Modular Pharmaceutical Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

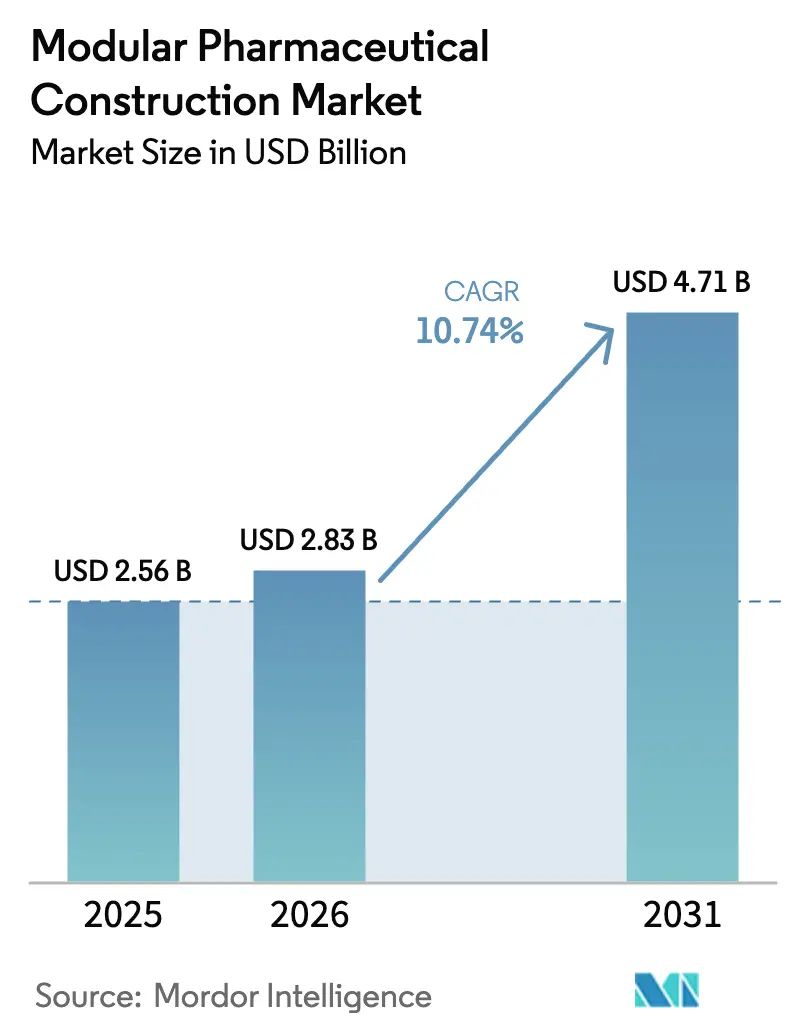

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 4.71 Billion |

| Growth Rate (2026 - 2031) | 10.74% CAGR |

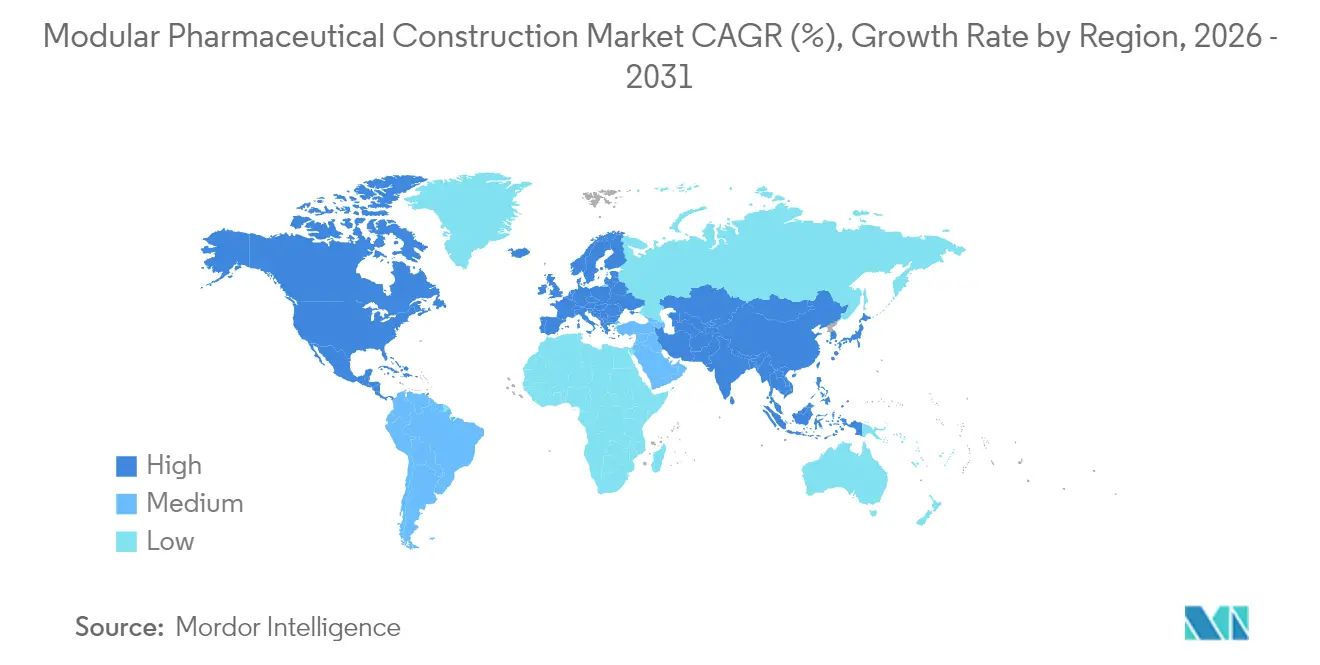

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modular Pharmaceutical Construction Market Analysis by Mordor Intelligence

Modular pharmaceutical construction market size in 2026 is estimated at USD 2.83 billion, growing from 2025 value of USD 2.56 billion with 2031 projections showing USD 4.71 billion, growing at 10.74% CAGR over 2026-2031. Accelerated biologics pipelines, rising capital-efficiency pressures, and regulator support for quality-by-design production models continue to underpin demand for factory-built cleanrooms that can be validated in parallel with on-site construction. Faster deployment is proving decisive for vaccine makers that cannot risk supply interruptions, while cost-sensitive biotech startups increasingly view turnkey pods as the most practical route into commercial manufacturing. Suppliers are countering supply-chain constraints by deepening relationships with HVAC and filter vendors and by pre-ordering long-lead components. Finally, the sector benefits from sustainability mandates as modular methods cut embodied carbon by about 36% relative to conventional builds.

Key Report Takeaways

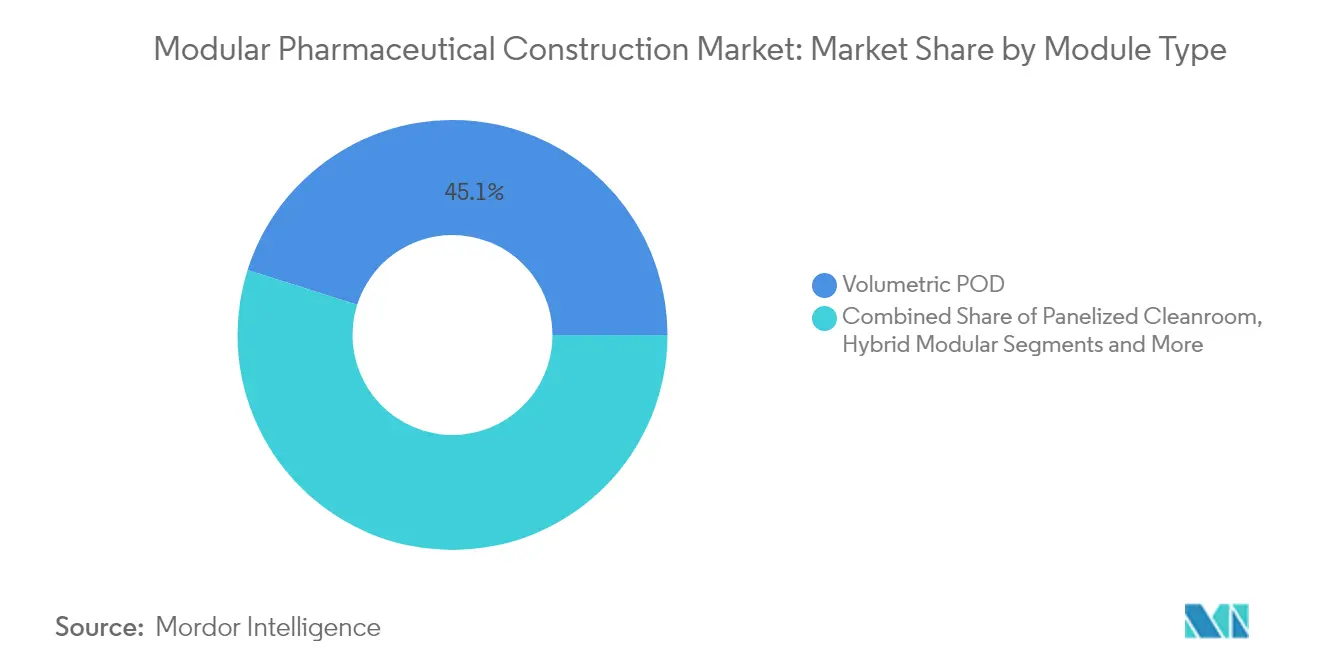

- By module type, volumetric POD systems held 45.12% revenue share in 2025, whereas containerized mobile modules are poised to expand at a 13.75% CAGR through 2031.

- By facility function, fill-finish and aseptic processing led the modular pharmaceutical construction market with 37.65% of the market share in 2025, while personalized R&D pods are forecasted to post a 13.05% CAGR through 2031.

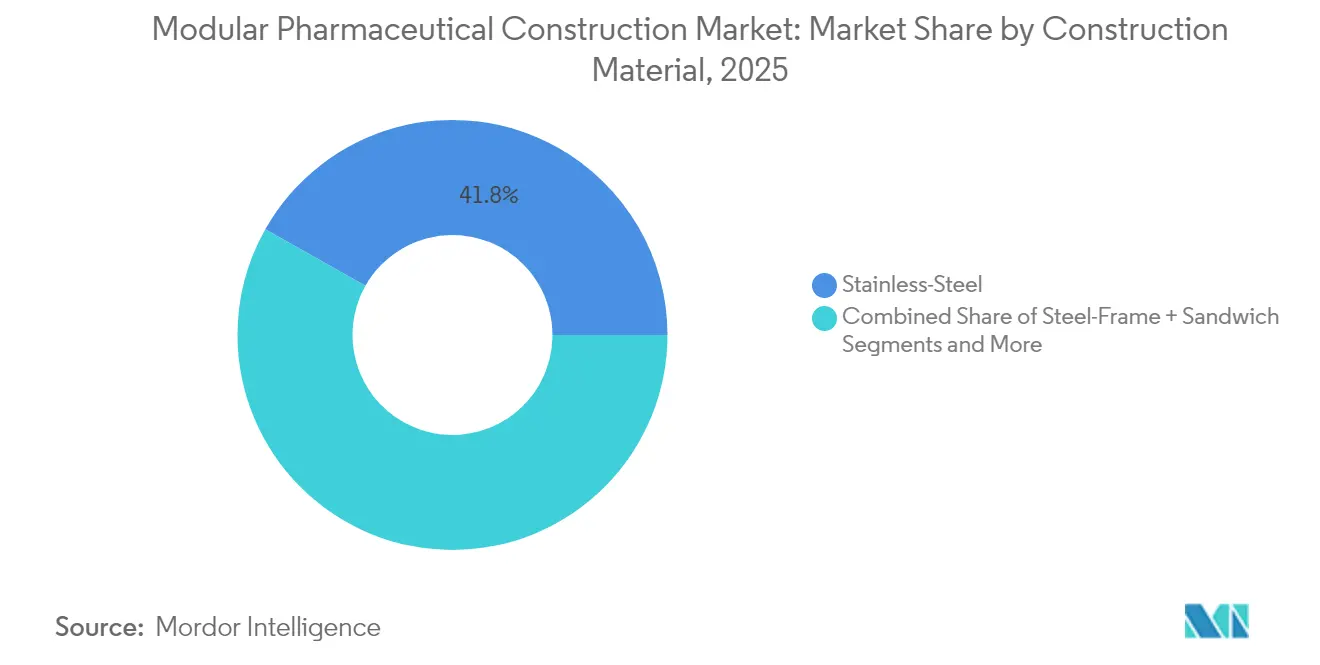

- By construction material, stainless steel accounted for 41.82% of the modular pharmaceutical construction market size in 2025; aluminium-composite panels are projected to grow at a 11.64% CAGR between 2026 and 2031.

- By client type, pharmaceutical innovator firms commanded 46.05% market share in 2025, whereas biotech startups are set to record a 14.58% CAGR, the highest among all customer groups.

- Geographically, North America accounted for 33.62% of 2025 revenue, while the Asia-Pacific region is advancing at the fastest 10.08% CAGR, driven by aggressive biomanufacturing investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Modular Pharmaceutical Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Faster time-to-market for biologics & vaccines | +2.80% | Global; early North America, EU | Medium term (2-4 years) |

| CAPEX & OPEX savings vs stick-built plants | +2.10% | Global | Short term (≤ 2 years) |

| Regulators endorsing modular quality by design | +1.90% | North America, EU; spill-over to APAC | Long term (≥ 4 years) |

| Personalized-medicine micro-facilities | +1.60% | North America core; expanding EU & APAC | Long term (≥ 4 years) |

| Brownfield pod retrofits of ageing sites | +1.40% | North America & EU | Medium term (2-4 years) |

| ESG-led embodied-carbon reductions | +1.20% | Global; strongest in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Faster Time-to-Market for Biologics & Vaccines

Parallel module fabrication and on-site groundwork trim facility delivery cycles from 4-6 years to roughly 18-24 months. Sanofi’s EUR 558 million Singapore plant reached mechanical completion within two years by installing pre-validated cleanroom blocks while foundations were still being poured. Exyte replicated this speed with ExyCell pods for WACKER’s mRNA hub in Germany, underscoring how rapid capacity additions enhance pandemic readiness. Regulatory clarity from the FDA’s Q13 guidance further reduces adoption risk by outlining data requirements for multi-unit continuous systems[1]FDA Staff, “Q13 Continuous Manufacturing of Drug Substances and Drug Products,” U.S. Food & Drug Administration, fda.gov. Shorter build times also protect product launch windows for high-value monoclonal antibodies, prompting developers to lock in pod orders earlier in their clinical programs. With competitive pressures mounting in immunology and oncology, a compressed facility schedule is now a board-level metric for most large sponsors.

CAPEX & OPEX Savings vs Stick-Built Plants

Factory-built modules deliver controlled environments that virtually eliminate weather delays and boost labor productivity, yielding reported cost reductions of 20-50%. Fluor’s cell-therapy building for Bayer in California attained LEED v4 Platinum while cutting annual energy costs by 52.6% through integrated modular design. Operational expenditure also falls when pods can be de-risked off-site, allowing equipment vendors to complete FAT and SAT in one continuous sequence. Single-use equipment inside modular shells permits multi-product campaigns without major turnover capital. These economics resonate with contract development and manufacturing organizations that juggle dozens of client‐specific processes and must adjust capacity every quarter. The same logic appeals to venture-backed biotech’s that look for deferred-capex pathways to first-in-human supply.

Regulators Endorsing Modular Quality by Design

The FDA’s Advanced Manufacturing Technologies Designation Program offers priority reviews to projects that demonstrate higher quality, lower cost, and improved security criteria that modular systems inherently satisfy. In Europe, revised GMP Annex 1 emphasises controlled environments, supporting pre-engineered cleanrooms with verifiable airflow and particulate data[2]International Society for Pharmaceutical Engineering Editors, “China & India Target Future GMP Manufacturing,” Pharmaceutical Engineering, ispe.org. Standardised building blocks mean each project begins with a dossier of prior-use documentation, easing validation. This alignment between design and compliance lowers documentation burdens for firms unfamiliar with complex facility filings. Momentum grows further as ICH Q13 harmonises expectations for continuous-flow lines that are usually housed inside compact modular bays. Consequently, regulators are moving from passive acceptance to active promotion of factory-built facilities, a shift that is accelerating procurement decisions worldwide.

ESG-Led Embodied-Carbon Reductions

Lifecycle assessments reveal that factory-assembled modules cut material waste and transport emissions, driving a 36% decline in embodied carbon compared with traditional projects[3]MDPI Authors, “Comparison of the Embodied Carbon Emissions and Direct Construction Costs for Modular and Conventional Residential Buildings in South Korea,” MDPI, mdpi.com . Brands now link environmental metrics to executive compensation, elevating low-carbon construction from a procurement preference to a compliance requirement. EU taxonomy rules encourage green financing for projects that demonstrate measurable carbon savings, and modular designs readily quantify reductions through digital bill-of-materials. Several insurers offer premium rebates for buildings using circular-economy materials such as aluminium-composite panels that are 95% recyclable. Collectively, these incentives translate into lower weighted-average cost of capital, further sharpening the modular value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital for bespoke modules | -1.80% | Global | Short term (≤ 2 years) |

| Shortage of off-site pharma-grade fabricators | -1.50% | Global; acute in APAC | Medium term (2-4 years) |

| Digital-twin interoperability gaps | -1.20% | North America & EU | Medium term (2-4 years) |

| HEPA & HVAC component supply risk | -0.90% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital for Bespoke Modules

Specialized finishes, electro-polished piping, and rigorous documentation often raise initial quotes 8% above stick-built shells, challenging approval by finance teams focused on headline expenditure. Yet ownership cost analyses consistently show break-even within five years once faster time-to-revenue is factored in. PCI Pharma Services nevertheless secured USD 365 million to retrofit US and EU campuses, demonstrating investor willingness when the business case includes multiproduct flexibility. Vendor financing and leasing models are emerging to ease capex hurdles for early-stage firms. Governments add momentum through accelerated depreciation on clean-technology infrastructure, amplifying after-tax returns.

Shortage of Off-Site Pharma-Grade Fabricators

Demand has outstripped capacity among the dozen or so global firms certified to weld, panelize, and pre-test ISO-classified suites. Lead times for large pod orders now stretch beyond 12 months, creating scheduling risk for drug launches. APAC faces the steepest bottlenecks as only a handful of steel fabricators hold GMP-aligned quality systems. G-CON’s decision to open a 144,000 sq ft Texas facility will help, yet similar investments are needed in Singapore, India, and Brazil to normalize supply. Some purchasers pre-qualify multiple suppliers and split orders to hedge capacity risk, though doing so complicates validation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: Containerized Units Drive Innovation

Volumetric POD suites retained 45.12% of 2025 revenue because their plug-and-play format satisfies a broad range of batch sizes without major redesign. Nevertheless, containerized mobile modules are on track for a rapid 13.75% CAGR thanks to growing humanitarian and defence use cases that require deployment in weeks rather than months. The modular pharmaceutical construction market size for containerized formats is set to more than double by 2031 as demand for point-of-care production matures. Panelized cleanroom kits and skid-mounted units remain relevant for large molecule purification trains where skid scope boundaries reduce piping complexity. Hybrid layouts that merge volumetric cores with skid corridors are rising as sponsors juggle speed, flexibility, and throughput.

Containerized platforms differ in that utilities are pre-stubbed and validated, enabling re-use across therapeutic campaigns. This portability lowers barriers for nonprofit vaccine institutes that lack permanent GMP infrastructure yet must respond to regional outbreaks. Meanwhile, investors view volumetric PODs as asset-light structures that preserve resale value, an attractive hedge against clinical failure. Recent order backlogs from Africa CDC and ASEAN health ministries suggest the format’s appeal is no longer confined to Western majors. As unit volumes grow, competition among chassis suppliers is expected to narrow total delivered cost, spurring a broader uptake.

By Facility Function: Aseptic Processing Leads Market

Sterile fill-finish suites accounted for 37.65% of 2025 turnover, as injectable biologics dominate late-stage pipelines. The segment benefits from tighter Annex 1 standards, prompting firms to retire ageing glass-lined isolators in favor of modern robotic fillers inside ISO 5 modules. Drug-substance halls follow closely as mRNA and viral vector processes demand higher single-use reactor capacity. The modular pharmaceutical construction market size for personalized R&D pods, although small today, is predicted to climb swiftly at a 13.05% CAGR as precision-oncology trials proliferate.

Analytical-testing zones also pivot towards modular designs that segregate potency assays from microbiological labs, minimizing cross-contamination. Packaging shells using innovative conveyors increasingly attach to upstream pods, streamlining cold-chain handoffs. Collectively, these shifts indicate a convergence toward end-to-end modular campuses that house both clinical and commercial operations, thereby reducing tech-transfer risk while maximizing space utilization.

By Construction Material: Steel Dominance with Composite Growth

Stainless steel remained the material of choice in 2025, occupying 41.82% share due to its inertia and proven cleanability credentials. However, aluminum-composite panels are gaining ground at a forecast 11.64% CAGR, aided by lighter weight, better insulation, and near-total recyclability. Cost-sensitive buyers often select steel frames clad with composite sandwich panels that balance strength and thermal performance. Reinforced concrete appears mostly in earthquake-prone regions where code compliance dictates higher structural margins.

Material choice now intertwines with ESG metrics as sponsors quantify cradle-to-gate emissions. Several European buyers specify low-carbon steel produced using hydrogen direct-reduced iron, whereas Australian projects experiment with cross-laminated timber for non-process areas. As verification frameworks such as EPDs mature, procurement teams will likely demand dual certification covering both GMP suitability and carbon footprint.

By Client Type: Biotech Startups Accelerate Adoption

Originator pharmaceutical firms still led with 46.05% revenue share in 2025, leveraging abundant capital to integrate pods into multi-product hubs. Yet biotech startups are the fastest climbers, registering 14.58% CAGR, because pods eliminate the need for large initial footprints and can later be redeployed if programmes shift. The modular pharmaceutical construction market share commanded by CDMOs is also increasing as they seek to offer slot-in capacity for cell-and-gene therapy clients. Government-backed vaccine institutes in the Middle East and Southeast Asia form another emerging cohort, attracted by the rapid build times that enhance public health readiness.

Startups benefit from lease-to-own financial models that convert capital outlays into predictable operating expenses. In parallel, big pharma utilizes pods to localize production in emerging markets, sidestepping lengthy customs processes associated with finished-dose importation. These dynamics collectively accelerate decentralization, positioning modular approaches as a leveler between corporate giants and young innovators.

Geography Analysis

North America accounted for 33.62% of 2025 revenue, as the United States continued to invest heavily in advanced domestic manufacturing, exemplified by Novo Nordisk’s USD 4.1 billion expansion in North Carolina. Canada supplements regional capacity through policy incentives that reward green construction, while Mexico leverages proximity logistics to attract secondary packaging pods. The modular pharmaceutical construction market size is poised for further growth as the Biomedical Advanced Research and Development Authority (BARDA) allocates new funds to pandemic-preparedness facilities.

Europe exhibits steady adoption driven by environmental directives and harmonized GMP rules. Germany, the United Kingdom, and France dominate installations, yet Spain and Italy are scaling containerized units to meet biologics demand. Exyte’s delivery of WACKER’s mRNA competence center in Halle demonstrates how rapid builds can satisfy both national resilience goals and sustainability targets. EU-wide carbon-pricing mechanisms could further tilt procurement toward low-waste, modular options, consolidating the region’s share even as absolute growth rates lag behind those of APAC.

Asia-Pacific is the fastest-growing territory at 10.08% CAGR. China and India are funneling subsidies into home-grown biologics capability, and both nations aim for ICH Pe-register equivalence by 2030. Japan’s AGC Biologics integrated Cytiva’s FlexFactory skids into a Yokohama site in under 16 months, illustrating regional proficiency in large-scale modularization. South Korea’s new sterile-filtration plant and Australia’s biomanufacturing stimulus add momentum. Emerging ASEAN economies increasingly purchase containerized facilities for vaccine fill-finish, seeking self-sufficiency amid geopolitical supply risks.

Competitive Landscape

Competition is moderate, with the top five vendors accounting for roughly 55% of global revenue. Pharmadule Morimatsu, Exyte, and G-CON lead based on track record, regulatory credibility, and global project execution. Exyte strengthened its edge by acquiring TTP Group and Kinetics Group during 2024-2025, thereby integrating engineering, construction, and facility management under one umbrella. Pharmadule focuses on turnkey GMP villages, whereas G-CON specializes in autonomous standard-dimension PODs that ship by road or sea without oversized permits.

Digital innovation is an emerging differentiator. Samsung Biologics leverages computational fluid dynamics twins to optimize airflow, reduce cleanroom energy consumption, and shorten validation by simulating particle counts before build-out. Lonza’s USD 1.2 billion purchase of Roche’s Vacaville site demonstrates how CDMOs use acquisitions to secure land and utilities and then overlay modular expansions to support multi-client pipelines.

Regional localization also shapes strategy. G-CON’s Texas expansion triples POD output capacity for North American customers, while Germfree partners in Saudi Arabia to create the region’s first modular ATMP campus. Vendors are increasingly offering OPEX-based service models that bundle maintenance, spare parts, and digital analytics to lock in long-term revenue and deepen client loyalty.

Modular Pharmaceutical Construction Industry Leaders

Pharmadule Morimatsu

Exyte

G-CON Manufacturing

IPS

Cytiva

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: PCI Pharma Services completed a USD 365 million upgrade programme across EU and US sites to embed modular suites for high-potency products.

- June 2025: King Faisal Specialist Hospital & Research Centre and Germfree unveiled the first modular ATMP campus in Saudi Arabia, boosting Middle-East cell-therapy capacity.

- May 2025: G-CON Manufacturing opened a 144,000 sq ft facility in Texas dedicated to POD production.

- April 2025: Varda Space Industries raised USD 90 million to scale orbital drug-manufacturing modules.

Global Modular Pharmaceutical Construction Market Report Scope

| Volumetric POD Modules |

| Panelised Cleanroom Modules |

| Skid-Mounted Process Modules |

| Containerised Mobile Modules |

| Hybrid Modular Systems |

| Drug-Substance Manufacturing |

| Fill-Finish & Aseptic Processing |

| Quality-Control Laboratories |

| Packaging & Warehousing |

| R&D / Pilot Plants |

| Stainless-Steel Structures |

| Aluminium-Composite Panels |

| Steel-Frame + Sandwich Panels |

| Reinforced-Concrete Hybrid |

| Others (Timber / FRP) |

| Pharma Innovator Firms |

| CDMOs |

| Generics Manufacturers |

| Biotech Start-ups |

| Government / Non-profit Vaccine Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Module Type | Volumetric POD Modules | |

| Panelised Cleanroom Modules | ||

| Skid-Mounted Process Modules | ||

| Containerised Mobile Modules | ||

| Hybrid Modular Systems | ||

| By Facility Function | Drug-Substance Manufacturing | |

| Fill-Finish & Aseptic Processing | ||

| Quality-Control Laboratories | ||

| Packaging & Warehousing | ||

| R&D / Pilot Plants | ||

| By Construction Material | Stainless-Steel Structures | |

| Aluminium-Composite Panels | ||

| Steel-Frame + Sandwich Panels | ||

| Reinforced-Concrete Hybrid | ||

| Others (Timber / FRP) | ||

| By Client Type | Pharma Innovator Firms | |

| CDMOs | ||

| Generics Manufacturers | ||

| Biotech Start-ups | ||

| Government / Non-profit Vaccine Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected growth rate of the modular pharmaceutical construction market?

The modular pharmaceutical construction market is forecast to grow at a 10.74% CAGR from USD 2.83 billion in 2026 to USD 4.71 billion by 2031.

Which module type commands the highest revenue today?

Volumetric POD systems lead with 45.12% of 2025 revenue, primarily because of their scalability across multiple therapies.

Why are biotech startups adopting modular facilities so quickly?

Pods allow startups to defer large capital outlays, scale production as pipelines mature, and meet GMP standards without building permanent factories.

Which region is expanding fastest?

Asia-Pacific shows the highest regional CAGR at 10.08%, driven by strategic investments in China, India, Japan, and South Korea.

How do modular builds support sustainability goals?

Factory-assembled modules typically cut embodied carbon by about 36% compared with conventional construction, helping firms meet ESG targets and secure green financing.

What is the main supply-chain risk facing modular projects?

Long lead times for pharma-grade HEPA filters and HVAC components pose scheduling challenges, especially in fast-track vaccine facilities.

Page last updated on: