Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

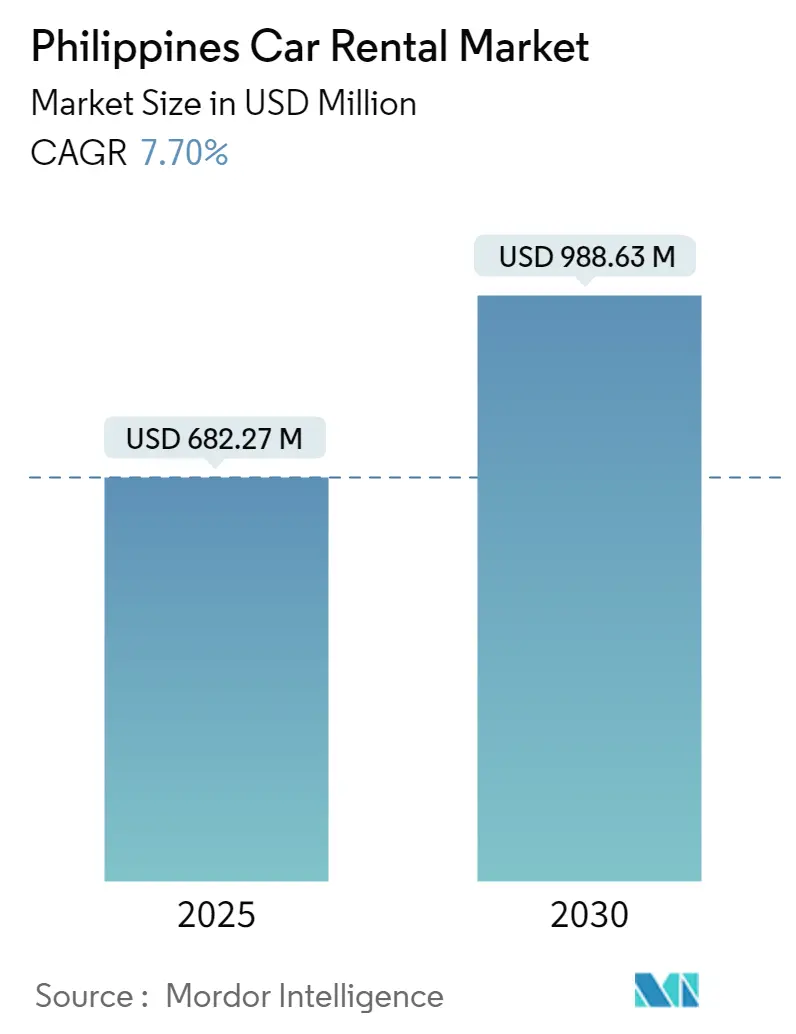

| Market Size (2025) | USD 682.27 Million |

| Market Size (2030) | USD 988.63 Million |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Car Rental Market Analysis by Mordor Intelligence

The Philippines car rental market stands at USD 682.27 million in 2025 and is projected to reach USD 988.63 million by 2030, reflecting a 7.70% CAGR through the forecast period (2025-2030). A surge in international arrivals fuels demand for leisure-oriented rentals as tourists extend stays and explore multiple destinations. Large-scale infrastructure spending, such as the USD 2.98 billion rehabilitation of Ninoy Aquino International Airport (NAIA), gives operators a bigger passenger base to serve and encourages fleet expansion[1]“NAIA Rehabilitation Deal Signed,”, Philippine News Agency, pna.gov.ph. Momentum also stems from the expanding digital economy, where online travel bookings witnessed significant growth in 2024, pushing operators to optimize app-based distribution and real-time pricing. Finally, corporate mobility programs tied to the country’s business-process-outsourcing (BPO) sector sustain weekday vehicle utilization. At the same time, Republic Act 11687 sets the stage for the gradual electrification of rental fleets through tax incentives and purchase mandates[2]“Republic Act 11687 and EV Mandates,”, Clean Air Asia, cleanairasia.org.

Key Report Takeaways

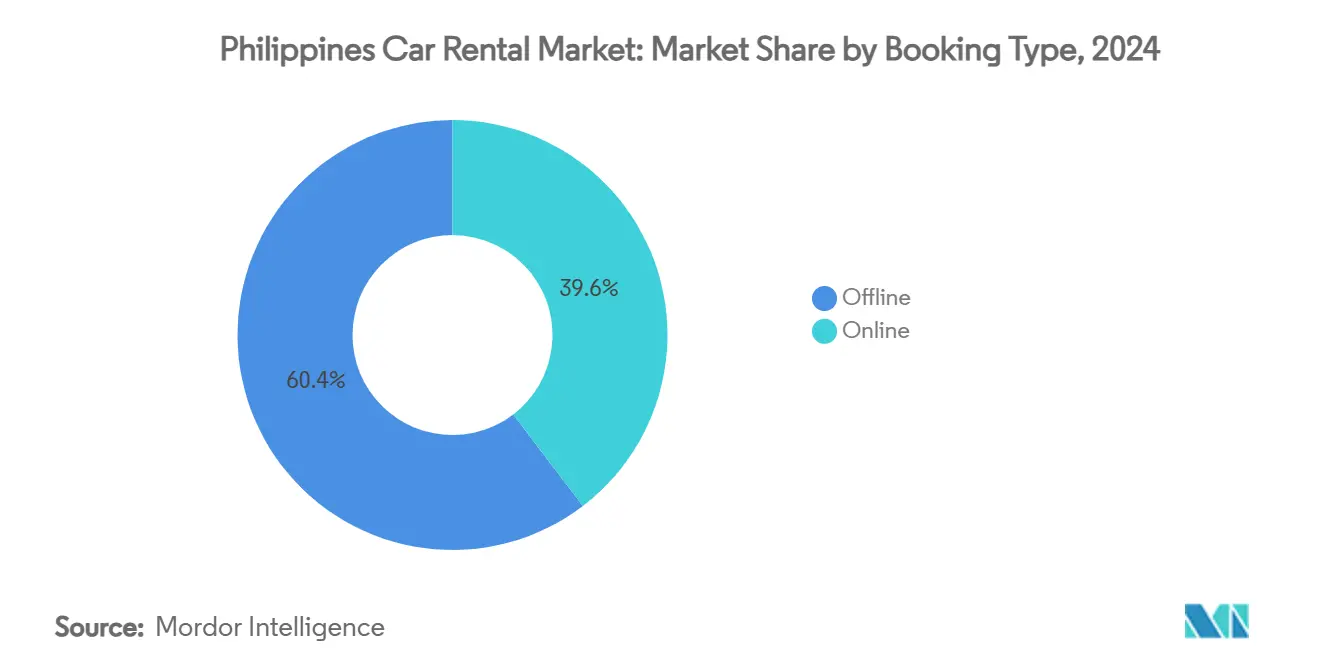

- By booking channel, offline reservations held 60.37% of the Philippines car rental market share in 2024, whereas online bookings are forecast to advance at 9.75% CAGR through 2030.

- By rental duration, short-term contracts captured 65.21% of the Philippines car rental market revenue share in 2024; long-term rentals are projected to rise at 9.87% CAGR to 2030.

- By vehicle type, sedans led the Philippines car rental market with 37.34% of the share in 2024, while sport-utility vehicles are poised for the fastest 10.84% CAGR.

- By application, tourism accounted for 73.27% of the Philippines' car rental market size in 2024 and is expanding at an 11.35% CAGR.

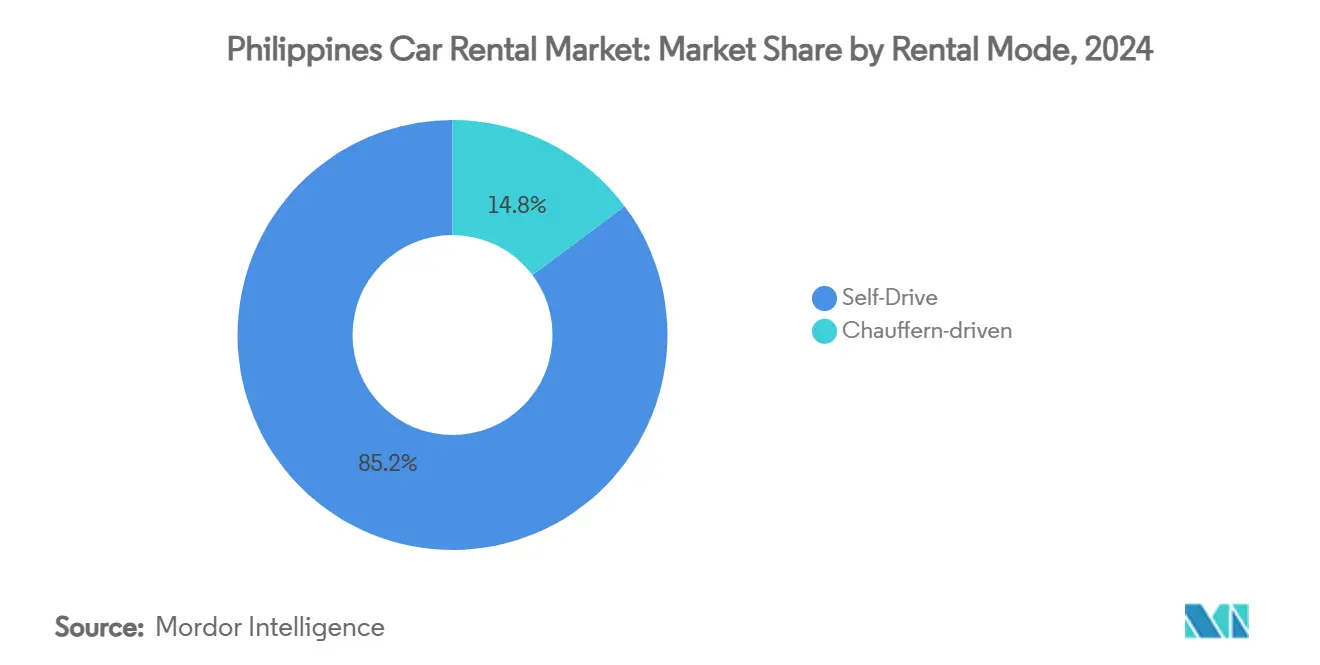

- By rental mode, self-drive solutions dominated with an 85.23% of the Philippines car rental market share in 2024; chauffeur-driven services exhibit a 10.25% CAGR outlook.

- By vehicle class, economy models represented 49.45% of the Philippines car rental market share in 2024, whereas premium cars are forecast to grow at a 9.34% CAGR.

- By fuel type, internal-combustion-engine (ICE) models held 86.34% of the Philippines car rental market share in 2024; electric vehicles show a 15.37% CAGR potential

Philippines Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Double-Digit Rise in International Tourist Arrivals Fueling Leisure Rentals | +2.1% | National; concentration in Metro Manila, Cebu, Boracay | Medium term (2-4 years) |

| Rapid Shift To Digital-First OTA and Super-App Bookings | +1.8% | National; led by Metro Manila and major urban centers | Short term (≤ 2 years) |

| Rising Corporate Demand From BPO Sector and Hybrid-Work Mobility | +1.2% | Metro Manila, Cebu, Davao, Clark | Medium term (2-4 years) |

| Airport Infrastructure Upgrades Unlocking Regional Demand | +1.1% | Laoag, Tacloban, Clark, Kalibo | Medium term (2-4 years) |

| Government EV-Tax Incentives Expanding “Green” Rental Fleets | +0.9% | National; early adoption in Metro Manila, Cebu | Long term (≥ 4 years) |

| Embedded-Insurance APIs Lowering Customer Friction | +0.6% | National; technology-forward operators | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Double-digit Rise in International Tourist Arrivals Fueling Leisure Rentals

The Philippines experienced a rise in international visitors in 2024, surpassing the pre-pandemic tourism receipt levels. South Korea, the United States, and China dominate source markets, creating dense point-to-point corridors that operators can target with tailored promotions. Average length of stay now exceeds 11 nights, and per-capita outlays top USD 2,000 - the highest in ASEAN, supporting uptake of premium vehicles and add-on services. Travelers increasingly choose multi-destination itineraries to emerging eco-tourism spots, elevating the need for flexible, self-driving rentals that conventional point-to-point buses cannot match. These trends underpin sustained leisure demand and buoy overall fleet utilization.

Rapid Shift to Digital-First OTA & Super-App Bookings

Super-app ecosystems, such as JoyRide’s tie-up with Toyota RentaCar, integrate bookings, payments, and loyalty, letting users secure cars for as little as 10 hours or as long as three years[3].“Toyota RentaCar Teams with JoyRide,”, Newsbytes.PH, newsbytes.ph Real-time application-programming interface (API) connectivity enables dynamic pricing, instant confirmations, and friction-free upselling, while embedded insurance shortens checkout flows. Operators that link inventory to these high-traffic platforms gain distribution scale, whereas stand-alone players risk lower visibility and thinner margins.

Rising Corporate Demand from the BPO Sector and Hybrid-Work Mobility

Hybrid work models in business-process-outsourcing drive flexible transport needs. Car rentals configured as monthly leases or pay-per-use pools complement company shuttles that run at capacity during peak hours. Integrated expense-management APIs streamline billing and compliance, prompting procurement teams to opt for right-sized contracts rather than underutilized fixed fleets. Consistent weekday demand from BPO tenants helps balance weekend tourism spikes, stabilizing revenue throughout the year.

Government EV-Tax Incentives Expanding “Green” Rental Fleets

Republic Act 11687 mandates at least 5% EV penetration in government and corporate car pools, generating institutional demand that rental firms can serve via dedicated electric sub-fleets. The Electric Vehicle Industry Development Act (EVIDA) layers import-duty waivers over value-added-tax exemptions, accelerating fleet electrification economics. BPI Tokyo Century and BYD’s launch of Atto 3 rentals through Diamond Rent-a-Car demonstrates a first-mover advantage in matching ESG-minded corporates with green mobility options. Yet, limited fast-charging density, government goals call for up to 40,000 points by 2040, keeping adoption clustered in Metro Manila for now.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Fuel Prices Compressing Operator Margins | -1.4% | National; acute impact on provincial operators | Short term (≤ 2 years) |

| Growing Ride-Hailing Substitutes in Metro Areas | -0.9% | Metro Manila, Cebu, Davao, urban centers | Medium term (2-4 years) |

| Chronic Urban Congestion Reducing Self-Drive Appeal | -0.8% | Metro Manila, Cebu, Davao urban cores | Medium term (2-4 years) |

| Slow Rollout of Charging Points Limiting EV Rental Uptake | -0.5% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Fuel Prices Compressing Operator Margins

Year-to-date pump increases of USD 0.17 for gasoline and USD 0.17 for diesel erode profitability, especially for provincial operators lacking scale to hedge or absorb costs. Retail prices straddle USD 0.89 - USD 1.30 per liter for gasoline and USD 0.86 - USD 1.22 for diesel, leaving little room for operators to pass on surcharges without dampening demand. Smaller fleets may pivot toward fuel-efficient compact cars or hybrids, but upfront capital outlays strain cash flow. Volatility complicates budgeting for monthly corporate contracts that lock in rates months ahead.

Chronic Urban Congestion Reducing Self-Drive Appeal

Metro-Manila gridlock makes driving stressful for visitors unfamiliar with local traffic. Parking scarcity and steep toll road fees further diminish the value proposition of self-driving trips within city cores. Consequently, chauffeur-driven services that bundle navigation expertise command premium uptake among tourists and executives. Nonetheless, demand rebounds for self-drive rentals in inter-city and leisure corridors where new or upgraded airports shorten travel to less congested areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Channels Accelerate Despite Offline Dominance

Offline reservations retained a 60.37% share of the Philippines car rental market in 2024, underscoring consumer comfort with face-to-face transactions for high-value bookings. Brick-and-mortar counters remain vital in airports and hotel lobbies, where agents up-sell insurance and accessories. However, the online segment is outpacing all others at 9.75% CAGR to 2030, as smartphone penetration climbs and digital wallets normalize payment habits.

Hybrid distribution models are emerging. Customers discover vehicles and secure reservations through apps, yet still visit counters for vehicle inspection, ID verification, or last-minute upgrades. For operators, digital bookings slash acquisition costs and enable dynamic yield management, while on-site interactions preserve the opportunity to cross-sell GPS units, child seats, and premium insurance. This blended approach maximizes revenue per rental and improves fleet utilization, positioning multi-channel firms to out-compete single-channel rivals as the Philippines car rental market evolves.

By Rental Duration: Short-Term Dominance Faces Long-Term Growth Challenge

Short-term contracts captured 65.21% revenue in 2024, reflecting the Philippines' car rental market’s heavy dependence on tourism, where travelers typically rent for three to seven days. Yet, long-term agreements are on track for a 9.87% CAGR through 2030 as BPO firms rely on monthly leases to meet flexible staffing needs and reduce capital tied up in owned fleets.

Long-duration rentals deliver predictable cash flow and lower acquisition costs because contract renewals often roll over automatically. Conversely, short-term bookings deliver higher daily yields but require continuous marketing spend. New “micro-lease” products bridging daily and monthly horizons - such as the 10-hour-to-3-year options offered on JoyRid allow companies to reposition idle vehicles quickly, smoothing peaks and troughs in demand.

By Vehicle Type: SUVs Challenge Sedan Leadership Through Versatility

Sedans retained 37.34% of the Philippines' car rental market share in 2024 because of their fuel efficiency and affordability for urban and inter-city use. However, SUVs are accelerating at 10.84% CAGR, attracting travelers who need higher ground clearance for island roads and adventure activities that sedans cannot handle.

SUVs command higher daily tariffs that offset greater fuel burn and maintenance. Operators also leverage SUVs to bundle experience-based packages such as surf trips to Siargao or mountain tours in Benguet, monetizing vehicles as part of curated itineraries. Sedans still dominate corporate mobility because of cost sensitivity, but the growing popularity of experiential travel tips incremental growth toward SUVs over the outlook period.

By Application Type: Tourism Supremacy Reinforced by Record Arrivals

Tourism rentals accounted for 73.27% of the Philippines' car rental market size in 2024 and carry the strongest 11.35% CAGR through 2030. Leisure travelers often book larger vehicles or SUVs when venturing outside city centers, boosting average daily revenue.

Commuting and corporate applications smooth seasonality by filling weekday gaps, especially in Metro Manila and Cebu, where BPO operations run 24/7 shifts. Operators with mixed tourism-corporate portfolios can shuttle fleets between applications to keep utilization above breakeven. Digitally driven corporate accounts also feed data into demand-forecasting algorithms, improving future fleet procurement decisions.

By Rental Mode: Self-Drive Leadership Confronts Chauffeur Growth

Self-drive solutions dominated at 85.23% of the Philippines' car rental market share in 2024 because they appeal to cost-conscious tourists eager to explore multiple islands on flexible itineraries. Yet, chauffeur-provided services are climbing at 10.25% CAGR, benefiting from urban congestion and the comfort sought by high-spending tourists or executives who value door-to-door convenience.

Technology elevates the chauffeur proposition. Real-time driver tracking, route optimization, and contactless payments reduce wait times and enhance perceived safety. Operators capitalize on higher yields, while drivers gain formal employment and tip income. When paired with electric sedans, chauffeur products align with corporate sustainability objectives, opening new revenue lines.

By Vehicle Class: Economy Foundations Support Premium Aspirations

Economy models held a 49.45% share in 2024, underpinning the Philippines car rental market’s mass-market accessibility. Competitive daily rates lure backpackers and domestic vacationers, while corporates deploy economy cars as pool vehicles for errand runs. Premium-class cars are set to expand at 9.34% CAGR as rising tourist spending above USD 2,000 per capita signals a willingness to pay for comfort and advanced safety features.

Luxury vehicles remain niche but profitable for weddings, VIP transfers, and film shoots. Operators balance fleet mix by sourcing used imports at favorable tariffs, leveraging higher residual values on premium models to mitigate depreciation risk. Upselling insurance and concierge add-ons around premium cars further widens margins.

By Fuel Type: ICE Dominance Faces Electric Disruption

ICE vehicles controlled an 86.34% share of the Philippines car rental market in 2024, supported by a wide fueling infrastructure and lower upfront costs. Electric-vehicle rentals, however, will post the fastest 15.37% CAGR through 2030 on the back of government mandates and tax incentives. Early deployments, such as Diamond Rent-a-Car’s BYD Atto 3 units, target Metro Manila, where charging density and corporate ESG demand intersect.

Hybrid platforms bridge the gap for consumers wary of range limitations, offering quieter rides and up to 30% fuel savings without specialized charging. As charging networks expand and integrate into airport modernization initiatives, we can expect a subsequent increase in adoption in rural areas. This shift will significantly broaden the reach of the green-rental market, opening up new opportunities for eco-friendly transportation solutions beyond urban centers.

Geography Analysis

Metro Manila dominates volume because NAIA funnels the largest share of inbound passengers, and the capital hosts a dense BPO footprint that drives weekday car demand. The country's ride-hailing saturation does dampen self-driving bookings inside city limits. Yet, pick-up in NAIA remains a high-margin revenue source thanks to tourists headed to provincial destinations.

Central Visayas, which Cebu anchors, has become the Philippines' fastest-growing regional cluster of car rental markets. Mactan-Cebu International Airport continues to add new routes, and BPO campuses push corporate usage mid-week. Start-ups such as SWAT Mobility demonstrate how app-orchestrated shuttles and rental hybrids can lower transport costs for employers by 20% while keeping fleet utilization near 95%.

Northern Luzon’s Laoag, Clark, and Baguio corridors benefit from upgraded runways and new charter flights to Japan and South Korea, encouraging operators to station SUVs suited to beach and mountain itineraries. Meanwhile, Mindanao remains under-penetrated as operators monitor security developments and wait for critical road links to finish. The government’s PHP 7.7 billion airport-modernization push covering 15 airports in 2025 gradually adds new demand nodes, rewarding fleets agile enough to redeploy vehicles among emerging gateways[4]“Gov’t Earmarks PHP 7.7 B for Airport Upgrades,”, Philippine News Agency, pna.gov.ph.

Competitive Landscape

The Philippines car rental market is dominated by several key players, such as Avis, Hertz, and Enterprise. Global brands rely on uniform service standards and frequent-flyer tie-ins to attract inbound tourists. Domestic leaders such as ORIX METRO Leasing and Diamond Car Rental leverage lower cost structures and deeper provincial reach. Digital insurgents like GrabRent exploit super-app user bases to cross-sell day rentals alongside ride-hailing, threatening legacy incumbents with price transparency and instant fulfillment.

Technology partnerships define the current strategy. Toyota RentaCar’s integration with JoyRide lets users book anything from a 10-hour stint to a three-year lease, fostering repeat engagement and diversified income streams. BPI Tokyo Century’s EV collaboration with BYD Cars Philippines signals an early land-grab for green-fleet mindshare and positions Diamond Rent-a-Car as a go-to supplier for sustainability-driven corporations.

Operators also differentiate via ancillary services. Some bundle embedded insurance APIs that reduce claim documentation, while others deploy predictive maintenance platforms to cut downtime. Mild consolidation is expected as mid-size provincial fleets seek capital partners to electrify line-ups and connect to OTA channels. Mergers that boost purchasing leverage and technology investment capacity will likely accelerate over the next three years.

Philippines Car Rental Industry Leaders

Enterprise Holdings, Inc.

Avis Rent A Car LLC

Europcar Mobility Group

Hertz Global Holdings

LXV Car Hire Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Toyota RentaCar partnered with JoyRide to offer an in-app booking feature, allowing users to reserve vehicles for periods ranging from 10 hours to three years. The service is initially launching in Metro Manila, providing both residents and visitors with convenient and flexible rental car options.

- May 2025: Carbnb introduced an innovative fleet of self-driving electric vehicles for rent in the Philippines, marking a significant advancement in transportation innovation. This initiative provides Filipinos with a cutting-edge, accessible, and environmentally sustainable alternative to traditional travel options. With a strong focus on sustainability, Carbnb aims to revolutionize mobility in the Philippines, enabling easier exploration of surroundings while promoting eco-friendly practices.

- May 2024: BPI Tokyo Century and BYD collaborated to launch a new initiative: the rental of Atto 3 electric vehicles through Diamond Rent-a-Car. This partnership represents a significant step toward promoting eco-friendly transportation, offering customers access to the advanced features and sustainable benefits of BYD's latest electric model. With this addition, Diamond Rent-a-Car aims to enhance its fleet, catering to environmentally conscious drivers seeking a modern and efficient driving solution.

Philippines Car Rental Market Report Scope

Car rental or car lease companies rent vehicles for a specific time for a set price. This service is frequently organized with multiple local offices, typically located around extensive city areas and backed by a website that allows online bookings.

The Philippine car rental market is segmented by booking type, rental duration, vehicle type, and application. By booking type, the market is segmented into online and offline booking. The market is segmented by rental duration into short-term and long-term. By vehicle type, the market is segmented into hatchbacks, sedans, sport utility vehicles, and multi-purpose vehicles. By application, the market is segmented into tourism and commuting. The market sizing and prediction are made for each segment based on the value (USD).

By Booking Type

| Online |

| Offline |

By Rental Duration

| Short Term |

| Long Term |

By Vehicle Type

| Hatchbacks |

| Sedans |

| Sport Utility Vehicles |

| Multi-purpose Vehicles |

By Application Type

| Tourism |

| Commuting |

By Rental Mode

| Self-drive |

| Chauffeur-driven |

By Vehicle Class

| Economy |

| Premium |

| Luxury |

By Fuel Type

| Internal Combustion Engine |

| Hybrid Electric |

| Battery Electric |

| Plug-in Hybrid Electric |

| Alternative Fuels |

| By Booking Type | Online |

| Offline | |

| By Rental Duration | Short Term |

| Long Term | |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| Sport Utility Vehicles | |

| Multi-purpose Vehicles | |

| By Application Type | Tourism |

| Commuting | |

| By Rental Mode | Self-drive |

| Chauffeur-driven | |

| By Vehicle Class | Economy |

| Premium | |

| Luxury | |

| By Fuel Type | Internal Combustion Engine |

| Hybrid Electric | |

| Battery Electric | |

| Plug-in Hybrid Electric | |

| Alternative Fuels |

Key Questions Answered in the Report

What is the current size of the Philippines car rental market?

The market is valued at USD 682.27 million in 2025 and is forecast to reach USD 988.63 million by 2030 at a 7.70% CAGR.

Which booking channel is growing the fastest?

Online reservations are expanding at 9.75% CAGR, driven by an 88% jump in digital travel spending and widespread mobile-wallet adoption.

How big is the opportunity for electric-vehicle rentals?

EV rentals are projected to post a 15.37% CAGR through 2030, supported by Republic Act 11687’s 5% fleet mandate and tax incentives under EVIDA.

How does fuel price volatility affect operators?

Year-to-date increases of USD 0.22 for gasoline and USD 0.17 for diesel compress margins, pushing fleets to adopt fuel-efficient or hybrid vehicles to manage costs.

Page last updated on: