Indonesia Passenger Car Taxi Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.51 Billion |

| Market Size (2026) | USD 4.82 Billion |

| Market Size (2031) | USD 6.69 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

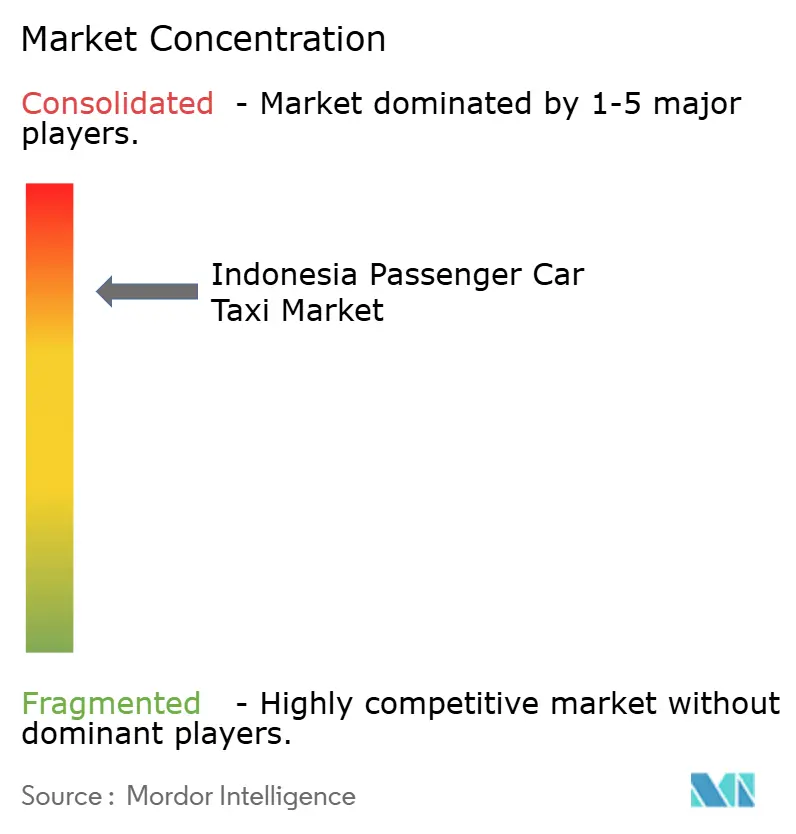

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Passenger Car Taxi Market Analysis by Mordor Intelligence

The Indonesian passenger car taxi market size in 2026 is estimated at USD 4.82 billion, growing from 2025 value of USD 4.51 billion with 2031 projections showing USD 6.69 billion, growing at 6.78% CAGR over 2026-2031. Digital-first mobility habits, rising urbanization, and state‐backed electrification programmes sustain the upward trajectory of the Indonesian taxi market while super-app ecosystems steadily replace standalone dispatch operations. Price-sensitive riders propel shared trips, yet tariff floors imposed by the Ministry of Transportation cushion operators from predatory pricing. Jakarta’s congestion fuels on-demand bookings, but underserved secondary cities now attract new fleets, especially as electric vehicles (EVs) lower lifetime costs. High smartphone penetration, a mature e-wallet landscape, and the prospect of a Grab-GoTo combination continue to reshape competitive dynamics.

Key Report Takeaways

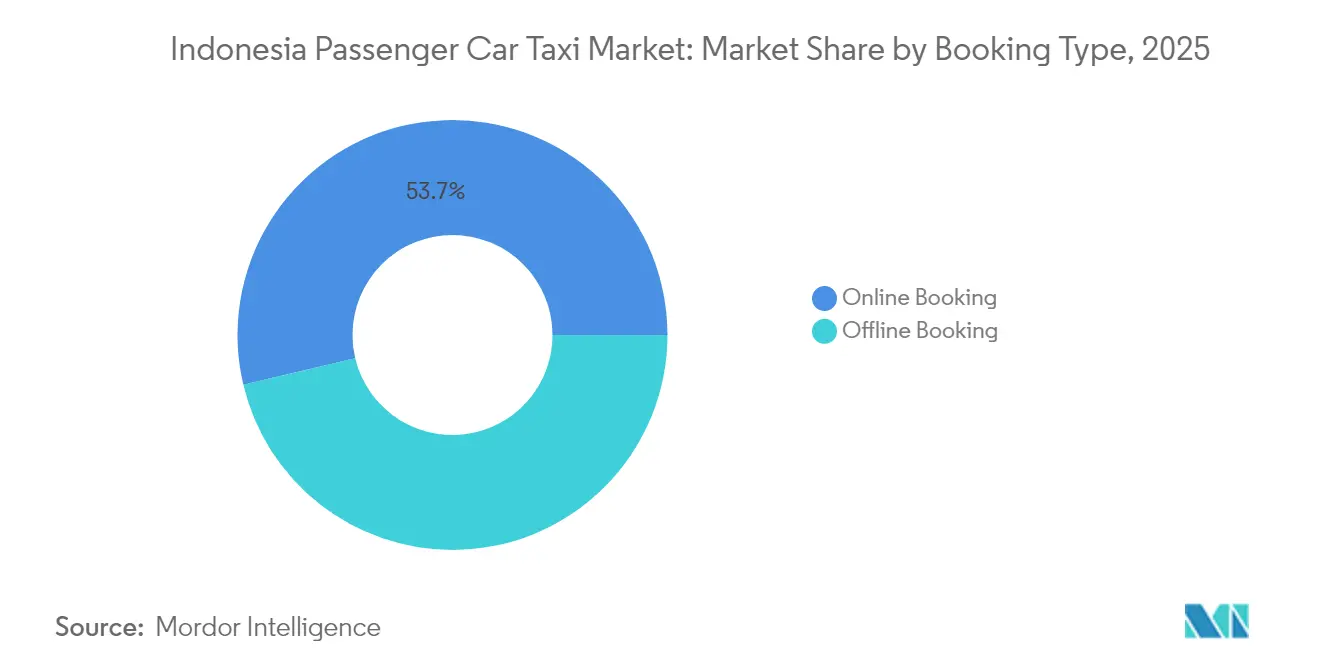

- By booking type, online booking led with 53.72% revenue share in 2025, while the same channel is expanding at a 11.91% CAGR through 2031.

- By service type, ride-hailing held 74.93% of the Indonesian taxi market share in 2025, and ride-sharing is forecast to advance at a 17.02% CAGR to 2031.

- By vehicle type, sedans accounted for 41.12% of the Indonesian taxi market size in 2025; hatchbacks delivered the fastest 14.71% CAGR during 2026-2031.

- By customer segment, residential users contributed 58.77% in 2025, while leisure and tourism are expected to post the strongest 16.74% CAGR up to 2031.

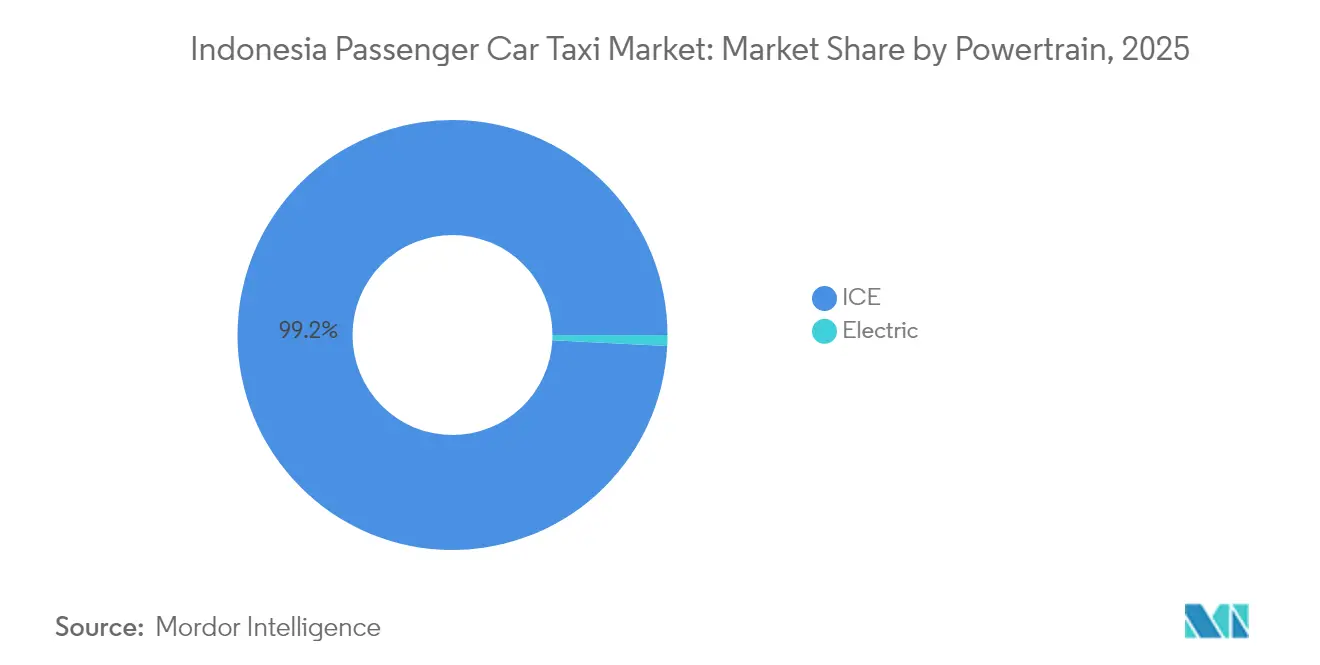

- By powertrain, ICE vehicles dominated with a 99.18% share in 2025, yet electric taxis accelerate at a 43.64% CAGR to 2031.

- By use case, urban commute represented a 48.56% share in 2025, and airport transfers are expected to grow quickest at 15.89% CAGR through 2031.

- By region, Jakarta commanded 16.55% share in 2025, whereas Bali and Nusa Tenggara emerges as the fastest-growing geography at an 8.01% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Passenger Car Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Urban Congestion | +1.1% | Jakarta, Surabaya, Bandung, Medan | Short term (≤ 2 years) |

| Electrification and Charging Infrastructure Initiatives | +0.9% | Java, Sumatra, Bali | Medium term (2-4 years) |

| Growing Digital Payments Ecosystem | +0.6% | Jakarta, Surabaya, Bandung | Short term (≤ 2 years) |

| Suburban and Secondary Cities | +0.4% | West Java, East Java, North Sumatra | Long term (≥ 4 years) |

| OTA Integration Enabling | +0.4% | Jakarta, Bali, Yogyakarta | Medium term (2-4 years) |

| Data-Driven Fleet Optimization | +0.3% | Jakarta, Surabaya, Medan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Urban Congestion Accelerating Adoption of Ride-Hailing Apps

Jakarta remains one of the world’s most congested capitals, and commuters incur mounting travel delays that raise the opportunity cost of private car ownership. Ride-hailing platforms shorten wait times by matching latent demand with nearby drivers, a value proposition magnified around new MRT stations that funnel last-mile riders directly to designated pick-up zones. Flexible earnings for drivers increase fleet density and further compress response times, creating a virtuous usage cycle. The Ministry of Transportation’s quota of 83,906 licensed online taxis shows that the government now treats app-based fleets as integral mobility infrastructure. Yet quota allocations still favour the Jabodetabek region, signalling gradual expansion into smaller metropolitan areas.

Government Incentives for Electric Taxi Fleets and Charging Infrastructure

Presidential Regulation 55/2019 introduced 0% import duty and 1% VAT on locally compliant battery-electric cars, lowering initial capex for fleet operators. PLN scaled public chargers to 1,582 units across 1,131 locations by mid-2024 and plans to prioritize high-traffic corridors, easing range anxiety for prospective taxi owners. Traditional operator Blue Bird targets 600 additional EVs in 2025, elevating its battery-powered portion to 10% by 2030, because lower energy costs extend vehicle lifespans and support premium pricing[1]The Jakarta Post Staff, “Blue Bird to add 600 electric taxis this year,” The Jakarta Post, thejakartapost.com. Foreign entrant Xanh SM likewise positions fully-electric fleets to capitalise on incentives and differentiate service. Although most chargers cluster in Java, impending nickel-based battery output promises cheaper models, accelerating provincial electrification.

Rapid Growth of Indonesia’s Digital Payments Ecosystem

Mobile wallets dominate everyday finance, and frictionless in-app settlement encourages customers to choose ride-hailing over cash-only street taxis. Integrated loyalty programs convert freelance riders into habitual subscribers through discounted bundles that combine mobility, food delivery, and bill payments. Operators analyse payment data for demand forecasting, aligning driver supply with peak hours and cutting idle time. National targets for 90% adult digital inclusion strengthen the backbone for cashless rides, yet patchy connectivity outside big cities still necessitates hybrid options. As fintech ecosystems mature, dynamic pricing and subscription tiers will raise average revenue per user despite intense fare competition.

Under-Penetrated Suburban and Secondary Cities Opening New Demand Nodes

Beyond Jakarta, scores of fast-growing municipalities lack reliable mass transit and present white-space opportunities. New players deploy lower commission models to woo drivers, while incumbents test two- and four-wheel hybrids to match narrow road networks. Conversion costs remain modest because smartphone adoption has reached critical mass even in tier-two cities. Localised marketing and driver training tailor services to cultural nuances, offsetting lower per-trip yields through volume scale. Infrastructure projects that link industrial parks to surrounding suburbs generate commuter clusters that on-demand fleets can efficiently serve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Regulatory Frameworks | -0.6% | All provinces with varying intensity | Long term (≥ 4 years) |

| Price Wars | -0.4% | Jakarta, Surabaya, Bandung | Short term (≤ 2 years) |

| Fast-Charging Infrastructure Shortage | -0.3% | Sumatra, Kalimantan, Sulawesi | Medium term (2-4 years) |

| Two-Wheelers Preference | -0.2% | Java, Sumatra, Bali | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Frameworks Across Provinces

Indonesia’s decentralised governance grants districts discretion over licensing, tariffs and vehicle quotas, forcing multi-regional fleets to juggle varied rulesets. Compliance audits, tax levies and paperwork inflate administrative overheads and delay expansion plans. Recent ministerial decrees cap commissions and permit driver welfare fees, but enforcement differs by locale, perpetuating uncertainty. Where local ordinances remain unaligned with national guidelines, legal ambiguities deter inward investment. The slated Omnibus Law seeks to harmonise statutes, yet its transport-specific clauses may take years to filter into provincial bylaws.

Price Wars Eroding Operator Profitability

Aggressive discounting has become the default customer-acquisition tactic, pushing blended take-rates below sustainable thresholds. Operators routinely subsidise fares and driver incentives, producing headline growth while accumulating losses. Government-mandated minimum tariffs restrict over-discounting, yet competitive pressure keeps margins razor-thin. Drivers, squeezed by lower incentives, stage periodic strikes demanding pay hikes, raising reputational risks for platforms. New entrants employing rock-bottom commissions intensify the race to the bottom, limiting room for rational pricing. Sustained profitability, therefore, hinges on consolidation or differentiated service tiers rather than pure fare cuts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Transition Accelerates Gradually

Online reservations captured the majority share at 53.72% in 2025 as super-apps embedded ride buttons directly into lifestyle ecosystems, making the Indonesian taxi market the first mobility touchpoint for many e-commerce users. Offline hails persist among older riders and corporate travellers who favour predictable flag-down service, but their patronage declines as app literacy spreads. The Indonesian taxi market size for online bookings is projected to expand swiftly at 11.91% CAGR, supported by biometric log-ins, voice ordering and loyalty integrations that compress booking friction. Payment wallets auto-populate receipts, easing expense claims and attracting enterprise accounts. Conversely, kiosk and phone bookings migrate online as fleet operators phase out call centres to cut costs.

App operators layer push notifications, gamified rewards and subscription bundles to increase trip frequency and lock in customers. Uptake further accelerates when rail or bus apps cross-sell discounted first-mile coupons to funnel riders into integrated journeys. Nevertheless, offline channels retain a foothold in airports and hotels where concierge-based dispatch aligns with customer service expectations. A seamless blend of touchpoints therefore remains essential to bridge Indonesia’s varied digital readiness levels. Over the forecast horizon, digital literacy programmes and wider 4G coverage in archipelagic regions will narrow the gap, ensuring that online channels become the default.

By Service Type: Ride-Sharing Emerges as Growth Engine

Ride-hailing dominated with a 74.93% share in 2025, cementing its role as the on-demand backbone of the Indonesian taxi market. Yet ride-sharing pools, where strangers split fares, clock an impressive 17.02% CAGR as cost-aware commuters accept slightly longer routes in exchange for savings. This momentum is further amplified when platforms blend algorithmic matching with real-time routing that limits detours to minutes, preserving service satisfaction. Fleet operators exploit larger vehicle formats during peak hours, raising seat utilisation and diluting fuel spend per passenger.

Regulatory clarity recognising shared trips under the same transport category as exclusive hires simplifies licensing and insurance, unblocking capital allocation. In addition, employers encourage pooled rides in corporate mobility programmes aimed at carbon reduction, indirectly sustaining demand. Even so, service-quality benchmarks, such as maximum detour allowances, must be met to avoid rider churn. Over time, rising fuel prices and sustained inflationary pressure should reinforce the value proposition, positioning ride-sharing as the Indonesian taxi market’s primary incremental growth lever.

By Vehicle Type: Efficiency Drives Hatchback Preference

Sedans continued to headline the vehicle mix, holding 41.12% of Indonesia's taxi market share in 2025, thanks to roomy cabins that satisfy corporate travellers and airport passengers. However, hatchbacks eclipse all other categories in pace, expanding at 14.71% CAGR because shorter wheelbases ease navigation through congested alleys while cutting fuel bills. Operators prefer hatchbacks for short-hop urban deployments where quick turnaround multiplies daily trip counts, thereby boosting driver earnings.

SUVs and multi-utility vehicles address niche family or tourist groups requiring greater luggage allowance. Premium sub-segments, including chauffeur-led executive sedans, maintain loyal clientele but represent limited volume. Electric variants gradually enter each body type, yet early adoption concentrates in hatchbacks whose lighter frames yield better range. Divergent road conditions across the archipelago also influence fleet composition; pothole-prone provincial roads often necessitate sturdier suspensions offered by crossover models. As total cost of ownership analytics gain prominence, fleet managers will fine-tune mix, yet efficiency-led hatchbacks are set to widen their footprint.

By Customer Segment: Tourism Recovery Fuels Leisure Growth

Residential riders formed the bedrock, delivering 58.77% contribution in 2025 as citizens habitually booked taxis for daily commutes, errands, and social outings. Leisure and tourism, heavily hit by pandemic restrictions, rebounds with a forecast 16.74% CAGR, stimulating incremental trips as holidaymakers return to beaches and heritage circuits. The Indonesian taxi market size linked to holiday traffic benefits from bundled vouchers marketed by airlines and OTAs, which guarantee pre-paid transfers at destination airports.

Corporate mobility spending stabilises as hybrid work models reduce weekday peaks but spawn cross-city trips for quarterly meetings. Operators, therefore, deploy flexible subscription passes that companies can top up for employees. Meanwhile, government events and MICE gatherings create episodic demand spikes, prompting fleets to adopt dynamic scaling through driver rental marketplaces. Overall, changing travel patterns encourage segment diversification so that revenue does not rely excessively on single customer archetypes.

By Powertrain: Electric Revolution Begins Despite Infrastructure Gaps

Internal-combustion cars still constituted 99.18% of active taxis in 2025, bolstered by ubiquitous refuelling options and proven maintenance ecosystems. Yet electric units, though a mere 0.82% share presently, will surge at 43.64% CAGR as battery costs fall and charging networks spread, redirecting future gains in the Indonesian taxi market. Operators weigh higher sticker prices against energy savings that can trim per-kilometre operating cost by up to 50%.

Multi-stakeholder schemes install kerbside chargers at malls and office towers, easing range anxiety and aligning station utilisation with driver dwell breaks. Government fleet targets give OEMs predictable volume, accelerating local assembly and parts localisation. Still, roll-out beyond Java hinges on resolving grid constraints and introducing battery swap models that shrink down-time. Over the next decade, a mixed-powertrain landscape will prevail, but total cost economics lean decisively in favour of electrification.

By Use Case: Airport Transfers Lead Specialized Growth

Urban commutes absorbed 48.56% of rides in 2025, underscoring taxis’ role in bridging inadequate public transport. Airport transfers, however, flourish at 15.89% CAGR, powered by aviation recovery and marketing tie-ups with airlines that bundle “home-to-runway” packages. Pre-booked airport rides provide predictability, enabling operators to align high-capacity van fleets with peak flight banks and lift average ticket sizes for the Indonesian taxi industry.

Inter-city point-to-point runs face competition from improved express bus and rail links, yet premium offerings with flat fares and door-to-door convenience hold niche appeal among time-sensitive travellers. Hourly hire services cater to tourists requiring hop-on flexibility across dispersed attractions, while corporate events generate bulk bookings that justify dedicated dispatch desks. Each use case has distinct peak patterns, motivating algorithmic scheduling to allocate drivers efficiently across the day.

Geography Analysis

Jakarta retained a 16.55% slice of the Indonesian taxi market in 2025, propelled by dense corporate headquarters, embassy districts, and an expanding MRT spine that feeds first- and last-mile rides. Heightened congestion sustains fare demand, yet fierce competition compresses margins as platforms jockey for loyalty. Regulatory agencies maintain tariff floors and quota systems that stabilise operations but slow capacity expansion. An imminent merger between leading platforms could temper price wars and pivot focus toward profitability.

As manufacturing parks, universities, and tourism sites intensify mobility needs, Java benefits from spill-over economic activity. Cities like Surabaya and Bandung showcase robust app adoption, and a growing charger footprint underpins gradual electric taxi introductions. Traditional operators leverage provincial hubs to diversify away from saturated Jakarta, installing satellite depots that shorten driver dead-head distances. As digital wallets penetrate smaller towns, online bookings jump, compressing the digital divide.

Bali and Nusa Tenggara deliver the fastest 8.01% CAGR on the back of resurgent international arrivals and infrastructure upgrades that ease intra-island travel. Tourism-centric peaks necessitate flexible fleet scaling and multilingual driver support. Beyond these islands, Sumatra, Kalimantan and Sulawesi represent long-term growth reservoirs but grapple with smartphone gaps, patchier chargers and provincial fee heterogeneity. Coordinated public-private investment in roads and electricity networks will dictate adoption pace in these emerging corridors.

Competitive Landscape

The Indonesian taxi market exhibits a concentrated duopoly structure where Grab and Gojek control more than half of the market share. This concentration creates pricing power potential that remains unrealized due to intense competition and regulatory price controls, with both digital platforms reporting significant losses despite high transaction volumes as they prioritize market share over profitability. The contemplated Grab–GoTo tie-up, valued above USD 7 billion, would consolidate user bases, harmonise driver pools, and restore pricing discipline should regulators approve. Smaller challengers differentiate via lower commissions, localised service tweaks, and deeper secondary-city penetration, but limited capital hampers national scale-up.

Technology remains the primary battleground. Market leaders deploy AI-driven dispatch, predictive maintenance and personalised promotions to lift conversion rates and trim idle kilometres. Blue Bird’s real-time telematics now mirrors app-native competitors, demonstrating that traditional fleets can retrofit innovation without jettisoning legacy brand trust. Meanwhile, foreign entrant Xanh SM bets on fully electric fleets to capture eco-conscious riders and corporate CSR budgets, signalling intensifying green competition.

Future rivalry will hinge less on raw app downloads and more on ecosystem breadth, payments, e-commerce and media, as super-apps seek to anchor users across daily routines. Profit sustainability depends on cross-subsidies from adjacent verticals and disciplined incentive spending. Regulatory vigilance over antitrust concerns ensures space for midsized operators, even as scale economics favour a tighter oligopoly.

Indonesia Passenger Car Taxi Industry Leaders

Grab Holdings Inc.

PT Aplikasi Karya Anak Bangsa (Gojek)

PT Blue Bird Tbk

Maxim

PT Express Transindo Utama Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Blue Bird announced plans to add 600 electric vehicles to its fleet in 2025, targeting 1,000 EVs by year-end and 10% fleet composition by 2030.

- March 2025: PT Express Transindo Utama relaunched taxi operations in Jakarta with a fleet of BYD M6 electric cars.

- January 2025: Cititrans, a shuttle brand under Blue Bird Group, introduced an airport route linking Juanda International Airport to Malang.

- December 2024: PT Xanh SM rolled out electric VinFast VF e34 taxis in Jakarta and outlined plans for up to 10,000 units by 2025.

Indonesia Passenger Car Taxi Market Report Scope

| Online Booking |

| Offline Booking |

| Ride Hailing |

| Ride Sharing |

| Traditional Taxis |

| Hatchback |

| Sedan |

| SUVs |

| MUVs |

| Corporate |

| Leisure and Tourism |

| Residential |

| ICE |

| Electric |

| Urban Commute |

| Airport Transfer |

| Inter-city / Long-haul |

| Tourist/Leisure |

| Hourly Hire |

| Corporate/MICE Movements |

| Jakarta |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Bali and Nusa Tenggara |

| Papua and Maluku |

| By Booking Type | Online Booking |

| Offline Booking | |

| By Service Type | Ride Hailing |

| Ride Sharing | |

| Traditional Taxis | |

| By Vehicle Type | Hatchback |

| Sedan | |

| SUVs | |

| MUVs | |

| By Customer Segment | Corporate |

| Leisure and Tourism | |

| Residential | |

| By Powertrain | ICE |

| Electric | |

| By Use Case | Urban Commute |

| Airport Transfer | |

| Inter-city / Long-haul | |

| Tourist/Leisure | |

| Hourly Hire | |

| Corporate/MICE Movements | |

| By Region | Jakarta |

| Java | |

| Sumatra | |

| Kalimantan | |

| Sulawesi | |

| Bali and Nusa Tenggara | |

| Papua and Maluku |

Key Questions Answered in the Report

How large is the Indonesia passenger car taxi sector in 2026 and how fast is it expanding?

The sector is valued at USD 4.82 billion in 2026 and is projected to grow at a 6.78% CAGR to reach USD 6.69 billion by 2031.

Which booking channel captures the majority of Indonesian taxi trips today?

Online platforms lead with 53.72% share in 2025 and are widening the gap as smartphone use and e-wallet adoption deepen.

What segment is set to post the quickest growth through 2031?

Ride-sharing bookings are forecast to rise at a 17.02% CAGR, outpacing ride-hailing and traditional street-hails.

How fast is electric-taxi deployment expected to accelerate?

Battery-electric taxis are projected to surge at a 43.64% CAGR from a 0.82% base, propelled by tax breaks and expanding charging networks.

Which region offers the fastest revenue upside for operators?

Bali and Nusa Tenggara are set to advance at an 8.01% CAGR thanks to tourism recovery and new infrastructure.

Page last updated on: