Thailand Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

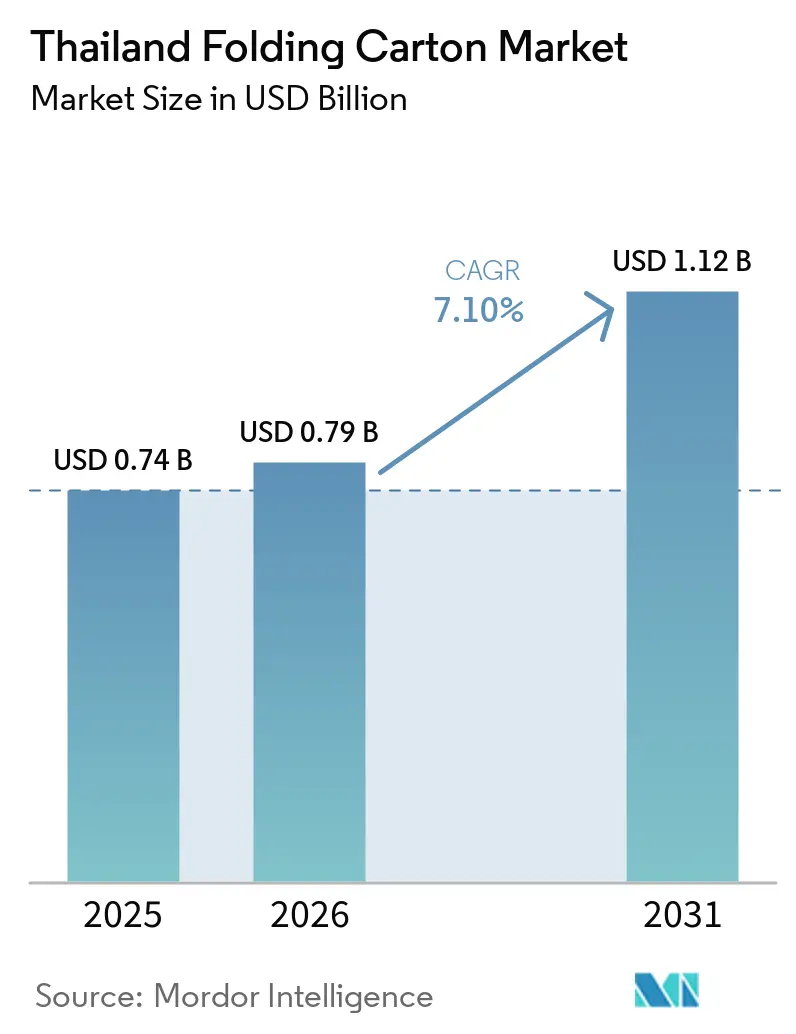

| Base Year Market Size (2025) | USD 0.74 Billion |

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

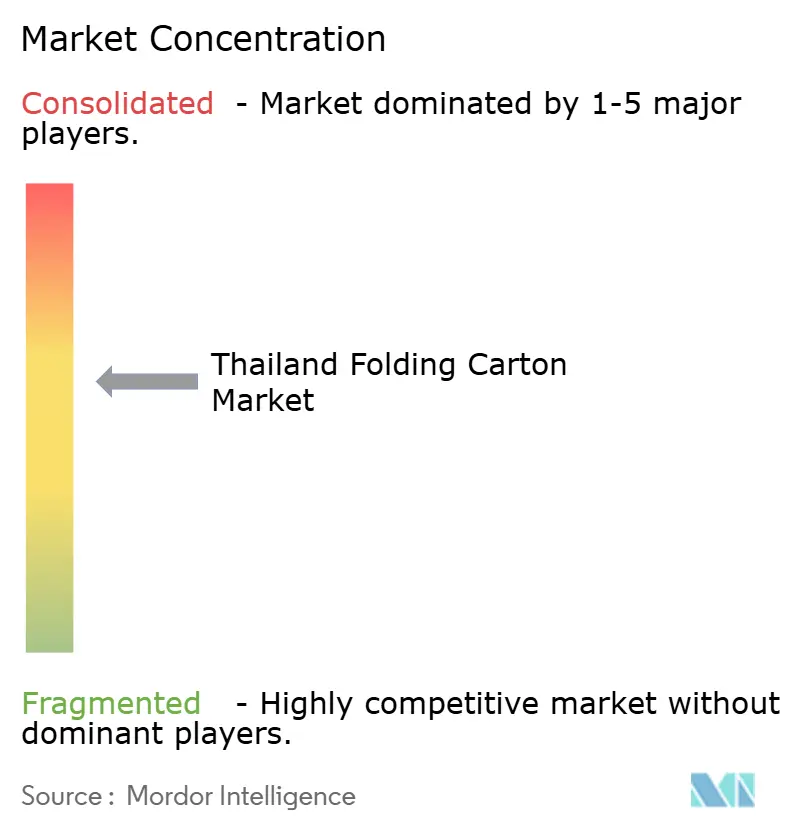

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Folding Carton Market Analysis by Mordor Intelligence

The Thailand folding carton market size was valued at USD 0.74 billion in 2025 and estimated to grow from USD 0.79 billion in 2026 to reach USD 1.12 billion by 2031, at a CAGR of 7.10% during the forecast period (2026-2031). Strong momentum comes from the nation’s role as a regional food-processing hub and from rapid digital commerce growth, both of which require high-graphic, shelf-ready carton that protect products in transit and stand out at retail. Brand owners are leaning on premium substrates and variable printing to meet global labeling rules while signaling quality to domestic shoppers. Converters are adding digital workflows, micro-flute laminators, and inline inspection to keep pace with shorter runs and traceability demands, even as pulp price volatility and labor shortages push operating costs higher. New environmental rules on per- and polyfluoroalkyl substances are expected to narrow the cost gap between recyclable paperboard and flexible plastic, tilting buying decisions toward the Thailand folding carton market.

Key Report Takeaways

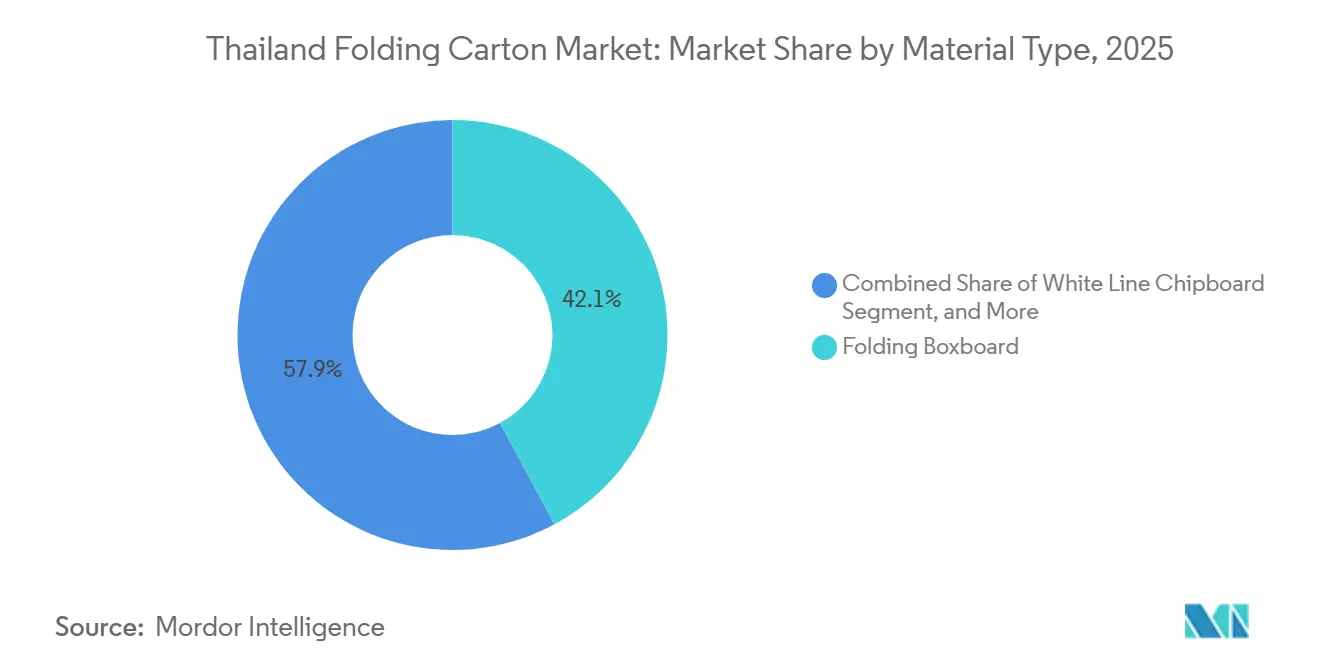

- By material type, folding boxboard captured 42.13% of the Thailand folding carton market share in 2025.

- By printing technology, the Thailand folding carton market size for the digital printing segment is forecast to advance at a 9.14% CAGR through 2031.

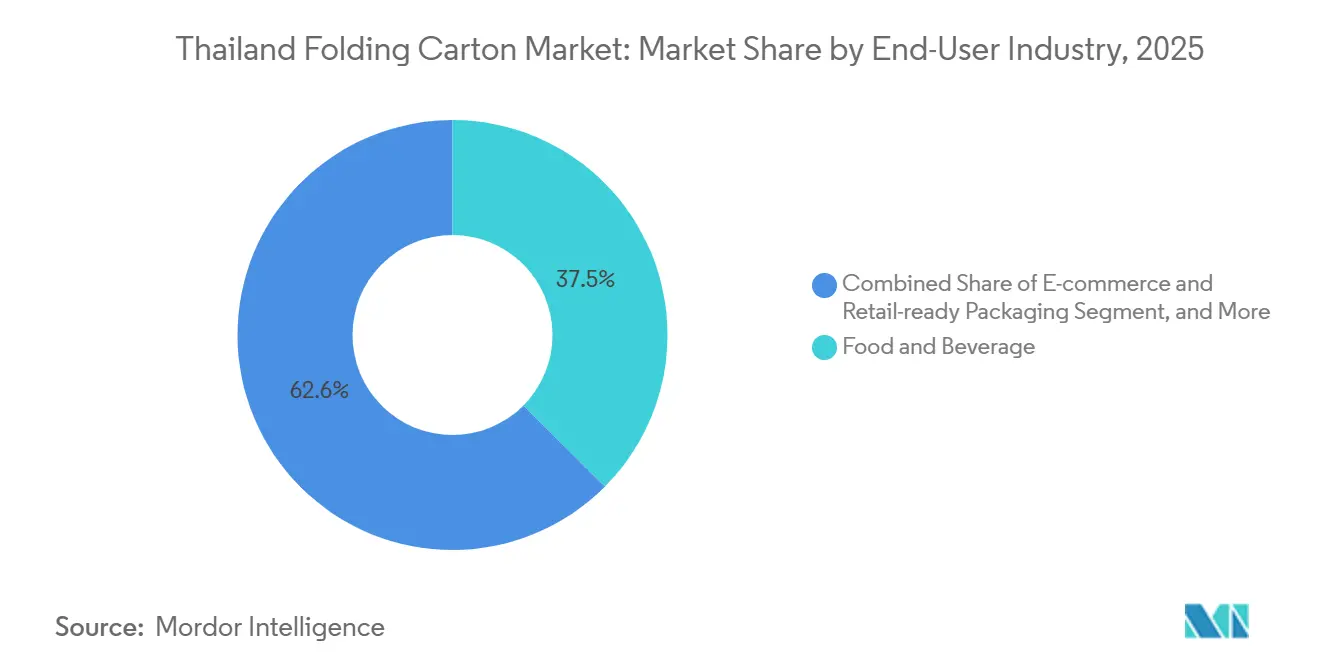

- By end-user industry, food and beverage captured 37.45% of the Thailand folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Thailand's Food And Beverage Processing Industry | +2.1% | National, concentrated in Greater Bangkok, Chonburi, Rayong, Ayutthaya | Medium term (2-4 years) |

| Booming E-Commerce Demand For Shelf-Ready Packaging | +1.8% | National, highest in Bangkok Metropolitan Region and provincial capitals | Short term (≤ 2 years) |

| Growing Consumer Preference For Sustainable And Recyclable Packaging | +1.4% | National, premium urban segments adopting early | Medium term (2-4 years) |

| Rising Urban Middle-Class Consumption Of Packaged Goods | +1.2% | National, faster in Chiang Mai, Khon Kaen, Hat Yai | Long term (≥ 4 years) |

| Government Incentives For SMEs Adopting Digital Printing In Packaging | +0.9% | National, uptake in Bangkok and Eastern Seaboard | Short term (≤ 2 years) |

| Increasing Adoption Of QR-Coded Carton For Track And Trace In Pharmaceuticals | +0.7% | National, mandate phasing in 2025-2027 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Thailand’s Food and Beverage Processing Industry

Food and beverage exports reached USD 50.9 billion in 2024, cementing the country’s top-ten global food exporter ranking.[1]Foreign Agricultural Service, “Thailand: Food Processing Ingredients,” fas.usda.gov Production of ready-to-eat meals is growing by 2.3% to 3.3% each year as tourism rebounds and dual-income households demand convenience.[2]Krungsri Research, “Thailand E-Commerce and Ready-to-Eat Market Outlook,” krungsri.com Instant noodle and chilled-meal brands are switching from shrink-wrapped trays to QR-enabled folding carton that support the Thai Food and Drug Administration e-labeling system. Kasikorn Research estimates eco-friendly food packaging spend at up to THB 16 billion (USD 458 million) by 2025, indicating a willingness to pay more for recyclable substrates. This premiumization favors solid bleached sulfate, which maintains integrity in refrigerated chains better than white-line chipboard.

Booming E Commerce Demand for Shelf-Ready Packaging

The national e-commerce sector is on track to reach USD 32 billion in 2025, with mobile sales accounting for over 80% of transactions. Online fulfillment uses carton as both protective shippers and instant shelf displays when goods are returned or cross-docked. Converters integrate perforated tear strips, crash-lock bottoms, and auto-lock features that cut warehouse labor while surviving last-mile bumps. The Thai Printing Association reports SMEs flocking to digital presses that handle 500-unit runs without plates, unlocking regional promotions and influencer tie-ins. Inline inspection now checks code readability at 15,000 sheets per hour, meeting platform mandates for tamper-evidence and scan accuracy.

Growing Consumer Preference for Sustainable and Recyclable Packaging

A 2024 survey found that 78% of Thai consumers would pay more for recyclable packaging and that 65% actively research a brand’s environmental footprint. Charoen Pokphand Group declared that 99.9% of its packaging is now reusable, recyclable, or compostable and has directed suppliers to report Scope 3 carbon emissions by 2027. SCG Packaging collected 3.8 million tons of recovered paper at 99 regional centers in 2025, feeding mills, and reducing virgin pulp exposure. Draft extended producer responsibility rules, expected in 2027, will place collection targets on brand owners and reward converters with FSC or PEFC chain-of-custody certification. Non-certified suppliers face margin pressure as procurement shifts toward documented sustainability.

Rising Urban Middle Class Consumption of Packaged Goods

Urbanization reached 54% in 2025, and incomes in secondary cities now outpace those in Bangkok. Shoppers are moving from bulk wet-market buys to branded packs in modern trade, driving demand for carton that differentiate on crowded shelves. Health-conscious consumers are driving demand for organic snacks, plant-based proteins, and functional drinks that need impactful graphics to showcase certifications. Ready-to-eat meals are expanding as dual-income lifestyles shorten cooking time, and converters are responding with UV coatings, soft-touch laminates, and augmented-reality triggers that link to recipe videos. Cosmetics and personal care remain the peak of premiumization, with carton costs at times exceeding product manufacturing expenses, positioning the Thailand folding carton market as a branding platform.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Virgin Pulp Prices | -1.3% | National, linked to global pulp and freight markets | Short term (≤ 2 years) |

| Competitive Pressure From Flexible Plastic Packaging | -1.1% | National, greatest in dry snacks, single-serve beverages, pet food | Medium term (2-4 years) |

| Shortage Of Skilled Prepress Technicians For High-Color Jobs | -0.6% | National, acute in Greater Bangkok and Eastern Seaboard | Medium term (2-4 years) |

| Stringent Limits On Ink Migration For Food Contact Surfaces | -0.5% | National, tied to Thai Industrial Standards and Ministry of Public Health rules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Pulp Prices

Spot paperboard prices jumped from USD 905 per tonne in Q1 2025 to USD 1,145 per tonne in Q2, a 26% leap caused by energy hikes at Scandinavian mills and reduced recovered-paper flow from China.[3]Fastmarkets RISI, “Southeast Asia Paperboard Price Report Q1-Q2 2025,” risiinfo.com Thailand relies on imports for 60% of its virgin pulp, exposing converters to currency and freight swings. Smaller firms without hedging tools must either pass costs within six weeks or absorb margin hits. SCG Packaging lifted alternative-fuel use to 39% of its energy mix in 2025 and captured 3.8 million tonnes of recovered fiber, containing input inflation. Non-integrated converters are structurally vulnerable, prompting consolidation and cross-border mergers that secure fiber and smooth cost curves.

Competitive Pressure from Flexible Plastic Packaging

Flexible pouches cut material costs by up to 30% and freight by 25%, winning dry snack and single-serve beverage slots. Stand-up pouches with zippers are popular, yet regulatory winds are shifting. The Ministry of Public Health proposed PFAS limits of 25 ppb per compound and 250 ppb cumulative, a move likely to force costly reformulations in multilayer films.[4]SGS, “Thailand Food Contact Packaging Regulations,” sgs.com As consumers pay premiums for recyclability, carton gain ground, supported by crash-lock forms that assemble faster and by digital serial numbers that beat flexo lead times. Carton converters use these levers to defend share and grow the Thailand folding carton market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type - Solid Bleached Sulfate Gains on Premium Positioning

The segment captured 42.13% of 2025 revenue through folding boxboard, a cost-efficient solution for cereal and instant noodles. Solid bleached sulfate is tracking an 8.90% CAGR to 2031, almost three points ahead of folding boxboard, because cosmetics and pharma brands need virgin fiber for migration compliance and vivid graphics. Coated unbleached kraft is used for durable goods where tensile strength outweighs color range. White line chipboard maintains a foothold in low-margin displays but faces looming bisphenol A non-detection rules that threaten its direct food contact eligibility.

SCG Packaging directed THB 2,450 million (USD 70 million) toward a 75,000-tonne-per-year expansion targeting premium food and pharma grades. Hybrid micro-flute laminates combine cushioning and printability, making them ideal for e-commerce journeys with multiple handling points. Thai Industrial Standards TIS 2948-2562 and TIS 3438-2565 set strict migration caps for phthalates and heavy metals, effective June 2026, nudging brand owners toward virgin fiber and enlarging the Thailand folding carton market.

By Printing Technology - Digital Printing Unlocks Batch-of-One Economics

Lithography held 48.71% revenue share in 2025 because it offers unbeatable per-unit cost on runs above 10,000 sheets. Digital printing is forecast to grow at a 9.14% CAGR to 2031, driven by a 200% tax deduction on digital transformation spending capped at THB 300,000 (USD 8,600) through December 2027. Flexography stays in corrugated volumes, while gravure clings to ultra-long cigarette runs. Digital’s surge mirrors limited-edition launches that require 500-sheet quantities, which are impossible on offset without plate waste.

The Thai Printing Association reports that operators are being retrained in raster image processing and variable data. Shrinkflex spent THB 188.6 million (USD 5.4 million) on flexo lines aimed at SMEs, revealing the pressure traditional technologies feel. E-commerce firms require serialized QR codes at press speed, a native function for inkjet heads, whereas offset needs separate units that slow output. New Board of Investment incentives for AI and robotics, including five-year tax holidays, will further accelerate digital adoption and lift the Thai folding carton market.

By End-User Industry - E Commerce Reshapes Carton Functionality

Food and beverage accounted for 37.45% of revenue in 2025, anchored by Thailand’s USD 50.9 billion food-export engine, which uses high-barrier carton with multilingual graphics. E-commerce and retail-ready packs are projected to grow at a 9.18% CAGR through 2031, as direct-to-consumer fulfillment requires carton that withstand the rigors of parcel networks and then double as shelf displays when goods re-enter brick-and-mortar channels. Healthcare and pharmaceuticals require tamper-evident carton bearing serialized QR codes that comply with the Medical Device Act B.E. 2568, lifting demand for inline vision systems that verify DataMatrix accuracy at full press speed. Personal care and cosmetics buyers favor soft-touch laminates and foil stamping that reinforce premium positioning, and converters are responding with single-pass digital presses that swap SKUs within minutes to meet short promotion windows. Electrical and electronics brands specify anti-static coatings and cushioned inserts, whereas household and industrial goods lean on structural integrity over graphics, creating a price tier that continues to absorb coated unbleached kraft.

Across segments, brand owners face tightening sustainability targets, such as Charoen Pokphand Group’s requirement for Scope 3 carbon disclosure by 2027, which shifts volume toward FSC- and PEFC-certified paperboard. The Thailand folding carton market size for serialization-ready medical carton is poised to expand steadily as the Food and Drug Administration pilot scales nationwide. Carton for instant noodles now feature crash-lock bottoms that reduce packing line labor by 20%, demonstrating how converter innovation directly supports end-user cost goals. Digital-print economics allow batch-of-one runs so e-commerce sellers can personalize messages inside the lid, strengthening loyalty and adding perceived value. Each of these dynamics points to sustained growth for the Thailand folding carton market through 2031.

Geography Analysis

Greater Bangkok, Chonburi, Rayong, and Ayutthaya together accounted for well over half of Thailand's folding carton market in 2025, thanks to dense clusters of food processors, automotive plants, and deep-sea ports that demand just-in-time packaging deliveries. Proximity cuts lead times to under 24 hours for many high-volume customers, an advantage regional converters leverage against imports. The Eastern Economic Corridor hosts more than 60% of export-oriented manufacturing and benefits from five-year corporate tax exemptions on automation investments that help converters upgrade to Industry 4.0 line control.

Secondary cities are now the fastest growers. Chiang Mai, Khon Kaen, and Hat Yai collectively accounted for close to 15% of the Thailand folding carton market share in 2025, and their combined demand is advancing at a mid-single-digit CAGR as household incomes climb. Converters responding to this shift have opened satellite warehouses, reducing delivery times from 7 days to 48 hours and aligning with the small-lot orders favored by independent retailers. Modern trade chains expanding into these provinces require retail-ready packs with perforated fronts, nudging additional volume into graphics-capable substrates. Urban middle-class shoppers in these cities consistently choose branded, portion-controlled snacks, reinforcing the nationwide pull for premium paperboard.

Thailand’s role as an export gateway further boosts demand. Food exporters must meet United States, European Union, and Japanese migration rules, prompting converters to certify plants under ISO 22000 and BRC Packaging. Thai Containers Group leverages 16 domestic plants plus 13 in Vietnam and Indonesia to harmonize carton specs across. This regional footprint supports multinational clients that split production across borders but expect identical shelf presence. E-commerce cross-border flows through the Greater Mekong Subregion are rising, and carton compliant with multiple languages ride these routes daily, cementing Thailand as a print and converting hub for neighboring economies. These geographic advantages indicate a healthy runway for the Thailand folding carton market through the forecast horizon.

Competitive Landscape

The Thailand folding carton market remains moderately concentrated. SCG Packaging commands the largest domestic network through a 70% stake in Thai Containers Group, plus a THB 10,000 million (USD 286 million) 2026 capital plan that funds artificial intelligence, robotics, and alternative fuel projects. Rengo, Toppan, Huhtamaki, Amcor, and Oji each operate Thai subsidiaries, yet none exceeds 20% of revenue, leaving ample room for regional specialists to win on customization speed. Scale players are vertically integrating fiber procurement and digital workflows, while mid-tier firms pivot toward niche cosmetics and pharmaceutical orders that demand rapid artwork changes.

Strategic moves emphasize sustainability and automation. Huhtamaki Thailand opened a second Samut Sakhon plant in April 2026 to produce Blueloop mono-material structures aimed at brands shifting away from multi-layer films. SCG Packaging saved THB 260 million (USD 7.4 million) in 2025 from AI-enabled process optimization and targets THB 450 million (USD 12.9 million) in 2026, demonstrating how data analytics lowers waste and energy use. Oji Packaging installed an Aopack BM3000-HD corrugated box maker in August 2025, trimming die-cut changeovers and expanding e-commerce capacity. Converters lacking similar investments face margin erosion as buyers tighten total-cost benchmarks.

Certification breadth is now a decisive factor. Thai Containers Group lists ISO 9001, ISO 14001, ISO 45001, FSC chain-of-custody, BRC Global Packaging, and SMETA audits, meeting the procurement checklists of multinational fast-moving consumer goods firms. Pharmaceutical serialization offers white-space upside, and converters adding inline vision systems capable of validating GS1 codes at 15,000 sheets per hour can command premium pricing. Digital-first disruptors market 48-hour delivery via online configurators, squeezing lead times industry-wide. Combined, these dynamics create a barbell market in which large players pursue integrated scale while agile boutiques capture high-margin micro-runs, underlining a competitive yet opportunity-rich Thailand folding carton market.

Thailand Folding Carton Industry Leaders

SCG Packaging Public Company Limited

Rengo Packaging (Thailand) Co., Ltd.

Toppan Packaging (Thailand) Co., Ltd.

Huhtamaki (Thailand) Ltd.

Oji Packaging (Thailand) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Huhtamaki Thailand inaugurated a second flexible-packaging plant in Samut Sakhon, adding Blueloop mono-material lines for food brands shifting to recyclable structures.

- February 2026: The Ministry of Public Health released draft PFAS limits of 25 ppb per compound and 250 ppb cumulative, with consultation closing Mar 31 2026.

- December 2025: Mandatory compliance dates were set for Thai Industrial Standards TIS 2948-2562 and TIS 3438-2565, effective Jun 22 2026.

- October 2025: SCG Packaging acquired a 60% stake in PT Prokemas Indonesia, expanding to 29 ASEAN plants.

Thailand Folding Carton Market Report Scope

The Thailand folding carton market refers to the production and commercialization of paperboard-based packaging solutions that are folded into carton for the packaging, protection, and display of a wide range of products across industries such as food and beverage, healthcare, personal care, and retail.

The Thailand Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, Other Material Types), Printing Technology (Lithographic, Flexographic, Digital, Gravure, Other Printing Technologies), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-Commerce and Retail-Ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-Commerce and Retail-Ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the Thailand folding carton market?

The Thailand folding carton market size stood at USD 0.74 billion in 2025 and is projected at USD 0.79 billion in 2026.

Which material segment is growing fastest within Thailand's folding carton demand?

Solid bleached sulfate is forecast to expand at an 8.90% CAGR between 2026 and 2031 as cosmetics and pharmaceutical brands favor virgin-fiber substrates.

How will e-commerce influence folding carton design requirements?

Growing direct-to-consumer shipments push converters to add tear strips, crash-lock bottoms, and serialized QR codes that protect goods in transit while enabling shelf-ready presentation.

What are the main regulatory changes affecting carton substrates?

Draft limits on PFAS chemicals and mandatory Thai Industrial Standards for food-contact migration will tighten acceptable chemistries and likely increase demand for certified virgin fiber.

Which printing technology will gain share through 2031?

Digital printing is set to grow at a 9.14% CAGR because tax incentives reduce capital costs and variable-data capability suits limited-edition, regional, and personalized SKUs.

How are converters mitigating pulp price volatility?

Integrated players like SCG Packaging expand recovered-paper collection and lift alternative-fuel usage, lowering reliance on imported virgin pulp and stabilizing input costs.

Page last updated on: