth units are tracking an 11.84% CAGR, fastest among connectivity types, as clinics deploy mobile carts and community-screening vans where peer-to-peer links outperform congested office Wi-Fi. Bluetooth 5.0 supports 2 Mbps throughput across 10 meters, sufficient for high-resolution stills and short clips. Dentulu’s MouthCAM auto-switches between Bluetooth and Wi-Fi, cutting dropped connections 60% versus single-protocol rivals.

Wi-Fi continues to command 48.76% share because 1080p video at 60 fps needs 15-plus Mbps sustained bandwidth. Proprietary RF and NFC together account for under 3% of shipments, largely in legacy systems. The lack of a DICOM-equivalent standard for intraoral photographs prolongs software silos and complicates multi-site data migration.

By Application: Orthodontics Accelerates on Aligner Adoption

Implantology led with 27.65% revenue in 2025, but orthodontics is forecast to grow fastest at 12.65% as clear aligners proliferate and insurers require photographic proof for pre-authorization. Align Technology processed 2.8 million aligner cases in Q3 2024, underscoring imaging’s role in treatment planning.

Wireless cameras let orthodontists snap progress photos each visit without relocating patients, trimming chair time by up to 5 minutes. Endodontics and oral surgery each hold mid-teen shares, driven by medico-legal documentation needs. Teledentistry models in U.S. schools and nursing homes have cut per-patient costs up to 40%, though uneven reimbursement keeps growth patchy.

By End-User: Hospitals Narrow the Gap on Integrated Networks

Specialty dental clinics and diagnostic centers controlled 58.33% demand in 2025 because 25-plus daily patients amortize device costs quickly. Hospitals, however, are growing at an 11.78% CAGR as integrated delivery networks standardize imaging workflows across inpatient and ambulatory settings. Wireless cameras streamline electronic health-record uploads, slashing documentation time 40-plus percent and aiding Joint Commission compliance.

Academic programs and public health agencies together comprise roughly one-fifth of demand, valuing ruggedness and compatibility over bleeding-edge resolution. Multi-chair group practices increasingly rotate Bluetooth cameras among operatories to cut per-chair spend by up to 70%.

By Distribution Channel: Online Sales Surge on Subscription Bundles

Direct sales retained 55.87% share in 2025 because high-ticket equipment still needs dealer financing, installation, and staff training. Yet online channels are accelerating at a 12.43% CAGR as manufacturers capture full margin and bundle AI analytics and cloud storage. Henry Schein posted Q3 2025 dental merchandise sales of USD 1.8 billion, illustrating dealers’ staying power.

Subscription models reshape cash flow: MouthWatch’s USD 299 camera with a USD 49 monthly fee has landed in 42,000 offices, proving that SaaS pricing can disrupt legacy dealer ecosystems. EU MDR rules requiring in-region authorized representatives still shield European distributors from direct imports, preserving hybrid go-to-market structures.

Geography Analysis

North America held a 44.76% share in 2025, supported by 61 dentists per 100,000 residents and 77% insurance penetration, both of which de-risk capital purchases. Henry Schein’s nine-month 2025 net sales of USD 9.3 billion, up 3.8% year-over-year, signal steady refresh cycles for digital imaging[3]Henry Schein Inc., “Form 10-Q for Q3 2025,” henryschein.com . Teledentistry reimbursement remains uneven, with only 23 states mandating private-payer coverage, damping rural adoption. Canada’s high preventive-care uptake and Mexico’s rising middle-class spending also buttress regional momentum.

Asia-Pacific is forecast to grow at a 10.54% CAGR through 2031, the fastest worldwide. Chinese public filings from leading OEMs show double-digit expansion, while Vatech’s 2024 revenue of KRW 101.98 billion (USD 76.5 million) underscores export-led growth. India’s shortage of specialists makes wireless cameras critical to teledentistry pilots in tier-2 cities. Japan’s aging population sustains demand for implant diagnostics, and South Korea’s robust export base positions it as a regional manufacturing hub even as domestic adoption lags.

Europe represents roughly one-quarter of global revenue. The May 2024 enforcement of the EU MDR raised compliance barriers, favoring incumbents with Class II certifications. Germany, France, and the UK each exceed 50 dentists per 100,000 people, but reimbursement for preventive imaging varies by country, leading to uneven uptake. Planmeca’s late-2024 capacity expansion in Finland prepares for IDS 2025 launches and indicates confidence in premium local manufacturing. Middle East, Africa, and South America remain nascent due to broadband gaps and fragmented insurance markets, yet vendor donations—such as Vatech’s 2024 equipment grant to Tygerberg Hospital—seed long-term growth.

Competitive Landscape

The wireless intraoral camera market shows moderate fragmentation. Western leaders like Dentsply Sirona, Planmeca, and Carestream Dental protect installed bases through ecosystem lock-in; migrating away can exceed USD 50,000 in conversion costs. Edge-AI launches, such as DEXIS Ti2, reduce diagnostic variability on capture, appealing to multi-site dental service organizations.

Asian challengers leverage cost advantages: Shenzhen Bangvo sells CMOS cameras for USD 399-799 but struggles with after-sales coverage in GDPR markets. Vatech’s 2025 Pearl AI partnership illustrates a pivot from hardware margins to subscription ARR, echoing SaaS playbooks in medical imaging. MouthWatch’s direct-to-clinic model converts capex into opex and has onboarded 42,000 practices without legacy dealer support.

Differentiators are shifting from megapixels to workflow: battery endurance, cybersecurity, and seamless EHR integration top buyer checklists. ISO 23450:2021 establishes a performance baseline while leaving interoperability voluntary, so vendors racing to certify cloud APIs and end-to-end encryption are set to gain share in increasingly compliance-centric purchasing cycles.

Wireless Intraoral Camera Industry Leaders

Dentsply Sirona

Planmeca Oy

MouthWatch LLC

Carestream Dental LLC

Acteon Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vatech partnered with Pearl AI to embed caries, implant, and periodontal algorithms into its imaging suite.

- December 2024: Planmeca invested in Finnish manufacturing to ready new dental units and scanners for IDS 2025.

Global Wireless Intraoral Camera Market Report Scope

As per the scope of the report, a wireless intraoral camera is a small, handheld device used by dental professionals to capture real-time images and videos of the inside of a patient's mouth. It operates without physical cables, providing greater flexibility and ease of use during examinations. This technology enhances diagnostic accuracy and patient communication.

The Wireless Intraoral Camera Market is Segmented by Resolution Level (HD and FHD), Sensor Technology (CMOS and CCD), Connectivity Technology (Wi-Fi, Bluetooth, and Other), Application (Implantology, Endodontics, Oral Surgery, Orthodontics, and Other), End-User (Hospitals, Specialty Clinics, and Other), Distribution Channel (Direct, Distributors, and Online), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| High-Definition (HD) |

| Full High-Definition (FHD) |

| CMOS |

| CCD |

| Wi-Fi |

| Bluetooth |

| Other Connectivity Technologies |

| Implantology |

| Endodontics |

| Oral And Maxillofacial Surgery |

| Orthodontics |

| Other Applications |

| Hospitals |

| Specialty Dental Clinics And Dental Diagnostic Centers |

| Other End-Users |

| Direct Sales |

| Distributors |

| Online |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Resolution Level | High-Definition (HD) | |

| Full High-Definition (FHD) | ||

| By Sensor Technology | CMOS | |

| CCD | ||

| By Connectivity Technology | Wi-Fi | |

| Bluetooth | ||

| Other Connectivity Technologies | ||

| By Application | Implantology | |

| Endodontics | ||

| Oral And Maxillofacial Surgery | ||

| Orthodontics | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Specialty Dental Clinics And Dental Diagnostic Centers | ||

| Other End-Users | ||

| By Distribution Channel | Direct Sales | |

| Distributors | ||

| Online | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current value of the wireless intraoral camera market?

The market is valued at USD 256.69 million in 2026 and is projected to reach USD 408.72 million by 2031.

Which segment is growing fastest within wireless intraoral imaging?

Orthodontic applications are expanding at a 12.65% CAGR thanks to the rise of clear aligners.

Why are CMOS sensors overtaking CCD in new wireless cameras?

CMOS delivers lower power draw and finer pixel pitch, extending battery life and improving image quality at lower cost.

How are online channels changing procurement?

Manufacturers now bundle cameras with cloud subscriptions, capturing full margin and converting capex to opex for clinics.

Which region is expected to see the strongest growth?

Asia-Pacific is forecast to grow at a 10.54% CAGR through 2031 as wireless imaging offsets specialist shortages.

What remains the biggest technical hurdle for widespread adoption?

Battery life, with most handpieces lasting about two hours of continuous use before needing a recharge.

Page last updated on: