Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 254.36 Billion |

| Market Size (2031) | USD 366.91 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

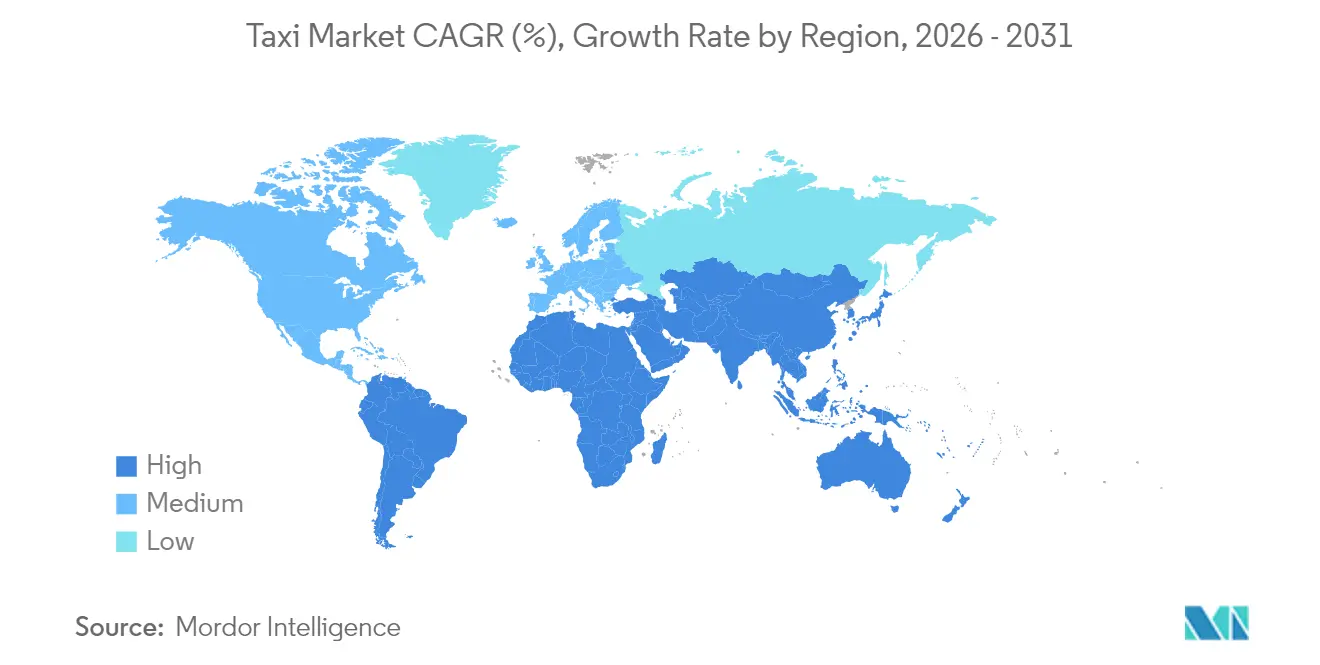

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

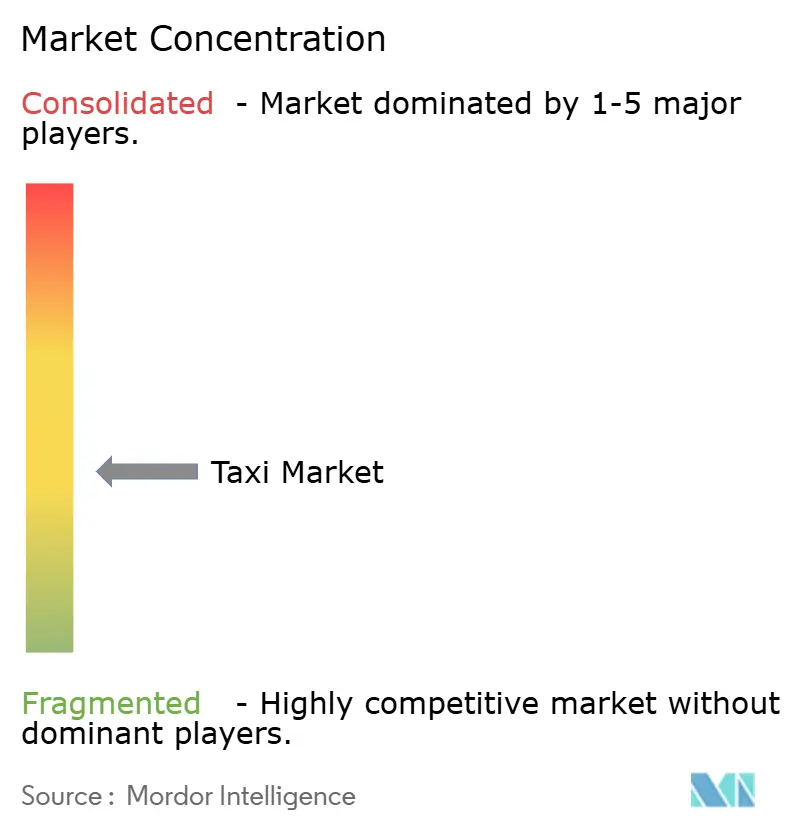

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taxi Market Analysis by Mordor Intelligence

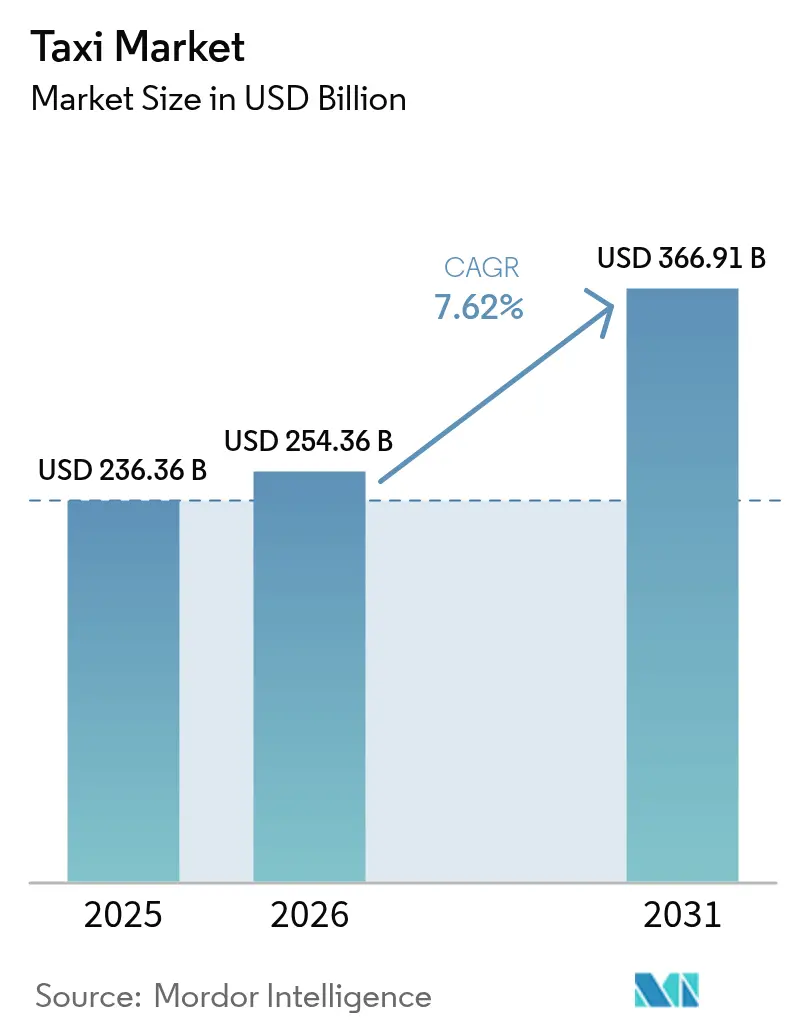

The Taxi Market size was valued at USD 236.36 billion in 2025 and estimated to grow from USD 254.36 billion in 2026 to reach USD 366.91 billion by 2031, at a CAGR of 7.62% during the forecast period (2026-2031). Underscoring a sizeable taxi market size that continues to expand on the back of digital integration, AI-driven dispatch systems, and growing urban populations. Demand accelerates as super-apps embed on-demand mobility alongside food, payments, and finance, enabling single-tap bookings that raise platform stickiness and average revenue per user. Operators are widening service portfolios with electric, autonomous, and accessibility-focused fleets that lower lifetime operating costs and open new revenue layers such as in-vehicle advertising. Governments increasingly view app-based taxis as complements to public transit and are issuing incentives for EV adoption, improved accessibility, and data sharing that favor agile players with strong regulatory teams. Taken together, these forces are reshaping driver economics, pushing industry participants to invest in algorithmic pricing, dynamic routing, and vertical integration that compress time-to-pickup and improve fleet utilization.

Key Report Takeaways

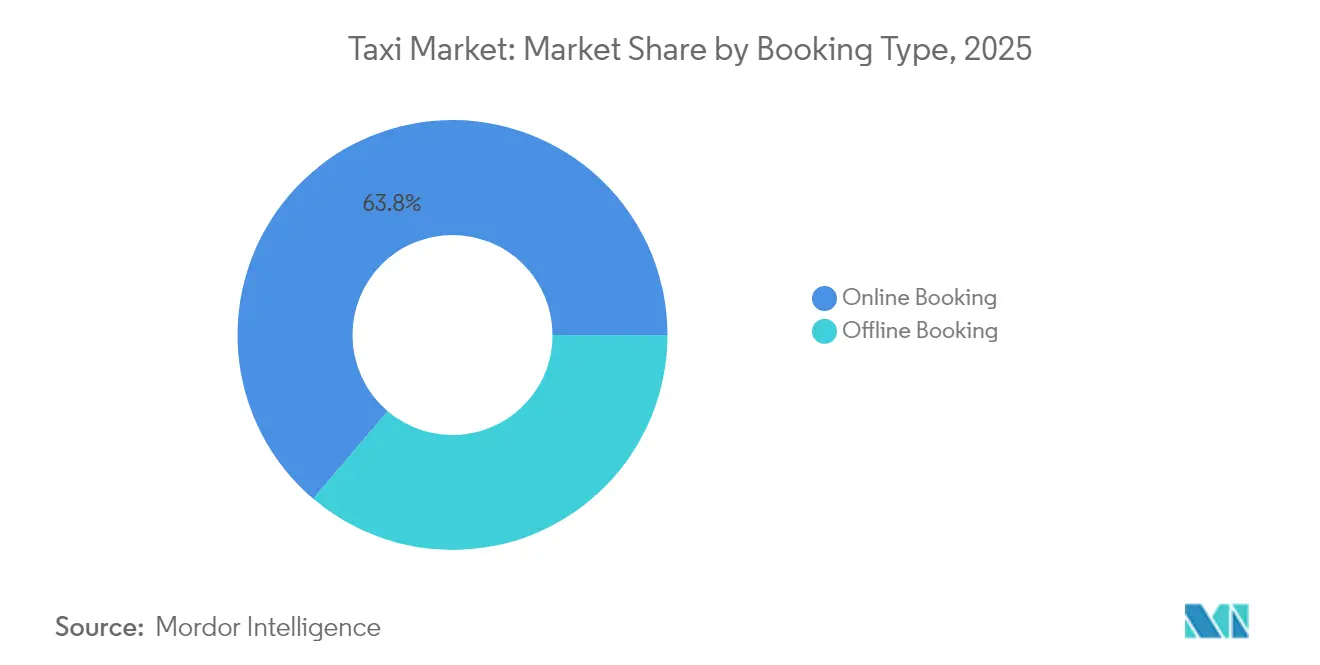

- By booking type, online channels captured 63.78% of taxi market share in 2025 and are forecast to grow at an 7.92% CAGR through 2031.

- By service type, ride-hailing secured 74.85% share of the taxi market size in 2025; pooled ride-sharing is advancing at an 7.78% CAGR through 2031.

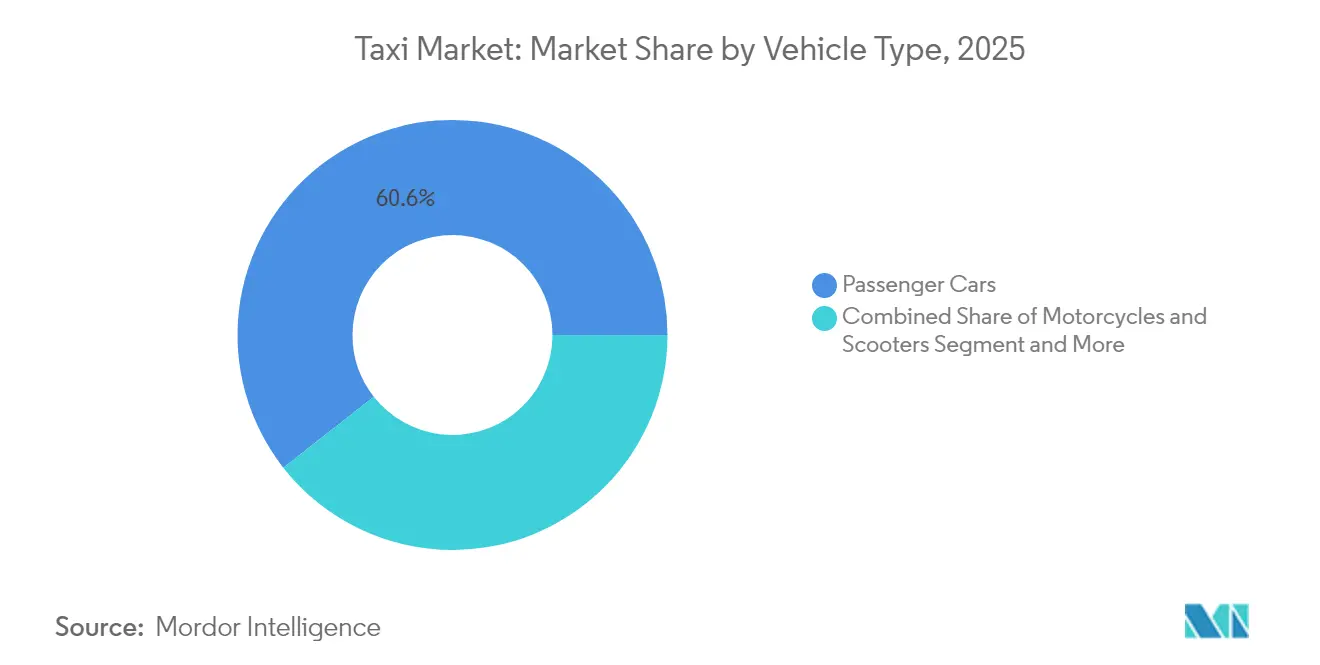

- By vehicle type, passenger cars held 60.58% of taxi market share in 2025, whereas two-wheeler formats are forecast to grow at an 7.71% CAGR over the same period.

- By propulsion, internal-combustion vehicles commanded 71.35% of the taxi market size in 2025; electric taxis are projected to scale at an 8.05% CAGR through 2031.

- By geography, Asia-Pacific led with 37.42% taxi market share in 2025; the Middle East and Africa is positioned to record an 7.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Smartphone and Internet Penetration | +1.8% | Global, with highest impact in Asia Pacific and Middle East and Africa | Medium term (2-4 years) |

| Urban Congestion and Declining Private-Car Ownership | +1.5% | Global, concentrated in major metropolitan areas | Long term (≥ 4 years) |

| Ride-Hailing Platform Expansion | +1.2% | Asia Pacific, Middle East and Africa, South America | Medium term (2-4 years) |

| AI-Based Dynamic Routing | +0.9% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Accessibility Mandates Driving Fleet Renewal | +0.7% | North America, Europe | Medium term (2-4 years) |

| Super-App API Integrations | +0.6% | Asia Pacific core, spill-over to global markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Smartphone & Internet Penetration

Smartphone penetration above four-fifths in leading urban centers lets platforms algorithmically match riders and drivers faster, shrinking average wait times from 15-20 minutes to under 5 minutes in top-tier cities[1]“Mobile Economy Asia Pacific 2024,” GSMA, gsma.com . Ubiquitous 5G coverage allows richer location data, which boosts fleet utilisation and lowers deadhead mileage. Higher data speeds also mean in-app video ads and real-time driver coaching, unlocking diversified revenue streams. Mobile wallets embedded in ride-hailing apps now account for more than four-fifths of transactions in developed markets, lowering cash-handling risk and reducing airport queue times. In emerging economies, internet upgrades bypass legacy dispatch systems, enabling leap-frog adoption of digital bookings.

Urban Congestion & Declining Private-Car Ownership

Vehicle utilisation in dense cities often falls slightly, motivating residents to replace private cars with on-demand rides that eliminate parking fees. Municipal congestion charges plus rising fuel prices raise the total cost of car ownership, reinforcing the appeal of taxi services, especially pooled formats that can cut per-trip fares by up to 40%. Younger consumers aged 25-35 are most receptive, preferring bundled mobility-as-a-service subscriptions integrating taxis with rail, bus, and micro-mobility in one app. Congestion costs topping USD 100 billion annually in the U.S. place political pressure on cities to privilege high-occupancy modes, indirectly boosting taxi market demand.

Ride-Hailing Platform Expansion In Emerging Economies

Localized playbooks such as cash payments, smaller vehicles, and tailored insurance let platforms penetrate frontier markets rapidly. Grab’s integration of legacy taxis raised gross bookings by more than four-fifths in certain Southeast Asian metros. In the MENA region, ride-sharing revenue is p rojected to scale exponentially by 2028 due to youthful demographics and supportive digital policies. Three-wheeler and motorcycle taxis resonate in congested cities because they lower trip costs and shorten travel times, accelerating ride-hailing adoption curves beyond those in developed markets.

AI-Based Dynamic Routing & Pricing Optimisation

Machine-learning systems now factor in weather, events, mass-transit outages, and micro-zone demand to rebalance vehicles proactively, lifting completed trips per driver by up to quarter[2]“i-Rebalance: Large-Scale Real-Time Repositioning,” Uber Technologies, uber.com . Uber’s i-Rebalance trials raised driver income nearly 10% and improved acceptance rates by almost two-fifth. Dynamic pricing models calibrate fares in real time, maximizing revenue per mile while keeping wait times competitive with public transit. Predictive analytics also support demand forecasting for scheduled events, prompting pre-positioning of vehicles that cuts surge spikes and enhances brand loyalty among price-sensitive users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving Licensing and Regulatory Crack-Downs | -1.1% | Global, with highest impact in Europe and North America | Medium term (2-4 years) |

| Intensifying Price Wars Eroding Driver Earnings | -0.8% | Global, concentrated in mature markets | Short term (≤ 2 years) |

| Limited Public EV-Charging Slowing E-Taxi Uptake | -0.6% | Global, most severe in developing markets | Long term (≥ 4 years) |

| Data-Privacy Litigation Around Trip-Tracking | -0.4% | Europe, North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Evolving Licensing & Regulatory Crack-Downs

City regulators are modernising medallion structures and tightening background-check rules, raising compliance costs for app-based and traditional operators. Seattle plans to phase out its medallion regime by March 2026, while New York City requires half of all cabs to be wheelchair-ready by March 2025. The Singaporean watchdog blocked Grab’s planned acquisition of Trans-Cab over antitrust concerns, signalling closer scrutiny of platform consolidation. Divergent regional standards increase legal complexity and can delay market entries, suppressing near-term growth momentum.

Intensifying Price Wars Eroding Driver Earnings

Fierce fare promotions in saturated cities drive down driver net income, raising churn to around two-fifths at some platforms. Subsidised pricing models pressure insurers like American Transit Insurance Company, whose USD 700 million in net losses threaten coverage availability for thousands of medallion holders. Continued investor subsidies mask structural profitability challenges, and any pullback in funding could trigger abrupt fare increases that dent demand elasticity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Adoption Outpaces Legacy Dispatch

Online channels delivered 63.78% of the taxi market share in 2025, illustrating the structural pivot toward app-based demand aggregation. The dominance of digital bookings strengthened business intelligence loops that sharpen demand prediction, resulting in higher asset utilisation and lower passenger wait times. The offline segment remains relevant among older demographics and jurisdictions where medallion systems still confer street-hail privilege, yet its growth trajectory lags the broader taxi market. Operators are therefore integrating voice-based IVR and kiosk interfaces alongside apps to preserve legacy users while nudging them toward digital interactions.

Looking forward, online bookings are forecast to grow at an 7.92% CAGR. Super-apps bundling mobility with payments and e-commerce will underpin incremental trip volumes, especially in APAC megacities where smartphone penetration exceeds four-fifths. Online channels also furnish granular trip-level data that powers targeted loyalty and dynamic pricing, reinforcing share gains. Contractual corporate accounts, airport concessions, and mandated accessibility services sustain the offline channel’s CAGR. Yet, its revenue mix is expected to shrink below one-third of the taxi market size by 2031.

By Service Type: Pooled Formats Lift Occupancy

Ride-hailing controlled 74.85% of taxi market size in 2025, owing to network effects that ensure quicker matches and transparent pricing. Market-leading platforms invest heavily in safety verification, real-time monitoring, and driver training that elevate service reliability above informal rivals. Pooled rides are projected to outpace overall taxi market expansion with an 7.78% CAGR because they ease congestion and lower per-seat fares by sharing costs among passengers. Environmental compliance agendas further catalyse pooled demand as corporates set fleet-wide carbon reduction targets.

Corporate mobility contracts, once dominated by black-car fleets, are increasingly awarded to app-based providers offering digital receipts and per-seat expense allocation. The embedded data facilitates carbon-reporting dashboards now demanded by ESG-focused boards. Although ride-hailing maintains gross-booking supremacy, pooled formats generate higher occupancy and superior asset productivity, especially during peak hours when single-occupancy trips face surge pricing.

By Vehicle Type: Two-Wheeler Momentum Builds

Passenger cars accounted for 60.58% of the taxi market share in 2025, yet motorcycles and scooters are growing at an 7.71% CAGR due to agility in traffic-choked corridors and lower acquisition costs. In Jakarta, two-wheelers slash peak-hour travel times by up to 50% relative to four-wheelers. Operators onboard couriers during off-peak hours, smoothing driver earnings and adding ancillary delivery revenue. Vans and MPVs remain niche, serving group travel and contract school runs where per-capita cost parity with mass transit is advantageous.

The electrification wave is most pronounced in the three-wheeler subset. India sold 1.73 million EV three-wheelers over the past decade under a subsidy-backed push to reduce urban pollution. With operating costs nearly two-fifths lower than diesel, electric three-wheelers strengthen driver profitability despite higher capex. Passenger cars will retain comfort-oriented use cases such as airport transfers, yet incremental volume growth will favor nimble two-wheeler fleets that can navigate gridlocked megacities efficiently.

By Propulsion Type: Electric Gains but ICE Persists

Internal-combustion vehicles still dominated 71.35% of the taxi market in 2025, but electric alternatives are growing fastest at an 8.05% CAGR, fostered by fuel savings and tightening emissions standards. China’s mandate that all new city taxis registered after 2025 must be electric is expected to shift more than a lakh units annually to zero-emission powertrains. Hybrid models serve as interim solutions in regions where charging remains uneven. Battery-swapping services led by Gogoro and Sun Mobility bypass charger scarcity, cutting downtime to under three minutes and appealing to high-utilisation fleets.

Fleet electrification supports upselling in-vehicle digital services such as immersive infotainment and targeted advertising leveraged by consistent 4G/5G connectivity. As the total cost of ownership parity with ICE cars arrives around 2027 for high-kilometre taxis, operators will allocate growing capex to EV fleets even in developing markets. However, limited grid capacity and fragmented charger standards may prolong ICE relevance in rural catchments, ensuring propulsion diversity over the forecast horizon.

Geography Analysis

Asia-Pacific contributed 37.42% taxi market share in 2025, sustained by rapid urbanisation, smartphone usage above four-fifth, and widespread two-wheeler taxis that thrive in dense corridors. Government policies offering EV subsidies and medallion exemptions accelerate fleet turnover throughout India, Vietnam, and Thailand. Japan’s taxi incumbents partner with Uber to integrate 20,000 vehicles on the platform, reinforcing cross-border digital standardisation.

The Middle East and Africa is projected to register an 7.88% CAGR through 2031, due to national digital-economy programmes and mega-city infrastructure. Dubai Taxi Company aims to migrate around four-fifth of rides to e-booking by 2029 while electrifying one-quarter of its fleet, aligning with the UAE Net-Zero 2050 roadmap. Ride-hailing apps proliferate in Egypt, Saudi Arabia, and Nigeria where youthful, tech-savvy populations leapfrog legacy dispatch models. Pan-regional super-apps such as Careem integrate payments, delivery, and transport under one umbrella, enhancing user retention. Authorities impose stricter accessibility and data-privacy mandates, requiring material compliance outlays that favor scaled operators. Lyft’s acquisition of FREENOW in April 2025 doubled its European reach to 11 countries and opened access to nearly 300 billion annual personal vehicle trips. Meanwhile, city councils across Germany are testing zero-emission zones that could bump EV adoption thresholds earlier than corporate plans anticipate. Net effect: growth slows but remains positive as platforms diversify into deliveries and subscription mobility passes.

Competitive Landscape

The taxi market shows moderate fragmentation with regional heavyweights buttressed by deep capital and data advantages. Uber commands more than three-fifth U.S. share, but faces localized challengers like Didi in China and Grab in Southeast Asia that tailor services to domestic user behaviors. Industry focus is shifting toward autonomous vehicle integration, with Uber investing USD 300 million in partnership with Lucid and Nuro to field 20,000 premium robotaxis from 2026, targeting business travellers willing to pay a surcharge for luxury self-driving rides.

Players accelerate vertical integration to capture value beyond core ride fees. Grab’s super-app bundles BNPL finance, grocery delivery, and travel-booking, driving multi-product cross-sell that lifts customer lifetime value. Traditional taxi cooperatives deploy white-label booking apps via SaaS vendors to stay relevant while lobbying for preferential street-hail rights. Data analytics and AI become bigger differentiators as seat-belt monitoring, fatigue detection, and personalised promo codes deliver safety improvements and incremental bookings.

White-space opportunities include specialised services for wheelchair users, schoolchildren, and corporate commuters requiring consistent service-level agreements. Electric vehicle makers such as BYD and Tesla are exploring direct fleet ventures, threatening to disintermediate platform middlemen where regulatory conditions permit. Start-ups offering battery-swap hubs and real-time fleet health analytics position themselves as enabling layers across the value chain, further intensifying competition for driver attention and customer loyalty.

Taxi Industry Leaders

Uber Technologies Inc.

Lyft Inc.

Didi Chuxing

GrabTaxi Holdings Pte Ltd

ANI Technologies Pvt. Ltd (Ola)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Uber entered a USD 300 million partnership with Lucid Group and Nuro to deploy at least 20,000 luxury robotaxis beginning in 2026.

- May 2025: Pony.ai partnered with Uber to pilot autonomous taxis in the Middle East with safety operators onboard during early deployments.

- April 2025: Lyft completed its EUR 175 million (USD 190 million) acquisition of FREENOW, expanding operations into 11 European countries.

Global Taxi Market Report Scope

Taxis are a type of vehicle leasing service that includes the hiring of a driver and the vehicle. It can be used by single or multiple passengers, with the option of sharing or not sharing.

The taxi market is segmented by booking type, vehicle type, service type, and geography.

By booking type, the market is segmented into online booking and offline booking. By vehicle type, the market is segmented into motorcycles, cars, and other vehicle types (vans). By service type, the market is segmented into ride-hailing and ride-sharing.

By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report covers the market size and forecasts the value (USD Billion) for all the above segments.

By Booking Type

| Online Booking |

| Offline Booking |

By Service Type

| Ride-hailing |

| Ride-sharing (pooled) |

| Corporate & Institutional Contracts |

By Vehicle Type

| Passenger Cars |

| Motorcycles & Scooters |

| Vans & MPVs |

| Auto-Rickshaws & Tuk-tuks |

By Propulsion Type

| Internal Combustion Engine (ICE) |

| Electric |

| Hybrid |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Booking Type | Online Booking | |

| Offline Booking | ||

| By Service Type | Ride-hailing | |

| Ride-sharing (pooled) | ||

| Corporate & Institutional Contracts | ||

| By Vehicle Type | Passenger Cars | |

| Motorcycles & Scooters | ||

| Vans & MPVs | ||

| Auto-Rickshaws & Tuk-tuks | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Electric | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the taxi market be by 2031?

It is projected to reach USD 366.91 billion by 2031, expanding at an 7.62% CAGR from 2026.

Which region contributes the highest revenue?

Asia-Pacific led with 37.42% share in 2025, supported by dense urban centers and high smartphone penetration.

What is driving electric taxi adoption?

Lower fuel costs, government subsidies, and city emissions mandates are pushing fleet operators toward EV formats that are growing at an 8.05% CAGR.

Why are two-wheeler taxis gaining popularity?

They navigate congestion efficiently and offer cheaper fares, which is why the segment is growing at an 7.71% CAGR, especially in Southeast Asia.

How are regulations affecting the sector?

Accessibility rules, evolving licensing, and data-privacy legislation raise compliance costs and can slow expansion.

Are autonomous taxis commercially viable yet?

Pilot deployments have begun, and partnerships like Uber-Lucid-Nuro aim to roll out 20,000 robotaxis from 2026, signaling accelerating commercialization within the decade.

Page last updated on: