Philippines Passenger Car Taxi Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

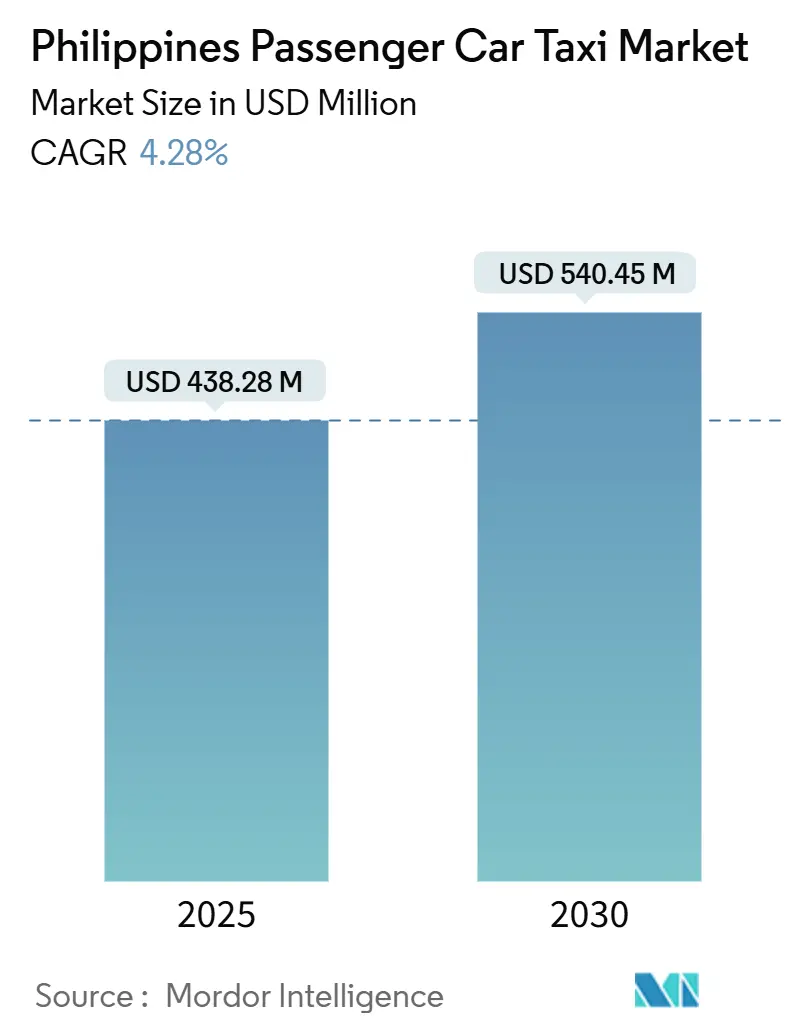

| Market Size (2025) | USD 438.28 Million |

| Market Size (2030) | USD 540.45 Million |

| Growth Rate (2025 - 2030) | 4.28% CAGR |

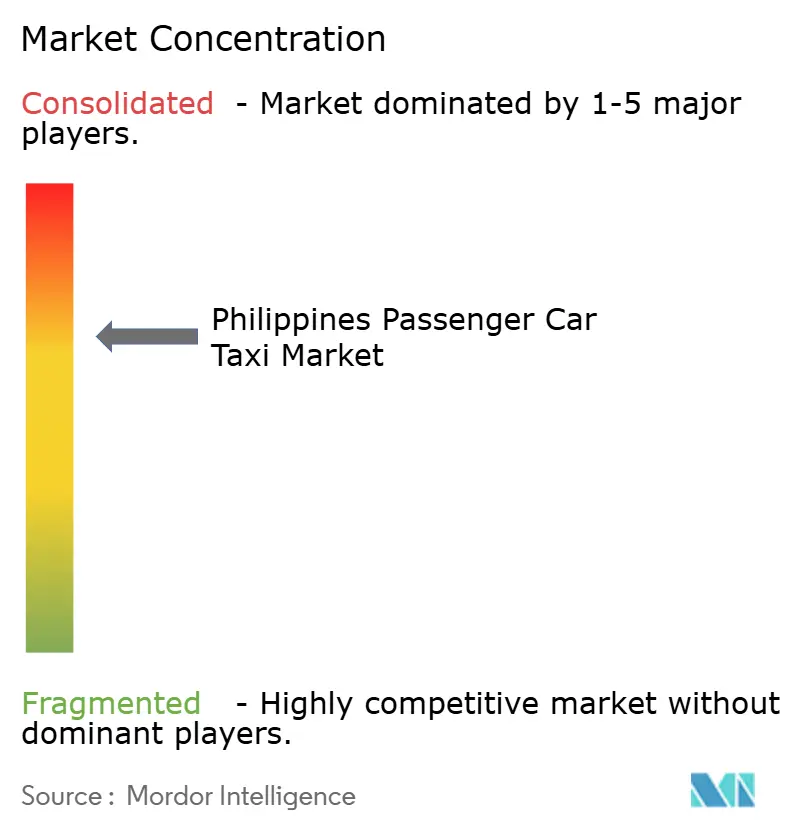

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Passenger Car Taxi Market Analysis by Mordor Intelligence

The Philippines passenger car taxi market stood at USD 438.28 million in 2025 and is projected to reach USD 540.45 million by 2030, expanding at a 4.28% CAGR over the forecast period. Ongoing regulatory modernization, fast-rising smartphone adoption, and recovering tourism demand steer the Philippines taxi market toward digitally enabled services. Intensifying platform competition, public-sector incentives for “green fleets,” and rebounding corporate travel budgets create additional momentum for operators able to invest in technology and fleet upgrades. Yet the sector continues to navigate fuel-price volatility, chronic congestion, and an uneven roll-out of charging infrastructure outside Metro Manila—all of which temper near-term utilization rates. Overall, the Philippines taxi market displays resilience, with structural reforms now translating into higher compliance levels and clearer growth pathways.

Key Report Takeaways

- By service type, traditional taxis led the Philippines taxi market with 52.86% of the share in 2024, whereas ride-sharing is projected to climb at a 7.56% CAGR to 2030.

- By booking type, offline channels accounted for 58.72% of the Philippines taxi market size in 2024, while online booking will grow at a 7.89% CAGR to 2030.

- By vehicle type, sedans captured 48.19% of the Philippines taxi market share in 2024, and hatchbacks are advancing at a 7.28% CAGR over the outlook period.

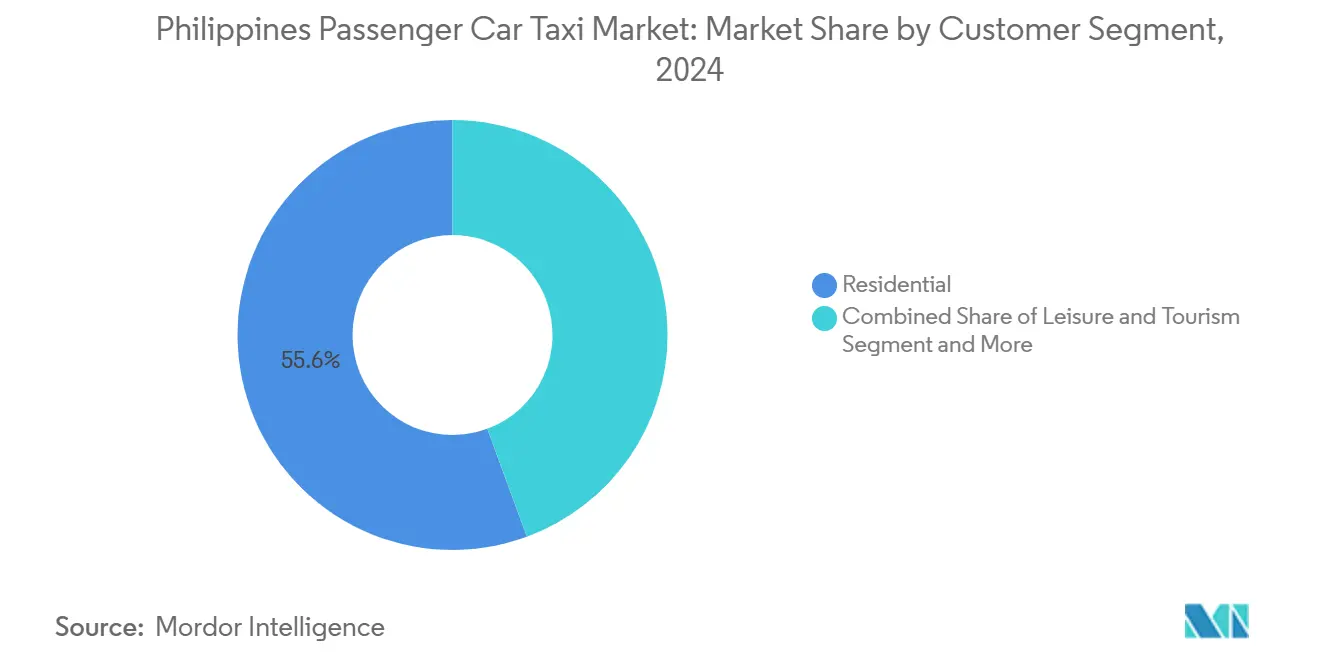

- By customer segment, residential users represented 55.63% of the Philippines taxi market size in 2024, whereas leisure and tourism rides are rising at a 7.33% CAGR through 2030.

- By powertrain, internal-combustion units dominated the Philippines taxi market, with an 89.48% share in 2024, and electric taxis are accelerating at an 8.65% CAGR to 2030.

- By use case, urban commute trips commanded a 59.38% share of the Philippines taxi market size in 2024, while tourist hourly hires are set to expand at an 8.56% CAGR by 2030.

- By geography, Metro Manila held 61.76% of Philippines taxi market share in 2024, while Visayas is forecast to expand at a 7.42% CAGR through 2030.

Philippines Passenger Car Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Super-app Dominance | +1.2% | National; strongest in Metro Manila | Medium term (2-4 years) |

| LTFRB Overhaul | +0.8% | National; early gains in NCR & Calabarzon | Long term (≥ 4 years) |

| Corporate Travel Rebound | +0.6% | Metro Manila, Cebu, Davao CBDs | Short term (≤ 2 years) |

| Tourism Rebound | +0.7% | Visayas & key tourist hubs | Medium term (2-4 years) |

| Digital Leasing Shift | +0.4% | Major urban centers | Short term (≤ 2 years) |

| E-taxi Incentives | +0.5% | National; Metro Manila first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Dominance of Super-Apps

Super-app ecosystems continue to redraw competitive boundaries in the Philippines taxi market by bundling ride-hailing, food delivery, and digital payments inside a single interface[1]“Grab’s Economic Impact Study,”, Gabriel Pabico Lalu, manilastandard.net. Grab’s 42 million Southeast Asian users generate PHP 3.42 in economic activity for every peso spent, creating powerful network effects in Metro Manila. The LTFRB’s approval of 100,000 new transport-network-vehicle slots legitimizes platform growth, while localized challengers such as JoyRide leverage telco partnerships to penetrate underserved provinces. Rising regulatory oversight of surge pricing keeps pressure on algorithms but is unlikely to derail consumer migration toward app-based bookings.

Corporate Mobility Budgets Recovering Post-COVID-19

Business travel and hybrid-work commuting are reviving taxi demand in CBDs. Asian Development Bank forecasts 6.2% GDP growth in 2025, restoring corporate mobility outlays that temporarily froze during lockdowns[2]“Asian Development Outlook 2024,”, Asian Development Bank, adb.org. Government agencies such as Bacolod City’s MABB Cab illustrate institutional uptake of app-based fleet management, signaling to suppliers that enterprise channels are viable revenue pools. Demand is strongest in finance, BPO, and logistics clusters in Metro Manila, Cebu, and Davao.

Underground Taxi-Leasing Market Shifting to Digital

Digital fleet-management apps disintermediate traditional intermediaries who previously leased licenses at opaque rates. By offering transparent driver earnings and centralized schedule management, emerging platforms cut informal costs and encourage compliance with franchise rules in metropolitan corridors.

“Green Fleet” Incentive Program for E-Taxis

Fiscal perks under the Electric Vehicle Industry Development Act, including import-duty exemptions and VAT zero-rating, improve the total cost of ownership of electric taxis. Green GSM’s USD 1 billion commitment to 2,500 EV cabs validates the economics and accelerates early-stage charging deployments in Metro Manila.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Congestion | −1.1% | Metro Manila & other large cities | Long term (≥ 4 years) |

| Fuel Price Volatility | −0.9% | National; most acute outside NCR | Short term (≤ 2 years) |

| Colorum Competition | −0.8% | Provincial routes | Medium term (2-4 years) |

| Limited EV Chargers | −0.6% | Visayas and Mindanao corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Fuel-Price Pass-Through on Fares

Fuel costs remain a swing factor for profitability because fare adjustments trail diesel and gasoline spikes. The LTFRB raised the flag-down rate to PHP 50 in November 2024, but operators had already weathered months of margin compression[3]“Fuel Fare Hike Approval,”, Daxim Lucas, sunstar.com.ph. Provincial fleets, which log longer average trip distances, feel volatility more than urban counterparts. Platform players are testing fuel-surcharge calculators, yet solutions remain nascent.

Slow EV-Charging Roll-Out Outside Metro Manila

The Department of Energy now requires large fuel stations to install chargers, yet coverage gaps persist across tourist belts in Visayas and Mindanao. Range anxiety forces EV-taxi operators to concentrate assets in NCR, delaying a nationwide green transition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Adoption Accelerates

Offline requests kept a 58.72% slice of the Philippines taxi market share in 2024, proving that street-hailing habits and patchy cellular coverage remain influential determinants of consumer behavior. However, online bookings are forecast to climb at a 7.89% CAGR through 2030 as smartphone penetration rises, mobile data plans become cheaper, and passengers seek transparent journey tracking.

The inflection toward app-based reservations gathers speed thanks to LTFRB guidelines that permit dynamic pricing within guardrails and compel driver-rating disclosures. Operators partnering with telcos unlock priority data lanes, improving uptime and acceptance rates. In peri-urban zones, offline channels will persist until 4G and 5G networks mature. Yet, blended strategies—equipping vehicles for both street and digital demand—offer the most resilient revenue mix.

By Service Type: Platform Competition Intensifies

Traditional taxis still controlled 52.86% of Philippines taxi market share in 2024, reflecting the longevity of franchise allocations and consumer familiarity with metered fares. Ride-sharing models, however, are sprinting ahead at a 7.56% CAGR as multi-stop pooling and in-app promos win budget-travel cohorts.

Regulators now vet surge-pricing formulas after investigative media flagged premiums levied during extended wait times. New arrivals such as Green GSM deploy all-electric fleets with zero booking fees to differentiate. Ride-hailing hybrids—licensed taxis operating on digital platforms—are emerging as a compliance-friendly bridge between the two archetypes.

By Vehicle Type: Sedan Preference Persists

Sedans accounted for 48.19% of the Philippines taxi market size in 2024 because they balance cabin comfort with operating costs in congestion-heavy corridors. Hatchbacks follow with the fastest expansion, advancing 7.28% annually as owners downsize engines to offset fuel inflation.

SUVs and MUVs carve out niche roles in premium or group hire, while electric sedans enter pilot fleets under green-fleet incentives. Mandatory Euro-4 standards push replacement cycles toward newer models equipped with idle-stop systems, further boosting fuel savings over older units.

By Customer Segment: Residential Demand Dominates

Residential commuters produced 55.63% of the Philippines' taxi market size in 2024 due to everyday mobility needs for work, school, and shopping. Leisure-and-tourism trips, though smaller, are accelerating at 7.33% as domestic travel rebounds.

Corporate ridership is stabilizing, underpinned by hybrid-work shuttles and employee travel accounts linked directly to super-apps for automated expense tracking. Seasonal spikes arrive during major holidays when family visits and tourist excursions add incremental demand.

By Powertrain: Electric Transition Begins

Internal-combustion engines dominated 89.48% of the Philippines' taxi market share in 2024, yet electric units are expanding at an 8.65% CAGR due to duty-free imports and VAT exemptions.

Green GSM’s 2,500-unit EV order illustrates the scale advantage possible when lifetime fuel savings offset CAPEX. Meanwhile, diesel fleets adopt alternative measures such as retreading low-rolling-resistance tires and using route-optimization apps to mitigate fuel costs until chargers proliferate.

By Use Case: Urban Commute Leads

Urban commuting captured 59.38% of the Philippines' taxi market share in 2024, mirroring population density and bus and rail coverage gaps. Tourist hourly hires post the highest 8.56% CAGR, using flexible multi-stop itineraries that accommodate sightseeing.

Airport transfers remain vital in regions lacking dedicated rail lines to terminals, whereas inter-city hires cater to provincial travelers who prioritize door-to-door convenience over bus connections. Corporate movement rides, though smaller, gain stickiness via integration with HR expense portals.

Geography Analysis

Metro Manila contributed 61.76% of the Philippines' taxi market size in 2024, underpinned by 13 million residents, dense CBD clusters, and round-the-clock activity across airports, seaports, and entertainment districts. While average 10-km trips take 25 minutes and 30 seconds, ongoing rail extensions and elevated-expressway projects should unlock new demand nodes even as congestion erodes near-term vehicle utilization. The LTFRB’s 96% consolidation success rate within the capital further standardizes service quality and accelerates digital adoption.

Visayas, encompassing Cebu, Bohol, and Palawan, is the fastest-expanding sub-region with a 7.42% CAGR through 2030. Airport expansion, hotel construction, and restored cruise itineraries magnify taxi bookings, especially for tourist hourly hires. Iloilo’s call for 200–300 extra units signals capacity shortages that new entrants can exploit. Seasonal peaks coincide with island festivals and diving season, requiring flexible fleet redeployment strategies.

Mindanao posts steady but lower growth as security perceptions and infrastructure gaps temper large-scale tourism. Davao City leads regional modernization, fielding QR-coded cashless taxis and experimenting with black-colored fleets that align with local ordinances. Zamboanga’s approval of 50 fresh units through a cooperative structure suggests that LTFRB modernization is taking root, albeit at a measured pace. Across all three island groups, localized pricing dynamics, regulatory compliance, and charging-infrastructure roll-outs will dictate sub-regional performance.

Competitive Landscape

The Philippines taxi market features a dual-tier structure in which a handful of digital platforms dominate bookings in urban centers. At the same time, a fragmented group of traditional operators serves price-sensitive or digitally excluded riders. Grab remains the leading super-app, generating PHP 3.42 in spillover economic activity per peso spent and lowering national unemployment by up to 1.6% during pandemic years. However, regulatory scrutiny of surge algorithms pressures the company to refine pricing models.

Green GSM’s USD 1 billion push for 2,500 EVs represents the boldest single expansion, targeting eco-conscious passengers and cost-sensitive drivers drawn by lower per-kilometer energy charges. Local challengers such as JoyRide leverage telco-grade connectivity to cut booking latency, while inDrive pilots blockchain-based mapping incentives that reward drivers with tokens for road-data collection.

Competitive differentiation now hinges on technology stack depth—real-time GPS, automated fare collection, and embedded finance—rather than fleet size alone. Operators integrating scheduling, maintenance, and driver-rating analytics can compress downtime and elevate customer loyalty. Conversely, colorum fleets relying on informal lease arrangements face shrinking addressable demand as enforcement tightens.

Philippines Passenger Car Taxi Industry Leaders

Grab Holdings Inc.

JoyRide Philippines

OWTO Philippines

Micab Systems Corp.

E Pick Me Up Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vietnamese firm Green GSM launched the nation’s first all-electric taxi service, deploying 2,500 VinFast units at a USD 1 billion cost, aiming to create up to 70,000 jobs.

- March 2025: Bacolod City launched MABB Cab for government employees through a partnership with Grab.

Philippines Passenger Car Taxi Market Report Scope

| Online Booking |

| Offline Booking |

| Ride Hailing |

| Ride Sharing |

| Traditional Taxis |

| Hatchback |

| Sedan |

| SUVs |

| MUVs |

| Corporate |

| Leisure and Tourism |

| Residential |

| ICE |

| Electric |

| Urban Commute |

| Airport Transfer |

| Inter-city / Long-haul |

| Tourist/Leisure Hourly Hire |

| Corporate/MICE Movements |

| Visayas |

| Mindanao |

| Luzon |

| By Booking Type (Value) | Online Booking |

| Offline Booking | |

| By Service Type (Value) | Ride Hailing |

| Ride Sharing | |

| Traditional Taxis | |

| By Vehicle Type (Value) | Hatchback |

| Sedan | |

| SUVs | |

| MUVs | |

| By Customer Segment (Value) | Corporate |

| Leisure and Tourism | |

| Residential | |

| By Powertrain (Value) | ICE |

| Electric | |

| By Use Case (Value) | Urban Commute |

| Airport Transfer | |

| Inter-city / Long-haul | |

| Tourist/Leisure Hourly Hire | |

| Corporate/MICE Movements | |

| By Geography (Value) | Visayas |

| Mindanao | |

| Luzon |

Key Questions Answered in the Report

How big will the Philippines taxi market be by 2030?

The sector is forecast to reach USD 540.45 million by 2030, reflecting a 4.28% CAGR from 2025.

Which region is expanding fastest for taxi services in the Philippines?

Visayas leads with a projected 7.42% CAGR, lifted by tourism recovery in Cebu, Bohol, and Palawan.

Are electric taxis commercially viable in the Philippines?

EV adoption remains nascent share but is accelerating at an 8.65% CAGR, helped by duty-free imports and zero-VAT incentives.

What recent policy changes impact taxi fares?

The LTFRB raised the nationwide flag-down rate to PHP 50 in November 2024, easing pressure from fuel-price spikes.

How is congestion affecting taxi profitability?

Metro Manila congestion cuts average trips per vehicle and results in USD 63.6 million daily productivity losses, lowering operator margins.

Page last updated on: