EV Taxi Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

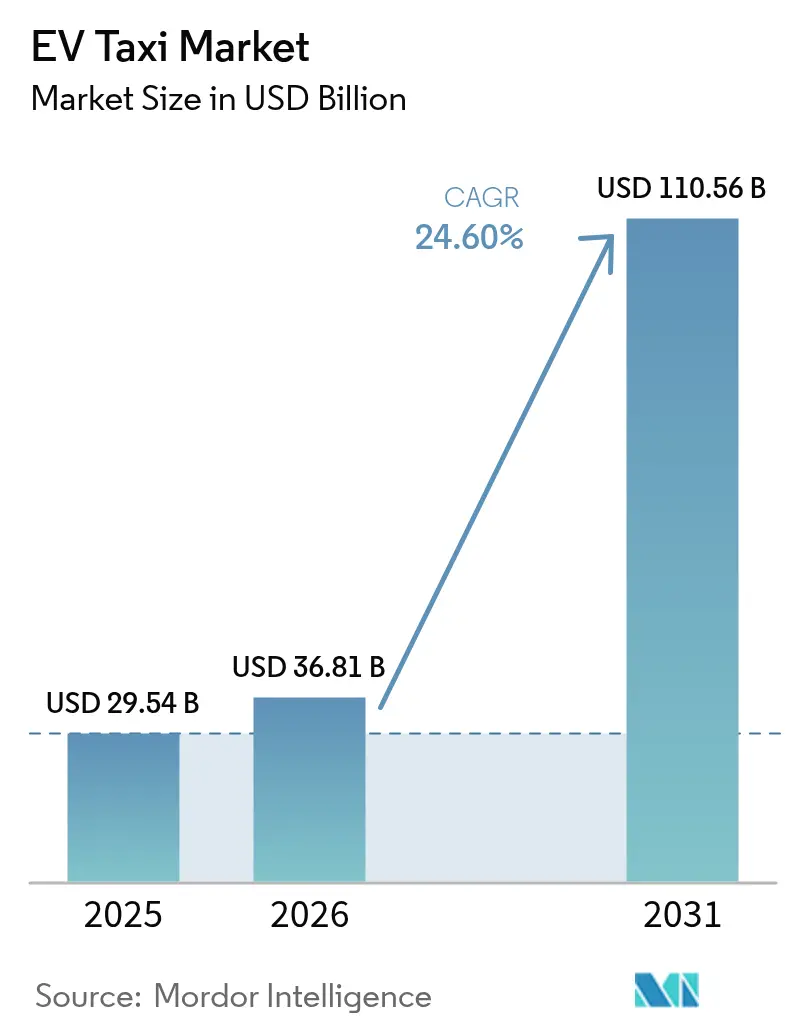

| Market Size (2026) | USD 36.81 Billion |

| Market Size (2031) | USD 110.56 Billion |

| Growth Rate (2026 - 2031) | 24.60% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EV Taxi Market Analysis by Mordor Intelligence

EV taxi market size in 2026 is estimated at USD 36.81 billion, growing from 2025 value of USD 29.54 billion with 2031 projections showing USD 110.56 billion, growing at 24.6% CAGR over 2026-2031. The growth trajectory reflects accelerating total-cost-of-ownership parity, tightening zero-emission taxi mandates, and rapid build-out of fast-charging hubs. Fleets also gain from lower fuel and maintenance outlays, while ride-hailing platforms pull demand forward through firm electrification timelines. Battery-as-a-service business models reduce upfront capital, and ESG-linked municipal finance programs unlock low-cost funding for operators. Asia-Pacific leads on volume, yet the Middle East and Africa register the fastest regional gains as oil-exporting economies pivot toward electrified mobility.

Key Report Takeaways

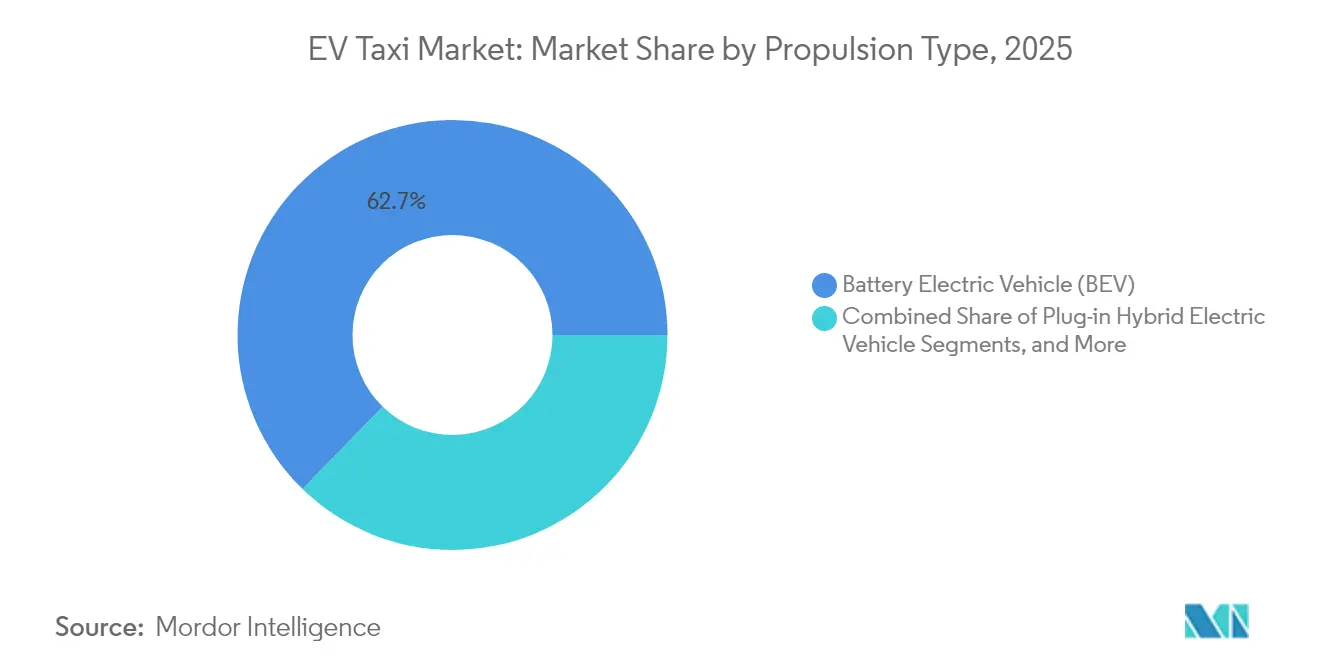

- By propulsion type, Battery Electric Vehicles held 62.72% of the EV taxi market share in 2025; Plug-in Hybrid Electric Vehicles are projected to expand at a 26.8% CAGR through 2031.

- By vehicle type, four-wheeler taxis accounted for 73.46% of the EV taxi market share in 2025, whereas two-wheeler formats are set to grow at a 27.9% CAGR to 2031.

- By service model, ride-hailing captured 72.88% of the EV taxi market share in 2025, while airport and tourism shuttles are forecast to advance at a 27.6% CAGR through 2031.

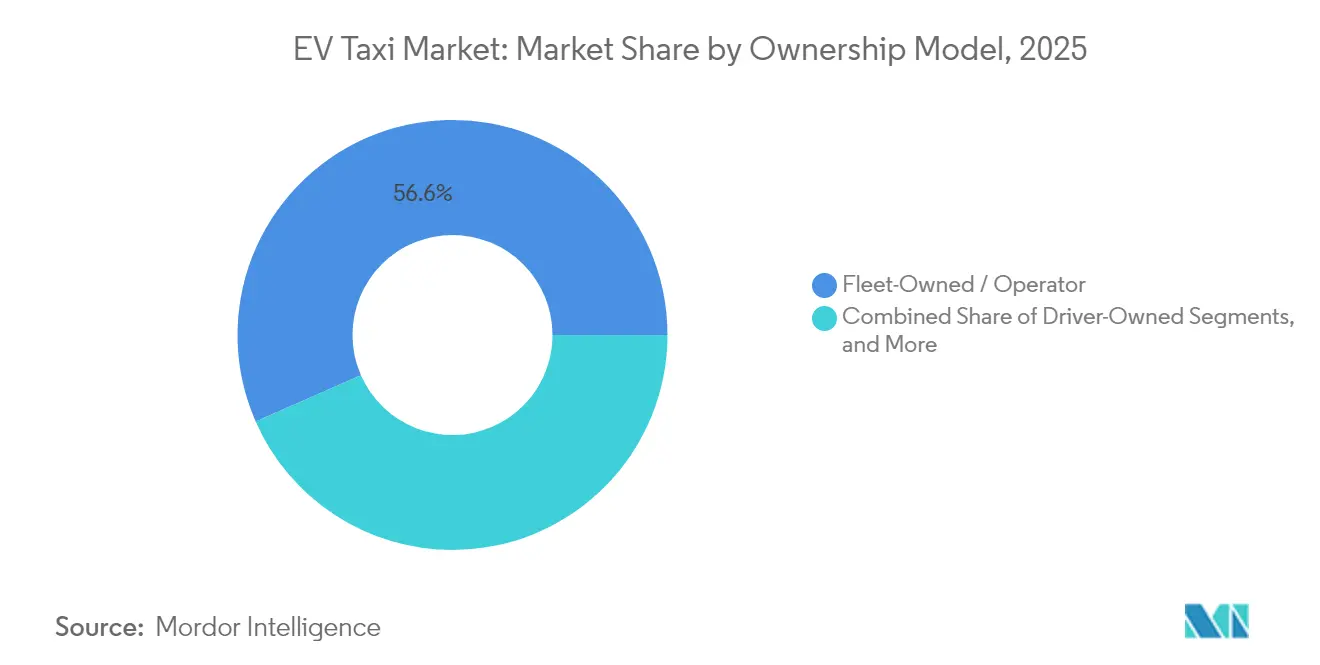

- By ownership, fleet-owned operations represented 56.58% of the EV taxi market share in 2025; leasing and subscription frameworks will post the fastest 26.7% CAGR to 2031.

- By battery capacity, 30–60 kWh packs commanded a 51.83% of the EV taxi market share in 2025, yet configurations above 60 kWh are expected to record a 27.85% CAGR through 2031.

- By geography, Asia-Pacific led with a 43.02% EV taxi market share in 2025, whereas the Middle East and Africa are positioned for a 28.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global EV Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Total-Cost-Of-Ownership (TCO) Parity by 2026 | +6.8% | North America and Europe, spill-over to Asia-Pacific core | Short term (≤ 2 years) |

| Ride-Hailing Platform Electrification Commitments | +5.1% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Government Zero-Emission Taxi Mandates | +4.2% | Global, with early gains in United Kingdom, California, Singapore | Medium term (2-4 years) |

| Battery-as-a-Service Subscription Economics | +3.8% | Asia-Pacific core, expanding to global markets | Medium term (2-4 years) |

| Expansion of Rapid-Charging Hubs at Airports/Urban Cores | +3.5% | Global, concentrated in major metropolitan areas | Medium term (2-4 years) |

| ESG-Linked Municipal Financing Programs | +2.9% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Total-Cost-of-Ownership Parity by 2026

Rapid battery cost declines—now under USD 100 per kWh—and high fuel prices drive economic inflection. In high-mileage taxi duty cycles, fuel and maintenance savings offset higher upfront pricing within three years of operation. Incentive structures such as purchase rebates and accelerated depreciation compress the payback horizon further. Operators consequently rewrite internal rate-of-return models around electric drivetrains rather than diesel powertrains. Lenders respond by offering longer-tenor, lower-coupon debt backed by predictable cash-flow savings.

Ride-Hailing Platform Electrification Commitments

Platforms use sustainability targets to differentiate and secure investor capital. Uber is striving toward its global sustainability objectives, pledging to achieve a zero-emission fleet by 2040. This goal is bolstered by strategic alliances and extensive procurement strategies, highlighted by a letter of intent to acquire electric vehicles from top manufacturers like BYD. Such actions indicate a transition from mere aspiration to tangible execution, empowering Uber to shape supply chains and set benchmarks in urban mobility. Meanwhile, Lyft offers riders “Green” options for a premium fare, subtly steering its driver partners towards electric models. Such guarantees create durable demand that underpins volume purchasing, catalyzing factory allocation for taxi-optimized trims.

Government Zero-Emission Taxi Mandates

Mandated phase-out deadlines for internal-combustion taxis are reshaping fleet procurement schedules. The United Kingdom requires 80% of new cars to be electric by 2030, while California targets 100% zero-emission taxi fleets that year [1]“Transitioning to Zero Emission Vehicles,”, United Kingdom Department for Transport, gov.uk. Singapore moves sooner, insisting that all new taxi registrations be electric from 2025. These mandates carry fines for non-compliance, turning optional sustainability pledges into binding financial obligations[2]“Advanced Clean Fleets Regulation Text,”, California Air Resources Board, arb.ca.gov. Fleet operators accelerate orders, and automakers prioritize certified zero-emission variants that meet regional homologation rules. Municipalities simultaneously carve out low-emission zones, ensuring immediate utilization advantages for compliant vehicles.

Expansion of Rapid-Charging Hubs at Airports and Urban Cores

Targeted deployment of 150 kW to 350 kW chargers at high-demand nodes curtails wait times that once eroded fleet utilization. In 2024, New York’s JFK installed 24 dedicated fast chargers for electric vehicles. Los Angeles International Airport and Zurich Airport have installed electric ports. City franchising authorities are bundling land-use concessions with zero-emission license renewals, aligning incentives between the public and private sectors. With faster turnarounds, drivers can fit in an additional peak-hour shift, bolstering wage stability and expanding the electric vehicle taxi market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Vehicle Downtime Due to Charging | -3.7% | Global, acute in markets with limited fast-charging | Short term (≤ 2 years) |

| Uncertain Residual Values for Used E-Taxis | -2.8% | North America and Europe, emerging concern in Asia-Pacific | Medium term (2-4 years) |

| Urban Grid-Capacity Bottlenecks | -2.1% | Major metropolitan areas globally | Long term (≥ 4 years) |

| OEM Production Priority Away from Taxi Variants | -1.9% | Global, particularly affecting specialized taxi models | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Vehicle Downtime Due to Charging

Electric taxis spend more time off-duty than gasoline equivalents because charging sessions are longer and queuing is common at peak hours. Operators in dense cities feel the pinch when simultaneous shift changes coincide with charger congestion. Lost service minutes translate directly to revenue attrition and tip reductions, making some drivers reluctant to convert even when subsidies exist. The constraint is expected to ease as megawatt charging and better load-management software scale, yet near-term capacity gaps still dampen adoption.

Uncertain Residual Values for Used E-Taxis

With their high annual mileage, taxi operations significantly strain electric vehicle batteries. This raises concerns about the batteries' long-term durability and the vehicles' value retention. Heavy usage and frequent charging cycles hasten battery degradation, potentially affecting performance and resale value. Market data indicate that electric cars depreciate faster than internal combustion vehicles over comparable time frames, especially in high-turnover segments such as ride-hailing. Lenders, insurers, and lessors price this uncertainty into higher monthly payments. Until robust battery-health certification standards emerge, smaller operators without balance-sheet depth hesitate to finance large fleets, and this limits the attainable electric vehicle taxi market size over the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: BEV Leadership Meets PHEV Hedging

Battery electric vehicles represented 62.72% share of the EV taxi market in 2025, illustrating that the electric vehicle taxi market favors drivetrain simplicity and low servicing costs. Plug-in hybrids, however, are gaining swiftly at a 26.8% CAGR through 2031, as operators hedge against sparse highway chargers in peri-urban zones. Therefore, the electric vehicle taxi industry will likely see dual-track procurement strategies until nationwide charging density normalizes. Forward-looking operators already pivot to pure electric in regions planning to exclude hybrids from zero-emission definitions after 2028. Meanwhile, fuel-cell pilots remain confined to hydrogen-corridor projects, collectively under 1% of the current electric vehicle taxi market.

Second-generation PHEVs pair 20+ kWh batteries with efficient range-extenders, allowing 80 km electric-only range that covers most intra-city trips. This flexibility appeals to mid-tier fleet operators who are balancing capex and uptime considerations. Nonetheless, when comparing five-year cash flows, analysts see BEVs achieving a lower net-present cost as soon as charger queuing times fall below twelve minutes. That inflection could lock in BEV dominance by the late decade.

By Vehicle Type: Four-Wheeler Core Faces Two-Wheeler Disruption

Four-wheeler sedans and hatchbacks commanded 73.46% of the electric vehicle taxi market share during 2025, thanks to entrenched regulations and passenger comfort expectations. Yet electric motorcycles and scooters are registering a brisk 27.9% CAGR through 2031, led by Indonesia, India, and Vietnam, where narrow streets, low fares, and modular battery packs propel adoption. These two-wheeler formats often need 3–8 kWh batteries, opening the door to curbside swapping that restores full range in under two minutes.

Regulators increasingly recognize two-wheelers as legitimate taxi categories, issuing digital permits linked to platform apps. That legitimacy improves driver income visibility and accelerates financing availability. Minivans and MPVs retain a role in multi-passenger airport routes. Still, they are not forecast to materially disrupt the dominance of smaller four-wheelers within the electric vehicle taxi market size metrics.

By Service Model: Ride-Hailing Still Dominant, Airport Shuttles Fastest

Ride-hailing apps hold a 72.88% share of the EV taxi market in 2025 and remain the principal channel through which customers access electric taxis. Their digitally matched supply-and-demand model optimizes vehicle utilization, which is crucial for amortizing battery costs. However, airport and tourism shuttle services will log the fastest 27.6% CAGR to 2031 as fixed routes synchronize neatly with scheduled charging windows. The electric vehicle taxi industry’s corporate shuttle niche expands as companies offset Scope 3 emissions.

Policy incentives reinforce the trend: many airports now discount curb fees or allocate priority ranks to zero-emission vehicles. Such privileges improve fare turnover, enticing private shuttle operators to electrify fleets earlier than ride-hailing independents.

By Ownership Model: Subscription Economics Challenge Fleet Dominance

Fleet-owned structures supplied 56.58% of all electric vehicle taxis in 2025, benefiting from scale procurement and in-house workshops. Yet leasing and subscription formats, buoyed by battery-as-a-service, are projected to surge at a 26.7% CAGR through 2031. Under these contracts, the battery remains with a specialized asset manager who guarantees replacement once its health falls below 80%. The arrangement slices upfront vehicle cost by up to one-third and protects operators from residual-value uncertainty.

Individual driver ownership grows only where micro-finance programs pair favorable interest rates with guaranteed platform demand. Absent those enablers, high capex deters single-cab entrepreneurs from joining the electric vehicle taxi market.

By Battery Capacity: Mid-Range Packs Prevail, High-Capacity in Ascent

Packs rated 30–60 kWh deliver 51.83% of the EV taxi market in 2025 because they offer 250 km urban range at a manageable cost and weight. Units above 60 kWh, though constituting a smaller base, are expanding at a 27.85% CAGR through 2031, as suburban and inter-city taxi segments require longer stretches between charges. Deployments of sub-30 kWh batteries concentrate in two-wheelers and dense Asian mega-cities, where micro-mobility trips rarely exceed 15 km.

Chemistry advances, such as lithium-iron-phosphate with higher energy density, are shaving pack weight and opening new body-style possibilities. By the late decade, mid-range packs may retain dominance in the total electric vehicle taxi market size, yet high-capacity variants will underpin premium fare classes and airport corridors.

Geography Analysis

Asia-Pacific holds 43.02% share of the EV taxi market in 2025, reflecting China’s manufacturing heft, India’s two-wheeler boom, and proactive policy incentives in Japan, South Korea, and Australia. Provincial dual-credit schemes in China allow fleet operators to trade compliance certificates, improving project economics. India’s FAME-II subsidies, meanwhile, boost localization of battery packs and chargers, deepening domestic supply chains that stabilize retail pricing.

The Middle East and Africa will record the fastest 28.45% CAGR through 2031, led by the United Arab Emirates’ zero-emission ground-transport vision for Expo 2030 and Saudi Arabia’s NEOM smart-city blueprint. Generous electricity tariffs and abundant solar capacity further reduce operating costs. Egypt and Morocco are rolling out green-bond-funded taxi electrification schemes, drawing on multilaterals for concessional finance.

California’s Advanced Clean Fleets rule sets the tone, while New York City caps new internal-combustion taxi medallions. Europe benefits from mature public charging networks, but lingering energy-price volatility still impacts driver payback calculations. South America trails due to exchange-rate risk and elevated cost of capital, yet Brazil and Colombia have begun piloting tariff discounts for overnight fleet charging.

Competitive Landscape

Market rivalry straddles automakers, platform companies, and specialist fleet operators. Uber and Lyft wield scale to negotiate bulk discounts, sometimes integrating direct-to-driver financing that speeds uptake. Chinese OEMs such as BYD, SAIC, and Geely leverage vertically integrated battery supply to undercut legacy manufacturers on price, enabling wider penetration into value-sensitive taxi segments.

Regional pure-plays also emerge. India’s BluSmart Mobility operates a fully electric fleet plus proprietary fast-charging depots across Delhi-NCR and Bengaluru. Vietnam’s GSM Green and Smart Mobility replicates the strategy, integrating home-grown ride-hailing software with charging infrastructure. Airports increasingly award exclusive concessions to operators committing to 100% zero-emission fleets, shifting competitive advantage toward early movers.

Regional pure-plays also emerge. India’s BluSmart Mobility operates a fully electric fleet plus proprietary fast-charging depots across Delhi-NCR and Bengaluru. Vietnam’s GSM Green and Smart Mobility replicates the strategy, integrating home-grown ride-hailing software with charging infrastructure. Airports increasingly award exclusive concessions to operators committing to 100% zero-emission fleets, shifting competitive advantage toward early movers.

EV Taxi Industry Leaders

Uber Technologies Inc.

Didi Chuxing Technology Co.

Grab Holdings Ltd.

Lyft Inc.

Ola Electric Mobility Pvt Ltd. (Ola Cabs)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Uber will acquire over 20,000 Lucid Gravity SUVs equipped with autonomous vehicle (AV) technology from Nuro. This deal highlights renewed efforts in self-driving cabs after earlier investments produced limited results. Uber will invest hundreds of millions in Lucid and Nuro, with USD 300 million allocated to Lucid.

- March 2025: Evera Cabs, an all-electric taxi service in India, raised USD 4 million from Mufin Green Finance Pvt. Ltd. through convertible debentures and debt financing, highlighting investor interest in India's electric mobility sector.

- July 2024: Uber Technologies, Inc. and BYD Co., Ltd. unveiled a strategic partnership, aiming to integrate 100,000 new BYD electric vehicles into the Uber platform over the coming years. This collaboration targets major global markets and aligns with Uber's commitment to sustainability by expanding its fleet of electric vehicles, thereby reducing carbon emissions and promoting eco-friendly transportation solutions.

Global EV Taxi Market Report Scope

An electric vehicle taxi refers to a taxi or ride-sharing vehicle powered by an electric motor and battery rather than traditional internal combustion engines fueled by gasoline or diesel. EV taxis offer a sustainable and environmentally friendly transportation option, emitting zero tailpipe emissions during operation.

The EV taxi market is segmented by type, vehicle type, and geography. By type, the market is segmented into hybrid electric vehicles, battery electric vehicles, and plug-in hybrid electric vehicles. By vehicle type, the market is segmented into four-wheelers and two-wheelers. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report offers the market sizes and forecasts for all the above segments in value (USD).

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Two-wheeler Taxi |

| Three-wheeler Taxi |

| Four-wheeler Taxi (Sedan/Hatchback) |

| Multi-Purpose Vehicle / Minivan |

| Ride-hailing (On-demand) |

| Ride-sharing (Pooling) |

| Corporate / Institutional Fleet |

| Airport and Tourism Shuttle |

| Fleet-Owned / Operator |

| Driver-Owned |

| Leasing and Subscription |

| Less than 30 kWh |

| 30-60 kWh |

| Above 60 kWh |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Propulsion Type | Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Vehicle Type | Two-wheeler Taxi | |

| Three-wheeler Taxi | ||

| Four-wheeler Taxi (Sedan/Hatchback) | ||

| Multi-Purpose Vehicle / Minivan | ||

| By Service Model | Ride-hailing (On-demand) | |

| Ride-sharing (Pooling) | ||

| Corporate / Institutional Fleet | ||

| Airport and Tourism Shuttle | ||

| By Ownership Model | Fleet-Owned / Operator | |

| Driver-Owned | ||

| Leasing and Subscription | ||

| By Battery Capacity | Less than 30 kWh | |

| 30-60 kWh | ||

| Above 60 kWh | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the electric vehicle taxi segment growing compared with conventional taxis?

Fleet electrification is projected to climb at a 24.6% CAGR through 2031 versus single-digit growth for conventional models, driven by lower operating cost and stricter emission mandates.

Which region will add the most new electric taxis by 2031?

Asia-Pacific will supply the highest absolute unit additions, yet the Middle East and Africa will register the fastest 28.45% CAGR on a smaller base.

Do operators prefer outright purchase or subscription for batteries?

Leasing and battery-as-a-service contracts are forecast to expand at 26.7% CAGR as they shift battery degradation risk away from drivers and reduce initial capital outlay.

What battery size dominates urban taxi operations?

Packs in the 30–60 kWh range account for 51.83% of active fleets because they balance 250 km daily range with manageable weight and cost.

Will plug-in hybrids remain relevant after 2028?

PHEVs fill infrastructure gaps today, but jurisdictions phasing them out of zero-emission definitions could dampen demand later in the decade.

Page last updated on: