Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

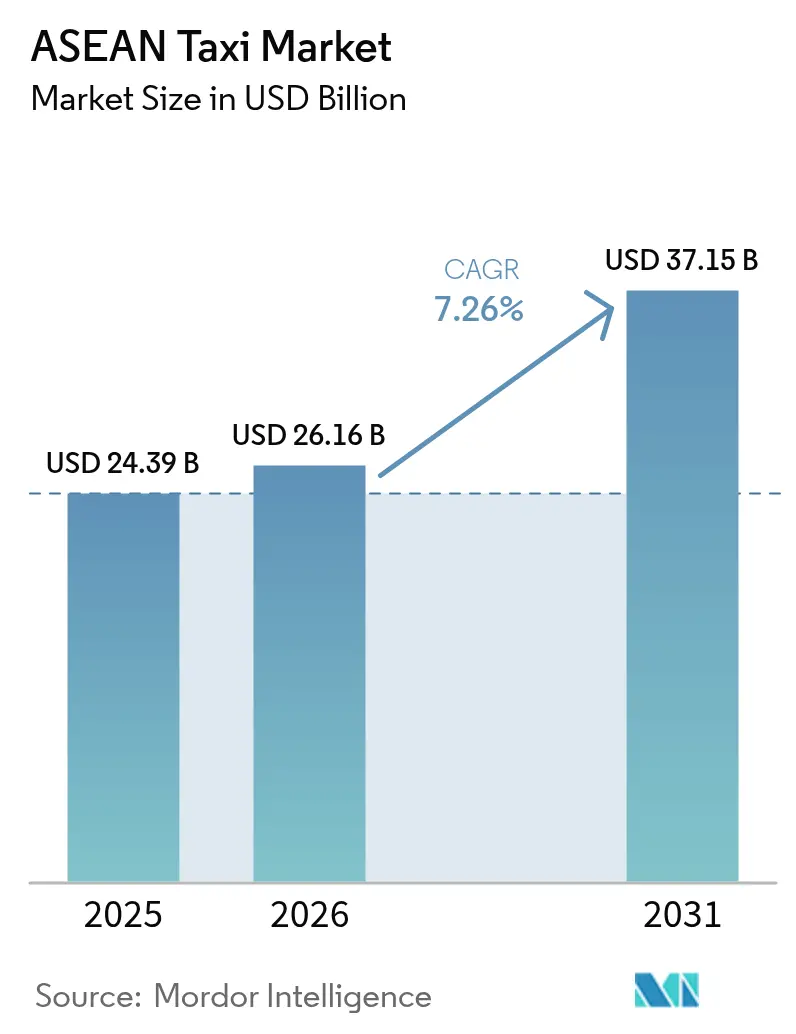

| Base Year Market Size (2025) | USD 24.39 Billion |

| Market Size (2026) | USD 26.16 Billion |

| Market Size (2031) | USD 37.15 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

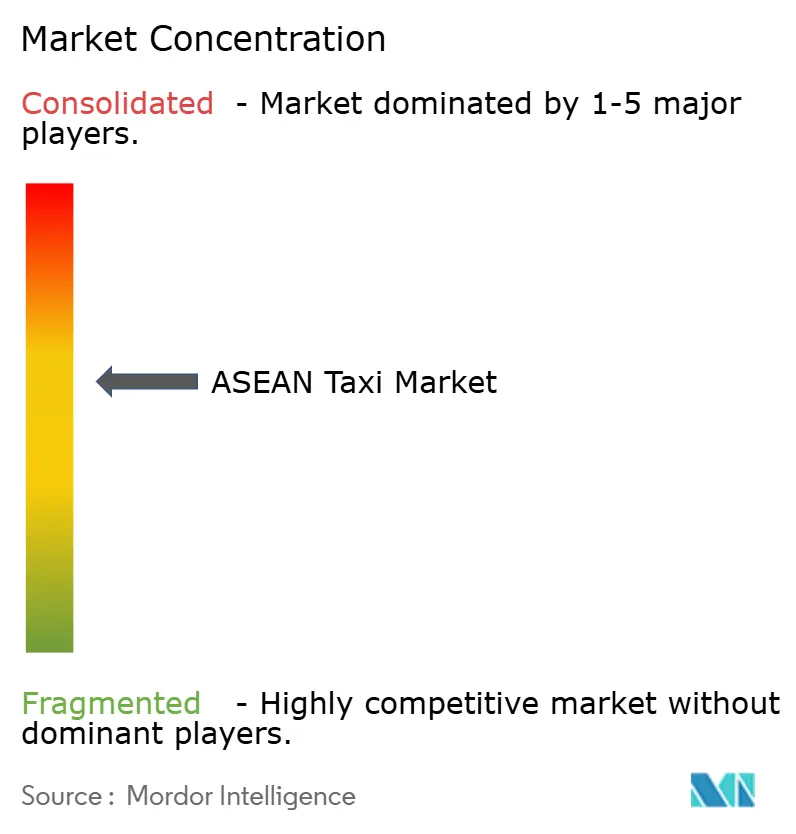

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Taxi Market Analysis by Mordor Intelligence

The ASEAN taxi market size is expected to grow from USD 24.39 billion in 2025 to USD 26.16 billion in 2026 and is forecast to reach USD 37.15 billion by 2031 at 7.26% CAGR over 2026-2031. Rapid urbanization, expanding smartphone ownership, and growing preference for cash-free mobility underpin this trajectory across Southeast Asia’s heterogeneous economies. Platform-integrated services are displacing street-hail models because real-time matching, transparent pricing, and centralized payments improve vehicle utilization and rider trust. Governments are modernizing legacy taxi legislation to legitimize app-based operations while regulating fares and driver accreditation, stabilizing growth expectations. Competitive differentiation now rests on electrification, multimodal linkages, and subscription-based corporate mobility programs, each amplifying demand for value-added services within the ASEAN taxi market.

Key Report Takeaways

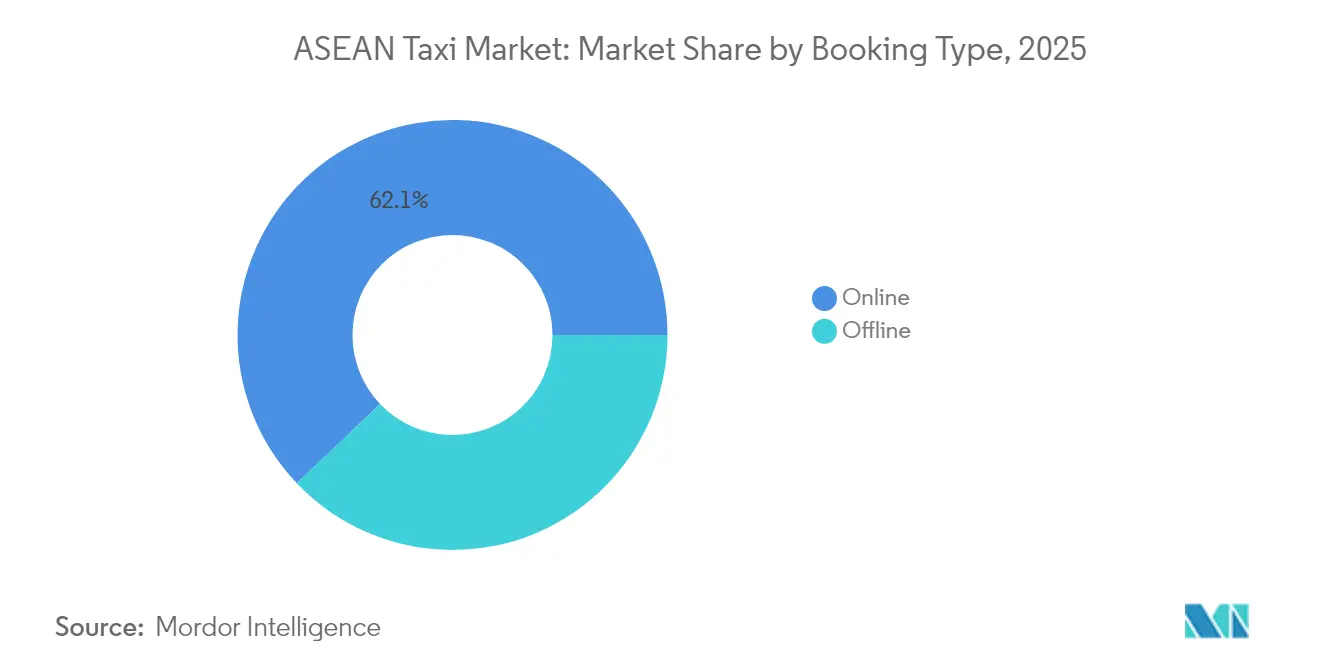

- By booking type, online booking commanded 62.11% of the ASEAN taxi market share in 2025 and is forecast to climb at a 7.72% CAGR through 2031.

- By service type, platform-integrated metered taxis delivered 43.55% of the ASEAN taxi market share in 2025, whereas shared shuttle services posted the highest projected CAGR at 7.63% to 2031.

- By vehicle body style, sedans held 42.76% of the ASEAN taxi market share in 2025; SUVs and MPVs exhibit the fastest momentum, advancing at an 8.48% CAGR through 2031.

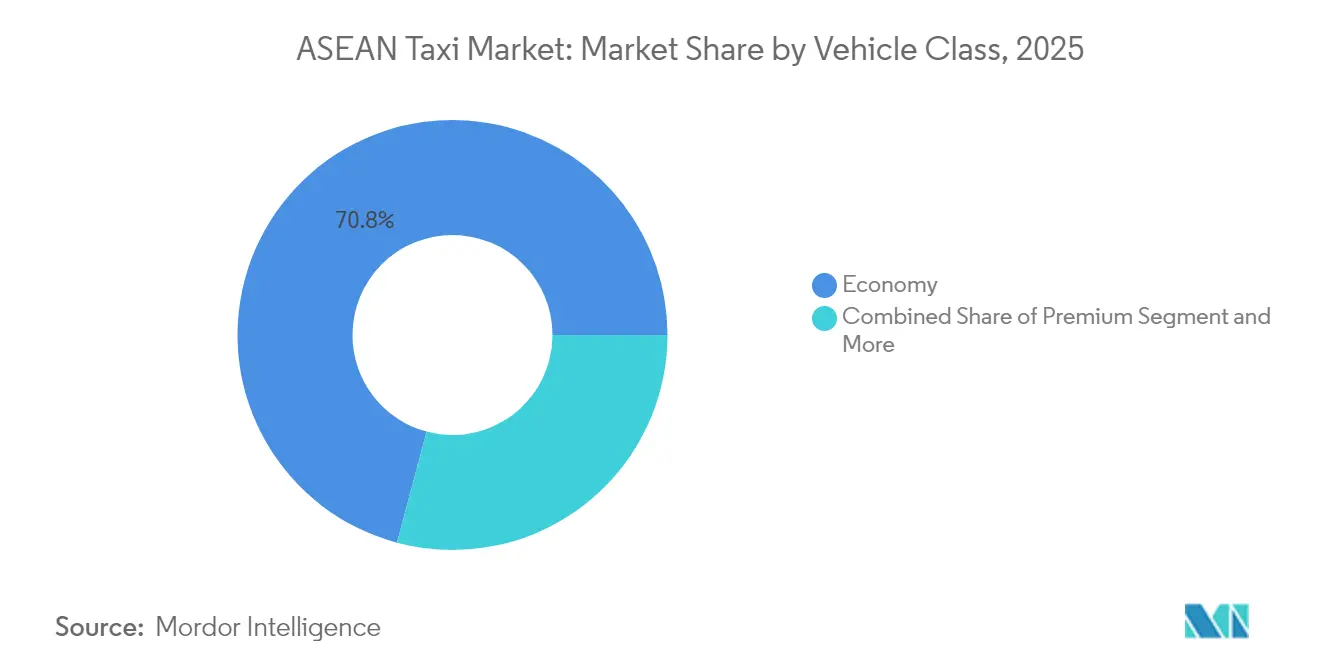

- By vehicle class, economy vehicles generated 70.84% of the ASEAN taxi market share in 2025, while premium and executive classes are set for an 8.29% CAGR through 2031.

- By end-user, corporate accounts represented 47.02% of the ASEAN taxi market share in 2025; airport services lead growth with an 8.16% CAGR through 2031.

- By country, Indonesia dominated with a 37.10% of the ASEAN taxi market share in 2025, whereas Vietnam registered the strongest forecast growth at an 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone and E-Wallet Penetration Enabling App-Based Bookings | +1.5% | Global ASEAN, led by Singapore, Thailand | Short term (≤ 2 years) |

| Rapid Urbanization and Worsening Congestion | +1.2% | Indonesia, Philippines, Vietnam core markets | Medium term (2-4 years) |

| Corporate Mobility-Subscription Demand Surge | +1.1% | Business districts across major ASEAN cities | Short term (≤ 2 years) |

| Taxi-Fleet Electrification Incentives (E-Taxis) | +0.9% | Vietnam, Indonesia, Thailand with EV policies | Long term (≥ 4 years) |

| Government Support for Regulated Ride-Hailing Frameworks | +0.8% | Thailand, Indonesia, Philippines regulatory zones | Long term (≥ 4 years) |

| Multimodal Integration with Mass-Transit Networks | +0.7% | Singapore, Bangkok, Kuala Lumpur metro areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Worsening Congestion

As urban congestion tightens its grip on ASEAN megacities, cities like Jakarta grapple with pronounced peak-hour slowdowns. In Manila, traffic toll manifests as significant productivity losses, underscoring the demand for dependable point-to-point mobility. Taxis are indispensable, particularly during seasonal challenges like flooding and when public transport falters. Meanwhile, ride-hailing platforms distinguish themselves by adeptly rerouting drivers, curbing travel uncertainties—this edge positions them favorably against conventional street-hail services in tech-savvy urban areas.

Corporate Mobility-Subscription Demand Surge

Across ASEAN, corporations are increasingly turning to mobility subscriptions, drawn by the allure of cost savings and enhanced operational flexibility. In a notable shift, companies are moving away from owning fleets and opting for platform-based services. This trend is underscored by providers like GoCorp, which have reported robust growth. The public sector isn't lagging, with Bacolod City prominently utilizing Grab for official travel. This move has allowed the city to enjoy streamlined billing and efficient compliance tracking benefits. As hybrid work models gain traction, the demand for flexible ride services intensifies, making subscription-based taxi services an attractive and scalable solution for businesses.

Taxi-Fleet Electrification Incentives (E-Taxis)

Thailand offers up to THB 100,000 per electric car, and Vietnam’s Xanh SM operates 30,000 e-taxis domestically before launching abroad[1]“Investor Relations Presentation 2024,”, VinFast, vinfastauto.com. Indonesia mandates a 20% electric composition in ride-hailing fleets by 2030. Electric vehicles cut fuel outlays by 60% and meet municipal air-quality goals, reinforcing government momentum behind cleaner fleets. ComfortDelGro in Singapore aims for full electrification by 2040 and is already running autonomous electric pilots, underscoring technology convergence within the ASEAN taxi market.

Government Support for Regulated Ride-Hailing Frameworks

Policy makers now view ride-hailing as integral to job creation, tax revenue, and digital-economy growth. Thailand authorized taxi-operated ride-hailing apps in 2024, providing traditional fleets a technology pathway adoption [2]“Ride-Hailing Regulation Update 2024,”, Ministry of Transport Thailand, mot.go.th. Indonesia capped platform commissions at 20% to safeguard driver earnings, which tempered public protests and stabilized service quality. Singapore’s Platform Worker Bill mandates social protections like insurance and CPF contributions, signaling government commitment to equitable gig-work conditions[3]“Platform Worker Bill Debates 2024,”, Parliament of Singapore, parliament.gov.sg. Such balanced regulation lowers operational risk and sustains investor confidence in the ASEAN taxi market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Traffic Lowers Driver Utilization and Reliability | -0.9% | Jakarta, Manila, Bangkok metropolitan areas | Short term (≤ 2 years) |

| Rising Platform Commission Fees Squeeze Driver Earnings | -0.8% | Indonesia, Philippines platform-dominated markets | Medium term (2-4 years) |

| Licensing Caps and Quota Restrictions | -0.6% | Singapore, Thailand traditional taxi sectors | Long term (≥ 4 years) |

| Preference For Motorcycle Taxis Over Cars in Key Cities | -0.5% | Indonesia, Philippines urban core areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heavy Traffic Lowers Driver Utilization and Reliability

In ASEAN megacities, severe traffic congestion undermines driver productivity and service reliability. Jakarta's peak-hour slow speeds curtail trip volumes and escalate fuel costs. Meanwhile, Bangkok and Manila grapple with significant economic setbacks caused by gridlock. Prolonged delays deter drivers from taking longer trips, particularly when return fares remain unpredictable. While ride-hailing platforms provide routing optimizations, they remain hampered by physical bottlenecks during rush hours, further entrenching the structural constraints of the region's taxi market.

Licensing Caps and Quota Restrictions

Across ASEAN, taxi fleet expansion is stymied by licensing caps and quota restrictions. In Singapore, stringent license quotas have curtailed the active fleet size. Meanwhile, Thailand and Malaysia grapple with permit limits and sluggish approval processes. This inflexible supply leads to fare surges during peak demand, eroding consumer trust and hindering market growth. Absent adaptable licensing frameworks, the ASEAN taxi sector falters in addressing escalating urban mobility demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Transformation Accelerates

Online channels captured 62.11% of the ASEAN taxi market share in 2025 and are growing at a CAGR of 7.72% through 2031, reflecting widespread smartphone adoption in core ASEAN cities. User propensity for real-time tracking and cashless settlement continues to pull demand from offline call centers and street-hail services, which still cater to tourists unfamiliar with local apps. Offline bookings hold a 37.89% share yet shrink annually as 4G networks extend to secondary towns.

The ASEAN taxi market benefits from traditional fleets launching proprietary apps in Thailand and Malaysia, a shift that blurs the distinction between online and offline categories. Hybrid models allow meter-based pricing while offering digital convenience, which sustains ridership among older demographics who favor regulated fares. Offline’s continued relevance at airports and hotels signals that high-touch service can coexist with digital convenience.

By Service Type: Platform Integration Reshapes Operations

Platform-integrated metered taxis delivered 43.55% of the ASEAN taxi market share in 2025. The ASEAN taxi market share associated with this hybrid model leverages regulated meters to preserve fare transparency while using apps for dispatch, resulting in higher trip density. Traditional operators that remain offline face declining occupancy rates as consumers rank real-time location sharing and digital wallets as must-have features.

Shared shuttle services post the fastest 7.63% CAGR to 2031, propelled by corporate cost-control mandates and sustainability targets. B2B clients prefer fixed-route pickups that yield consistent occupancy and lower emissions per passenger. The segment’s growth marginally tempers demand for solo rides during peak office hours, yet overall market value still climbs as enterprises shift from owned fleets to subscription mobility.

By Vehicle Body Style: SUVs Drive Premium Growth

Sedans continued to dominate with 42.76% of the ASEAN taxi market share in 2025 because established taxi pools across Singapore and Kuala Lumpur favor their fuel economy and moderate maintenance costs. Platform data show sedans still clock the highest daily trip count. Yet SUVs and MPVs outpace all other body styles with an 8.48% CAGR through 2031, reflecting rising family and group travel, and the mobility needs of business delegations carrying bulkier luggage.

Hatchbacks remain prevalent in price-sensitive clusters such as Cebu and Ho Chi Minh City, where narrow streets and cost constraints favor compact frames. Operators increasingly weigh total cost of ownership against revenue potential when selecting vehicle body style, a calculus that shapes future fleet mix within the ASEAN taxi market.

By Vehicle Class Type: Premium Segment Accelerates

Economy cars comprised 70.84% of the ASEAN taxi market share in 2025. This class ties directly to everyday commuting among middle-income riders who view taxis as an affordable adjunct to buses and rail. Platforms optimize route pools to sustain low fares that anchor this base of the ASEAN taxi market.

Premium and executive vehicles clock an 8.29% CAGR through 2031 as companies reopen travel budgets and tourists seek higher comfort. Leather seating, in-car Wi-Fi, and professional attire justify tariffs that sit 30-50% above economy rides. Luxury and business class niches remain small yet highly profitable, capturing events and VIP transfers at airports and hotels.

By End-User: Corporate Leadership with Airport Acceleration

Corporate clients controlled 47.02% of the ASEAN taxi market share in 2025 because centralized billing and analytics simplify expense management. The ASEAN taxi market size for enterprise mobility could approach USD 17.47 billion by 2031, driven by subscription models that replace gray car fleets. Hybrid work schedules raise variability in daily trip counts, favoring on-demand services over leased vehicles.

Airport rides are on the fastest trajectory, with an 8.16% CAGR to 2031, benefiting from tourism rebounds and the resumption of international events. Premium pricing, regulatory exclusivity, and captive demand elevate profitability. Tourist and individual segments sustain base volume but show lower ticket sizes, especially where mass transit extensions now serve downtown airport corridors.

Geography Analysis

Indonesia led the ASEAN taxi market with a 37.10% share in 2025, based on its residents and rapid uptake of digital payments, which now support nearly every ride-hailing transaction. Urbanization concentrates demand in Jakarta, Surabaya, and Medan, while commission caps at 20% protect driver margins and sustain fleet supply. The ASEAN taxi market size attributable to Indonesia could scale further as electrification subsidies and data-driven congestion pricing improve fleet economics.

Vietnam is the growth pacesetter with an 8.22% CAGR through 2031. Rising disposable income, government EV incentives, and Ho Chi Minh City’s metro rollout enhance multimodal integration. Xanh SM’s plan to electrify half its fleet by 2027 exemplifies the national ambition to lead green mobility.

Varied regulatory and infrastructure dynamics shape ASEAN taxi markets. Bangkok’s dedicated BTS taxi lanes have improved wait times, boosting spillover demand for metered cabs. In contrast, Singapore’s shrinking fleet is tightening supply but enabling premium pricing and trials of autonomous vehicles, keeping the city at the forefront of innovation. The Philippines is expanding capacity with new TNVS slots, signaling policy support for growth, while Malaysia continues to face delays in license processing, limiting expansion in secondary cities. Together, these trends reflect a region balancing innovation, demand, and regulatory constraints.

Competitive Landscape

The ASEAN taxi market is moderately concentrated; Grab and GoTo have established regional dominance. Both firms bundle food delivery, payments, and micro-insurance to deepen user retention. Autonomous pilots with partners like Pony.ai position incumbents for future cost reductions via driverless fleets. Electric vehicle rollouts are also accelerating as firms tap state subsidies, which reduce operating costs and align with corporate ESG mandates.

Traditional operators respond through digital pivots. ComfortDelGro migrated its Singapore fleet to an in-house app and plans full electrification by 2040, showcasing how incumbents leverage regulatory familiarity to remain competitive. Regional mid-tier players like Mai Linh in Vietnam invest in EV partnerships with VinFast that lower battery leasing costs and shorten charging downtimes.

Challengers exploit pricing gaps; inDrive waives commissions to recruit drivers in the Philippines and Indonesia, though sustainability remains uncertain without ancillary revenue streams. Corporate subscription services and multimodal passes tied to mass-transit operators offer additional white-space opportunities as enterprises and commuters seek integrated solutions within the ASEAN taxi market.

ASEAN Taxi Industry Leaders

Grab Holdings Inc.

Gojek (GoTo Group)

ComfortDelGro Taxi

Blue Bird Group

Mai Linh Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Pony AI Inc., a leading name in autonomous driving technology, debuted in Singapore. In collaboration with ComfortDelGro, Singapore's largest transportation service provider, Pony AI aims to roll out autonomous vehicles to streamline daily commutes for residents.

- July 2025: In a significant move for Singapore's taxi scene, Grab launched its inaugural fleet of GrabCabs. These modern, eco-friendly vehicles aim to boost ride availability, reduce environmental impact, and elevate the commuting experience throughout the island. This initiative underscores Grab's commitment to sustainable transportation and innovation in the mobility sector.

- December 2024: PT Xanh SM Green And Smart Mobility rolled out its electric taxi service, Xanh SM, in Indonesia. The launch marks a significant milestone as Vietnam's pioneering all-electric taxi firm expands its operations internationally. Xanh SM aims to address Indonesia's growing travel demand by offering sustainable and efficient transportation solutions.

ASEAN Taxi Market Report Scope

The taxi market refers to the industry and business sector providing transportation services to passengers in hired vehicles, commonly known as taxis or cabs. Taxis are a form of public transportation where individuals or groups can hire a vehicle, typically owned and operated by a taxi company or an independent driver, to transport them to a specific destination.

The ASEAN taxi market is segmented by booking type, vehicle type, service type, and country. By booking type, the market is segmented into online and offline booking. By vehicle type, the market is segmented into motorcycles, cars, and other vehicle types, van. By service type, the market is segmented into ride-hailing and ride-sharing. By countries, the market is segmented into the Philippines, Malaysia, Thailand, Singapore, and the rest of ASEAN.

For each segment, the market sizing and forecast have been done based on value (USD).

By Booking Type

| Online |

| Offline |

By Service Type

| Traditional Metered Taxi |

| Platform-Integrated Metered Taxi |

| Shared/Shuttle (Corporate/B2B) |

By Vehicle Body Style

| Sedan |

| Hatchback |

| SUVs & MPVs |

By Vehicle Class Type

| Economy |

| Premium/Executive |

| Luxury/Business |

By End-User

| Corporate |

| Tourist |

| Airport |

| Others (Individual etc.) |

By Country

| Singapore |

| Indonesia |

| Malaysia |

| Thailand |

| Philippines |

| Vietnam |

| Rest of ASEAN |

| By Booking Type | Online |

| Offline | |

| By Service Type | Traditional Metered Taxi |

| Platform-Integrated Metered Taxi | |

| Shared/Shuttle (Corporate/B2B) | |

| By Vehicle Body Style | Sedan |

| Hatchback | |

| SUVs & MPVs | |

| By Vehicle Class Type | Economy |

| Premium/Executive | |

| Luxury/Business | |

| By End-User | Corporate |

| Tourist | |

| Airport | |

| Others (Individual etc.) | |

| By Country | Singapore |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Philippines | |

| Vietnam | |

| Rest of ASEAN |

Key Questions Answered in the Report

How large will ASEAN taxi revenues be by 2031?

The ASEAN taxi market is projected to reach USD 37.15 billion by 2031, reflecting a 7.26% CAGR from 2026-2031.

Which country is expanding fastest?

Vietnam shows the strongest trajectory with an expected 8.22% CAGR through 2031, boosted by EV incentives and rising disposable income.

What booking model leads today?

Online app-based booking holds a 62.11% revenue share due to 80%+ smartphone penetration in major cities.

Are electric taxis economically viable?

Government subsidies cut purchase costs, while operators report operational savings of about 60% compared with gasoline cars, improving total cost of ownership for EV taxis.

Why are SUVs gaining popularity in fleets?

Higher seating, extra luggage space, and perceived safety help SUVs and MPVs grow at an 8.48% CAGR, outpacing sedans.

Page last updated on: