India Taxi Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

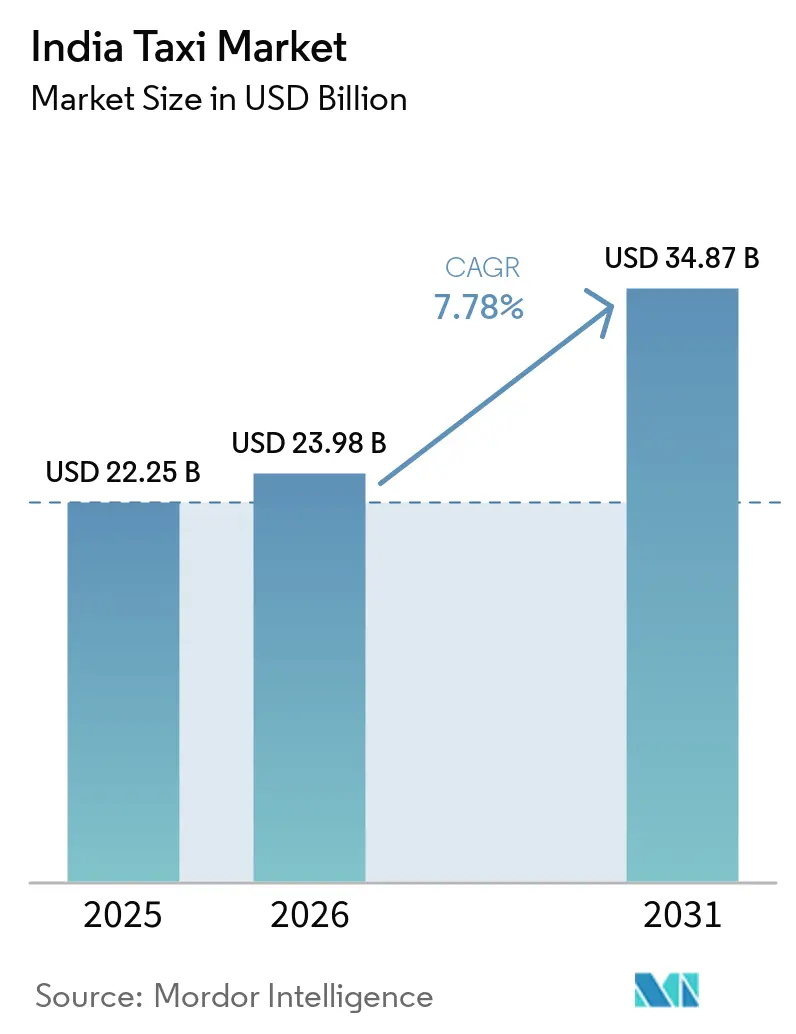

| Base Year Market Size (2025) | USD 22.25 Billion |

| Market Size (2026) | USD 23.98 Billion |

| Market Size (2031) | USD 34.87 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

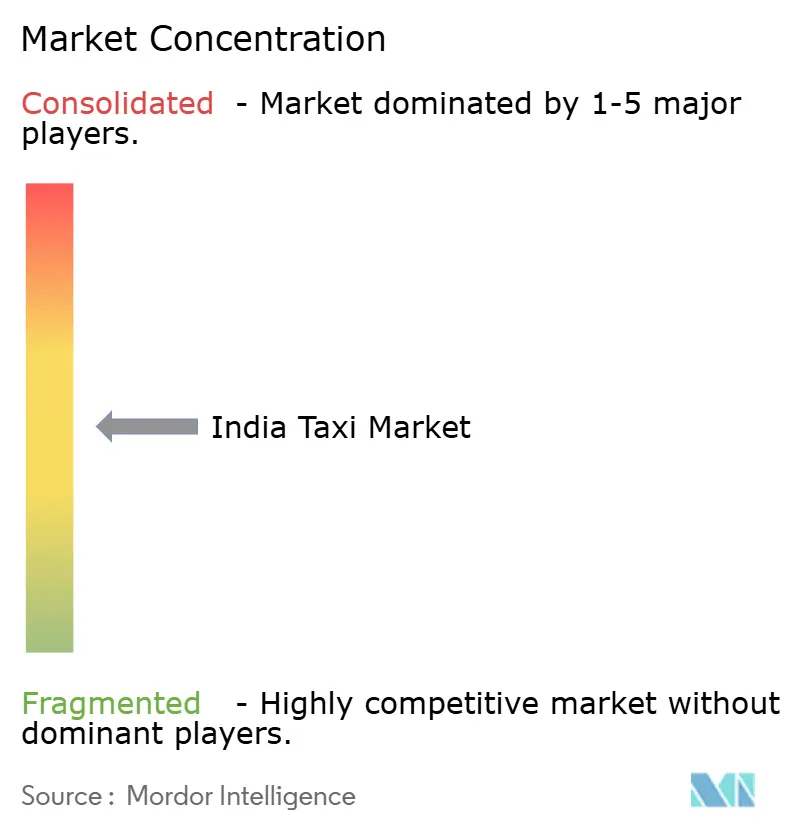

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Taxi Market Analysis by Mordor Intelligence

India Taxi Market size in 2026 is estimated at USD 23.98 billion, growing from 2025 value of USD 22.25 billion with 2031 projections showing USD 34.87 billion, growing at 7.78% CAGR over 2026-2031. Sharply rising smartphone adoption, UPI-enabled cashless transactions, and enabling regulations reinforce service accessibility, expand addressable demand, and attract new capital. Standardized fare policies under the Motor Vehicle Aggregator Guidelines 2025 improve price transparency and foster multi-modal integrations that keep churn low. Fleet electrification incentives, notably the Electric Mobility Promotion Scheme 2024, compress operating costs for two- and three-wheelers, spurring platforms to refresh vehicles quickly while preserving fare economics. Intensifying airport traffic, rising middle-class travel frequency, and tier-2 and tier-3 city urbanization create dependable pre-scheduled ride pools that help operators raise load factors. Tightening competition from subscription-fee cooperatives and specialized bike-taxi entrants promotes customer-centric pricing while forcing incumbents to expand safety technology and corporate mobility solutions.

Key Report Takeaways

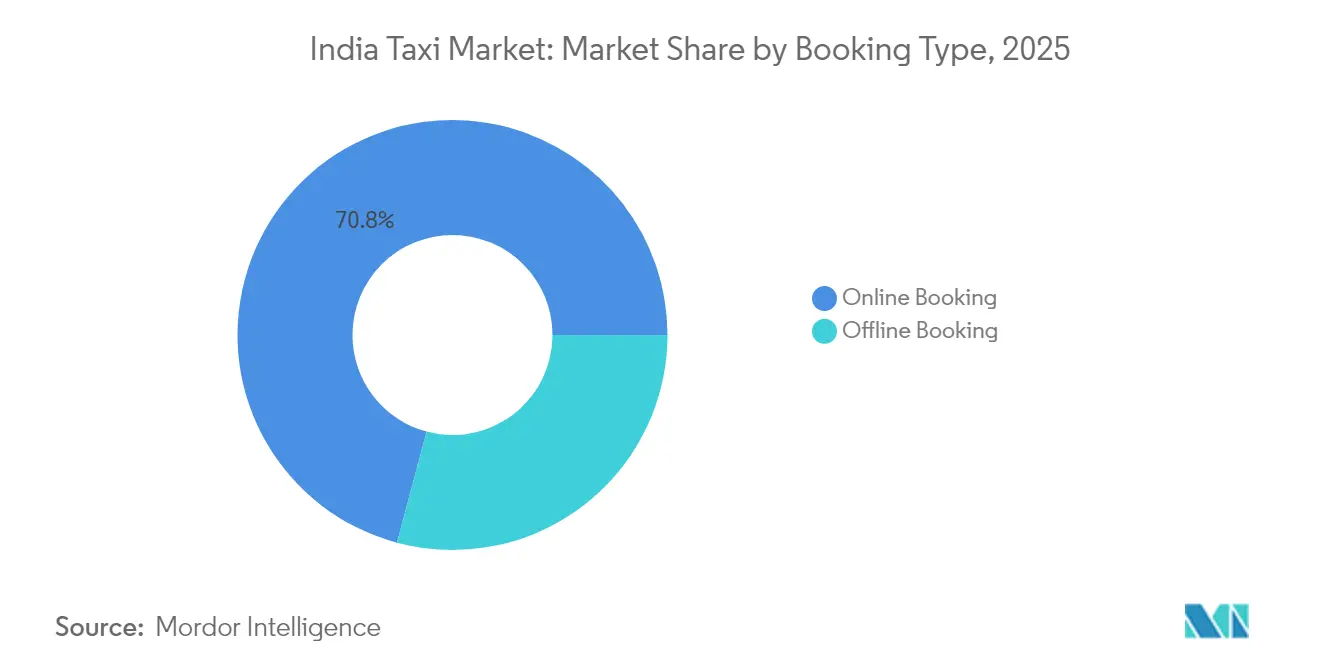

- By booking type, online channels retained 70.84% of the Indian taxi market share in 2025, and online booking is set to grow at a 7.80% CAGR to 2031.

- By service type, ride-hailing ruled with 65.10% of the Indian taxi market in 2025, and ride-sharing is forecast to post the fastest 7.98% CAGR through 2031.

- By vehicle type, passenger cars held 57.25% of the Indian taxi market share in 2025, while two-wheelers are predicted to deliver the quickest 7.83% CAGR over the outlook.

- By Propulsion Type, ICE fleets formed 83.72% of the Indian taxi market in 2025, yet electric taxis are on track for an 7.95% CAGR to 2031.

- By trip purpose, intra-city rides accounted for 60.75% of the Indian taxi market size in 2025, whereas airport transfers are projected to register an 7.90% CAGR through 2031.

- By customer segment, individual riders commanded 75.98% of the Indian taxi market in 2025, and corporate demand is expected to accelerate at a 7.84% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone Penetration | +1.8% | National, with metro concentration | Short term (≤ 2 years) |

| Urban Congestion | +1.5% | Tier-1 and Tier-2 cities | Long term (≥ 4 years) |

| Government EV Push | +1.2% | National, with Delhi and Maharashtra leading | Medium term (2-4 years) |

| Airport Traffic Boom | +0.9% | Major airport cities | Short term (≤ 2 years) |

| Cooperative/Tier-III Fleet Model Expansion | +0.7% | Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| AI-Based Mobility-As-A-Service Integrations | +0.6% | Metro cities initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smartphone Penetration & UPI-Enabled Digital Payments

UPI transaction volume grew exponentially in 2024, almost double the previous year's annual rise, which signals a permanent behavioral change in how riders pay for taxis[1]“UPI Product Statistics,” National Payments Corporation of India, npci.org.in . Millions of smartphone users already access ride apps, lowering cash dependence and enlarging target customer pools in tier-2 and tier-3 cities. Public transport systems mirror the adoption curve, as shown by Bangalore Metropolitan Transport Corporation collecting almost two-fifth of ticket revenue digitally in March 2025. Platforms adapt by piloting cash-only auto-rickshaw services that still employ in-app matching, confirming that digital contact does not always equal digital settlement. Biometric authentication and credit-linked UPI innovations further tighten security, encouraging corporate accounts to centralize travel spend under a single dashboard. As a result, the Indian taxi market leverages smoother booking funnels and better repeat ride conversion.

Urban Congestion & Less than 2% Private Car Ownership

Private car penetration remains minimal, and urban cores face daily congestion that stifles productivity. Tier-2 and tier-3 cities already generate three-fifths of GDP, see population densities soar, underpinning long-run dependence on shared mobility in the India taxi market. The UDAN regional airport scheme activated 625 routes serving multiple passengers, creating immediate last-mile taxi needs. Asset-light corporate mobility providers such as Ecos Mobility run 12,000 vehicles for 1,100 enterprises, validating subscription fleets as congestion countermeasures. Flexible work setups widen travel peaks across the day, so dynamic fleet allocation helps operators lift utilization while smoothing traffic loads

Government EV Push (FAME-II and State Policies)

The Electric Mobility Promotion Scheme 2024 is earmarked for e-2W and e-3W, incentivizing operators to shift high-utilization fleets into lower operating-cost electric formats[2]“Electric Mobility Promotion Scheme 2024,” Department of Heavy Industries, heavyindustries.gov.in . Delhi’s 2023 aggregator rules demand fleet electrification, spurring Amazon India to reach its target of EV commitment ahead of plan. Proposed FAME-III funding of INR 26,400 crore with tapered subsidies adds urgency to early adopters because grant amounts fall yearly. Maharashtra’s 2025 cab policy complements national programs by allowing higher fare ceilings for EVs, improving payback periods in dense corridors. Yet only 12,146 public chargers existed in 2024, so the need for 3.9 million points by 2030 frames a massive infrastructure revenue stream critical for the Indian taxi market expansion.

Airport Traffic Boom Powering Pre-Scheduled Rides

Domestic passenger traffic advanced in 2024, and future projections show an exponential increase in the number of flyers by 2037. Platforms capitalize through pre-book products; Uber Reserve logged double the annual growth with airport endpoints in two-fifths of trips. Evera Cabs disclosed that of all bookings linked to airport corridors, underscoring yield premiums in that lane. Government strategy targets 220 functioning airports by 2025, meaning new terminals will open recurring taxi lanes even in secondary cities. When BluSmart halted operations, ride-hailing rivals moved fast to fill airport supply gaps, showing how single-segment shocks redirect wallet share in the taxi market in India.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commission & Surge-Price Caps | -1.1% | National implementation with state variations | Short term (≤ 2 years) |

| High EV Total-Cost-Of-Ownership | -0.9% | National, with rural charging constraints | Long term (≥ 4 years) |

| Rider-Safety Issues | -0.8% | Metro cities with higher incident reporting | Medium term (2-4 years) |

| Regulatory Fragmentation Across Indian States | -0.7% | State boundaries with policy conflicts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commission & Surge-Price Caps

Regulatory ceilings restrict commissions to one-fifth of fare and limit surge multipliers to 2×, trimming peak-hour revenue potential. Driver associations claim that take rates nearly half persist in practice, leading to protests across Delhi in 2025 that disrupted service availability. Maharashtra now enforces minimal cancellation penalties on drivers and less than one-tenth on riders, applying Regional Transport Authority audits to contain side payments. With lower elasticity to pass through fuel spikes, operators pivot toward fixed-fee subscriptions that comply with caps yet stabilize driver income. Such shifts may blunt near-term margin expansion but could lift retention and support long-term growth in the India taxi market over time.

Rider Safety Issues & Driver Attrition

Karnataka’s 2024 bike-taxi ban removed up to lakhs of vehicles from Bengaluru streets after the spike in incidents. Uber responded with AI-verified helmet selfies and free safety kits, raising compliance costs and differentiating service quality. Attrition accelerates when earnings slide and safety worries rise, forcing platforms to increase incentive pools and insurance coverage. Variance in state rules, such as Maharashtra’s strict e-bike allowances versus Karnataka prohibitions, multiplies compliance complexity and deters fleet planning scale. Elevated expenses restrain growth even while high demand persists for the Indian taxi market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Uptake Strengthens

Online reservations accounted for 70.84% of the Indian taxi market in 2025 and are projected to expand at a 7.80% CAGR through 2031. Offline hail retains almost three-tenth, but its share keeps falling as smartphone literacy spreads in tier-2 corridors. The Taxi market in india size associated with online booking is poised to widen yearly because payments over UPI remain fee-free for riders and drivers.

The Open Network for Digital Commerce partnership lets platforms like Namma Yatri migrate toward subscription models that directly leave fare collections to riders and drivers, cutting aggregator commissions while preserving app visibility. Cooperatives under the new Sahkar Taxi program further shrink the middle-layer margin, though they still rely on app interfaces classified as digital booking in market definitions. Regulatory guidance is yet to harmonize data-sharing protocols, but the trajectory toward universal digital engagement appears locked in.

By Service Type: Shared Mobility Gains Speed

Ride-hailing produced 65.10% of the Indian taxi market revenue in 2025, while ride-sharing and car-pooling are expected to clock an 7.98% CAGR to 2031. Price-sensitive commuters choose shared trips during peak pricing windows because caps narrow the differential to solo rides.

State rules in Maharashtra formalize car-pool safety norms that boost female ridership confidence, helping share platforms retain loyalty. Corporate leasing and subscription fleets supply predictable monthly spend for employers that need last-mile shuttles in hybrid work models. As congestion continues, public policy encourages higher occupancy per vehicle, positioning ride-sharing to edge ride-hailing growth in the Indian taxi market.

By Vehicle Type: Two-Wheelers Advance Fast

Passenger cars contributed 57.25% of the Indian taxi market revenue in 2025, but two-wheelers are on track to grow at a 7.83% CAGR to 2031, due to the ministry advisory allowing motorcycles as contract carriages. The India taxi market size linked to bikes improves fleet utilization because riders accept shorter wait times and lower fares.

Rapido grew exponentially in 2025, operating up to five million bikes and reporting triple revenue growth, demonstrating investor belief in the format. Nonetheless, Bengaluru’s prohibition on bike taxis reveals how policy uncertainty can freeze regional rollouts. Operators deploying dual platforms for bikes and autos hedge against abrupt rule shifts and stabilize aggregate volume.

By Propulsion Type: Electric Shift Accelerates

ICE vehicles captured 83.72% of the Indian taxi market revenue in 2025, but electric variants are forecast for an 7.95% CAGR by 2031. The India taxi market share of EV rides climbs faster in metros where charging density rises and access fees remain low.

BluSmart, with electric sedans and proprietary hubs, illustrates the capital commitment needed when public chargers lag. Subsidy tapering under the draft FAME-III plan compresses payback periods, so operators race to procure before grants vanish. Battery-swap models for two-wheelers shorten downtime, letting fleets finish more daily trips and improving earnings resilience.

By Trip Purpose: Airport Transfers Outperform

Intra-city trips delivered 60.75% of the Indian taxi market revenue in 2025, while airport transfers are expected to progress at an 7.90% CAGR to 2031. The Indian taxi market observes premium per-kilometer yields on airport corridors because travelers value punctuality and luggage space.

Government plans for more airports by 2025 enhance route certainty and raise taxi lane allocations. Platforms deploy dedicated airport driver pools that pre-place vehicles at terminals, reducing idle cruising time and boosting CO2 efficiency. Outstation routes, notably Mumbai–Pune and Delhi–Agra, sustain elevated utilization on return legs, reinforcing multi-day driver earnings.

By Customer Segment: Corporate Accounts Climb

Individuals formed 75.98% of the Indian taxi market revenue in 2025, whereas corporate and institutional bookings are set for a 7.84% CAGR to 2031. Subscription contracts yield steady cash flows and often include bundled safety tech, attracting companies under new Occupational Safety mandates.

Ecos Mobility exemplifies asset-light execution by leasing vehicles yet owning minimal rolling stock, thereby sidestepping depreciation risk. As organizations decentralize offices, door-to-door employee shuttles become embedded in HR budgets, reinforcing structural demand for premium fleet categories within the Indian taxi market.

Geography Analysis

Metropolitan clusters dominate demand today, yet the Indian taxi market rapidly penetrates tier-2 and tier-3 cities that produce three-fifths of GDP while occupying just a fraction of land, fueling exponential growth in the urban population by 2036. Northern India leads policy-led electrification, with Delhi’s aggregator guidelines compelling platform fleets to adopt EVs sooner than the national timetable. Maharashtra sets fare norms that stabilize earnings and codify cancellation penalties, fostering trust among riders and drivers.

Southern states benefit from high-tech adoption; Bengaluru recorded nearly two-fifths of digital bus ticketing, illustrating readiness for app-based taxi payments. The western corridor's robust inter-city demand, especially the Mumbai–Pune route, ranks highest on Uber’s 2023 inter-city list. Eastern and northeastern corridors derive momentum from UDAN airstrip activations that extend taxi-addressable markets into tourism belts.

Regulatory fragmentation persists, with Karnataka’s bike-taxi ban juxtaposed against Maharashtra’s e-bike approval. Multi-state operators must modularize apps to comply with local fare tables, insurance requirements, and propulsion mandates. Uniform digital KYC standards would ease cross-border fleet dispatch and unlock smoother scaling for the Indian taxi market.

Competitive Landscape

Market concentration is moderate because Ola and Uber now jointly hold significant market share rather than the near-monopoly positions of previous years. Rapido claims notable growth in selected metros by harnessing bike-taxi collaborations and a subscription fee revenue model. Government-backed cooperatives, such as Sahkar Taxi, intensify rivalry by eliminating commissions, fortifying driver loyalty, and potentially lowering end-user fares.

Strategic moves include Uber’s early discussions to absorb BluSmart, seeking to augment electric sedan capacity after BluSmart’s April 2025 exit. Ola announced in-house AI chips for autonomous readiness by 2026, pledging complete electric conversion of three-wheeler and four-wheeler fleets. Namma Yatri raised USD 11 million in 2024 and eyes North American alliances with driver unions.

Airport lane disruptions, corporate shuttle procurement, and tier-3 city rollouts represent the next growth frontiers. Operators differentiate through safety AI, premium loyalty tiers, and open API integrations with metro rail passes. Complying with the Motor Vehicle Aggregator Guidelines 2025 demands investment in data logs, insurance cover, and fare disclosure dashboards, creating capital barriers for smaller firms yet raising trust for mass adoption across the Indian taxi market.

India Taxi Industry Leaders

Uber Technologies

ANI Technologies Private Limited (Ola Cabs)

Meru Cabs

Carzonrent India Pvt Ltd.

Savaari

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Ministry of Road Transport and Highways issued updated Motor Vehicle Aggregator Guidelines 2025, allowing surge pricing up to 2× base fare and imposing 10% driver-side cancellation penalties.

- May 2025: Maharashtra enacted the Aggregator Cabs Policy 2025, standardizing fares through Regional Transport Authority oversight and encouraging EV deployment.

- July 2024: Namma Yatri secured USD 11 million in pre-Series A funding, led by Blume Ventures and Antler with Google participation. The company outlines plans to enter the United States ride-sharing arena.

India Taxi Market Report Scope

The Indian taxi market refers to the industry within India's transportation sector that encompasses the various services providing point-to-point transportation through taxi vehicles. It can be used for single or multiple passengers, with the option of sharing or not sharing.

The scope of the India taxi market is segmented by booking type, service type, and vehicle type. By booking type, the market is segmented into online booking and offline booking. By service type, the market is segmented into ride-hailing and ride-sharing. By vehicle type, the market is segmented into motorcycles, cars, and other vehicle types (vans).

For each segment, market sizing and forecast have been done on the basis of value (USD).

| Online Booking |

| Offline Booking |

| Ride-Hailing |

| Ride-Sharing / Car-Pooling |

| Subscription & Corporate Leasing |

| Passenger Cars |

| Two-Wheelers |

| Three-Wheeler Auto-Rickshaws |

| Vans & MPVs |

| ICE (Petrol/Diesel/CNG) |

| Electric |

| Hybrid |

| Intra-city Point-to-Point |

| Airport Transfers |

| Outstation / Inter-city |

| Corporate Mobility |

| Individual Consumers |

| Corporate / Institutional |

| By Booking Type | Online Booking |

| Offline Booking | |

| By Service Type | Ride-Hailing |

| Ride-Sharing / Car-Pooling | |

| Subscription & Corporate Leasing | |

| By Vehicle Type | Passenger Cars |

| Two-Wheelers | |

| Three-Wheeler Auto-Rickshaws | |

| Vans & MPVs | |

| By Propulsion Type | ICE (Petrol/Diesel/CNG) |

| Electric | |

| Hybrid | |

| By Trip Purpose | Intra-city Point-to-Point |

| Airport Transfers | |

| Outstation / Inter-city | |

| Corporate Mobility | |

| By Customer Segment | Individual Consumers |

| Corporate / Institutional |

Key Questions Answered in the Report

What is the 2026 revenue value of the Indian taxi market?

The sector is valued at USD 23.98 billion in 2026.

How fast is the Indian taxi market expected to grow?

It is projected to register a 7.78% CAGR from 2026 to 2031.

Which booking channel leads volumes?

Online reservations captured 70.84% of rides in 2025 and remain ahead through 2031.

Why are electric taxis gaining ground?

EV incentives, subsidy tapering urgency, and lower operating costs support an 7.95% CAGR for electric fleets.

Which segment is the most promising for premium fares?

Airport transfers are forecast to rapidly advance at an 7.90% CAGR as domestic air travel scales.

How are cooperatives changing competition?

The Sahkar Taxi model removes aggregator commissions, boosting driver earnings and sharpening fare competition.

Page last updated on: