New Energy Vehicle Taxi Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

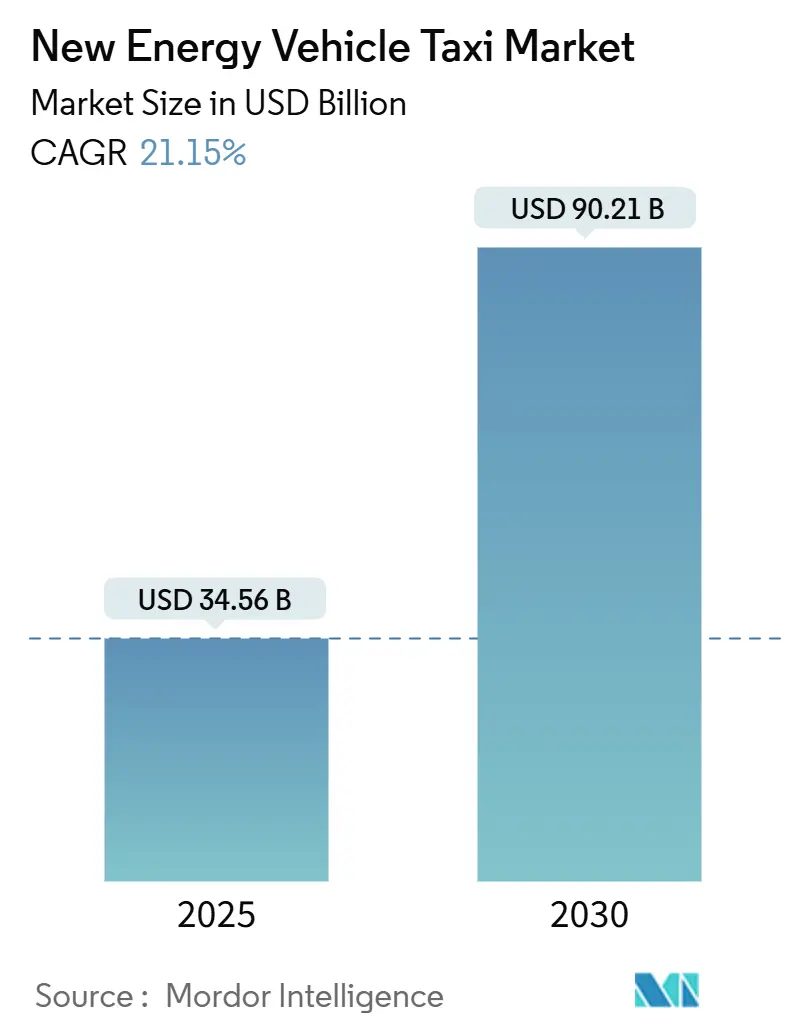

| Market Size (2025) | USD 34.56 Billion |

| Market Size (2030) | USD 90.21 Billion |

| Growth Rate (2025 - 2030) | 21.15% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Energy Vehicle Taxi Market Analysis by Mordor Intelligence

The New Energy Vehicle Taxi Market size is estimated at USD 34.56 billion in 2025, and is expected to reach USD 90.21 billion by 2030, at a CAGR of 21.15% during the forecast period (2025-2030). The projected growth underscores a rapid scale-up phase that is reshaping urban fleet economics and charging infrastructure planning. City-level zero-emission mandates, falling battery prices, and the growing prevalence of digital ride-hailing platforms are the primary engines of this growth. Wide gaps remain in charging coverage outside first-tier cities. Yet, policy roadmaps in Asia-Pacific, Europe, and North America continue to tighten internal-combustion restrictions, effectively locking in demand for electric and hydrogen alternatives. Total cost of ownership for high-mileage taxis has already crossed parity with gasoline equivalents in several major markets, leading operators to front-load electrification investments rather than wait for further incentives. At the same time, mass-market battery electric multipurpose vehicles and an expanding catalogue of fuel-cell models now address range, refuelling, and seating constraints that once deterred fleet managers. Finally, autonomous pilots signal a second-order transition in which ride-hailing platforms consolidate vehicle ownership and further amplify adoption economics by removing labour costs.

Key Report Takeaways

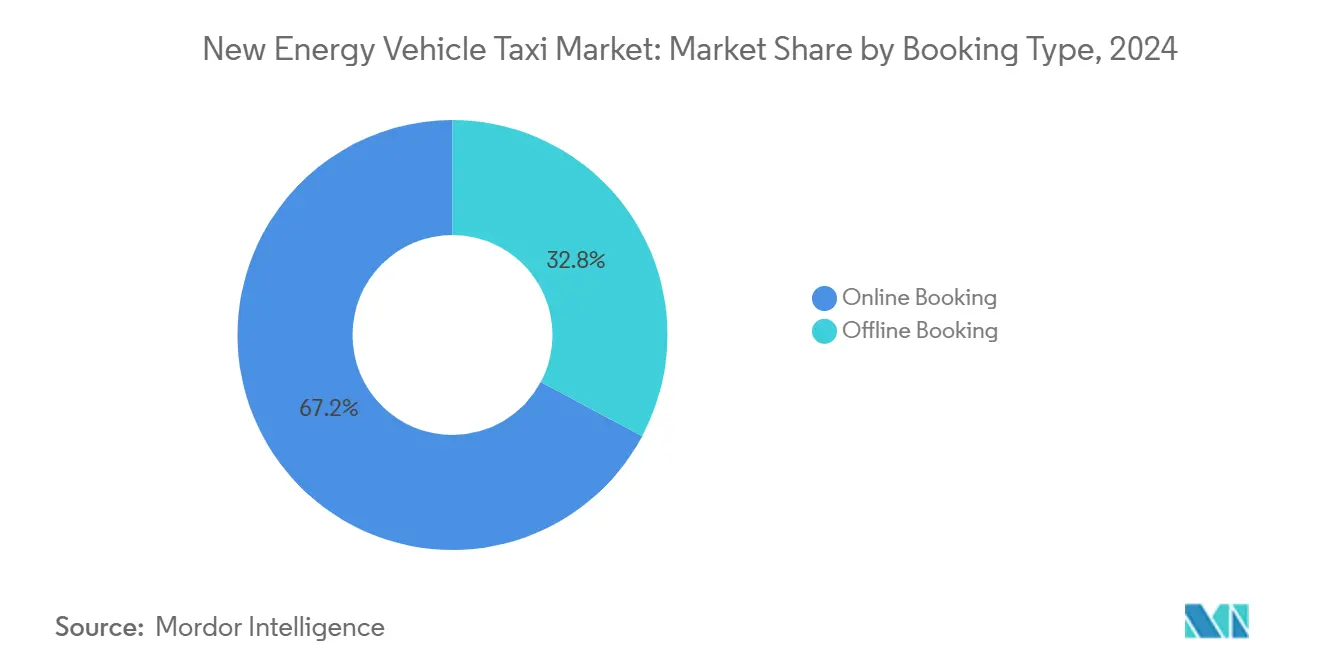

- By booking type, online platforms held 67.18% of the new energy vehicle taxi market share in 2024 and are expanding at a 21.17% CAGR as cashless payments and dynamic dispatch tools boost fleet utilisation.

- By service type, ride-hailing accounted for 73.26% of the new energy vehicle taxi market share in 2024; it is also the fastest-growing service subsegment, with a 21.19% CAGR, due to scale efficiencies in centralised charging and vehicle procurement.

- By propulsion, battery electric models captured 54.57% of the new energy vehicle taxi market share in 2024. In contrast, fuel-cell taxis are advancing at a 21.28% CAGR and are on track to close the gap in range-sensitive duty cycles.

- By vehicle type, hatchbacks led with 48.12% of the new energy vehicle taxi market share in 2024. In contrast, multipurpose vehicles are the fastest climbers at 21.23% CAGR, propelled by demand for high-seating-capacity, swap-ready models.

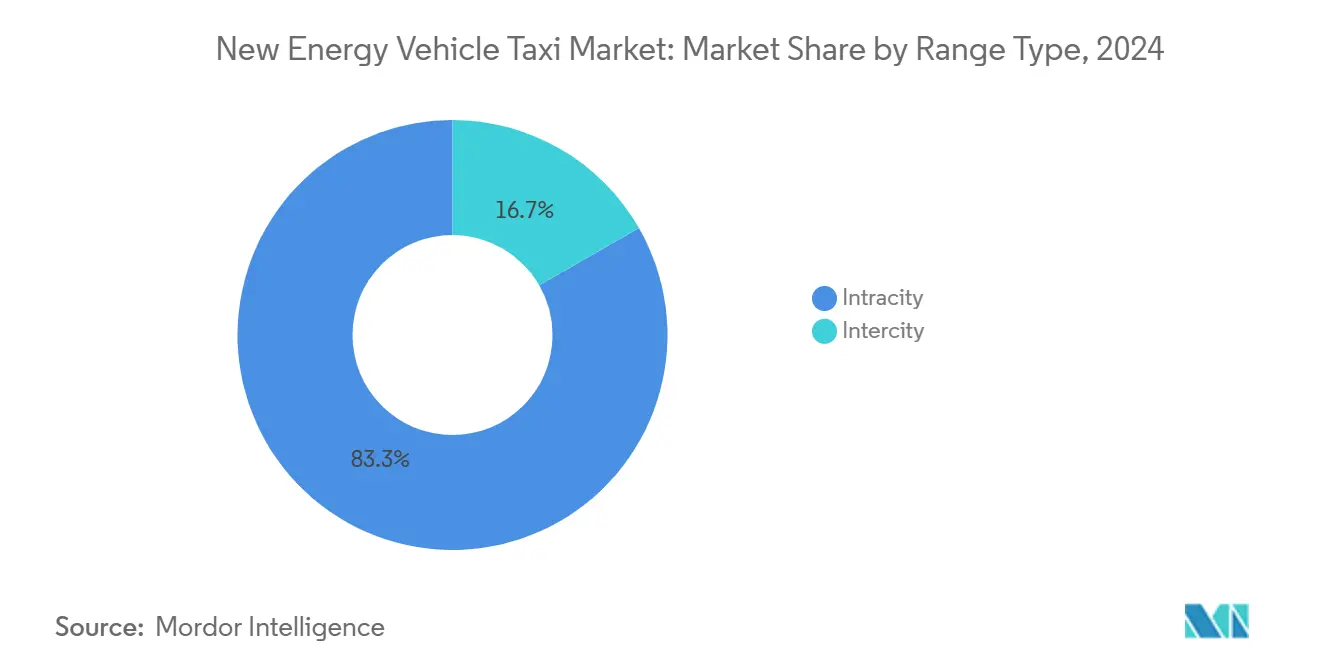

- By range type, Intracity services captured 83.28% of the new energy vehicle taxi market share in 2024, while intercity routes are forecast to expand at a 21.27% CAGR through 2030.

- By ownership, company-controlled fleets commanded 65.47% of the new energy vehicle taxi market share in 2024; this cohort is forecast to expand at a 21.24% CAGR as platform operators secure bulk vehicle orders and negotiate preferential charging tariffs.

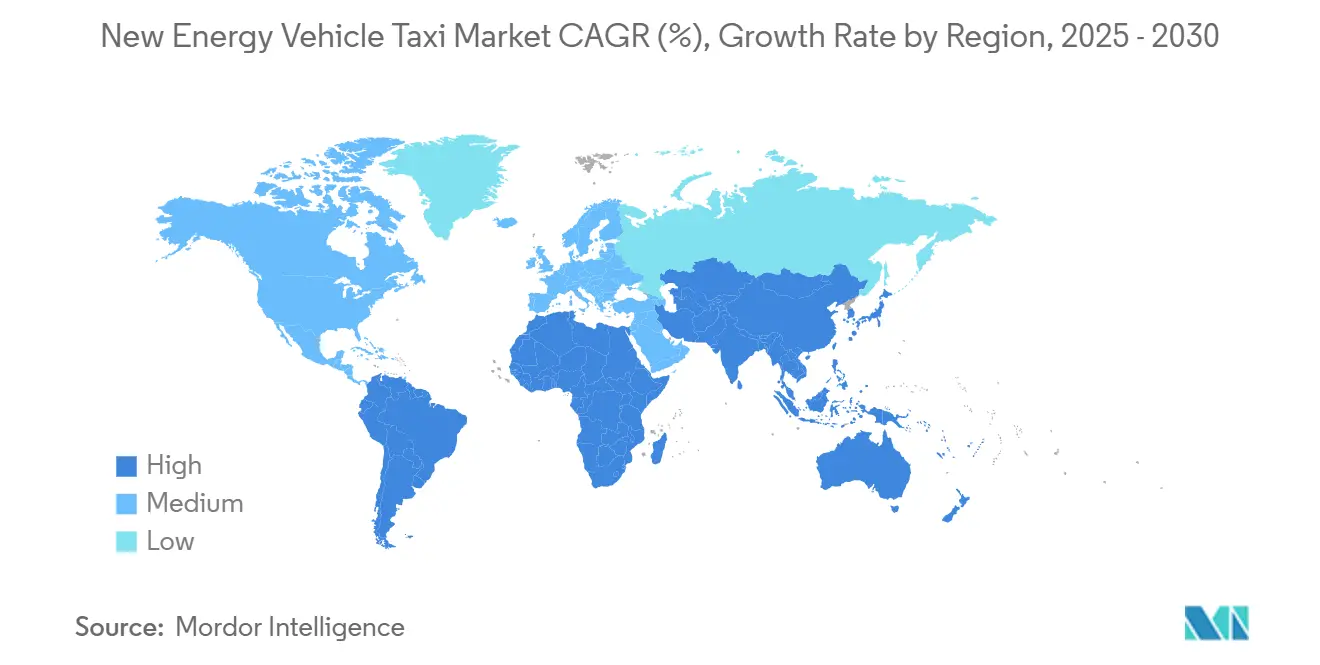

- By geography, Asia-Pacific dominated with 42.27% of the new energy vehicle taxi market share in 2024, while South America is projected to post the fastest CAGR of 21.31% through 2030.

Global New Energy Vehicle Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Decline Of Battery | +4.1% | Global, accelerated in China manufacturing hubs | Short term (≤ 2 years) |

| Urban Clean-Air Zones Banning ICE Taxis | +3.5% | European cities, expanding to Asia Pacific megacities | Medium term (2-4 years) |

| Subsidy Extension and Zero-Emission Fleet Mandates | +3.2% | Global, with early gains in EU, China, California | Medium term (2-4 years) |

| Global Ride-Hailing Penetration | +2.8% | Asia Pacific core, spill-over to Latin America, MEA | Long term (≥ 4 years) |

| Robotaxi Pilots Cutting Driver Capex | +2.3% | North America and select EU cities, China trials | Long term (≥ 4 years) |

| Battery-Swap-Ready MPVs | +1.9% | China core, pilot expansion to Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline of Battery USD/kWh Improving TCO

Average lithium-ion pack prices fell slightly in 2023 and are projected to drop to USD 58-86 per kWh by 2030, which reduces the acquisition premium and compresses payback periods to less than three years for many city fleets [1]“Global EV Outlook 2025,” International Energy Agency, iea.org . High-mileage taxis accrue annual operating savings of USD 1,600-1,800 in the United States, a delta large enough to offset financing hurdles. LFP chemistry crossed two-fifths of global battery capacity in 2023, and it now underpins the bulk of entry-tier models produced by leading Chinese OEMs, delivering lower upfront costs despite lower energy density. Even if European countervailing duties of up to one-third briefly lift landed prices, operators still lock in lower lifetime operating costs relative to gasoline and diesel.

Urban Clean-Air Zones Banning ICE Taxis

Local air-quality rules now function as hard stop dates for gasoline and diesel taxi licenses. London’s Ultra Low Emission Zone and Rome’s municipal ordinance approving hydrogen cabs eliminate the compliance ambiguity that previously slowed electrification decisions. Asian hubs replicate the pattern: Seoul’s metropolitan government introduced a graduated fee waiver for zero-emission taxi medallions in 2025. Beijing is finalising a ban on new ICE taxi registrations starting in 2027. Clear deadlines shield fleet operators from technology-risk debates because the regulatory pathway signals that resale values for ICE vehicles will continue to collapse [2]“Ultra Low Emission Zone Expansion,” London City Hall, london.gov.uk .

Subsidy Extension & Zero-Emission Fleet Mandates

Global governments keep purchase and operating incentives in place even as volume scales, locking in a positive investment horizon for fleet operators. China doubled vehicle-replacement subsidies in July 2024, while Argentina scrapped import tariffs on low-cost electric and hybrid taxis in January 2025, making entry-level models cost-competitive overnight. Hong Kong’s grant program for 3,000 e-taxis now combines purchase vouchers with a full first-registration-tax waiver, accelerating fleet turnover schedules. Across the European Union, low-emission zones have broadened to cover most major capitals, turning optional electrification into a legal prerequisite for taxi licensing. The bloc’s Alternative Fuels Infrastructure Regulation also mandates minimum charger density per kilometre of road, ensuring that charging access rises parallel with vehicle demand [3]“Alternative Fuels Infrastructure Regulation,” European Parliament, Europa. eu.

Global Ride-Hailing Penetration & Digital Payments

Online booking drives around two-thirds of total bookings and continues to expand at a robust CAGR, creating a vast data backbone that feeds predictive maintenance and smart-charging algorithms. Cashless payments shorten turnaround times and cut leakage, pushing utilisation levels higher than legacy street-hail services. Uber’s framework agreement with BYD to supply a lakh electric taxis illustrates how platform scale converts digital demand signals into discounted bulk orders, further shrinking costs per mile. In parallel, new payment rails in emerging markets such as Argentina’s QR-code mandates standardise electronic settlements and lift user confidence in app-based transport.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Fast-Charging | -2.1% | Global, pronounced in developing markets | Medium term (2-4 years) |

| High Upfront Vehicle Cost | -1.8% | Price-sensitive markets, emerging economies | Short term (≤ 2 years) |

| Patchy Ride-Hailing Regulations | -1.3% | Latin America, Southeast Asia, India | Long term (≥ 4 years) |

| Li-Ion Residual-Value Risk | -0.9% | Global, acute in secondary markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse Fast-Charging in Tier-2/3 Cities

Public charger density remains skewed toward first-tier metros. Hong Kong has numerous public points across all districts. At the same time, smaller urban nodes in Latin America run pilot stations at single-digit counts, forcing taxis to queue or deadhead for power. Gravity Mobility’s rollout of 500 kW curbside chargers in New York City highlights blistering recharge speeds. However, replication beyond flagship sites is slow because grid upgrades and real-estate costs inflate capex. Rural and suburban operators default to overnight depot charging, requiring land, three-phase power, and capital that many small firms lack.

High Upfront Vehicle Cost vs ICE Taxis

Even as pack prices fall, sticker premiums linger in markets without local production or tax holidays. The IEA calculates that electric taxis remain almost one-fourth more expensive than ICE in Europe and the U.S., while over three-fifths of Chinese EVs already undercut gasoline peers on price. OEMs use finance incentives. LEVC’s GBP 1,500 deposit contribution is one case to neutralise the delta, yet such programs tend to be time-bound. Removal of China’s national purchase-tax exemption in 2024 forces provinces to fill the gap, adding policy uncertainty for smaller cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Platforms Cement Leadership

Online reservations accounted for 67.18% of the new energy vehicle taxi market share in 2024, advancing at a 21.17% CAGR. This channel lifts utilisation through algorithmic dispatch and slashes idle time, a critical lever in squeezing more passenger miles out of expensive electric assets. Offline street-hails still serve older demographics and areas with patchy cell coverage, but their one-third share is plateauing as regulators legalise apps and smartphone penetration spreads. Across both channels, operator data indicate that digital fleets record slightly lower empty-mile ratios than analogue peers. This gap feeds directly into lower per-trip energy costs and faster capital payback.

The online wedge underpins platform-OEM mega-deals such as Uber’s 100,000-unit order with BYD. Bulk procurement carves as much as minimum off factory gate pricing and often bundles tenure-based battery warranty extensions, further de-risking operator finances. Because digital booking captures trip metadata, fleets can schedule high-demand windows and cue vehicles into swap or charge slots during trough periods, smoothing grid loads and unlocking participation in demand-response markets where regulations allow aggregated assets to bid into power exchanges.

By Service Type: Ride-Hailing Expands Share

Ride-hailing claimed 73.26% of the new energy vehicle taxi market share in 2024 and will maintain a 21.19% CAGR as corporate travel, airport transfers, and daily commutes all migrate to app-based service. Fixed-fare taxi cooperatives continue to operate in regulated markets, yet dynamic pricing, advance ETA visibility, and digital payments funnel users to ride-hail apps. Pooled ride algorithms lift seat occupancy to 1.4–1.6 passengers per trip in mature markets, dampening revenue-per-mile but stretching fleet capacity without parallel vehicle growth.

Corporate procurement teams lock long-term ride-hail contracts to meet Scope 3 emission targets. HysetCo’s hydrogen taxi fleet in Paris, which fields 500 dedicated FCEVs, posted triple-digit annual growth by tapping professional users who value guaranteed zero-emission credentials. Autonomous functionality promises a second jump in segment economics: removing human drivers could lower operating costs by two-fifths, allowing platforms to drop fares or expand margins while keeping vehicles rolling during overnight demand spikes.

By Propulsion Type: BEV Leads While FCEV Accelerates

Battery electric units captured 54.57% of the new energy vehicle taxi market share in 2024, underwritten by maturing fast-charge networks and the rise of low-cost LFP cells. The segment still grows on par with the new energy vehicle taxi market, yet fuel-cell cabs are the relative outperformer with a 21.28% CAGR. Hydrogen’s 3-5 minute refill and robust cold-weather performance have proved compelling for high-latitude cities such as Berlin and Oslo and desert climates like Dubai, where ambient-temperature charging imposes thermal derating on batteries.

Paris hosts 250 FCEV taxis under the H2 Moves Europe program, accumulating nearly five lakh passenger journeys since launch. Tallinn joined the list in September 2025 when Bolt fielded its first Mirai-based fleet, underscoring the technology’s eastward expansion beyond the core EU. Meanwhile, BEVs innovate on downtime via swap-compatible packs and 800 V ultra-fast architecture. The competition between refuel-based and recharge-based models will likely settle into operational niches dictated by route length, climate, and charger economics.

By Vehicle Type: Hatchbacks Maintain Scale, MPVs Gain Speed

Cost-efficient hatchbacks earned 48.12% of the new energy vehicle taxi market share in 2024, offering a manoeuvrable footprint suited to dense city grids and short-haul trips. Multipurpose vehicles, though, are sprinting ahead with a 21.23% CAGR as ride-sharing and accessibility mandates boost demand for spacious cabins. BYD’s e6 and Geely’s L380 seat up to seven passengers and ship with optional wheelchair ramps, making them attractive for regulated airport lanes and paratransit contracts.

Hatchbacks still dominate value-conscious fleets because they need less kWh per mile and carry smaller, cheaper batteries. Yet as swap networks proliferate, larger MPVs sidestep the charging-time handicap that once favoured compact cars. Several jurisdictions now require a fixed fraction of wheelchair-accessible vehicles per fleet license, tilting new orders toward high-roof MPVs. Premium SUV taxis cater to business-class and tourist segments, but their market share remains single-digit due to higher list prices and elevated energy demand.

By Range Type: Intracity Reigns, Intercity Picking Up

Short-range intracity circuits produced 83.28% of the new energy vehicle taxi market share in 2024, reflecting taxi density in mega-cities where average trip distance sits below 15 km. Intercity services, however, are closing the gap at 21.27% CAGR as express-charger corridors blanket major highways. EU law now obliges member states to install 150 kW stations every 60 km on core networks, reducing range anxiety for cross-regional operators. In China, electricity spot-market reforms allow fleets to schedule charging when prices dip at night, enhancing margins on long-haul airport runs that start before dawn.

Fuel-cell taxis have carved an early foothold in long-distance use because their refuelling pattern mirrors gasoline norms, making driver adoption frictionless. Battery models still dominate commuter corridors where depot charging suffices, but rising 700-V architectures and 100-kWh packs are lengthening real-world range. Route-planning software plugs state-of-charge data into traffic forecasts to pre-book charger slots, mitigating dwell risk on long routes.

By Ownership Type: Company-Controlled Fleets Command Capital

Company-owned vehicles represented 65.47% of the new energy vehicle taxi market share in 2024 and will advance at a 21.24% CAGR as platform operators internalise fleet control to guarantee service uptime and charger discipline. Central ownership consolidates bargaining power when negotiating electricity tariffs, parking concessions, and financing structures. Individual owner-operators still generate a third of fleet count, mainly in legacy medallion systems and regions where driver cooperatives hold political sway.

Uber’s multi-regional BYD deal layers in leasing packages and battery health guarantees, reducing capex fears for drivers who migrate onto corporate vehicle pools. In Paris, HysetCo rents hydrogen taxis to professional drivers who pay a daily fee covering the vehicle, insurance, and refuelling, thus derisking residual-value exposure. Data-driven predictive maintenance inside company fleets cuts downtime by one-third compared with individually owned cabs, giving the model a structural cost edge as vehicles electrify.

Geography Analysis

Asia-Pacific contributed 42.27% of the new energy vehicle taxi market share in 2024, reflecting China’s robust subsidy matrix, India’s FAME incentives, and Japan’s aggressive hydrogen infrastructure rollout. Chinese provincial schemes now fill the gap left by the 2024 sunset of national purchase-tax exemptions, but replacement subsidies and local-government fleet-transition grants sustain momentum. India’s Production Linked Incentive program backstops local cell and vehicle output, trimming upstream costs for fleet buyers. South Korea’s fuel-cell roadmap and Japan’s Tokyo-centric refuelling expansion underpin a fertile landscape for hydrogen taxis, particularly inter-airport shuttles.

South America is the fastest grower at 21.31% CAGR off a smaller baseline. Argentina cut tariffs on imported low-cost EVs in January 2025 and issued new auto-assembly credits to entice OEM localisation. Brazil’s ride-hailing boom and São Paulo’s city ordinance favouring zero-emission taxi permits have triggered bilateral supply agreements with Chinese manufacturers. Chile leverages abundant solar and hydro generation to tout a nearly zero-carbon charging mix, an attractive marketing hook for fleets wooing ESG-focused passengers.

Europe remains a mature yet sizable arena as low-emission zones transition from carrot to stick. Countervailing duties of up to one-third lift Chinese BEV prices, but fleet operators partially offset the impact through EU charging grants and reduced congestion fees. H2 Moves Europe’s 300-vehicle deployment across Paris, Brussels, and Berlin validates fuel-cell taxi economics when green hydrogen is priced under parity with diesel.

North America’s evolution is shaped by California’s zero-emission ride-hail mandate and new federal tax credits for commercial EV purchases. Canada follows with its own ZEV standards, though colder temperatures motivate extra focus on heat-pump integrations and battery conditioning. The Middle East, led by Dubai’s Mirai pilot, illustrates hydrogen’s viability in high-temperature settings, but grid upgrades remain an adoption bottleneck in parts of Africa.

Competitive Landscape

Competition is diffuse and alliance-driven rather than head-to-head. Ride-hailing platforms such as Uber, Didi, Bolt, and Grab orchestrate demand while leaning on OEMs for supply. BYD dominates the battery electric offering due to vertically integrated cell-to-pack systems and competitive pricing. BAIC, SAIC, and new entrants from China are accelerating exports but face tariff headwinds in the EU and safety-rating constraints in North America.

Western automakers focus on premium segments and autonomous pilots, illustrated by Volkswagen’s ID. Buzz rollout with Uber and General Motors’ Cruise subsidiary eyeing commercial driverless deployment.

HysetCo’s capital raise embodies the trend toward end-to-end hydrogen ecosystems: the company builds refuelling stations, leases taxis, and sells carbon credits in a looped business model. Battery-swap providers such as NIO and Ample carve a niche by bundling vehicles with energy-as-a-service, turning capex into opex. Waymo, Mobileye, and Tesla compete in autonomy software; their success could tip bargaining power toward technology stack owners that can dictate hardware specs and platform integrations. Emerging disruptors focus on specialised needs, including wheelchair-accessible MPVs, high-capacity battery vans, and intercity swap stations.

New Energy Vehicle Taxi Industry Leaders

Didi Chuxing

Uber Technologies

Grab Holdings Ltd.

ANI Technologies (Ola)

Lyft Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Bolt launched its first hydrogen-powered ride-hailing fleet in Tallinn, Estonia, bringing fuel-cell taxis to the Baltic region for the first time.

- April 2025: Volkswagen and Uber unveiled a decade-long partnership to deploy thousands of autonomous, all-electric ID. Buzz vans across multiple U.S. cities, with Los Angeles set for commercial launch in 2026.

- March 2025: Tesla applied to the California Public Utilities Commission to operate passenger services using entirely self-driving electric cars without steering wheels and pedals.

Global New Energy Vehicle Taxi Market Report Scope

| Online Booking |

| Offline Booking |

| Ride-hailing |

| Ride-sharing (pooled) |

| Corporate & Institutional Contracts |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Hatchback |

| SUV |

| MPV |

| Intracity |

| Intercity |

| Company-Owned |

| Individually-Owned |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Booking Type | Online Booking | |

| Offline Booking | ||

| By Service Type | Ride-hailing | |

| Ride-sharing (pooled) | ||

| Corporate & Institutional Contracts | ||

| By Propulsion Type | Battery Electric Vehicle (BEV) | |

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Vehicle Type | Hatchback | |

| SUV | ||

| MPV | ||

| By Range Type | Intracity | |

| Intercity | ||

| By Ownership Type | Company-Owned | |

| Individually-Owned | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the new energy vehicle taxi market by 2030?

The market is forecast to reach USD 90.21 billion by 2030, expanding from USD 34.56 billion in 2025.

Which propulsion type is advancing fastest within electric taxi fleets?

Fuel-cell taxis are growing at a 21.28% CAGR, outpacing battery models, especially on range-sensitive routes.

Why are online booking channels critical for electric taxi economics?

Digital platforms raise utilization through algorithmic dispatch and enable bulk vehicle procurement, cutting per-mile costs.

How do battery-swap stations improve fleet productivity?

Swap systems cut energy stops to under five minutes, allowing high-duty taxis to log more revenue miles per shift.

Which region shows the highest growth momentum?

South America posts the fastest CAGR at 21.31% through 2030, thanks to tariff cuts and ride-hail expansion.

What role do autonomous pilots play in future taxi economics?

Driverless systems promise a 30-40% cost reduction by removing labor expenses, further amplifying the savings of electrification.

Page last updated on: