Ophthalmology PACS (Picture Archiving And Communication System) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

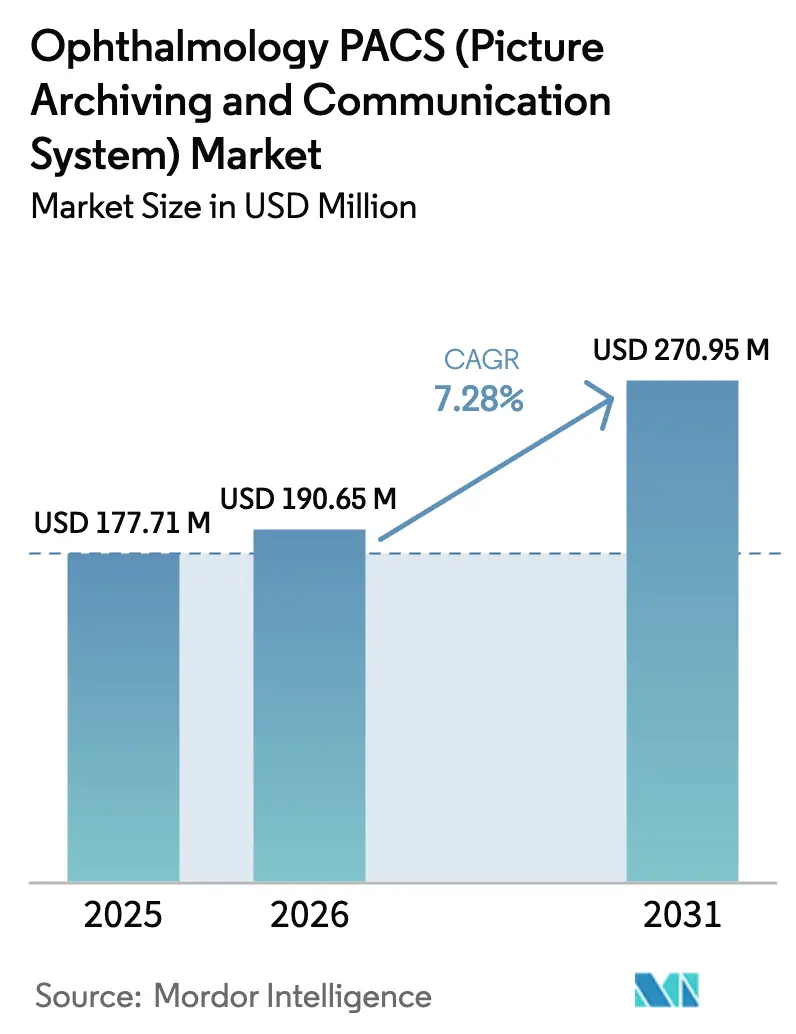

| Market Size (2026) | USD 190.65 Million |

| Market Size (2031) | USD 270.95 Million |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

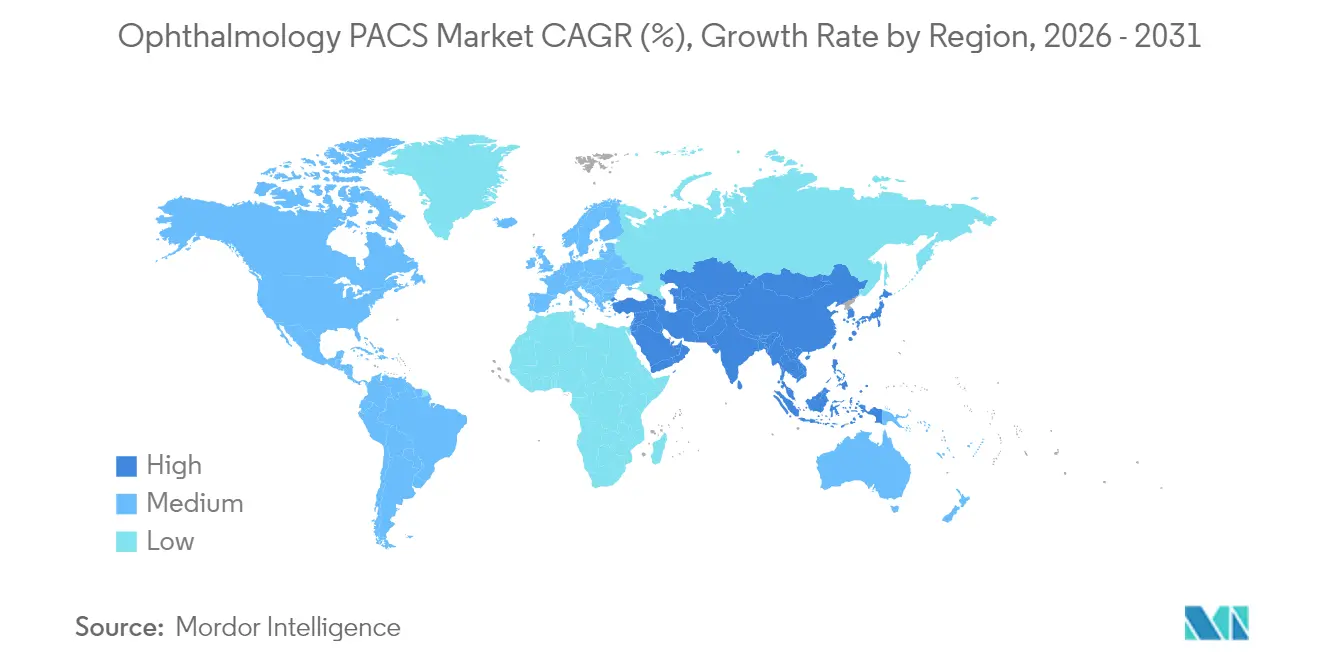

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

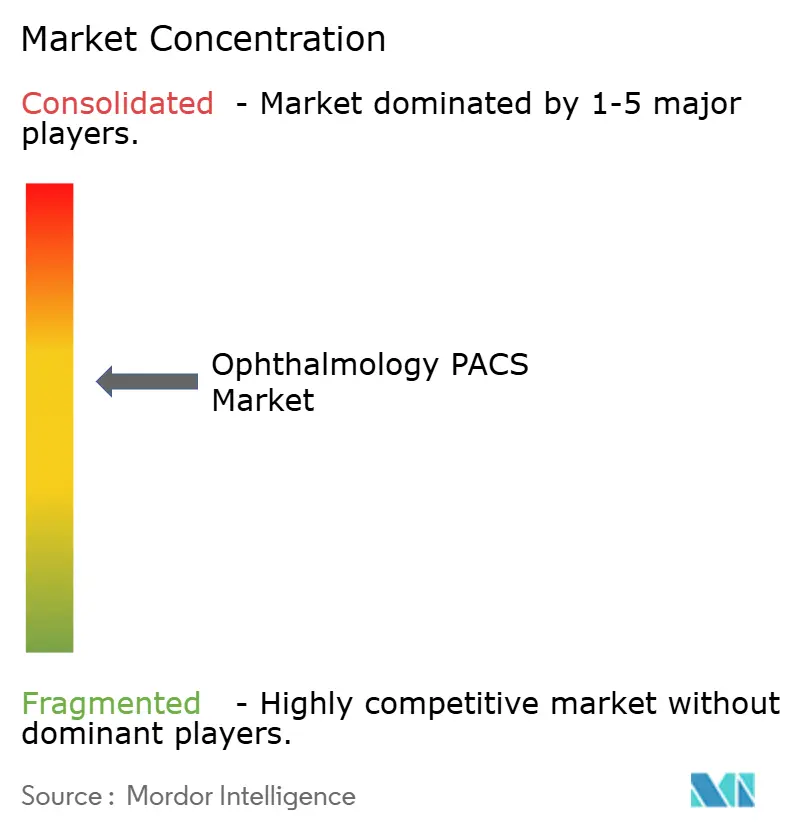

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmology PACS (Picture Archiving And Communication System) Market Analysis by Mordor Intelligence

The Ophthalmology PACS (Picture Archiving and Communication System) Market size is expected to grow from USD 177.71 million in 2025 to USD 190.65 million in 2026 and is forecast to reach USD 270.95 million by 2031 at 7.28% CAGR over 2026-2031. The growing digitization of imaging, the rapid uptake of artificial intelligence tools, and the large pool of elderly and diabetic patients are the primary forces that are expanding the ophthalmology PACS market. Integrated platforms that consolidate acquisition, storage, and analytics functions are replacing siloed, film-based workflows. At the same time, hospital groups and multisite eye-care networks pursue technology that supports value-based reimbursement and tighter clinical governance. Cloud deployment remains the fastest-growing delivery model because subscription pricing lowers capital outlays and simplifies access to AI modules, yet on-premise systems still dominate where data-sovereignty rules and legacy investments prevail. Vendors able to balance security, bandwidth efficiency, and intraoperative OCT integration continue to unlock new efficiencies for clinicians and payers.[1]Source: National Institute of Standards and Technology, “Securing Picture Archiving and Communication System,” nist.gov

Key Report Takeaways

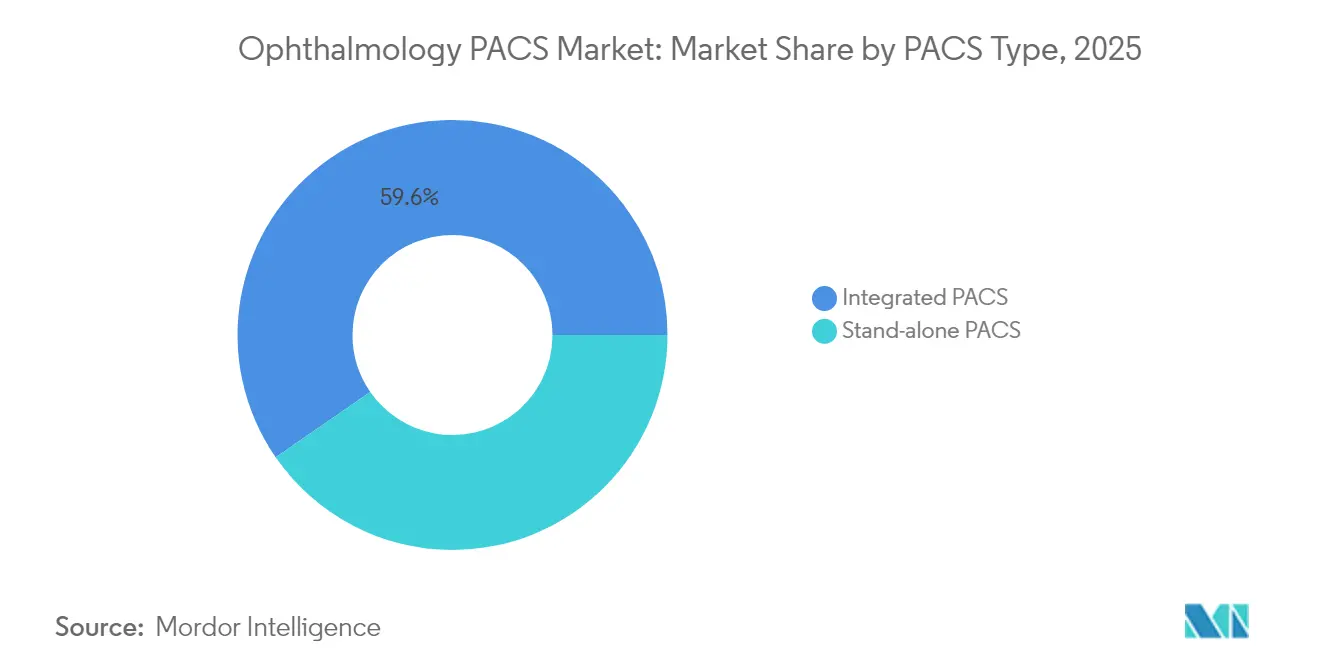

- By PACS type, integrated solutions led with 59.63% revenue share in 2025, and the same segment is forecast to grow at an 8.62% CAGR through 2031, underscoring a preference for single-vendor ecosystems.

- By delivery model, the on-premise segment held 58.22% of the Ophthalmology PACS market share in 2025, while cloud deployments are set to expand at an 8.31% CAGR by 2031.

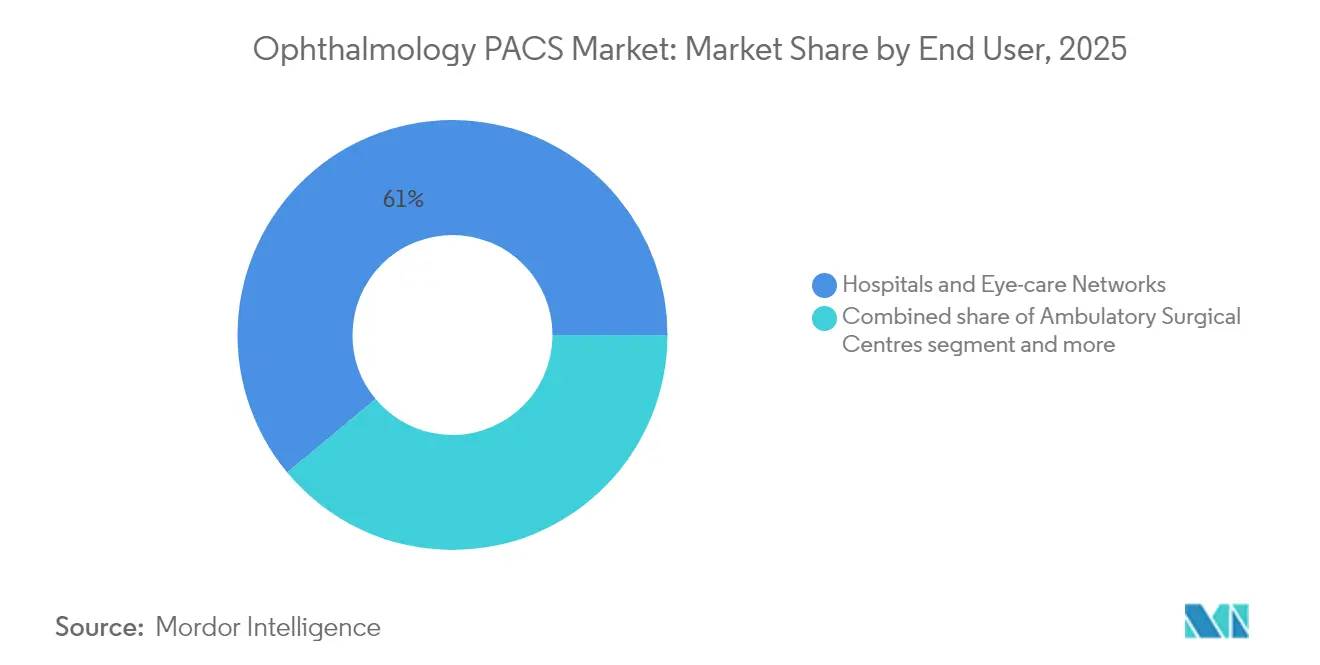

- By end user, hospitals and eye-care networks accounted for 61.05% share of the Ophthalmology PACS market size in 2025; ambulatory surgical centers are advancing at an 7.96% CAGR through 2031.

- By geography, North America commanded 42.12% revenue share in 2025, while Asia Pacific is projected to record the highest CAGR of 8.18% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ophthalmology PACS (Picture Archiving And Communication System) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic eye diseases | +1.8% | Global, with highest impact in Asia Pacific and aging Western populations | Long term (≥ 4 years) |

| Aging & diabetic population expansion | +1.5% | Global, concentrated in North America, Europe, and urban Asia | Long term (≥ 4 years) |

| Tele-ophthalmology scale-up & home-monitoring | +1.2% | Global, accelerated adoption in rural and underserved regions | Medium term (2-4 years) |

| Shift to AI-enabled cloud PACS lowering TCO | +1.0% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Surgical guidance integration (intra-op OCT feeds) | +0.8% | Advanced healthcare markets: US, Germany, Japan | Medium term (2-4 years) |

| Value-based reimbursement favouring imaging analytics | +0.7% | Primarily North America, expanding to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Eye Diseases

Global cases of diabetic retinopathy are projected to climb 17.9% by 2030, generating unprecedented imaging volumes that require robust storage and analytics. Modern OCT angiography and fundus systems produce gigabyte-level studies, pushing buyers toward PACS platforms that can rapidly visualize and analyze multilayer datasets. Hospitals link early deployment of such systems with improved outcomes in glaucoma, where earlier intervention prevents irreversible vision loss. Consequently, the ophthalmology PACS market is increasingly viewed as a preventive-care enabler rather than a cost center.

Aging and Diabetic Population Expansion

Adults older than 65 need eye examinations three to four times more often than younger cohorts, and the 4.3 billion-strong Asia Pacific population is aging quickly. Chronic diabetes adds a second demand driver, with the United States spending USD 7.2 billion annually on diabetic eye disease management. PACS solutions that support remote screening allow overextended clinicians to triage and follow higher-risk patients, reinforcing payer incentives that promote preventive imaging.

Tele-ophthalmology Scale-up and Home Monitoring

Virtual vitreoretinal consultations rose 38-fold during 2024 in several health systems, establishing tele-ophthalmology as standard care rather than a pilot service.[2]Source: Journal of Retina and Vitreous, “Virtual vitreoretinal clinics: a service delivery pathway of the future,” biomedcentral.com Home-based OCT devices stream high-resolution imagery that must flow directly into hospital archives. Cloud-native PACS with edge compute features handle intermittent connectivity, letting rural patients receive expert grading without travel. One large public program reported a 43% drop in unnecessary referrals after adding AI triage to its tele-ophthalmology workflow.

Shift to AI-enabled Cloud PACS Lowering TCO

Five-year total cost of ownership for a cloud PACS averages USD 41,250 for centers producing 1,000 studies monthly versus USD 200,000–500,000 for local deployments. Automated positioning checks, quality scoring, and draft reports cut radiologist workloads by up to 40% while improving sensitivity, making AI the differentiator that neutralizes lingering security doubts around cloud adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation & maintenance costs | -1.2% | Global, particularly impacting smaller practices and developing markets | Short term (≤ 2 years) |

| Cyber-security & data-sovereignty concerns | -0.8% | Global, with heightened sensitivity in EU and healthcare-regulated markets | Medium term (2-4 years) |

| Bandwidth limits for high-resolution ocular images | -0.6% | Rural and developing regions with limited internet infrastructure | Medium term (2-4 years) |

| Interoperability gaps with legacy ophthalmic devices | -0.5% | Global, affecting healthcare systems with diverse vendor ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation and Maintenance Costs

Comprehensive PACS rollouts can pass USD 300,000 after cables, training, and data migration, while annual support adds 15-20% of up-front spend. Complex OCT angiography archives strain budgets for independent clinics, which sometimes defer upgrades, slowing demand in price-sensitive regions.

Cybersecurity and Data-sovereignty Concerns

Healthcare cybersecurity incidents jumped 42% in 2024, and ransomware specifically targeted imaging archives. Revised FDA guidance now requires software bills of materials and continuous patching regimes for imaging products.[3]Source: National Institute of Standards and Technology, “Securing Picture Archiving and Communication System,” nist.gov Providers in Europe must also prove that cross-border cloud storage respects General Data Protection Regulation mandates, elongating procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PACS Type: Integrated Solutions Drive Market Consolidation

Integrated systems captured 59.63% ophthalmology PACS (picture archiving and communication system) market share in 2025, displacing stand-alone servers as buyers prioritize seamless modality connectivity and lower lifetime service costs. The same cohort is projected to grow at an 8.62% CAGR, indicating that future investments lean even further toward single-vendor stacks.

Healthcare groups favor integrated environments because optical coherence tomography, fundus cameras, and angiography units can upload studies into a single viewer without manual reconciliation. Faster AI deployment also tilts decisions toward integrated architectures, as algorithm providers certify one connection rather than adapting to many proprietary formats. As a result, the ophthalmology PACS market increasingly rewards vendors that bundle hardware, cloud, and analytics into one contract.

By Delivery Model: Cloud Migration Advances Despite On-premise Dominance

Although on-premise deployments held 58.22% of the ophthalmology PACS (picture archiving and communication system) market size in 2025, cloud systems are growing at 8.31% annually as bandwidth improves and CIOs seek subscription pricing. Multisite networks prefer cloud for unified governance, while independent clinics embrace it to avoid large hardware refreshes.

Performance bottlenecks persist where 10 Mbps links are unavailable, yet next-generation compression keeps imaging usable at 1 Mbps. Continuous AI model updates further push decision-makers toward cloud because new algorithms reach every location without local installs, reinforcing the long-term growth path.

By End User: ASC Growth Mirrors Outpatient Shift

Hospitals and integrated eye-care networks together controlled 61.05% share in 2025, reflecting their extensive modality fleets and training programs. Ambulatory surgical centers will post an 7.96% CAGR because cataract and retina surgeries continue migrating to outpatient sites where operating costs are lower and patient turnover is quicker.

ASC managers value browser-based PACS that support intraoperative view and postoperative quality checks from any workstation, shortening case cycle times. Emerging office-based surgery suites replicate this demand and prefer compact, subscription-priced archives that scale with case volume.

Geography Analysis

North America retained 42.12% of global revenue in 2025 as mature IT ecosystems, value-based reimbursement, and strict DICOM mandates under the Department of Veterans Affairs converged to sustain high capital investment cycles. Growth moderates, however, as many large networks already completed primary PACS installations and now prioritize incremental AI upgrades.

Asia Pacific is projected to add the largest incremental revenue at an 8.18% CAGR through 2031 due to large aging populations, higher diabetes incidence, and national e-health programs in China and India. Governments subsidize cloud infrastructure and tele-ophthalmology pilots, creating fertile ground for vendors delivering low-bandwidth solutions.

Europe shows steady adoption, aided by pan-regional interoperability initiatives and cloud approvals that satisfy GDPR. Philips recently expanded enterprise imaging services across the region, demonstrating that compliant-by-design platforms can overcome data-localization hurdles. The Middle East, Africa, and South America collectively represent an emerging opportunity pool; however, sporadic broadband and limited ophthalmologist density delay large-scale PACS rollouts. Vendors often pair philanthropic screening programs with commercial pilots to build reference sites that validate return on investment.

Regulatory Landscape

Ophthalmology PACS platforms that incorporate diagnostic functions and AI-assisted decision support increasingly fall under Software as a Medical Device (SaMD) oversight. In the United States, the FDA has published guidance and reference pages for AI-enabled medical devices, and buyers and vendors are aligning update workflows to FDA expectations, including documenting a Predetermined Change Control Plan (PCCP) for certain AI-enabled software modifications, alongside cybersecurity and lifecycle controls.

In Europe, market access for ophthalmology PACS components with medical-purpose software depends on CE marking under EU MDR 2017/745, with software classification commonly governed by MDR Annex VIII Rule 11 and the corresponding technical documentation requirements. Interoperability and image-exchange compliance are also shaped by standards bodies, with ophthalmic imaging workflows commonly relying on DICOM ophthalmic photographic imaging objects (DICOM Supplement 91). Technical files typically map software development and risk management expectations to IEC 62304 and ISO 14971.

Competitive Landscape

The Ophthalmology PACS market features moderate fragmentation. Carl Zeiss Meditec, and Heidelberg Engineering bundle hardware with native archives, leveraging device integration to defend installed bases. Sectra, Visage Imaging, and RamSoft pursue cloud-first strategies that interoperate regardless of capture modality, appealing to multisite groups seeking vendor neutrality.

Acquisition activity illustrates convergence. Philips is strengthening cloud capacity via Amazon Web Services. Strategic aims center on embedding AI algorithms inside the PACS viewer so clinicians need no separate application.

Regulatory compliance and cybersecurity are emerging battlegrounds. Platforms certified under NIST SP 1800-24 reference architecture win preference in enterprise tenders. Companies able to show continuous monitoring, zero-trust network segmentation, and Software Bill of Materials transparency differentiate themselves as hospitals tighten procurement thresholds.

Ophthalmology PACS (Picture Archiving And Communication System) Industry Leaders

Agfa-Gevaert N.V.

Carl Zeiss Meditec AG

Heidelberg Engineering GmbH

Visbion Limited

IBM (Merge PACS)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability modernization remains a primary whitespace area, since many ophthalmology imaging environments still operate as device-centric silos that drive manual data entry and incomplete order-based workflows. In the United States, ONC programs such as the Interoperability Standards Advisory (ISA), the inclusion of diagnostic imaging within USCDI, and the 21st Century Cures Act Final Rule provisions on interoperability and information blocking strengthen the business case for DICOM-consistent archives and structured exchange with EHRs using HL7, SMART on FHIR patterns. This supports demand for ophthalmology PACS offerings that connect acquisition devices to orders via DICOM Modality Worklist and expose images and associated metadata through enterprise imaging pathways, rather than leaving content in isolated departmental repositories.

Vendor-neutral, cloud-enabled enterprise imaging deployments also create a second opportunity lane when buyers want ophthalmology content unified with radiology and other specialties under common governance and security frameworks. Recent procurement and go-live activity reflects this consolidation direction, including Children’s Health Ireland selecting Sectra for a tailored ophthalmology PACS in April 2025 and Dayton Children’s Hospital going live on Sectra’s ophthalmology solution in July 2026. At the same time, collaboration layers and tele-ophthalmology scale-up increase the need for browser-based sharing, referral coordination, and integrated analytics, reinforcing the shift toward integrated platforms that consolidate acquisition, storage, and AI-enabled workflow support.

Recent Industry Developments

- July 2026: Dayton Children's Hospital went live with Sectra's ophthalmology solution as part of its enterprise imaging platform to unify ophthalmology imaging with other specialties. The deployment supports cross-department access and governance of ocular images, reinforcing enterprise imaging as a pathway to reduce ophthalmology data silos within health systems.

- November 2025: Optain Health completed the acquisition of EyePACS, expanding its teleophthalmology network footprint and aligning retinal imaging workflows with AI-enabled screening programs in primary care settings. The combination connects distributed image acquisition and grading to larger data-sharing workflows, raising expectations for PACS-integrated tele-ophthalmology operations.

- April 2024: Carl Zeiss Meditec finalized its acquisition of Dutch Ophthalmic Research Center (D.O.R.C.), broadening its retina and cornea surgical portfolio and reinforcing end-to-end workflow strategies around the ZEISS ecosystem. As surgical and diagnostic workflows tighten, this portfolio expansion supports deeper integration opportunities between devices, software, and archives used in ophthalmic care pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers ophthalmology-focused picture archiving and communication systems used to capture, store, manage, and retrieve eye imaging files across clinical workflows. The value includes revenue earned from software platforms and related modules that support image archiving, secure access, and ophthalmic workflow use.

Scope exclusions: We exclude generic image viewers, enterprise archives not tailored to ophthalmology workflows, and stand-alone service contracts that do not include an archival module.

Segmentation Overview

- By PACS Type

- Integrated PACS

- Stand-alone PACS

- By Delivery Model

- Cloud-based

- On-premise

- By End User

- Hospitals and Eye-care Networks

- Ambulatory Surgical Centres

- Specialty Clinics / Solo Practices

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the foundation for how ophthalmic imaging is produced, stored, and accessed across care sites, and how buying patterns differ between hospitals and specialty eye clinics. We reference public sources such as the World Health Organization for eye disease burden, the US FDA device databases for relevant software and imaging clearances, and the National Institutes of Health and peer-reviewed journals to understand modality usage (such as OCT and fundus imaging) and workflow changes.

To keep assumptions realistic, we also review company filings, investor presentations, and association websites tied to ophthalmology and medical imaging. We add reputable press updates on digital health adoption and cloud policies where they help explain purchasing behavior. Where helpful, paid subscriptions are used for company financials and intelligence and for patent databases, mainly to validate product direction, commercialization timelines, and module bundling practices. These desk sources are illustrative and not exhaustive, since additional references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys help confirm what providers actually buy, how solutions are deployed, and how pricing changes between license and subscription models. We engaged with hospital imaging leaders, ophthalmology clinic administrators, IT managers, and implementation specialists across the Americas, EMEA, and APAC to verify adoption timing, renewal cycles, and module attach rates against reported purchasing behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 41% |

| Mid tier: 56% | Functional/Unit leaders: 30% | EMEA: 37% |

| Smaller Players: 19% | Managers: 57% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using top-down demand pool logic, where care-site counts and ophthalmic imaging activity are translated into likely PACS adoption and replacement needs by region. We then corroborate totals with selective bottom-up approximations using sampled pricing ranges, typical contract structures, and channel checks so the final totals stay aligned with what providers can budget and deploy.

Key inputs used in the model include the installed base of ophthalmic imaging equipment in care sites, the share of imaging that is digitally archived versus locally stored, the readiness for cloud deployment in provider IT setups, the mix of hospitals versus specialty clinics and ambulatory surgical centers, and average revenue per site driven by modules and the number of users. When direct volume data is not available, gaps are handled through conservative ranges validated in interviews, followed by consistency checks against procurement cycles and observed migration patterns from on-premise to hosted deployments.

For forecasting, scenario analysis is used so adoption and pricing can be adjusted under different conditions, such as faster cloud uptake, slower capital spending, or tighter data residency rules. The final forecast path is selected only after the variable direction and range are confirmed with expert feedback, and after we confirm that growth remains consistent with healthcare IT spending signals in the major regions.

Data Validation & Update Cycle

Validation is done through multiple checkpoints so the final output is not dependent on one assumption. We compare model outputs with independent signals such as care-site counts, typical contract values, and regional digitization maturity, and then investigate any large variances before sign-off.

When anomalies appear, assumptions are revisited and the research team re-contacts sources to confirm whether the issue is timing, pricing, or an inclusion difference in what is being purchased. Reports refresh annually, and interim updates are added when material events can shift demand or revenue recognition. Before delivery, an analyst runs a fresh pass so clients receive the latest updated view with consistent logic across history and forecasts.

Mordor Intelligence's Ophthalmology Pacs Picture Archiving and Communication System Market Estimate Compared With Other Published Estimates

Published market sizes for ophthalmology PACS can vary even when the topic name looks similar. In day-to-day research, differences usually come from what is counted as an ophthalmology PACS product, how deployment models are treated, and which year is used as the anchor for pricing and adoption.

By checking modality-linked usage (such as OCT and fundus imaging workflows) and refreshing site-level pricing assumptions, Mordor Intelligence keeps the total focused on ophthalmology-specific archiving and workflow platforms, instead of including broad enterprise archives or generic viewers that are not built for eye-care imaging.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 177.71 M (2025) | |

| Global Consultancy A | USD 163.84 M (2024) | Uses a different base year and a wider scope lens that can blend adjacent imaging IT tools into the revenue pool, which shifts the starting value and then carries into the forecast. |

| Industry Publisher B | USD 151.42 M (2024) | Applies alternate type and delivery definitions and may treat standalone tools and communication features differently, which can lower the counted revenue for the same year. |

The spread in the table is mainly explained by scope boundaries and anchoring year, not by disagreement that the market is expanding. When scope is kept to ophthalmology-specific archiving and workflow use, and assumptions are cross-checked with care-site buying and renewal patterns, the result stays easier to trace and repeat across regions and time.

Key Questions Answered in the Report

Why are integrated ophthalmic PACS platforms gaining preference over stand-alone systems?

Hospitals and multi-site eye-care networks favor integrated solutions because they remove vendor fragmentation, streamline multi-modality workflows, and better support AI analytics, reducing both clinical hand-offs and IT complexity.

What strategic benefit does cloud deployment offer ophthalmology practices?

Cloud PACS lowers up-front capital, speeds access to new AI modules, and enables anytime image review, giving smaller practices enterprise-grade capability without maintaining local hardware.

How are ambulatory surgical centers shaping demand for ophthalmic PACS?

The outpatient shift in cataract and retina procedures pulls demand toward browser-based PACS that support intraoperative viewing and quick postoperative review, aligning with ASCs’ need for fast case turnover.

Which technology feature most influences buying decisions for new PACS installations?

Native AI tools—such as automated image quality checks and retinal layer segmentation—have become decisive, as administrators seek productivity gains and consistent diagnostic accuracy.

What is the primary security concern slowing PACS adoption in regulated regions?

Health systems worry about ransomware and data-sovereignty compliance, so vendors that demonstrate zero-trust architectures and full audit trails gain procurement advantage.

How does tele-ophthalmology expansion affect PACS requirements?

With home-based OCT devices and virtual consultations generating distributed data, buyers demand cloud-native archives that can ingest images from remote sites while maintaining diagnostic fidelity.

Page last updated on: