Nigeria Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

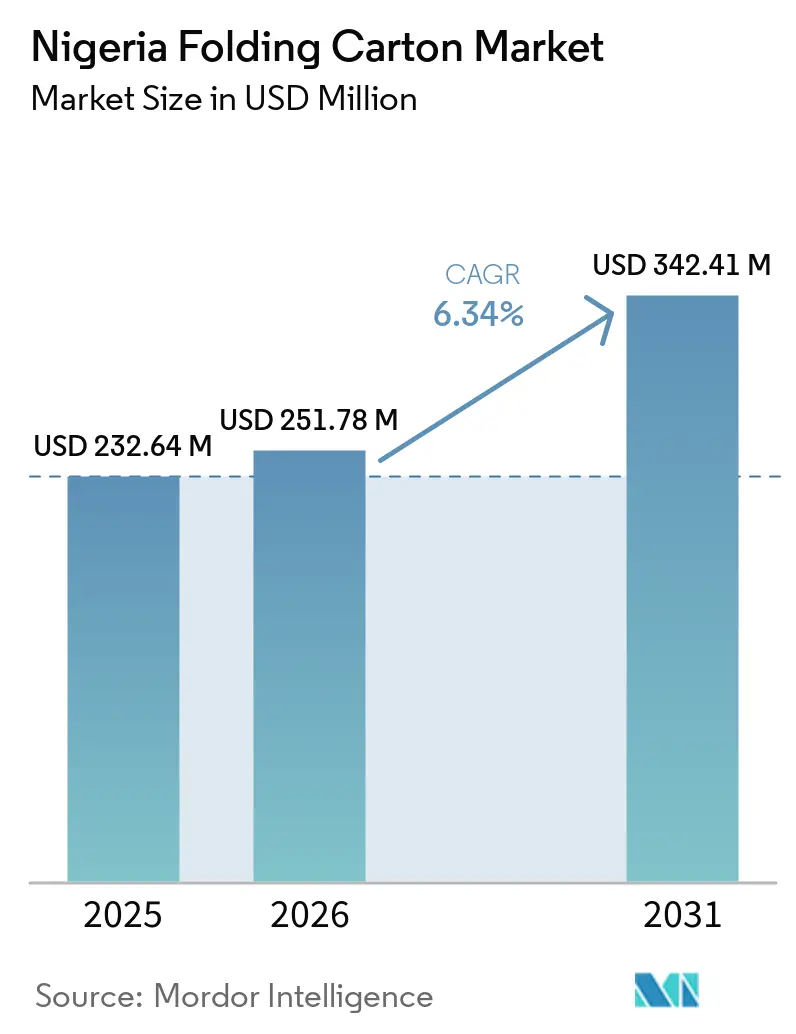

| Base Year Market Size (2025) | USD 232.64 Million |

| Market Size (2026) | USD 251.78 Million |

| Market Size (2031) | USD 342.41 Million |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

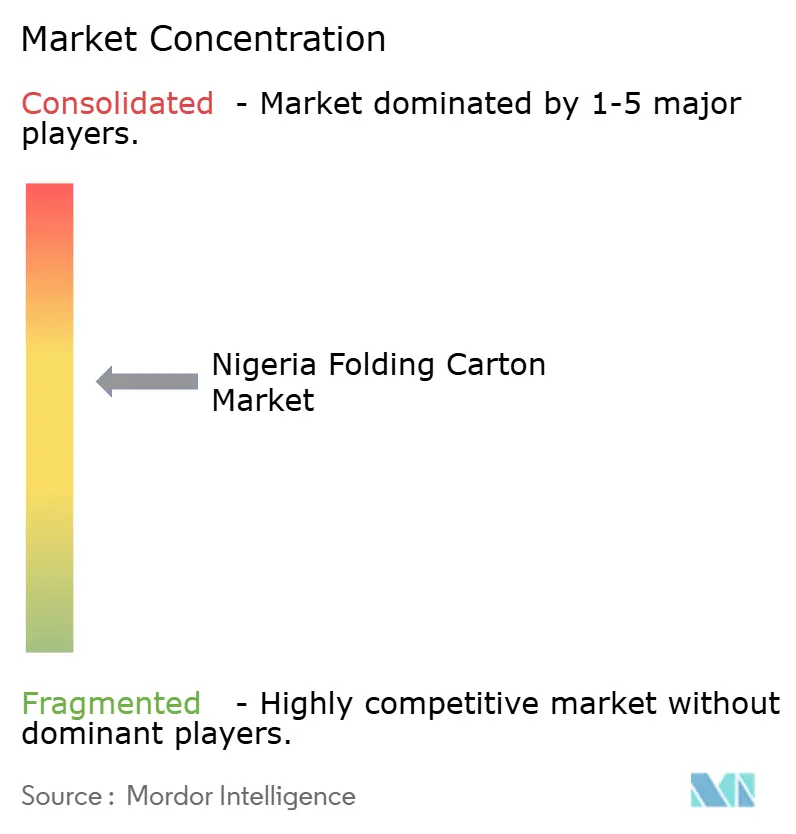

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Folding Carton Market Analysis by Mordor Intelligence

The Nigeria Folding Carton Market size is projected to expand from USD 232.64 million in 2025 and USD 251.78 million in 2026 to USD 342.41 million by 2031, registering a CAGR of 6.34% between 2026 to 2031. Regulatory pressure following Lagos State’s single-use plastic ban, together with a federal implementation committee launched in April 2026, is accelerating substitution toward fiber-based formats. Demand is also shifting geographically as e-commerce fulfillment matures in tier-2 cities where traditional retail remains thin, while premium brands in spirits, cosmetics, and pharmaceuticals adopt higher-grade boards that support anti-counterfeit graphics and barrier coatings. At the same time, grid instability pushes conversion costs higher because more than 60% of manufacturers rely on diesel or gas generators, creating a structural cost gap relative to imports. Pulp-price volatility, inadequate domestic recycling, and competition from flexible pouches round out a risk profile that keeps margins under pressure even as top-line growth remains healthy.

Key Report Takeaways

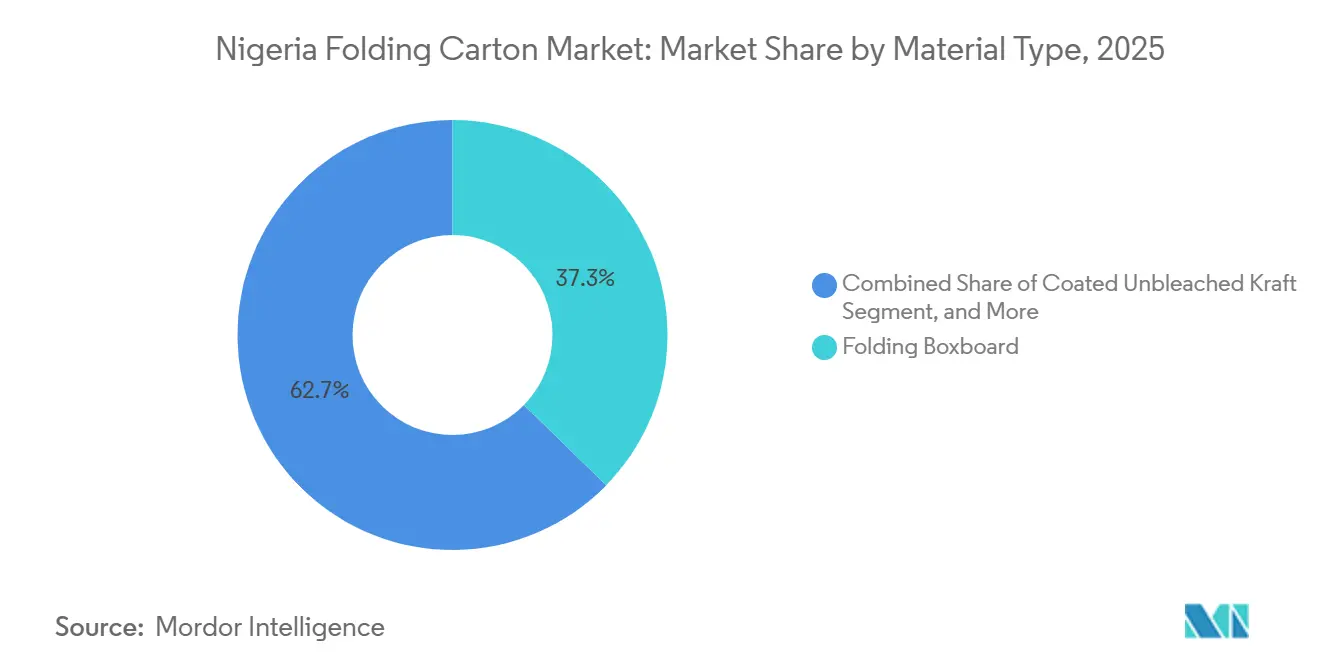

- By material type, folding boxboard captured with 37.32% of the Nigeria folding carton market share in 2025.

- By printing technology, the Nigeria folding carton market size for digital printing is projected to grow at a 8.77% CAGR to 2031.

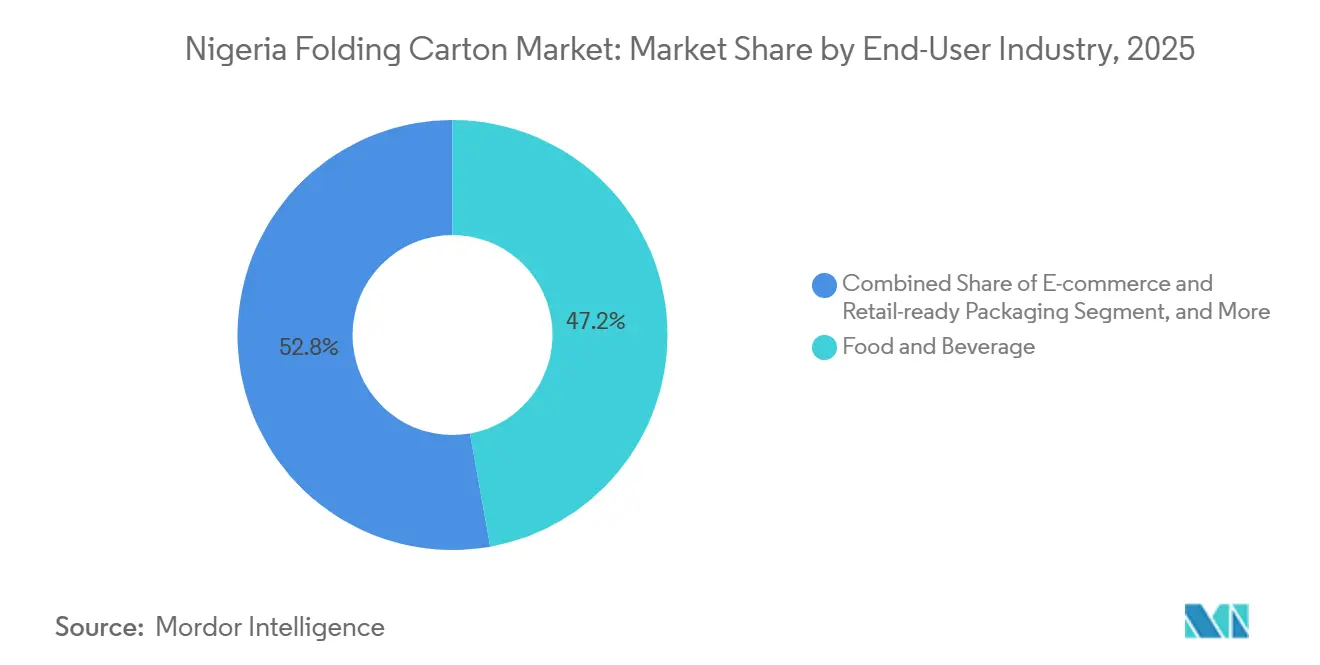

- By end-user industry, the food and beverage industry captured 47.19% of the Nigeria folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Ban on Single-Use Plastics Accelerating Substitution | +1.8% | National, early enforcement in Lagos State and federal offices | Short term (≤ 2 years) |

| Rising Demand for Eco-Friendly Packaging Solutions | +1.5% | National, highest uptake in Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Growth of Quick-Service Restaurants and Takeaway Culture | +1.2% | National, concentrated in Lagos, Abuja, tier-1 cities | Medium term (2-4 years) |

| Increasing Penetration of E-Commerce Fulfillment Centers in Tier-2 Cities | +1.0% | Ibadan, Kano, Enugu and other tier-2 locations | Medium term (2-4 years) |

| Expansion of Organized Retail Chains | +0.5% | Lagos, Abuja and selected tier-1 cities | Long term (≥ 4 years) |

| Local Brand Premiumization Creating Higher Graphics Requirements | +0.4% | National, premium demand clustering in Lagos and Abuja | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Ban on Single-Use Plastics Accelerating Substitution

Lagos enforced a single-use plastic ban on 1 July 2025, and a federal committee formed in April 2026 to coordinate nationwide rollout, prompting public agencies and quick-service restaurants to shift procurement toward recyclable folding cartons faster than converters initially forecast. Federal offices had already barred single-use plastics in August 2024, creating a demonstration effect that shaped state-level policies. The National Environmental Standards and Regulations Enforcement Agency has partnered with the Global Environment Facility to fund circular-economy pilots, while expected extended producer responsibility rules targeting 25% recycled content by 2029 increase the urgency for fiber-based secondary packaging. Converter capacity is now strained, especially on lithographic lines operating near peak utilization, giving flexographic and digital players an opening to gain share. As a result, order lead times for premium folding cartons shortened from 12 weeks in 2024 to roughly six weeks in 2026, underscoring the pace of substitution.

Rising Demand for Eco-Friendly Packaging Solutions

A 2024 academic survey in Akwa Ibom State showed that sustainable-packaging attributes significantly influence consumer brand choice, a trend most visible among urban middle-class households exposed to global environmental narratives. Tetra Pak’s collaboration with WeCyclers in Lagos demonstrates how multinationals integrate recycling into brand positioning even though the national recycling rate is only 2%. The company’s EUR 60 million (USD 67.8 million) investment in paper-based barrier technology, with a pilot line scheduled for early 2027, signals a long-term pivot away from aluminum-foil laminates. Spirits producers tapped into this sentiment by relaunching their BEST portfolio with fully recyclable glass and cartons in October 2025 and April 2026. Gross margins in premium cartons reach 40-60%, compared with 10-15% for commodity grades, encouraging converters to invest in digital presses and specialty coatings that support sustainable, high-graphic packs.

Growth of Quick-Service Restaurants and Takeaway Culture

The overlap of Ramadan and Lent in 2026 compressed mealtimes and sparked a surge in takeaway orders, further entrenching the quick-service model. Courier revenues climbed 56.28% year-on-year to NGN 248.14 billion (USD 155.1 million) in the first nine months of 2025, confirming the scale of off-premise consumption. Nightlife spending during Lagos’s “Detty December” season surpassed NGN 4.3 billion (USD 2.7 million) in 2025, and many clubs insisted on branded carton packs that double as advertising when carried through the city’s streets. Suppliers such as DW Packs report unit prices of NGN 150-350 (USD 0.09-0.22), making cartons competitive with flexible pouches for moderate portion sizes. The robustness of food service demand cushions converters against fluctuations in organized retail, where supermarket chain restructuring has introduced uncertainty.

Increasing Penetration of E-Commerce Fulfillment Centers in Tier-2 Cities

Jumia disclosed that 49% of deliveries now terminate in rural areas compared with 35% to primary cities, reflecting 357 pickup stations, 67 logistics partners, and more than 32,000 JForce agents who bridge last-mile gaps. Tier-2 cities benefit from lower real-estate costs and growing populations underserved by traditional retail, making them prime targets for converter investment. Pharmaceutical firms whose revenue jumped 56.8% to NGN 117.6 billion (USD 73.5 million) in 2024 use the platform to distribute blister-packed over-the-counter products nested inside folding cartons compliant with the National Agency for Food and Drug Administration and Control labeling rules. The federal import ban on bottled water, corrugated cartons, and glass bottles, effective 1 April 2026, intensifies localization and motivates converters to establish plants closer to these fast-growing consumption zones. As a result, Ibadan, Kano, and Enugu have emerged as preferred destinations for greenfield projects that serve both e-commerce and wholesale channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power Supply Instability Raising Conversion Costs | -1.2% | National, most acute in Lagos, Kano, and Ogun State | Short term (≤ 2 years) |

| Volatility in Imported Pulp Prices | -0.9% | Nationwide, affecting converters reliant on virgin fiber imports | Medium term (2-4 years) |

| Inadequate Domestic Recycling Infrastructure | -0.5% | National, Lagos, and Abuja have slightly better collection rates | Long term (≥ 4 years) |

| Competition From Flexible Pouches in Sachet-Dominant Segments | -0.4% | Rural and low-income urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power Supply Instability Raising Conversion Costs

More than 60% of Nigerian manufacturers operate off-grid, driving self-generated energy to roughly 40% of total production expense and undermining price competitiveness against imports. Grid collapses occurred three times within a 30-day window straddling December 2025 and January 2026, while Band A tariffs reached NGN 209.50 (USD 0.13) per kWh, pushing converters toward diesel or gas generators despite fuel prices that rose 167% after subsidy removal. The Manufacturers Association of Nigeria reported NGN 676.6 billion (USD 423.1 million) in energy spending during the first half of 2025 alone.[1]The Guardian Nigeria, “Manufacturers Spend N676.6bn on Energy in H1 2025,” guardian.ng Printbox Nigeria’s January 2026 flexographic plant includes redundant power systems, which are inflating capital costs and lengthening payback periods. Smaller converters struggle to fund similar upgrades, limiting the adoption of energy-efficient digital printing that could reduce overall exposure.

Volatility In Imported Pulp Prices

Nigeria sources most virgin fiber abroad, making pulp purchases sensitive to foreign-exchange swings that saw the naira depreciate about 40% in 2024. Converters have limited hedging tools because local derivatives markets remain shallow, forcing them to absorb margin pressure or pass costs to customers who may switch to flexible pouches with lower material intensity. The April 2026 import ban on corrugated cartons removes a safety valve that once allowed buyers to offset pulp inflation by importing finished packs, aggravating cost stress during price spikes. Domestic recycled fiber is scarce; the national recycling rate stands at 2%, and Lagos still falls below 10%, so converters cannot easily substitute away from virgin inputs. While Polysmart’s 100,000-tonne recycling plant, being commissioned through July 2026, addresses polyethylene terephthalate streams, it offers little immediate relief to the paperboard supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Premium Substrates Gain Share Despite Cost Headwinds

Solid bleached sulfate is projected to outpace the Nigerian folding carton market for substrates, expanding at an 8.13% CAGR through 2031 as pharmaceutical and premium-cosmetic brands demand printability, barrier performance, and tamper-evidence. Folding boxboard retained 37.32% revenue in 2025 because its stiffness-to-cost ratio remains attractive to food, beverage, and personal-care brands. Specialty players leverage digital presses to monetize 40-60% gross margins on premium jobs, while commodity converters depend on scale to counter foreign-exchange-driven pulp inflation.

Adoption of coated unbleached kraft and white-line chipboard is limited to niche industrial or price-sensitive segments, partly because Nigeria’s 2% recycling rate restricts consistent post-consumer fiber supply. Tetra Pak’s USD 67.8 million investment in barrier technology could eventually pull solid bleached sulfate into beverage applications previously dominated by foil-based laminates.[2]Tetra Pak, “Paper-Based Barrier Technology Investment,” tetrapak.com Spirits producers validated premium trends with a 100% recyclable redesign of the BEST line in 2025-2026, absorbing a 15-20% price premium over folding boxboard.

By Printing Technology: Digital Adoption Gains Momentum

Lithography controlled 42.83% of 2025 revenue owing to superior color fidelity and economies of scale beyond 10,000 impressions, yet digital presses are growing fastest at an 8.77% CAGR. Brands chasing limited-edition stock-keeping units for events such as “Detty December” use digital workflows to personalize graphics and add anti-counterfeit QR codes without plate costs. The Nigeria folding carton market share for digital output remains concentrated in Lagos and Abuja, where electricity access and operator skills are relatively higher.

Flexography, promoted at a 2025 executive seminar as 60% the cost of offset, attracts mid-market clients seeking water-based plates with lower regulatory burdens. Printbox Nigeria’s hybrid plant combines KBA offset and 8-color ultraviolet flexo to fine-tune job allocation, mitigating downtime caused by unstable grid power. Gravure persists in ultra-high-volume cigarette packs, while screen and letterpress serve specialty roles. As energy prices rise, digital’s lower kilowatt-hour footprint improves its economics, but widespread adoption hinges on finance options for capital-hungry equipment.

By End-User Industry: E-Commerce Redraws Demand Patterns

Food and beverage applications accounted for 47.19% of 2025 revenue, supported by quick-service and takeaway chains that leaned on folding cartons during the Ramadan-Lent overlap. Yet e-commerce and retail-ready packs will post an 8.56% CAGR, surpassing the overall Nigerian folding carton market's growth momentum, as Jumia channels 49% of parcels to rural destinations through a dense agent network. Healthcare and pharmaceuticals accelerate carton uptake to meet National Agency for Food and Drug Administration and Control labeling mandates, while personal care brands embrace premium graphics and recyclable boards to signal quality differentiation.

Electronics, industrial goods, and tobacco demand track macro conditions, though inflation at 23.71% in April 2025 and fuel costs up 167% strain discretionary spend. The April 2026 import ban on bottled water, corrugated cartons, and glass bottles forces rapid localization of secondary packaging, lifting near-term converter utilization. Capital expenditure by nine major fast-moving consumer-goods firms more than doubled to NGN 476.76 billion (USD 298.6 million) in 2025, underscoring confidence in domestic folding carton supply chains despite energy headwinds.

Geography Analysis

Lagos State remained the epicenter of the Nigerian folding carton market in 2025, backed by dense manufacturing clusters, organized retail, and early enforcement of the single-use plastic ban. Despite a recycling rate still below 10%, Lagos outperforms the national average of 2%, yet converters in the state grapple with grid failures that erode margins. Abuja follows as a pharmaceuticals and government-procurement hub, but 54% of its plastic waste remains unmanaged, compelling buyers to source cartons from Lagos at higher freight costs.

Ogun State leverages its proximity to the Apapa and Tin Can Island ports, streamlining the import of virgin pulp for converters in its industrial corridors. Kano serves the Sahelian corridor’s food-and-beverage trade, though power instability and security concerns temper capacity additions. The Nigeria folding carton market size in tier-2 cities such as Ibadan, Enugu, and Port Harcourt is expanding faster than in Lagos as Jumia’s network of 357 pickup stations reduces last-mile friction.

Graphic Packaging’s Ibadan plant positions the firm to tap southwestern demand while exporting to Benin and Togo, validating a multiregional footprint strategy.[3]Graphic Packaging, “Annual Report,” graphicpkg.com Federal bans on select packaging imports and the nationwide plastics committee, inaugurated in April 2026, level the regulatory playing field across states, giving early-movers in tier 2 a competitive edge. Access to cassava-based adhesives and lower land costs further incentivize capacity investments outside the commercial capital.

Competitive Landscape

The Nigeria folding carton market is moderately fragmented, with international firms such as Graphic Packaging, Mayr-Melnhof Karton, and Huhtamaki serving premium niches, while domestic players, including Printbox Nigeria, Nova Packaging, and Zenith Packaging, compete on speed, proximity, and resilience to power disruptions. Tetra Pak maintains a Lagos commercial office and recycles through WeCyclers, but considers local aseptic carton production uneconomical until volumes triple.

Polysmart’s USD 60 million recycling facility augments the supply of extended-producer-responsibility-compliant polyethylene terephthalate, signaling vertical integration plays that could spill into paper fiber in the long term. Strategic themes emphasize captive power generation. 20 major firms installed 1,045 MW of self-generation capacity between January and September 2025 to mitigate grid failures.

Quality management and traceability are becoming increasingly important as multinational brands demand ISO 9001, 14001, and 45001 certifications; Printbox Nigeria’s new plant meets these standards, creating a barrier for smaller shops.[4]Printbox Nigeria, “Facility Information,” printboxnigeria.com Flexographic entrants exploit lower setup costs to attack mid-volume segments ignored by lithographic incumbents, while adjacent flexible-packaging giants such as Dangote Packaging hint at diversification if pulp-price volatility narrows the cost gap.

Nigeria Folding Carton Industry Leaders

Graphic Packaging Holding Company

Tetra Pak International SA

Nova Packaging Nigeria Ltd.

sonnex packaging nigeria ltd

Mayr-Melnhof Karton AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The federal government inaugurated a committee to implement a nationwide single-use plastic ban, extending Lagos’s July 2025 policy.

- April 2026: Imports of bottled water, corrugated cartons, and glass bottles above specified thresholds were banned, accelerating localization.

- March 2026: Polysmart began commissioning a 100,000-tonne recycling plant after raising NGN 13 billion (USD 8.1 million) in commercial paper.

- January 2026: Printbox Nigeria opened a 4,500 m² flexographic plant in Lagos with 7.2 million m annual capacity and ISO triple certification.

Nigeria Folding Carton Market Report Scope

The scope of this report covers the analysis of the folding carton market in Nigeria. Folding cartons are paper-based packaging solutions widely used across various industries, including food and beverage, personal care, pharmaceuticals, and others. These cartons are lightweight, customizable, and recyclable, making them a preferred choice for sustainable packaging. The report examines market trends, growth drivers, challenges, and opportunities, providing insights into the current market dynamics and future prospects.

The Nigeria Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and projected size of the Nigeria folding carton market?

The Nigeria Folding Carton Market size is projected to expand from USD 232.64 million in 2025 and USD 251.78 million in 2026 to USD 342.41 million by 2031, registering a CAGR of 6.34% between 2026 to 2031.

How is the single-use plastic ban influencing packaging demand?

Lagos’s 2025 ban and a federal rollout beginning 2026 are accelerating shifts from plastic to recyclable folding cartons, lifting converter order books for food service, retail, and e-commerce formats.

Which substrate is growing fastest within folding cartons?

Solid bleached sulfate is forecast to expand at an 8.13% CAGR through 2031, driven by pharmaceutical and premium-cosmetic requirements for high-barrier, high-graphic packaging.

Why is digital printing gaining ground in Nigeria’s carton sector?

Brand owners favor digital presses for variable data, anti-counterfeit features, and short runs that support frequent promotions, making it the fastest-growing technology at an 8.77% CAGR.

How do power challenges affect carton converters?

More than 60% of manufacturers rely on captive power, and self-generated electricity absorbs about 40% of production cost, eroding competitiveness against imports and slowing technology upgrades.

Which regions are emerging growth hotspots beyond Lagos?

Tier-2 cities such as Ibadan, Kano, and Enugu are attracting investment as e-commerce networks deepen and real-estate costs remain lower than in Lagos or Abuja.

Page last updated on: