Pharmaceutical Manufacturing Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

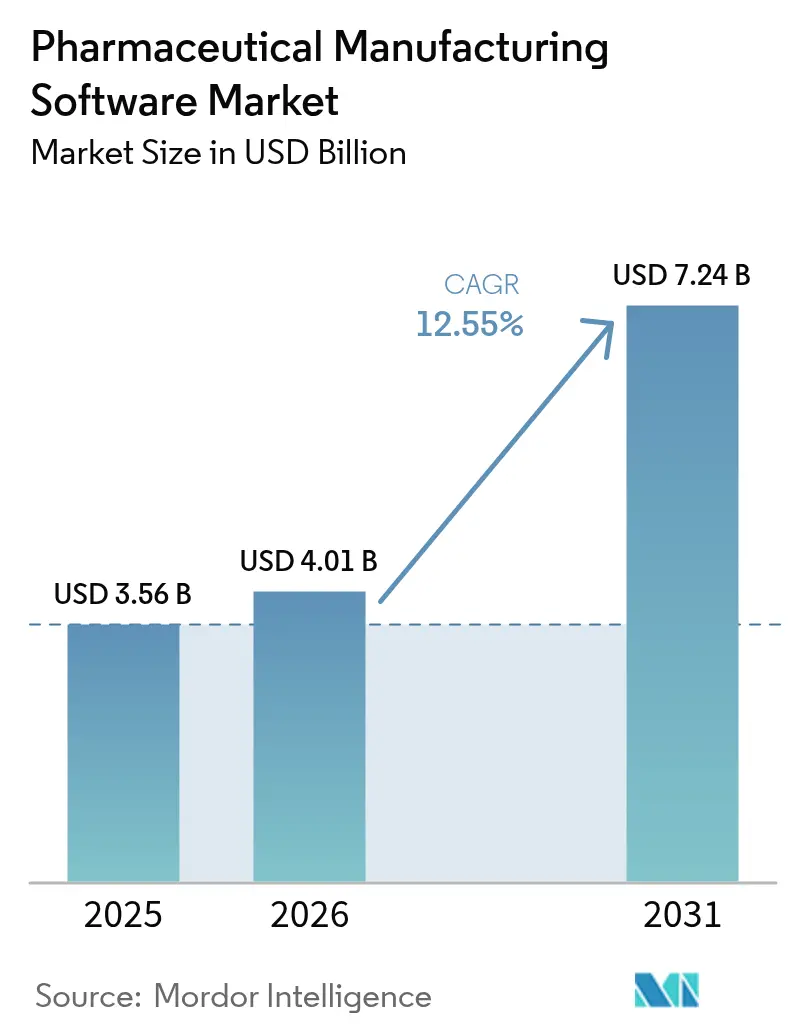

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 7.24 Billion |

| Growth Rate (2026 - 2031) | 12.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Manufacturing Software Market Analysis by Mordor Intelligence

Pharmaceutical Manufacturing Software market size in 2026 is estimated at USD 4.01 billion, growing from 2025 value of USD 3.56 billion with 2031 projections showing USD 7.24 billion, growing at 12.55% CAGR over 2026-2031.

Rising regulatory expectations, cost pressures, and the convergence of artificial intelligence with manufacturing execution systems underpin sustained demand for purpose-built digital platforms. Industry participants move away from fragmented legacy solutions toward unified suites that provide real-time visibility, automated deviation management, and predictive quality controls. Cloud deployment grows quickly as manufacturers balance data-sovereignty needs with the scalability required for multi-site operations. Segment momentum is strongest among small and medium-sized enterprises (SMEs) that now access enterprise-grade capabilities through subscription models, while contract development and manufacturing organizations (CDMOs) accelerate software adoption to support specialized, transferable processes. North America maintains volume leadership thanks to early FDA-driven digitization, yet Asia-Pacific records the fastest growth as regional capacity expansions coincide with national digital-factory programs.

Key Report Takeaways

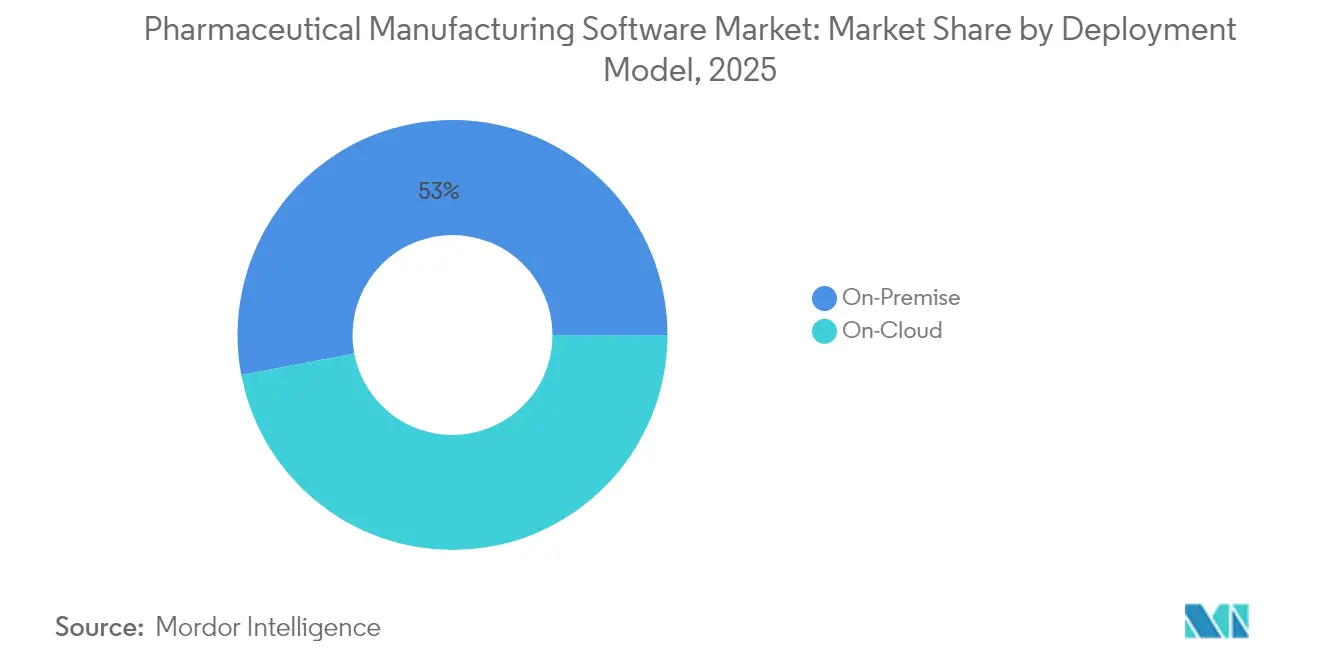

- By deployment model, on-premise solutions led with 52.98% of pharmaceutical manufacturing software market share in 2025, whereas cloud deployments are projected to expand at a 13.28% CAGR through 2031.

- By enterprise size, large enterprises held 60.90% of the pharmaceutical manufacturing software market share in 2025, while SMEs are expected to post the highest 14.29% CAGR to 2031.

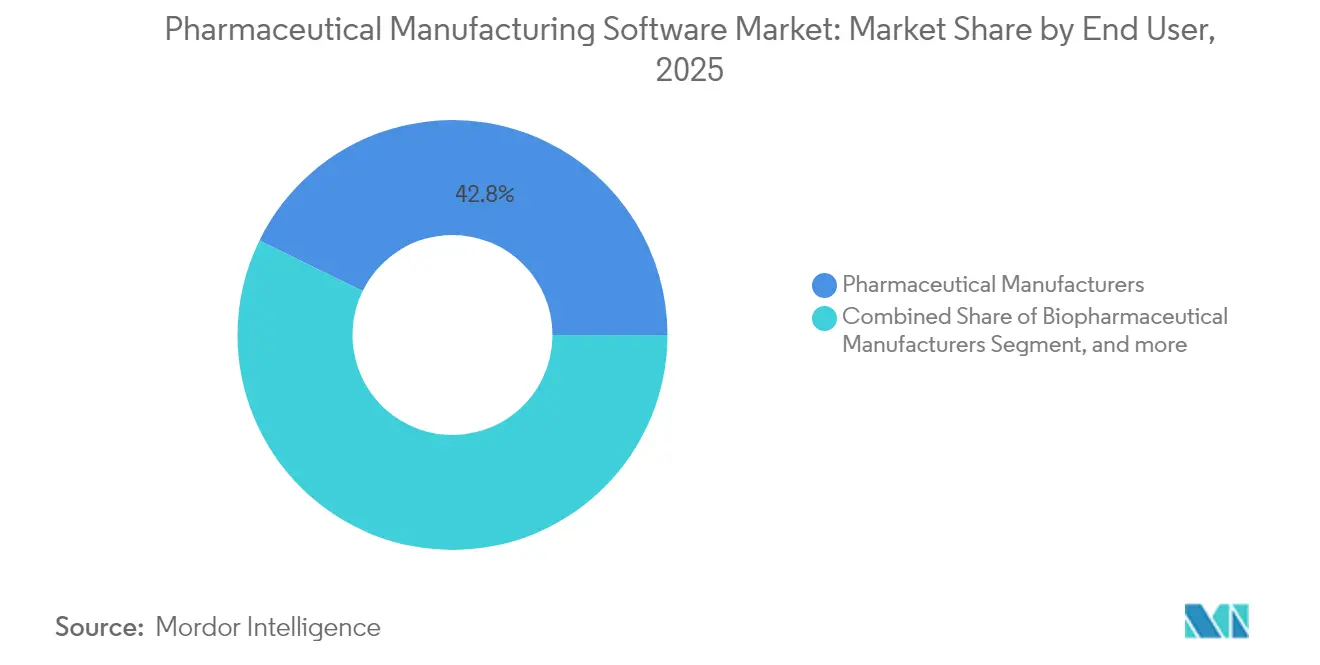

- By end user, pharmaceutical manufacturers held 42.75% of the pharmaceutical manufacturing software market share in 2025 while CDMOs represent the fastest-growing segment with 14.88% at the same CAGR through 2031.

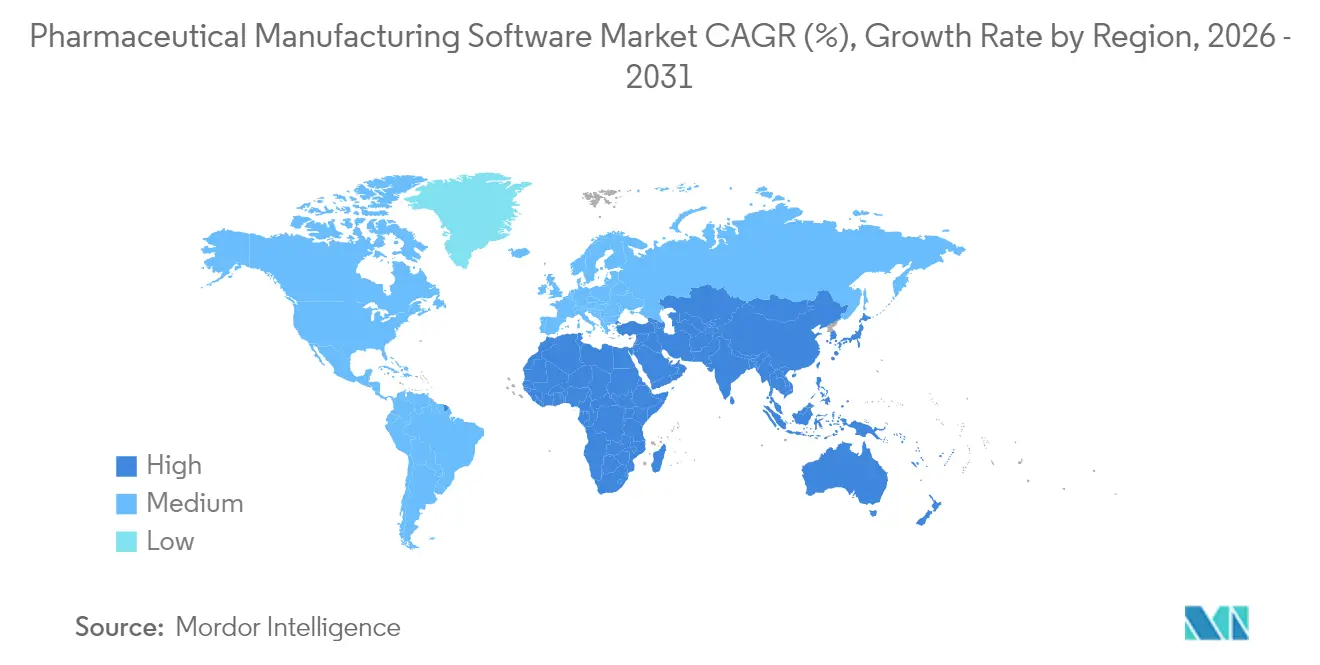

- By geography, North America commanded 40.35% revenue share of the pharmaceutical manufacturing software market in 2025; Asia-Pacific leads future expansion with a 15.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Manufacturing Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Automation | +2.8% | Global, with early gains in North America & Europe | Medium term (2-4 years) |

| Rising Drug Production Costs | +2.1% | Global, particularly acute in developed markets | Long term (≥ 4 years) |

| Regulatory Compliance Requirements | +3.2% | Global, led by FDA & EMA jurisdictions | Short term (≤ 2 years) |

| Advancements in Cloud-Based Solutions | +1.9% | North America & APAC core, spill-over to Europe | Medium term (2-4 years) |

| Growing Demand for Data-Driven Decision Making | +1.7% | Global, with concentration in innovation hubs | Medium term (2-4 years) |

| Expansion of Pharmaceutical Supply Chains | +1.4% | APAC core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Automation

Manufacturers invest in robotics and integrated manufacturing execution systems (MES) to offset labor shortages and drive consistent quality. Predictive maintenance tools connected to MES cut unplanned downtime by up to 25% in validated facilities. Continuous manufacturing, which replaces static batch runs with dynamic flows, demands software that recalculates recipes in real time and reconciles streaming sensor data with electronic batch records. Japanese firms have piloted fully automated cell therapy suites that link robotics with MES to trim cycle times while preserving compliance. Automation also supports data-rich digital twins for process optimization, enabling faster scale-up when therapies advance from clinic to commercial production.

Rising Drug Production Costs

High-value biologics, complex formulations, and volatile raw-material prices heighten cost pressures. Advanced analytics platforms simulate multiple production scenarios, helping identify optimal run rates and ingredient yields. Plants using such models have reported 15-20% reductions in material waste after six months in operation.[1]NVIDIA Corporation, “Gefion Supercomputer Accelerates Pharmaceutical AI,” nvidia.com Energy-management modules integrated into MES monitor utilities in real time, cutting consumption without compromising Good Manufacturing Practice (GMP) standards. These savings offset rising specialty-ingredient costs and help facilities meet corporate sustainability pledges.

Regulatory Compliance Requirements

The FDA’s guidance on data integrity requires auditable electronic records and secure electronic signatures, prompting widespread adoption of validated software that embeds 21 CFR Part 11 controls.[2]U.S. Food & Drug Administration, “Data Integrity and Compliance With Drug CGMP,” fda.gov Europe’s EMA emphasizes quality-by-design principles, driving demand for platforms that can demonstrate process understanding throughout a product’s lifecycle.[3]European Medicines Agency, “GMP Annex 1 Revision,” ema.europa.eu Serialization mandates across more than 50 jurisdictions necessitate track-and-trace modules integrated into MES so that serial numbers traverse packaging, warehousing, and distribution seamlessly. Artificial intelligence layers now flag deviations in near real time, reducing batch-release delays and minimizing the risk of warning letters.

Advancements in Cloud-Based Solutions

Pharmaceutical-specific virtual private clouds certified to GMP standards have eased earlier security concerns. Hybrid architectures place regulated master data on-premise while using cloud analytics for multivariate process analysis. Vendors such as Körber migrated their PAS-X MES to Microsoft Azure to provide elasticity during scale-up, shortening deployment from months to weeks for greenfield facilities. SMEs favor subscription pricing that converts capital outlays into predictable operating expenses and grants them access to frequent functional upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Costs | -1.8% | Global, particularly acute for SMEs | Short term (≤ 2 years) |

| Complex Integration with Legacy Systems | -2.1% | Global, concentrated in established markets | Medium term (2-4 years) |

| Data Security and Privacy Concerns | -1.4% | Global, with heightened focus in EU & North America | Medium term (2-4 years) |

| Lack of Standardization | -1.2% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs

Validation expenses can exceed initial licensing fees by as much as 300% because every code change demands documentation that satisfies GMP auditors. Smaller firms frequently outsource implementation and validation to specialist integrators, increasing total project budgets. Although long-term returns often exceed 25% through productivity gains and fewer compliance findings, near-term cash-flow constraints still deter some first-time buyers. Government tax incentives for digital-factory investments have begun to ease the barrier in select markets.

Complex Integration with Legacy Systems

Many plants still run bespoke supervisory control and data acquisition (SCADA) tools built decades ago without standardized application programming interfaces. Harmonizing these systems with modern MES requires custom middleware and meticulous data-migration tasks to avoid losing historical batch records. Maintaining validation status during staged rollouts adds additional testing cycles and documentation. Companies often opt for modular implementations, but interim data silos can persist until complete migration is finalised, temporarily reducing real-time visibility across multi-site networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Gains Momentum Despite On-Premise Dominance

On-premise platforms retained 52.98% share of the pharmaceutical manufacturing software market in 2025 because large manufacturers prefer direct control of validated infrastructure. However, cloud solutions are forecast to grow at a 13.28% CAGR, reflecting enhanced cybersecurity certifications and regulator acceptance of virtual private cloud environments. Hybrid models dominate new projects, allowing master batch records to remain on-premise while analytics run in the cloud for burst compute requirements.

Cloud adoption also benefits SMEs that lack dedicated data-center resources. Subscription pricing reduces capital expenditure, and built-in validation templates shorten qualification timelines. Global enterprises adopt multi-tenant architectures to harmonize processes across product lines, driving demand for open application programming interface frameworks that integrate MES with enterprise resource planning (ERP) and laboratory information management systems. Vendors now embed machine-learning operations pipelines to refine predictive-quality models continuously, strengthening the value proposition of cloud MES.

By Enterprise Size: SMEs Drive Growth Despite Large-Enterprise Dominance

Large corporations commanded 60.90% of pharmaceutical manufacturing software market share in 2025, leveraging global IT teams to deploy uniform suites across dozens of sites. These companies prioritize end-to-end digital threads that link early-stage development to commercial production. Yet SMEs are expected to advance at a 14.29% CAGR as cloud provisioning and modular architectures lower entry barriers.

For SMEs, preconfigured GMP workflows minimize validation overhead, while role-based dashboards simplify user adoption. Implementation cycles can conclude in less than nine months, compared with multiyear rollouts in large multinational settings. Investors recognize the opportunity; QbDVision secured USD 13 million in 2025 to accelerate deployment of its Digital CMC platform for mid-market biopharma manufacturers finsmes.com. As SMEs scale production of niche therapies, they often require flexible batch sizes, which cloud MES supports through elastic compute and standard connectors to single-use equipment.

By End User: CDMOs Lead Growth as Outsourcing Accelerates

Traditional pharmaceutical companies retained 42.75% revenue share in 2025, but CDMOs are projected to expand at a 14.88% CAGR, making them the fastest-growing end-user group within the pharmaceutical manufacturing software market. Outsourcing rises as innovators focus on discovery while entrusting production to partners specializing in continuous processing, aseptic fill-finish, or advanced biologics.

CDMOs compete on technology differentiation, investing in AI-enhanced MES to offer sponsors predictive process-capability dashboards and accelerated tech-transfer routines. These systems streamline onboarding of multiple client products while safeguarding confidential process parameters inside secure data vaults. Biologics-focused CDMOs deploy cell-culture optimization modules that analyze viability, titer, and metabolite profiles in real time. Combined with electronic batch recording, such capabilities shorten batch-release cycles and reduce cost-of-goods, reinforcing CDMOs’ strategic importance to late-stage pipeline acceleration.

Geography Analysis

North America held 40.35% of pharmaceutical manufacturing software market revenue in 2025. Strict FDA enforcement of data-integrity guidance drives universal adoption of electronic batch records and audit-ready deviation management modules. Oracle’s recent expansion of AI-enabled health applications in Canada exemplifies regional appetite for cloud infrastructures, with the firm forecasting a 70% rise in related sales for 2025. United States facilities leverage enterprise-wide MES rollouts to synchronise production across biologics and small-molecule plants, improving capacity utilisation and reducing lot-release times.

Asia-Pacific is the fastest-growing region, registering a 15.18% CAGR through 2031. China and India upgrade plants to meet global GMP standards, with local regulators aligning data-integrity frameworks to facilitate export licensing. Japanese manufacturers lead regional automation pilots; Chugai Pharmaceutical reports cycle-time reductions after implementing an integrated digital-factory program, while Astellas formed a joint venture with Yaskawa Electric to create a robotics-based cell-therapy manufacturing platform. Government subsidies targeting Industry 4.0 adoption and foreign direct investment in greenfield biologics facilities further propel regional software demand.

Europe maintains steady momentum as EMA guidance promotes quality-by-design and sustainability. German clusters attract fresh capital from multinational firms seeking advanced production ecosystems, and the regional market favours platforms that track carbon emissions in real time. Brexit-driven supply-chain complexities boost adoption of visibility solutions to manage cross-channel batch documentation. Cloud-native deployments gain traction as data-sovereignty concerns ease within the confines of European-based data centres.

The Middle East & Africa and South America remain nascent but exhibit rising adoption as domestic producers seek international quality certifications. Incentives in Saudi Arabia’s National Industrial Strategy and Brazil’s digital-health roadmap encourage investment in validated MES, yet capital constraints and limited skilled labour temper short-term uptake. Vendors offering modular, subscription-based solutions are well positioned to capture early adopters in these emerging markets.

Competitive Landscape

The pharmaceutical manufacturing software market displays moderate consolidation as enterprise software giants acquire specialist capabilities and niche vendors innovate around cloud-native architectures. Siemens completed its USD 5.1 billion acquisition of Dotmatics in April 2025, integrating AI-driven discovery informatics with manufacturing execution to offer a seamless data continuum from molecule design to finished product. Oracle and SAP embed generative AI aides within their GMP workflow modules, guiding operators through complex exception handling while preserving electronic signatures.

Traditional MES stalwarts such as Körber and Honeywell modernize product lines with low-code configuration layers and containerized deployment options. Körber’s PAS-X in the cloud provides on-demand scalability for multi-site CDMO networks, whereas Honeywell integrates digital-twin engines for process-capability predictions. Technology competition increasingly centres on analytics sophistication, cybersecurity certifications, and the depth of out-of-the-box regulatory content.

Specialist challengers focus on speed and flexibility. QbDVision positions its Digital CMC platform as a plug-and-play solution for SMEs requiring right-sized validation templates, while Aizon targets electronic batch record (eBR) conversion with AI-enabled paper-to-digital utilities. Vendors also differentiate through application-programming-interface ecosystems that simplify connections with laboratory, quality, and supply-chain systems. Sustainability analytics and Internet of Things integrations emerge as white-space opportunities, prompting strategic partnerships between MES providers and sensor manufacturers to deliver energy-intensity dashboards and environmental-impact traceability.

Pharmaceutical Manufacturing Software Industry Leaders

BatchMaster Software

Vormittag Associates, Inc.

Oracle

Sage Group plc

MasterControl

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NVIDIA partnered with Novo Nordisk and DCAI to advance drug discovery through artificial intelligence, utilizing the Gefion supercomputer for customized AI models in early research and clinical development, demonstrating the convergence of high-performance computing with pharmaceutical manufacturing intelligence platforms.

- May 2025: QbDVision raised USD 13 million in Series A financing, bringing total funding to USD 28 million for its cloud-based Digital CMC platform aimed at biopharma organizations transitioning from research and development to commercial manufacturing.

- May 2025: Persist AI secured USD 12 million in Series A funding to expand their robotic laboratory and enhance AI models for pharmaceutical formulation development, focusing on Chemistry, Manufacturing, and Controls applications for drug development.

- April 2025: Siemens completed its USD 5.1 billion acquisition of Dotmatics, extending its AI-powered software portfolio into life sciences and creating comprehensive digital threads from research to manufacturing for pharmaceutical companies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pharmaceutical manufacturing software market as purpose-built digital platforms that drive shop-floor execution, batch genealogy, quality documentation, inventory control, and integrated MRP/ERP workflows inside licensed drug-production plants, delivered either on-premise or through secure cloud services.

Scope exclusion: Discovery informatics suites, standalone LIMS, and generic office productivity tools remain outside this coverage.

Segmentation Overview

- By Deployment Model

- On-Cloud

- On-Premise

- By Enterprise Size

- Large Enterprises

- Small & Medium-Sized Enterprises (SMEs)

- By End User

- Pharmaceutical Manufacturers

- Biopharmaceutical Manufacturers

- Contract Development & Manufacturing Organisations (CDMOs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with plant engineering heads, IT directors, and quality managers across North America, Europe, India, and China, and short web surveys captured adoption timelines at midsize firms. These dialogues refined license penetration ratios, module mix, and upgrade budgets, letting us challenge desk assumptions before final modeling.

Desk Research

We began by mapping open datasets from regulators such as the US FDA, EMA EudraGMDP, and Japan's PMDA, which list active plants and inspection cadence, and then blended them with ISPE, EFPIA, and PhRMA publications quantifying line counts and automation adoption. Annual reports, investor decks, and import-export logs drawn from Volza anchored baseline installation figures, while paid access to D&B Hoovers and Dow Jones Factiva helped us trace vendor bookings and service revenues. These sources illustrate the range; many other reputable outlets were referenced during fact-gathering and validation.

Market-Sizing & Forecasting

We reconstructed 2024 spending through a top-down lens that multiplies software average selling prices by the eligible installed base derived from regulator plant registries, and then cross-checked it with a selective bottom-up roll-up of reported vendor bookings. Core variables shaping the model include cGMP-certified line counts, average users per line, cloud migration pace, upgrade cycles, and regulatory fee inflation. A multivariate regression using those drivers feeds the 2025-2030 forecast, while scenario analysis adjusts for sudden policy shifts such as Annex 11 revisions. Gaps in bottom-up counts are bridged through tiered penetration assumptions that were endorsed by primary experts.

Data Validation & Update Cycle

Outputs pass variance checks against independent MES and ERP trackers; anomalies trigger re-interviews before senior review. Reports refresh annually, and we issue interim pulses whenever material events, regulatory or M&A, shift the baseline, ensuring clients receive a current view.

Why Mordor's Pharmaceutical Manufacturing Software Baseline Earns Trust

Published figures often diverge because firms group dissimilar modules, apply static ASPs, or extrapolate from broader MES curves without testing pharma-specific assumptions.

By contrast, Mordor Intelligence ties scope tightly to cGMP plants, validates prices in the field, and refreshes models every year, giving decision-makers a balanced, reproducible baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.56 Bn (2025) | Mordor Intelligence | - |

| USD 3.38 Bn (2025) | Global Consultancy A | Omits cloud support fees; counts MES seats only |

| USD 3.30 Bn (2024) | Industry Association B | Blends pharma with medical-device licenses; uses static ASPs |

| USD 2.90 Bn (2023) | Trade Journal C | Narrow geography; excludes on-premise renewals |

These comparisons show that once scope, pricing, and refresh cadence are normalized, Mordor's estimate remains the most dependable guide for investment and planning.

Key Questions Answered in the Report

What is the current size of the pharmaceutical manufacturing software market?

The market is valued at USD 4.01 billion in 2026 and is forecast to reach USD 7.24 billion by 2031.

Which deployment model is growing fastest?

Cloud-based solutions are expanding at a 13.28% CAGR, outpacing on-premise installations as security certifications mature.

Why are CDMOs adopting software faster than drug innovators?

CDMOs invest in advanced MES to differentiate services, streamline tech transfer, and support multi-client operations, resulting in a 14.88% CAGR.

How do regulations influence software adoption?

FDA and EMA data-integrity guidelines mandate auditable electronic records, driving accelerated rollout of validated digital platforms across all regions.

What challenges limit software uptake among SMEs?

High validation costs and integration with legacy systems remain primary barriers, though modular cloud offerings are lowering entry hurdles.

Which region will contribute most to future market growth?

Asia-Pacific leads in growth at a projected 15.18% CAGR, supported by capacity expansion in China, India, and Japan and government incentives for digital factories.

Page last updated on: